Pakistan

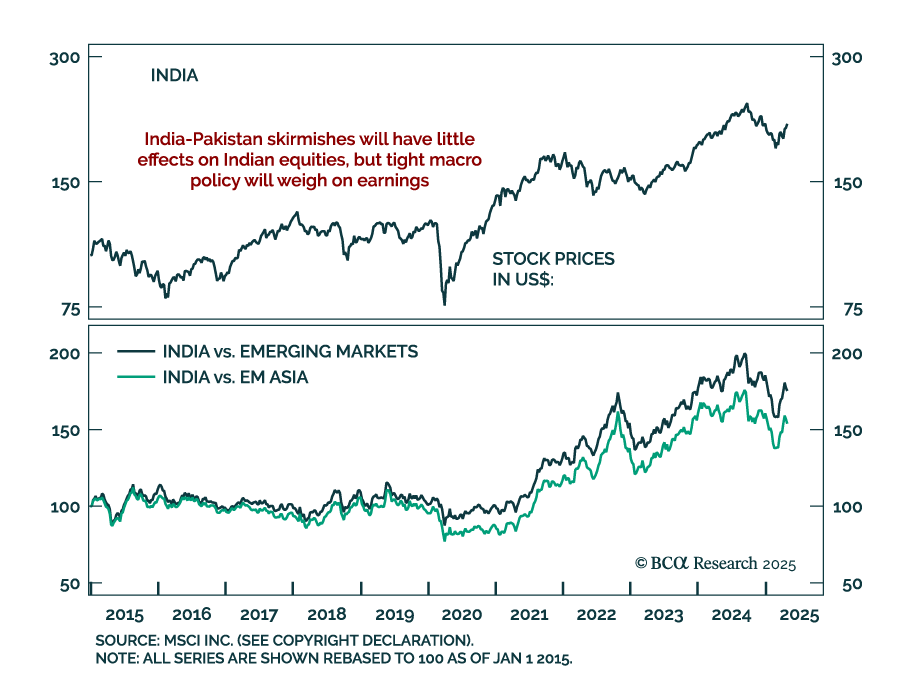

Indian equities remain resilient despite rising India-Pakistan tensions, but BCA’s EM strategists stay underweight India while favoring local-currency bonds. The latest flare-up follows Indian retaliation to last month’s terrorist attack in Kashmir,…

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

Executive Summary EU Embargoes Russian Oil The EU imposed an embargo on 90% of Russian oil imports, which will provoke retaliation. Russia will squeeze Europe’s economy ahead of critical negotiations over the coming 6-12 months. Russian gains on the battlefield in Ukraine point to a ceasefire later, but not yet – and Russia will need to retaliate against NATO enlargement. The Middle East and North Africa face instability and oil disruptions due to US-Iran tensions and Russian interference. China’s autocratic shift is occurring amid an economic slowdown and pandemic. Social unrest and internal tensions will flare. China will export uncertainty and stagflation. Inflation is causing disparate effects in South Asia – instability in Pakistan and Sri Lanka, and fiscal populism in India. Asset Initiation Date Return Long Brazilian Financials / Indian Equities (Closed) Feb 10/22 22.5% Bottom Line: Markets still face three geopolitical hurdles: Russian retaliation; Middle Eastern instability; Chinese uncertainty. Feature Global equities bounced back 6.1% from their trough on May 12 as investors cheered hints of weakening inflation and questioned the bearish consensus. BCA’s Global Investment Strategy correctly called the equity bounce. However, as BCA’s Geopolitical Strategy service, we see several sources of additional bad news. Throughout the Ukraine conflict we have highlighted two fundamental factors to ascertain regarding the ongoing macroeconomic impact: Will the war cut off the Russia-EU energy trade? Will the war broaden beyond Ukraine? Chart 1Russian-Exposed Assets Will Suffer More In this report we update our views on these two critical questions. The takeaway is that the geopolitical outlook is still flashing red. The US dollar will remain strong and currencies exposed to Russia and geopolitical risk will remain weak (Chart 1). In addition, China’s politics will continue to produce uncertainty and negative surprises this year. Taken together, investors should remain defensive for now but be ready to turn positive when the market clears the hurdles we identify. The fate of the business cycle hangs in the balance. Energy Ties Eroding … Russia Will Retaliate Over Oil Embargo Chart 2AEU Embargoes Russian Oil Europe is diversifying from Russian oil and natural gas. The European Union adopted a partial oil embargo on Russia that will cut oil imports by 90% by the end of 2022. It also removed Sberbank from the SWIFT banking communications network and slapped sanctions on companies that insure shipments of Russian crude. The sanctions will cut off all of Europe’s seaborne oil imports from Russia as well as major pipeline imports, except the Southern Druzhba pipeline. The EU made an exception for landlocked eastern European countries heavily dependent on Russian pipeline imports – namely Hungary, Slovakia, the Czech Republic, and Bulgaria (Chart 2A). Focus on the big picture. Germany changed its national policy to reduce Russian energy dependency for the sake of national security. From Chancellors Willy Brandt to Angela Merkel, Germany pursued energy cooperation and economic engagement as a means of lowering the risk of war with Russia. Ostpolitik worked in the Cold War, so when Russia seized Crimea in 2014, Merkel built the Nord Stream 2 pipeline. But Merkel’s policy failed to persuade Russia that economic cooperation is better than military confrontation – rather it emboldened President Putin, who viewed Europe as divided and corruptible. Chart 2BRussia Squeezes EU’s Natural Gas Russia’s regime is insecure and feels threatened by the US and NATO. Russia believed that if it invaded Ukraine, the Europeans would maintain energy relations for the sake of preserving overall strategic stability. Instead Germany and other European states began to view Russia as irrational and aggressive and hence a threat to their long-term security. They imposed a coal ban, now an oil ban the end of this year, and a natural gas ban by the end of 2027, all formalized under the recently announced RePowerEU program. Russia retaliated by declaring it would reduce natural gas exports to the Netherlands and probably Denmark, after having already cut off Finland, Poland, and Bulgaria (Chart 2B). As a pretext Russia points to its arbitrary March demand that states pay for gas in rubles rather than in currencies written in contracts. This ruble payment scheme is being enforced on a country-by-country basis against those Russia deems “unfriendly,” i.e. those that join NATO, adopt new sanctions, provide massive assistance to Ukraine, or are otherwise adverse. Chart 3Russia Actively Cutting Gas Flows Russia and Ukraine are already reducing natural gas exports through the Ukraine and Turkstream pipelines while the Yamal pipeline has been empty since May – and it is only a matter of time before flows begin to fall in the Nord Stream 1 pipeline to Germany (Chart 3). German government and industry are preparing to ration natural gas (to prioritize household needs) and revive 15 coal plants if necessary. Europe is attempting to rebuild stockpiles for the coming winter, when Russian willingness and capability to squeeze natural gas flows will reach a peak. The big picture is demonstrated by game theory in Diagram 1. The optimal situation for both Russia and the EU is to maintain energy exports for as long as possible, so that Russia has revenues to wage its war and Europe avoids a recession while transitioning away from Russian supplies (bottom right quadrant, each side receives four points). The problem is that this solution is not an equilibrium because either side can suffer a sudden shock if the other side betrays the tacit agreement and stops buying or selling (bottom left and top right quadrants). Diagram 1EU-Russia Standoff: What Does Game Theory Say? The equilibrium – the decision sets in which both Russia and the EU are guaranteed to lose the least – is a situation in which both states reduce energy trade immediately. Europe needs to cut off the revenues that fuel the Russian war machine while Russia needs to punish and deter Europe now while it still has massive energy leverage (top left quadrant, circled). Once Europe diversifies away, Russia loses its leverage. If Europe does not diversify immediately, Russia can punish it severely by cutting off energy before it is prepared. Russian energy weaponization is especially useful ahead of any ceasefire talks in Ukraine. Russia aims for Ukrainian military neutrality and a permanently weakened Ukrainian state. To that end it is seizing territory for the Luhansk and Donetsk People’s Republics, seizing the southern coastline and strategic buffer around Crimea, and controlling the mouth of the Dnieper river so that Ukraine is forever hobbled (Map 1). Once it achieves these aims it will want to settle a ceasefire that legitimizes its conquests. But Ukraine will wish to continue the fight. Map 1Russian Invasion Of Ukraine, 2022 Russia will need leverage over Europe to convince the EU to lean on Ukraine to agree to a ceasefire. Something similar occurred in 2014-15 when Russia collaborated with Germany and France to foist the Minsk Protocols onto Ukraine. If Russia keeps energy flowing to EU, the EU not only gets a smooth energy transition away from Russia but also gets to keep assisting Ukraine’s military effort. Whereas if Russia imposes pain on the EU ahead of ceasefire talks, the EU has greater interest in settling a ceasefire. Finally, given Russia’s difficulties on the battlefield, its loss of European patronage, and potential NATO enlargement on its borders, Moscow is highly likely to open a “new front” in its conflict with the West. Josef Stalin, for example, encouraged Kim Il Sung to invade South Korea in 1950. Today Russia’s options lie in the Middle East and North Africa – the regions where Europe turns for energy alternatives. Not only Libya and Algeria – which are both inherently fertile ground for Russia to sow instability – but also Iran and the broader Middle East, where a tenuous geopolitical balance is already eroding due to a lack of strategic understanding between the US and Iran. Russia’s capabilities are limited but it likely retains enough influence to ignite existing powder kegs in these areas. Bottom Line: Investors still face a few hurdles from the Ukraine war. First, the EU’s expanding energy embargo and Russian retaliation. Second, instability in the Middle East and North Africa. Hence energy price pressures will remain elevated in the short term and kill more demand, thus pushing the EU and the rest of the world toward stagflation or even recession. War Contained To Ukraine So Far … But Russia To Retaliate Over NATO Enlargement At present Russia is waging a full-scale assault on eastern and southern Ukraine, where about half of Donetsk awaits a decision (Map 2). If Russia emerges victorious over Donetsk in the summer or fall then it can declare victory and start negotiating a ceasefire. This timeline assumes that its economic circumstances are sufficiently straitened to prevent a campaign to the Moldovan border.1 Map 2Russia May Declare Victory If It Conquers The Rest Of Donetsk There are still ways for the Ukraine war to spill over into neighboring areas. For example, the Black Sea is effectively a Russian lake at the