Policy

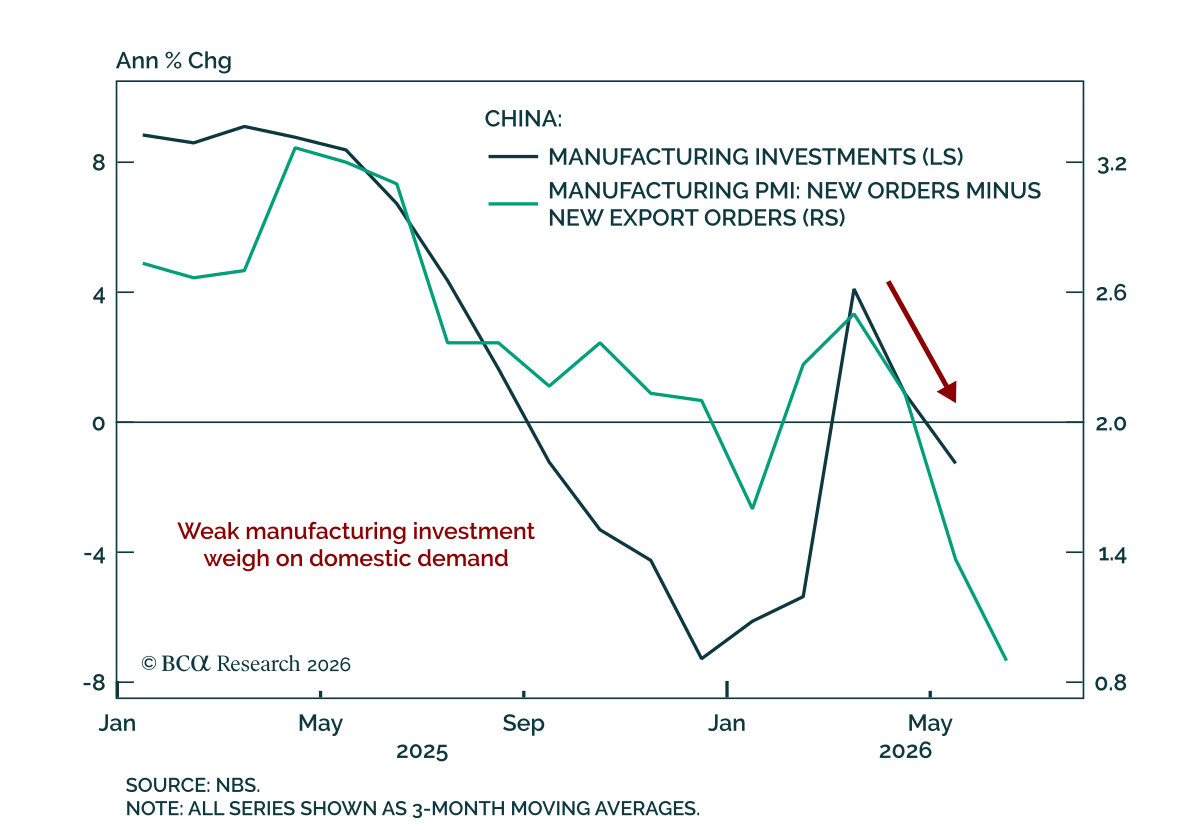

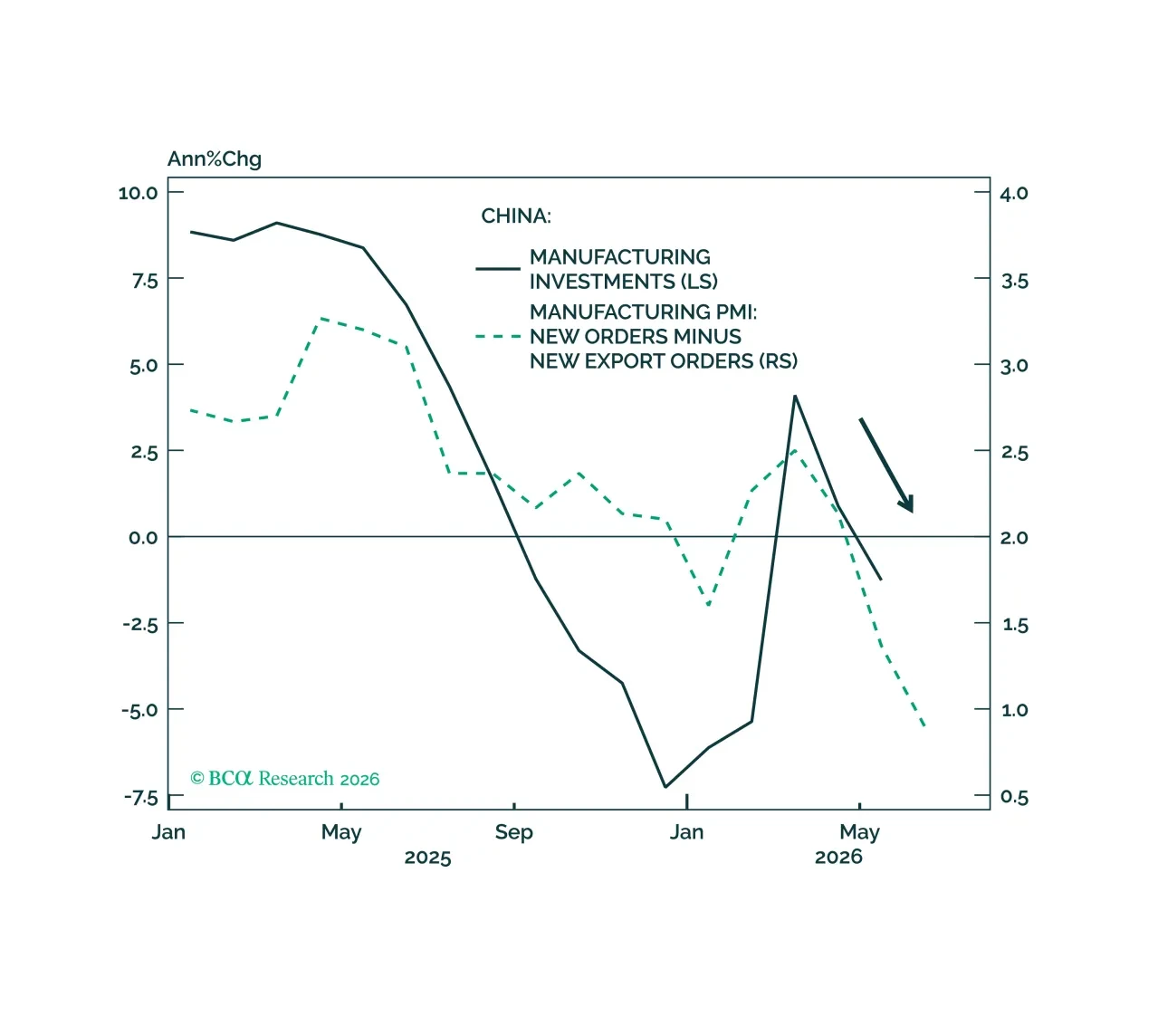

The rebound in China's producer prices and profits this year owes more to external demand than to meaningful progress under Beijing's anti-involution campaign.

