Policy

Highlights The helicopter drops are over, … : The economic impact payments and supplemental unemployment insurance benefits may have stopped, but their full impact has yet to be felt. … but fiscal and monetary policy will continue to support demand, … : US households are sitting on more than $2 trillion of excess pandemic savings. If they were to spend just half of their stash over the next two or three years, the economy would gain a steady tailwind. … and the macro backdrop will remain equity-friendly, … : Monetary policy will be less accommodative going forward but it will remain solidly supportive of markets and the economy across all of 2022. … so investors should stick around for one last round: Equities and spread product outperform when monetary policy is easy. As long as COVID-19 doesn’t spring a nasty surprise, the expansion will continue and risk assets will once again generate positive excess returns over Treasuries and cash. Feature BCA editors’ annual sit-down with Mr. and Ms. X provides a welcome opportunity to gather our thoughts for the coming year and review how this year’s calls panned out. Looking back to this time last year,1 our risk-friendly recommendations performed well as the rationale behind them proved to be sound. Financial markets thrived in the wake of monetary and fiscal policy measures intended to err on the side of providing too much accommodation. The policy efforts were massive, and their support for markets and the economy has yet to be fully exhausted; indeed, their lengthy half-life is a key pillar of our sanguine 2022 outlook. Unlike last December, investors cannot look forward to peak accommodation in the year ahead; the peak is behind us and monetary and fiscal stimulus will be throttled back. The Fed is currently deliberating how much to accelerate its taper timetable, with an eye toward gaining the flexibility to hike rates sooner than previously planned. The hawkish turn foreshadowed by Chair Powell two weeks ago in Congressional testimony unsettled markets somewhat, but it is important to note that monetary policy settings are merely on track to become less accommodative – they are nowhere near crossing the line to restrictive and will not approach it anytime soon. Investors can be certain that markets will enjoy ample policy support across all of 2022 and we expect that equities will still be in a bull market when Mr. and Ms. X return to discuss the outlook for 2023. We are on board with the BCA consensus as detailed in the Bank Credit Analyst’s 2022 outlook.2 Early indications suggest that the Omicron variant will not be enough of a threat to provoke a negative growth surprise and we expect that the pandemic will recede in importance as the year unfolds. As it fades, supply chains should become less snarled, easing the near-term pressures that have been pushing prices higher. We expect that markets are overestimating inflation in the near term and that growth will be robust in the US and other developed economies. Despite the dialing back of some accommodation, monetary policy will remain easy, supporting economic activity and market valuations. We foresee another year of solidly positive excess returns for risk assets. The Economy Is Firing On All Cylinders You wouldn’t necessarily know it to talk with investors, much less consumer confidence survey respondents, but aggregate demand is surging and ought to remain robust going forward. Households are in fantastic shape. Although their net worth growth slowed in the third quarter, its 13% annualized seven-quarter (1Q20 through 3Q21) pace is within a whisker of all-time highs (Chart 1). They have accumulated $2.3 trillion of excess savings since the pandemic began and have plenty of capacity to borrow to augment their spending power. Just about anyone who wants a job can have one: the ratio of job openings to unemployed workers is making new highs (Chart 2) and the share of people in the labor force filing initial jobless claims is approaching the all-time lows set before the pandemic (Chart 3). Chart 1The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

The Wealth Effect Will Support Consumption

Chart 2More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

More Jobs Than People Without Them ...

Businesses are on a solid financial footing, as well. Debt as a share of net worth is near the lower end of its typical range since the high yield bond market got going in the late ‘80s (Chart 4). Borrowing costs are scraping all-time lows (Chart 5) and profit margins are wide (Chart 6). Banks and fixed income asset managers are falling all over themselves to lend to businesses and will continue to do so while default rates remain low. Chart 3... And Almost No Layoffs

... And Almost No Layoffs

... And Almost No Layoffs

Chart 4Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Corporations Have Less Debt And More Equity, ...

Chart 5... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

... But Debt Has Never Cost Less ...

Chart 6... And Profit Margins Are Wide

... And Profit Margins Are Wide

... And Profit Margins Are Wide

Financial conditions will remain highly accommodative despite the Fed’s and other major developed world central banks’ moves to make them less easy at the margin. Below-equilibrium policy rates will continue to encourage financed purchases of homes, autos and other durable goods and entice investment via low hurdle rates. If sovereign bond yields rise modestly in 2022 in line with our high-conviction base case, governments won’t feel any pressure to tighten the fiscal screws. That may nourish modern monetary theory fantasies to the ultimate detriment of public finances, but it should ensure that all three engines of domestic demand – households, businesses and government – will hum in 2022. Omicron has reminded everyone that the pandemic is not over, but the shadow it casts on public health and economic activity is set to shrink. Booster shots of the Pfizer vaccine apparently provide effective protection, and Omicron’s mutations will not allow it to evade Merck’s and Pfizer’s soon-to-be-approved antiviral pills. The availability of pills to treat those who contract COVID could possibly be a game-changer in terms of neutralizing its global threat. Distributing shelf-stable pills is vastly simpler than delivering vaccines that need to be transported at temperatures below -70 degrees Fahrenheit. The Earnings Bar Has Been Set Very Low Our constructive view would not translate into risk friendly investment strategy if asset prices already discounted it or were expecting something even better. Just as the economy is on a better path than consumers seem to perceive and investors believe can persist, S&P 500 earnings per share are poised to grow over the next four quarters by more than the bottom-up analyst consensus expects. As compared to the simple annualized run rate of last quarter’s earnings ($215.76, or $53.89 times 4), the analyst consensus is calling for effectively no growth ($215.87) over the four quarters through 3Q22. That is a surprising prediction based on two sets of empirical evidence. First, earnings typically rise outside of recessions (Chart 7). Second, analysts have consistently forecast that forward four-quarter earnings would top the run rate of the last reported quarter’s earnings for four decades (Chart 8). This year, though, analysts have repeatedly called for quarter-over-quarter declines in earnings (Table 1), only to have reported numbers shred their estimates by jaw-dropping margins, just as they have in all six full quarters since COVID-19 arrived (Chart 9). We interpret the phase shift in the magnitude of earnings beats as evidence that companies have surprised themselves by how much they’ve been able to increase efficiency and/or cut costs during the pandemic. Our interactions with the investment community suggest that it has also been surprised but views the gains as one-off events that are unlikely to continue. Chart 7Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Earnings Declines Outside Of Recessions Are Rare

Chart 8This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

This Has Been An Odd Time To Expect 40-Year Lows In Earnings Growth

Table 1Grim Expectations

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Expectations of sequentially declining earnings would fit if the economy were flirting with falling below stall speed, as it regularly did during the sluggish post-GFC expansion. But they are completely at odds with the Bloomberg economist consensus that GDP will grow at a 5% real annualized rate this quarter and 3.9% in calendar 2022 (Table 2). Over time, S&P 500 revenue growth should converge with nominal GDP growth, so the current expectations for around 10% and 7% annualized nominal GDP growth in 4Q21 and 2022, respectively, are a decent starting point for estimating S&P 500 revenue growth over those periods. While we expect that S&P 500 profit margins have peaked, we do not foresee a sharp decline in 2022, and operating leverage should ensure that high single-digit revenue growth will translate into healthy earnings gains.