moment, which prevents Ukrainian grain from reaching global markets where food prices are soaring. Eventually the western maritime powers will need to attempt to restore freedom of navigation. However, Russia is imposing a blockade on Ukraine, has more at stake there than other powers, and can take greater risks. The US and its allies will continue to provide Ukraine with targeting information against Russian ships but this assistance could eventually provoke a larger naval conflict. Separately, the US has agreed to provide Ukraine with the M142 High Mobility Artillery Rocket System (HIMARS), which could lead to attacks on Russian territory that would prompt a ferocious Russian reaction. Even assuming that the Ukraine war remains contained, Russia’s strategic conflict with the US and the West will remain unresolved and Moscow will be eager to save face. Russian retaliation will occur not only on account of European energy diversification but also on account of NATO enlargement. Finland and Sweden are attempting to join NATO and as such the West is directly repudiating the Putin regime’s chief strategic demand for 22 years. Finland shares an 830 mile border with Russia, adding insult to injury. The result will be another round of larger military tensions that go beyond Ukraine and prolong this year’s geopolitical risk and uncertainty. Russia’s initial response to Finland’s and Sweden’s joint application to NATO was to dismiss the threat they pose while drawing a new red line. Rather than forbidding NATO enlargement, Russia now demands that no NATO forces be deployed to these two states. This demand, which Putin and other officials expressed, may or may not amount to a genuine Russian policy change. Russia’s initial responses should be taken with a grain of salt because Turkey is temporarily blocking Finland’s and Sweden’s applications, so Russia has no need to respond to NATO enlargement yet. But the true test will come when and if the West satisfies Turkey’s grievances and Turkey moves to admit the new members. If enlargement becomes inevitable, Russia will respond. Russia will feel that its national security is fundamentally jeopardized by Sweden overturning two centuries of neutrality and Finland reversing the policy of “Finlandization” that went so far in preventing conflict during the Cold War. Chart 4Military Balances Stacking Up Against Russia Russia’s military options are limited. Russia has little ability to expand the war and fight on multiple fronts judging by the army’s recent performance in Ukraine and the Red Army’s performance in the Winter War of 1939. This point can be illustrated by taking the military balance of Russia and its most immediate adversaries, which add up to about half of Russian military strength even apart from NATO (Chart 4). Russian armed forces already demonstrated some pragmatism in April by withdrawing from Kyiv and focusing on more achievable war aims. Unless President Putin turns utterly reckless and the Russian state fails to restrain him, Russia will opt for defensive measures and strategic deterrence rather than a military offensive in the Baltics. Hence Russia’s military response will come in the form of threats rather than outright belligerence. However, these threats will probably include military and nuclear actions that will raise alarm bells across Europe and the United States. President Dmitri Medvedev has already warned of the permanent deployment of nuclear missiles in the Kaliningrad exclave.2 This statement points to only the most symbolic option of a range of options that will increase deterrence and elevate the fear of war. Otherwise Russia’s retaliation will consist of squeezing global energy supply, as discussed above, including by opening a new front in the Middle East and North Africa. Instability should be expected as a way of constraining Europe and distracting America. Higher energy prices may or may not convince the EU to negotiate better terms with Russia but they will sow divisions within and among the allies. Ultimately Russia is highly unlikely to sacrifice its credibility by failing to retaliate for the combination of energy embargo and NATO enlargement on its borders. Since its military options are becoming constrained (at least its rational ones), its economic and asymmetrical options will grow in importance. The result will be additional energy supply constraints. Bottom Line: Even assuming that the war does not spread beyond Ukraine – likely but not certain – global financial markets face at least one more period of military escalation with Russia. This will likely include significant energy cutoffs and saber-rattling – even nuclear threats – over NATO enlargement. China’s Political Situation Has Not Normalized China continues to suffer from a historic confluence of internal and external political risk that will cause negative surprises for investors. Temporary improvements in government policy or investor sentiment – centered on a relaxation of “Zero Covid” lockdowns in major cities and a more dovish regulatory tone against the tech giants – will likely be frustrated, at least until after a more dovish government stance can be confirmed in the wake of the twentieth national party congress in October or November this year. At that event, Chinese President Xi Jinping is likely to clinch another ten years in power and complete the transformation of China’s governance from single-party rule to single-person rule. This reversion to autocracy will generate additional market-negative developments this year. It has already embedded a permanently higher risk premium in Chinese financial assets because it increases the odds of policy mistakes, international aggression, and ultimately succession crisis. The most successful Asian states chose to democratize and expand free markets and capitalism when they reached a similar point of economic development and faced the associated sociopolitical challenges. But China is choosing the opposite path for the sake of national security. Investors have seen the decay of Russia’s economy under Putin’s autocracy and would be remiss not to upgrade the odds of similarly negative outcomes in China over the long run as a result of Xi’s autocracy, despite the many differences between the two countries. China’s situation is more difficult than that of the democratic Asian states because of its reviving strategic rivalry with the United States. US Secretary of State Antony Blinken recently unveiled President Biden’s comprehensive China policy. He affirmed that the administration views China as the US’s top strategic competitor over the long run, despite the heightened confrontation with Russia.3 The Biden administration has not eased the Trump administration’s tariffs or punitive measures on China. It is unlikely to do so during a midterm election year when protectionist dynamics prevail – especially given that the Xi administration will be in the process of reestablishing autocracy, and possibly repressing social unrest, at the very moment Americans go to the polls. Re-engagement with China is also prohibited because China is strengthening its strategic bonds with Russia. President Biden has repeatedly implied that the US would defend Taiwan in any conflict with China. These statements are presented as gaffes or mistakes but they are in fact in keeping with historical US military actions threatening counter-attack during the three historic Taiwan Strait crises. The White House quickly walks back these comments to reassure China that the US does not support Taiwanese independence or intend to trigger a war with China. The result is that the US is using Biden’s gaffe-prone personality to reemphasize the hard edge (rather than the soft edge) of the US’s policy of “strategic ambiguity” on Taiwan. US policy is still ambiguous but ambiguity includes the possibility that a president might order military action to defend Taiwan. US attempts to increase deterrence and avoid a Ukraine scenario are threatening for China, which will view the US as altering the status quo and penalizing China for Russia’s actions. Beijing resumed overflights of Taiwan’s air defense identification zone in the wake of Biden’s remarks as well as the decision of the US to send Senator Tammy Duckworth to Taiwan to discuss deeper economic and defense ties. Consider the positioning of US aircraft carrier strike groups as an indicator of the high level of strategic tensions. On January 18, 2022, as Russia amassed military forces on the Ukrainian border – and the US and NATO rejected its strategic demands – the US had only one publicly acknowledged aircraft carrier in the Mediterranean (the USS Harry Truman) whereas it had at least five US carriers in East Asia. On February 24, the day of Russia’s invasion of Ukraine, the US had at least four of these carriers in Asia. Even today the US has at least four carriers in the Pacific compared to at least two in Europe – one of which, notably, is in the Baltics to deter Russia from attacking Finland and Sweden (Map 3). The US is warning China not to take advantage of the Ukraine war by staging a surprise attack on Taiwan. Map 3Amid Ukraine War, US Deters China From Attacking Taiwan Of course, strategic tensions are perennial, whereas what investors are most concerned about is whether China can secure its economic recovery. The latest data are still disappointing. Credit growth continues to falter as the private sector struggles with a deteriorating demographic and macroeconomic outlook (Chart 5). The credit impulse has entered positive territory, when local government bonds are included, reflecting government stimulus