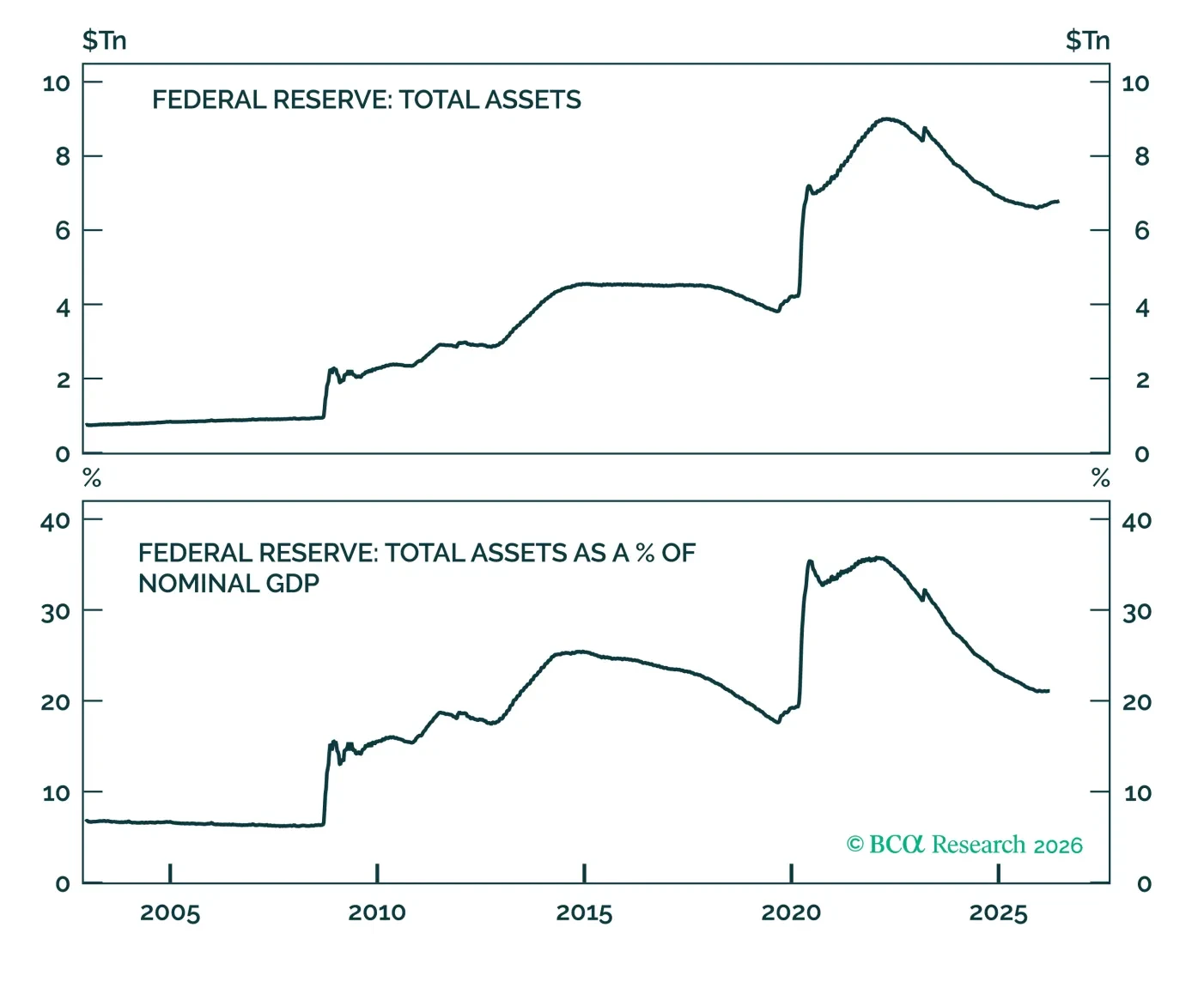

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.

