Policy

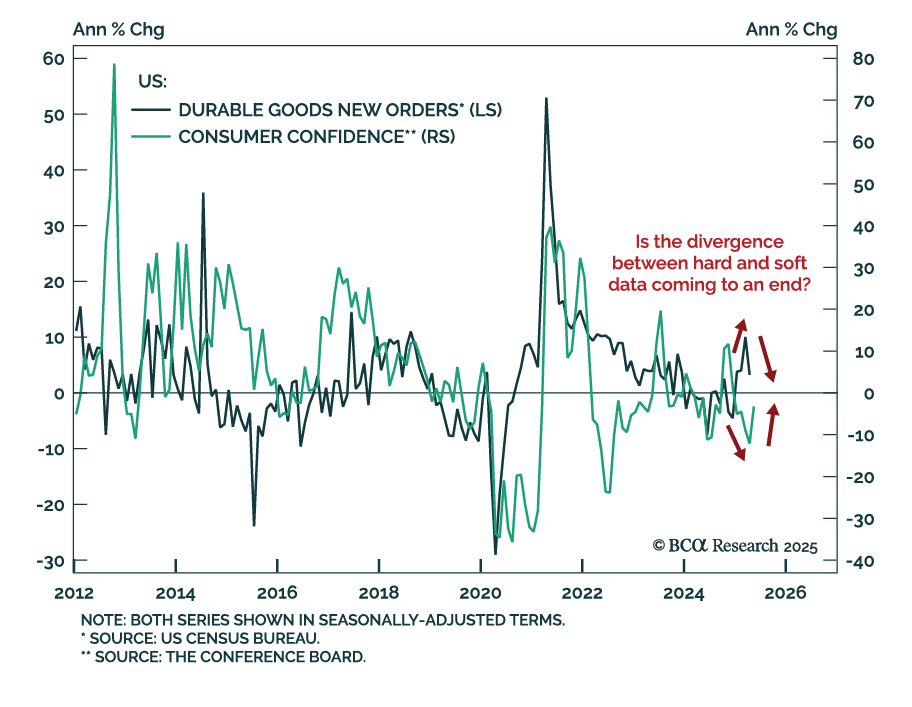

The latest US durable goods orders and consumer confidence figures suggest that hard and soft data are converging, but stocks remain at risk. After months of rising prints, new orders for manufactured goods sank by 6.3% in April compared to the previous…

