Policy

This week’s report discusses the questions we were asked most frequently when we met with investors in the Midwest two weeks ago. We reiterate our pessimistic fundamental take and our neutral asset allocation recommendations.

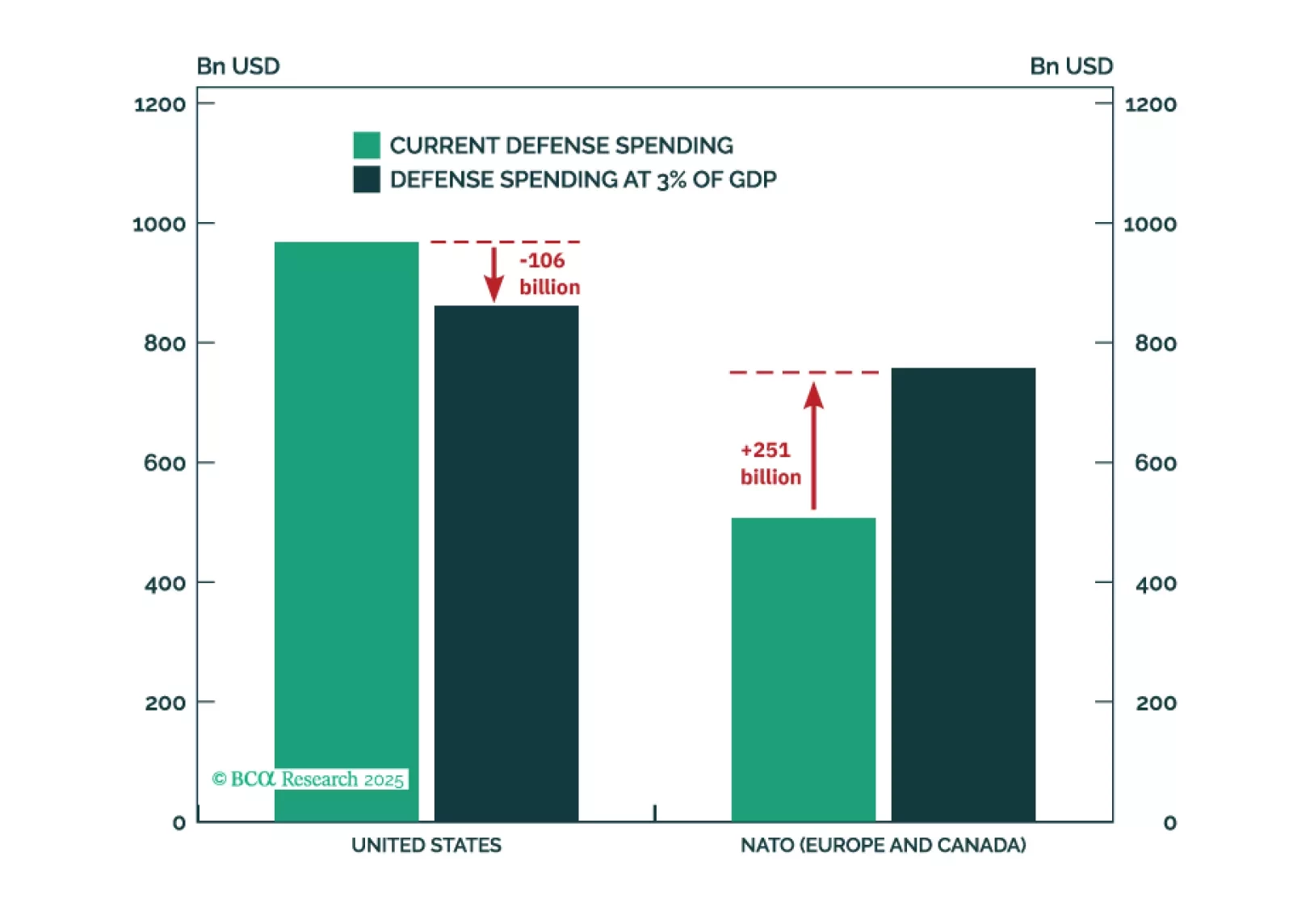

The Trump administration posits that the world owes the US for the provision of its security. In this report, we perform a quantitative analysis to come up with a naïve estimate of the cost of that peace. More importantly (and more seriously), our qualitative assessment argues that save for a number of frontline countries that rely on the US defense umbrella, the vast majority of the world faces manageable security threats due to the complex multipolar global environment and a growing number of alternatives to the US security blanket.

