Policy

Dear Client, We will be presenting our quarterly webcast next week, and, as a result, will not be publishing on 29 July 2021. We will cover our major calls for the quarter and provide a look-ahead. I look forward to the Q+A, and am hopeful you will tune in. Bob Ryan Chief Commodity & Energy Strategist Highlights Chart Of The WeekOPEC 2.0's Hand Strengthened By Production Agreement

OPEC 2.0s Hand Strengthened By Production Agreement

OPEC 2.0s Hand Strengthened By Production Agreement

The deal crafted by OPEC 2.0 over the weekend to add 400k b/d of oil every month from August preserves the coalition, and sends a credible signal of its ability to raise output after its 5.8mm b/d of spare capacity is returned to market next year.1 KSA and Russia will remain primi inter pares, but the position of OPEC 2.0's core producers – not just the UAE, which negotiated an immediate baseline increase – was enhanced for future negotiations. This deal explicitly recognizes they are the only ones capable of increasing output over an extended period. We assume the revised production baselines for core OPEC 2.0 effective May 2022 reflect the coalition's demand expectations from 2H22 onward. Our modeling indicates core OPEC 2.0's output will almost converge on the revised baseline production of 34.3mm b/d by 2H23, when we expect these producers to be at ~ 33.4mm b/d. Holding our demand estimates constant from last week, our revised supply expectations prompt us to move our forecast closer to our June forecast. We expect Brent to average $70/bbl in 2H21, with 2022 and 2023 averaging $74 and $80/bbl (Chart of the Week). Feature The deal concluded by OPEC 2.0 over the weekend will do more than add 400k b/d of spare capacity to the market every month beginning next month. It also does more than preserve the producer coalition's successful production-management strategy. The big take-away from the deal is the clear message being sent by the coalition's core members – KSA, Russia, Iraq, UAE and Kuwait – that they are able to significantly increase output after their 5.8mm b/d of spare capacity has been returned to the market over the next year or so. It does so by raising the baselines of the core producers starting in May 2022, clearly indicating the capacity and willingness to raise output and keep it there (Table 1). Table 1Baseline Increases For Core OPEC 2.0

OPEC 2.0's Forward Guidance In New Baselines

OPEC 2.0's Forward Guidance In New Baselines

What OPEC 2.0's Deal Signals Internally, the deal is meant to recognize the investment made by the UAE in particular, which was not being accounted for in its current baseline. Externally – i.e., to competitors outside the coalition – the deal signals OPEC 2.0's successful production management strategy will continue, by raising the likelihood the coalition will remain intact. This has kept the level of supply below demand over the course of the COVID-19 pandemic (Chart 2), and is responsible for the global decline in inventories (Chart 3). Chart 2OPEC 2.0 Durability Increases

OPEC 2.0 Durability Increases

OPEC 2.0 Durability Increases

Chart 3Inventories Will Remain Under Control

Inventories Will Remain Under Control

Inventories Will Remain Under Control

Specifically, the massive spare capacity still to be returned to the market between now and 2H22 can be accomplished with minimal risk of a market-share war breaking out among the core OPEC 2.0 members seeking to monetize their off-the-market production before the other members of the coalition. Most importantly, the revised benchmark production levels that becomes effective May 2022 signal the coalition members with the capacity to increase production can do so. Longer-Term Forward Guidance We assume the revised production baselines for core OPEC 2.0 effective May 2022 reflect the coalition's demand expectations from 2H22 onward. Our modeling indicates core OPEC 2.0's output will approach the revised baseline reference levels of 34.3mm b/d, hitting 33.4mm b/d for crude and liquids output by 2H23 (Table 2). Table 2BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances) To Dec23

OPEC 2.0's Forward Guidance In New Baselines

OPEC 2.0's Forward Guidance In New Baselines

This implies the core group expects to be able to cover production declines within the coalition and to meet demand increases going forward. The estimates are far enough into the future to prepare ahead of time to increase production. Our estimates for core OPEC 2.0 production reflects our assumption the revised baseline levels do reflect demand expectations of the coalition. In estimating the coalition's production, we rely on historical data from the US EIA, which allows us to estimate future production using regressors we consider reliable (e.g., GDP estimates from the IMF and World Bank). Non-OPEC 2.0 Production We use EIA historical data for non-OPEC 2.0 production as well. In last week’s balances, we substituted the EIA's estimates for non-OPEC 2.0 producers ex-US for our estimates, which resulted in lower supply numbers throughout our forecast sample. This threw off our balances estimates in particular, as we did not balance the decrease in supply from this group using the new data set with an increase from another group. We corrected this oversight this week: We will continue to use EIA estimates for non-OPEC 2.0 ex-US countries, but will balance the decrease in oil production from this cohort with increased supply from other countries. Chart 4US Shales Are The Marginal Barrel

US Shales Are The Marginal Barrel

US Shales Are The Marginal Barrel

For US oil production, we will continue to estimate it as a function of WTI price levels, the forward curve and financial variables – chiefly high-yield rates, which serve as a good proxy for borrowing costs for the marginal US shale producer, which we view as the quintessential marginal producer in the global price-taking cohort (Chart 4). Our research indicates US shale producers – like all producers, for that matter – are prioritizing shareholder interests first and foremost. This means they will focus on profitability and margins. While we have observed this tendency for some time, it appears it is gaining speed, as oil and gas producers are now considering whether they want to retain their existing exposure to their hydrocarbon assets.2 There appears to be a reluctance among resource producers generally – this is true in copper, as we have noted – to substantially increase capex. This could be the result of covid uncertainty, demand uncertainty, monetary-policy uncertainty or a real attempt to provide competitive returns. We think it is a combination of all of these, but the picture is clouded by the difficulty in separating all of these uncertainties. Income Drives Oil Demand Chart 5Income Drives Oil Demand

Income Drives Oil Demand

Income Drives Oil Demand

Our demand estimates will continue to be driven by estimates of GDP from the IMF and the World Bank. We have found the level of oil consumption is highly correlated with GDP, particularly for EM states (Chart 5). Holding our demand estimates constant from last week, our revised supply expectations prompt us to move our forecast closer to our June forecast. This week, we also will adjust our inventory calculations, which will rely less on EIA estimates of OECD stocks. In the recent past, these estimates played a sizeable role in our forecasts. From this month on, they will play a smaller part. This is why, even though our supply estimates have risen from last week, there is not a significant change to our inventory levels. Investment Implications Holding our demand estimates constant from last week, our revised supply expectations prompt us to move our forecast closer to our June forecast. We expect Brent to average $70/bbl in 2H21, with 2022 and 2023 averaging $74 and $80/bbl. We remain bullish commodities in general, given the continued tightness in these markets. We expect this to persist, as capex remains elusive in oil, gas and metals markets. This underpins our long S&P GSCI and COMT ETF commodity recommendations, and our long MSCI Global Metals & Mining Producers ETF (PICK) recommendation. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish US natural gas exports via pipeline to Mexico averaged just under 7 bcf/d in June, according to the EIA. Exports hit a record high of 7.4 bcf/d on 24 June 2021. The record high for the month was 7.4 Bcf/d on June 24. The EIA attributes the higher exports to increases in industrial and power demand, and high temperatures, which are driving air-conditioning demand south of the US border. Close to 5 bcf/d of the imported gas is used to generate power, according to the EIA. This was up close to 20% y/y. Increases in gas-pipeline infrastructure are allowing more gas to flow to Mexico from the US. Base Metals: Bullish China reportedly will be selling additional copper from its strategic stockpiles later this month, in an effort to cool the market. According to reuters.com, market participants expect China to auction 20k MT of Copper on 29 July 2021. This will bring total sales via auction to 50k MT, as the government earlier this month sold 30k MT at $10,500/MT (~ $4.76/lb). Prior to and since that first auction, copper has been trading on either side of $4.30/lb (Chart 6). Market participants expected a higher volume than the numbers being discussed as we went to press. In addition to auctioning copper, the government reportedly will auction other base metals. Precious Metals: Bullish Interest rates on 10-year inflation-linked bonds remain below -1%, as U.S. CPI inflation rises. US 10-year treasury yields have rebounded since sinking to a five-month low at the beginning of this week. The positive effect of negative real interest rates on gold is being balanced by a rising USD (Chart 7). Safe-haven demand for the greenback is being supported by uncertainty caused by COVID-19’s Delta variant. Gold prices are still volatile after the Fed’s ‘dot shock’ in mid-June.3 This volatility is reducing safe-haven demand for the yellow metal despite rising economic and policy uncertainty. Ags/Softs: Neutral Hot, dry weather is expected over most of the grain-growing regions of the US for the balance of July, which will continue to support prices, according to Farm Futures. Chart 6Copper Prices Going Down

