Policy

Highlights The Scottish parliamentary election does not present a near-term risk of a second referendum on Scottish independence. Independence is possible down the road but very unlikely due to a host of economic and geopolitical challenges still relevant in the twenty-first century. Book gains on long CHF-GBP. Go long FTSE 100 versus developed markets excluding the United States. Feature British equities have underperformed developed markets over the past decade – even if we exclude the market-leading United States (Chart 1). The British equity market is heavily concentrated in cyclical sectors like financials and materials and has a low concentration in information technology and communications services. As such the bourse has sprung to life since the advent of the COVID-19 vaccine and the prospect of a government-stimulated global growth recovery. In keeping with our strategic preference for value over growth we also look constructively at British equities. A potential source of geopolitical and political risk is Britain’s ongoing constitutional crisis, which flared up with the failed Scottish independence referendum in 2014 and the successful referendum to leave the EU in 2016. Tensions within the UK and between the UK and EU are part of the same problem – a loss of popular confidence and trust in the current nation-state and governing institutions in the aftermath of hyper-globalization.1 This constitutional crisis added insult to injury for UK stocks by jacking up policy uncertainty and undermining the attractiveness of domestic-oriented UK companies that suffered from trade disruptions with the European Union. Chart 1UK Referendums Added Insult To Injury

UK Referendums Added Insult To Injury

UK Referendums Added Insult To Injury

Chart 2Post-Brexit Trading Range For GBP-EUR

Post-Brexit Trading Range For GBP-EUR

Post-Brexit Trading Range For GBP-EUR

Now the COVID-19 pandemic and its aftermath have changed the global scene entirely and Brexit is no longer Britain’s chief concern. But there is still a lingering question over Scotland’s status. The Scottish question has recently weighed on the British pound and reinforced the new trading range for the GBP-EUR exchange rate in the aftermath of a “hard” exit from the European Union (Chart 2). Scotland voted for a new parliament on May 6 and the preliminary results are coming in as we go to press. The pro-independence Scottish National Party is still the most popular party and even if it falls short of a majority, as online betting markets expect, it has pro-independence allies with which it could form a coalition (Chart 3). Its leader, Scottish First Minister Nicola Sturgeon, has promised to pursue a second popular referendum on seceding from the United Kingdom by 2023. Chart 3Betting Markets Doubt Single-Party Majority For SNP

United Kingdom Stays United

United Kingdom Stays United

British Prime Minister Boris Johnson, backed by a strong Conservative Party parliamentary majority, has vowed not to allow a second referendum, arguing that the 2014 plebiscite was supposed to lay the question to rest for a while. Scottish opinion in favor of secession stands at 43.6% today, right near the 44.7% that nationalists achieved in 2014 (Chart 4). Chart 4Support For Independence Ticks Down, Still Shy Of Majority

United Kingdom Stays United

United Kingdom Stays United

Our takeaway is to fade the Scottish risk. Book gains on our long CHF-GBP tactical trade. Go long British equities relative to DM-ex-US on the expectation of global economic normalization, which is beneficially for the outwardly oriented British multinationals that dominate the British bourse. Does Scotland Have Grand Strategy? The history of Scotland is marked by internal differences that prevent it from achieving unity and independence. Even in the twenty-first century, when many factors have coalesced to make Scottish independence more likely than at any time since the eighteenth century, the 2014 referendum produced a 10% gap in favor of remaining in the United Kingdom. This majority is all the more compelling when viewed from the perspective of geography because cross-regional support for the union is clear (Map 1). Map 1Scottish Independence Referendum Result, 2014

United Kingdom Stays United

United Kingdom Stays United

Why is Scotland always divided? Because it is trapped by the sea and adjacent to a greater power, England. England is usually strong enough to keep Scotland from consolidating power and asserting control over its maritime and land borders. Specifically, Scotland contains a small population (at 5.5 million today) and small economic base (GBP 155 billion in economic output at the end of 2022) dispersed over an inconvenient geography. The low-lying plains around the Firth of Forth that form the historic core of Scotland share a porous border with England. The highlands provide a retreat for Scottish forces during times of conflict, which makes it extremely difficult for southern forces, whether Roman or Anglo-Saxon, to conquer Scotland. But the highlands are equally hard for any standalone Scottish state to rule. Meanwhile the western isles are even more remote from the seat of Scottish power and vulnerable to foreign maritime powers. Since England could never conquer Scotland, its solution was to coopt the Scottish elite, who reciprocated, culminating in a merger of the two monarchies and then the two states in the seventeenth and eighteenth centuries. The British empire provided Scotland with peace, prosperity, and access to the rest of the world. History and geopolitics do not imply that Scottish independence is impossible, i.e. that union with the rest of Britain is inevitable and permanent. The Anglo-Scots union is only 314 or 418 years old, whereas Scotland existed as a recognizable kingdom for roughly six centuries prior to the joining of the crowns in 1603. It is entirely possible for Scotland to secede and break up the union known as Great Britain. The principle of rule by consent and modern democratic ideology make it difficult for London and Westminster to force Scotland into subjection like in the old days. In particular, American hegemony over Europe since WWII and the rise of the European Union have created a pathway for Scottish independence. England is no longer the indispensable gateway to peace and prosperity. Scotland can exist independently under the EU’s economic umbrella and the American security umbrella. Europe has always played a major role in Scotland’s political fate and has always held the key to independence. Independence usually failed because European powers failed to devote large and steady resources to supporting Scotland militarily and economically. France was Scotland’s greatest patron and would lend its support for Scottish rebellion. But France also consistently failed Scotland (and Ireland) at critical junctures when independence might have been obtained. This is because France’s interests lay in distracting England rather than adopting Scotland. Chart 5Scottish Energy Production In Decline

United Kingdom Stays United

United Kingdom Stays United

Today’s unified European continent could be a much greater patron than France ever was alone. The EU could assure Scotland of investment and access to markets even in the face of British resistance. However, the EU is still not politically unified: some members fear separatism in their own borders and therefore tend to oppose Scottish accession. It is possible that the EU could overcome this difficulty but only after a series of major events (on which more below). It took an American empire to clear the way for Irish independence. But Ireland has the moat of the Irish Sea – and the United Kingdom still retained Northern Ireland. Today the United States can be expected to keep its distance from quarrels within the UK or between the UK and EU. However, it does not have an interest in Scottish secession or any other disintegration of the UK, whether from a global security point of view (the West’s conflict with Russia) or even from the point of view of US grand strategy relative to Europe (prevention of a European empire that could challenge the US). An independent Scotland would struggle economically. Its declining base of fossil fuel reserves illustrates the problem of generating sufficient revenue to maintain the Scandinavian-style social welfare state that Scotland’s nationalists imagine (Chart 5). Scottish nationalists are keen to embrace renewable energy – and the Scottish Greens are pro-independence – yet Scotland is not a manufacturing powerhouse that will produce its own solar panels and windmills. In the face of economic difficulties, Scotland would become politically divided like it was for most of its history prior to union with England. England would revert to an obstructive or sabotaging role. It is telling that the Scottish voter turnout in the 2014 independence referendum was very strong – much stronger than in other recent elections and plebiscites, including the Brexit referendum in Scotland (Table 1). The implication is that it is much harder for Scotland to strike out on its own than it appears. Opinion polling cited above suggests that neither Brexit nor the COVID-19 pandemic has moved the needle decisively in the direction of independence. If anything it is the opposite. The Scottish National Party has lost momentum since 2014 and is losing momentum in advance of today’s local election, which has been pitched as the opportunity to make a second go at independence (Chart 6). Table 1Scotland: High Turnout In 2014 Independence Referendum Implies Firm Conclusion To Stay In UK