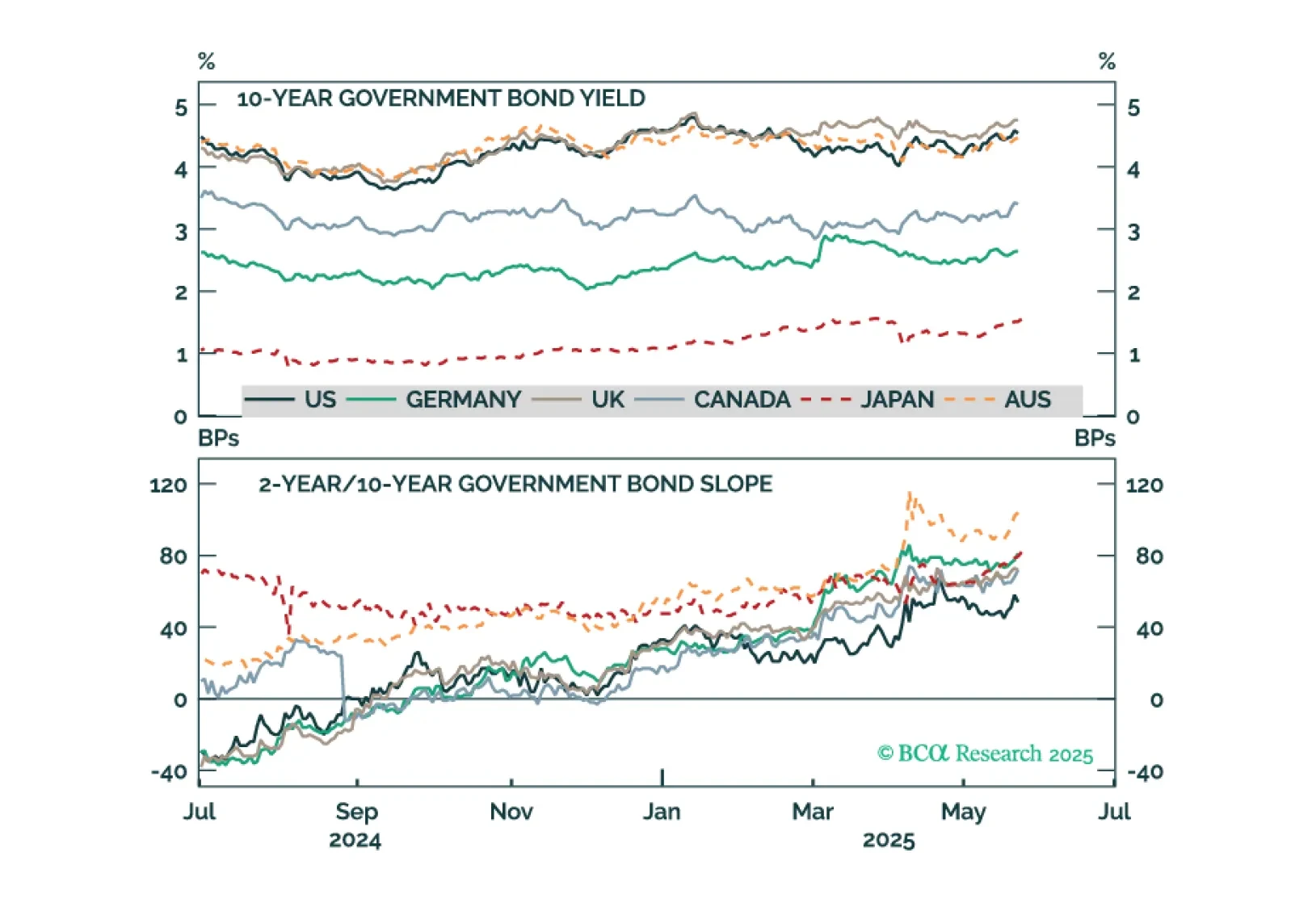

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.

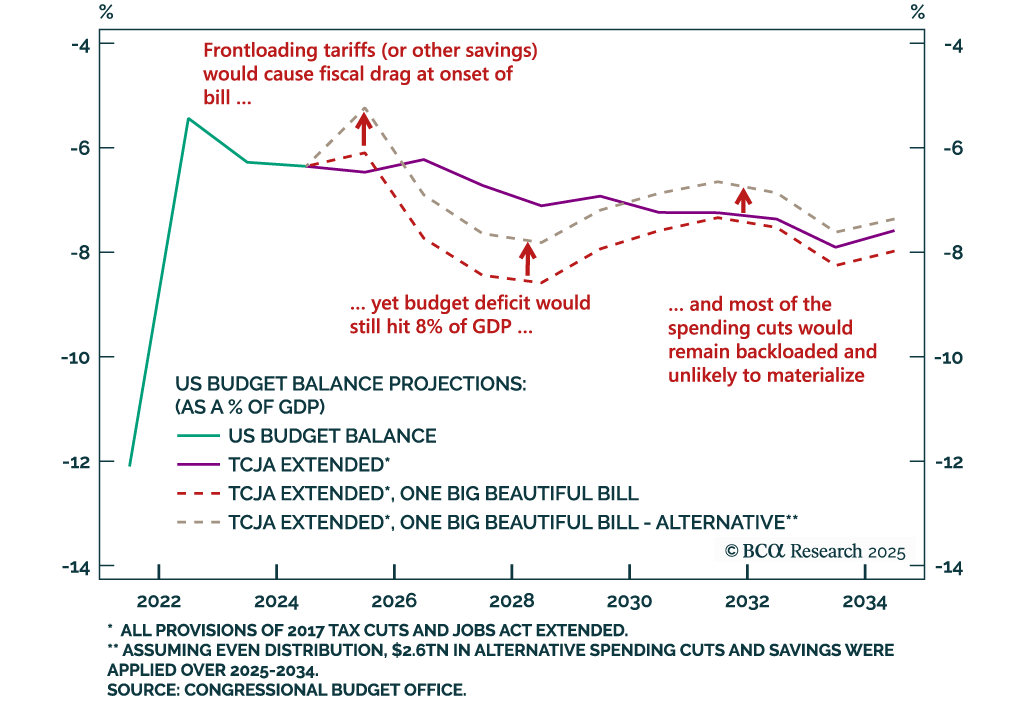

President Trump’s signature bill is surprising to the upside with budget deficits, as predicted by our Geopolitical Strategists. Some form of the bill is guaranteed to pass, no matter how many tries it takes. The bill will cut taxes more than…