Copper Prices Going Down

Copper Prices Going Down

Chart 7Weaker USD Supports Gold

Weaker USD Supports Gold

Weaker USD Supports Gold

Footnotes 1Please see 19th "OPEC and non-OPEC Ministerial Meeting concludes" published by OPEC 18 July 2021. 2Please see "BHP said to seek an exit from its petroleum business" published by worldoil.com July 20, 2021. 3Please refer to ‘“Dot Shock” Continues To Roil Gold; Oil…Not So Much’, which we published on July 1, 2021 for additional discussion. It is available at ces.bcaresearch.com. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed In 2021 Summary of Trades Closed

OPEC 2.0's Forward Guidance In New Baselines

OPEC 2.0's Forward Guidance In New Baselines

Feature June’s economic data and second-quarter GDP indicate that China’s economic recovery may have peaked. Slight improvements in some sectors, including manufacturing investment, exports and consumption, were offset by slowing in China’s old economy, such as infrastructure and real estate. A softening economy will weigh on Chinese corporate profits in 2H21. Inflation in Producer Price Index (PPI) has likely peaked, but it remains far above its historic average. Downstream industries may benefit from low interest rates and slightly less inflationary pressures on input prices, however, their profit growth has rolled over given weakening domestic demand and base effect. Industrial profits will shift downward in 2H21, meanwhile China’s macro policy will probably disappoint investors. Last week’s GDP’s numbers show that small-to-medium enterprises (SMEs) and private-sector businesses bore the brunt of rising global commodity prices and a slow recovery in domestic household consumption and services. The data, coupled with recent policy moves, support our view that China’s leadership is focused on helping vulnerable segments of the economy rather than boosting domestic demand by broadly easing policies (Chart 1). Nonetheless, the authorities may resort to easing policy later in 2021 if export growth weakens significantly in the second half of the year. A series of Reserve Requirement Ratio (RRR) and/or interest rate cuts, increased infrastructure project approvals, and/or looser real estate regulations, will signal that China’s ongoing policy tightening cycle has ended. In recent weeks both Chinese onshore and offshore stocks slipped further in absolute terms and relative to global benchmarks (Chart 2). We continue to recommend that investors remain cautious on Chinese stocks, at least through Q3. Chart 1No Broad Easing Yet

No Broad Easing Yet

No Broad Easing Yet

Chart 2Investors Still Cautious On China's Economy And Policy

Investors Still Cautious On China's Economy And Policy

Investors Still Cautious On China's Economy And Policy

Qingyun Xu, CFA Associate Editor qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Q2 GDP: Recovering At A Slower Pace China’s official GDP growth, on a year-over-year basis, slowed to 7.9% in Q2 from 18.3% in Q1 (Chart 3, top panel). While Q2’s weaker reading reflects the base effect in the data, it was slightly below the market’s expectation of 8.0-8.5%. Moreover, on a sequential basis (quarter-over-quarter), Q2’s seasonally adjusted GDP growth was one of the slowest in the past decade (Chart 3, bottom panel). These figures and the underlying data highlight that China’s economic growth momentum, which historically lags the credit impulse by six to nine months, has peaked (Chart 4). However, in 1H21, China aggregate output still grew by a 5.5% average annual rate during the same period over the past two years, well within Chinese policymakers’ target of above 5% growth needed to maintain a stable economy. Meanwhile, the bifurcation in China’s economic recovery continues. While robust external demand for Chinese goods helped to underpin manufacturing output, the sector’s profit growth has lagged upstream industries. Moreover, state-owned enterprises (SOEs) are experiencing soaring profit growth whereas SMEs have struggled with rising global commodity prices and sluggish domestic consumption as discussed below. We expect that the pace in credit growth deceleration will moderate in 2H21 and interest rates will stay at historically low levels. However, the authorities are unlikely to loosen macro policies until more signs of economic weaknesses emerge. Chart 3Q2 GDP: Slowing From An Elevated Level

Q2 GDP: Slowing From An Elevated Level

Q2 GDP: Slowing From An Elevated Level

Chart 4Chinese Economic Growth Should Soften Further In 2H21

Chinese Economic Growth Should Soften Further In 2H21

Chinese Economic Growth Should Soften Further In 2H21

Robust Exports, Sluggish Manufacturing Investment Chart 5Subdued Manufacturing Investment Recovery Despite Robust Exports

Subdued Manufacturing Investment Recovery Despite Robust Exports

Subdued Manufacturing Investment Recovery Despite Robust Exports

China’s export growth in June beat market expectations, despite shipping disruptions at major ports in Guangdong province due to a resurgence in COVID-19 cases. However, the recovery in manufacturing investment was muted through most of 1H21 even though export growth was resilient (Chart 5). There are several reasons for the sluggish recovery: the RMB’s rapid appreciation in the first five months of 2021, rising inflation and the limited pricing power that Chinese exporters gained in the first half of the year likely impeded their profits and curbed their propensity to invest (Chart 6). Total export values in USD significantly outpaced those in RMB terms, suggesting that the profit gains by Chinese exporters were offset by the strengthening local currency (Chart 7). Chart 6Rapid RMB Appreciation Will Weigh On Industrial Profits

Rapid RMB Appreciation Will Weigh On Industrial Profits

Rapid RMB Appreciation Will Weigh On Industrial Profits

Chart 7Divergence Between Exports In USD versus RMB

Divergence Between Exports In USD versus RMB

Divergence Between Exports In USD versus RMB

Furthermore, manufacturers in mid-to-downstream industries have been unable to fully pass on rising input costs to domestic consumers, which is evidenced in the faster growth of manufacturing output volume compared with price increases. It contrasts with the previous inflationary cycles, where surging prices for manufactured goods surpassed output volume (Chart 8A & 8B). Chart 8AChina's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

Chart 8BMuted Profit Margin Recovery In Manufacturing Compared With Mining

Muted Profit Margin Recovery In Manufacturing Compared With Mining

Muted Profit Margin Recovery In Manufacturing Compared With Mining

June’s improvement in manufacturing investment may not advance into 2H21 without added policy support. The nearly 2% depreciation in the RMB against the dollar in recent weeks will alleviate some pressure on exporters’ profit margins. However, export prices in USD also started to weaken (Chart 9). In addition, June’s manufacturing PMI and a Chinese business school survey,1 reported a deterioration in business conditions among smaller businesses. The weaker sentiment will depress manufacturing investments since China’s manufacturing sector is dominated by private and smaller businesses (Chart 10). Chart 9Chinese Export Prices In USD Are Rolling Over

Chinese Export Prices In USD Are Rolling Over

Chinese Export Prices In USD Are Rolling Over

Chart 10Deteriorating Business Sentiment Will Depress Manufacturing Investments

Deteriorating Business Sentiment Will Depress Manufacturing Investments

Deteriorating Business Sentiment Will Depress Manufacturing Investments

Recent policy measures to keep a low interest-rate environment will help the export and manufacturing sectors by reducing operating costs. The measures are also in keeping with China’s shift from boosting its service sector to maintaining a steady share of manufacturing output in its domestic economy (Chart 11). Chart 11Maintaining A Steady Share Of Manufacturing Output In China's Economy

Maintaining A Steady Share Of Manufacturing Output In China's Economy

Maintaining A Steady Share Of Manufacturing Output In China's Economy

Policy Tightening In The Old Economy Continues Chart 12Investments In Real Estate Have Lost Steam

Investments In Real Estate Have Lost Steam

Investments In Real Estate Have Lost Steam

Infrastructure investment growth slowed further in June. Investments in real estate, which drove China’s economic recovery in the second half of 2020, are also losing momentum (Chart 12). The slowdown, engineered by policymakers, will likely endure for the rest of the year. Bank loans to real estate developers tumbled to a cyclical low (Chart 13). In addition, deposit and advance payments, the main source of funds for real estate projects, nose-dived along with home sales (Chart 14). Chart 13No Signs Of Looser Financing Regulations In Property Sector