Chart 9

Table 2Above-Trend Growth Ahead

2022 Key Views: Stay For One More Round

2022 Key Views: Stay For One More Round

Bottom Line: The S&P 500 should have no trouble topping consensus estimates that foresee next to no growth in earnings over the next four quarters. There is ample room for corporate earnings to surprise to the upside. Our Major Disagreement With Markets Differences of opinion make markets and our biggest one pertains to the future direction of interest rates. We think the widespread conviction that the Fed will be unwilling or unable to raise the fed funds above 2%, if that, lest it crush financial markets and the real economy is way off base. The majority of investors seem to have taken the decade between the crisis and the pandemic as evidence that rates will remain very low for very long. Many of them must be buying the longer end of the Treasury curve in anticipation that an expedited liftoff date is the first step on the path to the next recession (Chart 10). Chart 10The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The Bond Market Sees Ice, Not Fire

The risk asset selloff that ensued in December 2018 after the FOMC marched the fed funds rate up to 2.5% looms large in the markets’ minds and feeds the widespread view that an ambitious program of rate hikes will pull the rug out from under financial assets and the economy. Many investors have also been conditioned by the post-crisis decade to assume that inflation cannot exceed 2% for a sustained period. The market view is rooted in honest-to-goodness evidence, but we think it is of little relevance now, given the way the massive pandemic fiscal stimulus programs have altered the backdrop. In the space of thirteen months from March 2020 through March 2021, Congress passed bills injecting over $5 trillion of aid – 25% of a year’s GDP – into the economy. The Herculean effort contrasted sharply with the skittish disbursement of less than 5% of GDP on the Bush and Obama administrations’ watch from 2008 through 2010. The aftermath of the crisis demonstrated that even multiple rounds of QE do not by themselves trigger inflation, especially if demoralized households and businesses are disinclined to borrow money to consume or invest, and chastened banks are subjected to regulatory strictures forcing them to maintain sizable new capital buffers and discouraging them from making any but plain-vanilla loans to highly rated borrowers. The Bernanke Fed’s three rounds of QE presumably tamped down interest rates, but the cash that bought the Treasury and agency securities barely tiptoed into the wider world before the primary dealer banks sent it right back to the Fed as excess reserves. With banks hiding their QE money under the mattress, the money supply didn’t expand in any notable way after the crisis. Thanks to Congress’ series of 2020-21 helicopter drops, the money supply has been growing at rates that would make the late Paul Volcker’s head spin (Chart 11). Inflation is fiendishly more complicated than Milton Friedman’s always-and-everywhere dictum suggests, but there’s now a whole lot of money chasing a limited amount of goods, services and assets. We expect that a receding pandemic will allow greater quantities of goods and services to be produced, and that securities underwriters and their clients are hard at work ramping up asset supply, but inflation has far more of a chance to gain traction now than it did in the decade before the pandemic. Chart 11Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

Bringing "Always And Everywhere" Back Into Vogue?

We therefore think the lower-for-longer and lower-for-ever crowd will find itself offsides at some point in the next few years. We do not think it will get its comeuppance in 2022, however, as we see long yields rising only modestly, with the 10-year Treasury yield ending next year at 2-2.25%. Though we expect the fed funds rate will end the upcoming hiking cycle well north of 2%, bringing about the end of the bull markets in equities and credit, and quite possibly inducing the next recession, we do not think markets will abandon their new-normal rates view by the end of next year. This story will be continued, likely with a greater sense of urgency, in our 2023 outlook. Investment Recommendations Consistent with the foregoing, we make the following recommendations for 2022: Overweight equities in multi-asset portfolios. Although they are not cheap, and may experience a turbulent ride in 2022 as inflation concerns wax and wane, COVID-19 infections periodically surge and the Fed tries to adjust its messaging and actions on the fly, stocks should continue to generate sizable positive excess returns over Treasuries and cash. Overweight cyclical sectors and underweight defensive sectors within equity portfolios. If we’re right to be constructive on the global economy, Energy, Industrials, Materials and Financials are better positioned to benefit than Health Care, Staples and Utilities. Overweight small-cap equities versus large-cap equities. The S&P 600 SmallCap Index has greater exposure to our cyclicals-over-defensives call and our US Equity Strategy colleagues highlight that its constituents are cheaper than the S&P 500’s and are projected to have better earnings growth. Adding small-cap exposure to equity portfolios aligns with our constructive view on the economy and markets. Underweight fixed income in multi-asset portfolios. Underweight Treasuries within bond portfolios. Maintain below-benchmark duration within bond portfolios. Though we do not expect the bond market to see things entirely our way next year, we think the long end of the yield curve will shift out somewhat. We therefore have little appetite for duration and Treasuries and expect spread product will outperform Treasuries and high-yield corporate bonds will outperform investment-grade corporates. Consider hybrid alternatives to traditional fixed income securities. When we roll out our multi-asset ETF portfolio next month, it will include a hybrid bucket of income-generating assets to help multi-asset investors seeking income find low-beta destinations with a fighting chance of generating positive real total returns. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the December 14, 2020 US Investment Strategy Report, "2021 Key Views: It’s The Policy, Stupid." 2 Please see the December 2021 Bank Credit Analyst, "OUTLOOK 2022: Peak Inflation – Or Just Getting Started?"

Highlights A partial reinvasion of Ukraine cannot be ruled out. The constraints on Russia are not prohibitive, especially amid global energy shortages. On this issue, it is better to be alarmist than complacent. We would put the risk of a partial re-invasion of Ukraine as high as 50/50, albeit with an uncertain time frame over 12-36 months. The negative impact of conflict may not stay contained within Russian and eastern European markets. The US and EU are now threatening major retaliatory sanctions if Russia invades. In response Russia could reduce energy exports, exacerbating global shortages and damaging Europe’s overall economy. Investors should stay short Russian assets and overweight developed European equities over emerging European peers. Stay long gold and GBP-CZK. The dollar will be flat-to-up. Feature Chart 1Ruble Faces More Downside From Geopolitics

Ruble Faces More Downside From Geopolitics

Ruble Faces More Downside From Geopolitics

Geopolitical tensions surrounding Russia remain unresolved and investors should continue to reduce holdings of assets exposed to any renewed conflict in Ukraine and the former Soviet Union. The ruble has dropped off its peaks since early November when strategic tensions revived (Chart 1). Presidents Joe Biden and Vladimir Putin held their second bilateral summit on a secure video link on December 7 to discuss the situation in Ukraine, where Russia has amassed 95,000-120,000 troops on the border in a major show of force. Russia also mustered troops in April and only partially drew them down after the Biden-Putin summit in Geneva where the two sides agreed to hold talks to address differences. The two presidents agreed to hold consultations regarding Ukraine. Putin accused NATO of building up Ukraine’s military and demanded “reliable, legally fixed guarantees excluding the expansion of NATO in the eastern direction and the deployment of offensive strike weapons systems in the states adjacent to Russia.”1 President Putin’s red line against Ukraine joining NATO is well known. Recently he said his red line includes the placement of western military infrastructure or missile systems in Ukraine. Biden refused to accept any limits on NATO membership in keeping with past policy. After the summit National Security Adviser Jake Sullivan said, “I will tell you clearly and directly [Biden] made no such commitments or concessions. He stands by the proposition that countries should be able to freely choose who they associate with.” 2 Biden, who had conferred with the UK, France, Germany, and Italy prior to the call, outlined the coordinated economic sanctions that would be leveled against Russia if it resorted to military force, as well as defense aid that would go to Ukraine and other eastern European countries. Thus Putin gave an ultimatum and Biden rebuffed it – and yet the two agreed to keep talking. The Russians have since said that they will present proposals to the Americans in less than a week. Talks are better than nothing. But neither side has given concrete indication of a change in position that would de-escalate strategic tensions – instead they have both raised the stakes. Therefore investors should proceed with the strong presumption that tensions will remain elevated or escalate in the coming months. Clearing Away Misconceptions Before going further we should clear away a few misconceptions about the current situation: Ukraine has unique strategic value to Russia. Like Belarus, but unlike Central Asia, Ukraine serves as critical buffer territory protecting Moscow and the Russian core from any would-be invaders. Russia lacks firm geological borders so it protects itself by means of distance and winter. This grand strategy succeeded against King Charles XII of Sweden, Napoleon, and Hitler. The collapse of the Soviet Union left Russia shorn of much of its buffer territory. Ukraine also offers access to the Black Sea. Russia has long striven to gain access to warm-water ports. The loss of control over Ukraine resulted in a loss of access. Russia’s seizure of Crimea in 2014 only partially rectified the situation. Ukraine’s southern coastline around Crimea is the territory at risk today (Map 1).

