Policy

Our Portfolio Allocation Summary for December 2023.

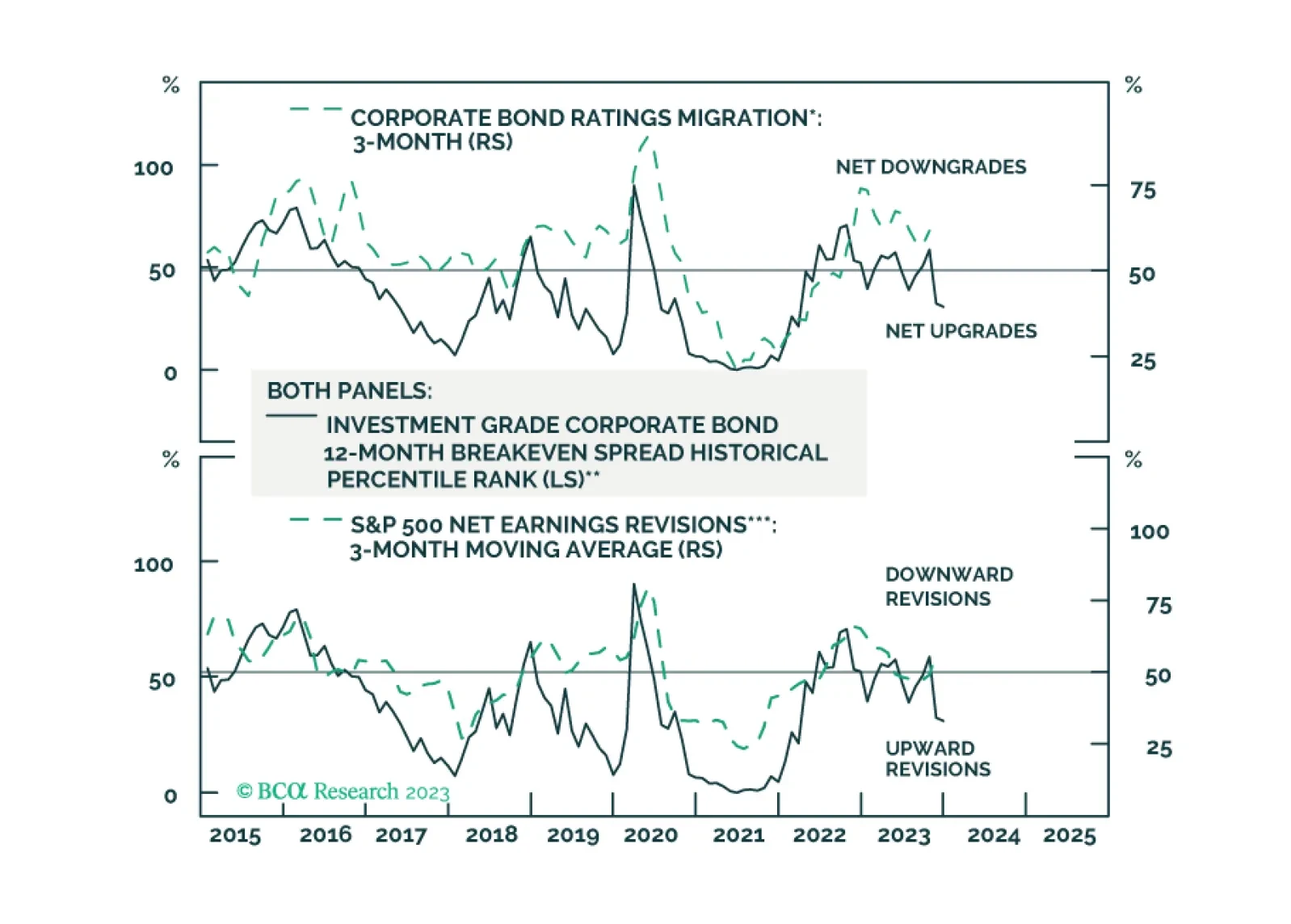

We enter 2024 as we were across the last four months of 2023, tactically equal weight across the board until the S&P 500 rally is complete and we gain a better entry point for underweighting equities and overweighting fixed income.

Treasury yields will sketch out a range between now and Q1 2024, with the upside determined by inflation and the downside determined by labor markets.