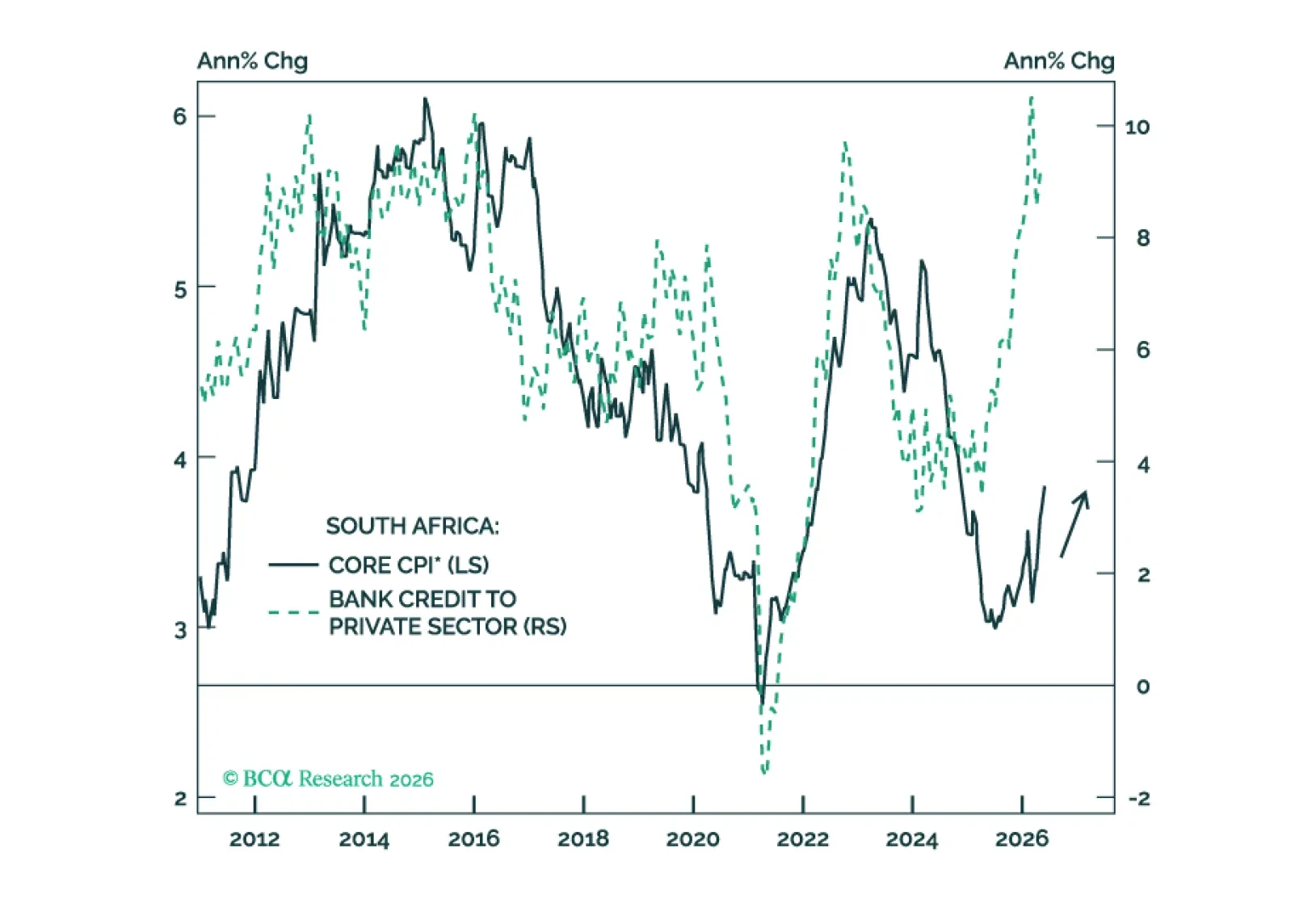

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

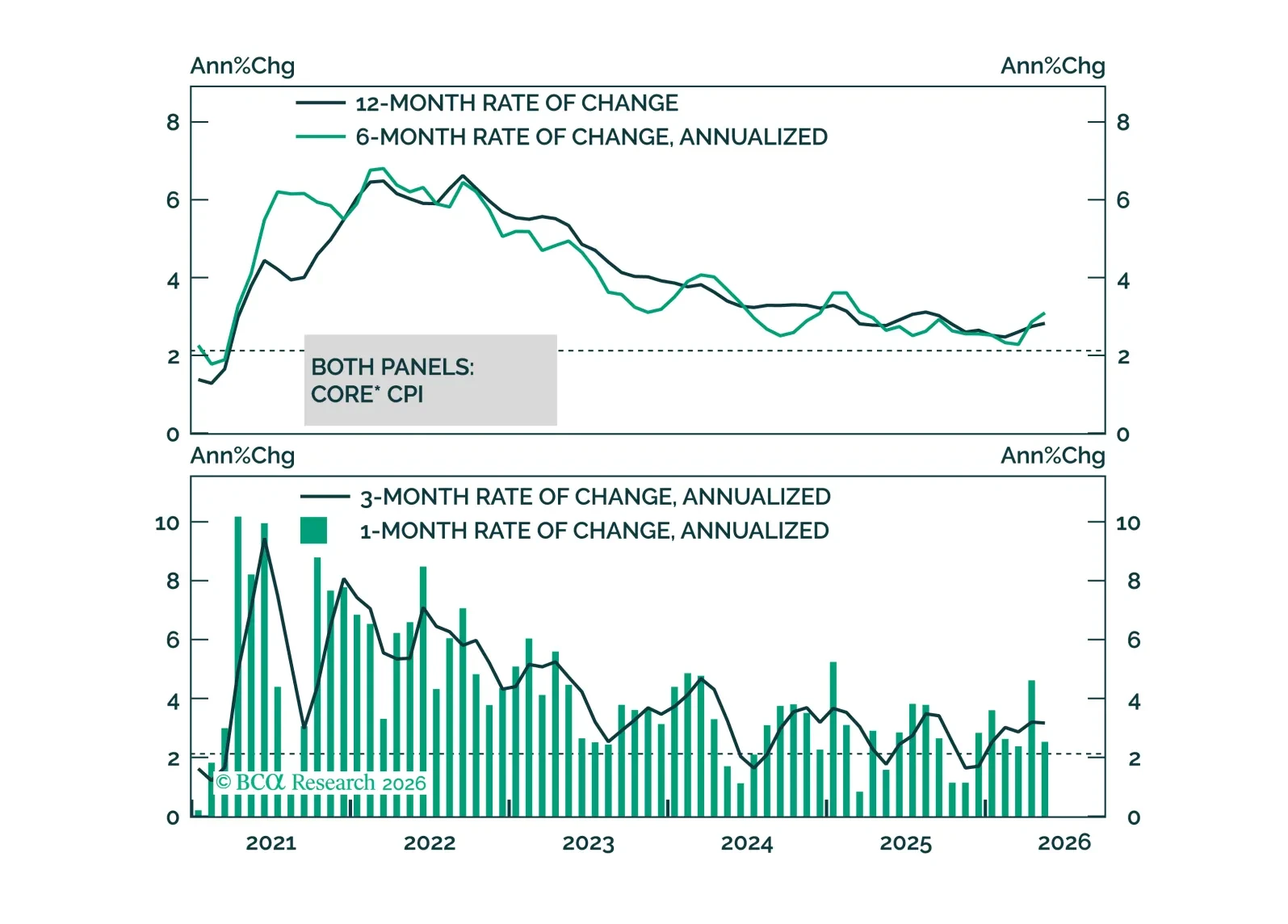

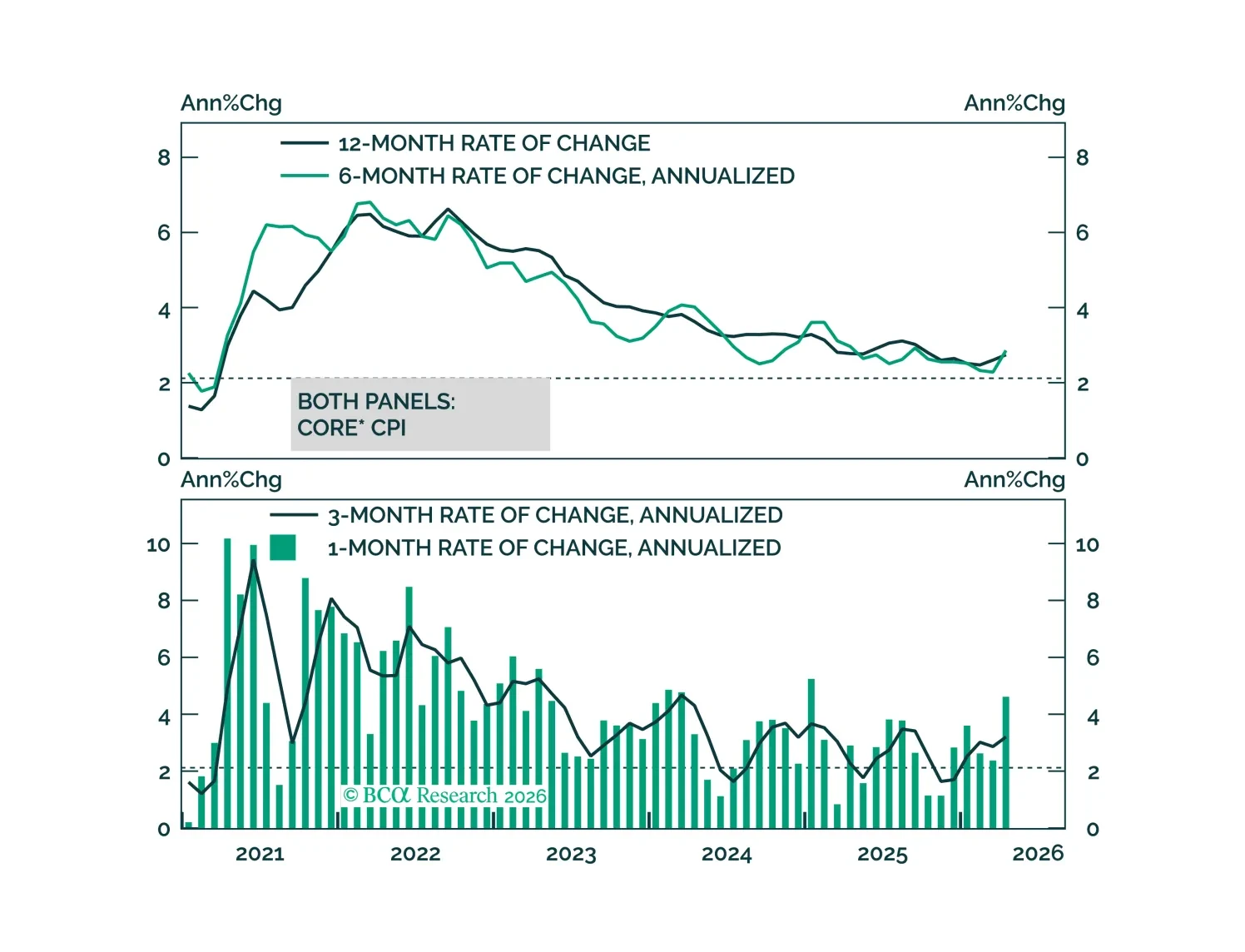