Chart

It is Ukraine’s physical existence and unique strategic value – not its democratic leanings or ideological orientation – that ensures perpetual tensions with post-Soviet Russia. Russia has a strategic imperative to reassert control or at least prevent control by foreign powers. Ideological opposition may make things worse but an anti-Russian Ukrainian dictator would also face Russian coercion or aggression, perhaps even more than the current weak democracy. In fact Russia is trying to force Ukraine to revise its constitution and adopt a federal structure so as to grant greater autonomy to separatist regions Donetsk and Luhansk that Russia helped break away in 2014. But Ukraine has not relented to Moscow’s demands of political reform. It is not authoritarianism but a permanent foreclosure of Ukrainian membership in the EU and NATO that Moscow is after. Yet it is highly unlikely that Russia would try to invade and conquer all of Ukraine. Ukraine is the largest country by territory in Europe and has 255,000 active soldiers and 900,000 reserves (contra Russia’s 1 million active and 2 million reserves) who would defend their freedom and sovereignty against an invader.3 Russia would not be able to stage a full-scale invasion with the 175,000 maximum troop buildup that US intelligence is warning about. It would have to mobilize fully, dangerously neglecting other vast dimensions of its national security, and would inevitably get bogged down fighting a vicious insurgency backed by the NATO powers. It would save blood and treasure by paralyzing Ukraine’s politics and preventing it from allying with western militaries, which is what Putin is attempting to do today. Putin uses foreign adventures to strengthen his grip at home but an adventure of this nature would impose such burdens as to threaten his grip at home. A limited re-invasion of Ukraine could yield historic strategic advantages to Russia. Moscow could focus on a partial military incursion that would annex or shore up Donbass, or extend its control from Donbass to the Black Sea, conceivably all the way to the Dnieper river. This pathway would yield Russia maritime access and a buffer space to fortify Crimea. Naval warfare could also yield control of deep-water ports (Yuzhne, Odessa, Mykolaiv, Chornomorsk), control of the mouth of the Dnieper, control of the canal that supplies water to Crimea, and a means of bottling up the Ukrainian navy and preventing foreign maritime assistance. Ukraine would be further weakened and Russia would have a larger beachhead in Ukraine for future pressure tactics. Russia is not bluffing – its military buildup poses a credible threat. If there is anywhere Russia’s threats are credible, it is in taking military action against former Soviet republics like Georgia (2008) and Ukraine (2014) that have pro-western leanings yet lack the collective security of the NATO alliance. At very least, given that Russian forces did deploy in Ukraine in 2014, Russian action in Ukraine cannot be ruled out. The military balance has not changed so significantly in that time and strongly favors Russia (Chart 2). The US has provided around $2.5 billion in military aid to Ukraine since 2014, and has sent lethal weapons including Javelin anti-tank missiles and launchers since 2017-18, including $450 million worth of military aid under the Biden administration (and $300 million just authorized by Congress on December 7). NATO allies have also provided defense aid. This is part of Putin’s complaint but these new arms are not game changers that would prevent Russia from taking military action.

Chart 2

Thus if the West rejects Moscow’s core demands, war is likely. This is true even if Russia would prefer to achieve its aims through political and economic rather than military means. Russia does not deem the West’s threat of sanctions as prohibitive of invasion. The West’s sanctions since 2014 have failed to change Russia’s government, strategy, or posture in Ukraine. Yes, European nations joined the US in imposing sanctions. But Germany also pursued the Nord Stream II pipeline as a means of bypassing Ukraine and working directly with Russia to preserve economic engagement and energy security. Former Chancellor Merkel forced the pipeline through despite the objections of eastern Europeans and the United States. The allies also formed the “Normandy Quartet,” excluding the US, to force Ukraine to accept the Minsk agreements on resolving the conflict. Thus the lesson of 2014-21 is not that NATO allies stood shoulder-to-shoulder in defense of Ukraine’s sovereignty and territorial integrity but rather that Germany and the EU, and the EU and the US, have major differences in interests and risk-tolerance in dealing with Russia. Russia does not face, or may think it does not face, a united front among the western powers. A partial reinvasion of Ukraine would bring the western allies together initially but probably not for long. Russia determines the timing of any new military incursion in Ukraine. Winter is not the ideal time to invade Ukraine, though it is possible. Russia could act in spring 2022, as the US has warned, but it could also act in the summer of 2023, the spring of 2024, or other times. From a strategic point of view, Russia has enjoyed a historic window of opportunity since 2001 when the US got bogged down in Afghanistan and Iraq and then the US and the EU got bogged down in economic and financial crisis. Given that the American political establishment is withdrawing from foreign quagmires, reactivating fiscal policy, bulking up the military-industrial complex, and making a dedicated effort to revitalize its global alliances, Russia may believe that its historic window is closing. Russia’s domestic fundamentals are deteriorating over time. Putin could decide it is necessary to seize strategic ground in Ukraine sooner rather than later. Bottom Line: Ukraine offers unique and irreplaceable buffer space and maritime access to Russia. Russia’s military actions in 2014 led to stalemate, such that Russia remains insecure, Ukraine remains defiant, and the West is still entertaining defense cooperation or even NATO membership with Ukraine. Yet the Crimea conflict also revealed a lack of concert among western powers exemplified by Germany’s Nord Stream II pipeline. Today Russia has the military capability to seize another slice of Ukrainian territory. Western retaliatory actions would be painful but may not be deemed prohibitive. Investors cannot rule out a partial re-invasion of Ukraine. Nord Stream Pipeline Is Not The Sole Factor Is Russia not making a show of military force merely to ensure that Nord Stream II pipeline goes into operation? Will Russia not back down if the pipeline is guaranteed? A common view in Washington and the financial industry is that Russia’s military buildup is just a bluff, i.e. Moscow’s aggressive way of demanding that Germany’s new government and the European Union approve Nord Stream. The pipeline finished construction in September but now awaits formal regulatory certification. Approval was originally expected by May 2022 but has now been delayed. The pipeline would carry 55 billion cubic meters of natural gas into Europe, about half of Russia’s current export capacity outside of Ukraine. Ukraine’s total capacity is around 150 billion cubic meters. The pipeline enables Russia and Germany to bypass Ukraine, whose conflicts with Moscow since 2004 have threatened Germany’s energy security. About 18% of EU’s total energy imports come from Russia, whilst this figure is 16% for Germany. That is about 0.5% and 0.2% of EU and German GDP, respectively. Meanwhile Russian energy exports to Germany and the EU make up 0.8% and 5.6% of GDP, respectively (Chart 3).

Chart 3

The problem with this reasoning is that the US conceded Nord Stream to Russia over the summer. The US initially raised the threat of sanctions because the pipeline strengthened Russo-German ties, diminished Ukraine’s leverage, and deprived the US of a chance to sell liquefied natural gas to Europe. But the Biden administration proved unwilling to take this aggressive approach. Secretary of State Anthony Blinken has a long history of arguing that the US should prioritize strong relations with its European allies rather than punitive measures to try to block Russian gas sales. Biden met with outgoing Chancellor Angela Merkel in July and agreed to let Nord Stream go forward. The only proviso was that Russia not “weaponize natural gas,” i.e. withhold supplies for geopolitical purposes, as it has done in the past.4 Before Russia’s military threats, Germany and the EU were expected to certify the pipeline by no later than May 2022 and an earlier certification looked possible because of Europe’s low natural gas supplies. Yet Russia, fresh off parliamentary elections, did precisely what Germany said it was not supposed to do. The pipeline was completed in September and reports of Russian limitations on natural gas supply surfaced in October. Moscow not only weaponized the gas but also mustered its army on the Ukrainian border again. Putin may have feared that the new German government, which officially took office on December 8, would change policy and refuse to certify the pipeline. He also could have feared that the US Congress would pass a Republican-backed provision that would require Biden to impose sanctions that would halt the pipeline. But these explanations are not satisfactory. First, the German government was not likely to halt Nord Stream. Quite the opposite, Berlin has pushed against all opposition to speed the pipeline into action. It only delayed the regulatory approval when Russia did the one thing that Germany had expressly prohibited, which was weaponize natural gas. Second, the US Congress was never likely to pass mandatory sanctions on Nord Stream operators. The Democrats opposed it, as it would have tied Biden’s hands, whereas presidents always retain discretion over foreign policy and national security. Even moderate Republicans opposed the measure, for the same reason. If either of these were the reason for Putin’s latest buildup, then the buildup will probably dissipate in the coming months. Putin also wants to force Ukraine to implement the Minsk agreements. But the Biden administration adopted the Minsk framework in June for the first time, which was a concession to Russia. So the latest military threats are not solely about coercing Europe to approve the pipeline or Ukraine to implement Minsk. Putin is driving at something else. Putin’s Focus On Ukraine And NATO Putin used military pressure on Ukraine’s border to force the US to accept the pipeline and the Minsk agreements. He is now using the same tactic to raise the stakes and demand that the US and its allies permanently rule out NATO membership and defense cooperation with Ukraine. Biden rejected the first demand during the summit, as mentioned. There is no way that the US or NATO will forswear any and all eastward expansion. Even on Ukraine specifically, Biden cannot give Russia a legal guarantee because it would require a 60-seat majority in the Senate (not likely). Any future president would retain prerogative over the matter anyway and Putin knows this. Moreover Ukraine is never going to join NATO. Russia would attack. And NATO members would not be unanimous (as is required for new members) because the collective defense treaty would require them to defend Ukraine. They would be signing up for a war with Russia. Still Biden is unlikely to disavow Ukrainian NATO membership because to do so would be to deny the self-determination of nations, capitulate to Russian coercion, and demoralize the Ukrainians, whom the US hopes will maintain a plucky resistance against Russian domination. It would also demoralize US allies and partners – namely Taiwan, which also lacks a formal defense treaty and would be forced to sue for peace with China in the face of American abandonment. Biden’s refusal to ban Ukraine from NATO is encapsulated in Diagram 1, an exercise in game theory that exemplifies why the risk of war should not be dismissed. Diagram 1Game Theory Suggests Russia Will Keep Applying Military Pressure