efforts. But it is still negative when excluding local governments. And even the positive measure is unimpressive, having ticked back down in April (Chart 6). Chart 5Credit Growth Falters Amid Economic Transition Chart 6Silver Lining: Credit Impulse Less Negative Bottom Line: Further monetary and fiscal easing will come in China, a source of good news for global investors next year if coupled with a broader policy shift in favor of business, but the effects will be mixed this year due to Covid policy and domestic politics. Taken together with a European energy crunch and Middle Eastern oil supply disruptions, China’s stimulus is not a catalyst for a sustainable global equity market rally this year. South Asia: Inflation Hammers Sri Lanka And Pakistan Since 2020 we have argued that the global pandemic would result in a new wave of supply pressures and global social unrest. High inflation is blazing a trail of destruction in emerging markets, notably in South Asia, where per capita incomes are low and political institutions often fragile. Chart 7South Asia: Surging Inflation Sri Lanka has been worst affected (Chart 7). Inflation surged to an eye-watering 34% in April and is expected to rise further. Surging inflation has affected Sri Lanka disproportionately because its macroeconomic and political fundamentals were weak to begin with. The tourism-dependent Sri Lankan economy suffered a body blow from terrorist attacks in 2019 and the pandemic in 2020-21. Then 2022 saw a power struggle between Sri Lanka’s President Gotabaya Rajapaksa and members of the national assembly including Prime Minister (PM) Mahinda Rajapaksa. The crisis hit a crescendo when the country defaulted on external debt obligations last month. These events weigh on Sri Lanka’s ability to transition from a long civil war (1983-2009) to a path of sustained economic development. While the political crisis has seemingly stabilized following the appointment of new Prime Minister Ranil Wickremesinghe, we remain bearish on a strategic time horizon. This is mainly because the new PM is unlikely to bring about structural solutions for Sri Lanka’s broken economy. Moreover, Sri Lanka holds more than $50 billion of foreign debt, or 62% of GDP. Another country that has been dealing with political instability alongside high inflation in South Asia is Pakistan, where inflation hit a three-year high in April (see Chart 7 above). The latest twist in Pakistan’s never-ending cycle of political uncertainty comes from the ousted Prime Minister Imran Khan. The former PM, who commands an unusual popular support group due to his fame as a cricketer prior to entering politics, is demanding fresh elections and otherwise threatening to hold mass protests. Pakistan’s new coalition government and Prime Minister Shehbaz Sharif, who came to power amid parliamentary intrigues, are refusing elections and ultimatums. From a structural perspective Pakistan is characterized by a weak economy and an unusually influential military. Now it faces high inflation and rising food prices – indeed it is one of the countries that is most dangerously exposed to the Russia-Ukraine war as it depends on these two for over 70% of its grain imports. Bottom Line: MSCI Sri Lanka has underperformed the MSCI EM index by 58.3% this year to date. Pakistan has underperformed the same index by 41.6% over the same period. Against this backdrop, we remain strategic sellers of both bourses. Instability in these countries is also one of the factors behind our strategic assessment of India as a country with a growing domestic policy consensus. South Asia: India’s Fiscal Populism And Geopolitics Inflation is less rampant in India, although still troublesome. Consumer prices nearly jumped to an 8-year high in April (see Chart 7). With a loaded state election calendar due over the next 12-18 months, the jump in inflation naturally triggered a series of mitigating policy responses. Ban On Wheat Exports: India produces 14% of the world’s wheat and 11% of grains, and exports 5% and 7%, respectively. India’s exports could make a large profit in the context of global shortages. But Prime Minister Narendra Modi is entering into the political end of the business cycle, with key state elections due that will have an impact on the ruling party’s political standing two years before the next federal election. He fears political vulnerability if exports continue amid price pressures at home. The emphasis on food security is typical but also bespeaks a lack of commitment to economic reform. Chart 8India's Real Interest Rates Fall Surprise Rate Hikes: The Reserve Bank of India (RBI) increased the policy repo rate by 40 basis points at an unscheduled meeting on May 4, thereby implementing its first rate hike since August 2018. With real rates in India lower than those in China or Brazil (Chart 8), the RBI will be forced to expedite its planned rate hikes through 2022. Tax Cuts On Fuel: India’s central government also announced steep cuts in excise duty on fuel. This is another populist measure that reduces political pressures but fails to encourage the private sector to adjust. These measures will help rein in inflation but the rate hikes will weigh on economic growth while the tax cuts will add to India’s fiscal deficit. Indeed, India is resorting to fiscal populism with key state elections looming. Geopolitical risk is less of a concern for India – indeed the Ukraine war has strengthened its bargaining position. In the short run, India benefits from the ability to buy arms and especially cheap oil from Russia while the EU imposes an embargo. But over the long run its economy and security can be strengthened by greater interest from the US and its allies, recently highlighted by the fourth meeting of the Quadrilateral Security Dialogue (Quad) and the launch of the US’s Indo-Pacific Economic Framework (IPEF). These initiatives are modest but they highlight the US’s need to replace China with India and ASEAN over time, a trend that no US administration can reverse now because of the emerging Russo-Chinese strategic alliance. At the same time, the Quad underscores India’s maritime interests and hence the security benefits India can gain from aligning its economy and navy with the other democracies. Bottom Line: Fiscal populism in the context of high commodity prices is negative for Indian equities. However, our views on Russia, the Middle East, and China all point to a sharper short-term spike in commodity prices that ultimately drives the world economy deeper into stagflation or recession. Therefore we are booking a 22.5% profit on our tactical decision to go long Brazilian financials relative to Indian equities. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Chart 9Russia: GeoRisk Indicator Chart 10Other Measures Of Russian Geopolitical Risk Chart 11China: GeoRisk Indicator Chart 12United Kingdom: GeoRisk Indicator Chart 13Germany: GeoRisk Indicator Chart 14France: GeoRisk Indicator Chart 15Italy: GeoRisk Indicator Chart 16Canada: GeoRisk Indicator Chart 17Spain: GeoRisk Indicator Chart 18Australia: GeoRisk Indicator Chart 19Taiwan: GeoRisk Indicator Chart 20Korea: GeoRisk Indicator Chart 21Turkey: GeoRisk Indicator Chart 22South Africa: GeoRisk Indicator Chart 23Brazil: GeoRisk Indicator Footnotes 1 Recent diplomatic flaps between core European leaders and Ukrainian President Volodymyr Zelensky reflect Ukraine’s fear that Europe will negotiate a “separate peace” with Russia, i.e. accept Russian territorial conquests in exchange for economic relief. 2 Dmitri Medvedev explicitly states ‘there can be no more talk of any nuclear-free status for the Baltic - the balance must be restored’ in warning Finland and Sweden joining NATO. Medvedev is suggesting that nuclear weapons will be placed in this area where Russia has its Kaliningrad exclave sandwiched between Poland and Lithuania. Guy Faulconbridge, ‘Russia warns of nuclear, hypersonic deployment if Sweden and Finland join NATO’, April 14, 2022, Reuters. 3 See Antony J Blinken, Secretary of State, ‘The Administration’s Approach to the People’s Republic of China’, The George Washington University, Washington D.C., May 26, 2022, state.gov. Additionally, see President Joe Biden’s remarks on China and getting involved military to defend Taiwan in a joint press conference with Japan’s Prime Minister Kishida Fumio. ‘Remarks by President Biden and Prime Minister Kishida Fumio of Japan in Joint Press Conference’, Akasaka Palace, Tokyo, Japan, May 23, 2022, whitehouse.gov. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix Section III: Geopolitical Calendar