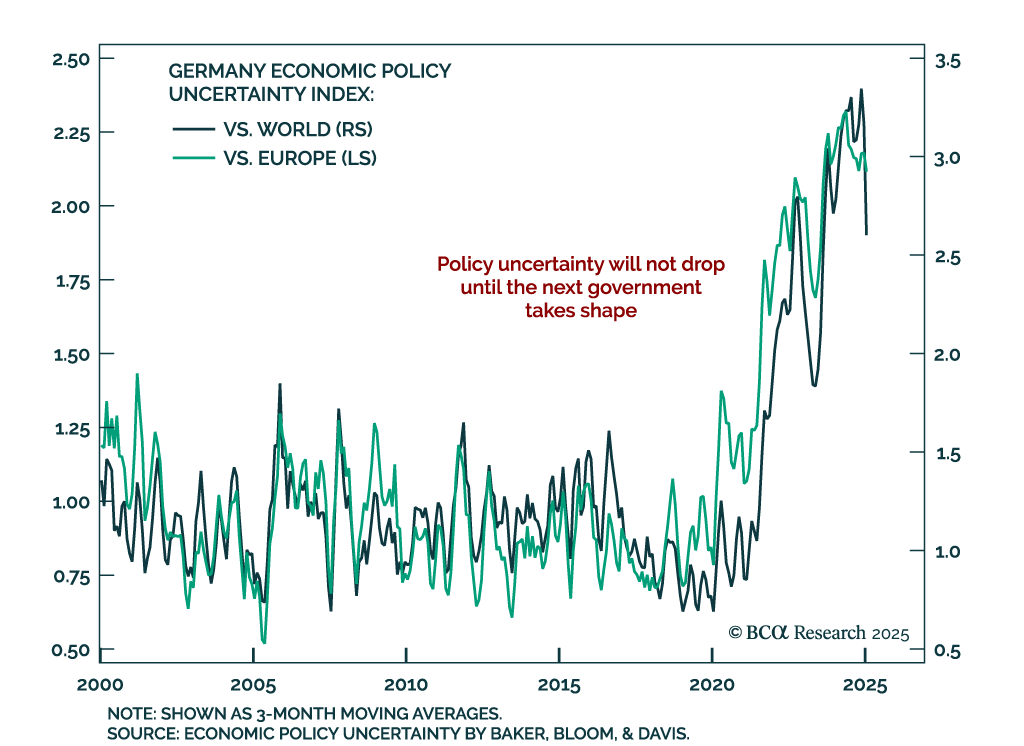

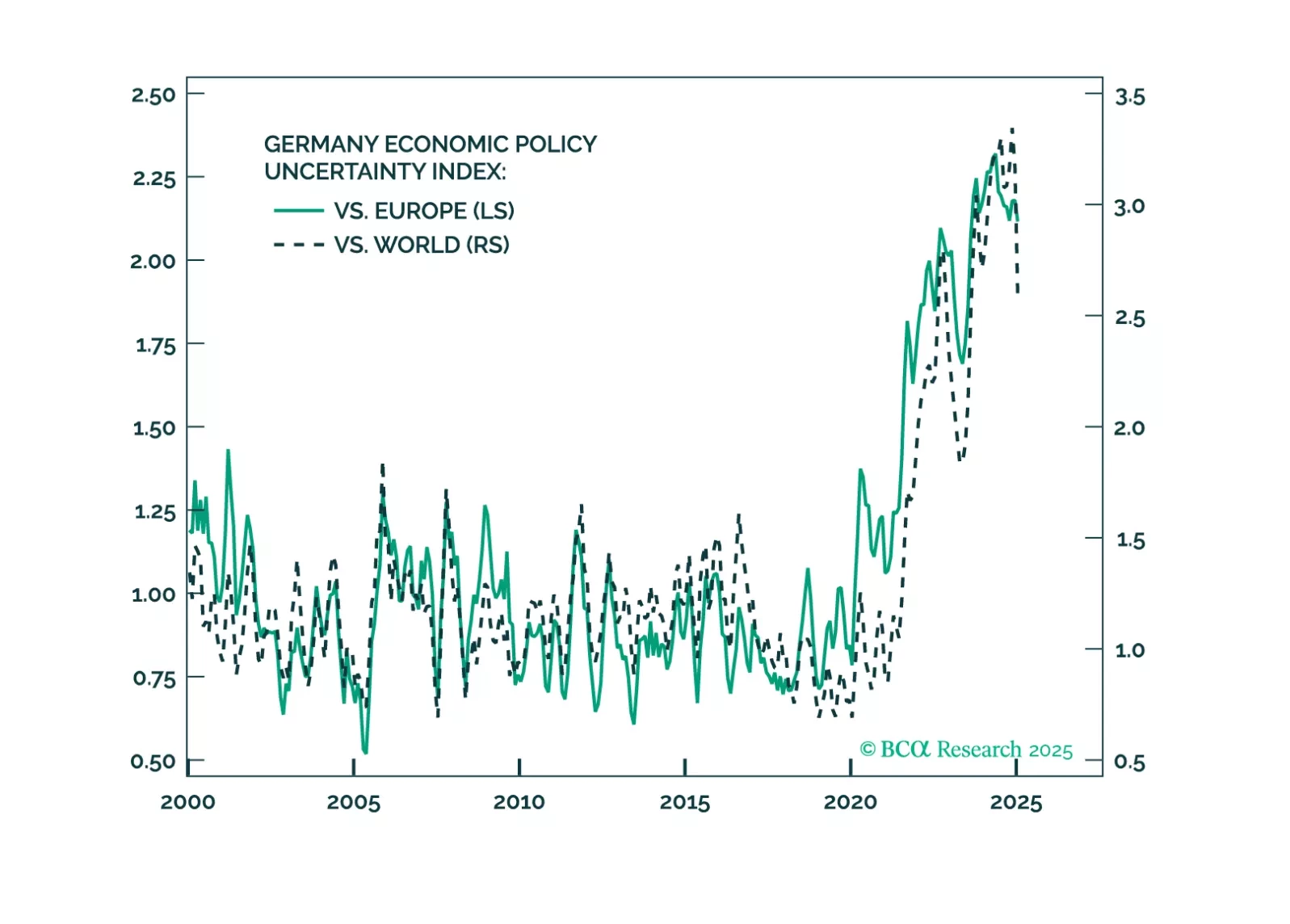

The rise of the far-right is challenging mainstream German politics. The CDU/CSU and SPD will govern Germany again after the election. A ceasefire in Ukraine will offer some relief, but Trump’s policies will keep tensions high.