Russia/Ukraine: Don’t Be Complacent

Russia/Ukraine: Don’t Be Complacent

Biden may give private or executive assurances on Ukraine and NATO but Putin will know that these mean nothing since Biden may be out of office as early as January 2025 and then Putin would have to renegotiate. America is not a credible negotiator because partisanship has resulted in extreme foreign policy vacillations – the next president could revoke the deal. Even after Putin is gone Russia would have to negotiate with the US to prevent the US from arming Ukraine. Hence Moscow may decide to reduce Ukraine and improve Russia’s strategic position by force of arms. This is true even if Biden forswears the NATO option, as Diagram 1 illustrates. Putin’s second demand – that the US not provide offensive weapon systems in countries adjacent to Russia – is more material. This is what the new round of talks will focus on. This new Ukraine line of talks is separate, more urgent and important, than the other bilateral dialogues on the arms race, and cyber-war. US-Russia talks on Iran are also urgent, however, and Russia’s cooperation there may be contingent on US concessions regarding Ukraine. The US may be willing to stop its defense cooperation with Ukraine but not with other allies and partners, however. It is also not clear what Putin will accept. These negotiations will have to be watched. Biden cannot make major concessions with a gun to his head. It is unclear how far the US is willing to concede on defense cooperation with countries around Russia. The US may quietly abandon Ukraine but then it would need to reinforce its other defense relationships. If Putin draws down the troops, and Biden calls a stop to defense aid to Ukraine, then a crisis may be averted. What Could Go Wrong? Economic sanctions under consideration in Washington are significant: the US could freeze bank transactions, expand restrictions on trading Russian sovereign and corporate debt, and lobby Belgium to kick Russia off the SWIFT financial messaging system. However, these sanctions may not be effective in preventing Russia from using military force. Russia has weathered US sanctions since 2014, and the smaller and weaker Iranian economy has weathered maximum pressure sanctions since 2019. Energy producers like Russia and Iran have maximum geopolitical leverage when global energy inventories draw down, as is the case today. Even in the face of Russian military aggression, the Biden administration is vacillating on sanctions targeting Russia’s energy sector that would contribute to global shortages and ultimately raise prices at the pump for voters in a midterm election year.5 Germany’s new government also hesitates to declare unambiguously that it will discontinue the Nord Stream II pipeline if Russia invades Ukraine. True, Germany signaled that the pipeline would be halted. Its energy regulator declared that the pipeline’s ownership must be unbundled, which pushes back the certification date to sometime after May 2022 – this was a geopolitical not a legalistic decision. But construction is completed, the pipeline physically exists, which will vitiate Germany’s commitment to sanctions whenever natural gas shortages occur, as is the case this winter (Chart 4). Shortages will continue to occur and Russia controls a large share of supply.

Chart 4

Chart 5

It would take a catastrophe to drive Germany to restart coal and nuclear plants, so natural gas will continue to be in demand. Germany does not have liquefied natural gas import capability yet. If Europe imposes crippling sanctions on Russia, Russia could reduce energy supplies and harm Europe’s economy (Chart 5). The Russian economy and society would suffer which is one reason any military action in Ukraine would be limited in scope. Still, Moscow may believe that Germany would restrain the EU, and the EU would restrain the US, thereby preventing sanctions from being fully, uniformly, and durably implemented. Prior to Russia’s aggression, public opinion polls showed that the German public strongly supported Nord Stream. Even a majority of Green Party members supported it despite the fact that the Greens were the most critical of increasing Germany’s dependency on fossil fuels and an authoritarian petro-state. While public approval of the pipeline has surely suffered in the face of Russian aggression, a majority probably still favors the pipeline. Germany has a national consensus in support of engagement with Russia and avoiding a new cold war, given that the original Cold War cut Germany in half. For that reason invasion may only temporarily unite the western powers – it could ultimately drive a wedge between Germany and other EU members, namely in the former Soviet bloc. It would also divide the more risk-averse EU from the US in terms of how to deal with Russia. And it would weaken the Biden administration at a time when it is extremely vulnerable, exacerbating America’s internal divisions. Russian domestic patriotism would rally, at least initially. Note that Russia could miscalculate on this issue and that is one reason for high level of risk. Perhaps the West would prove far more unified and aggressive in its sanctions enforcement than it was after 2014. A falling ruble and rising inflation could cause Russian social unrest. But Russia could misread the situation. Unless the US and Europe escalate the sanctions threat massively to better deter Russia, their lack of concert is another reason for investors not to be complacent about renewed conflict. Bottom Line: The threat of sanctions may prove insufficient to deter renewed Russian aggression against Ukraine. Germany favors engagement with Russia and Europe’s energy dependency on Russia makes it vulnerable to supply disruptions. Russia has leverage given tight global energy markets, Europe’s low natural gas inventories, and US domestic political considerations ahead of the 2022 midterms. Investment Takeaways The point of this report argues that a partial re-invasion of Ukraine cannot be ruled out. Russia has the capability to reinforce de facto control of Donbas, or expand its footprint in southern Ukraine, though not to invade the whole country. The threat of economic sanctions is not yet so overwhelming as to warrant overconfident predictions of de-escalation. In this case it is better to be alarmist than complacent. Russia would want to maintain an element of surprise so the timing of any belligerence is hard to predict. For de-escalation, investors should watch for Russia to withdraw troops from the Ukrainian border, US-Russia consultations to begin promptly and proceed regularly, and for the US and allies to delay or halt defense cooperation and arms transfers to Ukraine. While global investors would quickly become de-sensitized to conflict that is entirely contained in Ukraine, the trans-Atlantic threat of major sanctions now raises the stakes and suggests that global energy shocks could negatively affect the European or global economy in the event of conflict. Any conflict could also spill outside of Ukraine’s borders, as with Malaysian Airlines flight MH17, which was shot down by Russian-backed Ukrainian separatists in July 2014. The Black Sea has seen a dangerous uptick in naval saber-rattling and that strategic situation would become permanently more dangerous if Russia seized more of coastal Ukraine. Russian military integration with Belarus is also a source of insecurity for EU and NATO members. Global financial markets have only started to price the geopolitical risk emanating from Russia. Our Russian GeoRisk Indicator has ticked up (Chart 6). But Russian equity performance relative to broad emerging markets is only arguably underperforming what is implied by Brent crude oil prices. Chart 6Market Slow To React To Ukraine Crisis - Risk To Downside For Russian Assets

Market Slow To React To Ukraine Crisis - Risk To Downside For Russian Assets

Market Slow To React To Ukraine Crisis - Risk To Downside For Russian Assets

This relatively muted reaction suggests more downside lies ahead if we are right that strategic tensions will be flat-to-up over the coming months. Sell the RUB-USD on any strength. Stay long GBP-CZK. Tactically short Russian equities versus EM-ex-Asia (Chart 7). They are exposed to further correction as a result of escalating geopolitical risk. Chart 7Russia Falling Off Peaks Of Performance Versus EM-Ex-Asia

