Policy

Highlights The equity risk premium has turned negative for the first time since 2002. It follows that any significant rise in bond yields will cause risk-asset prices to collapse, quickly flipping any incipient inflationary shock into a deflationary shock. Shorting bonds yielding 2 percent is a ‘widow maker’ trade, as anybody who has tried this with a long list of government bonds has learned to their cost, the most recent being UK gilts. Hence, the next on the list for the ‘widow maker’ is shorting the US 30-year T-bond which is now yielding 2 percent. In fact, the US 30-year T-bond is a must-own structural investment. Fractal analysis: Medical equipment versus healthcare services. Feature Chart of the WeekThe Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

The Equity Risk Premium Turns Negative For The First Time Since 2002

Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. Mainstream investments are now priced to deliver negative, zero, or at best, feeble long-term investment returns. For example, the US 10-year Treasury Inflation Protected Security (TIPS) and the UK 10-year index linked gilt are yielding -1.3 percent and -2.8 percent respectively. Meaning that anybody who buys and holds these bonds to redemption is guaranteed a deeply negative 10-year real return. Meanwhile, in nominal yield space, 10-year government bonds yield -0.35 percent in Germany and Switzerland, 0.7 percent in the UK, and 1.3 percent in the US. What about equities? Unlike a bond’s redemption yield, equities do not offer a guaranteed long-term return for buy-and-hold investors. So, some analysts assume that the equity market’s earnings yield is the proxy for this long-term return. According to these analysts, the US equity market’s earnings yield of 4.4 percent means that it will deliver a prospective long-term real return of 4.4 percent per annum. Compared to the 10-year TIPS real yield of -1.3 percent, they argue that this offers an excess return or ‘equity risk premium’ of a comfortable +5.7 percent. Therefore, claim these analysts, equities are reasonably valued, relative to bonds, and in absolute terms. But as we will now demonstrate, this analysis is deeply flawed. The Equity Risk Premium Has Turned Negative The equity market’s earnings yield is a valuation metric, so clearly there is some connection between it and the prospective return delivered by the equity market. Nevertheless, the crucial point to grasp is that: The equity market’s earnings yield does not equal its prospective return. Charts I-2 - I-3 should make this point crystal clear. As you can see, the earnings yield rarely equals the delivered prospective 10-year return, either real or nominal. When the earnings yield is elevated, the prospective return turns out higher. Conversely, when the earnings yield is depressed, as now, the prospective return turns out to be much lower. Chart I-2The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

The Equity Market's Earnings Yield Does NOT Equal Its Prospective Return, Either In Real Terms...

Chart I-3...Or In Nominal ##br##Terms

...Or In Nominal Terms

...Or In Nominal Terms

Therefore, to take the current earnings yield of 4.4 percent and subtract the real bond yield of -1.3 percent to derive an equity risk premium of +5.7 percent is analytically flawed, just as it is analytically flawed to subtract apples from oranges. To derive the equity risk premium, the correct approach is first to translate the earnings yield into a prospective 10-year return based on the established mathematical relationship between these variables. Chart I-4 does this and shows that, based on a very tight mathematical relationship through the past thirty five years, an earnings yield of 4.4 percent translates into a prospective 10-year nominal return of just 1 percent. Chart I-4We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

We Must Mathematically Map The Earnings Yield Into A Prospective Return...

Having translated the earnings yield into a prospective 10-year nominal return of 1 percent, we can now make an apples-for-apples comparison with the 10-year T-bond yield of 1.3 percent (Chart I-5). Chart I-5...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

...And Only Then Subtract The Bond Yield

Derived correctly therefore, the equity risk premium has turned negative for the first time since 2002 (Chart of the Week). We deduce that the equity market is very richly valued both in absolute terms and relative to bonds. And crucially, that this rich valuation is contingent on bond yields remaining ultra-low, or going even lower. Shorting Bonds Yielding 2 Percent Is A ‘Widow Maker’ All of which brings us to one of the most pressing questions we get from clients. When a bond is offering a feeble yield, what is the point in owning it? Maybe the best people to answer are the casualties of the now infamous ‘widow maker’ trades. The original widow maker trade was the idea that the yield on the Japanese Government Bond (JGB), at 2 percent, was so feeble that there was no point in owning it. Furthermore, with massive Japanese fiscal stimulus coming down the pike, the ‘no-brainer’ investment strategy was not just to disown the JGBs, but to take an outright short position, as it seemed that the only direction that JGB yields could go was up. In fact, JGB yields did not go up, they continued to trend down. As feeble yields became even feebler, the owners of the short positions got carried out of their careers, feet first. Meanwhile, those investors who owned 30-year JGBs yielding a ‘feeble’ 2 percent in 2013 reaped returns of 75 percent, and even now, are sitting on handsome profits of 55 percent. Some people protest that Japan is an exceptional and isolated case, rather than a template for economies which will not repeat their putative policy-errors. Such protests have always struck us as factually wrong, blinkered, and even prejudiced. Nevertheless, let’s indulge these prejudices with a simple rejoinder – forget Japan, what about Switzerland, or the UK? (Chart I-6) Chart I-6Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Shorting Bonds Yielding 2 Percent Is A 'Widow Maker'

Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Meanwhile, those investors who owned 30-year UK gilts yielding a ‘feeble’ 2 percent in 2018 reaped returns of 40 percent, and even now are sitting on tidy profits of 30 percent. Just like the JGB widow maker, anybody who shorted UK gilts yielding 2 percent is nursing heavy losses. Bear in mind that a 30-year bond yielding a feeble 2 percent will deliver a cumulative return of more than 80 percent to redemption. And that if the feeble yield becomes even feebler, this return will get front-end loaded, creating widow makers for the short positions and spectacular gains for the long positions, as witnessed in JGBs and UK gilts. The 30-Year T-Bond Is A Must-Own Structural Investment The next candidate for the widow maker is shorting the US 30-year T-bond, which is yielding, you guessed it, 2 percent. Remember that while Japan may not be a great template for the US, the UK certainly is – because the US and UK have very similar economic, financial, political, social, and cultural structures. Until recently therefore, bond yields in the US and UK were moving in near-perfect lockstep (Chart I-7). Chart I-7The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

The Difference Between US And UK Bond Yields Is Just That The UK Has Had One More Deflationary Shock

So, what happened? The one word answer is: Brexit. The recent difference between US and UK bond yields is simply that the UK has had one more deflationary shock than the US. Put the other way around, the US is just one deflationary shock away from a UK level of bond yields – meaning the 30-year yield not at 2 percent, but at 1 percent. But why can’t the next shock be an inflationary shock resulting in much higher yields? The simple answer is that the equity risk premium has turned negative for the first time since 2002. Moreover, as we pointed out in The Road To Inflation Ends At Deflation the extremely rich valuation of $300 trillion of global real estate is also highly contingent on ultra-low bond yields. It follows that any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. In a $90 trillion global economy, this will quickly flip any incipient inflationary shock into a deflationary shock. Any significant rise in bond yields will collapse the value of $500 trillion of risk-assets. We conclude that the US 30-year T-bond is a must-own structural investment. Fractal Analysis Update As hospitals have rushed to clear their backlog of non-pandemic treatments and procedures, medical equipment stock prices have surged. This is particularly true for US medical equipment (ticker IHI) which, since June, is up by 25 percent versus US healthcare services (Iqvia, Veeva, or loosely proxied by ticker XHS). Given that the backlog of treatments will eventually clear, and that the intense rally is now extremely fragile on its 65-day fractal structure (Chart I-8), a recommended countertrend trade is to short US medical equipment versus healthcare services. Set the profit target and symmetrical stop-loss at 8.5 percent. Chart I-8The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