United Kingdom Stays United

United Kingdom Stays United

Chart 6Scottish National Party Losing Momentum Just Ahead Of Holyrood Election

Scottish National Party Losing Momentum Just Ahead Of Holyrood Election

Scottish National Party Losing Momentum Just Ahead Of Holyrood Election

Bottom Line: History suggests that the geopolitical and macroeconomic barriers to a unified and independent Scottish state are higher and stronger than they may appear at any given time, including the inevitable periods of tensions with England like today. The UK’s Saving Graces A fair question is whether the UK’s decision to leave the EU since 2016 has changed Scotland’s calculus. Brexit may also have affected the international context, reducing the EU’s willingness to intervene on the UK’s behalf and discourage Scottish ambitions. However, a handful of factors supports the continuation of the union despite Scotland’s grievances. The UK proved a boon amid COVID-19: While 62% of Scots voted against Brexit, the COVID-19 pandemic and recession have supplanted Brexit as the nation’s chief cause of concern. The UK and Scotland saw a higher rate of deaths during the biggest waves of the pandemic but now the pandemic is effectively over in the UK and Scotland, in stark contrast with the European Union (Chart 7). The UK has provided a net benefit to Scotland by inventing the vaccine and distributing it effectively (Chart 8). Scottish voters would have been worse off had they left the UK in 2014. Of course, Scottish nationalism is apparent in the fact that voters give the credit to Edinburgh while blaming London over its handling of the pandemic (Chart 9). But the underlying material reality – that being part of the UK provided a net benefit – will discourage independence sentiment. The Scottish Conservative Party and Labour Party are both in favor of sustaining the union and have benefited in opinion polling since the pandemic peaked. Chart 7COVID Deaths Collapse In ##br##United Kingdom

United Kingdom Stays United

United Kingdom Stays United

Chart 8Scotland Benefited From UK Vaccine And Rollout

United Kingdom Stays United

United Kingdom Stays United

Chart 9Scots Praise Edinburgh, Blame London On COVID Handling

United Kingdom Stays United

United Kingdom Stays United

Brexit is a cautionary economic tale: If Brexit is relevant to Scottish voters, it is not the source of grievance that it could have been. Prime Minister Boris Johnson achieved an exit and trade deal at the end of 2019-20 that largely preserves economic ties with the EU. True, the deal has problems that undermine the UK economy and enhance Scottish grievances. But these also serve as a warning to Scots who would attempt to exit the UK, highlighting the economic pitfalls of raising borders and barriers against one’s chief market. The UK’s trade is far more critical to Scotland’s economy than that of the EU (Chart 10). Chart 10Major Constraint On Scottish Independence

United Kingdom Stays United

United Kingdom Stays United

Unlike in the case of the UK and EU, Scotland shares the same currency and central bank with the UK. Scotland’s large banking sector stands to suffer drastically if the Bank of England ceases to be a lender of last resort. This would become a major problem at least until Scotland could be assured of admission into the EU and Euro Area. Otherwise redenomination into a national currency would deal an even greater financial and economic blow. Scots would face a far more painful economic divorce from the UK than the UK faced with the EU. The UK’s fiscal blowout helped Scotland: Since the bank run at Northern Rock in 2007, the UK and Scotland have suffered a series of crises. This instability should discourage risk appetite today when contrasted with the possibility of stimulus-fueled economic recovery. In particular, the UK government is no longer pursuing fiscal austerity – an economic policy that fanned the flames of Scottish secession back in 2012. Indeed, the UK tops the ranks of global fiscal stimulus, according to the change in government net lending and borrowing as reported by the IMF. The UK’s outlier status ensures that Scotland receives more fiscal support than it otherwise would have (Chart 11). A brief comparison with comparable countries – Ireland, Belgium, France, Norway, Portugal – reinforces the point. Chart 11Scotland Benefited From UK Fiscal Blowout

United Kingdom Stays United

United Kingdom Stays United

The UK’s aggressive policy of monetary and fiscal reflation is not a coincidence. It stems from the past two decades’ constitutional and political struggles – it is an outgrowth of domestic instability and populism. It includes an industrial policy, a green energy policy, and other rebuilding measures to combat the erosion of the state in the wake of hyper-globalization. Essentially the UK, even under a Tory government, is now about debt monetization and nation-building. While Scotland would have trouble bargaining for its share of EU resources, it benefits from the UK’s shift to government largesse and can use the threat of independence to receive greater funds from the United Kingdom. Geopolitics discourages a fledgling Scottish nation. Scotland hosts naval and air bases of considerable value to the UK, US, and broader NATO alliance. Former US President Trump’s punitive measures against the European allies and open doubts about the US’s commitment to NATO’s collective security illustrated the dangers of western divisions in the face of autocratic regimes like Russia and China. The US and EU are now recommitting to their economic and security bonds under the Biden administration. Scottish independence would undermine this recommitment and as such the small country would pit itself against the US, EU, and NATO. While the US and NATO would ultimately admit Scotland into collective security, for fear of cultivating a neutral Scotland that could eventually be exploited by Russia, they would likely discourage independence ahead of time to prevent a historic division within the UK and NATO. Chart 12No Urgency For A Second Referendum

United Kingdom Stays United

United Kingdom Stays United

As for the EU, the Spanish government has indicated that it would be willing to make an exception for Scottish independence if it were negotiated amicably with the United Kingdom.2 Such statements are doubtful, however, as any successful secession would lend ideological credibility to Spanish secessionism – not only in Catalonia but also in the Basque country and elsewhere. And Spain is not the only country that harbors deep hesitations over Scottish accession to the European Union. Belgium, Slovakia, and Cyprus could also oppose it. It only takes a single veto to halt the whole accession process. Ultimately the EU could accept Scotland, just as would NATO, to avoid the dangers of having a neutral state in a strategic location. But the point is that Scottish voters cannot be certain. For example, Scotland cannot secure EU accession prior to leaving the UK and yet to leave the UK and fail to achieve EU accession would render it a fledgling. This explains why Scottish voters are not eager to hold a new independence referendum (Chart 12). Bottom Line: The UK offers medical, economic, fiscal, and geopolitical advantages to Scotland that independence would revoke. The context of Great Power struggle with Russia and China means that an independent Scotland would probably ultimately be admitted into NATO and the EU – but Scottish voters cannot be certain, a factor that discourages independence at least in the short and medium run. Scottish Hurdles Table 2 highlights the historic results of Scottish elections according to political party, popular vote share, and share of seats in parliament. Early, tentative signs suggest that the Scottish National Party maxed out in 2011. The party has suffered from a leadership schism, offshoot parties, and a distraction of its key message since 2014. The implication is not only that Scottish independence is on ice for now but also that the tumultuous constitutional disagreements are subsiding and voters want to focus on economic recovery. Table 2Scottish National Party Hit High-Water Mark In 2011?

United Kingdom Stays United

United Kingdom Stays United

If the Scottish National Party manages to form a majority coalition capable of pushing forward a second referendum, it will face several hurdles. It will need a UK Supreme Court ruling on the legality of a referendum. If a referendum is declared legal (as it very likely will be), Scotland will need to forge an agreement with Prime Minister Boris Johnson to hold a referendum. If a referendum eventually is held and passes, an exit will need to be negotiated. In a post-Brexit world, investors cannot assume that any referendum will fail or that a referendum is a domestic political ploy that the ruling party has no serious intention of following through. Nevertheless it is true that the Scottish National Party could use the threat of a referendum to agree to negotiate a greater devolution of power from Westminster. The party could hold up England’s concessions as a victory while retaining the independence threat as leverage for a later date. Devolution in the past has strengthened the independence cause, as in the creation of the Scottish parliament in 1999. After all, a referendum loss would be devastating for the nationalists, whereas the threat of a referendum could yield victories without depriving the nationalists of their reason for being. It is notable that First Minister Nicola Sturgeon promised not to hold a “wildcat” referendum, in which Scotland holds a referendum regardless of what Westminster or the UK Supreme Court say. The implication is that Scottish nationalism is looking for a stable way to exit. But if stability is the hope then there is dubious support for independence in the first place. A wildcat referendum is theoretically still an option but a formal process with popular support is much more likely to result in a successful referendum than an informal process with dubious popular support. Chart 13Scotland’s Chronic Deficits

Scotland's Chronic Deficits

Scotland's Chronic Deficits

If Scottish independence succeeded in any wildcat referendum, an extreme controversy would follow as Edinburgh tried to translate this result to the formal political and constitutional sphere. If the referendum were not recognized by the UK then Scotland would be forced to secede unilaterally at greater economic cost. Otherwise a third referendum (second formal referendum) would need to be held to confirm the results. Any third referendum would be irrevocable. As with Brexit, the secessionists would have to carry one or more subsequent elections to execute the political will in the event of secession. The point for investors is that volatility would be prolonged as was the case with Brexit. A major complication in Scottish independence remains the problem of public finances. Scotland’s fiscal standing is weak. Scotland ran a 9.4% of GDP budget deficit prior to COVID-19, excluding transfers from the UK, which compensates for a gap of about 6% of GDP (Chart 13).3 The country maintains generous social spending alongside a low-tax regime. There is no sign of correction as all Scottish parties are proposing more expansive social spending in the parliamentary election. The Scottish National Party is even proposing universal basic income. Scotland’s emergency COVID deficits are larger than the UK’s as well and projections over the coming years suggest that they will stay elevated. Historically economic growth keeps closely in line with the rest of the UK and there is no reason to believe independence would boost growth. The implication is that Scotland would have to curtail spending or raise taxes to come into line with UK-sized deficits, which are not small (Chart 14).4 Of course Scotland would not embrace austerity unless financial market pressure forced it to do so. Chart 14Scottish Deficit Projected Larger Than UK