No Signs Of Looser Financing Regulations In Property Sector

No Signs Of Looser Financing Regulations In Property Sector

Chart 14Falling Home Sales Will Further Depress Real Estate Investments

Falling Home Sales Will Further Depress Real Estate Investments

Falling Home Sales Will Further Depress Real Estate Investments

Chart 15Sharp Pullback In New Infrastructure Project Approvals This Year

Sharp Pullback In New Infrastructure Project Approvals This Year

Sharp Pullback In New Infrastructure Project Approvals This Year

Infrastructure project approvals by the Ministry of Finance remain on a downward trend (Chart 15). Last week, China’s Banking and Insurance Regulatory Commission (CBIRC) announced a new rule to stop financial institutions from lending to local government financing vehicles (LGFV) that hold off-balance sheet government debt. LGFVs are largely used by provincial governments to borrow from banks to help fund infrastructure projects. Regulations targeting the real estate sector will further dampen real estate investments in the second half of this year. Land purchases and housing starts, both leading indicators for real estate investment, have declined since February. Excavator sales and investment in construction equipment also deteriorated sharply (Chart 16). Given that housing prices remain elevated, we do not expect real estate regulations to shift to an easier tone. The deceleration in China’s old economy is reflected in imports. While the value of imports remains strong, the volume has slowed, which suggests that the surge was due to soaring commodity prices (Chart 17, top panel). In particular, the growth in China’s imports of copper and steel, on a year-over-year basis and in volume terms, contracted in June (Chart 17, bottom panel). Chart 16Construction Activities Set To Slow Further

Construction Activities Set To Slow Further

Construction Activities Set To Slow Further

Chart 17Falling Import Volume

Falling Import Volume

Falling Import Volume

The Key To A Consumption Recovery Retail sales picked up slightly in June following two consecutive months of decline. However, retail sales remain below their pre-pandemic level (Chart 18). Labor market dynamics and household income growth, which stayed sluggish through 1H21, hold the key to the speed and magnitude of a recovery in consumption this year (Chart 19). Chart 18Sluggish Recovery In Household Consumption

Sluggish Recovery In Household Consumption

Sluggish Recovery In Household Consumption

Chart 19A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

A Lackluster Consumption Recovery Due To Slow Recovery in Household Income

Household precautionary savings, which remain elevated compared with their historical norms, have depressed the propensity to spend (Chart 20). While the overall unemployment rate in China’s urban centers has steadily declined this year, the rate of jobless young graduates (ages 16-24) picked up and is nearly three percentage points higher than its historical mean (Chart 21). However, the high unemployment among graduates will not encourage policymakers to stimulate the economy. The number of new graduates in both 2020 and 2021 is larger than the historical average, while the growth in new job creation has nearly recovered to that of the pre-pandemic years (Chart 22). Chart 20Households' Propensity For Precautionary Savings Remains Elevated

Households' Propensity For Precautionary Savings Remains Elevated

Households' Propensity For Precautionary Savings Remains Elevated

Chart 21Rising Unemployment Rate Among Younger Workers

Rising Unemployment Rate Among Younger Workers

Rising Unemployment Rate Among Younger Workers

Moreover, labor market slack among young graduates seems to be concentrated in the services sector, and this sector’s improvement is dependent on China’s domestic pandemic situation and inoculation rates rather than on stimulus (Chart 23). Chart 22Urban Job Creation Growth Still On The Mend

Urban Job Creation Growth Still On The Mend

Urban Job Creation Growth Still On The Mend

Chart 23Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Interruptions In Service Sector Recovery Due To Lingering COVID Cases

Elevated Inflation, Downshifting Industrial Profits Chart 24China's PPI May Have Reached A Cyclical Peak...

China's PPI May Have Reached A Cyclical Peak...

China's PPI May Have Reached A Cyclical Peak...

China’s domestic inflationary pressures eased slightly in June with a small decline in both consumer and producer prices. The input price component of the manufacturing PMI, which normally leads the PPI by about three months, dropped sharply last month, which indicates that the PPI may have reached its cyclical peak (Chart 24). However, producer price inflation will likely remain elevated in the second half of the year. Although global industrial metal prices have rolled over since May, they remain at their highest level since 2011 (Chart 25). A rapid deceleration in Chinese credit growth and weakening demand in 2H21 will remove some pressure in the sizzling hot commodity market, but global supply-side constraints will limit the downside in raw material prices, at least through the next six months. Therefore, diminishing inflationary pressures on the PPI will only slightly reduce input costs for China’s mid-to- downstream manufacturers, which have been unable to pass on rising commodity prices to domestic consumers (Chart 26). As discussed earlier, Chinese export prices in both USD and RMB terms have also rolled over. Chart 25...But Global Commodity Prices Are Still Elevated

...But Global Commodity Prices Are Still Elevated

...But Global Commodity Prices Are Still Elevated

Chart 26Absence Of Inflation Pass-Through

Absence Of Inflation Pass-Through

Absence Of Inflation Pass-Through

Given that price changes are more important to corporate profits than volume changes, Chinese mid-to-downstream industries will continue to face downward pressure on their profit margins. Profit growth in mid-to-downstream industries consistently lagged their upstream counterparts in the past 12 months (Chart 27). Moreover, state-holding enterprises, which dominate upstream industries, have seen a 150% jump in profit growth from a year ago, while the rate of profit gains among privately owned industrial companies tumbled this year (Chart 28). Chart 27A Faster Mean Reversal In Profit Growth Among Private Companies

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Chart 28A Faster Mean Reversal In Profit Growth Among Private Companies

A Faster Mean Reversal In Profit Growth Among Private Companies

A Faster Mean Reversal In Profit Growth Among Private Companies

Chinese policymakers will probably focus on addressing imbalances in China’s industrial sector and economy by supporting SMEs and the private sector. Meanwhile, industrial profit growth will decline in 2H21 from its V-shaped recovery last year, given weakening domestic demand and the waning base effect. Table 1China Macro Data Summary

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Table 2China Financial Market Performance Summary

Taking The Pulse Of China’s Slowing Economy

Taking The Pulse Of China’s Slowing Economy

Footnotes 1The CKGSB (Cheung Kong Graduate School Of Business) Business Conditions Index (BCI) comprises four sub-indices: corporate sales, corporate profits, corporate financing environment and inventory levels. Equity Sector Recommendations Cyclical Investment Stance

Highlights Metals prices are likely to suffer in the short term on the back of weakening Chinese demand and fading inflationary pressures. Accordingly, in our most recent Global Asset Allocation (GAA) Quarterly Outlook, we downgraded the AUD to underweight against the greenback. Bond yields, globally, are bound to rise moderately over the course of the coming 12 months. Australian yields, however, are likely to rise slower than those in the US. The RBA has been explicit in communicating what it would take to adjust its policy stance and is likely to lag behind other central banks in DM. We therefore recommend investors favor Australian government bonds in a global bond portfolio. Australian equities, now dominated by Financials rather than the Materials sector, would benefit from a rise in bond yields. However, a weaker AUD and declining metal prices warrant no more than a benchmark exposure to Australian equities within a global equity portfolio. Introduction Recently, clients have often been asking about Australia. The reasons seem clear. With a potential commodities “super-cycle” driven by a shift to renewable energy and electric vehicles (EVs), both the Australian economy and equities should be in a position to benefit. The reality, however, has been much less positive. Particularly the divergence between the core driver of the Australian market, industrial metals, and the performance of both equities and the currency over the past few years has been a concern (Chart 1). Over the past year and a half, Australian equities have underperformed the MSCI ACWI by 12.4% (Chart 2, panel 1). This underperformance was mainly due to the outperformance of the US. However, even against global markets excluding the US, Australian equities did not match the rise in commodity prices – particularly industrial metals (Chart 2, panel 2). Chart 1Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Despite The Rise In Metals Prices...