The Intense Rally In Medical Equipment Stocks Has Become Fragile

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades 6-Month Recommendations Structural Recommendations Closed Fractal Trades Closed Trades Asset Performance Equity Market Performance Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields ##br##- Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields ##br##- Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields ##br##- Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields ##br##- Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Feature Chart 1Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Chinese Offshore Stocks Tumbled Amid Regulatory Crackdowns

Relative to the global equity index, onshore and offshore Chinese stocks have fallen by 18% and 32%, respectively, since their peaks in mid-February (Chart 1). The panic sell-off in the offshore market, which saw greater losses due to its high concentration in internet stocks, appears to be overdone and may technically rebound in the near term. However, any short-term bounce in Chinese stocks from oversold levels will likely be short-lived (Chart 2). The crackdown on new economy companies reflects socio-political and economic shifts in China, which raises the odds that the restrictions will continue with further actions focused on social welfare and healthcare. August’s official PMIs and economic data indicate a broad-based softening in China’s domestic demand and production. However, compared with 2018/19 when the US-China trade war exacerbated the deterioration in an already slowing economy, the economy now remains well supported by strong exports. Moreover, the magnitude of the slowdown has not exceeded policymakers’ pain thresholds (Chart 3). Chart 2Tactical Bounce Was Short-Lived In Previous Downturns

Tactical Bounce Was Short-Lived In Previous Downturns

Tactical Bounce Was Short-Lived In Previous Downturns

Chart 3China's Economic Recovery Losing Steam, But From An Elevated Level

China's Economic Recovery Losing Steam, But From An Elevated Level

China's Economic Recovery Losing Steam, But From An Elevated Level

In 2018/19, stimulus was measured and the authorities did not meaningfully relax limits on bank lending standards and shadow banking. Furthermore, China recently reiterated its cross-cycle macro policy setting, which means that policymakers will not use significant stimulus to achieve high and short-term economic growth. Given financial stability measures that aim to contain risks associated with the housing market and hidden local government debt, any monetary and fiscal easing will likely help to stabilize credit growth instead of substantially boosting it this year. For the time being, China’s financial assets continue to face downside risks stemming from a confluence of a weakening business cycle and ongoing regulatory tightening. Thus, we recommend investors maintain an underweight allocation to Chinese equities within a global equity portfolio. Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com A Shining Moment For Chinese Small And Medium Caps Small and medium-cap (SMID-cap) stocks have outperformed large-caps since February and the recent regulatory restrictions have intensified the situation. The CSI500 index, which comprises 500 SMID-cap companies, has outperformed the large-cap CSI300 by 34% since mid-February (Chart 4, top panel). Uncertainties surrounding the pandemic and corporate earnings growth have fueled extreme dislocations between large-cap and SMID-cap stocks last year. Large-cap stocks were the main contributors to China’s stock rallies in the second half of last year, while the valuation premia in small cap stocks was compressed to near decade lows (Chart 4, bottom panel). Chart 4A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

A Low Valuation Premia And More Policy Support May Further Lift Prices Of SMID-Caps

Chart 5SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

SMID-Caps Tend To Outperform Large-Caps In Late Business Cycle

Historically, SMID-caps tend to outperform large-caps in the late cycle of an economic recovery (Chart 5). The spate of regulatory changes aimed at monopolistic behaviors in various sectors has curbed investors’ appetite for the industry leaders. In addition, the government’s increasing efforts to support small and medium corporates (SMEs) will help to shore up confidence in those companies. Therefore, small and medium caps will likely continue to outperform large-cap stocks this year. Fiscal Support: How Much Room In 2H? The July Politburo meeting pledged more fiscal support for the economy later in 2021 and into 2022. We expect local government bond (LGB) issuance to accelerate: a 4.47 trillion RMB new local government bond issuance quota was approved for 2021, including 820 billion in general bonds and 3.65 trillion in special purpose bonds (SPBs). By end-August, 2.37 trillion new local government bonds had been issued, which was only 53% of the entire year’s goal. However, there are some constraints that will likely reduce the reflationary effects on the economy. First, the quota for LGB issuance approved by the National People’s Congress is 16% lower than last year, but the amount of LGBs maturing this year is 30% higher. Therefore, even though this year’s gross LGB issuance has kept pace with that of last year, more than half of the LGBs issued from January to August was used for debt repayment (Chart 6). The move by local governments to use a large portion of their bond issuance quota to pay off existing debt resembles the situation in 2018 when a financial de-risking campaign encouraged local governments to reduce the stockpile of their leverage. As noted in last week’s report, infrastructure investment and the economy did not rebound in 2H2018, even though LGB issuance picked up (Chart 7). Chart 6More Than Half Of LGBs Issued This Year Has Been Used For Debt Repayment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chart 7Improvement In Infrastructure Investment Was Short-Lived In 2019

Improvement In Infrastructure Investment Was Short-Lived In 2019

Improvement In Infrastructure Investment Was Short-Lived In 2019

Even if we assume that local governments will use all of their remaining bond quota by year end, the gross monthly average in local government bond issuance will be around 580 billion, only slightly higher than in 2H 2020. Secondly, infrastructure investment is discouraged by stringent regulations to approve projects (including project assessment and debt repayment ability) and the accountability of local officials for project failures. Approvals for infrastructure projects remain at the lowest level since March last year (Chart 8). Finally, SPBs made up only about 15% of overall infrastructure spending in the past three years, while the majority came from public-private partnerships (PPP) financing, revenues from government-managed funds, government budgets and bank loans. Falling proceeds from land transfers have dragged down government-managed funds (Chart 9). In addition, government expenditures show no signs of a material increase (Chart 9, bottom panel). Chart 8Infrastructure Investment Will Remain Subdued

Infrastructure Investment Will Remain Subdued

Infrastructure Investment Will Remain Subdued

Chart 9Government Expenditures Remain Muted

Government Expenditures Remain Muted

Government Expenditures Remain Muted

As discussed in previous reports, local government bonds issuance only accounts for 12% of total social financing. As such, without a sizeable acceleration in bank loans, enhanced LGB issuance would not be enough to prompt a substantial increase in infrastructure investment growth. Our argument is underscored by the structural downshift in infrastructure investment since 2017 (Chart 7, top panel). Therefore, additional local government bond issuance this year will help to stabilize but not boost credit growth. August PMIs Confirm Slowing Economic Activity China's official PMIs eased further in August. The non-manufacturing index fell to contractionary territory of 47.5, below the expectation of a more muted 1.3-point decline to 52.0. Similarly, the manufacturing PMI eased by 0.3 points to 50.1, which is a hair above the 50 boom-bust line. Together, weakness in both sectors pushed down the composite index to 48.9 (Chart 10). Stringent restrictions designed to halt rising rates in COVID-19 infections explain much of the deterioration in China’s service-sector activity. The sector will likely rebound in September with the easing in infection levels (Chart 11). Chart 10PMIs Show Slowing Economic Activity

PMIs Show Slowing Economic Activity

PMIs Show Slowing Economic Activity

Chart 11Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Lingering COVID Effects Curb Service-Sector Recovery In 2H21

Meanwhile, the construction PMI surprisedly rebounded sharply in August (Chart 10, bottom panel). However, investors should be cautious not to read too much into the idiosyncratic month-on-month moves suggested by the construction PMI. Instead, construction activity has moderated significantly and is set to slow further, hinting at plunged excavator sales and real estate investment in construction (Chart 12). Chart 12Construction Activity Is Unlikely To Pick Up Meaningfully This Year

Construction Activity Is Unlikely To Pick Up Meaningfully This Year

Construction Activity Is Unlikely To Pick Up Meaningfully This Year

It is clear that China’s economy is losing momentum, but greater economic weakness will be needed for policymakers to stimulate meaningfully. Export Sector Remains A Bright Spot China’s exports remain robust. Export growth picked up in August from July on a year-over-year basis. Although the improvement in August reflects a base effect, exports in level reached a new high (Chart 13). Both skyrocketed exports container freight index and strong Korean exports suggest that global demand for Chinese manufacturing goods remains resilient (Chart 14). Even though manufacturing PMIs from developed markets have rolled over, they remain elevated and should continue to support China’s exports (Chart 15). Chart 13Chinese August Exports In Level Reached A New High

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chart 14Exports Will Remain Robust In The Rest Of The Year...