United Kingdom Stays United

United Kingdom Stays United

Scotland would become a high-debt economy. Its public debt-to-GDP ratio would be about 97%, on a back-of-the-envelope calculation. Back in 2013 estimates ranged around 80% of GDP.5 The Scottish National Party’s Sustainable Growth Commission projected in 2018 – before the pandemic blew an even wider hole in the budget deficit – that deficits would nearly have to be cut in half (i.e. capped at 5% of GDP and falling) to achieve a 50% debt-to-GDP ratio over 10 years.6 This is not going to happen. Scotland would also have to take on a portion of the UK’s national debt if it were to have an amicable divorce from the UK and retain the pound sterling. But then much of its newfound independence would be compromised from the beginning by legacy debt and monetary policy shackles. Similar restrictions would come with EU and euro membership. Any accession process after the pandemic would require conformity to the EU’s growth and stability pact, which limits deficits and debt. Redenomination into a national currency, as noted, would dilute domestic wealth, zap the financial industry, and self-impose austerity. Bottom Line: Even if the Scottish nationalists manage to put together a pro-independence majority in Edinburgh, they face a complex process in setting up a referendum. Its passage is doubtful based on the current evidence. But obviously in the wake of Brexit investors should not assume that a referendum attempt will fail or that a successful referendum will be thwarted by parliament after a “leave” vote. The timeline for a second referendum is not imminent – and Scottish independence is highly unlikely, albeit possible at some future date given that middle-aged Scots lean in favor of independence. Investment Takeaways We will conclude with two market takeaways: Chart 15UK Stocks Recovering From Referendum Fever

UK Stocks Recovering From Referendum Fever

UK Stocks Recovering From Referendum Fever

Chart 16Hindsight On How To Play A Constitutional Struggle

Hindsight On How To Play A Constitutional Struggle

Hindsight On How To Play A Constitutional Struggle

The UK’s referendum fever has compounded political uncertainty and contributed to negative factors for the UK equity market over the past decade. A segmentation of the FTSE 100 according to country shows that Scottish-based companies’ share prices rolled over in the aftermath of the 2014 referendum, while the non-Scottish segment performed better (Chart 15). The implication is not that the referendum caused stocks to fall but that the 2014 independence push was the result of national exuberance supercharged by high commodity prices. Enthusiasm for independence has been flat since that time. What is clear is that financial markets look even less favorably upon Scottish equities than other British equities – another sign of the economic problems that will ultimately discourage Scottish voters from going it alone. In advance of the Scottish election, we went tactically long the Swiss franc relative to the British pound to capitalize on jitters that we expected to hit the currency. This trade was in keeping with the long fall of GBP-CHF over the past decade (Chart 16). But the stronger forces of global stimulus, vaccination, economic normalization, and recovery will soon provide a tailwind for sterling yet again. Therefore we are booking 1% gains and shifting to a more optimistic outlook on the pound. With the Brexit saga and the COVID crisis in the rear view mirror, and the tail risk of Scottish independence unlikely, the pound can resume its upward trajectory – at least relative to the Swiss franc. International equities and cyclicals are also poised to continue rising as the world recovers. We recommend investors go long the FTSE 100 relative to developed markets excluding the United States. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Jeremy Black, “The Legacy of the Scottish Referendum,” Foreign Policy Research Institute E-Notes, September 22, 2014, fpri.org. 2 See Akash Paun et al, "Scottish Independence: EU Membership And The Anglo-Scottish Border," Institute For Government, March 2021, instituteforgovernment.org.uk. 3 See Eve Hepburn, Michael Keating, and Nicola McEwen, "Scotland’s New Choice: Independence After Brexit," Centre on Constitutional Change, 2021, centreonconstitutionalchange.ac.uk. 4 See David Phillips, "Updated projections of Scotland’s fiscal position – and their implications," Institute for Fiscal Studies, April 29, 2021, ifs.org.uk. 5 Granting that the UK’s general government gross debt stood at GBP 1.88 trillion at the end of 2020, and assuming that Scotland takes on a share of this debt equivalent to Scotland’s share of the UK’s total population and output (roughly 8%), the Scottish debt would stand at GBP 150 billion out of a Scottish GDP at current market prices of GBP 156 billion, or 97% of GDP. For the 2013 estimate of at least 80% of GDP, see David Bell, "Scottish Independence: Debt And Assets," Centre on Constitutional Change, December 3, 2013, centreonconstitutionalchange.ac.uk. 6 Scottish National Party, "Part B: The Framework & Strategy for the Sustainable Public Finances of an Independent Scotland," Sustainable Growth Commission, May 2018, sustainablegrowthcommission.scot. The commission’s debt curbs will have to be revised in the wake of COVID-19. For discussion see Chris Giles and Murie Dickie, "Independent Scotland would face a large hole in its public finances," Financial Times, April 2, 2021, ft.com.

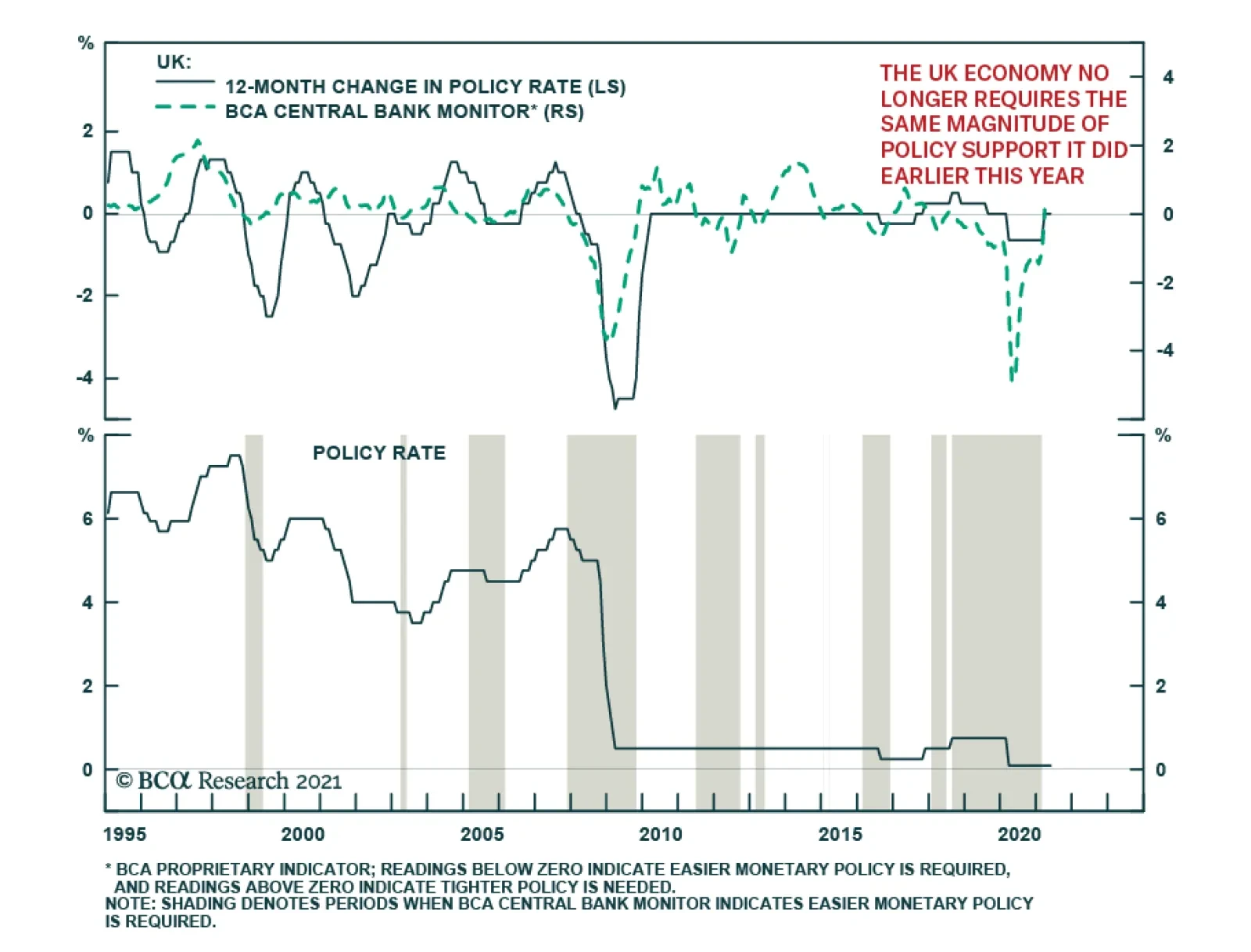

As expected, the Bank of England maintained the bank rate at 0.1% and kept the total target stock of asset purchases unchanged at its Thursday meeting. However, the central bank upgraded its growth outlook and now forecasts GDP to rise 7.25% in 2021 – up from…