Executive Summary Macron Still Favored, But Le Pen Cannot Be Ruled Out Macron is still favored to win the French election but Le Pen’s odds are 45%. Le Pen would halt France’s neoliberal structural reforms, paralyze EU policymaking, and help Russia’s leverage in Ukraine. But she would lack legislative support and would not fatally wound the EU or NATO. European political risk will remain high in Germany, Italy, and Spain. Favor UK equities on a relative basis. Financial markets are complacent about Russian geopolitical risk again. Steer clear of eastern European assets. Do not bottom feed in Chinese stocks. China faces social unrest. North Korean geopolitical risk is back. Australia’s election is an opportunity, not a risk. Stay bullish on Latin America. Prefer Brazil over India. Stay negative on Turkey and Pakistan. Trade Recommendation Inception Date Return TACTICALLY LONG US 10-YEAR TREASURY 2022-04-14 Bottom Line: Go long the US 10-year Treasury on geopolitical risk and near-term peak in inflation. Feature Last year we declared that European political risk had reached a bottom and had nowhere to go but up. Great power rivalry with Russia primarily drove this view but we also argued that our structural theme of populism and nationalism would feed into it. Related Report Geopolitical StrategyThe Geopolitical Consequences Of The Ukraine War In other words, the triumph of the center-left political establishment in the aftermath of Covid-19 would be temporary. The narrow French presidential race highlights this trend. President Emmanuel Macron is still favored but Marine Le Pen, his far-right, anti-establishment opponent, could pull off an upset victory on April 24. The one thing investors can be sure of is that France’s ability to pursue neoliberal structural reforms will be limited even if Macron wins, since he will lack the mandate he received in 2017. Our GeoRisk Indicators this month suggest that global political trends are feeding into today’s stagflationary macroeconomic context. Market Complacent About Russia Again Global financial markets are becoming complacent about European security once again. Markets have begun to price a slightly lower geopolitical risk for Russia after it withdrew military forces from around Kyiv in an open admission that it failed to overthrow the government. However, western sanctions are rising, not falling, and Russia’s retreat from Kyiv means it will need to be more aggressive in the south and east (Chart 1). Chart 1Russia: GeoRisk Indicator Russia has not achieved its core aim of a militarily neutral Ukraine – so it will escalate the military effort to achieve its aim. Any military failure in the east and south would humiliate the Putin regime and make it more unpredictable and dangerous. The West has doubled down on providing Ukraine with arms and hitting Russia with sanctions (e.g. imposing a ban on Russian coal). Germany prevented an overnight ban on Russian oil and natural gas imports but the EU is diversifying away from Russian energy rapidly. Sanctions that eat away at Russia’s export revenues will force it to take a more aggressive posture now, to achieve a favorable ceasefire before funding runs out. Sweden and Finland are reviewing whether to join NATO, with recommendations due by June. Russia will rattle sabers to underscore its red line against NATO enlargement and will continue to threaten “serious military-political repercussions” if these states try to join. We would guess they would remain neutral as a decision to join NATO could lead to a larger war. Bottom Line: Global equities will remain volatile due to a second phase of the war and potential Russian threats against Ukraine’s backers. European equities and currency, especially in emerging Europe, will suffer a persistent risk premium until a ceasefire is concluded. What If Le Pen Wins In France? By contrast with the war in Ukraine, the French election is a short-term source of political risk. A surprise Le Pen victory would shake up the European political establishment but investors should bear in mind that it would not revolutionize the continent or the world, as Le Pen’s powers would be limited. Unlike President Trump in 2017, she would not take office with her party gaining full control of the legislature. Le Pen rallied into the first round of the election on April 10, garnering 23% of the vote, up from 21% in 2017. This is not a huge increase in support but her odds of winning this time are much better than in 2017 because the country has suffered a series of material shocks to its stability. Voters are less enthusiastic about President Macron and his centrist political platform. Macron, the favorite of the political establishment, received 28% of the first-round vote, up from 24% in 2017. Thus he cannot be said to have disappointed expectations, though he is vulnerable. The euro remains weak against the dollar and unlikely to rally until Russian geopolitical risk and French political risk are decided. The market is not fully pricing French risk as things stand (Chart 2). Chart 2France: GeoRisk Indicator The first-round election results show mixed trends. The political establishment suffered but so did the right-wing parties (Table 1). The main explanation is that left-wing, anti-establishment candidate Jean-Luc Mélenchon beat expectations while the center-right Republicans collapsed. Macron is leading Le Pen by only five percentage points in the second-round opinion polling as we go to press (Chart 3). Macron has maintained this gap throughout the race so far and both candidates are very well known to voters. But Le Pen demonstrated significant momentum in the first round and momentum should never be underestimated. Table 1Results Of France’s First-Round Election Chart 3French Election: Macron Maintains Lead Are the polls accurate? Anti-establishment candidates outperformed their polling by 7 percentage points in the first round. Macron, the right-wing candidates, and the pro-establishment candidates all underperformed their March and April polls (Chart 4). Hence investors should expect polls to underrate Le Pen in the second round. Chart 4French Polls Fairly Accurate Versus First-Round Results Given the above points, it is critical to determine which candidate will gather the most support from voters whose first preference got knocked out in the first round. The strength of anti-establishment feeling means that the incumbent is vulnerable while ideological camps may not be as predictable as usual. Mélenchon has asked his voters not to give a single vote to Le Pen but he has not endorsed Macron. About 21% of his supporters say they will vote for Le Pen. Only a little more of them said they would vote for Macron, at 27% (Chart 5). Chart 5To Whom Will Voters Drift? Diagram 1, courtesy of our European Investment Strategy, illustrates that Macron is favored in both scenarios but Le Pen comes within striking distance under certain conservative assumptions about vote switching. Diagram 1Extrapolating France’s First-Round Election To The Second Round Macron’s approval rating has improved since the pandemic. This is unlike the situation in other liberal democracies (Chart 6). Chart 6Macron Handled Pandemic Reasonably Well The pandemic is fading and the economy reviving. Unemployment has fallen from 8.9% to 7.4% over the course of the pandemic. Real wage growth, at 5.8%, is higher than the 3.3% that prevailed when Macron took office in 2017 (Chart 7). Chart 7Real Wages A Boon For Macron But these positives do not rule out a Le Pen surprise. The nation has suffered not one but a series of historic shocks – the pandemic, inflation, and the war in Ukraine. Inflation is rising at 5.1%, pushing the “Misery Index” (inflation plus unemployment) to 12%, higher than when Macron took office, even if lower than the EU average (Chart 8). Chart 8Misery Index The Key Threat To Macron Le Pen has moderated her populist message and rebranded her party in recent years to better align with the median French voter. She claims that she will not pursue a withdrawal from the European Union or the Euro Area currency union. This puts her on the right side of the one issue that disqualified her from the presidency in the past. Yet French trust in the EU is declining markedly, which suggests that Le Pen is in step with the median voter on wanting greater French autonomy (Chart 9). Le Pen’s well-known sympathy toward Vladimir Putin and Russia is a liability in the context of Russian aggression in Ukraine. Only 35% of French people had a positive opinion of Russia back in 2019, whereas 50% had a favorable view of NATO, and the gap has likely grown as a result of the invasion (Chart 10). However, the historic bout of inflation suggests that economic policy could be the most salient issue for voters rather than foreign policy. Chart 9Le Pen Only Electable Because She Accepted Europe Chart 10Le Pen’s NATO Stance Not Disqualifying Le Pen’s economic platform is fiscally liberal and protectionist, which will appeal to voters upset over the rising cost of living and pressures of globalization. She wants to cut the income tax and value-added tax, while reversing Macron’s attempt at raising the retirement age and reforming the pension system. France’s tax rates on income, and on gasoline and diesel, are higher than the OECD average. In other words, Macron is running on painful structural reform while Le Pen is running on fiscal largesse. This is another reason to take seriously the risk of a Le Pen victory. What should investors expect if Le Pen pulls off an upset? France’s attempt at neoliberal structural reforms would grind to a halt. While Le Pen may not be able to pass domestic legislation, she would be able to halt the implementation of Macron’s reforms. Productivity and the fiscal outlook would suffer. Le Pen’s ability to change domestic policy will be limited by the National Assembly, which is due for elections from June 12-19. Her party, the National Rally (formerly the Front National), has never won more than 20% of local elections and performed poorly in the 2017 legislative vote. Investors should wait to see the results of the legislative election before drawing any conclusions about Le Pen’s ability to change domestic policy. France’s foreign policy would diverge from Europe’s. If Le Pen takes the presidency, she will put France at odds with Brussels, Berlin, and Washington, in much the same way that President Trump did. She would paralyze European policymaking. Yet Le Pen alone cannot take France out of the EU. The French public’s negative view of the EU is not the same as a majority desire to leave the bloc – and support for the euro currency stands at 