Exports Will Remain Robust In The Rest Of The Year...

Exports Will Remain Robust In The Rest Of The Year...

In contrast to resilient exports, China’s official PMI export new orders subindex has declined for five consecutive months. Even though falling PMI new export orders subindex heralds a slowing in exports growth, a reading of below the 50 boom-bust threshold in the former does not suggest a contraction in the growth rate of the latter. Furthermore, the month-over-month nature of PMI new export orders subindex tends to overstate the volatility in exports. The divergence between the PMI new export orders subindex and real export growth also occurred in 2018/19 during the height of the US-China trade war when export orders were volatile (Chart 16). Chart 15...And Will Continue To Benefit From Strong Global Demand

...And Will Continue To Benefit From Strong Global Demand

...And Will Continue To Benefit From Strong Global Demand

Chart 16A Divergence Between PMI New Export Orders And Export Growth

A Divergence Between PMI New Export Orders And Export Growth

A Divergence Between PMI New Export Orders And Export Growth

Regulatory Tightening In Real Estate Sector Stringent regulations in housing since the beginning of the year have started to cool the sector (Chart 17). However, home prices inflation in tier-one cities is still elevated (Chart 18). Thus, we expect the controls on housing and among property developers will remain in place for the next 6 to 12 months. Chart 17Housing Sector Is Cooling...

Housing Sector Is Cooling...

Housing Sector Is Cooling...

Chart 18...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

...But Housing Prices In First-Tier Cities Keep Rising At A Faster Rate

Industrial Profits: Rising Prices, Falling Production China’s industrial profit growth remained solid in July despite the waning low base effect. Manufacturing producer prices continued to rise, offsetting weaker production growth (Chart 19). In addition, a low interest-rate environment helped to lift profits in the manufacturing sector by reducing debt servicing costs. While we expect weakening domestic demand and peaking producer prices to weigh on corporate profits in the rest of this year, profit growth is rolling over from a lofty height and will not likely drop sharply in the coming months (Chart 20). In addition, producer prices will likely remain at a historically high level in the next six months given robust global demand for raw materials and persistent global supply shortages. Chart 19Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Rising Prices And Low Interest Rates Helped To Offset Falling Industrial Production

Chart 20Peaking Producer Prices Will Weigh On Corporate Profits

Peaking Producer Prices Will Weigh On Corporate Profits

Peaking Producer Prices Will Weigh On Corporate Profits

Meanwhile, there is a large gap between the prices for producer goods and consumer goods, suggesting that manufacturers in mid-to-downstream industries have not been able to fully pass on rising input costs to domestic consumers (Chart 21). Profit growth continues to be disproportionally stronger in the upstream industrial producers than in the downstream industries, while the profit margin in the manufacturing sector remains much more muted (Chart 22). Chart 21Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Inflation Passthrough From Manufacturers To Domestic Consumers Remains Limited

Chart 22Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Profit Growth In Upstream Industries Still Outpaces Manufacturing Sector

Table 1

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Table 2

Chinese Small And Medium Caps Are Finding Their Shining Moment

Chinese Small And Medium Caps Are Finding Their Shining Moment

Footnotes Market/Sector Recommendations Cyclical Investment Stance

Highlights Economic policy uncertainty is rising in the US and will generate volatility this fall. But by the end of the year the result should be more fiscal reflation. Biden’s approval rating is now “underwater” – net negative – but this was expected. Unless he suffers another black eye, he can still shepherd his two big bills through Congress by year’s end. Public support for Biden’s tax hikes is weak. Some tax hikes are likely but aggressive hikes are now off the table. The midterm elections were already likely to produce a Republican win in the House. History supports this consensus. But the Senate is still an open game. The presidential election outlook is only marginally affected, at most, by the messy Afghanistan pullout. Value stocks are re-testing their low point against growth stocks. We do not expect them to break down when Congress is about to pass historic new spending increases. Feature Economic policy uncertainty is reviving in the US and set to increase this fall. This is true in absolute terms and relative to global uncertainty, even at a time when China’s sweeping regulatory crackdown is generating a lot of global uncertainty (Chart 1). Chart 1US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

US Relative Policy Uncertainty Reviving

Chart 2Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

Policy Uncertainty Breakdown

The latest increase in the policy uncertainty index is largely driven by rising uncertainty over future government spending (Chart 2, panel 2) and expiring tax provisions (Chart 2, panel 3), more so than by public sentiment reflected in the mainstream media or even the inflation debate. The looming budget battle this fall will have major implications for taxes and spending and will lift the uncertainty indicators regarding sentiment and consumer prices. Volatility will ensue in the coming months. But by the end of the year, Congress will have passed at least one, likely two, new laws that will increase government fiscal support for the economy and dispel deflationary tail risks. The lingering pandemic will if anything help concentrate lawmakers’ minds on passing more stimulus. Therefore we expect US equities and cyclical sectors to grind higher. The passage of these bills will mark the high point in policy reflation, after which clouds will loom on the horizon in 2022. Biden’s Net Negative Approval Rating President Biden’s job approval rating is now officially “underwater” – more people disapprove of his leadership than approve (Table 1). This is raising serious doubts about his ability to shepherd legislation through Congress this fall. However, these doubts are overrated. Table 1Biden’s Net Approval Is Officially Negative

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Biden’s approval has mostly fallen due to his mishandling of the US military’s withdrawal from Afghanistan – which most Americans agree was necessary, however much they deplored the commander-in-chief’s handling of it. Therefore Biden’s approval rating will not fall much farther – at least not until he suffers another black eye. Until that happens, Biden’s approval will stabilize in the range of Obama’s and above Trump’s. The reason is that he retains a solid political base of support – and his political base is larger than President Trump’s, so his general approval will stay higher. Indeed his approval is still stronger than Obama’s among Democrats (Charts 3A and 3B). This is counterintuitive since Obama was a charismatic, young, and progressive Democrat. The reason is that Democrats are still very cognizant and fearful of the alternative: President Trump. This anti-Trump tailwind will help Biden for some time. Support among Democrats is critical for maintaining party discipline in passing the reconciliation bill this fall. It is also important for the midterm elections. Chart 3ABiden’s Job Approval Collapses

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 3BBiden’s Approval Holding Up Among Democrats

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

On specific issues, Biden is weaker than Obama on foreign policy and than Trump on the economy (Charts 4A and 4B). The economy will remain the central concern, notwithstanding Afghanistan, and on this front Biden should stabilize or improve. However, other foreign policy issues could rise to the fore and hurt him at any time given today’s fraught geopolitical environment. Chart 4ABiden’s Falling Approval On Economy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 4BBiden’s Falling Approval On Foreign Policy