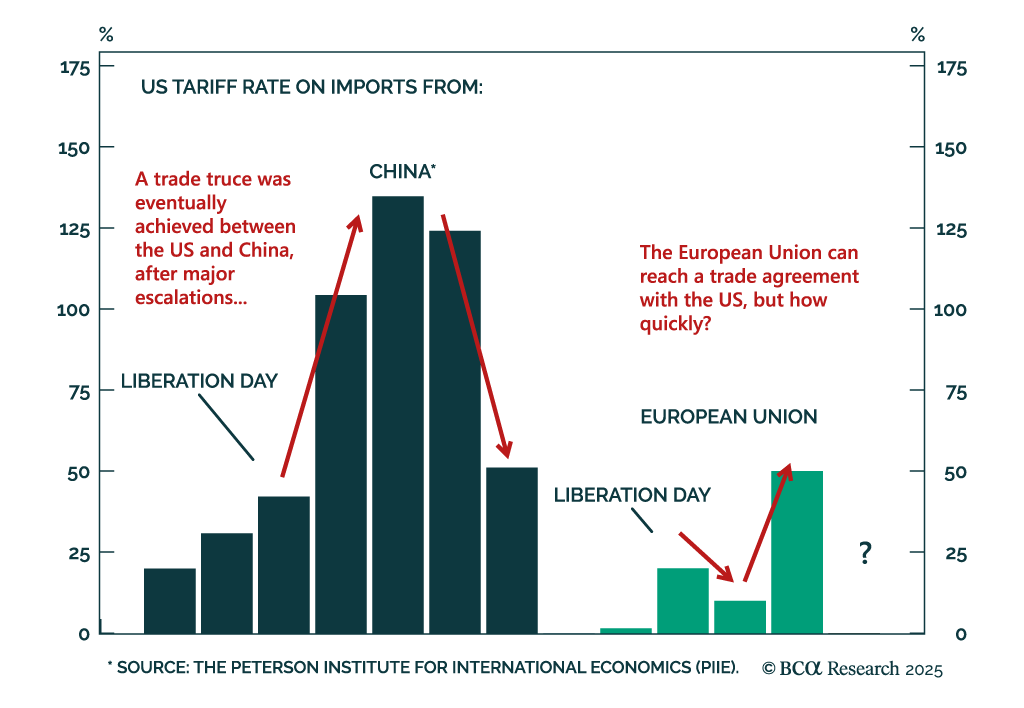

Last Friday, President Trump announced new 50% tariffs on imported goods from the European Union (EU), effective June 1st, and threatened US company Apple with 25% tariffs unless it made iPhones in the US. Global stock markets reacted negatively to the news,…

UK inflation surprised to the upside in April. Headline inflation rose to a 15-month high of 3.5%, from 2.6% the month before. Core inflation also surprised above estimates, printing 3.8% vs. 3.4% in March. Services inflation climbed to 5.4% from 4.7%. Higher…