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

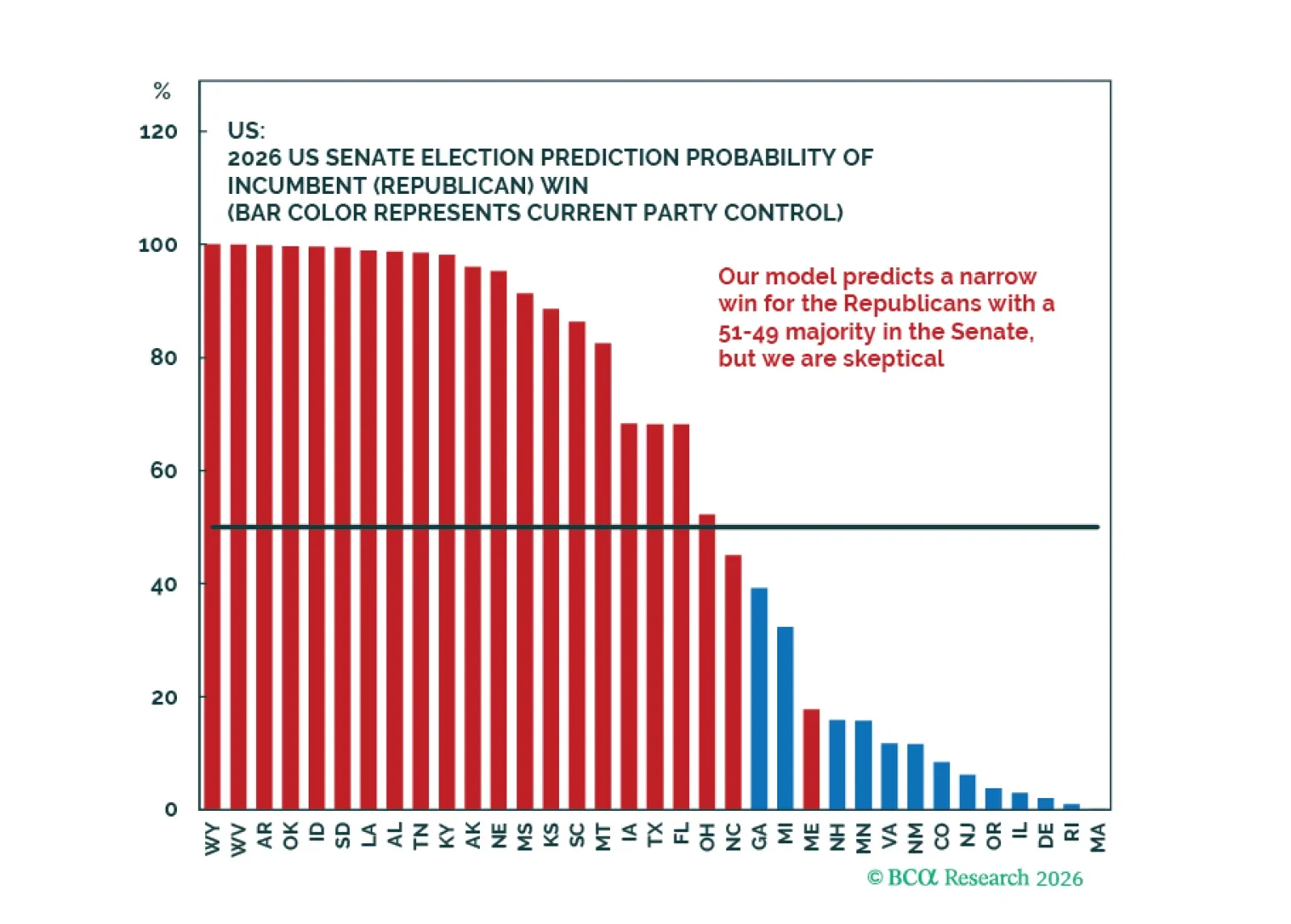

Midterms matter but geopolitics are the main risk this year. Markets will eventually refocus on geopolitical and inflation risks, raising Fed rate hike odds and supporting US dollar and stocks over global counterparts this year.