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

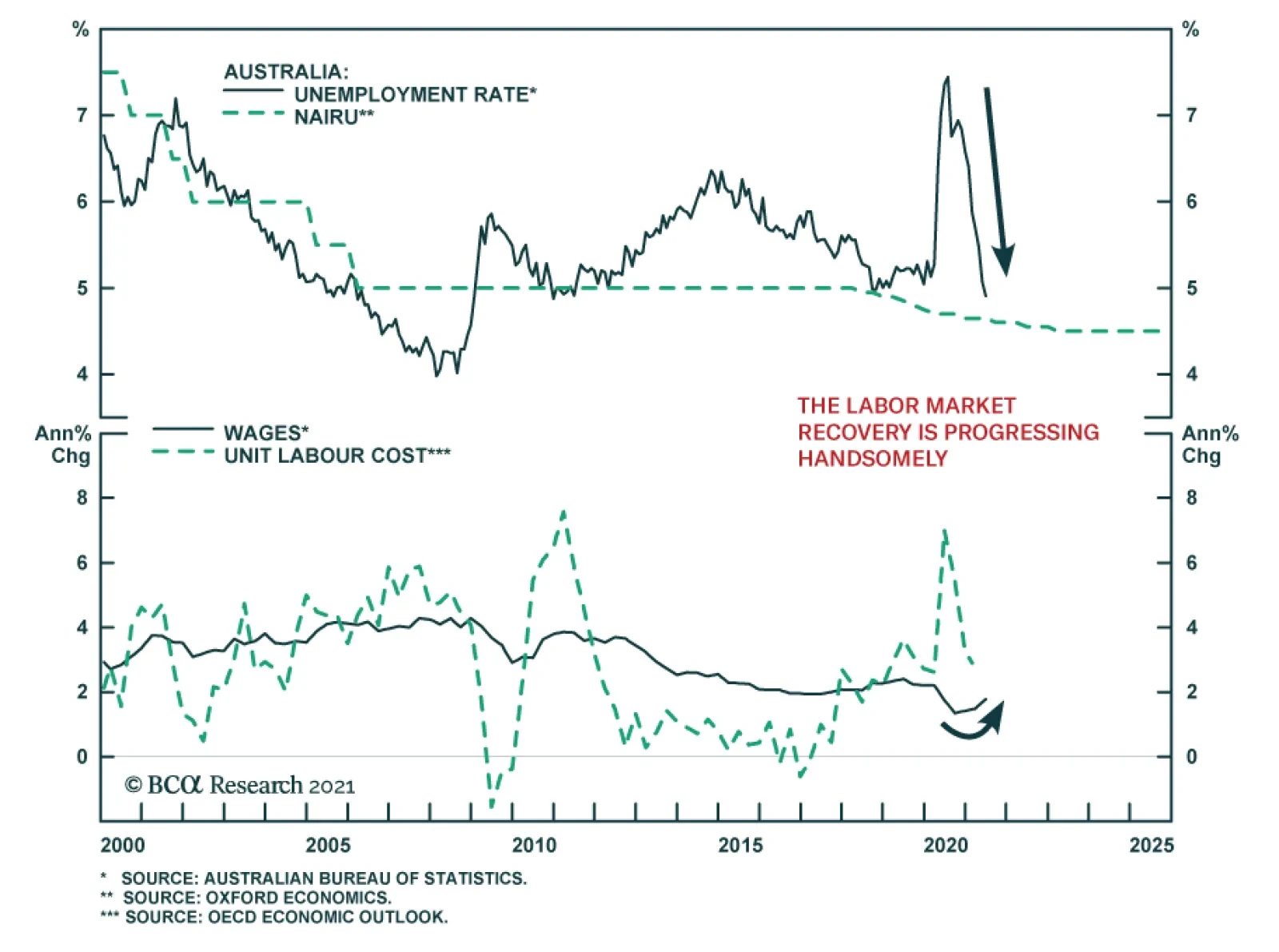

We say Biden’s score on the economy will improve because consumer confidence will rebound once the Delta variant of COVID-19 subsides (Chart 5). Both manufacturing and service sectors are performing better than when Biden was elected and employment is holding up in both sectors. The new orders-to-inventories measures suggest the service sector will continue to improve (Chart 6). The headline unemployment rate has dropped to 5.2%. Chart 5Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Consumer Confidence Should Support Biden

Chart 6PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

PMIs Also Offer Some Support For Biden

Given the above, Biden still has enough clout to steer his signature legislation through Congress this fall, albeit with major modifications to his unwieldy $3.5 trillion American Families Plan. Moderate Democratic Senator Joe Manchin of West Virginia has called for a pause in new big spending legislation, but a close look at his words shows that he does not oppose the bill, he merely wants to water it down, which is not a change from his earlier position.1 He speaks for other moderates. The left-wing faction led by Senator Bernie Sanders of Vermont will make counter-threats yet ultimately has no choice other than to support the most progressive social legislation in recent memory. The bill will be watered down. Could this watering down process result in a total jettison of the Democrats’ proposed tax hikes? The Wall Street Journal reports that congressional support for tax hikes is losing steam.2 While aggressive tax hikes are off the table, we highly doubt that all tax hikes will be removed. Financial markets have not responded much to the threat of higher taxes. Small business owners, who are most sensitive to the risk of new taxes and regulation imposed by Democrats, have not shown much concern for either issue this year – they are much more worried about inflation (Chart 7). We assume the equity market would rally if tax hikes were dropped but we do not think this is likely to happen. Americans support higher taxes – but only Democrats are enthusiastic about across-the-board hikes on individuals, corporations, and capital gains. Polls show that 59% of independent voters, not to mention Democrats, support higher taxes on high-income earners, although the proposed 28% corporate is increasingly likely to be cut down (Chart 8). This is the fundamental reason for investors to expect Democrats to band together in the eleventh hour and include tax hikes in their reconciliation bill. If nothing else, a partial reversal of President Trump’s Tax Cut and Jobs Act will be necessary to give a veneer of affordability to Biden’s giant spending bill to get it past Senate moderates. Chart 7Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Business Will Worry About Tax Hikes When (If) They Pass