Chart 2...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

...Australian Equities Have Not Outperformed

Chart 3Financials Dominate Australian Equities

Financials Dominate Australian Equities

Financials Dominate Australian Equities

The structure of the Australian market has changed over the past few years. The commodities boom and subsequent global liquidity boom over the past two decades have fueled a housing bubble in Australia and an unsustainable rise in household debt. As a result, Australian equities are no longer dominated by metals and mining stocks, but rather by banks (Chart 3). We structured this Special Report in a Q&A format, answering questions we think are most relevant for investors to assess both the short- and long-term outlook for Australia. We aim to provide an overview of the economy and draw some conclusions on how investors should be positioned. Our conclusions are as follows: Over the past year and a half, the Australian economy has shown how complementary actions between fiscal and monetary policy, as well as social restriction measures, can mitigate both economic and human damage. The Reserve Bank of Australia (RBA) will be in no rush to adjust its policy stance until wage growth is back to its 3% target. However, RBA officials risk running the economy hot in the meantime given that measures of employment are back to their pre-pandemic levels. The RBA is not likely to change its policy stance before reaching its wage growth and inflation targets and will probably lag behind other global central banks in tightening. In that case, investors should favor Australian government bonds in a global bond portfolio. Australian banks remain well-funded and in good health. But their excessive exposure to the housing sector puts them at grave risk if home prices collapse. Despite this, there seems to be a feedback loop where a decline in mortgage rates fuels further demand for loans, pushing up home prices. A slowdown in Chinese credit growth and economic activity will hamper commodity demand, weighing down on Australian equities. The longer-term outlook remains compelling for Australian equities and metals as we enter into a new commodities “supercycle” fueled by a transition to renewable and alternative energy. The Australian economy stands to benefit given that the country has high levels of both production and reserves of the minerals needed for this transition. Q: How Does The Economy Look In The Short-Term? A: Australia can be regarded as one of the few countries that successfully navigated the pandemic with a minimal amount of damage, both to its population and economy. With swift measures to limit travel and implement social restrictions, the spread of the outbreak was curtailed to slightly over 30,000 total cases, representing only 0.12% of its population (Chart 4). On the other hand, its vaccination campaign has been much slower (at 38 doses administered per 100 people) than in other DM economies such as the US, UK, France, or Germany with 100, 120, 90, and 102 doses per 100 people, respectively. In the short term, this might not seem particularly damaging to the economy. However, if vaccination rates do not pick up rapidly, Australia’s international travel restrictions (which cannot sustainably be kept in place) will hamper economic growth and become a major drag on the tourism and education sectors (Chart 5, panels 1 & 2). Chart 4Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Government Policies Contained The Pandemic Outbreak...

Chart 5...At The Expense Of Tourism

...At The Expense Of Tourism

...At The Expense Of Tourism

Ample fiscal support – in the form of wage subsidies and business support through the JobKeeper program – mitigated the shortfall in household incomes (Chart 6). This provided a boost to both consumers and businesses with Q1 GDP growth coming in at 1.8% quarter-on-quarter (7.4% annualized). GDP expectations for the remainder of this year and next show a resilient strong momentum for Australian growth and domestic demand (Chart 7). Chart 6Fiscal Stimulus Supported Employment...

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

Chart 7...And Overall Growth

...And Overall Growth

...And Overall Growth

Chart 8Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

Labor Market Back To Pre-Pandemic Levels...

The labor market recovery has been an excellent example of how fiscal support and lockdown measures complement each other. Most employment indicators have almost recovered or surpassed their pre-pandemic levels: The unemployment rate stands at 4.90%, compared to 5.13%, the underemployment rate is at 7.44%, compared to 8.60%. The total number of those employed is now above its pre-pandemic level, albeit still below the 2018-2019 growth trend (Chart 8). Q: When Will The RBA Shift Its Policy Stance? A: The RBA has been explicit in communicating that changes in its policy stance hinge on Australian wage growth rising sustainably towards 3% – a level last reached in Q1 2013. Even with economic activity mostly restored, wage growth remains low at 1.49% (Chart 9). Our belief is that until that occurs, the RBA will probably maintain its accommodative stance. Our global fixed-income strategists, in a recent report, highlighted their belief that the RBA is likely to be less hawkish than markets currently expect – on both tapering and hiking rates. We agree with that assessment. Comments by RBA Governor Lowe earlier last month back our dovish belief: He stated that “The Board is committed to maintaining highly supportive monetary conditions to support a return to full employment in Australia and inflation consistent with the target…This is unlikely to be until 2024 at the earliest”. Market expectations nevertheless remain much more hawkish – pointing to a first rate hike by mid 2022 and almost 70 basis points of hikes by 2024 (Chart 10). Chart 9...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

...However Wage Growth Remains Muted

Chart 10Market Expects A Hawkish RBA...

Market Expects A Hawkish RBA

Market Expects A Hawkish RBA

Chart 11...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

...And Is Already Pricing That Down The Curve

Chart 12Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target

Inflation Remains Well-Below The RBA's Target

This means that the RBA will probably risk running the economy hot for a while. With total employment back to its pre-pandemic level and other employment indicators closely behind, inflationary pressures, sooner or later, will begin to mount. Higher growth prospects and inflation risks are being discounted further down the curve (Chart 11). The June CPI print is likely to reflect a transitory short-term base effect and the RBA is mostly going to see through that. In the meantime, we would watch other broad inflation indicators to gauge for price pressures. Broader measures such as the trimmed-mean inflation index or median inflation remain subdued at 1.1% and 1.3%, respectively. The 10-year breakeven rate currently stands at 2.1%, within the RBA’s range of 2%-3%, highlighting the market’s belief that long-term inflation remains well under control (Chart 12). Bottom Line: The RBA is likely to maintain its dovish stance for longer than the market expects. A return to sustainable levels of wage growth and inflation will remain the top objectives and it is unlikely that policy will be reversed before they are achieved. Our global fixed-income strategists laid out a checklist of what would make the RBA turn less dovish. So far, only 1 out of 5 items on their list (the recovery in private-sector demand) signals the need for a more hawkish stance. The remaining items signal no imminent pressure on the RBA to adjust policy (Table 1). The RBA is also wary of the currency appreciating if it took a more hawkish stance ahead of other central banks (e.g., the Fed) and is therefore likely to switch policy only after other central banks do so (Chart 13). Accordingly, investors should favor Australian government bonds within a global bond portfolio. Table 1RBA Checklist

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

Chart 13The RBA Will Be Wary Of A Rising AUD

The RBA Will Be Wary Of A Rising AUD

The RBA Will Be Wary Of A Rising AUD

Q: Are There Signs Of Improvement In The Banking Sector? A: Headline indicators of the health of the Australian banking sector paint a picture of a well-capitalized, highly funded, and profitable industry. Return on equity (ROE) has averaged 12.1% over the past decade. Capital adequacy and Tier 1 capital ratios stand at 14.5% and 18.2%, respectively – much higher than at the start of the Global Financial Crisis (GFC). The ratio of non-performing loans remains low and Australian banks’ reliance on leverage has also decreased (Chart 14). Chart 14Banks Look Healthy...

Banks Look Healthy...

Banks Look Healthy...

Chart 15...But Remain Exposed To The Housing Sector...

...But Remain Exposed To The Housing Sector

...But Remain Exposed To The Housing Sector

However, these indicators mask a major underlying risk. Banks remain heavily exposed to the housing market, with housing loans as high as 62% of banks’ gross outstanding loans and 40% of total assets (Chart 15, panel 1). Over the past decade and a half, banks have lent an average of A$56 of housing-related loans for every A$100 in total loans (Chart 15, panel 2). Chart 16...Which Is Showing No Signs Of Slowing Down

...Which Is Showing No Signs Of Slowing Down

...Which Is Showing No Signs Of Slowing Down

Chart 17Households Remain Heavily Indebted

Households Remain Heavily Indebted

Households Remain Heavily Indebted

With interest rates falling over the past few decades, construction activity has boomed. Consequently, the demand for loans for new homes has been rising, leading home prices higher (Chart 16). This also meant that household debt levels have climbed and currently standing at a staggering 130% of GDP and 180% of disposable income (Chart 17). So what does this mean for banks’ stock prices? The short answer is that absent a bursting of the bubble in house prices, banks should continue to fare well. Interestingly, the long-standing relationship between bond yields and banks’ relative stock price returns – one that works in other financial-heavy markets such as the euro area – did not hold in Australia, at least until recently. In fact, we find that, historically, Australian banks outperformed the broad market when bond yields were falling. This relationship changed post-GFC, most likely when inflation expectations became unanchored and trended lower – reflecting lower commodity prices (Chart 18). Bottom Line: Rising rates, reflecting better growth prospects and higher long-term inflation, should be a tailwind for bank stocks in the short term. Accommodative monetary policy will spur activity in the property market, propping up bank profits. This, however, puts banks at even greater risk when profitability starts to decline, NPLs rise and regulations tighten further. The latter risk is one we would highlight following RBA deputy governor Guy Debelle’s statement that monetary policy will not be used as a tool to curtail housing prices and that there are other tools to address that issue. Chart 18Rising Yields Will Be A Tailwind For Australian Equities