Russia Falling Off Peaks Of Performance Versus EM-Ex-Asia

Russia Falling Off Peaks Of Performance Versus EM-Ex-Asia

Chart 8Developed Europe A Safer Bet Than Emerging Europe Amid Tensions

Developed Europe A Safer Bet Than Emerging Europe Amid Tensions

Developed Europe A Safer Bet Than Emerging Europe Amid Tensions

Stick to long DM Europe versus EM Europe – our main trade this year to capture rising geopolitical risk between Russia and the West (Chart 8). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 President of Russia, "Meeting with US President Joseph Biden," December 7, 2021, kremlin.ru. 2 White House, "Press Briefing by Press Secretary Jen Psaki and National Security Advisor Jake Sullivan, December 7, 2021," whitehouse.gov. 3 Dan Peleschuk, "Ukraine’s military poses a tougher challenge for Russia than in 2014," Politico, April 14, 2021, politico.eu.; see also Gav Don, "LONG READ: Russia looks poised to invade Ukraine, but what would an invasion actually look like?" Intellinews, November 24, 2021, intellinews.com. 4 US Department of State, "Joint Statement of the United States and Germany on Support for Ukraine, European Energy Security, and our Climate Goals," July 21, 2021, state.gov. 5 Kylie Atwood and Natasha Bertrand, "US likely to hold off for now on energy sanctions for Russia, fearing impact on global prices," CNN, December 9, 2021, cnn.com. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months)

Highlights The last two years have taught us to live with Covid-19. This means global growth will remain strong in 2022. That is not reflected in a strong dollar. The RMB will be a key arbiter between a bullish and bearish dollar view. This is because a weak RMB will be deflationary for many commodity currencies, especially if it reflects weak Chinese demand. Inflation in the US will remain stronger than in other countries. The key question is what the Federal Reserve does next year. In our view, they will stay patient which will keep real interest rates in the US very low. Upside in the DXY is nearing exhaustion according to most of our technical indicators. We upgraded our near-term target to 98. Over a longer horizon, we believe the DXY will break below 90, towards 85 in the next 12-18 months. A key theme for 2022 will be central bank convergence. Either inflation proves sticky and dovish central banks turn a tad more hawkish, or inflation subsides and aggressive rate hikes priced in some G10 OIS curves are revised a tad lower. The path for bond yields will naturally be critical. Lower bond yields will initially favor defensive currencies such as the DXY, CHF and JPY. This is appropriate positioning in the near-term. Further out in 2022, as bond yields rise, the Scandinavian currencies will be winners. Portfolio flows into US equities have been a key driver of the dollar rally. This has been because of the outperformance of technology. Should this change, equity flows could switch from friend to foe for the dollar. A green technology revolution is underway and this will benefit the currencies of countries that will supply these raw materials. The AUD could be a star in 2022 and beyond. The rise in cryptocurrencies will continue to face a natural gravitational pull from policy makers. Gold and silver will rise in 2022, but silver will outperform gold. Feature 2022 has spooky echoes of 2020. In December 2019, we were optimistic about the global growth outlook, positive on risk assets, and bearish the US dollar. That view was torpedoed in March 2020, when it became widely apparent that COVID-19 was a truly global epidemic. More specifically, the dollar DXY index (a proxy for safe-haven demand) rose to a high of 103. US Treasury yields fell to a low of 0.5%. Chart 1Covid-19 And The Dollar

Covid-19 And The Dollar

Covid-19 And The Dollar

Today, the DXY index is sitting at 96, exactly the midpoint of the March 2020 highs and the January 2021 lows. Once again, the dollar is discounting that the new Omicron strain will be malignant – worse than the Delta variant, but not as catastrophic as the original outbreak (Chart 1). Going into 2022, we are cautiously optimistic. First, we have two years of data on the virus and are learning to live with it. This suggests the panic of March 2020 will not be repeated. Second, policymakers are likely to stay very accommodative in the face of another exogenous shock. This will especially be the case for the Fed. Our near-term target for the DXY index is 98, given that the macro landscape remains fraught with risks. This is a speculative level based on exhaustion from our technical indicators (the dollar is overbought) and valuation models (the dollar is expensive). Beyond this level, if our scenario analysis plays out as expected, we believe the DXY index will break below 90 in 2022. Omicron And The Global Growth Picture Chart 2Global Growth And The Dollar

Global Growth And The Dollar

Global Growth And The Dollar

Our golden rule for trading the dollar is simple – sell the dollar if global growth will remain robust, and US growth will underperform its G10 counterparts. Historically, this rule has worked like clockwork. Using Bloomberg consensus growth estimates for 2022, US growth is slated to stay strong, but give way to other economies (Chart 2). News on the Omicron variant continues to be fluid. As we go to press, Pfizer suggests a third booster dose of its vaccine results in a 25-fold increase in the antibodies that attack the virus. Additionally, a new vaccine to combat the Omicron variant will be available by March. If this proves accurate, it suggests the world population essentially has protection against this new strain. The good news is that vaccinations are ramping up around the world, especially in emerging markets. Countries like the US and the UK were the first countries to see a majority of their population vaccinated. Now many developed and emerging market countries have a higher share of their population vaccinated compared to the US (Chart 3). Chart 3ARising Vaccinations Outside The US

Rising Vaccinations Outside The US

Rising Vaccinations Outside The US

Chart 3BRising Vaccinations Outside The US

Rising Vaccinations Outside The US

Rising Vaccinations Outside The US

This has resulted in a subtle shift – growth estimates for 2022 are increasingly favoring other countries relative to the US (Chart 4). Let us consider the case of Japan - just in June this year, ahead of the Olympics, only 25% of the population was vaccinated. Today, Japan has vaccinated 77% of its population and new daily infections are near record lows. While Omicron is a viable risk, the starting point for Japan is very encouraging and should open a window for a recovery in pent-up demand and a pickup in animal spirits. Chart 4ARising Growth Momentum Outside The US

Rising Growth Momentum Outside The US

Rising Growth Momentum Outside The US

Chart I-4

This template could very much apply to other countries as well. This view is not embedded in the dollar, which continues to price in an outperformance of US growth (Chart 5). The Risks From A China Slowdown China sits at the epicenter of a bullish and bearish dollar view. If Chinese growth is bottoming, then the historical relationship between the credit impulse and pro-cyclical currencies will hold (Chart 6). This will benefit the EUR, the AUD, the CAD and even the SEK which that track the Chinese credit impulse in real time. As an expression of this view, we went long the AUD at 70 cents. Chart 5Economic Surprises Outside The US

Economic Surprises Outside The Us

Economic Surprises Outside The Us

Chart 6Chinese Credit Demand And Currencies

Chinese Credit Demand And Currencies

Chinese Credit Demand And Currencies

Just as global policy makers are calibrating the risk from the Omicron variant, the Chinese authorities are also acknowledging the risk of an avalanche from a property slowdown. They have already eased monetary policy on this basis. Specific to the dollar, a key arbiter of a bullish or bearish view will be the Chinese RMB. So far, markets have judiciously separated the risk, judging that the Chinese authorities can surgically diffuse the real estate market, without broad-based repercussions in other parts of the economy (such as the export sector). Equities and corporate credit prices have collapsed in specific segments of the Chinese market but the RMB remains strong (Chart 7). Correspondingly, inflows into China remain very robust, a testament to the fact that Chinese growth (while slowing) remains well above that of many other countries (Chart 8). Chart 7The RMB Has Diverged From The Carnage In China

The RMB Has Diverged From The Carnage In China

The RMB Has Diverged From The Carnage In China

Chart 8Strong Portfolio Inflows Into China

Strong Portfolio Inflows Into China

Strong Portfolio Inflows Into China

China contributed 20% to global GDP in 2021 and will likely contribute a bigger share in 2022, according to the IMF (Chart 9). This suggests that foreign direct investment in China will remain strong . This will occur at a time when the authorities could have diffused the risk from a property market slowdown.