69%. Le Pen does not have the support for “Frexit,” French exit from the EU. Moreover European states face immense pressures to work together in the context of global Great Power Rivalry. Independently they are small compared to the US, Russia, and China. Hence the EU will continue to consolidate as a geopolitical entity over the long run. Russia, however, would benefit from Le Pen’s presidency in the context of Ukraine ceasefire talks. EU sanctions efforts would freeze in place. Le Pen could try to take France out of NATO, though she would face extreme opposition from the military and political establishment. If she succeeded on her own executive authority, the result would be a division among NATO’s ranks in the face of Russia. This cannot be ruled out: if the US and Russia are fighting a new Cold War, then it is not unfathomable that France would revert to its Cold War posture of strategic independence. However, while France withdrew from NATO’s integrated military command from 1966-2009, it never withdrew fully from the alliance and was always still implicated in mutual defense. In today’s context, NATO’s deterrent capability would not be much diminished but Le Pen’s administration would be isolated. Russia would be unable to give any material support to France’s economy or national defense. Bottom Line: Macron is still favored for re-election but investors should upgrade Le Pen’s chances to a subjective 45%. If she wins, the euro will suffer a temporary pullback and French government bond spreads will widen over German bunds. The medium-term view on French equities and bonds will depend on her political capability, which depends on the outcome of the legislative election from June 12-19. She will likely be stymied at home and only capable of tinkering with foreign policy. But if she has legislative support, her agenda is fiscally stimulative and would produce a short-term sugar high for French corporate earnings. However, it would be negative for long-term productivity. UK, Italy, Spain: Who Else Faces Populism? Chart 11Rest Of Europe: GeoRisk Indicators Between Russian geopolitical risk and French political risk, other European countries are likely to see their own geopolitical risk premium rise (Chart 11). But these countries have their own domestic political dynamics that contribute to the reemergence of European political risk. Germany’s domestic political risk is relatively low but it faces continued geopolitical risk in the form of Russia tensions, China’s faltering economy, and potentially French populism (Chart 11, top panel). In Italy, the national unity coalition that took shape under Prime Minister Mario Draghi was an expedient undertaken in the face of the pandemic. As the pandemic fades, a backlash will take shape among the large group of voters who oppose the EU and Italian political establishment. The Italian establishment has distributed the EU recovery funds and secured the Italian presidency as a check on future populist governments. But it may not be able to do more than that before the next general election in June 2023, which means that populism will reemerge and increase the political risk premium in Italian assets going forward (Chart 11, second panel). Spain is still a “divided nation” susceptible to a rise in political risk ahead of the general election due by December 10, 2023. However, the conservative People’s Party, the chief opposition party, has suffered from renewed infighting, which gives temporary relief to the ruling Socialist Worker’s Party of Prime Minister Pedro Sanchez. The Russia-Ukraine issue caused some minor divisions within the government but they are not yet leading to any major political crisis, as nationwide pro-Ukraine sentiment is largely unified. The Andalusia regional election, which is expected this November, will be a check point for the People’s Party’s new leadership and a test run for next year’s general election. Andalusia is the most populous autonomous community in Spain, consisting about 17% of the seats in the congress (the lower house). The risk for Sanchez and the Socialists is that the opposition has a strong popular base and this fact combined with the stagflationary backdrop will keep political polarization high and undermine the government’s staying power (Chart 11, third panel). While Prime Minister Boris Johnson has survived the scandal over attending social events during Covid lockdowns, as we expected, nevertheless the Labour Party is starting to make a comeback that will gain momentum ahead of the 2024 general election. Labour is unlikely to embrace fiscal austerity or attempt to reverse Brexit anytime soon. Hence the UK’s inflationary backdrop will persist (Chart 11, fourth panel). Bottom Line: European political risk has bottomed and will rise in the coming months and years, although the EU and Eurozone will survive. We still favor UK equities over developed market equities (excluding the US) because they are heavily tilted toward consumer staples and energy sectors. Stay long GBP-CZK. Favor European defense stocks over tech. Prefer Spanish stocks over Italian. China: Social Unrest More Likely China’s historic confluence of internal and external risks continues – and hence it is too soon for global investors to try to bottom-feed on Chinese investable equities (Chart 12). A tactical opportunity might emerge for non-US investors in 2023 but now is not the right time to buy. Chart 12China: GeoRisk Indicator In domestic politics, the reversion to autocracy under Xi is exacerbating the economic slowdown. True, Beijing is stimulating the economy by means of its traditional monetary and fiscal tools. The latest data show that the total social financing impulse is reviving, primarily on the back of local government bonds (Chart 13). Yet overall social financing is weaker because private sector sentiment remains downbeat. The government is pursuing excessively stringent social restrictions in the face of the pandemic. Beijing is doubling down on “Covid Zero” policy by locking down massive cities such as Shanghai. The restrictions will fail to prevent the virus from spreading. They are likely to engender social unrest, which we flagged as our top “Black Swan” risk this year and is looking more likely. Lockdowns will also obstruct production and global supply chains, pushing up global goods inflation. Meanwhile the property sector continues to slump on the back of weak domestic demand, large debt levels, excess capacity, regulatory scrutiny, and negative sentiment. Consumer borrowing appetite and general animal spirits are weak in the face of the pandemic and repressive political environment (Chart 14). Chart 13China's Stimulus Has Clearly Arrived Chart 14Yet Chinese Animal Spirits Still Suffering Hence China will be exporting slow growth and inflation – stagflation – to the rest of the world until after the party congress. At that point President Xi will feel politically secure enough to “let 100 flowers bloom” and try to improve economic sentiment at home and abroad. This will be a temporary phenomenon (as were the original 100 flowers under Chairman Mao) but it will be notable for 2023. In foreign politics, Russia’s attack on Ukraine has accelerated the process of Russo-Chinese alliance formation. This partnership will hasten US containment strategy toward China and impose a much faster economic transition on China as it pursues self-sufficiency. The result will be a revival of US-China tensions. The implications are negative for the rest of Asia Pacific: Taiwanese geopolitical risk will continue rising for reasons we have outlined in previous reports. In addition, Taiwanese equities are finally starting to fall off from the pandemic-induced semiconductor rally (Chart 15). The US and others are also pursuing semiconductor supply security, which will reduce Taiwan’s comparative advantage. Chart 15Taiwan: GeoRisk Indicator South Korea faces paralysis and rising tensions with North Korea. The presidential election on May 9 brought the conservatives back into the Blue House. The conservative People Power Party’s candidate, Yoon Suk-yeol, eked out a narrow victory that leaves him without much political capital. His hands are also tied by the National Assembly, at least for the next two years. He will attempt to reorient South Korean foreign policy toward the US alliance and away from China. He will walk away from the “Moonshine” policy of engagement with North Korea, which yielded no fruit over the past five years. North Korea has responded by threatening a nuclear missile test, restarting intercontinental ballistic missile tests for the first time since 2017, and adopting a more aggressive nuclear deterrence policy in which any South Korean attack will ostensibly be punished by a massive nuclear strike. Tensions on the peninsula are set to rise (Chart 16). Three US aircraft carrier groups are around Japan today, despite the war in Europe (where two are placed), suggesting high threat levels. Chart 16South Korea: GeoRisk Indicator Australia’s elections present opportunity rather than risk. Prime Minister Scott Morrison formally scheduled them for May 21. The Australian Labor Party is leading in public opinion and will perform well. The election threatens a change of parties but not a drastic change in national policy – populist parties are weak. No major improvement in China relations should be expected. Any temporary improvement, as with the Biden administration, will be subject to reversal due to China’s long-term challenge to the liberal international order. Cyclically the Australian dollar and equities stand to benefit from the global commodity