Rising Yields Will Be A Tailwind For Australian Equities

Rising Yields Will Be A Tailwind For Australian Equities

Q: How Does Chinese Policy Impact Australian Growth? A: China's role in global supply chains, as both a producer and consumer, has increased dramatically since the early 2000s. China’s demand for commodities generally and industrial metals in particular has grown over the past two decades from an average of 10% of total global demand to 50% for most metals (Chart 19). Australia stood to benefit, redirecting more and more of its metals’ production away from the rest of the world and towards China. For example, during the same period, the share of Australian iron ore exports to China increased fourfold (Chart 20). Chart 19China Is A Major Consumer Of Metals...

China Is A Major Consumer Of Metals...

China Is A Major Consumer Of Metals...

Chart 20...And This Has Benefited Australia Over The Past Two Decades

...And This Has Benefited Australia Over The Past Two Decades

...And This Has Benefited Australia Over The Past Two Decades

However, this dynamic leaves the Australian economy very exposed to the Chinese business cycle – one that is heavily reliant on policymakers’ decisions on how much liquidity to inject into the economy. After strong credit and fiscal support throughout 2020, the Chinese authorities – wary of excessive leverage in the economy – have begun paring back stimulus which is likely to lead to weaker growth in the second half of the year and put downward pressure on metal demand (Chart 21). Chart 21Weakening Chinese Demand Will Hurt Metals In The Short-Term

Weakening Chinese Demand Will Hurt Metals In The Short-Term

Weakening Chinese Demand Will Hurt Metals In The Short-Term

Heightened political tensions between Australia and China have also played a role. China recently imposed restrictions, including additional tariffs and bans, on Australian imports such as beef, wine, coal, and other goods. Consequently, Australian exports to China slowed. However, the goods not imported by China were absorbed by other economies – Australian export growth did not fall that much. It is unlikely that a new commodity-heavy marginal buyer will emerge in the short-term to replace Chinese demand. The recent rise in commodity prices reflected a return to economic activity, as well as inflationary fears, and supply, shipping, and logistical backlogs. These will ease in the short term, weighing on both the AUD and Australian equities. Q: Can The Shift To Renewable Energy Spur Future Australian Growth? A: The shift to renewable energy and electrification – particularly in the transport sector – will occur sooner rather than later. Some commodity-exporting countries stand to benefit, and Australia is likely to be one. We previously highlighted that modeling longer-term demand is tricky since it relies on assumptions for the emergence of new technologies, metals’ efficiency and recycling rates, and the rate of conversion to renewables. Chart 22The Shift To Renewables Will Require More Resources...

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

The mechanics of the future demand/supply relationship hinge on the following: Demand will rise during this energy transition period – simply due to the fact that the new clean energy systems require more minerals (such as copper and zinc) than the current traditional hydrocarbon-fueled energy system (Chart 22, panel 1). Electric vehicles (EVs) require about four and a half times more of certain commodities – particularly copper, nickel, and graphite – than conventional vehicles do (Chart 22, panel 2). Supply limitations, on the other hand, are what might propel metal prices even higher and lead the world economy into a new commodities “supercycle”. A study by the Institute for Sustainable Futures has shown that, in the most positive energy transition scenarios, demand for some metals will exceed supply, in terms of both available resources and reserves (Table 2). Table 2...Which Are Likely To Be In Short Supply

A Deeper Dive Into The Land Down Under

A Deeper Dive Into The Land Down Under

For some of those metals, Australia is either among the top producers, or has the largest reserves. For example, Australia produces almost 45% and 12% of the world’s lithium and zinc, and has 22% and 27% of the world’s reserves. Looking at other metals, supply disruptions – particularly in economies where political, social, and environmental influences are an issue – might be the driver of further price rises. For example, Chile has the largest shares of global lithium reserves (~44%), and copper reserves (~23%), while South Africa has the largest share of global manganese reserves (~40%). Bottom Line: The transition to renewable energy is already underway and is likely to intensify. Forecast demand should outstrip supply and Australia stands to benefit given its large share of current production and/or reserves. How much will depend on the pace of renewable energy integration but miners are likely to be long-term winners. Q: What Is The Outlook For The AUD? A: The Global Asset Allocation (GAA) service, in its latest Quarterly Outlook, turned negative on the AUD. The currency has historically had a high positive correlation with commodity prices and industrial metals prices, which in turn are very sensitive to Chinese demand (Chart 23). Given our outlook for metals in the short term (falling demand driven by slowing Chinese activity), we expect some weakening in the AUD over the coming 9-to-12 months (Chart 24). Chart 23The AUD Is Highly Correlated To Metal Prices...

The AUD Is Highly Correlated To Metal Prices...

The AUD Is Highly Correlated To Metal Prices...

Chart 24...Which In Turn Are Highly Correlated To Chinese Activity

...Which In Turn Are Highly Correlated To Chinese Activity

...Which In Turn Are Highly Correlated To Chinese Activity

Additionally, short-term weakness in the economy, caused by further lockdowns as Delta-variant COVID cases rise, is a risk since it might reduce domestic demand. From a valuation perspective, the AUD is slightly below its fair value (Chart 25). However, this on its own does not compel us to remain positive on the currency. We also consider other indicators such as investor positioning – which has reached a decade high, according to Citibank’s FX Positioning Alert Indicator (PAIN) (Chart 26). This indicator suggests that active FX traders hold substantial long positions in the AUD against the USD. Historically, this indicator has provided contrarian signals, with extreme optimism (pessimism) providing useful short (long) signals. Chart 25The AUD Is Close To Fair Value

The AUD Is Close To Fair Value

The AUD Is Close To Fair Value

Chart 26Investors Are Long The AUD

Investors Are Long The AUD

Investors Are Long The AUD

Bottom Line: Short-term weakness in the economy and a reversal in metal prices warrant caution on the currency. While valuations do not signal overbought conditions, investor positioning (a contrarian indicator) does. Q: How Should Equity Investors Be Positioned? A: Our recent Special Report on whether country or sector effects drive equity performance showed that sector composition was relatively important in Australia, given the large difference in sector weightings relative to the global benchmark. Our analysis showed that cumulative Australian sector performance over the past two decades detracted from overall returns (Chart 27). Given that framework, and the relationship between the Australian economy and industrial metals, we find that Australian equity performance relative to the US mirrors the performance of global metal and mining relative to global tech stocks (Chart 28). This underperformance makes sense: Commodity prices have been in a structural downtrend throughout the past decade. Chart 27Country Vs Sector Effect

Country Vs Sector Effect

Country Vs Sector Effect

Chart 28Australia / US = Metals / Tech

Australia / US = Metals / Tech

Australia / US = Metals / Tech

Therefore, given our view of the outlook for metals, we would not want to shun Australian equities. The Global Asset Allocation (GAA) service is currently neutral the Australian market within a global equity portfolio, and underweight the Materials sector over the next 12 months. We believe this positioning makes sense given the slowdown in the Chinese economy and the improbability that another country will emerge as the alternative marginal buyer of commodities. The longer-term outlook is more compelling however, as the shift to decarbonization, renewables, and alternative energy gets underway. Conclusions In the short term metals prices are likely to suffer on the back of weakening Chinese demand (with no immediate substitute as a marginal buyer) as well as fading inflationary fears and an easing of supply/logistical issues. Our analysis shows that sector composition is a larger driver of Australian equity relative performance than country composition. While Australian equities – dominated by Financials – would benefit from a moderate rise in global bond yields, yields will rise more slowly in Australia than in the US and the AUD is likely to weaken. Over the next 12 months, investors should remain neutral on Australian equities within a global equity portfolio. The RBA is likely to lag other central banks in tightening policy. Investors should therefore favor Australian government bonds over other developed economies such as the US and Canada. Amr Hanafy, Senior Analyst Global Asset Allocation amrh@bcaresearch.com