Biden’s first 100 days can be summed up as the return of Big Government, i.e. “the Leviathan.” But markets are not afraid of one-off corporate tax hikes that only partially reverse the previous administration’s tax cuts amid a brand new stimulus-charged economic cycle. Biden’s approval rating after his first 100 days is comparable to that of Presidents Bill Clinton and George W. Bush, suggesting that he can accomplish a major legislative achievement. The $2.3 trillion American Jobs Plan will be watered down in Congress but not to a great extent. Green energy investments and funding for research and development will survive. Thus Biden’s plan will sow the seeds of a productivity mini-boom, if not a structural boom, in the 2020s. Republicans are favored to win the midterm elections in 2022 but investors should not make any decisions based on that expectation. The risk of Democrats keeping the House of Representatives – and therefore having a new chance to surprise with taxes in the second half of Biden’s term – is much greater than the historical pattern suggests. Stick with our long materials versus tech trade. Stick with short health care trades. Go long renewable energy stocks. Feature President Biden passed the 100 day mark at the end of April. The most striking characteristic of his administration is the giant deficit spending. Biden marks the symbolic return of the “leviathan,” i.e. the state, to American political economy. Normally the budget deficit tracks closely with the unemployment rate because rising unemployment causes tax revenue to fall and government spending to rise. The divergence between the deficit and unemployment became pronounced in 2016 and revealed the structural forces – e.g. slow growth, disinflation, high debt, inequality, populism – driving US policymakers to abandon fiscal discipline. But the 2016-20 political cycle combined with the pandemic broke the dam and the divergence is now gigantic (Chart 1). Chart 1Biden's First 100 Days: An Historic Divergence

Biden's First 100 Days: An Historic Divergence

Biden's First 100 Days: An Historic Divergence

All else equal, the implication is inflationary, though inflation will respond to a range of factors on different time frames. Signs of inflation today may well be under control, as Federal Reserve Chairman Jay Powell and Secretary of Treasury Janet Yellen believe, but over the long run we take the inflation risk seriously as the policy elite has fundamentally shifted to be vigilant about deflation, not inflation. Biden’s Approval Is “Just Enough” Biden’s popularity is “fair to middling” as his honeymoon comes to an end. His approval rating clocks in right between that of Presidents Barack Obama and Donald Trump (Chart 2A). He is not as popular and charismatic as Obama and not as unpopular and controversial as Trump. His approval among Democratic voters is higher than that of Obama, similar to Trump among Republicans, due to the fact that the US has hit historic levels of political polarization (Chart 2A, second panel). His embrace of left-wing policy is keeping him in good standing among Democratic voters but may become a liability during the 2022 midterm election (more on that below). Chart 2ABiden’s Approval Rating: Fair-To-Middling

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Chart 2BBiden Close To Clinton, Bush At 100 Days

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

American presidential approval ratings have fallen continuously for decades and they typically fall after inauguration. This is true of Biden but he looks more like Presidents Bill Clinton or George W. Bush than Trump. His approval is likely to stay over 50% for the foreseeable future due to a supercharged economic recovery (Chart 2B). Trump stands out conspicuously in this chart for his negative net approval, which implies that on a relative basis Biden will be more capable in conducting policy. And yet Trump got his signature piece of legislation – the Tax Cut and Jobs Act – through Congress, which has some bearing on Biden’s proposals. Our political capital index (Appendix) shows that Biden will benefit from consumer confidence and wage growth shooting up, business sentiment strengthening, and polarization slightly abating due to a slight rise in Republican approval. While Biden’s Democratic Party has only the narrowest of majorities in the Senate, Biden’s signature legislative proposal – the American Jobs Plan – still has an 80% chance of passing in some form. Senate minority leader Mitch McConnell of Kentucky declared this week that Biden will not get any Republican votes for this package of infrastructure and corporate tax hikes but budget reconciliation is a ready way for the bill to pass on a partisan basis. Biden’s fiscal blowout should be seen as the culmination of a popular shift against fiscal discipline (or “austerity”) that took root in the middle of the last decade and was also expressed by Republican support for the big-spending President Trump. But it is more extravagant than what the Republicans proposed or would have been able to get had Trump been elected. Chart 3 highlights the difference between the Democratic and Republican spending proposals for the early 2021 COVID-19 relief bill and infrastructure plan. Chart 4 highlights the corporate tax increases Biden has proposed in excess of the Trump rate. Chart 3Biden’s Spending In Excess Of Republican Plans

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Chart 4Biden’s Taxes In Excess Of Republican Plans

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

From an investment point of view, now is the perfect time to raise corporate taxes as the early cyclical surge in economic activity will prevent the one-off hit to earnings, which should be around 5%-8% according to our Global Investment Strategy, from hindering the stock market for long. The output gap, apparent from still relatively low industrial capacity utilization, will rapidly be plugged regardless of the tax hikes, as is evident from the surge in retail sales and core capital goods new orders and the decline in fuel inventories (Chart 5). The hyper-stimulated economy has been a key reason for our argument that Biden will mostly get what he wants, in terms of corporate taxes, since growth will be fine. The public is positively crying out for taxing corporations, as we showed in our April 7 missive and other reports. Chart 5The Output Gap Will Close Quickly

The Output Gap Will Close Quickly

The Output Gap Will Close Quickly

Given that Biden’s political capital is only “just enough,” and that it is falling over time, many investors believe that Biden’s major legislative proposals will be watered down beyond recognition. They will be watered down but the reconciliation process ensures that Democrats will pass at least one bill and that it will largely gratify the party’s preferences. And any watering down will affect tax hikes more so than spending, since tax hikes are the most controversial parts of the bill for moderate Senate Democrats. As Table 1 reveals, an infrastructure package with half the revenue increase is a $1.3 trillion addition to the budget deficit over the eight-to-15 year life-cycle of the bill, as opposed to a fictitious $341 billion in the event that all tax hikes pass Congress. Hence the paring back of Biden’s ambitions does not imply fiscal restraint and is not bullish for US Treasuries. Table 1Watering Down Biden’s Proposals Not Good For Deficit

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

A Productivity Boomlet How can we benchmark the magnitude of the structural transformation taking place in the US as a result of Biden’s Leviathanic spending proposals? From the perspective of government spending as a contributor to economic output, the Leviathan shrank in the decades after President Lyndon B. Johnson’s “Great Society” and Vietnam debacle. But from the perspective of government accounts, Big Government never actually went away (Chart 6), as Reagan used spending to win the Cold War and Clinton only enjoyed the briefest hiatus from deficits in the 1990s. From these charts we can conclude that Biden’s administration will create unprecedented spending and deficits that, taken with an extremely accommodative Fed, will increase the risk of substantially higher inflation over the 2020s. Chart 6Johnson’s ‘Great Society’ Versus Biden’s ‘Green Society’

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Chart 7US Adds To Expansive Social Safety Net