upcycle as well as relative geopolitical security due to American security guarantees (Chart 17). Chart 17Australia: GeoRisk Indicator Bottom Line: China’s reversion to autocracy will keep global sentiment negative on Chinese equities until 2023 at earliest. Stay short the renminbi and Taiwanese dollar. Favor the Japanese yen over the Korean won. Favor South Korean over Taiwanese equities. Look favorably on the Australian dollar. Turkey, South Africa, And … Canada Turkish geopolitical risk will remain elevated in the context of a rampant Russia, NATO’s revival and tensions with Russia, the threat of commerce destruction and accidents in the Black Sea region, domestic economic mismanagement, foreign military adventures, and the threat posed to the aging Erdogan regime by the political opposition in the wake of the pandemic and the lead-up to the 2023 elections (Chart 18). Chart 18Turkey: GeoRisk Indicator While we are tactically bullish on South African equities and currency, we expect South African political risk to rise steadily into the 2024 general election. Almost a year has passed since the civil unrest episode of 2021. Covid-19 lockdowns have been lifted and the national state of disaster has ended, which has helped quell social tensions. This is evident in the decline of our South Africa GeoRisk indicator from 2021 highs (Chart 19). While fiscal austerity is under way in South Africa, we have argued that fiscal policy will reverse course in time for the 2024 election. In this year’s fiscal budget, the budget deficit is projected to narrow from -6% to -4.2% over the next two years. Government has increased tax revenue collection through structural reforms that are rooting out corruption and wasteful expenditure. But the ANC will have to tap into government spending to shore up lost support come 2024. Thus South Africa benefits tactically from commodity prices but cyclically the currency is vulnerable. Chart 19South Africa: GeoRisk Indicator Canadian political risk will rise but that should not deter investors from favoring Canadian assets that are not exposed to the property bubble. Prime Minister Justin Trudeau has had a net negative approval rating since early 2021 and his government is losing political capital due to inflation, social unrest, and rising difficulties with housing affordability (Chart 20). While he does not face an election until 2025, the Conservative Party is developing more effective messaging. Chart 20Canada: GeoRisk Indicator India Will Stay Neutral But Lean Toward The West Chart 21Sino-Pak Alliance’s Geopolitical Power Is Thrice That Of India US President Joe Biden has openly expressed his administration’s displeasure regarding India’s response to Russia’s invasion of Ukraine. This has led many to question the strength of Indo-US relations and the direction of India’s geopolitical alignments. To complicate matters, China’s overtures towards India have turned positive lately, leading clients to ask if a realignment in Indo-China relations is nigh. To accurately assess India’s long-term geopolitical propensities, it is important to draw a distinction between ‘cyclical’ and ‘structural’ dynamics that are at play today. Such a distinction yields crystal-clear answers about India’s strategic geopolitical leanings. In specific: Indo-US Relations Will Strengthen On A Strategic Horizon: As the US’s and China’s grand strategies collide, minor and major geopolitical earthquakes are bound to take place in South Asia and the Indo-Pacific. Against this backdrop, India will strategically align with the US to strengthen its hand in the region (Chart 21). While the Russo-Ukrainian war is a major global geopolitical event, for India this is a side-show at best. True, India will retain aspects of its historic good relations with Russia. Yet countering China’s encirclement of India is a far more fundamental concern for India. Since Russia has broken with Europe, and China cannot reject Russia’s alliance, India will gradually align with the US and its allies. India And China Will End Up As A Conflicting Dyad: Strategic conflict between the two Asian powers is likely because China’s naval development and its Eurasian strategy threaten India’s national security and geopolitical imperatives, while India’s alliances are adding to China’s distrust of India. Thus any improvement in Sino-Indian diplomatic relations will be short-lived. The US will constantly provide leeway for India in its attempts to court India as a key player in the containment strategy against China. The US and its allies are the premier maritime powers and upholders of the liberal world order – India serves its national interest better by joining them rather than joining China in a risky attempt to confront the US navy and revolutionize the world order. Indo-Russian Relations Are Bound To Fade In The Long Run: India will lean towards the US over the next few years for reasons of security and economics. But India’s movement into America’s sphere of influence will be slow – and that is by design. India is testing waters with America through networks like the Quadrilateral Dialogue. It sees its historic relationship with Russia as a matter of necessity in the short run and a useful diversification strategy in the long run. True, India will maintain a trading relationship with Russia for defense goods and cheap oil. But this trade will be transactional and is not reason enough for India to join Russia and China in opposing US global leadership. While these factors will mean that Indo-Russian relations are amicable over a cyclical horizon, this relationship is bound to fade over a strategic horizon as China and Russia grow closer and the US pursues its grand strategy of countering China and Russia. Bottom Line: India may appear to be neutral about the Russo-Ukrainian war but India will shed its historical stance of neutrality and veer towards America’s sphere of influence on a strategic timeframe. India is fully aware of its strategic importance to both the American camp and the Russo-Chinese camp. It thus has the luxury of making its leanings explicit after extracting most from both sides. Long Brazil / Short India Brazil’s equity markets have been on a tear. MSCI Brazil has outperformed MSCI EM by 49% in 2022 YTD. Brazil’s markets have done well because Brazil is a commodity exporter and the war in Ukraine has little bearing on faraway Latin America. This rally will have legs although Brazil’s political risks will likely pick back up in advance of the election (Chart 22). The reduction in Brazil’s geopolitical risk so far this year has been driven mainly by the fact that the currency has bounced on the surge in commodity prices. In addition, former President Lula da Silva is the current favorite to win the 2022 presidential elections – Lula is a known quantity and not repugnant to global financial institutions (Chart 23). Chart 22Brazil's Markets Have Benefitted From Rising Commodity Prices Chart 23Brazil: Watch Out For Political Impact Of Commodity Prices Whilst there is no denying that the first-round effects of the Ukraine war have been positive for Brazil, there is a need to watch out for the second-round effects of the war as Latin America’s largest economy heads towards elections. Surging prices will affect two key constituencies in Brazil: consumers and farmers. Consumer price inflation in Brazil has been ascendant and adding to Brazil’s median voter’s economic miseries. Rising inflation will thus undermine President Jair Bolsonaro’s re-election prospects further. The fact that energy prices are a potent polling issue is evinced by the fact that Bolsonaro recently sacked the chief executive of Petrobras (i.e. Brazil’s largest listed company) over rising fuel costs. Furthermore, Brazil is a leading exporter of farm produce and hence also a large importer of fertilizers. Fertilizer prices have surged since the war broke out. This is problematic for Brazil since Russia and Belarus account for a lion’s share of Brazil’s fertilizer imports. Much like inflation in general, the surge in fertilizer prices will affect the elections because some of the regions that support Bolsonaro also happen to be regions whose reliance on agriculture is meaningful (Map 1). They will suffer from higher input prices. Map 1States That Supported Bolso, Could Be Affected By Fertilizer Price Surge Chart 24Long Brazil Financials / Short India Given that Bolsonaro continues to lag Lula on popularity ratings – and given the adverse effect that higher commodity prices will have on Brazil’s voters – we expect Bolsonaro to resort to fiscal populism or attacks on Brazil’s institutions in a last-ditch effort to cling to power. He could even be emboldened by the fact that Sérgio Moro, the former judge and corruption fighter, decided to pull out of the presidential race. This could provide a fillip to Bolso’s popularity. Bottom Line: Brazil currently offers a buying opportunity owing to attractive valuations and high commodity prices. But investors should stay wary of latent political risks in Brazil, which could manifest themselves as presidential elections draw closer. We urge investors to take-on only selective tactical exposure in Brazil for now. Equities appear cheap but political and macro risks abound. To play the rally yet stave off political risk, we suggest a tactical pair trade: Long Brazil Financials / Short India (Chart 24). Whilst we remain constructive on India on a strategic horizon, for the next 12 months we worry about near-term macro and geopolitical headwinds as well as India’s rich valuations. Don’t Buy Into Pakistan’s Government Change Chart 