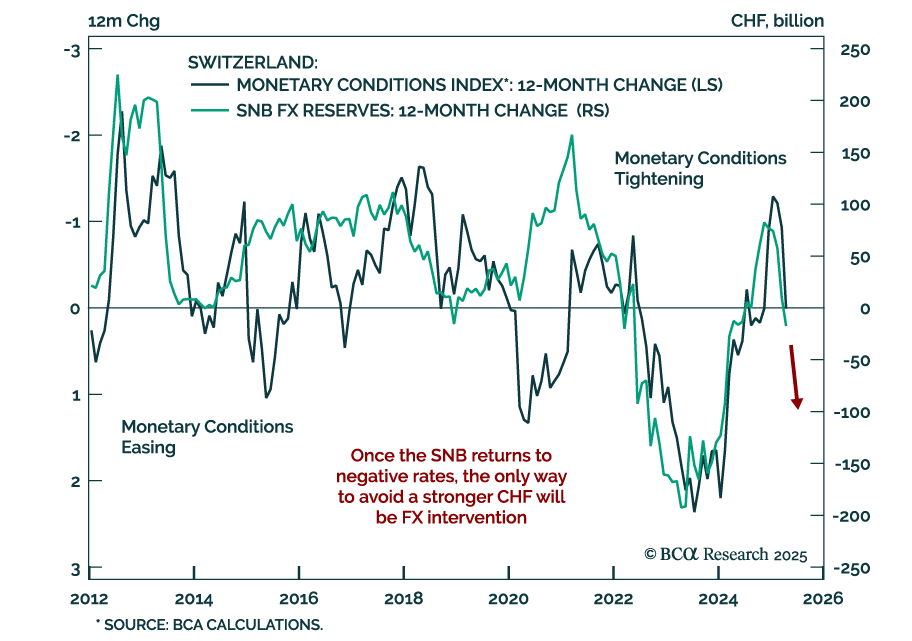

Swiss National Bank will have to resort to negative interest rates and FX intervention before year-end. Swiss inflation fell to 0% year-over-year in April, or the lower end of the SNB’s 0%-2% target range, and the continued strength in the Swiss Franc…

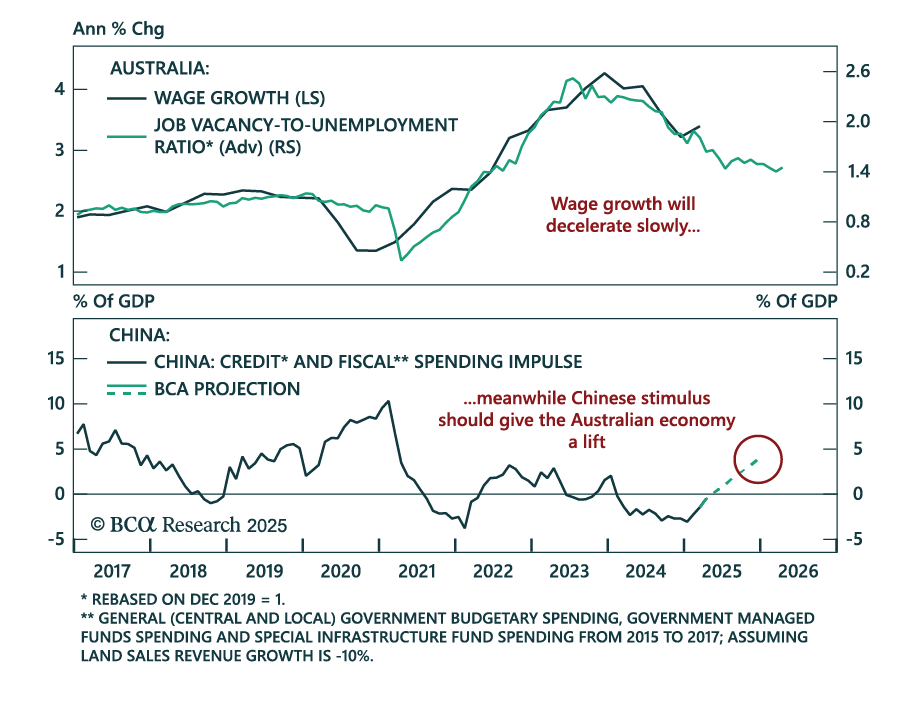

Overnight, the Reserve Bank of Australia (RBA) cut the cash rate target by 25bps to 3.85%, as widely expected. After this cut, the market still prices in about 50bps of easing over the next six months. According to our Global Fixed-Income strategists,…