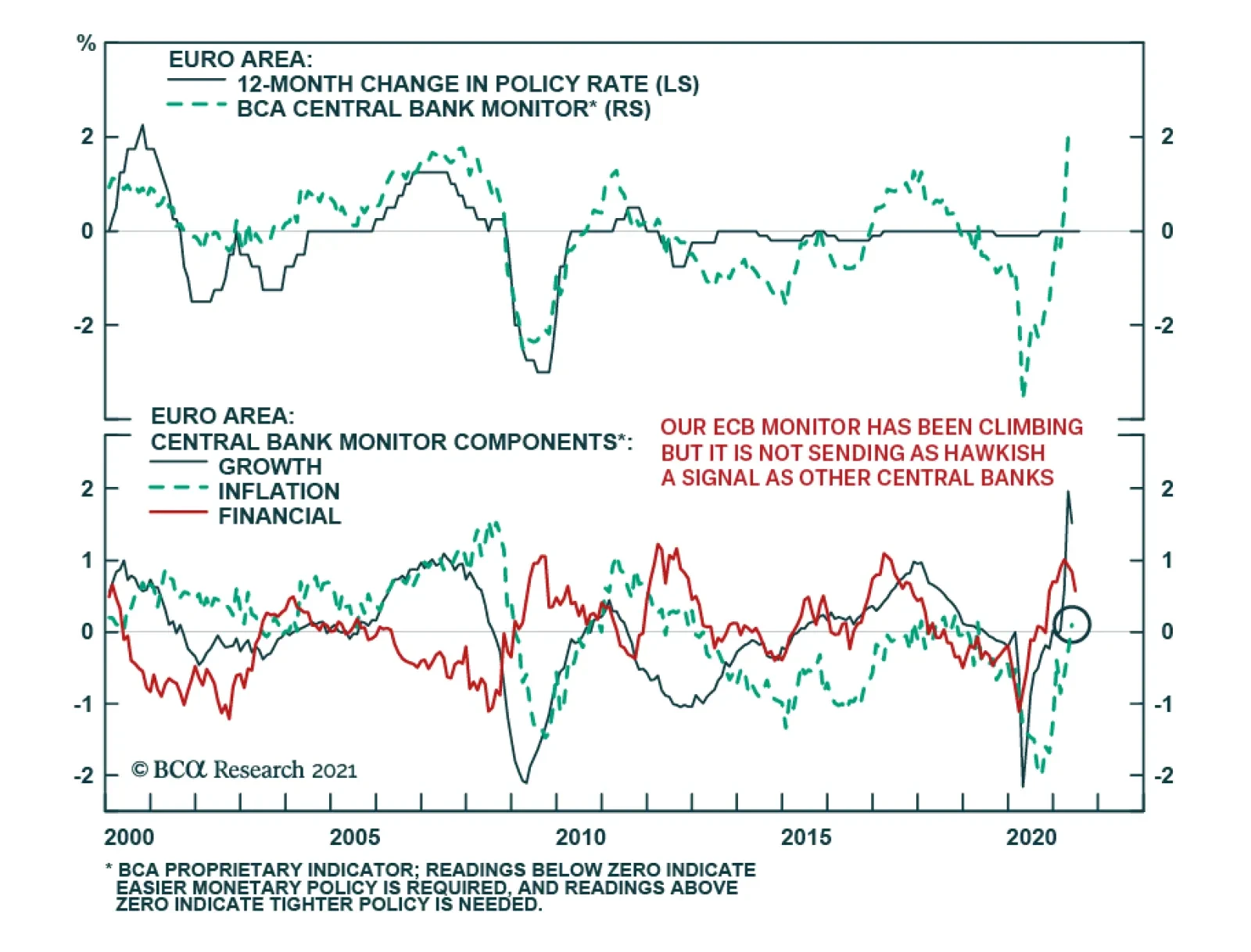

Highlights The ECB has changed its inflation target, but its credibility remains weak. Inflation will not allow the ECB to tighten policy anytime soon. Instead, the ECB will have to add to its asset purchase program next year and may even consider dual interest rates. EUR/USD should continue to appreciate because of the weakness in the USD, but EUR/GBP, EUR/NOK, and EUR/SEK will soften. The SNB will follow the ECB; buy Swiss stocks / sell Eurozone defensives as an uncorrelated trade. China matters more than COVID-19 for the cyclical/defensive ratio. Despite our pro-cyclical medium- to long-term portfolio bias, the reflation trade is pausing. Remain tactically long telecom / short consumer discretionary as a hedge. European momentum stocks are near critical levels relative to growth equities. Feature The European Central Bank has found a new way to shed its Bundesbank heritage further and to justify the continuation of its QE program well after other central banks around the world will have ended their asset purchases. The early results of the Strategy Review and the subsequent comments by President Christine Lagarde will make it near impossible for the ECB to taper its asset purchases anytime soon. Practically, this means that the European yield curve will steepen relative to that of the US. Additionally, this policy should not hurt EUR/USD, but it will hurt EUR/GBP, EUR/NOK, and EUR/SEK. In the equity space, Swiss stocks will outperform European defensive equities, creating an opportunity for an uncorrelated trade. A New Tougher Target The ECB has abandoned its long-standing target of “close but below” 2% inflation. Even more importantly, the ECB followed the Bank of Japan and the Fed in adopting an approach whereby both downside and upside deviations from the 2% inflation target are to be fought. The ECB’s credibility was already hurt by its inability to achieve its more modest previous inflation target. Since 2009, the Euro Area HICP only averaged 1.2% (Chart 1). To prevent losing further credibility under its new mandate, the ECB will have to increase its stockpile of assets. Moreover, the ECB is far from achieving its new mandate, which will add to the ECB’s need to expand stimulus to the system even once the impact of owner-equivalent rent is included in CPI. Chart 1Mission Impossible

Mission Impossible

Mission Impossible

Chart 2Narrow Inflationary Pressures

Narrow Inflationary Pressures

Narrow Inflationary Pressures

Today, the ECB’s measure of core inflation stands at 1%, while headline inflation is 1.9%. As the economy re-opens, a surge in inflation is likely, but this spike will be transitory, even more so than in the US. As we recently showed, our estimate of the Eurozone trimmed-mean CPI has plunged close to 0%, which highlights that inflation pressures remain narrow (Chart 2). The labor market is another hurdle that will prevent Eurozone inflation from durably reaching 2% anytime soon. Currently, the total hours worked in the Euro Area remains well below the equilibrium level implied by the working-age population (Chart 3), which historically constrains wages. Moreover, it generally takes many quarters after labor shortages become prevalent before inflation begins to inch higher (Chart 4). Chart 3No Wage Pressure Yet

No Wage Pressure Yet

No Wage Pressure Yet

Chart 4No Inflation Labor Shortages For A While

No Inflation Labor Shortages For A While

No Inflation Labor Shortages For A While

The euro is the last force that caps European inflation. Despite the recent depreciation in EUR/USD, the trade-weighted euro remains near all-time highs, which historically imparts strong deflationary pressures to the economy (Chart 5). Beyond the time it will take for realized inflation to reach the ECB’s new target, inflation expectations are still inconsistent with 2% inflation. As the top panel of Chart 6illustrates, market-based inflation expectations in the Eurozone remain well below both 2% and the levels that prevailed before the Great Financial Crisis, even though rising commodity prices are lifting global inflation expectations. Market participants are not alone in doubting the ECB; professional forecasters do not see inflation at 2% in the near-term or the long-term (Chart 6, bottom panel). Chart 5The Euro Is Deflationary