25Pakistan’s Military Is Unusually Influential The newest phase in Pakistan’s endless cycle of political instability has begun. Prime Minister Imran Khan has been ousted. A new coalition government and a new prime minister, Shehbaz Sharif, have assumed power. Prime Minister Sharif’s appointment may make it appear like risks imposed by Pakistan have abated. After all, Sharif is seen as a good administrator and has signaled an interest in mending ties with India. But despite the appearance of a regime change, geopolitical risks imposed by Pakistan remain intact for three sets of reasons: Military Is Still In Charge: Pakistan’s military has been and remains the primary power center in the country (Chart 25). Former Prime Minister Khan’s rise to power was possible owing to the military’s support and he fell for the same reason. Since the military influences the civil administration as well as foreign policy, a lasting improvement in Indo-Pak relations is highly unlikely. Risk Of “Rally Round The Flag” Diversion: General elections are due in Pakistan by October 2023. Sharif is acutely aware of the stiff competition he will face at these elections. His competitors exist outside as well as inside his government. One such contender is Bilawal Bhutto-Zardari of the Pakistan People’s Party (PPP), which is a key coalition partner of the new government that assumed power. Imran Khan himself is still popular and will plot to return to power. Against such a backdrop the newly elected PM is highly unlikely to pursue an improvement in Indo-Pak relations. Such a strategy will adversely affect his popularity and may also upset the military. Hence we highlight the risk of the February 2021 Indo-Pak ceasefire being violated in the run up to Pakistan’s general elections. India’s government has no reason to prevent tensions, given its own political calculations and the benefits of nationalism. Internal Social Instability Poor: Pakistan is young but the country can be likened to a social tinderbox. Many poor youths, a weak economy, and inadequate political valves to release social tensions make for an explosive combination. Pakistan remains a source of geopolitical risk for the South Asian region. Some clients have inquired as to whether the change of government in Pakistan implies closer relations with the United States. The US has less need for Pakistan now that it has withdrawn from Afghanistan. It is focused on countering Russia and China. As such the US has great need of courting India and less need of courting Pakistan. Pakistan will remain China’s ally and will struggle to retain significant US assistance. Bottom Line: We remain strategic sellers of Pakistani equities. Pakistan must contend with high internal social instability, a weak democracy, a weak economy and an unusually influential military. As long as the military remains excessively influential in Pakistan, its foreign policy stance towards India will stay hostile. Yet the military will remain influential because Pakistan exists in a permanent geopolitical competition with India. And until Pakistan’s economy improves structurally and endemically, its alliance with China will stay strong. Investment Takeaways Cyclically go long US 10-year Treasuries. Geopolitical risks are historically high and rising but complacency is returning to markets. Meanwhile inflation is nearing a cyclical peak. Favor US stocks over global. It is too soon to go long euro or European assets, especially emerging Europe. Favor UK equities over developed markets (excluding the US). Stay long GBP-CZK. Favor European defense stocks over European tech. Stay short the Chinese renminbi and Taiwanese dollar. Favor the Japanese yen over the Korean won. Favor South Korean over Taiwanese equities. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Jesse Anak Kuri Associate Editor Jesse.Kuri@bcaresearch.com Yushu Ma Research Analyst yushu.ma@bcaresearch.com Guy Russell Senior Analyst GuyR@bcaresearch.com Alice Brocheux Research Associate alice.brocheux@bcaresearch.com Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Regional Geopolitical Risk Matrix Section III: Geopolitical Calendar

Highlights Three distinct forces are likely to make South Asia’s geopolitical risks increasingly relevant to global investors. First, India’s tensions with China stem from China’s growing foreign policy assertiveness and India’s shift away from traditional neutrality toward aligning with the US and its allies. This creates a security dilemma in South Asia, just as in East Asia. Second, India’s economy is sputtering in the wake of the COVID-19 pandemic, adding fuel to nationalism and populism in advance of a series of important elections. India will stimulate the economy but it could also become more reactive on the international scene. Third, the US is withdrawing from Afghanistan and negotiating a deal with Iran in an effort to reduce the US military presence in the Middle East and South Asia. This will create a scramble for influence across both regions and a power vacuum in Afghanistan that is highly likely to yield negative surprises for India and its neighbors. Traditionally geopolitical risks in South Asia have a limited impact on markets. India’s growth slowdown and forthcoming fiscal stimulus are more relevant for investors. However, a sharp rise in geopolitical risk would undermine India’s structural advantages as the West diversifies away from China. Stay short Indian banks. Feature Geopolitical risks in South Asia are slowly but surely rising. India-Pakistan and China-India are well-known “conflict-dyads” or pairings. Historically, these two sets have been fighting each other over their fuzzy Himalayan border with limited global financial market consequences. But now fundamental changes are afoot that are altering the geopolitical setting in the region. Specifically, the coming together of three distinct forces could trigger a significant geopolitical event in South Asia. The three forces are as follow: Force #1: Sino-Indian Tensions Get Real About a year ago, Indian and Chinese troops clashed in Ladakh, a disputed territory in the Kashmir region. Following these clashes China reduced its military presence in the Pangong Tso area but its presence in some neighboring areas remains meaningful. Besides the troop build-up along India’s eastern border, China is building more air combat infrastructure in its India-facing western theatre. China’s major air bases have historically been concentrated in China’s eastern region, away from the Indian border (Map 1). Consequently, India has historically enjoyed an advantage in airpower. But China appears to be working to mitigate this disadvantage. Map 1Most Of China’s Major Aviation Units Are Located Away From India Owing to China’s increased military focus along the Sino-India border, India’s threat perception of China has undergone a fundamental change in recent years. Notably, India has diverted some of its key army units away from its western Indo-Pak border towards its eastern border with China. India could now have nearly 200,000 troops deployed along its border with China, which would mark a 40% increase from last year.1 Turning attention to the Indo-Pak border, India’s problems with Pakistan appear under control for now. This is owing to the ceasefire agreement that was renewed by the two countries in February 2021. However, this peace cannot possibly be expected to last. This is mainly because core problems between the two countries (like Pakistan’s support of militant proxies and India’s control over Kashmir) remain unaddressed. History too suggests that bouts of peace between the two warring neighbors rarely last long. These bouts usually end abruptly when a terrorist attack takes place in India. With both political turbulence and economic distress in Pakistan rising, the fragile ceasefire between India and Pakistan could be upended over the next six months. In fact, two events over the last week point to the fragility of the ceasefire: Two drones carrying explosives entered an Indian air force station located in Jammu and Kashmir (i.e. a northern territory that India recently reorganized, to Pakistan’s chagrin). Even as no casualties were reported, this attack marks a turning point for terrorist activity in India as this was the first-time terrorists used drones to enter an Indian military base. Hours later, another drone attack struck an Indian base at the Ratnuchak-Kaluchak army station, the site of a major terrorist attack in 2002. Chart 1China, Pakistan And India Cumulatively Added 41 Nuclear Warheads Over 2020 Given that the ceasefire was agreed recently, any further increase in terrorist activity in India over the next six months would suggest that a more substantial breakdown in relations is nigh. Distinct from these recent tensions, China’s troop deployment along India’s eastern arm and Pakistan’s presence along India’s western arm creates a strategic “pincer” that increasingly threatens India. India is naturally concerned. China and Pakistan are allies who have been working closely on projects including the strategic China-Pakistan Economic Corridor (CPEC). The CPEC is a collection of infrastructure projects in Pakistan that includes the development of a port in Gwadar where a future presence of the People's Liberation Army Navy (PLAN) is envisaged. Gwadar has the potential of providing China land-based access to the Indian Ocean. Trust in the South Asian region is clearly running low. Distinct from troop build-ups and drone-attacks, China, Pakistan, and India cumulatively added more than 40 nuclear warheads over the last year (Chart 1). China is reputed to