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Biden is not fighting an economic depression and world war, like Franklin D. Roosevelt, although the US has experienced a Great Recession and is entering a new cold war with China. So the shift should be seen as a generational change in the role of government and not as an ephemeral, four-year trend. This is true notwithstanding the fact that the US already spends a lot on health and education (Chart 7) and not as an ephemeral, four-year trend. The element of international competition is critical to the unique components of Biden’s spending package. Biden jettisoned the health care debates of the Obama era – to our surprise – and instead inaugurated the American foray into the global green energy race. Looking at the OECD’s measure of the “greenness” of global fiscal stimulus – and supplementing it with Biden’s proposed jobs plan – the US compares favorably with the EU and China (Chart 8). Chart 8US Enters The Green Energy Race

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

True, climate policy is more controversial in the US, which means it may well be frozen after Biden’s major bill. The EU and China will spend more on renewable energy and environmental protection because they are net energy importers and manufacturing powers. But the US is highly unlikely to exit the green race in the future, as younger generations care about it more than their elders and it is connected to the US strategic imperative of technological leadership. Biden will have opened up a new field of national policy, regardless of where on the field the players will fight over the ball at any given time. Biden is also pumping federal money into research and development, another area of geopolitical competition (Chart 9). The takeaway is that Biden’s first year in office – which may be his most consequential year in terms of legislation, particularly if he is a one-term president – is sowing the seeds for a productivity boom, or at least a mini-boom, in the coming years (Chart 10). The pace of productivity growth in the coming years is a matter of speculation and the long term trend is down. But the expected cyclical increase should be supplemented with the knowledge that the US is now aggressively monetizing debt, aggressively pursuing industrial policy and technological advancement, and aggressively competing with geopolitical rivals like China (and even allies like the EU). The likelihood of productivity breakthroughs may go up in such an extraordinary context. We cannot know but we cannot discount the possibility. Chart 9US Doubles Down On Tech Race

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Chart 10Productivity Will Rise Cyclically But What About Structurally?

Productivity Will Rise Cyclically But What About Structurally?

Productivity Will Rise Cyclically But What About Structurally?

Vaccines And Immigration Elsewhere Biden’s first 100 days are less specific to his administration. The US is performing very well on the pandemic, both in innovating vaccines and distributing them, but an objective analysis will force Biden to share the credit with the Trump administration (Chart 11). On immigration, by comprehensively weakening enforcement and raising refugee allowances, all in the midst of a surging American economy, Biden will be vulnerable to Republican accusations of encouraging a humanitarian crisis on the border, vitiating rule of law, and making a cynical ploy to expand the Democratic voter base. The number of southwest border encounters by the Customs and Border Protection agency began to skyrocket over the past year – and as such it reflects structural factors that would have troubled a second Trump administration as well. But the election seems to have had an impact based on the inflection point in the data at the end of 2020 (Chart 12). Chart 11COVID-19 Vaccination Campaign On Track

COVID-19 Vaccination Campaign On Track

COVID-19 Vaccination Campaign On Track

Chart 12Immigration: Biden's Fatal Flaw?

Immigration: Biden's Fatal Flaw?

Immigration: Biden's Fatal Flaw?

Regardless, Biden has made the decision to cater to the pro-immigration side of his party and will now own this trend. It will be a unifying force for Republicans, although they remain deeply split over a range of issues and are not any closer to healing their wounds. The market impact is limited in the short run. In the medium run, if unchecked immigration feeds the nativist and populist elements of the Republican Party, then Biden’s decision could have a substantial impact on future US policy by generating a backlash. Our best guess at the moment is that Biden’s actions will reinforce the Republican Party’s embrace of Trump’s policy platform. Since Biden is not making major bipartisan legislative efforts to reform immigration comprehensively, the great immigration debate will return in 2024 or thereafter. Public opinion suggests Republican nativism is out of fashion but a large influx of immigrants could opinion over time as today’s issues fade. Thus Biden’s successes on economic recovery today are sowing the seeds of his party’s biggest vulnerability in domestic policy in future. But admittedly it is too soon to say whether this weakness will be effectively exploited by the opposition. In the meantime investors and corporations will cheer the prospect of cheap and abundant labor. An Overlooked Market Risk From The Midterm Elections This overview of Biden’s honeymoon period naturally refers to the 2022 midterm elections in several places. The Republicans will not be able to repeal Biden’s laws if they take the House of Representatives – or less likely the Senate – in the 2022 vote. But they will be able to grind proposals to a halt. The fate of Biden’s third major legislative proposal, the $1.8 trillion American Families Plan, will hang in the balance, as will green energy subsidies, the child tax credit, and various social initiatives. Much has been made about the 2020 US census and the reapportionment of seats in the House of Representatives according to the population. States that have a single party in control of the governor’s mansion and the legislature can gerrymander or redraw congressional districts as they please to favor their party. Table 2 shows that this partisan process could easily yield two Republican seats on a net basis. This is less than expected but Republicans only need a net of five seats to reclaim the House. Table 2US Census And Reapportionment Favors Republicans Slightly

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Redistricting is an important theme because it perpetuates political polarization. But it is not important in determining who will win the House in 2022. The House has changed hands numerous times despite gerrymandered districts. Midterms almost always work against the president’s party. Only in 1934, during the Great Depression, and 2002, immediately after the Twin Towers were attacked, did voters strengthen a first-term president’s hold on Congress. Judging by Biden’s approval rating, Democrats would be lined up for a loss of far more than five seats on a net basis in 2022. They could lose 20 or more (Chart 13). As noted in the previous section, Republicans may find a rallying point on immigration. Chart 13Midterm Elections Dominated By Opposition Party – And Need For Checks And Balances

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Having said that, investors should not make any decisions based on the midterm election. While Republicans have a 95% chance of winning the House according to the modern historical pattern, they have a lower 73% chance according to the online political betting hub Predictit.org, and we would side with the latter or even lower, at this early stage in the political cycle. The pandemic and social unrest of 2020, combined with the slow-growth 2010s and trade war, create a context of upheaval that is not entirely dissimilar to the exceptional midterm elections of 1932 and 2002. Biden’s rescue packages and the economic recovery will be a huge boon for the Democratic Party in 2024 and it is possible that they will reap some benefits even in 2022. This is especially the case because Trump and his allies will challenge establishment and elitist Republicans in the primary elections, which could result in Republicans losing five-to-nine seats. If they put up Trumpists in competitive, purple, or suburban districts, voters will swing toward moderate Democrats over populist Republicans in order to preserve the “bread and butter” gains of Biden’s agenda. The bottom line is that Republicans are favored to take the House in 2022 but the 75% odds are much more realistic than the 95% historical probability and possibly even too high. Gridlock would freeze Biden’s spend-and-tax agenda in place but the absence of gridlock would come as a surprise to investors who counted on a Republican victory. Tax hikes on wealthy individuals and capital gains – as projected in the American Families Plan – could still be on the table after the midterm. These tax hikes would still be unlikely to overturn the equity bull market but they could cause investors to reassess the overall policy setting for the worse. The implication would be that the 2020 political change marked a more lasting leftward shift in US policy. For example, taxes could go up beyond what Biden currently projects. Midterm risks should not trouble investors in the near term but they should be on the radar, particularly as the Republican primaries get underway next year and as investors get a better read on inflation in the wake of Biden’s mammoth spending. Investment Takeaways We would draw a few main investment takeaways from Biden’s first 100 days. In the short run, we would call attention to the “buy the rumor, sell the news” behavior exhibited by financial markets during President Trump’s first year in office with full party control of Congress. US equities stood to benefit from tax cuts, especially relative to the rest of the world, which would not receive tax cuts but could face trade tariffs. This expectation played out after Trump’s election but the market sold upon the news of his inauguration. It played out again after Republicans failed to repeal Obamacare, suggesting they might fail to cut taxes. The market correctly bid up US equities on the rumor that the GOP would then turn its full attention to cutting taxes. US equities outperformed until the end of the year when the tax cuts became a fait accompli, at which point the news was sold (Chart 14, top panel). The implication today is that US stocks, especially cyclical stocks and infrastructure-related plays, will continue generally to rally ahead of Biden signing the American Jobs Plan into law, likely around November. Obviously a correction could occur at any time but upon the signing of the law one should not be surprised to see some serious profit-taking. An analogy can also be drawn to renewable energy plays after the Democrats’ “Blue Sweep” in 2020. Markets have largely discounted the surge in renewable energy plays that occurred upon the recession in 2020 and the rising likelihood that Trump would lose reelection (Chart 14, bottom panel). This creates a buying opportunity for a long-term theme. Republicans will not be able to repeal Biden’s green projects and there is some risk that Democrats retain legislative control. And younger generations, even Republicans, are favorable toward the greening of society. Therefore we recommend going long US renewable energy stocks. It also follows that cyclical and value stocks have not yet exhausted their run against defensives and growth stocks. We will therefore hang onto our long materials / short Big Tech trade until we see more substantial signs that near-term disinflationary risks will derail this trade (Chart 15). We will also stick with our short managed health care trade – and our preference for health care equipment and facilities within the health care sector – despite the Democrats’ tentative decision to sideline the health care policies that would have hit the health insurers and Big Pharma. Chart 14Investment Takeaways: Buy The Green Hype (For Now)