Chart I-9

The commodity-side of the equation will also be important to monitor, especially as it correlates strongly with developed-market commodity currencies. It is remarkable that despite the slowdown in Chinese real estate, commodity prices remain resilient (Chart 10). This has been due to adjustment on the supply side, as our colleagues in the Commodity & Energy Strategy team have been writing. Finally, China offers one of the best real rates in major economies. It also runs a current account surplus. This suggests there is natural demand and support for the RMB (Chart 11). A strong RMB limits how low developed-market commodity currencies can fall. Chart 10Commodity Prices Remain Well Bid

Commodity Prices Remain Well Bid

Commodity Prices Remain Well Bid

Chart 11Real Interest Rates Favor The RMB

Real Interest Rates Favour The RMB

Real Interest Rates Favour The RMB

Inflation And The Policy Response Output gaps are closing around the world as fiscal stimulus has helped plug the gap in aggregate demand. This suggests that while inflation has been boosted by idiosyncratic factors (supply bottlenecks) that could soon be resolved, rising aggregate demand will start to pose a serious problem to the inflation mandate of many central banks. Chart 12A Key Driver Of The Dollar Rally

A Key Driver Of The Dollar Rally

A Key Driver Of The Dollar Rally

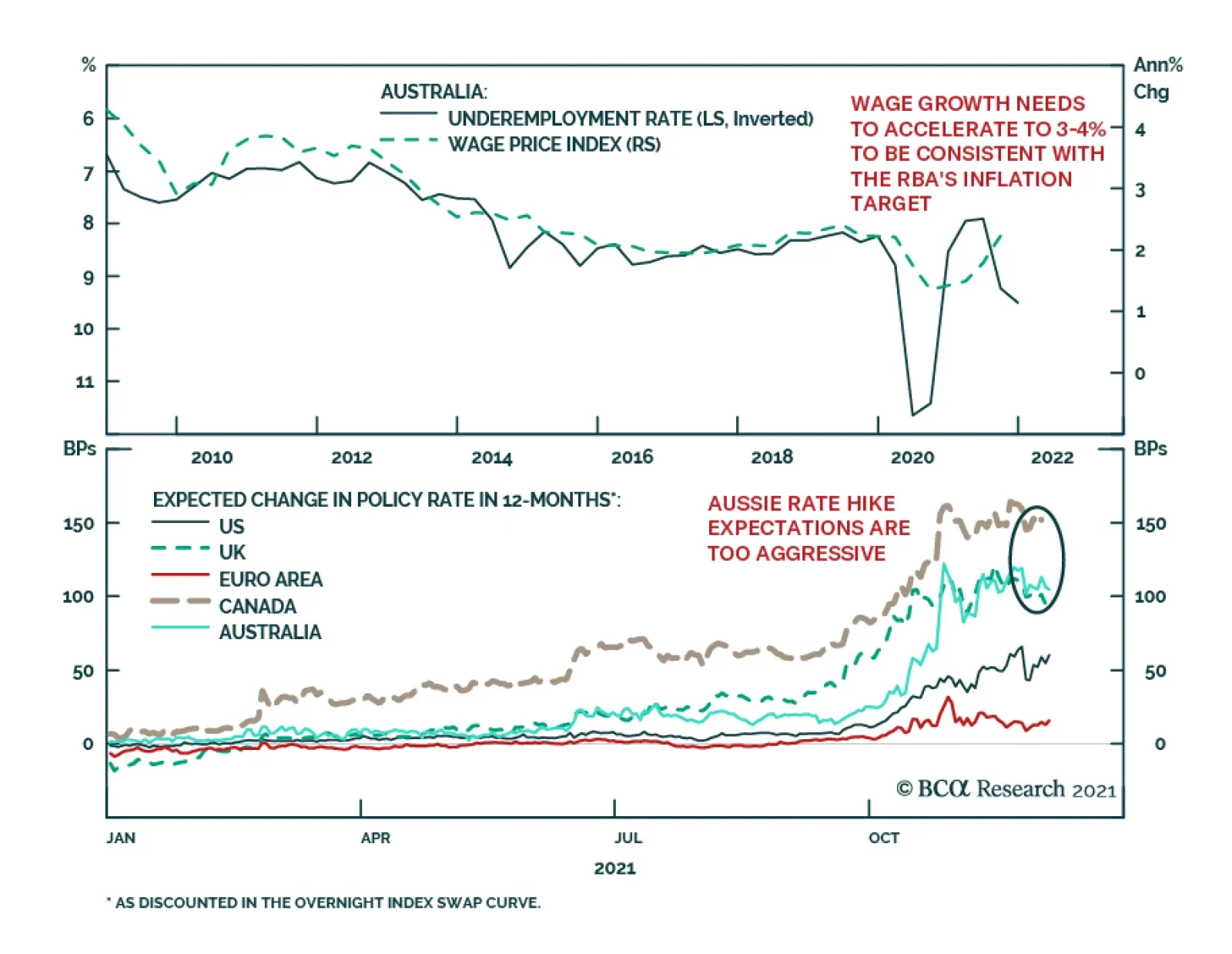

As we wrote a few weeks ago, there have been consistencies and contradictions with the market response to higher inflation. The market is now pricing in that the Fed will raise interest rates much faster, compared to earlier this year. According to the overnight index swap (OIS) curve, the Fed is now expected to lift rates at least twice by December 2022, compared to earlier this year. Meanwhile, market pricing is even more aggressive when looking at the December 2022 Eurodollar contract, relative to either the Euribor contract (European equivalent) or Tibor (Japanese equivalent) (Chart 12). The reality is that outside the ECB and the BoJ, other central banks have actually been more proactive compared to the Federal Reserve. The Bank Of Canada has ended QE and will likely raise interest rates early next year, the Reserve Bank of New Zealand has ended QE and raised rates twice, and the Reserve Bank of Australia has already been tapering asset purchases. The Bank of England will also be ahead of the Fed in raising interest rates, according to our Global Fixed Income Strategy colleagues. This suggests that the pricing of a policy divergence between the Fed and other G10 central banks could be a miscalculation and a potential source of weakness for the dollar. Chart 13The US Is Generating Genuine Inflation

The US Is Generating Genuine Inflation

The US Is Generating Genuine Inflation

Rising inflation is a global phenomenon and not specific to the US (Chart 13). So either inflation subsides and the Fed turns a tad more accommodative, or inflation proves sticky and other central banks turn a tad more hawkish to defend their policy mandates. We have two key short-term trades penned on this view – long EUR/GBP and long AUD/NZD. While the European Central Bank will lag the Bank of England (and the Fed) in raising interest rates, expectations for the path of policy are too hawkish in the UK, with 4 rate hikes priced in by the end of 2022. Similarly, hawkish expectations for the Reserve Bank of New Zealand are likely to be revised lower, relative to the Reserve Bank of Australia. As for the US, the Fed is likely to hike interest rates next year but real rates will remain very low relative to history (Chart 14A and 14B). Low real rates will curb the appeal of US Treasuries. Chart 14AReal Interest Rates In The US Are Very Negative

Real Interest Rates In The US Are Very Negative

Real Interest Rates In The US Are Very Negative

Chart I-14

The Dollar And The Equity Market Chart 15The US Stock Market And The Dollar

The US Stock Market And The Dollar

The US Stock Market And The Dollar

One of the biggest drivers of a strong dollar this year (aside from rising interest rate expectations), has been equity inflows. The greenback tends to do well when US bourses are outperforming their overseas peers (Chart 15). It is also the case that value tends to underperform growth in an environment where the dollar is rising. We discussed this topic in depth in our special report last summer. Flows tend to gravitate to capital markets with the highest expected returns. So if investors expect the pandemic winners (technology and healthcare) to keep driving the market in an Omicron setting, the US bourses that are overweight these sectors will do well. We will err on the other side of this trade for 2022. Part of that is based on our analysis of the global growth picture in the first section of this report. If growth rotates from the US to other economies, their bourses should do well as profits in these economies recover. Earnings revisions in the US have been sharply revised lower compared to other countries (Chart 16). This has usually led to a lower dollar eventually. In the case of the euro area, there has been a strong and consistent relationship between relative earnings revisions vis-à-vis the US, and the performance of the euro (Chart 17). Chart 16Earnings Revisions Are Moving Against US Companies

Earnings Revisions Are Moving Against US Companies

Earnings Revisions Are Moving Against US Companies

Chart 17Earnings Revisions Are Moving In Favor Of Euro Area Companies

Earnings Revisions Are Moving In Favor Of Euro Area Companies

Earnings Revisions Are Moving In Favor Of Euro Area Companies

In a nutshell, should profits in cyclical sectors recover on the back of rising bond yields, strong commodity prices and a tentative bottoming in the Chinese economy, value sectors that are heavily concentrated in countries with more cyclical currencies such as Australia, Norway, Sweden, and Canada, will benefit. Ditto for their currencies. The Outlook For Petrocurrencies