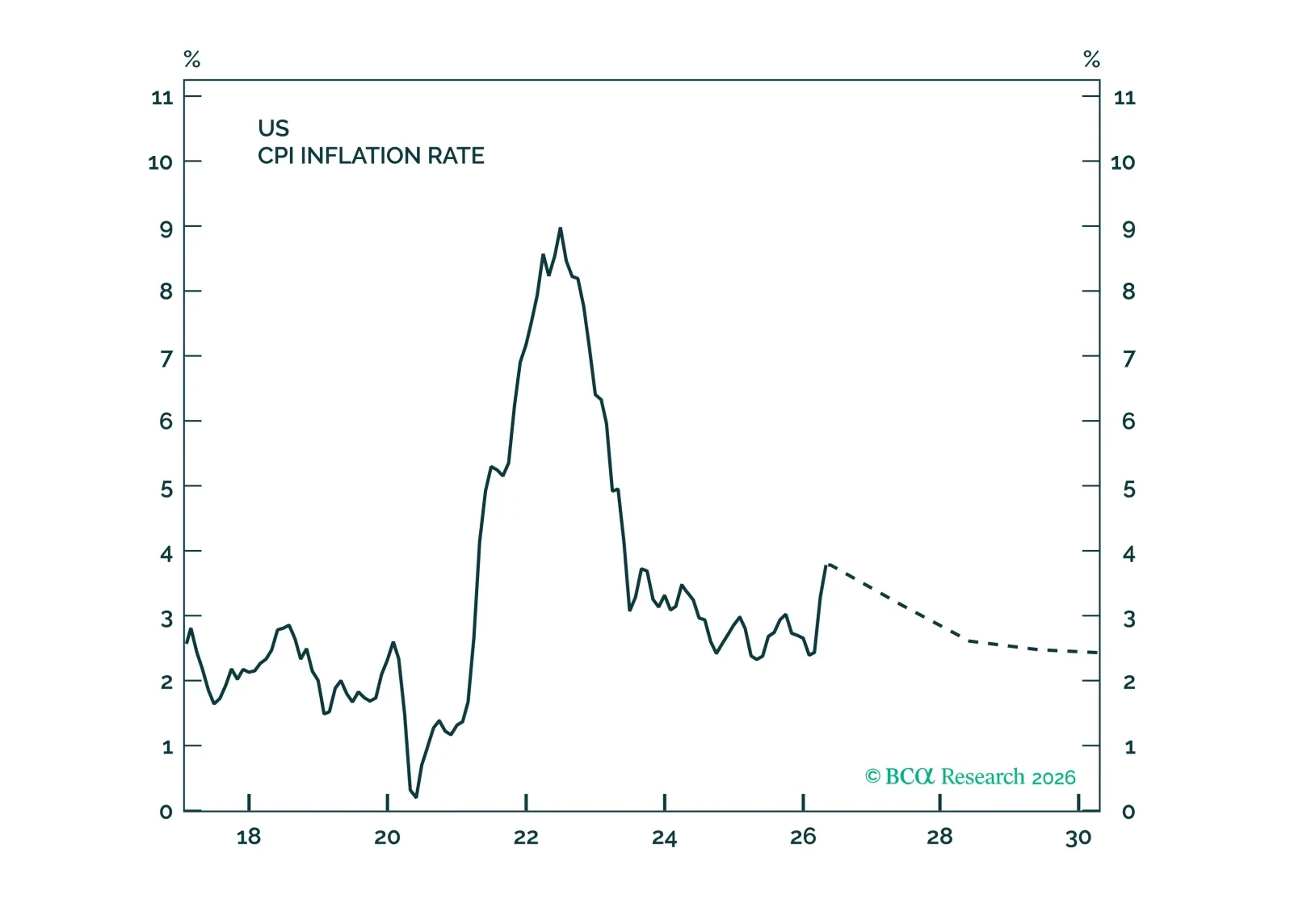

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

Our Portfolio Allocation Summary for June 2026.