Chart 8Look Out: Americans Support Higher Taxes

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

The impact of Biden’s corporate tax hike is expected to be a 5%-8% one-off hit to corporate earnings, according to our Global Investment Strategy. The impact could be less than that but the combination of popular opinion and the Democratic Party’s need to finance their social agenda suggests that investors should plan for the worst, which in this case is not that bad – key tax rates will still be lower than they were under President Obama. The chief risk to Biden’s legislation is that passing the bipartisan infrastructure bill (80% subjective odds) consumes so much political capital that there is not enough left for Biden’s reconciliation bill (50%-65% subjective odds, depending on circumstances). This is possible. Congressional Democrat leaders want to tie these two bills together but most likely the quick success of infrastructure, which is more popular than social welfare, will lead Democrats to conclude that a bird in the hand is worth two in the bush. They will pass infrastructure on less-than-perfect assurances from Senate moderates that they will support reconciliation. Then a separate battle over reconciliation will ensue, in which Biden must cajole the left-wing and moderate factions of his party into a “yea” vote while Republicans obstruct. The second major risk to Biden’s legislation – and the macro backdrop – comes if he mismanages foreign policy more generally, such as with the looming crisis over Iran. A foreign policy failure beyond Afghanistan could cause permanent damage to his political capital. And yet Democrats would be even more desperate for a legislative victory then, as they would face a wipeout in the midterm elections if they had no legislative victories and two foreign policy humiliations. In other words, Biden is nowhere near so unpopular that moderate Democrats will abandon his signature legislative agenda and condemn their party and his administration to a heavy defeat in 2022. Bottom Line: Biden’s legislation will pass, including some tax hikes. The revised magnitude of tax hikes will not be known until later this fall when the Senate and House start producing legislative text. Policy uncertainty and equity volatility will trend upward this fall but the end-game is more reflationary policy, which should keep equities grinding higher at least through Christmas. Midterm Elections: The Best Case For Democrats Is Not Good Enough Are Republicans more likely to take Congress now that Biden’s approval is underwater? How would this impact the policy and macroeconomic outlook? While Republicans are highly likely to retake the House of Representatives, the Senate is still slightly tipped for the Democrats. Biden would have to fail to pass legislation or commit another major policy mistake to give Republicans full control of Congress, although this outcome is slightly favored in online betting markets. The House currently consists of 220 Democrats and 212 Republicans. There is always some fluctuation in the exact numbers. Three vacancies should be filled in November’s special elections, which could bring the count to 222 Democrats and 213 Republicans.3 With 218 votes needed to pass legislation on an absolute majority vote, Democrats can only afford to lose three votes at present. This is an extremely tight margin and shows that this fall’s reconciliation bill is at risk in the House as well as the Senate. In the midterm elections, Republicans only need to take five-to-six seats to regain the majority (218). This is easy on paper: the average seat gain for the opposition in midterm House elections is 35. Biden’s latest approval rating puts Democrats in line to lose 37 seats based on history. The opposition typically makes gains in the midterm because it is fired up whereas the presidential party is complacent. In addition Republicans are expected to gain two seats (possibly as many as four) via gerrymandering in 2022. True, Democrats have some underrated supports in 2022. In all probability the pandemic will be waning while the economy will be waxing. Biden will likely have passed at least a bipartisan infrastructure deal. The divisions within Republican ranks over Trumpism will also persist, which may or may not increase Democratic turnout and vote-switching from suburban Republicans. Hence it is reasonable to ask whether Democrats could surprise to the upside and retain the House. Online betting markets put the probability at 29%, and these odds make sense to us. The historical record helps to define what kind of events might alter the outlook for the midterms. Table 2 shows the midterm elections in which the presidential party performed best (the opposition party disappointed the historical norm). The following points are salient: Table 2Best-Case Outcomes For Presidential Party In Midterm Elections

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

There are only two cases in which the presidential party gained seats (Clinton 1998, Bush 2002) and three cases in which they only lost a few seats (Kennedy 1962, Reagan 1986, arguably Bush 1990). The Democratic victory of 1998 occurred at the top of an economic boom while the Republican victory of 2002 occurred one year after the 9/11 terrorist attacks. Neither is likely to be replicated for Democrats in 2022. Republicans’ mild losses in 1990 occurred just after Iraq invaded Kuwait. Republican’s mild losses in 1986 occurred despite a big legislative victory (tax reform). If either of the last two scenarios played out for Democrats in 2022, Democrats would likely lose the House by a whisker. Only if the Democrats’ 1962 scenario played out would Democrats retain the House in 2022, and only by a single seat. Yet the 1962 election occurred in the midst of the Cuban Missile Crisis! The takeaway is that a foreign policy crisis could help Democrats pare their losses in the midterms if Biden is deemed to have handled the crisis adroitly. But even then the ruling party would likely lose the House judging by history. Needless to say these are just historical examples. They also show that Democratic fortunes could turn around drastically between now and next fall (e.g. Kennedy went from a recession and the Bay of Pigs fiasco to gaining his party seats). The Senate outlook is less straightforward. Biden’s approval rating suggests a loss of four seats for Democrats based on the historical pattern. But the same pattern suggested Republicans would lose four seats in 2018 and instead they gained two. Our quantitative Senate election model, which we update every week in the Appendix, still tips the Democrats to gain one seat (a 51-49 majority) or at least retain their de facto one seat majority (50-50). Chart 9Presidential Vetoes In History

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

What are the macroeconomic implications? A Republican House and Democratic White House would play “constitutional hardball,” just as occurred from 2011-14, given that the country is still at historically peak levels of political polarization.4 There are likely to be critical differences between 2011 and 2023 – populism has fundamentally weakened support for fiscal austerity – but the most likely result is gridlock and deadlock. Republicans will not be able to slash spending or cut taxes as Biden will have the presidential veto, but Democrats will not be able to increase spending or hike taxes (Chart 9). The problem for Biden would be the need to avoid a national default when and if the Republicans insist on spending cuts to raise the debt ceiling. The looming debt ceiling showdown this fall will increase uncertainty and volatility but ultimately Democrats have the votes to avoid a default. That would not necessarily be the case if Republicans controlled the House. And this time around Republicans could be driven to impeach the president, for whatever reason, in retaliation for President Trump’s impeachment in 2019. This situation obviously cannot be ruled out, even though it would be virtually impossible for the Senate to convict. At the same time, some bipartisanship could occur, as it did under Trump following the 2018 midterms. Anti-trust legislation and immigration reform are the two most important policy areas to watch on this front. Republican gains in Congress would marginally weaken the Democrats’ hold on the White House in 2024, though we continue to believe that Democrats are favored. American voters are likely to be better off in November 2024 than they were in November 2020, amid a pandemic, recession, and nationwide social unrest. Our quantitative model tips Democrats with 308 electoral votes (Appendix). Professor Allan Lichtman’s “13 Keys” to the presidency – a nearly flawless prediction system since 1984 – currently suggest that the Democrats only have three keys turned against them. They would need to see six or more in order to lose the White House (Table 3). Obviously the long-term status of the economy will be a critical factor (Chart 10). Table 3Lichtman’s Keys To The Presidency (Updated Sept 2021)

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart 10Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Will Biden's Economy Grow Faster Than That Of His Two Predecessors?

Bringing it all together, US fiscal policy has taken a more proactive turn but it is still likely to freeze after this fall. It will be hard to pass major budget bills in 2022 ahead of the election and gridlock is the likeliest outcome, making 2025 the next realistic chance for major fiscal changes. The immediate implication is that Biden and Democratic leaders will have to disconnect the bipartisan infrastructure bill from the partisan social welfare reconciliation bill this autumn. This will require a major concession from House Speaker Nancy Pelosi. Otherwise both bills could collapse and with them the Democratic Party’s fortunes. Biden and moderate Democrats that face competitive races in 2022 will demand a quick victory before moving onto the less popular part. Investment Takeaways Value stocks are re-testing their cycle lows against growth stocks (Chart 11). The Delta variant and global growth jitters continue to weigh on this trade. Chart 11S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

S&P Value Re-Tests Lows Versus Growth

The S&P 500’s “Big Five” are rallying and outperforming the other 495 companies once again (Chart 12). Chart 12S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

S&P 5 Recovery Versus 495

We expect politically induced volatility throughout the fall but we also expect it to be resolved in new and reflationary legislation. Signs that Biden’s legislation will pass should enable cyclical sectors and value stocks to recover, though the pandemic, global growth, and Chinese stability may prevent them from outperforming defensive sectors and growth stocks. A new set of hurdles will face markets if Republicans regain the House and halt fiscal easing from 2022-24. However, they will not be rewarded by voters if they create a fiscal or economic crisis, implying that the proactive fiscal turn in public opinion will prevail over the long run. If Biden’s legislation fails then it suggests that US fiscal policy is dysfunctional even under single-party control. This would heighten the deflationary tail risk and force us to reassess our macro and policy outlook. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1USPS Trade Table

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A2Political Risk Matrix

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A1Presidential Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Chart A2Senate Election Model

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A3Political Capital Index

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4APolitical Capital: White House And Congress

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4BPolitical Capital: Household And Business Sentiment

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Table A4CPolitical Capital: The Economy And Markets

Biden Is Underwater But His Legislation Will Float

Biden Is Underwater But His Legislation Will Float

Footnotes 1 See Senator Joe Manchin, “Why I Won’t Support Spending Another $3.5 Trillion,” Wall Street Journal, September 2, 2021, wsj.com. 2 Richard Rubin, “Progressives’ Tax-The-Rich Dreams Fade As Democrats Struggle For Votes,” Wall Street Journal, September 5, 2021, wsj.com. 3 The three special House elections are: Florida’s 20th District, previously Democratic held; Ohio’s 11th District, previously Democratic held; Ohio’s 15th District, previously Republican held. 4 See Mark V. Tushnet, “Constitutional Hardball,” John Marshall Legal Review 37 (2004), pp. 523-53, scholarship.law.georgetown.edu.