Chart I-18

When the pandemic first hit in 2020, oil prices (specifically the Western Texas Intermediate blend) went negative. This drop pushed the Canadian dollar towards 68 cents and USD/NOK punched above 12. This time around, the drop in oil prices (20% from the peak for the Brent blend) has been more muted. We think this sanguine market reaction is more appropiate in our view for two key reasons. First, as our colleagues in the Commodity & Energy Stategy team have highlighted, investment in the resource sector, specifically oil and gas, has been anemic in recent years. In Canada, investment in the oil and gas sector has dropped 68% since 2014 at the same time as energy companies are becoming more and more compliant vis-à-vis climate change (Chart 18). Second, if we are right, and Omicron proves to be a red herring, then transportation demand (the biggest source of oil demand) will keep recovering. In terms of currencies, our preference is to be long a petrocurrency basket relative to oil consumers. As the US is the biggest oil producer in the world (Chart 19), being long petrocurriences versus the dollar has diverged from its historical positive relationship with oil prices. Chart 20 shows that a currency basket of oil producers versus consumers has had both a strong positive correlation with oil prices and has outperformed a traditional petrocurrency basket. Chart 19The US Is Now A Major Oil Producer

The US Is Now A Major Oil Producer

The US Is Now A Major Oil Producer

Chart 20Hold A Basket Of Oil Consumers Versus Producers

Hold A Basket Of Oil Consumers Versus Producers

Hold A Basket Of Oil Consumers Versus Producers

Technical And Valuation Indicators The dollar tends to be a momentum-driven currency. Past strength begets further strength. We modelled this when we published our FX Trading Model, which showed that a momentum strategy outperformed over time (Chart 21). The problem with momentum is that it works until it does not. Net speculative long positions in the dollar are approaching levels that have historically signaled exhaustion (Chart 22). There is a dearth of dollar bears in today’s environment. That is positive from a contrarian standpoint. Meanwhile, our capitulation index (a measure of how overbought or oversold the dollar is) is approaching peak levels. Chart 21The Dollar Is A Momentum Currency

The Dollar Is A Momentum Currency

The Dollar Is A Momentum Currency

Chart 22Long Dollar Is A Consensus Trade

Long Dollar Is A Consensus Trade

Long Dollar Is A Consensus Trade

Valuation is another headwind for the dollar. According to all of our in-house models, the dollar is expensive. That is the case according to both our in-house curated PPP model (Chart 23) and a simple one based on headline consumer prices (Chart 24).

Chart I-23

Chart 24The Dollar is Expensive

The Dollar is Expensive

The Dollar is Expensive

In a broader sense, we have built an attractiveness ranking for currencies (Chart 25). This ranks G10 currencies on a swathe of measures, including their basic balances, our internal valuation models, sentiment measures, economic divergences, and external vulnerability. The ranking is in order of preference, with a lower score suggesting the currency is sitting in the top/most attractive quartile of the measures. The Norwegian krone and Swedish krona are especially attractive as 2022 plays.

Chart I-25

More specifically, the Scandinavian currencies have been one of the hardest hit this year. The Norwegian krone will benefit from the reopening of economies, particularly through the rising terms-of-trade. The Swedish krona will benefit from a pickup in the industrial sector, and continued strength in global trade. The least attractive G10 currencies are the New Zealand dollar and the greenback. This is mostly due to valuation. As we have highlighted in previous reports, valuation is a poor timing tool in the short term but over a longer-term horizon, currencies tend to revert towards fair value. Where Next For EUR/USD? Our bias is that the euro has bottomed. The ECB will lag the Fed in raising interest rates, but the spread between German bund yields and US Treasuries does not justify the current level of the euro. More importantly, if European growth recovers next year, this will sustain portfolio flows into the eurozone, which are cratering (Chart 26). Our 2022 target for EUR/USD is 1.25, a level that will unwind 10.6% of the undervaluation versus the dollar. Beyond valuation,s a few key factors support the euro: As a pioneer in green energy and a pro-cyclical currency, the euro will benefit from portfolio flows into renewable energy companies, as well as foreign direct investment. A close proxy for these flows are copper prices, that have positively diverged from the performance of the euro (Chart 27). Chart 26The Euro And Portfolio Flows

The Euro And Portfolio Flows

The Euro And Portfolio Flows

Chart 27EUR/USD And Copper

EUR/USD And Copper

EUR/USD And Copper

Inflation in the euro area is lagging the US, but is undeniably strong. As such, while the ECB will lag the Fed in tightening monetary policy, the divergence in monetary policy will not widen. Earnings revisions are moving in favor of European companies, as we have shown earlier. Historically, this has put a floor under the euro. Safe-Haven Demand: Long JPY Safe-haven currencies will perform well in the near term. We are long the yen, which is the cheapest currency according to our models and also one of the most shorted. CHF will also do well in the near term, though as we have argued, will induce more intervention from the Swiss National Bank.

Chart I-28

We are long both the yen and CHF/NZD as short-term trades, but our preference is for the yen. First, Japan has one of the highest real rates in the developed world. So, outflows from JGBs are going to be curtailed. Second, the DXY and USD/JPY have a strong positive correlation, and this places the yen in a very enviable position as the dollar weakens in 2022 (Chart 28). A Final Word On Gold, Silver, And Precious Metals Chart 29Hold Some Gold

Hold Some Gold

Hold Some Gold

Along with our commodity strategists, we remain bullish precious metals. In our view, inflation could prove stickier than most investors expect. This will depress real rates and support precious metals. Within the precious metals sphere, we particularly like silver and platinum. Almost every major economy now has negative real interest rates. Gold (and silver) have a long-standing relationship with negative interest rates (Chart 29). Central banks are also becoming net purchasers of gold, which is bullish for demand. The true precious metals winner in 2022 could be silver. The Gold/Silver ratio (GSR) tends to track the US dollar quite closely, so a bearish view on the dollar can be expressed by being short the GSR (Chart 30). Second, gold is very expensive compared to silver (Chart 31). In general, when gold tends to make new highs (as it did in 2020), silver tends to follow suit. This means silver prices could double from current levels over the next few years, to reclaim their 2011 highs. Finally, the bullish case for platinum is the same as for silver. It has lagged both gold and palladium prices. Meanwhile, breakthroughs are being made in substituting palladium for platinum in gasoline catalytic converters. Chart 30Hold Some Silver

Hold Some Silver

Hold Some Silver

Chart 31Stay Short The GSR

Stay Short The GSR

Stay Short The GSR

Concluding Thoughts Our currency positions, as we enter 2022, are biased towards a lower dollar, but we also acknowledge that there are key risks to the view. Our recommendations are as follows: The DXY will could touch 98 in the near term, but will break below 90 over the next 12-18 months. An attractiveness ranking reveals the most appealing currencies are JPY, SEK, and NOK, while the least attractive are USD and NZD. Chart 32Hold Some AUD

Hold Some AUD

Hold Some AUD

Policy convergence will be a key theme at the onset of 2022. Stay long EUR/GBP and AUD/NZD as a play on this theme. Look to buy a basket of oil producers versus consumers once volatility subsides. We went long the AUD at 70 cents. Terms of trade are likely to remain a tailwind for the Australian dollar (Chart 32). The AUD will benefit specifically in a green revolution. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

Highlights 1. How will the pandemic resolve? 2. Will services spending recover to its pre-pandemic trend? 3. Will we spend our excess savings? 4. How will central banks react to inflation? 5. Will cryptocurrencies continue to eat gold’s lunch? 6. How fragile is Chinese real estate? 7. Will there be another shock? Fractal analysis: Personal goods versus consumer services. Feature Chart of the WeekWill Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

Will Services Spending Recover To Its Pre-Pandemic Trend?