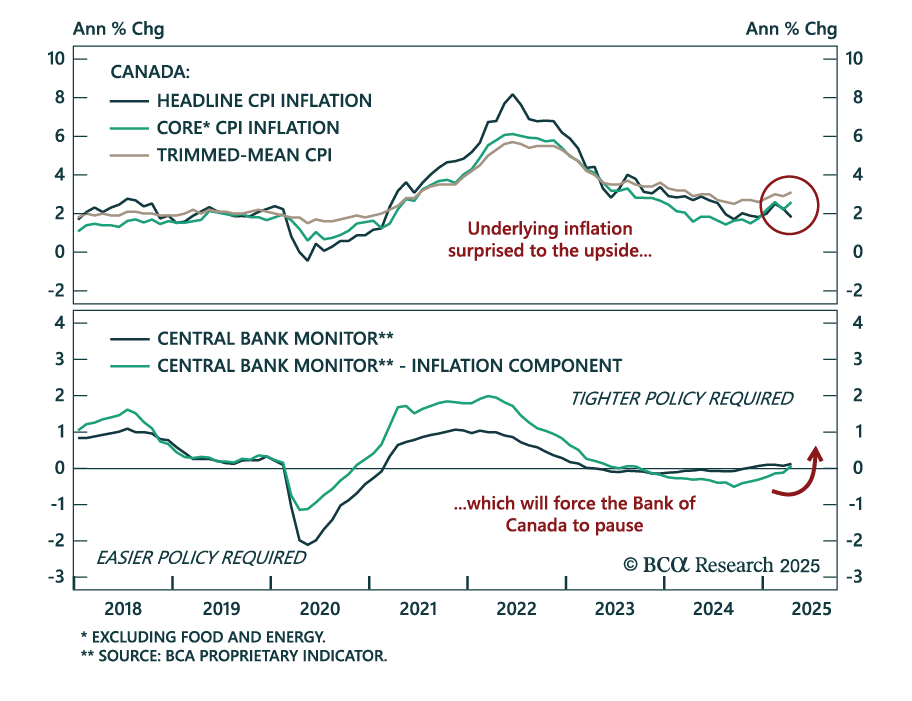

Although Canada’s headline CPI slowed to 1.7% y/y from 2.3% on Tuesday, most measures of underlying inflation surprised to the upside, thus raising the likelihood that the Bank of Canada (BoC) will stay put at its next meeting in three weeks. The…

Our European strategists are upgrading the communication services sector to overweight on a structural investment horizon. In March, they highlighted the sector's near-term attractiveness. Since the Great Financial Crisis, the European telecom…

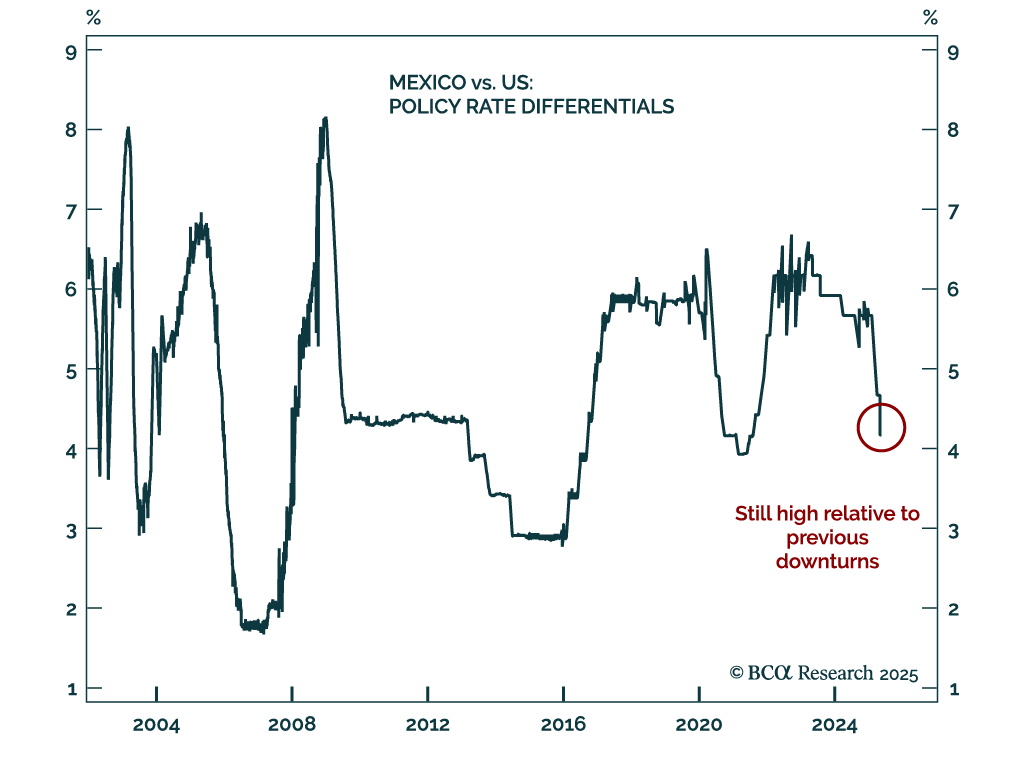

Banxico’s 50 bps rate cut reinforces our bullish view on Mexican bonds, with easing likely to continue as inflation falls and growth slows. The central bank unanimously lowered its policy rate to 8.5%, and we expect further cuts ahead as Mexico heads toward a…