Highlights Chart 1Employment Growth Will Rebound

Employment Growth Will Rebound

Employment Growth Will Rebound

August’s weak employment growth reflects the surge of Delta variant COVID cases in the United States. This is evidenced by the fact that Leisure & Hospitality sector payrolls held flat in August after having grown by 415k in July and 397k in June (Chart 1). While Delta could still be a drag on employment growth for another month or two, there is mounting evidence that the daily new case count is close to its peak. Leisure & Hospitality employment growth will regain its prior pace as new Delta cases trend down. This will lead to a resumption of strong monthly payroll reports (500k – 1000k) as we head into the new year. For monetary policy, we calculate that average monthly nonfarm payroll growth of 414k will be sufficient for the Fed to start rate hikes before the end of 2022 (bottom panel). We anticipate that this threshold will easily be met. The Treasury curve will bear-flatten as employment growth improves and the market prices-in an earlier start and quicker pace of Fed rate hikes. Investors should maintain below-benchmark portfolio duration and stay short the 5-year Treasury note versus a duration-matched 2/10 barbell. Feature Table 1Recommended Portfolio Specification

The Delta Drag

The Delta Drag

Table 2Fixed Income Sector Performance

The Delta Drag

The Delta Drag

Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds underperformed the duration-equivalent Treasury index by 5 basis points in August, dragging year-to-date excess returns down to +166 bps. The combination of above-trend economic growth and accommodative monetary policy supports continued positive excess returns for spread product versus Treasuries. At 91 bps, the 3-year/10-year Treasury slope remains steep. This is a strong signal that monetary conditions are accommodative. But despite the positive macro back-drop, investment grade valuations are extremely tight (Chart 2). A recent report looked at what different combinations of Treasury slope and corporate spreads have historically signaled for corporate bond excess returns.1 It shows that tight corporate spreads only correlate with negative excess returns once the 3-year/10-year Treasury slope is below 50 bps. Though we retain a positive view of spread product as a whole, better value can be found outside of the investment grade corporate sector. Specifically, we recommend that investors shift into high-yield corporates, municipal bonds and USD-denominated Emerging Market sovereigns and corporates. We also advise investors to favor long-maturity corporate bonds and those corporate sectors with elevated Duration-Times-Spread.2 Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