“Judge a man by his questions, not by his answers” The quotation above is often misattributed to Voltaire instead of its true author, Pierre-Marc-Gaston de Lévis. Irrespective of the misattribution, we agree with the maxim. Asking the right questions is more important than finding answers to the wrong questions. In this vein, this report takes the form of the seven crucial questions for 2022 (and our answers). 1. How Will The Pandemic Resolve? As new variants of SARS-CoV-2 have arrived like clockwork, the number of new global cases of infection and the virus reproduction rate have formed a near-perfect mathematical ‘sine wave’. This near-perfect sine wave will propagate into 2022 (Chart I-2). Chart I-2The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

The Pandemic's Sine-Wave Will Propagate Into 2022

But how will this sine wave of infections translate into mortality, morbidity, and stress on our healthcare systems? As we explained in RNA Viruses: Time To Tell The Truth, the answer depends on the specific combination of contagiousness, immuno-evasion, and pathogenicity of each variant. Yet none of this should come as any surprise. Flus and colds also come in waves, which is why we call them flu and cold seasons. And the morbidity of a given flu and cold season depends on the aggressiveness of that season’s flu and cold variant. So, just like the flu and the cold, Covid will become an endemic respiratory disease which comes in waves. The trouble is that our under-resourced health care systems can barely cope with a bad flu season, let alone with an additional novel disease that can be worse than the flu. Hence, until we add enough capacity to our healthcare systems, expect more disruptions to economic activity from periodic non-pharmaceutical interventions such as travel bans, vaccine passports, and face-mask mandates. 2. Will Services Spending Recover To Its Pre-Pandemic Trend? The pandemic has given us a crash course in virology and epidemiology. We now understand antigens, antibodies, and ‘reproduction rates.’ We understand that a virus transmits as an aerosol in enclosed unventilated spaces, and that singing, and yelling eject this viral aerosol. We understand that vaccinations for RNA viruses have limited longevity, do not prevent reinfections, and that certain environments create ‘super-spreader’ events. Armed with this new-found awareness, a significant minority of people have changed their behaviour. Services which require close contact with strangers – going to the dentist or in-person doctors’ appointments, going to the cinema or to amusement parks, or using public transport – are suffering severe shortfalls in demand. Given that this change in behaviour is likely long-lasting, demand for these services is unlikely to regain its pre-pandemic trend in 2022 (Charts I-3 - I-6). Chart I-3Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Dental Services Are Far Below The Pre-Pandemic Trend

Chart I-4Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Physician Services Are Far Below The Pre-Pandemic Trend

Chart I-5Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Recreation Services Are Far Below The Pre-Pandemic Trend

Chart I-6Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Public Transportation Is Far Below The Pre-Pandemic Trend

Therefore, to keep overall demand on trend, spending on goods will have to stay above its pre-pandemic trend. This will be a tough ask. Durables, by their very definition, last a long time. Even clothes and shoes, though classified as nondurables, are in fact quite durable. Meaning that are only so many cars, iPhone 13s, gadgets, clothes and shoes that any person can own before reaching saturation. If, as we expect, spending on goods falls back to its pre-pandemic trend, but spending on services does not recover to its pre-pandemic trend, then there will be a demand shortfall in 2022 (Chart of the Week). 3. Will We Spend Our Excess Savings? If spending falls short of income – as it did through the pandemic – then, by definition, our savings have gone up. Many people claimed that this war chest of savings would unleash a tsunami of spending. Well, it didn’t. And, it won’t. Previous episodes of excess savings in 2004, 2008, and 2012 had no impact on the trend in spending (Chart I-7).

Image

The explanation comes from a theory known as Mental Accounting Bias. The theory states that we segment our money into different accounts, which are sometimes physical, sometimes only mental, and that our willingness to spend money depends on which mental account it occupies. This contrasts with standard economic theory which assumes that money is perfectly fungible, meaning that a dollar in a current (checking) account is no different to a dollar in a savings or investment account. In practice, money is not fungible, because we attach different emotions to our different mental accounts. A dollar in our current account we will gladly spend, but a dollar in our savings account we will not spend. Hence, the moment we move the dollar from our current account into our savings account, our willingness to spend it collapses. This explains why consumption trends have no connection with windfall income receipts once those income receipts end up in our savings mental or physical account. Pulling all of this together, the war chest of savings accumulated during the pandemic is unlikely to change the overall trend in spending. 4. How Will Central Banks React To Inflation? The real story of the current ‘inflation crisis’ is that while goods and commodity prices have surged exactly as expected in a positive demand shock, services prices have not declined as would be expected in the mirror-image negative demand shock. The result is that aggregate inflation has surged even though aggregate demand has not (Chart I-8 and Chart I-9). Chart I-8Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Goods Prices Have Reacted To A Positive Demand Shock...

Chart I-9...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

...But Service Prices Have Not Reacted To A Negative Demand Shock

Why have services prices remained resilient despite a massive negative demand shock? One answer, as explained in question 2, is that much of the shortfall in services demand is due to behavioural changes, which cannot be alleviated by lower prices. If somebody doesn’t go to the dentist or use public transport because he is worried about catching Covid, then lowering the price will not lure that person back. In fact, the person might interpret the lower price as a signal of greater risk, and might become more averse. In technical terms, the price elasticity of demand for certain services has flipped from its usual negative to positive. This creates a major problem for central banks, because if the price elasticity of services demand has changed, then surging aggregate inflation is no longer a reliable indicator of surging aggregate demand. To repeat, inflation is surging even though aggregate demand is barely on its pre-pandemic trend. Hence in 2022, central banks face a Hobson’s choice. Choke demand that does not need to be choked, or turn a blind eye to inflation and risk losing credibility. 5. Will Cryptocurrencies Continue To Eat Gold’s Lunch? Most of the value of gold comes not from its economic utility as a beautiful, wearable, and electrically conductive metal, but from its investment value as a hedge against the debasement of fiat money. The multi-year investment case for cryptocurrencies is that they are set to displace much of gold’s investment value. Still, to displace gold’s investment value, cryptocurrencies need to match its other qualities: an economic utility, and limited supply. A cryptocurrency’s economic utility comes from its means of exchange for the intermediation services that its blockchain provides. For example, if you issue a bond or smart-contract using the Ethereum blockchain, then you must pay in its cryptocurrency ETH. Which gives ETH an economic utility. Furthermore, the number of blockchains that will succeed as go-to places for intermediation services will be limited, and each cryptocurrency has a limited supply. Thereby, the supply of cryptocurrencies that have a utility is also limited. With an economic utility, a limited supply, and drawdowns that are becoming smaller, cryptocurrencies can continue to displace gold’s dominance of the $12 trillion anti-fiat investment market. Therefore, the cryptocurrency asset-class can continue its strong structural uptrend, albeit punctuated by short sharp corrections (Chart I-10). Chart I-10Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

Cryptocurrencies Will Continue To Displace Gold's Investment Value

The corollary is that the structural outlook for gold is poor. 6. How Fragile Is Chinese Real Estate? A decade-long surge in Chinese property prices has lifted Chinese valuations to nosebleed levels. According to global real estate specialist Savills, prime real estate yields in China’s major cities are now barely above 1 percent, and the world’s five most expensive cities are all in China: Hangzhou, Shenzhen, Guangzhou, Beijing, and Shanghai (Chart I-11).

Chart I-11

Without a social safety net and with limited places to park their money, Chinese savers have for years been encouraged to buy homes, in the widespread belief that property is the safest investment, whose price only goes up. With the bulk of people’s wealth in property acting as a perceived economic safety net, even a modest decline in house prices would constitute a major shock to the household sector’s hopes and expectations of what property is. Therefore, in contrast to the US housing debacle in 2008, the Chinese government will ensure that its property market adjustment does not come from a collapse in home prices. Rather, it will come from a collapse in property development and construction activity. This will have negative implications for commodities, emerging Asia, developing countries that produce raw materials, and machinery stocks worldwide. 7. Will There Be Another Shock? Most strategists claim that shocks, such as the pandemic, are unpredictable. We disagree. Yes, the timing and source of an individual shock is unpredictable, but the statistical distribution of shocks is highly predictable. We define a shock as any event that causes the long-duration bond price in a major economy to rally or slump by at least 20 percent.1 Using this definition through the last 60 years, the statistical distribution of the number of shocks in any ten-year period is Poisson (3.33) and the time between shocks is Exponential (3.33). This means that in any ten-year period, the likelihood of suffering a shock is a near-certain 95 percent; in any five-year period, it is an extremely high 80 percent; in a two-year period it is a coin toss at 50 percent; and even in one year it is a significant 30 percent (Chart I-12).

Chart I-12

Therefore, on a multi-year horizon, another shock is a near-certainty even if we do not know its source or precise timing. The question is, will it be net deflationary, or net inflationary? Our high-conviction view is that it will be net deflationary. Meaning that even if it starts as inflationary, it will quickly morph into deflationary. The simple reason is that it is not just Chinese real estate that is fragile. Through the past ten years, world prime residential prices are up by 70 percent while rents are up by just 25 percent2 (Chart I-13). Meaning that the bulk of the increase in global real estate prices is due to skyrocketing valuations. The culprit is the structural collapse in global bond yields – which, in turn, is due to persistently ultra-low policy interest rates combined with trillions of dollars of quantitative easing. Chart I-13Property Price Inflation Has Far Exceeded Rent Inflation

Property Price Inflation Has Far Exceeded Rent Inflation

Property Price Inflation Has Far Exceeded Rent Inflation