The Euro Is Deflationary

The Euro Is Deflationary

Chart 6The ECB Lacks Credibility

The ECB Lacks Credibility

The ECB Lacks Credibility

In addition to the continued inability of the ECB to achieve its previous inflation target, let alone its present one, sovereign risk still hamstrings the central bank. The Italian economy remains fragile, because little structural reform has taken place. The Spanish economy cannot stand on its own two feet while the tourism industry continues to suffer due to COVID-19 related fears. And the exploding debt load of the French economy as well as its structural current account deficit raise the possibility that OATs will become unmoored. The ECB will ensure that spreads in those nations do not widen, or Eurozone inflation will never reach the new 2% target. Bottom Line: When it was time to achieve near—but below—2% inflation, the credibility of the ECB was already limited. The new target will be even harder to reach, but the symmetry around it gives the ECB more leeway to provide additional support to the Eurozone economy. Market Implications The ECB is now bound to maintain policy accommodation beyond the scheduled end of the PEPP program in March 2022, or the new policy target will be even less credible than the previous one. BCA Global Fixed Income Strategy team expects the ECB to maintain its asset purchase program beyond the stated end of the PEPP. Practically, this means that the ECB will fold the program into the pre-pandemic APP. The ECB cannot tighten policy while it remains so far from its target, especially now that missing the goalpost to the downside is as problematic as missing it to the upside. We expect the ECB to hint at this on Thursday. Chart 7The EONIA Curve Anticipated The Strategy Review

The EONIA Curve Anticipated The Strategy Review

The EONIA Curve Anticipated The Strategy Review

The ECB will also not increase interest rates for the foreseeable future, which the EONIA curve already anticipates (Chart 7). Money markets only expect a first hike in late 2024, which is appropriate. Compared to a month ago, overnight rates 10-year forward fell by more than 10bps, from 0.75% to 0.61%. We are inclined to fade this move. More stimulus raises the outlook for long-term policy rates. Amid the correction in global bond yields, betting against the decline in the long-term EONIA rate is akin to catching a falling knife; however, because the ECB is easing relative to the Fed, a box trade of buying European steepeners at the same time as US flatteners remains appropriate. The ECB could also lower the rate on TLTRO operations, resulting in a dual interest rate regime in the Eurozone. As Megan Greene and Eric Lonergan have argued, this policy would provide a further lift to the Euro Area economy by boosting the attractiveness of borrowing; at the same time, it would limit the deleterious impact of ever-more negative deposit rates on the profitability of the banking sector, because banks would borrow at extremely negative rates to finance lending activities. Chart 8JPY And YCC

JPY And YCC

JPY And YCC

The effect of the policy on the euro is more complex. When Japan announced its Yield Curve Control strategy in September 2016, it defined price stability as achieving a 2% inflation rate over the span of the business cycle. In other words, the BoJ implemented a backdoor average inflation mandate. Following this announcement, USD/JPY strengthened (Chart 8), but this move reflected the dollar rally and the global bond selloff around the US election, not yen-specific factors. This suggests that the euro will continue to track the USD inversely. BCA’s FX Strategy team remains bearish on the greenback, as a result of the growing US current account deficit and the fact that the Fed continues to target an overshoot in inflation, which suggests that, even if US nominal interest rates rise, real rates will lag behind. The EUR is nonetheless set to underperform compared to other European currencies. In the UK, house price gains are accelerating, the jobless count is declining rapidly as the economy re-opens, and the cheapness of the pound is accentuating positive inflation surprises. This combination suggests that the BoE is likely to follow the path of the Bank of Canada or the Reserve Bank of New Zealand, by beginning to tighten policy by early next year. Norway also faces a similar set of circumstances and has already announced it will lift interest rates this year. As we argued two months ago, the Riksbank is likely to follow its western neighbor, because the Swedish housing market is roaring, and the economy will remain well supported by the upcoming global capex boom. Hence, EUR/GBP, EUR/NOK, and EUR/SEK will depreciate. The Swiss National Bank should be the outlier that will follow the ECB. Swiss headline and core inflation linger at 0.6% and 0.4%, respectively. Wage growth is a meager 0.5%, because the Swiss output gap remains a massive 5.5% of GDP (Chart 9, top panel). Meanwhile, consumer confidence and retail sales are much weaker than those of Sweden, Norway, or the UK. Finally, Swiss private debt stands at 270% of GDP, which means that this economy still risks falling into a Fisherian debt-deflation trap. As a result, the SNB will continue to try to cap the upside in the CHF vis-à-vis the EUR, because the currency remains the main determinant of Swiss monetary conditions. Moreover, according to the central bank, the Swiss franc is still 10% overvalued relative to the euro, which is weighing on the country’s competitiveness (Chart 9, bottom panel). To fight the recent depreciation of EUR/CHF, the SNB will not raise rates for a long time and will intervene further in the FX market. The liquidity injections should prompt additional increases in the SNB’s domestic sight deposits, which since 2015 have resulted in a rise of Swiss bond yields relative to those of Germany (Chart 10). While counterintuitive, this relationship reflects the reflationary impact of the SNB’s asset purchases. It also means that the Swiss real estate market is set to become ever bubblier. Chart 9The SNB Will Follow The ECB

The SNB Will Follow The ECB

The SNB Will Follow The ECB

Chart 10Swiss/German Spreads To Widen

Swiss/German Spreads To Widen

Swiss/German Spreads To Widen

For Swiss shares, the picture is more complex. Swiss equities are extremely defensive, but, while they underperform Euro Area stocks when global yields rise, widening Swiss / German spreads often provide a lift to the SMI. A simple model, assuming US 10-year Treasury yields rise to 2.25% by the end of 2022 (BCA’s US Bond Strategy forecast) and that Swiss/German spreads widen to 20bps as the SNB domestic sight deposits swell, suggests that Swiss stocks will underperform that of the Euro Area over the coming 18 months (Chart 11). However, if we compare Swiss equities to European defensive sectors, then the widening in Swiss/German spreads should prompt an outperformance of Swiss equities, because their multiples benefit from ample liquidity conditions in Switzerland (Chart 12). Chart 11Swiss Stocks Are Too Defensive To Outperform Durably...

Swiss Stocks Are Too Defensive To Outperform Durably...

Swiss Stocks Are Too Defensive To Outperform Durably...

Chart 12...But They Will Beat Euro Area Defensives

...But They Will Beat Euro Area Defensives

...But They Will Beat Euro Area Defensives

Bottom Line: The results of the ECB Strategy Review will force this central bank to remain a laggard and continue to expand its balance sheet well after the expected end of the PEPP program. Eurozone interest rates will also fall behind that of other major economies. The ECB may even consider cutting the interest rate on TLTROs to boost lending. These policies will have a minimal impact on EUR/USD, which will continue to be dominated by the dollar’s fluctuations. However, EUR/GBP, EUR/SEK, and EUR/NOK will suffer. Finally, the SNB will follow the ECB and expand its balance sheet further, which will paradoxically lift Swiss/German spreads. As a result of their defensive nature, Swiss stocks will underperform Euro Area ones over the next 18 months, but they will outperform European defensive equities. Go long Swiss equities relative to European defensives, as a trade uncorrelated to the broad market. Follow China, Not Delta Chart 13

The ECB’s New Groove

The ECB’s New Groove

In recent days, doubts have grown about the European re-opening trade because of the resurgence of COVID-19 cases. The Delta variant (or any subsequent mutation for that matter) will cause hiccups along the way, but, ultimately, the re-opening will continue to proceed. As a result of the growing rate of vaccination, hospitalizations and deaths remain stable even if new cases are climbing rapidly in many countries (Chart 13). As long as the burden on the healthcare system remains limited, governments will find it difficult to justify further large-scale lockdowns. Instead, measures such as Macron’s Pass Sanitaire will provide increasing, widespread incentives for greater vaccination. Despite this sanguine take on the Delta variant, we remain concerned for the near-term outlook for cyclical equities because of the Chinese economy, even after the recent 50bps cut in the Reserve Requirement Ratio. BCA’s China Investment Strategy service believes that the RRR cut does not signal the beginning of a policy easing cycle. More evidence would be needed, such as additional RRR cuts, rising excess reserves, or supportive policies for the infrastructure and real estate sectors. For now, we heed the message from PBoC official Sun Guofeng that “the RRR cut is a standard liquidity operation.” Chart 14Fade The RRR Cut