be engaged in an even larger increase in its nuclear arsenal than the data show.2 From a structural perspective, too, geopolitical risks in the South Asian peninsula are bound to keep rising. When it comes to the conflicting Indo-Pak dyad, India’s geopolitical power has been rising relative to that of Pakistan in the 2000s. However, the geopolitical muscle of the Sino-Pak alliance is much greater than that of India on a standalone basis (Chart 2). Chart 2India Has Aligned With The QUAD To Counter The Sino-Pak Alliance China’s active involvement in South Asia is responsible for driving India’s increasing desire to abandon its historical foreign policy stance of non-alignment. India’s membership in the Quadrilateral Security Dialogue (also known as the QUAD, whose other members include the US, Japan, and Australia) bears testimony to India’s active effort to develop closer relations with the US and its allies (Chart 2). India’s alignment with the US is deepening China’s and Pakistan’s distrust of India. Conventional and nuclear military deterrence should prevent full-scale war. But the regional balance is increasingly fluid which means geopolitical risks will slowly but surely rise in South Asia over the coming year and years. Force #2: A Growth Slowdown Alongside India’s Loaded Election Calendar The pandemic has hit the economies of South Asia particularly hard. South Asia historically maintained higher real GDP growth rates relative to Emerging Markets (EMs). But in 2021, this region’s growth rate is set to be lower than that of EM peers (Chart 3). History is replete with examples of a rise in economic distress triggering geopolitical events. South Asia is characterized by unusually low per capita incomes (Chart 4) and the latest slowdown could exacerbate the risk of both social unrest and geopolitical incidents materialising. Chart 3South Asian Economies Have Been Hit Hard By The Pandemic Chart 4South Asia Is Characterized By Very Low Per Capita Incomes To complicate matters a busy state elections calendar is coming up in India. Elections will be due in seven Indian states in 2022. These states account for about 25% of India’s population. State elections due in 2022 will amount to a high-stakes political battle. During state elections in 2021, the ruling Bharatiya Janata Party (BJP) was the incumbent in only one of the five states. In 2022, the BJP is the incumbent party in most of the states that are due for elections, which means it has the advantage but also has a lot to lose, especially in a post-pandemic environment. Elections kick off in the crucial state of Uttar Pradesh next February. Last time this state faced elections Prime Minister Narendra Modi was willing to go to great lengths to boost his popularity ahead of time. Specifically, he upset the nation with a large-scale and unprecedented de-monetization program. Given the busy state election calendar in 2022, we expect the BJP-led central government to focus on policy actions that can improve its support among Indian voters. Two policies in particular are likely to come through: Fiscal Stimulus Measures To Provide Economic Relief: India has refrained from administering a large post-pandemic stimulus thus far. As per budget estimates, the Indian central government’s total expenditure in FY22 is set to increase only by 1% on a year-on-year basis. But the expenditure-side restraint shown by India’s central government could change. With elections and a pandemic (which has now claimed over 400,000 lives in India), the central government could consider a meaningful increase in spending closer to February 2022. Map 2Northern India Views Pakistan Even More Unfavorably Than Rest Of India India’s Finance Minister already announced a fiscal stimulus package of $85 billion (amounting to 2.8% of GDP) earlier this week. Whilst this stimulus entails limited fresh spending (amounting to about 0.6% of India’s GDP), we would not be surprised if the government follows it up with more spending closer to February 2022. Assertive Foreign Policy To Ward-Off Unfriendly Neighbors: India’s northern states are known to harbor unfavorable views of Pakistan (Map 2). The roots of this phenomenon can be traced to geography and the bloody civil strife of 1947 that was triggered by the partition of British-ruled India into the two independent dominions of India and Pakistan. Given the north’s unfavorable views of Pakistan and given looming elections, Indian policy makers may be forced to adopt a far more aggressive foreign policy response, to any terrorist strikes from Pakistan or territorial incursions by China. This kind of response was observed most recently ahead of the Indian General Elections in April-May 2019. An Indian military convoy was attacked by a suicide-bomber in early February 2019 and a Pakistan-based terrorist group claimed responsibility. A fortnight later the Indian air force launched unexpected airstrikes across the Line of Control which were then followed by the Pakistan air force conducting air strikes in Jammu and Kashmir. While the next round of Pakistani and Indian general elections is not due until 2023 and 2024, respectively, it is worth noting that of the seven state elections due in India in 2022, four are in the north (Uttar Pradesh, Punjab, Uttarakhand, and Himachal Pradesh). Force #3: Power Vacuum In Afghanistan The final reason to be wary of the South Asian geopolitical dynamic is the change in US policy: both the Iran nuclear deal expected in August and the impending withdrawal from Afghanistan in September. The US public has now elected three presidents on the demand that foreign wars be reduced. In the wake of Trump and populism the political establishment is now responding. Therefore Biden will ultimately implement both the Iran deal and the Afghan withdrawal regardless of delays or hang-ups. But then he will have to do damage control. In the case of Iran, a last-minute flare-up of conflict in the region is likely this summer, as the US, Israel, Saudi Arabia, and Iran underscore their red lines before the US and Iran settle down to a deal. Indeed it is already happening, with recent US attacks against Iran-backed Shia militias in Syria and Iraq. A major incident would push up oil prices, which is negative for India. But the endgame, an Iranian economic opening, is positive for India, since it imports oil and has had close relations with Iran historically. In the case of Afghanistan, the US exit will activate latent terrorist forces. It will also create a scramble for influence over this landlocked country that could lead to negative surprises across the region. The first principle of the peace agreement between the US and Afghanistan states that the latter will make all efforts to ensure that Afghan soil is not used to further terrorist activity. However, the enforceability of such a guarantee is next to impossible. Notably, the US withdrawal from Afghanistan will revive the Taliban’s influence in the region. This poses major risks for India, which has a long history of being targeted by Afghani terrorist groups. The Taliban played a critical role in the release of terrorists into Pakistan following the hijacking of an Indian Airlines flight in 1999. Furthermore, the Haqqani network, which has pledged allegiance to the Taliban, has attacked Indian assets in the past. Any attack on India deriving from the power vacuum in Afghanistan would upset the precarious regional balance. Whilst there are no immediate triggers for Afghani groups to launch a terrorist attack in India, the US withdrawal will trigger a tectonic shift in the region. Negative surprises emanating from Afghanistan should be expected. Investment Conclusions Chart 5Indian Banks Appear To Have Factored In All Positives We reiterate the need to pare exposure to Indian assets on a tactical basis. India’s growth engine is likely to misfire over the second half of the Indian financial year. Macroeconomic headwinds pose the chief risk for investors, but major geopolitical changes could act as a negative catalyst in the current context. So we urge clients to stay short Indian Banks (Chart 5). Financials account for the lion’s share of India’s benchmark index (26% weight). India could opt for an unexpected expansion in its fiscal deficit soon. Whilst we continue to watch fiscal dynamics closely, we expect the fiscal expansion to materialize closer to February 2022 when India’s most populous state (i.e. Uttar Pradesh) will undergo elections. Over the long run, India’s sense of insecurity will escalate in the context of a more assertive China, stronger Sino-Pakistani ties, and a power vacuum in Afghanistan. For that reason, New Delhi will continue to shed its neutrality and improve relations with the US-led coalition of democratic countries, with an aim to balance China. This process will feed China’s insecurity of being surrounded and contained by a hegemonic American system. This security dilemma is a source of South Asian geopolitical risk that will become more globally relevant over time. China’s conflict with the US and western world should create incentives for India to attract trade and investment. However, its ability to do so will be contingent upon domestic political factors and regional geopolitical factors. Ritika Mankar, CFA Editor/Strategist ritika.mankar@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Sudhi Ranjan Sen, ‘India Shifts 50,000 Troops to China Border in Historic Move’, Bloomberg, June 28, 2021, bloomberg.com. 2 Joby Warrick, “China is building more than 100 missile silos in its western desert, analysts say,” Washington Post, June 30, 2021, washingtonpost.com.