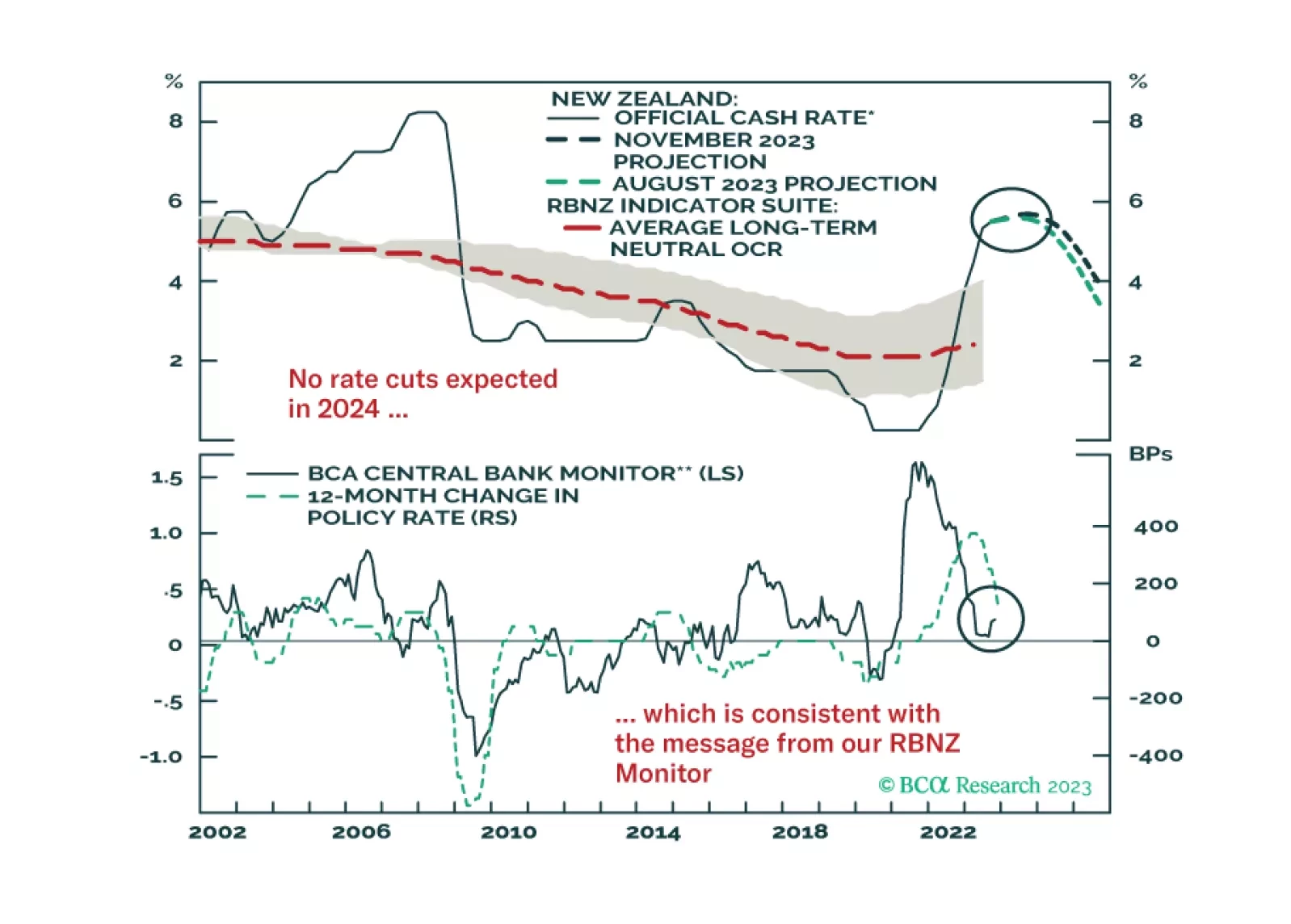

In this Insight, we discuss the outlook for monetary policy in New Zealand after this week’s RBNZ policy meeting, and introduce related fixed income and currency trade ideas.

Q3 US real GDP was revised higher in the second estimate that was released on Wednesday. The 5.2% q/q annualized increase beat expectations of a more muted upwards revision to 5.0% q/q from the advance estimate of 4.9% q/q. In particular, updates to…

Recent Euro Area economic data have been sending a less pessimistic signal. Wednesday’s releases are in line with this trend. The European Commission’s confidence indicator shows a mild improvement in economic sentiment in November – confirming the recent…

The Reserve Bank of New Zealand (RBNZ) held its key interest rate steady at 5.5% at the November policy meeting yesterday. That decision was as expected, but the messaging surrounding the announcement was surprisingly hawkish. The RBNZ statement…

According to BCA Research’s Bank Credit Analyst service, events that have occurred since the onset of the pandemic have highlighted that the easy money era that prevailed from 2009-2021 is very likely over. The Fed will cut interest rates meaningfully…

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

After widening since mid-year, the spread between German bunds and Italian BTPs has been narrowing over the past month. What is driving this move? Our Chief Global Fixed Income Strategist highlighted in Tuesday's BCA Live & Unfiltered livestream that both…