The Delta Drag

The Delta Drag

Table 3BCorporate Sector Risk Vs. Reward*

The Delta Drag

The Delta Drag

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 66 basis points in August, bringing year-to-date excess returns up to +502 bps. A recent report looked at the default expectations that are currently priced into the junk index and considered whether they are likely to be met.3 If we demand an excess spread of 100 bps and assume a 40% recovery rate on defaulted debt, then the High-Yield index embeds an expected default rate of 3.0% (Chart 3). Using a model of the 12-month trailing speculative grade default rate that is based on gross corporate leverage (pre-tax profits over total debt) and C&I lending standards, we estimate that the 12-month default rate will fall to between 2.3% and 2.8%, below what the market currently discounts. Notably, the corporate default rate is tracking at an annualized rate of roughly 1.7% through the first seven months of the year, well below the estimate generated by our macro model. Another recent report looked at the incremental spread pick-up investors can earn by moving out of investment grade corporates and into junk.4 It concluded that the extra spread available in high-yield is worth grabbing and that B-rated bonds look particularly attractive in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 3 basis points in August, dragging year-to-date excess returns down to -67 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries tightened 4 bps in August. The spread is wide compared to recent history, but it remains tight compared to the pace of mortgage refinancings (Chart 4). The conventional 30-year MBS option-adjusted spread (OAS) widened 2 bps in August (panel 2), and it is now starting to look attractive compared to other similarly risky spread sectors. The conventional 30-year MBS OAS sits at 38 bps, below the 56 bps offered by Aa-rated corporate bonds but above the 20 bps offered by Aaa-rated consumer ABS and the 35 bps offered by Agency CMBS. In a recent report we looked at MBS performance and valuation across the coupon stack.5 We noted that the higher convexity of high-coupon MBS makes them likely to outperform lower-coupon MBS in a rising yield environment. Higher coupon MBS also have greater OAS than lower coupons. This makes the high-coupon MBS more likely to outperform in a flat bond yield environment as well. Given our view that bond yields will be higher in 6-12 months, we recommend favoring high coupons (4%, 4.5%) over low coupons (2%, 2.5%, 3%) within an overall underweight allocation to Agency MBS. Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index outperformed the duration-equivalent Treasury index by 27 basis points in August, bringing year-to-date excess returns up to +84 bps (Chart 5). Sovereign debt outperformed duration-equivalent Treasuries by 122 bps in August, bringing year-to-date excess returns up to +7 bps. Foreign Agencies outperformed the Treasury benchmark by 8 bps on the month, bringing year-to-date excess returns up to +44 bps. Local Authority bonds outperformed by 9 bps in August, bringing year-to-date excess returns up to +382 bps. Domestic Agency bonds outperformed by 3 bps, bringing year-to-date excess returns up to +30 bps. Supranationals outperformed by 5 bps, bringing year-to-date excess returns up to +31 bps. USD-denominated Emerging Market (EM) Sovereign bonds outperformed US corporates in August and relative valuation between the two sectors is starting to equalize (panel 4). That said, we retain a preference for EM sovereigns over US corporates, particularly the bonds of Russia, Mexico, Saudi Arabia, UAE and Qatar where value remains attractive. A recent report looked at valuation within the investment grade USD-denominated EM corporate space.6 It found that EM corporates are attractively priced relative to US corporate bonds across the entire investment grade credit spectrum. It also found that EM corporates are attractive relative to EM sovereigns within the A and Baa credit tiers. EM sovereigns have the edge in the Aa credit tier. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 9 basis points in August, dragging year-to-date excess returns down to +262 bps (before adjusting for the tax advantage). The economic and policy back-drop remains favorable for municipal bond performance. Trailing 4-quarter net state & local government savings were already positive through the end of Q1 2021 and they received another significant boost in Q2 as funds from the American Rescue Plan were doled out (Chart 6). With state & local government balance sheets in such good shape, we are comfortable moving down in quality within municipal bonds. A move down in quality is especially compelling because of tight Aaa muni valuations relative to Treasuries (top panel). Valuation is more compelling in the lower investment grade credit tiers, especially at the long-end of the curve.7 GO munis in the 12-17 year maturity bucket offer a 5% breakeven tax rate versus corporates with the same credit rating and duration. 12-17 year Revenue munis actually offer a before-tax yield pick-up (panel 2). Finally, high-yield muni spreads are reasonably attractive relative to high-yield corporates, offering a breakeven tax rate of 23% (panel 4). But despite the attractive spread, we recommend only a neutral allocation to high-yield munis versus high-yield corporates as the deep negative convexity of high-yield munis makes them susceptible to extension risk if bond yields rise. Treasury Curve: Buy 2/10 Barbell Versus 5-Year Bullet Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved higher in August, with the 5-year and 7-year maturities bearing the brunt of the sell-off. The 2-year/10-year Treasury slope steepened 5 bps to end the month at 110 bps. The 5-year/30-year slope flattened 5 bps to end the month at 115 bps. We expect bond yields to be higher in 6-12 months, but we also anticipate that the next significant move higher in bond yields will coincide with curve flattening, not steepening. At 1.93%, the 5-year/5-year forward Treasury yield is not that far below our target fair value range of 2% - 2.25%. In a recent report, we demonstrated that yield curve steepening only occurs when either the Fed is cutting rates or the 5-year/5-year forward yield rises.8 This means that the 2/10 Treasury curve is more likely to flatten than steepen during the next 6-12 months, even as bond yields move higher. Similarly, we observe that the overnight index swap (OIS) curve is priced for the fed funds rate to be 0.21% in one year’s time and 1.47% in five years (Chart 7). The latter rate has 146 bps of upside if it converges all the way back to its 2018 high, but this pales in comparison to the 265 bps of upside in the 12-month forward rate. The yield curve will flatten as the 12-month forward OIS rate converges with the 5-year forward rate (panel 3). Investors should position in yield curve flatteners on a 6-12 month horizon. Specifically, we recommend shorting the 5-year bullet versus a duration-matched 2/10 barbell. TIPS: Neutral Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS performed in line with the duration-equivalent nominal Treasury index in August, leaving year-to-date excess returns unchanged at +578 bps. The 10-year and 5-year/5-year forward TIPS breakeven inflation rates both fell by 7 bps in August. At 2.37%, the 10-year TIPS breakeven inflation rate is near the middle of the 2.3% to 2.5% range that is consistent with inflation expectations being well anchored around the Fed’s target (Chart 8). Meanwhile, at 2.21%, the 5-year/5-year forward TIPS breakeven inflation rate is only just below target (panel 3). With long-dated inflation expectations close to the Fed’s target levels, we see limited upside on a 6-12 month investment horizon. We also see the cost of short-maturity inflation protection falling during the next few months as realized inflation continues to moderate from its current extremely high level. This will lead to some modest steepening of the inflation curve (bottom panel). While the inflation curve has some room to steepen, we don’t see it returning to positive territory. An inverted inflation curve is simply more consistent with the Fed’s Average Inflation Target than a positively sloped one. This is because the Fed’s new framework calls for it to attack its inflation target from above rather than from below. ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in August, bringing year-to-date excess returns up to +40 bps. Aaa-rated ABS outperformed by 2 bps on the month, bringing year-to-date excess returns up to +30 bps. Non-Aaa ABS outperformed by 4 bps, bringing year-to-date excess returns up to +92 bps. The stimulus from last year’s CARES Act led to a significant increase in household savings when individual checks were mailed in April 2020. That excess savings has still not been spent and the most recent round of stimulus checks has only added to the stockpile (Chart 9). The extraordinarily large stock of household savings means that the collateral quality of consumer ABS is also extraordinarily high. Indeed, many households have been using their windfalls to pay down consumer debt (bottom panel). Investors should remain overweight consumer ABS and should also take advantage of the high quality of household balance sheets by moving down the quality spectrum. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 6 basis points in August, bringing year-to-date excess returns up to +193 bps. Aaa Non-Agency CMBS outperformed Treasuries by 10 bps in August, bringing year-to-date excess returns up to +92 bps. Non-Aaa Non-Agency CMBS underperformed Treasuries by 9 bps on the month, dragging year-to-date excess returns down to +529 bps (Chart 10). Though returns have been strong and spreads remain attractive, particularly for lower-rated CMBS, we continue to recommend only a neutral allocation to the sector because of the structurally challenging environment for commercial real estate. Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 4 basis points in August, bringing year-to-date excess returns up to +91 bps. The average index option-adjusted spread held flat on the month. It currently sits at 35 bps (bottom panel). Though Agency CMBS spreads have recovered to well below pre-COVID levels, they still look attractive compared to other similarly risky spread products. Stay overweight. Ryan Swift US Bond Strategist rswift@bcaresearch.com Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 12 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 12 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

The Delta Drag

The Delta Drag

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of August 31st, 2021)

The Delta Drag

The Delta Drag

Footnotes 1 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 2 For ideas on how to increase the average spread of a US bond portfolio please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 3 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 4 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 5 Please see US Bond Strategy Weekly Report, “A New Conundrum”, dated April 20, 2021. 6 Please see US Bond Strategy Weekly Report, “The Post-FOMC Credit Environment”, dated June 29, 2021. 7 Please see US Bond Strategy Weekly Report, “The Collapsing Credit Risk Premium”, dated July 20, 2021. 8 Please see US Bond Strategy / Global Fixed Income Strategy Weekly Report, “A Bump On The Road To Recovery”, dated July 27, 2021.

The Reserve Bank of Australia maintained its benchmark cash rate target unchanged at 0.1% at its meeting on Tuesday. Instead, the central bank announced a reduction in the pace of its asset purchases to AUD 4 billion a week from the previous AUD 5 billion. …

Highlights A trio of ECB hawks raised the prospect of an ECB taper. In the past, the current set of economic conditions in the Euro Area would have prompted the ECB to tighten policy. A potential economic deceleration this fall, the transitory nature of the Eurozone’s inflation spike, and the level of inflation expectation in the region limit the ECB’s ability to taper this week. We expect a one-off return to the pre-Q2 2021 level of asset purchases couched in a very dovish forward guidance. Peripheral bonds and European corporate bonds will outperform German and other core European paper. Stay long European curve steepeners, while buying US curve flatteners. Overweight German Bunds versus US Treasury Notes, on a USD-hedged basis. European productivity will remain structurally hampered compared to that of the US. US real bond yields will rise relative to Europe. Feature Last week, a chorus of ECB Governing Council members raised the idea among investors that the central bank may soon begin to taper its asset purchases, which prompted Bund yields to hit -0.35% on Wednesday. Robert Holzmann of Austria, Klaas Knot of the Netherlands, and Jens Weidmann of Germany all suggested that monetary conditions were too accommodative for the Eurozone and that the ECB needed to remedy this problem. The complaints of this hawkish trio reflect the current environment. In August, the Eurozone HICP reached a 3% annual rate while the preliminary estimate for core CPI clicked in at 1.6%. Meanwhile, July PPI rose to 12.1%. Such robust inflation readings are at odds with the low level of interest rates in the Eurozone, where the yields on European IG credit and 10-year Italian BTPs average a paltry 0.45% (Chart 1). Beyond the level of inflation, its broad geographic nature is an additional source of concern. Headline CPI is accelerating across all the bloc’s nations, and it stands above 2% in 82% of the members’ states. Historically, this kind of inflationary backdrop resulted in either higher interest rates or some tapering of asset purchases, especially when economic activity was also improving in the Eurozone (Chart 2). Chart 1A Gap For The Hawks

A Gap For The Hawks

A Gap For The Hawks

Chart 2In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

In The Past, The ECB Would Have Tightened

Will the ECB listen to its most hawkish members and follow its past script? We do not believe that the Governing Council is about to start a sustained period of decreased bond buying, even if a return to the pre-Q2 2021 pace of buying is likely this fall. Thus, a dovish taper is the most likely outcome of this week’s meeting. The ECB’s Three Constraints The outlook for growth, the temporary nature of the current spike in European inflation, and the low-level of Euro Area inflation expectations limit the ECB’s ability to remove monetary accommodation. First, European economic growth is at its apex and will decelerate over the next six months. Currently, domestic activity as approximated by the Services PMI stands at near a 15-year high of almost 60. Moreover, despite the spike in COVD-19 cases linked to the Delta variant, mobility remains very robust. If anything, the decline in cases in Spain and France should lead to further improvement in mobility (Chart 3). Nonetheless, the recent fall in consumer confidence and the recent US experience, which the European economy usually follows, point to a deceleration in the Services PMI. The case for a decline in manufacturing activity is more pronounced. The European manufacturing sector responds strongly to the fluctuation of the global industrial sector. US consumer spending on durable goods is 21% above its pre-pandemic trend and is beginning to weaken as pent-up demand for such products has been satiated and households shift their spending back toward services. Moreover, the Chinese credit cycle, which leads the Eurozone Manufacturing PMI by nine months, indicates a greater deceleration in the coming quarters, because European exports to China will slow (Chart 4, top and middle panels). In response to these two forces, Europe will not diverge from the deterioration in our Global Activity Nowcast (Chart 4, bottom panel). Chart 3So Far, No Delta Impact

So Far, No Delta Impact

So Far, No Delta Impact

Chart 4The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

The Coming Manufacturing Slowdown

Chart 5Abnormal Goods Inflation

Abnormal Goods Inflation

Abnormal Goods Inflation

Second, most evidence still suggests that the current inflation increase will be temporary, despite its violence. To begin with, the spike in inflation remains consigned to the goods sectors, while services inflation stands at 1.1%, in line with the experience of the past 10 years (Chart 5). Even within goods prices, the spike in CPI is limited to sectors facing bottlenecks or linked closely to commodity and shipping prices. As Chart 6 illustrates, the categories experiencing abnormal inflation are directly related to higher energy prices, cars, complex machinery, hotels, and fresh food. Meanwhile, underlying inflation as estimated by our trimmed-mean CPI measure is bottoming, but remains at a very low 0.2% annual rate (Chart 7). Chart 6Inflation Remains A Commodity and Bottleneck Story

The ECB Taper Dilemma

The ECB Taper Dilemma

In the same vein, the surge in Selling Price Expectations of the European Commission Business Survey is a function of commodity inflation (Chart 8). In other words, companies feel they can increase their selling prices, because natural resource prices have spiked. However, inflation across many commodities is currently peaking, which suggests that Selling Price Expectations will soon do so as well. Moreover, this process indicates that headline inflation should hit its summit by year end, because Selling Price Expectations are a coincident indicator of inflation (Chart 8, bottom panel). Chart 7Narrow Inflation

Narrow Inflation

Narrow Inflation

Chart 8Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

Rising Selling Prices And Commodities

A wage-inflation spiral also remains far away. Historically, rapidly accelerating wage growth marked periods of elevated inflation. Despite current fears, such a development is not taking place in the Eurozone. For the whole bloc, negotiated wages are growing at a modest 1.7% annual rate (Chart 9). Even in Germany, negotiated wages are only increasing at the same rate. While some labor shortages have been reported, total hours worked remain below the equilibrium level based on the Euro Area demographic profile (Chart 9, bottom panel). Furthermore, the past ten years reveal that labor shortages only caused stronger salary growth with a multi-year delay. Third, the market doubts the credibility of the ECB when it comes to achieving a 2% inflation target. So far, survey-based inflation expectations remain below 2% at all tenors (Chart 10, top panel). The same is true of market-based measures, which are still lower than the levels that prevailed before the sovereign debt crisis of the past decade (Chart 10, bottom panel). Chart 9No Wages/Inflation Spiral

No Wages/Inflation Spiral

No Wages/Inflation Spiral

Chart 10The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

The ECB's Inflation Mandate Is Not Yet Credible

Bottom Line: Risks to growth over the winter, the transitory nature of the recent inflation shock, and inflation expectations that remain significantly below target are constraints limitating the ability of the ECB to announce a true tapering of its asset purchases this Thursday. A Dovish Taper? Considering the current set of conditions prevailing in the Eurozone, we expect the ECB to announce a return to the pace of asset purchases that existed prior to Q2 2021. However, the Governing Council (GC) will go out of its way to issue clear forward guidance that strongly indicates this is not the beginning of a taper campaign. Instead, the GC will hint at the transmutation of a large proportion of the PEPP monthly buying into the PSPP after March 2022. The inflation target change enacted at the conclusion of the ECB’s strategy review in July limits the central bank’s ability to go back to its old rule book and tighten policy at the first hint of inflation. First, the ECB must believe that inflation will overshoot 2% on a durable basis, which will necessitate an upgrade to its long-term inflation forecast above the target. Too many members of the GC do not share this view, which makes it unlikely that inflation forecasts will rise this much this week. Moreover, inflation expectations are also too low to warn of a meaningful change in the behavior of European economic agents, especially if the current spike in inflation proves to be transitory. Another problem for the ECB is the Fed. If the ECB were to announce a durable tapering of its asset purchase this week, it would be doing so ahead of the Fed. The GC fears that this action would put considerable upward pressure on EUR/USD, which would create a grave deflationary tendency in the Eurozone (Chart 11). Despite these shackles, the ECB will also acknowledge that the current emergency pace of asset purchases is no longer warranted. Starting Q2 2021, the ECB increased its average monthly purchase from EUR80 billion in the August 2020 to March 2021 period, to EUR95 billion since April 2021 (Chart 12). However, these increased purchases followed a 0.1% GDP contraction in Q1 in the wake of a spike in COVID-19 cases and deaths, which prompted a large reduction in mobility. Moreover, the larger bond buying also followed large increases in bond yields across the main economies of the continent, a rise which, if it had been left unchecked, would have exacerbated the economic malaise. Chart 11The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

The ECB Fears A Strong Euro

Chart 12Normalizing Purchases

The ECB Taper Dilemma

The ECB Taper Dilemma

None of these factors are still present. The increasing level of vaccination has dulled the economic impact of the third wave of infection. The economy is expanding robustly and, even if it slows in the months ahead, growth will remain well above trend. Crucially, financial conditions are much more generous than in the first half of the year, with a euro that trades 4% below its January peak and with yields in the bloc’s four largest economies 25 to 45 basis points below their spring peaks. Bottom Line: In response to the aforementioned crosscurrents, we anticipate the ECB to announce a return of its monthly asset purchases to the level that prevailed in the August 2020 to March 2021 period. However, the GC will also clearly indicate, as it did last March, that this policy shift is a one-off, and that investors must not anticipate any further curtailment of asset purchases over the next six months. To reinforce this guidance, we expect the ECB’s inflation forecast to show a return of HICP below 2% by the end of 2023. The GC might also hint at the roll-over of the PEPP program into the PSPP after March 2022. Investment Implications An ECB that conducts a dovish taper on Thursday will support our main fixed-income themes in Europe. First, it will remain a tailwind behind an overweight position in peripheral government bonds versus German bonds. The combination of continued purchases of EUR80 billion a month of bonds over the foreseeable future, above-trend growth, and the fiscal risk mutualization from the NGEU and REACT EU programs means that investors can continue to safely pocket the yield premium offered by BTPs and BONOs. Moreover, our geopolitical strategists expect a left-wing coalition to govern Germany after the September 26 election, which will limit the pressures to tighten budgets in the periphery over the coming years. Chart 13European Corporates Remain Attractive

European Corporates Remain Attractive

European Corporates Remain Attractive