Investment Takeaways: Buy The Green Hype (For Now)

Investment Takeaways: Buy The Green Hype (For Now)

Chart 15Housekeeping: Stick With Materials Over Tech

Housekeeping: Stick With Materials Over Tech

Housekeeping: Stick With Materials Over Tech

In the long run, we would point out that the shift away from Reaganism toward Johnsonianism – the return of Leviathan – is a lasting trend that will bring significant change to the US policy setting. These are mostly but not all inflationary. Larger immigration and a productivity boost are not inflationary. But large deficits, tax hikes, and wage pressures are inflationary. Therefore the risk of inflation has gone up in a historic way even though the magnitude of the risk can be overstated in the short term – when there is still slack in the economy – and there are still disinflationary factors that could work against the risk as events unfold. We remain cyclically bullish. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1USPS Trade Table

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Table A2Political Risk Matrix

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Table A3Political Capital Index

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Table A4APolitical Capital: White House And Congress

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Chart A4BPolitical Capital: Household And Business Sentiment

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Table A4CPolitical Capital: The Economy And Markets

Leviathan: Biden's First 100 Days

Leviathan: Biden's First 100 Days

Highlights A slower money and credit growth in China will eventually generate disinflationary pressures by weighing on demand for commodities. The PBoC has shifted its inflation anchor and policy framework to target core CPI and the PPI rather than headline CPI. Beijing is scaling back its fiscal supports and cooling the property sector to tackle local government and housing sector debt issues. In the next six to nine months we favor companies and sectors that will benefit from global economic recovery rather than China’s domestic demand. We are long CSI500 relative to China’s A shares. The CSI500 has a larger exposure to the global economy and lower valuation relative to China’s broad onshore market. Feature As a follow up to last week’s report, we look at another topic raised in recent client meetings: whether rapidly rising producer prices in China will morph into a broad-based inflationary risk and how macroeconomic policies will evolve to counter such a risk. Clients who believe that the ongoing producer price inflation is transitory cited China’s low consumer price inflation, and slowing money and credit growth, as leading indicators of budding disinflationary pressures. Advocates of sustained inflation pointed to robust recoveries and demand among advanced economies, extremely accommodative monetary conditions worldwide, massive fiscal stimulus in the US, a weak US dollar, and supply constraints. It remains to be seen what the worldwide pandemic’s impact will be on the balance between global production capacity and aggregate demand. In this report we analyze the PBoC’s inflation target and policy framework, and conclude that while China’s monetary policy has not become more hawkish, policy tightening seems to be taking place on the fiscal front. Is Inflation In China A Risk? It is debatable whether the strong rebound in GDP growth in Q4 last year and in Q1 this year has closed China’s output gap and will lead to widespread inflation. Given data distortions due to low-base effects from the previous year and uncertainty about China’s productivity and labor force growth, any calculation of the output gap will be unreliable. In addition, China’s employment statistics lack cyclicality and cannot be used to gauge inflationary pressure stemming from wage growth and unit labor costs. Chart 1A Rollover In Credit Growth Will Weigh On Chinese Demand For Commodities

A Rollover In Credit Growth Will Weigh On Chinese Demand For Commodities

A Rollover In Credit Growth Will Weigh On Chinese Demand For Commodities

Our cyclical view of inflation is therefore based on the framework that the ongoing moderation in China's money and credit growth will eventually generate disinflationary pressures by weighing on the country’s demand for and price of commodities (Chart 1). Furthermore, behind a resilient PPI, there are suggestions that the strength in China’s economy is still bifurcated. A narrow-based uptrend in the PPI lacks the ground for sustained inflation, and is unlikely to trigger a general tightening in monetary policy. While mounting global prices for raw materials propelled strong upstream PPI, producer prices for consumer goods and core consumer price inflation remain very subdued (Chart 2). The inconsistency in producer prices among various industries highlight the unevenness of the economic recovery and, importantly, persistently muted household consumption (Chart 3). Chart 2A Bifurcated Economic Recovery

A Bifurcated Economic Recovery

A Bifurcated Economic Recovery

Chart 3A Muted Recovery In Household Consumption

A Muted Recovery In Household Consumption

A Muted Recovery In Household Consumption

Chart 4Weak Price Transmission From Upstream To Downstream Industries

Weak Price Transmission From Upstream To Downstream Industries

Weak Price Transmission From Upstream To Downstream Industries

The transmission from upstream industrial PPI to the middle and downstream sectors has also been weak (Chart 4). It is evidenced in the faster growth of manufacturing output volume compared with price increases (Chart 5). This contrasts with the previous inflationary cycles, as well as mining and ferrous metals where surging prices for raw materials have way surpassed recovery in output volume (Chart 6). Given that price changes are more important to corporate profits than volume changes, Chinese middle-to-downstream industries face downward pressure on their profit margins and will likely deliver disappointing profits, despite a strong rebound in production. Chart 5China's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

China's Manufacturing Recovery: Stronger Volume Than Prices

Chart 6China's Upstream Industries: Prices Surged Faster Than Production

China's Upstream Industries: Prices Surged Faster Than Production

China's Upstream Industries: Prices Surged Faster Than Production

Furthermore, PMI input prices, which lead core CPI by about nine months, rolled over in April (Chart 7). While it is too soon to conclude that input prices have peaked, it is implied that upward pressure on core CPI from input prices may start to ease in 2H21. Bottom Line: So far there is no sign that elevated upstream producer prices will create sustainable inflationary pressure on consumer prices. Hence our view is that the PBoC will not respond to a rising PPI by further tightening monetary policy. Chart 7PMI Input Prices Have Rolled Over

PMI Input Prices Have Rolled Over

PMI Input Prices Have Rolled Over

Chart 8Core CPI And PPI Have Been The PBoC's Inflation Targets Since 2015

Core CPI And PPI Have Been The PBoC's Inflation Targets Since 2015

Core CPI And PPI Have Been The PBoC's Inflation Targets Since 2015

The PBoC’s Inflation Target Since 2015, China’s monetary tightening cycles have closely correlated with a combination of the core CPI and PPI instead of headline CPI (Chart 8). The shift to targeting core CPI and PPI occurred despite the central bank’s frequent mention of headline CPI as its inflation target. The reasons for the shift are twofold. First, swings in food and fuel prices have become much larger since 2014, often dominating fluctuations in headline CPI (Chart 9). Secondly, the price swings were often driven by supply-side factors and did not reflect changes in demand. Therefore, monetary policies could do little to mitigate inflationary or deflationary pressures. Furthermore, the PPI seems to play a greater role in the PBoC’s monetary policymaking than the headline and core CPI (Chart 10). The tighter relationship between the de facto policy rate and the PPI is not surprising, given that China’s ex-factory price inflation reflects changes in corporate pricing, profit, and inventory cycles – all are driven by the country’s money supply and credit cycles. Chart 9Large Swings In Food And Energy Prices Distorted Headline CPI In Recent Years

Large Swings In Food And Energy Prices Distorted Headline CPI In Recent Years

Large Swings In Food And Energy Prices Distorted Headline CPI In Recent Years

Chart 10PPI Plays A Greater Role In The PBoC's Monetary Policymaking

PPI Plays A Greater Role In The PBoC's Monetary Policymaking

PPI Plays A Greater Role In The PBoC's Monetary Policymaking

The relationship between the 7-day repo rate - the de jure policy rate - and the PPI has broken down since 2015 (Chart 11). Meanwhile, the 3-month repo rate has maintained a close relationship with the PPI (Chart 10, bottom panel). The change in the relationship is because the PBoC shifted its policy to target interest rates instead of the quantity of money supply since 2015 (Chart 12). Moreover, since 2016 the PBoC has generated monetary policy tightening measures through changes in its Macro Prudential Assessment Framework (MPA) rather than directly through interest rate hikes. Chart 11Relationship Between The 7-Day Repo Rate And The PPI Has Broken Down Since 2015...