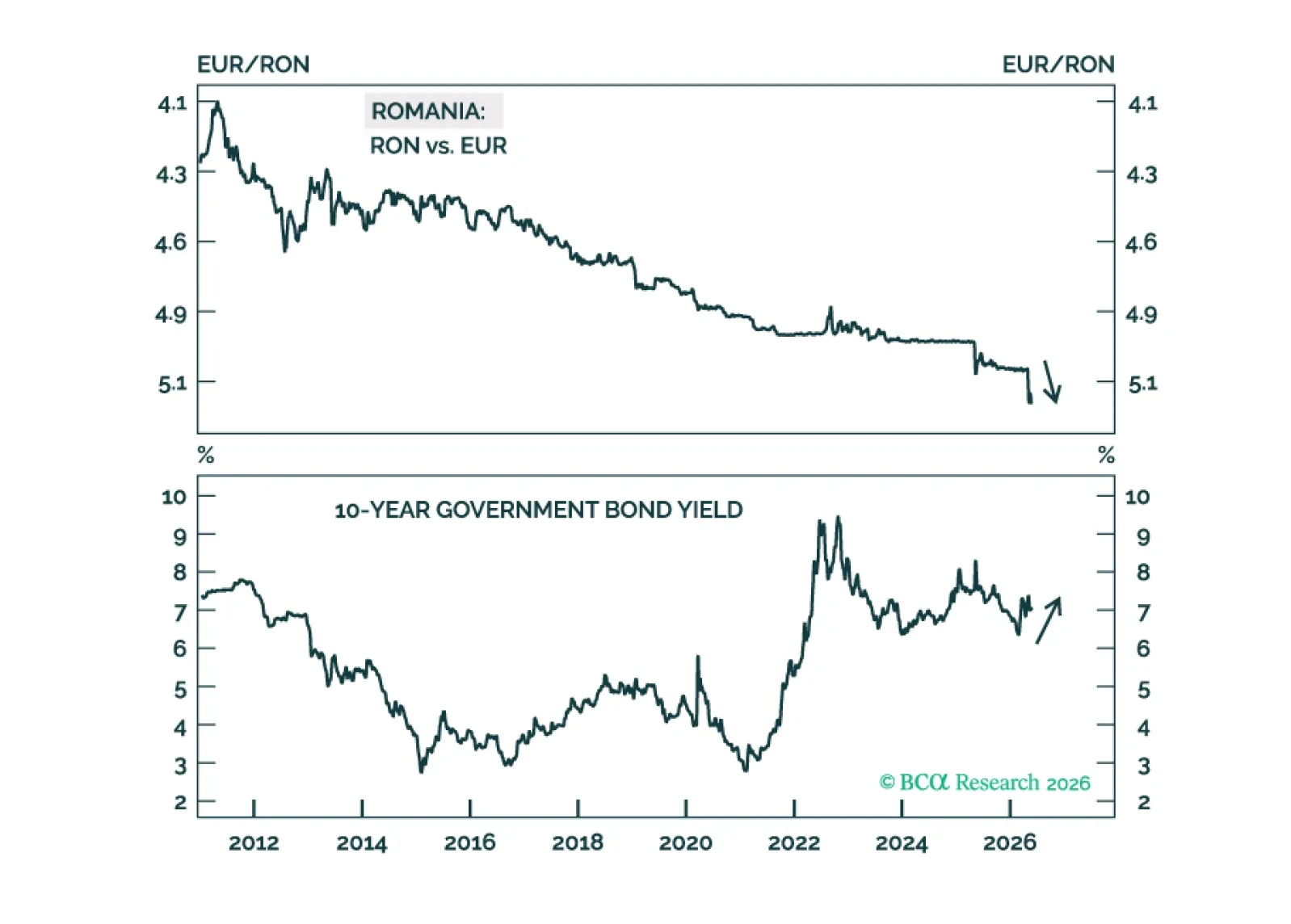

In Romania, large fiscal and current account deficits, high inflation, negative real rates, an overvalued exchange rate, and deteriorating growth point to budding currency devaluation. Investors should short the Romanian currency versus the euro and underweight Romanian local bonds, equities, and sovereign credit.

The April CPI report showed clear evidence of the direct effect of higher oil prices on inflation but, so far, limited evidence of passthrough to core.