Persian (Gulf)

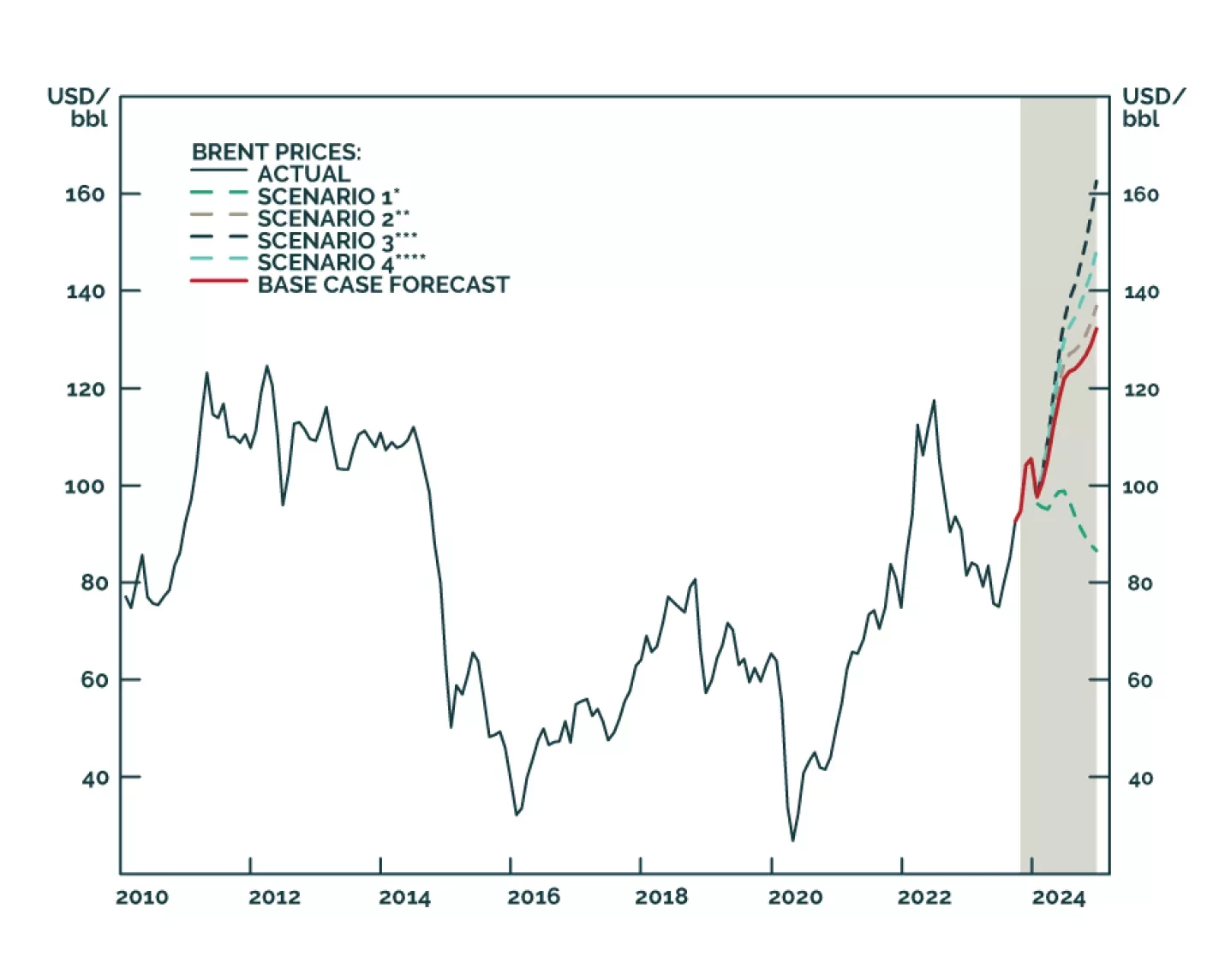

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

The Israeli-Arab crisis is more likely to expand and cause oil disruptions than market consensus holds. Close long dollar trades and go long energy and defense stocks relative to cyclicals.

Hamas’s attack on Israel raises the odds of a wider conflict in the Gulf, which would lead to higher oil prices. Given the response of oil prices Monday, markets appear to be relatively restrained in their assessment of a sharp escalation in prices. However, this is early days in a strategy that is just revealing itself.

Volatility will remain the key dynamic in oil markets in the aftermath of the surprise Hamas attacks against Israel on October 7. The risk of a major oil supply shock has gone up, but meanwhile supply constraints will remain at variance with global growth problems stemming from restrictive monetary policy over the next 12 months. Favor bonds over stocks, large caps over small caps, defense and energy stocks over other cyclicals, and US equities relative to global equities.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

Investors should underweight global equities and risk assets; overweight US stocks relative to global; and overweight defensive sectors versus cyclicals.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.

China’s economic and diplomatic interests in the GCC region will expand, as will its military presence. Whether or not this stabilizes the region is yet to be determined, particularly if tensions in the South China Sea and other international waters traversed by both the US and China escalate. Underlying risk in energy markets will remain elevated. We remain bullish energy generally, and continue to favor equity ETF exposure to energy (XOP and XME), and commodity exposure via the COMT ETF.