Relationship Between The 7-Day Repo Rate And The PPI Has Broken Down Since 2015...

Relationship Between The 7-Day Repo Rate And The PPI Has Broken Down Since 2015...

Chart 12...Due To Monetary Policy Regime Shifted

...Due To Monetary Policy Regime Shifted

...Due To Monetary Policy Regime Shifted

Bottom Line: The PBoC has shifted its inflation anchor and policy framework since 2015. Core CPI and the PPI are now the main inflation targets. A Quiet Fiscal Tightening? Despite a jump in the PPI, the 3-month repo rate fell sharply in the past two months (Chart 10 on page 6, bottom panel). It is possible that the PBoC considers escalating producer prices as transitory and, therefore, intends to keep its overall policy stance unchanged. However, the PBoC’s relaxed policy response towards inflation risk may be explained by Beijing’s quiet tightening on the fiscal front. Chart 13The Central Bank Has Made Little Interbank Liquidity Injections Lately

The Central Bank Has Made Little Interbank Liquidity Injections Lately

The Central Bank Has Made Little Interbank Liquidity Injections Lately

The PBoC can hold its policy rates steady by supplying adequate liquidity to the interbank system through open market operations or by reducing the demand for liquidity. On a net basis, the PBoC has recently injected very little liquidity into the interbank system, implying that banks’ liquidity demand has likely softened (Chart 13). This might be a sign of weakening credit origination. In a previous report we discussed how fiscal stimulus has become a more relevant driver of China’s credit origination since the onset of the 2014/15 economic downcycle. A rising 3-month SHIBOR can be the result of rapid fiscal and quasi-fiscal expansions, which occurred in Q3 last year. A flood of local government bond issuance drained liquidity from commercial banks, which boosted the banks’ needs to borrow money from the interbank system and pushed up interbank rates. Despite higher interest rates, credit growth soared in Q3 as fiscal multiplier provided an imminent and powerful reflationary force to the economy. In contrast, local government bond issuance was down sharply in the first four months of this year, compared with 2019 and 2020. Local governments sold 222.7 billion yuan of special-purpose bonds (SPBs) from January to April, a plunge from 730 billion yuan of debt sold in the same period in 2019 and 1.15 trillion yuan in 2020. The total local government bond issuance in Q1 this year has also been 36% and 44% lower than in Q1 2019 and 2020, respectively. A lack of local governments’ appetite to borrow coupled with a shortage in profitable infrastructure projects might have contributed to the sharp drop in bond issuance this year. Local government financing and spending have been under increased scrutiny this year. Following the State Council Executive Meeting in late March, in which Premier Li Keqiang pledged to reduce government leverage ratio and raise regulatory standards on infrastructure investment, Beijing suspended two high-speed rail projects that were initiated by provincial governments. Messages from Politburo’s meeting last week reinforced our view that policymakers may be scaling back fiscal support while further tightening regulations in the property sector. Both aspects have the potential to cool China’s demand for industrial metals and global industrial material prices (Chart 14 and Chart 15). Chart 14A Slowdown In Chinese Manufacturing Demand Will Have A Greater Impact On Global Industrial Material Prices

A Slowdown In Chinese Manufacturing Demand Will Have A Greater Impact On Global Industrial Material Prices

A Slowdown In Chinese Manufacturing Demand Will Have A Greater Impact On Global Industrial Material Prices

Chart 15Lower Housing Demand In China Will Help To Cool Industrial Metal Prices

Lower Housing Demand In China Will Help To Cool Industrial Metal Prices

Lower Housing Demand In China Will Help To Cool Industrial Metal Prices

We expect the intensity of policy tightening to reach its peak between mid-year to third-quarter 2021. It is unclear at this point whether policymakers are willing to allow local governments to significantly undershoot their SPB quota for this year. Local governments reportedly experienced a shortage in profitable investment projects towards the end of last year, and thus, parked more than 10% of proceeds from 2020 SPB issuance at the central bank. The central government may be taking a wait-and-see attitude this year, and saving more fiscal dry powder for later this year when the economic slowdown becomes more meaningful. Bottom Line: Beijing is pulling back its fiscal supports and cooling the property sector to tackle local government and housing sector debt issues. The deleveraging efforts will curb China’s demand for commodities, and may work to ease inflationary pressure on prices for raw materials. Investment Conclusions The outlook for China’s risk asset prices remains bearish, at least in the next six months. If the credit and fiscal impulse slow enough to depress corporate pricing power, inflation will not be a problem because disinflationary pressures will resurface. However, the growth of corporate profits will disappoint (Chart 16). Beijing may be saving more fiscal dry powder for later this year. Still, SPBs are only a small part of local governments’ financing source for infrastructure projects. Given the central government’s renewed focus on reducing public debt, policymakers are unlikely to unleash fiscal power to significantly boost infrastructure spending or economic growth. In the next six to nine months, we favor companies and sectors that will benefit from global economic recovery rather than China’s domestic demand. With this week's report, we initiate a long position on the CSI500 index, which has a larger exposure to the global market and lower valuation relative to China’s broad onshore market (Chart 17). Chart 16Aggregate Corporate Profit Growth Will Slow Even Though Inflation Is No Longer An Issue

Aggregate Corporate Profit Growth Will Slow Even Though Inflation Is No Longer An Issue

Aggregate Corporate Profit Growth Will Slow Even Though Inflation Is No Longer An Issue

Chart 17Long CSI500/Broad Market

Long CSI500/Broad Market

Long CSI500/Broad Market

Jing Sima China Strategist jings@bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Highlights Sweden’s economic recovery is robust and will deepen. Policy is accommodative. Very few advanced economies will benefit as much from the global economic rebound. The labor market will tighten, capacity utilization will increase, and inflation will rise faster than the Riksbank forecasts. On a one- to two-year investment horizon, the SEK is a buy against both the USD and the EUR. Despite their pronounced outperformance, Swedish stocks possess significantly more upside against both Eurozone and US equities over the remainder of the cycle. Swedish industrials will beat their competitors in both these markets. Nonetheless, China’s policy tightening creates a meaningful tactical risk, which selling Norwegian stocks can hedge. Italy’s fiscal plan constitutes a new salvo in Europe’s efforts to avoid last decade’s mistakes. Feature Last week, the Swedish Riksbank did not follow in the footsteps of the Norges Bank. The Swedish central bank acknowledged that the economy is performing better than anticipated and that the housing market is gaining in strength; yet, it refrained from hinting at any forthcoming adjustment to its policy rate or the pace of its asset purchase program. The positive outlook for the Swedish economy will force the Riksbank to tighten policy significantly before the ECB. As a result, we expect the Swedish Krona to outperform the euro and the US dollar. Moreover, investors should continue to overweight Swedish equities due to their large exposure to industrials and financials, even if they have already significantly outperformed the Euro Area. Sweden’s Economic Outlook The Swedish economy will accelerate, which will put pressure on resource utilization and fan inflationary risk in the years ahead. The degree of stimulus supporting Sweden is consequential. Chart 1A Dual Labor Market

A Dual Labor Market

A Dual Labor Market

On the fiscal front, the government support measures that have been announced since the beginning of the COVID-19 crisis currently amount to SEK420bn, or SEK197bn for 2020 (4% of GDP), and SEK223bn for 2021 (4.5% of GDP). Moreover, generous labor market protection and part-time employment schemes meant that the number of employees in permanent employment contracts remained stable during the pandemic (Chart 1). Thus, the bulk of the rise in Swedish unemployment came from workers on fixed-term contracts. Monetary policy remains very accommodative as well. The Riksbank left its repo rate unchanged at 0% through the crisis, but cut its lending rate from 0.75% to 0.1%. More importantly, the Swedish central bank is aggressively injecting liquidity into the economy. It set up a SEK500bn funding-for-lending facility in order to incentivize bank lending to the nonfinancial private sector, and started a SEK700bn QE program, which as of Q1 2021 had purchased SEK380bn securities and which will purchase another SEK120bn in Q2, with covered bonds issued by banks accounting for 70% of it. As a result, the amount of securities held on the Riksbank balance sheet will nearly triple by year end (Chart 2). Chart 2The Riksbank Is Open For Business