Fade The RRR Cut

Fade The RRR Cut

The dominant force for the Chinese economy remains the previous deterioration in the credit impulse, which suggests that Q3 and Q4 growth will decelerate materially (Chart 14, top panel). Moreover, the softening impulse is consistent with weaker global economic activity, as approximated by our Global Nowcast (Chart 14, middle panel), especially since the lingering effect of the past RRR increases is still consistent with a global deceleration (Chart 14, bottom panel). In this context, we continue to hedge our long-term preference for cyclical stocks because of the near-term risks created by China and the excessively rapid move in the cyclical-to-defensives ratio (Chart 15). In response to this pause in the reflation trade, we continue to favor a long telecom/short consumer discretionary tactical position, which is supported by valuations and RoE differentials, as well as the still extended relative momentum (Chart 16). The period of risk to the global reflation trade should also allow the dollar to remain firm in the near-term, which means that for the coming months, the euro will not go beyond its trading range in place since the beginning of the year. Chart 15Cyclicals Remain Tactically Vulnerable

Cyclicals Remain Tactically Vulnerable

Cyclicals Remain Tactically Vulnerable

Chart 16Stay Long Telecom / Short Consumer Discretionary

Stay Long Telecom / Short Consumer Discretionary

Stay Long Telecom / Short Consumer Discretionary

Bottom Line: China’s RRR cut is not yet enough to bet against the temporary pause in the global reflation trade. Thus, investors should continue to hedge pro-cyclical long-term bets in their portfolios via a long telecom / short consumer discretionary position. An Exciting Chart A chart caught our eye this week: The underperformance of Eurozone momentum stocks relative to growth stocks is massively overdone (Chart 17). For now, we only want to highlight the phenomenon, but, in the coming weeks, we will delve deeper into the topic to gauge if these oversold conditions constitute an attractive opportunity. Chart 17Washed Out Moment

Washed Out Moment

Washed Out Moment

Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Currency Performance

The ECB’s New Groove

The ECB’s New Groove

Fixed Income Performance Government Bonds

The ECB’s New Groove

The ECB’s New Groove

Corporate Bonds

The ECB’s New Groove

The ECB’s New Groove

Equity Performance Major Stock Indices

The ECB’s New Groove

The ECB’s New Groove

Geographic Performance

The ECB’s New Groove

The ECB’s New Groove

Sector Performance

The ECB’s New Groove

The ECB’s New Groove

Highlights With geopolitical risks increasing around China, India is attracting greater attention from global investors. India’s youthful demographics also mark a stark contrast with China. While this demographic dividend is real, its benefits should not be overstated. India is young but socially complex, which will create unique social conflicts and policy risks. In particular, the country faces structurally large budget deficits. Regional political differences could slow down reforms. Lastly, competition with China will increase India’s own geopolitical risks. Macroeconomic and (geo)political factors, not youth alone, will determine India’s equity market returns. The bullish long-term view faces near-term challenges. Feature Map 1 PreviewIndia’s Demographic Dividend Can Be Overstated

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

“Independence had come to India like a kind of revolution; now there were many revolutions within that revolution … All over India scores of particularities that had been frozen by foreign rule, or by poverty or lack of opportunity or abjectness, had begun to flow again.” – Sir VS Naipaul, India: A Million Mutinies Now (Vintage, 1990) What is well known is that India is populous, young, and boasts a high GDP growth rate. India is also largely free of internal conflicts. Its democratic framework is seen as a pressure valve that can release social tensions. India’s hefty 58% cross-cycle premium to Emerging Markets (EM) is often attributed to the fact that India is younger than its peers, especially China. In this report we highlight that India’s demographic advantage is real but should not be overstated. For instance, India’s northern region can be likened to a demographic tinderbox. It accounts for about 45% of India’s population and is also younger than the national average. However, per capita incomes in this region are lower than the national average and to complicate matters, this region is crisscrossed by several social fault lines. This heterogeneity and economic backwardness in India’s population is the reason why the trend-line of India’s demographic dividend will not be linear. Its diverse population’s attempt to break out of its poverty will spawn unique policy risks. The North Is A Demographic Tinderbox, The South Is Prosperous But Ageing India will soon be the most populous country in the world (Chart 1). India’s median age is a decade lower than that of China to boot (Chart 2). Some emerging market investors fret about India’s low per capita income but India holds the promise of lifting individual incomes over time. This is because its GDP growth rate has been higher than that of its peers (Chart 3). Chart 1India Will Soon Be The Most Populous Country

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

Chart 2India Is A Decade Younger Than China

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

Chart 3India’s Per Capita Income Is Low, But GDP Growth Rate Is High

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

However, the “demographic dividend” narrative oversimplifies India’s investment case. India is young but also socially heterogenous and its median voter is poor. This complicates India’s development process and makes its demographic dividend trend-line non-linear. India’s social complexity is best understood if India is characterized as an amalgamation of three major regions: the North, the South (which we define to include the western region), and the East. Each of these parts are unique and have distinctive socio-demographic identities. India hence is more comparable to a continent like Europe than a country like the US. Like the European Union, India is a union of multiple social, religious, and ethnic groups. It straddles a vast geography and represents a very wide spectrum of interests. India’s South is more like a middle-income Asian country such as Sri Lanka or Vietnam whilst India’s East is more like a poor Latin American economy with latent social unrest. Understanding the heterogeneity of India’s vast populace is key to get a better sense of why an investment strategy for India must be nuanced and tactical in its approach, even if the overarching strategic view is constructive. The key features of each of these three regions can be summarized as follows: Region #1: The North This region comprises the triangular area between Jammu & Kashmir, Rajasthan and Jharkhand. This is the largest landmass in India stretching from the Himalayas to the fertile Gangetic plains of central India. Ethnically most of the population here is of Indo-Aryan descent. A lion’s share of this region’s population remains engaged in agriculture and allied activities. The North accounts for about 45% of the nation’s total population and is a demographic tinderbox. Per capita incomes are low and one in five persons falls in the age group of 15-24 years. To complicate matters, wage inflation in the farm sector, which employs a large majority of the populace in this region, has been slowing. If job creation in the non-farm sector stays insufficient then it will fan fires of social instability. The North includes states like Uttar Pradesh and Punjab which have seen a steady increase in small but notable socio-political conflicts in the recent past. Issues that triggered social conflict ranged from inter-religious marriages to resistance to amending farmer-friendly laws. Region #2: The South India’s South constitutes the large inverted-triangular region on the map and spans the area between Gujarat, Kerala, and West Bengal. We include India’s western region in this category because of its socio-economic similarities with the southern peninsula. Together the South and West account for the entirety of India’s peninsular coastline and for about 40% of total population. Historically, the South has seen far fewer external invasions and its social fabric is more homogenous than that of the North. This region is characterized by high per capita incomes, balanced gender ratios (Chart 4), and higher literacy ratios (Chart 5). Socio-political conflicts in this region are less common as compared to the North. Chart 4India’s South Has Healthy Gender Ratios Compared To North

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

Chart 5India’s South Is More Educated Than The Rest Of India

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details

The state of Kerala is an exception in this region. The social fabric in this state is unusual, with Hindus accounting for only 55% of its population (versus the national average of 80%). The high degree of religious heterogeneity in this southern Indian state could perhaps be the reason why the state has lately seen a rise of small but significant incidences of social conflict. Unlike India’s young North, the median age of the population in India’s South is likely to be higher than the national average. Whilst India’s South is clearly young by global standards, this region will have to deal with problems of an ageing population before India’s North or East. The Southern region in India even today relies on migrant workers from India’s North. Region #3: The East This region is the youngest and the smallest of the three, as it accounts for the remaining 15% of India’s population. The region is young but must contend with low per capita incomes and very high degrees of religious diversity. Muslims, Christians, and other religions account for 20% of India’s population nationally but +50% of the population in India’s East. By virtue of sharing borders with countries like Bangladesh, Nepal, and Myanmar, this region is often the entry point for migration into India. It is historically the least stable of the three regions owing to its heterogeneity and the steady influx of migrants. To conclude, India is young but is also socially complex. Whilst a youthful population yields economic advantages, if this young population lacks economic opportunity then social dissatisfaction and associated risks can be a problem. Furthermore, history suggests that if a region’s populace is young but poor and diverse, then it often spawns the rise of identity politics, which takes policymakers’ attention away from matters of economic development. Social Complexity Index To better represent India’s demographic granularities, we created a Social Complexity Index (SCI), as shown in Map 1. Map 1India’s North Is A Demographic Tinderbox; South Is Prosperous But Ageing

India’s Demographics: The Devil Is In The Details

India’s Demographics: The Devil Is In The Details