Take A Chance On Sweden

Take A Chance On Sweden

Beyond the monetary and fiscal stimulus, many factors point to greater economic strength for Sweden. Despite a slow start to the process, as of last week, nearly 30% of the Swedish population had received at least one vaccine dose, which is broadly in line with vaccination rates prevalent in France or Germany. Crucially, the pace of vaccination is accelerating at a rate of 13% per week. Even if this second derivative slows, more than 70% of the population will have received at least one dose by this summer. Thus, greater mobility is in the cards during the second quarter, which will boost household spending. Chart 3The Wealth Effect

The Wealth Effect

The Wealth Effect

The housing market also favors a pick-up in consumption. The HOX housing price index is growing at a 15% annual rate, its fastest expansion in over 5 years. As a result of the wealth effect, this rapid appreciation is consistent with a swift improvement in the growth rate of household expenditures (Chart 3). Moreover, spending on durable goods now stands 1.3% above its pre-pandemic levels, while spending on non-durables is back to pre-pandemic levels. This context suggests that increased mobility translates into greater spending. The industrial sector remains a particularly bright spot in the Swedish economy. Sweden is extremely sensitive to the global industrial and trade cycle, because exports represent 45% of GDP. Moreover, the highly cyclical intermediate and capital goods comprise 56% of the country’s foreign shipments, which accentuates the beta of the Swedish economy. BCA Research remains optimistic about the global industrial cycle. Sweden will reap a significant dividend. Already the Swedish PMI points to stronger industrial production, and the index’s exports component is roaring ahead (Chart 4). The potential for a greater uptake in consumption, capex, and durable goods spending in the rest of the EU (Sweden’s largest trading partner) bodes well for the Swedish manufacturing sector. Additionally, if the collapse in the US inventory-to-sales ratio is any indication for the rest of the world, a global restocking cycle is forthcoming, which will further boost Swedish industrial activity (Chart 4, bottom panels). Finally, global public infrastructure plans are on the rise, which will also help Sweden. Chart 4Sweden Is well Placed

Sweden Is well Placed

Sweden Is well Placed

Chart 5Brightening Labor Market Prospects

Brightening Labor Market Prospects

Brightening Labor Market Prospects

In this context, the Swedish labor market should tighten significantly in the approaching quarters. Already, job vacancies are rebounding, and redundancy notices have normalized, which matches both the GDP growth surprise in Q1 and the continued rise in the NIER Sweden Economic Tendency Indicator. Furthermore, the employment component of the PMIs stands at 58.9 and is consistent with a sharp improvement in job growth over the coming year (Chart 5). The expected labor market growth will contribute to an increase in capacity utilization, which will place upward pressure on wages and inflation. When the 12-month moving average of US and Eurozone imports rises, so does the Riksbank Resource Utilization Indicator, because global trade has such a pronounced effect on the Swedish economy (Chart 6). Meanwhile, greater resource utilization leads to accelerated inflation, greater labor shortages, and rising unit labor costs (Chart 7). Chart 6CAPU Will Rise

CAPU Will Rise

CAPU Will Rise

Chart 7The Coming Pressure Buildup

The Coming Pressure Buildup

The Coming Pressure Buildup

Bottom Line: As a result of generous stimulus and the global economic recovery, the Swedish economy is set to continue its rebound. Consequently, employment and capacity utilization will improve meaningfully, which will lead to a resurgence of inflation and wages in the coming 24 months. Investment Implications On a 12 to 24 months horizon, we remain positive on the Swedish krona and Swedish equities. Fixed Income And FX Chart 8Three Hikes By 2025

Three Hikes By 2025

Three Hikes By 2025

The backend of the Swedish OIS curve only discounts 75bps of hikes by 2025. This pricing is too modest (Chart 8). The Swedish economy will rebound further as the vaccination campaign advances, and rising house prices and household indebtedness will fan growing long-term risk to financial stability, both of which suggest that the Riksbank will have to change its tack in 2022. The great likelihood that the Fed will start tapering off its asset purchase toward the end this year, that the ECB will follow sometime in 2022, and that the Norges Bank will be increasing interest rates next year will give more leeway to the Swedish central bank. A wider Sweden/Germany 10-year government bond spread is not an appealing vehicle to play a more hawkish Riksbank down the road. This spread hit a 23-year high in March and now rests at 62bps or its 98th percentile since 2000. Moreover, the terminal rate proxy embedded in the German money market curve is currently so low that the spread between Sweden’s and the Eurozone’s terminal rate proxy stands near a record high. Hence, German yields already embed much more pessimism than Swedish ones. Nonetheless, BCA recommends a below benchmark duration exposure within the Swedish fixed-income space, as we do for other government bond markets around the world.1 A bullish bias toward the SEK is a bet on the Riksbank that offers a very appealing risk/reward ratio, according to BCA Research’s Foreign Exchange Strategy strategists.2 The krona is very cheap against both the euro and the US dollar, trading at 9% and 29% discounts to purchasing power parity, respectively. Moreover, the Swedish current account stands at 5.2% of GDP, compared to 2.3% and -3.1% for the Euro Area and the US, creating a natural underpinning under the SEK. Chart 9The SEK Loves Growth

The SEK Loves Growth

The SEK Loves Growth

Over the coming 12 to 24 months, cyclical forces favor selling EUR/SEK and USD/SEK on any strength. The SEK is one of the most cyclical G-10 currencies and has one of the strongest sensitivities to the US dollar. Hence, our positive global economic outlook and our FX strategists negative view on the greenback are synonymous with a weak USD/SEK. These same factors also mean that the krona will appreciate more than the euro, as the negative correlation between EUR/SEK and our Boom/Bust Indicator and global earnings growth illustrate (Chart 9). Equities We also like Swedish equities, but the state of the Swedish economy and the evolution of the Riksbank policy surprise have a limited impact on Swedish equities. The Swedish bourse is mostly about the evolution of the global business cycle. The Swedish benchmark heightened sensitivity to the global business cycle reflects its massive overweight in deep cyclicals, with industrials, financials, consumer discretionary, and materials accounting for 38.4%, 26.1%, 9.7% and 3.7% of the MSCI index respectively, or 78% altogether (Table 1). As a result, BCA’s preference for global cyclicals at the expense of defensives and this publication’s fondness for the recovery laggards like the industrial and financial sectors automatically translate into a favorable bias toward Sweden’s stocks.3 Table 1Mamma Mia! That’s A Lot Of Cyclicals

Take A Chance On Sweden

Take A Chance On Sweden

Valuations offer a more complex picture, but they do not diminish our predilection for Sweden. Swedish equities trade at a discount to US stocks but at a premium to Euro Area ones (Chart 10). However, Swedish stocks offer higher RoEs and profit margins than both the US and the Euro Area, while also sporting lower leverage (Chart 11). Thus, their valuation premium to Euro Area stocks is warranted and their discount to US ones is excessive, especially when rising yields hurt the relative performance of the growth stocks that dominate US indexes. Chart 10Swedish Discounts And Premia

Swedish Discounts And Premia

Swedish Discounts And Premia

Chart 11Profitable Sweden

Profitable Sweden

Profitable Sweden

The outlook for Swedish earnings is appealing, both in absolute and relative terms. The Swedish market’s extreme sensitivity to global economic activity means that Sweden’s EPS increase and beat US profits when the Riksbank Resource Utilization Indicator expands (Chart 12). These relationships are artefacts of the Swedish economy’s pro-cyclicality, which causes capacity utilization to interweave tightly with the global business cycle (Chart 6). Chart 12The Winner Takes It All

The Winner Takes It All

The Winner Takes It All

Chart 13Better Capex Play Than You

Better Capex Play Than You

Better Capex Play Than You

Global capex and infrastructure spending favor Swedish equities compared to Euro Area ones. Over the past thirty years, Sweden’s stocks have outperformed those of the Eurozone when capital goods orders in the advanced economies have expanded (Chart 13). This reflects the Swedish benchmark’s large overweight in industrials, a sector that is the prime beneficiary of global capex. Capital goods orders are recovering well, and their growth rate can climb higher, especially as western multinationals announce capex plans and as governments from the US to Italy intend to ramp up infrastructure spending. Moreover, the large pent-up demand for durable goods in the Eurozone further enhances the potential of industrial firms, and thus, of Swedish equities.4 Chart 14Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality