Policy

Highlights We are lowering our expectation for oil-demand growth this year, bringing it more in line with levels expected by OPEC, the IEA and EIA. Our GDP-driven demand estimates have proven too bullish for 1Q21, considering the wide margin by which we missed actual demand in January and February. Our expectation for oil demand growth this year is lowered to 5.5mm b/d, down from 6.6mm b/d last month. For 2022, we are increasing our growth assumption to 4.1mm b/d, up from 2.8mm b/d. We continue to expect Brent prices to reflect an accommodation between Russia's and KSA's preferred Brent ranges of $50-$55/bbl and $70-$75/bbl, respectively. We are keeping our forecast for average prices at $65/bbl and $70/bbl for this year and next, with WTI averaging $2-$3/bbl below that (Chart of the Week). Brent benchmark pricing confusion subsided, following the decision of S&P Global Platts to revert to free-on-board (FOB) reporting of prices. However, as the center of gravity for crude oil demand settles on Asia, confusion around the North Sea benchmark could provide an opening for regional benchmarks and consolidation of futures platforms trading crudes delivered to the region. Feature The decision by the Kingdom of Saudi Arabia (KSA) to voluntarily remove 1mm b/d of its production from the market over February – April will be remembered as one of the more prescient reads on the state of global oil demand during the COVID-19 pandemic. KSA's insistence on seeing improvement in actual demand – as opposed to forecasted demand – before it commits to returning production to the market could not have been more clear-sighted. The upcoming April 1 meeting of OPEC 2.0 will convey useful information to the market re changes, if any, to the production-management strategy of the coalition, which is led by KSA and Russia. Perhaps the most important information coming out of the meeting will be how KSA reads the current state of global oil demand, as it has not committed to a date-certain when it will return this production to market. We expect the Kingdom to extend its production cuts and to lobby for continued restraint by the other member states of OPEC 2.0 at the meeting. Going into the meeting, OPEC 2.0 will be assessing global demand against a deteriorating public-health backdrop in important consuming markets. The EU's policy failures in securing sufficient vaccinations to protect its population, and public-health missteps regarding the AstraZeneca vaccine continue to retard Europe's efforts to contain the pandemic.1 Chart of the WeekOPEC 2.0 Expected To Maintain Production Discipline

OPEC 2.0 Expected To Maintain Production Discipline

OPEC 2.0 Expected To Maintain Production Discipline

Increasing lockdowns in several EU countries and a higher likelihood of a resurgence in COVID-19 infection rates in the US – particularly in the states that are reopening before they have achieved herd immunity or have vaccinated a large share their populations – will slow demand recovery. The annual Spring Break holidays in the US potentially could become a world-class super-spreader event. Elsewhere, LatAm is distressed, particularly Brazil, which, like the EU, has misjudged and mishandled its vaccination policy and rollout, leaving its populations at higher risk for infection. This also has the attendant risk of producing an environment ripe for further COVID-19 mutations and the spread of new variants. Lower Oil Demand Forecast For 2021 We were wrong on our call expecting stronger demand growth in 1Q21 – our consumption forecasts exceeded realized demand an average of 2.3mm b/d in 1Q21. We are now more aligned with demand expectations of IEA, EIA, and OPEC (Chart 2). Our expectation for oil demand growth this year is lowered to 5.5mm b/d, down from 6.6mm b/d last month. For 2022, we are increasing our growth assumption to 4.1mm b/d, up from 2.8mm b/d. We expect non-OECD oil consumption, our proxy for EM demand, to average 53.2mm b/d this year and 55.5mm b/d next year, vs. 54mm b/d and 55.4mm b/d last month. DM demand, proxied by OECD oil consumption, is expected to average 44.5mm b/d and 46.3mm b/d next year, versus our previous forecast of 44.9mm and 46.3mm b/d last month. Chart 2Lower Oil Demand In 2021, Higher Next Year

Lower Oil Demand In 2021, Higher Next Year

Lower Oil Demand In 2021, Higher Next Year

We continue to expect the massive fiscal and monetary stimulus to support markets and lead to stronger growth going forward. The recently approved package by the US Congress calling for an additional $1.9 trillion of fiscal stimulus will have global knock-on effects, which will be bullish for commodity demand, once the COVID-19 pandemic is contained (Chart 3). Chart 3Pandemic Recovery Will Spur Pent-Up Demand

OPEC 2.0 Production Discipline Still Required To Balance Markets

OPEC 2.0 Production Discipline Still Required To Balance Markets

OPEC 2.0 Production Discipline Persists The salient feature of the oil market during the pandemic has been the cohesion of OPEC 2.0 and its production discipline. We expect that to continue going into and coming out of the coalition's April 1 meeting. Our view that OPEC 2.0 's overall strategy as the dominant producer in the market is to calibrate the level of supply to the level of demand remains intact. We expect production for the coalition to average 46.0mm b/d in 2021 and 46.2mm b/d in 2022 (Chart 4). We do not expect OPEC 2.0 to raise production, given the increasing uncertainty around demand vis-à-vis getting the COVID-19 pandemic under control in large consuming markets like the EU and LatAm, and higher infection rates out of the US. However, as we noted above, we are closely watching what KSA does and says at the upcoming meeting for any clue that global demand is improving faster than we now expect. Chart 4OPEC 2.0 Production Discipline Persists

OPEC 2.0 Production Discipline Persists

OPEC 2.0 Production Discipline Persists

Outside OPEC 2.0, our expectation for the bellwether US shale-oil producers' output remains relatively unchanged. We continue to expect production to move higher, and to remain constrained by capital availability. US shale output is expected to average 10.7mm b/d this year, and 12.1mm b/d next year. In our modeling, the shale producers lead the price-taking cohort, which produces whatever the market allows it to produce. We continue to expect capital-market discipline to keep US oil producers from getting too far out ahead of their balance sheets' ability to profitably grow production. The same holds for producers outside the OPEC 2.0 coalition ex-US (Table 1). Table 1BCA Global Oil Supply - Demand Balances (MMb/d, Base Case Balances)

OPEC 2.0 Production Discipline Still Required To Balance Markets

OPEC 2.0 Production Discipline Still Required To Balance Markets

Markets Balance On OPEC 2.0 Discipline OPEC 2.0's production strategy will keep markets balanced, as relatively high compliance among those producers capable of increasing production is observed and markets are not over-supplied (Chart 5). This will allow inventories to continue to draw then stabilize around mid-year. It is important to point out that this balancing is an iterative process, driven by OPEC 2.0's read on the state of demand, which, perforce, is occurring with lags in the data it is responding to. We continue to keep a weather eye on the USD, given the impact it has on commodity fundamentals. We continue to expect dollar weakening and model for that, but the path of the USD has been difficult to call, given it is highly correlated with global economic policy uncertainty, which is heavily influenced by the evolution of the COVID-19 pandemic (Chart 6). Chart 5Markets Remain Balanced...

Markets Remain Balanced...

Markets Remain Balanced...

Chart 6The USD's Evolution Remains Important

The USD's Evolution Remains Important

The USD's Evolution Remains Important

A Hue and Cry In Brent Additional uncertainty is entering oil markets from an unlikely corner: The Brent benchmark pricing index used to set prices on some two-thirds of all the oil traded in the world. Brent benchmark pricing was thrown into wide-eyed confusion when S&P Global Platts – the leading price reporting agency for the index used as a reference in Brent physical contracts (Dated Brent) – decided to convert the index from a free-on-board (FOB) index to a cost-insurance-freight (CIF) index. Platts' proposed Brent reporting changes two weeks ago essentially would have transformed the pricing index from a pure spot index that assumes the buyer will arrange insurance and freight after purchasing a cargo at a North Sea terminal into a delivered index reflecting CIF-Rotterdam terms provided by the seller. After a great hue and cry went up, Platts reverted to quoting Brent on an FOB basis. But that hardly ends the drama. Brent production is collapsing – by next year, only one 600k-barrel cargo a day of Brent will be loaded out of North Sea terminals. This is a very thin reed supporting the global oil market's primary price index. In an effort to expand the Brent pricing pool, Platts also is looking to include US WTI in one form or another, but nothing's been settled upon to date. The confusion around Brent pricing comes as the center of gravity for crude oil demand and trading continues its inexorable shift to Asia. This could provide an opening for regional benchmarks – e.g., the UAE's Murban crude oil, which supports a just-launched futures contract calling for delivery in Asia, where most of the demand for oil is met by Middle East suppliers. It could even allow for consolidation of other futures platforms in the region (e.g., the Dubai Mercantile Exchange), which also are used to price and hedge Asia-bound crude cargoes out of the Gulf. As interesting and complex as the global oil market is, it is nothing without a viable pricing benchmark. Much of the world's oil business hinges on that index being determined by the price of a single cargo loaded every day. We will be following this with great interest. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Commodities Round-Up Energy: Bullish An exceptionally cold winter resulted in a sharp drawdown US natgas inventories down, which are expected to end the 2020-21 winter season at 2021 at 1.6 Tcf by the US EIA's reckoning (Chart 7). This would be 13% lower than the 5-year average level of inventories, according to the EIA. Over the April-October injection season, EIA is expecting natgas inventories to finish at ~ 3.7 Tcf, or ~ 2% below their 5-year average. Spot natgas prices at Henry Hub, LA – the delivery point for NYMEX/CME futures – averaged $5.35/MMBtu in February, the highest level since February 2014, the EIA noted. Natural gas for April 2021 delivery at Henry Hub closed at $2.562/MMBtu on Tuesday. Base Metals: Bullish COMEX copper came close to its 2011 highs late last month, at $4.30/lb but has since retreated. However, we believe fundamental supply-demand factors will keep copper prices moving higher over the longer term. As highlighted in an earlier report (BCA Research - Renewables, China's FYP Underpin Metals Demand), the move to EVs and renewable energy will keep demand for copper and the overall base metals complex well-bid during this decade. The International Renewable Energy Agency (World Energy Transitions Outlook: 1.5°C Pathway (Preview) (irena.org)) reported on Tuesday that copper-intensive renewable power capacity will have to increase by more than 10-fold by 2050 to avert severe climate change. On the supply side, in our recent report entitled BCA Research - Copper's Supply Challenges, we noted falling copper investment and declining copper ore quality inexorably will increase production costs. Only higher copper prices will incentivize producers to increase mining activity. Rising demand and stagnant supply will put copper supply-demand balances in a deficit over the short-to-medium term, causing inventories to decline over this period as well. Precious Metals: Bullish The sharp run-up in 10-year US real rates since the end of 2020 pulled gold prices from down from their 2021 high of ~ $1,950/oz in January to ~ $1,680/oz earlier this month (Chart 8). Price have since rebounded above $1,740/oz as real rates weakened. We expect markets to re-price gold when it becomes apparent the rally in rates was more a function of higher growth expectations for the US economy than a higher likelihood of Fed tightening. Our view that the Fed's ultra-accommodative monetary policy and massively expansive US fiscal policy will spur growth and inflation has not changed. We expect the Fed to remain behind the inflation curve in its rate hikes, which will keep US real rates on their downward trajectory. Chart 7

OPEC 2.0 Production Discipline Still Required To Balance Markets

OPEC 2.0 Production Discipline Still Required To Balance Markets

Chart 8

Gold Prices Down From Their 2021 High

Gold Prices Down From Their 2021 High

Footnotes 1 Please see Extent of damage to AstraZeneca vaccine’s perceived safety in Europe revealed published by yougov.co.uk 7 March 2021. See also States lift Covid restrictions, drop mask mandates and reopen businesses despite warnings from Biden officials published by cnbc.com 11 March 2021, and European travel restrictions: Non-essential travel curbed published by dw.com 15 March 2021. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

Highlights The American Rescue Plan Act confirms the shift to “Big Government” and proactive fiscal policy in US politics. This sea change in policy is durable for now, given that Democrats can pass one or two more budget reconciliation bills without a Republican vote. Details of forthcoming tax hikes are starting to leak from Washington. Investors should not assume that progressive proposals like a wealth tax, a financial transactions tax, or a minimum corporate tax are dead on arrival. Taxing corporations and the rich is popular. The Republican Party is likely to choose a Trumpian agenda going forward and Trump has a good chance of being the presidential candidate in 2024. But cyclical and structural factors disfavor Republicans at this early stage. Industrials have rallied sharply in advance of Biden’s first law and are now overbought. But we would favor them over health care over a 12-month period, given the macro backdrop and relative policy risks. Feature Were there any surprises in the American Rescue Plan Act (ARPA) signed by President Biden on March 11? Only that some of Biden’s health care and infrastructure agenda slipped into the bill, alongside a provision holding that if states cut taxes and lose revenue, they will lose an equivalent amount in state and local aid. The plan illustrates that the budget reconciliation process is an effective tool for the ruling party to get most of what it wants. The Biden administration will be able to pass one or two more reconciliation bills for FY2022 and FY2023. While the next bills will be harder to pass than the first, and moderate Democratic senators will limit Congress’s options somewhat, the point is that Democrats have just enough political capital to achieve their policy agenda without a single Republican vote. As always, our Political Capital Index is updated in the Appendix and highlights falling political polarization and improving business sentiment, which is positive for Biden’s political capital. Investors will continue to bet on a cyclical recovery but will also become more concerned about tax hikes on one hand and excessive deficit spending on the other. The latter threatens eventually to overheat the economy and speed up the Fed’s rate hike cycle. In this report we conduct a quick recap of the ARPA now that it is official law, we review the tax hike proposals swirling out of the Washington rumor mill, and we update the status of the civil war in the Republican Party. We conclude with a look at industrial stocks, which have rallied tremendously on the back of the cyclical economic upturn (Chart 1) but may still offer some value relative to sectors like health care that face policy risks. Chart 1Cyclical Indicators High On Stimulus

Cyclical Indicators High On Stimulus

Cyclical Indicators High On Stimulus

ARPA Symbolizes The ‘Big Government’ Shift The well-known provisions of the ARPA include: Treasury checks of $1,400 sent directly to individuals who earn less than $80,000 per year; extended unemployment benefits and a renewed federal top-up of $300 per week through September 6, 2021; $65 billion in business aid; and generous funding for various welfare programs such as the expanded Child Tax Credit and larger subsidies for enrollees in the Affordable Care Act health insurance marketplaces (Chart 2).1 Chart 2American Rescue Plan Act

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

In total the US fiscal stimulus amounts to $5 trillion or 23% of GDP since COVID-19 emerged, with $2.8 trillion or 13% of GDP passed since December. It is a gargantuan fiscal stimulus that will supercharge the economy today but lead to a rocky descent once it is exhausted in the coming years (Chart 3). Expiring provisions will occasion political showdowns over whether to make them permanent and how to address waste, corruption, and the long-term budget deficit. Chart 3The COVID-19 Fiscal Blowout

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

The provisions are so far flung that educated American citizens living abroad are reportedly receiving stimulus checks. Nevertheless the bulk of the impact will be felt by low-income people with high marginal propensities to consume. They are the prime beneficiaries of the $850 billion share of the law that funnels cash to individuals as opposed to businesses (Chart 4). This means that at least one-third of the money will be spent, while around two-thirds will be used to pay down debt, enabling consumers to spend more later, according to our Global Investment Strategy. The general effects are very supportive of the recovery. For example, the number of children living in poverty is estimated to fall by 40%, while about one in five renters are expected to catch up on their rent.2 Evictions, bankruptcies, and loan delinquencies will not revive in this context. The total amount of spending is almost twice the size of the output gap, which is now widely expected to be filled by the end of 2022. Chart 4Cash Handouts To Families With High Propensity To Consume

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

While ARPA mainly consists of short-term cash relief – with pro-productivity investments to come in the reconciliation bill for FY2022 focused on infrastructure and renewables – nevertheless it is not wholly devoid of long-term investment. Each of the 50 states will receive $500 million in aid (more depending on their unemployment rate). Since state and local government revenues are not as dire as expected, some of this money will go into infrastructure, including soft infrastructure like the rural broadband buildout. States will be discouraged from cutting taxes, as mentioned.3 The most important takeaway is that the ARPA will reinforce the shift in public attitudes in favor of a larger government role in the economy. Democrats passed their “liberal wish list” and the result is that a range of constituencies – from those on food and housing programs to those working in the health and education systems – will receive a windfall of federal support. In this way a one-off and probably excessive relief bill will contribute to a sea change in American attitudes toward government. Conservatives and Republicans will still argue in favor of limited government but that is a relative concept and the goalposts just moved. Bottom Line: The ARPA secures the recovery, plugs the output gap, and likely reinforces the shift in public attitudes in favor of a larger role of government in society and the economy. The amount of stimulus is likely excessive, assuming the economy avoids any other bad shocks in the coming years. Hence the law marks a historic shift from reactive to proactive fiscal policy and sets the stage for an inflation overshoot in the long run if not the short run. Yellen Becomes Warren? Not Quite, But Expect Negative Tax Surprises The next budget reconciliation bill is expected to be a 10-year green infrastructure package that will be partially offset by tax hikes. Whether in the same bill, or prioritized above it, we expect Biden to push for his expansion of the Affordable Care Act (only a small part of his health agenda was included in the ARPA). The House will draft its version in April and Biden may sign the final bill into law as early as September or as late as December. We discussed the bill in our March 3 missive. Rumors about the tax proposals are starting to leak out of Washington. At present none of the rumors change the policy consensus, based on Biden’s campaign proposal shown in Table 1. However, they do tentatively support our view that tax hikes will deliver negative surprises to the equity market this year, given that investors have so far been unperturbed by the prospect of higher taxes. Table 1Taxman Cometh

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Secretary of Treasury Janet Yellen raised some eyebrows when she indicated that a wealth tax is being considered by the Biden administration.4 Previously a tax on a person’s (or trust’s) net assets, as opposed to a tax on their income, was the domain of Biden’s progressive-left rivals such as Senators Bernie Sanders and Elizabeth Warren. Warren’s proposal would levy a 2% annual tax on those who possess more than $50 million in net wealth, rising to 3% on billionaires. During the Democratic primary election their proposals were estimated to raise anywhere from $1.4 trillion – if Warren’s proposal met with extreme tax avoidance – to $4.5 trillion, as estimated by Sanders.5 Yellen has also spoken to the finance ministers of France and Germany as part of a diplomatic initiative through the OECD to encourage global participation in a minimum corporate tax rate of around 12%. In exchange for enacting this tax floor, Yellen signaled to the Europeans that she would not insist on providing American Big Tech with a “safe harbor” from Europe’s planned digital tax.6 Whatever ends up happening internationally, the implication is that the Biden administration will push forward with its proposed 15% minimum tax on corporation’s book income. Yellen says that she expects tax hikes to be phased in the latter part of the 10-year budget window for FY2022 so as to make sure that the government’s interest burden is manageable over the long run. She is not concerned about excess deficits or debt in the short run, as they are related to the pandemic relief and economic recovery and interest rates are below the nominal growth rate of the economy. But she has endorsed passing tax hikes for later in the decade, as did both President Biden and Vice President Kamala Harris on the campaign trail. Several of the more ambitious tax proposals face limitations in Congress. Moderate senators like Joe Manchin of West Virginia have raised objections to a large tax hike during trying times. He might be joined by other moderates like John Tester of Montana and the four narrowly elected senators from Arizona and Georgia. However, while these moderates will keep the tax agenda in check, it is important to understand their position. None of these senators are against tax hikes in principle – that would be a Republican stance. They are against tax hikes that increase the burden on the middle class or jeopardize the economic recovery. From that point of view Biden’s proposals are fairly palatable: the highest individual income tax bracket would go back to where it stood in 2016, the corporate rate would go halfway (at most) to its pre-Trump level, and the estate tax would be restored. These proposals focus on big corporations and the wealthy and are likely to be watered down in negotiation, so we would not rule out moderate Democratic support. Investors should not rest easy about the tax agenda until more information is known. Negative surprises are likely. The consensus is that the Democrats will not pass a wealth tax, or a “Wall Street tax” on financial transactions, or other progressive proposals. But these taxes would be popular and politically defensible – some polls even show a majority of Republicans supporting a wealth tax. Therefore these taxes cannot be ruled out in advance.7 Bottom Line: The tax debate is underway and our expectation of negative surprises is looking more, not less, likely. How Will Republicans Respond To The Big Government Onslaught? Republicans have duly retreated to the political wilderness after their election loss and the January 6 Capitol Hill riot. The critical question is whether and how they will regroup to contest future elections – the deeper their divisions, the more certain Democratic policy becomes. At the center of this question is whether the Republican Party will adopt Trumpist policy and whether Trump himself will continue to be the flagbearer and presumptive nominee for the presidential election in 2024. Our answer is that the Republicans will adopt a Trumpist agenda of tough trade and immigration policies combined with fiscal largesse but they will struggle over Trump himself and how to broaden their base. Every election is unique. COVID-19 reinforces the point. There is a clear case to be made that Trump would have won the election if not for the pandemic and recession. We favor this view given how narrowly he lost in the midst of the crisis. But there is also a clear case to be made that he would have lost anyway.8 The problem for the Republicans going forward is that cyclical and structural trends work against them. Cyclically, the economy should be in full stride in 2022-24 and the Federal Reserve is highly likely to play a supportive role. This may or may not prevent the usual midterm opposition gains but it will make it very hard for an opposition presidential candidate to win. True, Democrats will not have a full incumbent advantage if President Biden passes the baton to Vice President Harris. Inflation and other problems will emerge. But given the timing of the pandemic, election, and vaccine, voters will probably be much better off in four years than they were last November, which is the most reliable prediction of whether the incumbent party will stay in power. Structurally, demographic change in America diminishes Trump’s base. A generational shift is transforming the American electorate, as the Silent Generation, which is the most reliably Republican, passes on (Chart 5). Millennials favored the Democratic Party by 6% in the 2020 election (10% in Georgia and 21% in Pennsylvania). Chart 5Generational Shift A Risk To Unreconstructed Republicans

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Ethnic minorities also skew Democratic, generally speaking, and are taking a much larger share of the electorate, especially in critical swing states – as highlighted by Biden’s victories in Arizona and Georgia (Chart 6). Hispanics favored Biden by 33% (24% in Arizona). Chart 6US Demographics Drive Political Change

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Demographic extrapolations by the Center for American Progress show that even if post-Millennial generations grow more conservative over time, the Electoral College will shift inexorably against the Republicans as long as current trends continue (Chart 7). Chart 7Electoral Math Frowns On Republicans Even Without Generational Shift

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Demographics are not destiny: Trump would never have won in 2016 if projections based on age and race were so predictive. Yet Republicans cannot merely wait on cyclical or exogenous events to discredit the Democrats. The electoral math is devastating if they do not broaden their appeal. Their quandary is that generating enthusiasm among their base of white voters with less formal education may exclude the very groups to whom they need to appeal: suburban women, educated whites, and ethnic minorities. The immediate question is what to do about Trump, who has divided the party over the Capitol riot, culminating in seven Republican votes against him in his second impeachment. On the surface the Republican Party is a much older entity than any single member or leader and can therefore play a longer strategy. It could choose the correct electoral strategy of courting independents, women, and Hispanics even if it meant losing an election or two due to divisions with the Trumpists. The problem is that Trump’s personal following is uniquely threatening to the viability of the party. Trump alone could split the Republican Party and nullify its chances in 2022-24 and beyond. Trump has suggested starting his own party, the Patriot Party. Opinion polls show that 46% of Republicans would join it while only 27%would insist on sticking with the Republican Party (Chart 8). Even if a Trumpist party stole only 2-3% of Republican voters it would be enough to ensure a Democratic victory in any election given the very small margins of victory in swing states in recent decades. Trump would easily spoil the Republican bid, just as Ross Perot did in the 1990s, Robert La Follette did for the Democrats in the 1930s, and Theodore Roosevelt did in 1912 (Table 2). As Senator Lindsey Graham said of Trump and the Republican Party, after holding post-election negotiations with the former president: “He can make it bigger. He can make it stronger. He can make it more diverse. And he also could destroy it.”9 Chart 8Trump Could Start Third Party, Give Democrats A Decade-Plus Ascendancy

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table 2Major Third Party Breakaway Candidates Undercut Their Former Party

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

So What Will Republicans Do? We conducted an exercise using game theory to determine the likeliest strategy that Trump and the party will take. We used the famous “Prisoner’s Dilemma” as our template because both sides have a lot to gain if they cooperate and a lot to lose if not.10 But they do not trust each other. And each side will lose the most if it stays true while the other betrays it, worsening the distrust. Diagram 1 shows the outcome. Republicans could win eight years in the Oval Office if they adopted Trump’s agenda yet put forward a young new candidate with Trump’s personal endorsement; or they could win four years if they chose Trump himself (the constitutional limitation). By contrast, if they chose an establishment Republican agenda, they could win eight years (reduced to four in Diagram 1 because less likely) or zero years if Trump opposed. Trump, for his part, would win zero years if he bowed out to support the Republicans regardless of whether they adopted his agenda, but he would have a chance of winning four more years if he ran at the head of a Trumpist Republican Party. The outcome is that the Republicans will adopt Trumpism while Trump himself could easily run for president again, given his sway over the party. Diagram 1Game Theory Says Republicans Will Court Trump

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

The game works out the same way if we assign minimal positive payoffs (e.g. one point for a win, zero points for a loss), various other probability weighted payoffs (50% chance of winning), or negative payoffs for time spent out of power. In each variation a stable equilibrium emerges in which Republicans adopt Trump’s agenda and Trump runs again in 2024. Of course, if one changes the structure of the game or assigns subjective scores a different outcome can be produced. But the clearest and most logical games all produce the same outcome: Trump 2024. This view fits with the consensus in online betting markets. According to the bookies, Trump has between a 20% and 35% chance of running as the Republican nominee in 2024. The same markets give Republicans a 44%-50% chance of winning the White House that year. At this early stage we would take the “over” on Trump and the “under” on a GOP victory given the above points about the cyclical and structural factors weighing against Republicans (Chart 9). Our quantitative US election model, which produced the correct result for all states except Arizona, Georgia and Michigan in 2020, gives the Republicans a 44% chance of winning in 2024 but that number will fall sharply as the economy improves. Chart 9Trump's Odds Of Winning The Republic Nomination In 2024

Trump's Odds Of Winning The Republic Nomination In 2024

Trump's Odds Of Winning The Republic Nomination In 2024

What might change this outcome, according to game theory? Republicans could offer a powerful sweetener to convince Trump to bow out of the race and support the party’s candidate, such as letting one of his children or his son-in-law Jared Kushner run in his place. Alternately Democrats could increase the danger to Trump of their winning again, perhaps by threatening to throw him in jail. Otherwise Trump may not be sufficiently convinced of his party’s loyalty, or frightened of Democratic rule, to bow out of the race. We are never beholden to game theory and there are countless real-world ways in which the 2022-24 election outlook could change. But as things stand today, Republicans are highly likely to adopt Trump’s agenda. Trump may or may not do what is best for the party. He is unpredictable and at critical junctures over the past year he has not done so. He could start his own party just for the fun of it and in doing so break the party of Lincoln. This irrational factor creates an imbalance in the game that the Republican Party will be anxious to prevent, reinforcing its likely decision to adopt his agenda and let him seek the nomination freely. If the Republican Party does split, officially or unofficially, the Democrats will be guaranteed to expand their hold on Congress in 2022 and keep the White House in 2024. Note that Republicans would normally be heavily favored to retake the House of Representatives in 2022, though not the Senate, so such an outcome would be a political earthquake. A Democratic ascendancy could last for more than one election cycle: Republicans held the White House from 1980-92 and Democrats held it from 1932-52. Since we cannot reliably forecast Trump’s individual behavior, we cannot rule out a deep Republican rift. On the other hand, while the demographic trends point to Democratic rule out to 2036 and beyond, no Democratic ascendancy would last that long, given economic cycles, international threats, and the inevitable corruptions of single-party rule. But policy uncertainty would collapse over the 2022-24 cycle, pushing the timing of major policy change to 2026 or later. Investors would face a high probability that a sweeping Democratic agenda would be enacted, even assuming the persistence of checks and balances provided by moderate Democratic senators and the judicial branch. One clear implication is that financial markets may not evade the risk of negative regulatory and tax surprises over the long run even if they manage to do so in the FY2022 and FY2023 reconciliation bills – which we doubt. Bottom Line: Republicans cannot win the White House in 2024 without Trump’s popular base, even though they would prefer to have a fresh face capable of expanding that base. Trump cannot win without the Republican Party but he can unpredictably decide to do something other than win, i.e. endorse a Republican successor or start a third party. As a result a true Republican split cannot be ruled out. Meanwhile Republicans will have to court Trump rather than vice versa. Democratic policy is well ensconced for now, an underrated risk to the equity market. Investment Takeaways We know that Democrats are pushing forward on their legislative agenda and capable of passing one or two more budget reconciliation bills. We know that cyclical and especially structural factors will put Republicans at a disadvantage in the 2024 presidential race and possibly even the 2022 midterm. We also know that the Republican Party has a non-negligible risk of fracturing due to Trump’s personal following and unpredictability. These points suggest investors should not bet against the current policy setup. The macro backdrop favors cyclical sectors such as industrials, energy, materials, and financials. In our US Political Risk Matrix we have highlighted that the policy backdrop is especially beneficial to industrials (Appendix, Table A1). This is reinforced by ARPA and Biden’s forthcoming reconciliation bills on infrastructure and green projects, subsidies for domestic production, and simultaneous attempts to reduce trade tensions with US allies and partners – if not with China. Of course, industrials have rallied enthusiastically alongside a sharp rebound in core durable goods orders, a more gradual improvement in non-residential capital expenditures, and an environment in which capex intentions will respond to a general domestic and global upswing (Chart 10). A weak dollar, premised on a global recovery, excess liquidity, lower interest rates for longer, and large budget and trade deficits, also favors the industrial sector and reinforces the recovery in global trade and growth. Rising commodity prices are driven by supply constraints as much as global demand, as our Commodity & Energy Strategy has showed in depth, and help to restore pricing power to industrial firms (Chart 11). Chart 10Industrials Outperform On Recovery And Stimulus

Industrials Outperform On Recovery And Stimulus

Industrials Outperform On Recovery And Stimulus

Chart 11Commodity Boom Supports Industrials' Pricing Power

Commodity Boom Supports Industrials' Pricing Power

Commodity Boom Supports Industrials' Pricing Power

Hence the good news is largely priced into industrials, which are tactically overvalued according to our BCA valuation indicator. The sector looks more or less expensive on all valuation metrics other than price-to-sales (Chart 12). Therefore the best value must be sought on a relative basis, where industrials are outperforming communications services and just beginning to outperform the superstars, tech and health care. From a policy point of view, health care is one of the biggest losers of the Biden administration, which aims to expand health insurance coverage and reduce drug prices. This may be for the benefit of society but it comes at the expense of old cash cows. Investors should stay guarded against a near-term correction in industrials due to looming tax hikes but strategically favor them over health care and tech (Chart 13), which are even more vulnerable to higher taxes. We will execute this trade by going long against health care over a strategic time frame. Chart 12Industrials Overvalued On Most Measures

Industrials Overvalued On Most Measures

Industrials Overvalued On Most Measures

Chart 13Favor Industrials Over Health Care

Favor Industrials Over Health Care

Favor Industrials Over Health Care

Industrials also have a favorable profile against consumer discretionary stocks but we maintain a positive outlook on the US consumer in an era of government largesse. Our Geopolitical Strategy has also highlighted that Great Power struggle will prevent the Biden administration from cutting defense spending – another boon for industrials. Instead it will have to increase spending for defense as well as supply chain resilience and research and development in the midst of a cold war with China. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1Political Risk Matrix

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A2Political Capital Index

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3APolitical Capital: White House And Congress

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3BPolitical Capital: Household And Business Sentiment

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A3CPolitical Capital: The Economy And Markets

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Table A4Biden’s Cabinet Position Appointments

Republicans, Industrials, And Tax Rumors

Republicans, Industrials, And Tax Rumors

Footnotes 1 Garrett Watson and Erica York, “The American Rescue Plan Act Greatly Expands Benefits Through The Tax Code In 2021,” Tax Foundation, March 12, 2021, taxfoundation.org. 2 Committee for a Responsible Federal Budget, “American Rescue Plan Act Will Help Millions And Bolster The Economy,” March 15, 2021, cbpp.org. 3 See footnote 2 above. 4 Paul Kiernan and Catherine Lucey, “Yellen Says Biden Administration Undecided On Wealth Tax,” Wall Street Journal, wsj.com. 5 Kyle Pomerleau, “How Much Revenue Would A Wealth Tax Raise?” On The Margin, American Enterprise Institute, April 20, 2020, aei.org. 6 Jeff Stein, “Yellen pushes global minimum tax as White House eyes new spending plan,” Washington Post, March 15, 2021, washingtonpost.com. 7 Howard Schneider and Chris Kahn, “Majority of Americans favor wealth tax on very rich: Reuters/Ipsos poll,” Reuters, January 10, 2020, reuters.com; Matthew Sheffield, “New poll finds overwhelming support for an annual wealth tax,” The Hill, February 6, 2019, thehill.com. 8 A recession could have happened as a result of the cyclical slowdown from the trade war, which hurt the Midwestern swing states. The yield curve had inverted and the economy’s margin of safety was low. There would not have been any fiscal stimulus without the pandemic. 9 James Walker, “Lindsey Graham Warns Donald Trump Could ‘Destroy’ GOP After Combative CPAC Speech,” Newsweek, March 8, 2021, newsweek.com. 10 The Prisoner’s Dilemma involves two prisoners detained separately and pressured into confessing their crimes. If they both stay quiet, nothing can be proved and they only spend one year in jail. If they both confess, they are proven guilty and both spend five years in jail. If only one of them confesses while the other stays silent, the confessor goes scot free while the other spends 20 years in jail! The incentive is to confess. The equilibrium is for both to confess. The traditional game reveals the benefits of trust as well as the difficulty of maintaining it in isolation and doubt.

US Treasurys sold off on Wednesday morning, with the 10-year Treasury yield making a new intraday pandemic high and the 2/10 yield curve steepening ahead of the conclusion of the Fed meeting. The subsequent Fed message soothed the market and US equities…

Highlights The report from last week’s National People’s Congress (NPC) indicates a gradual pullback in policy support this year. Fiscal thrust will be neutral in 2021, whereas the rate of credit expansion will be slightly lower compared with last year. China’s economy should run on its own momentum in the first half, before slowing to a benign and managed rate. Nonetheless, the risk of policy overtightening is nontrivial and could threaten the cyclical outlook on China’s economy and corporate profits. The recent price correction in Chinese stocks has not yet run its course. Moreover, equity prices in both onshore and offshore markets are breaching their technical resistance. We are downgrading our tactical (0 to 3 months) and cyclical (6 to 12 months) positions on Chinese stocks to underweight relative to global benchmarks. Feature China’s budget and key economic initiatives unveiled at last week’s NPC indicate that policy tightening will be gradual this year. Overall, maintaining stability, both socially and economically, remains the focal point of Premier Li Keqiang’s work plan presented at the NPC’s annual plenary session in Beijing. However, investors have centered on the government’s plan to have a smaller policy push on growth in its budget compared with last year, fearing that economic and corporate profit rebound will disappoint. The Shanghai Composite Index dropped by 6% during the week when the NPC took place. In our view, the risks of a policy over-tightening in the next six months are high. As such, with this report we are downgrading our cyclical call on Chinese stocks to underweight within a global equity portfolio. Reading Policy Tea Leaves China's growth trajectory since the middle of 2020 has given the government comfort in staying the course on policy normalization. The question is how much Chinese policymakers are willing to pull back support for the economy this year. Overall, the central government plans a smaller policy push in this year's budget and intends to let the economy run on its own steam. Further policy reflation is not in the cards unless a relapse in the economy threatens job creation. The NPC outlined a growth target “above 6%” for 2021 and did not set a numerical goal for the 14th Five-Year Plan from 2021 to 2025. However, de-emphasizing growth does not mean China has abandoned its GDP targets (Table 1). Indeed, in most years in the past two decades, China’s expansion in GDP has overshot objectives set at the NPC (Chart 1). Our baseline estimate is that real GDP will increase by 8% in 2021. Table 12021 Economic And Policy Targets

National People’s Congress Sets Tone For 2021 Growth

National People’s Congress Sets Tone For 2021 Growth

Chart 1Actual Econ Growth Rates Have Overshot Targets In Most Years

Actual Econ Growth Rates Have Overshot Targets In Most Years

Actual Econ Growth Rates Have Overshot Targets In Most Years

We also maintain our view that the rate of credit expansion will be reduced by 2 to 3 percentage points this year to about 11% annually, which is in line with nominal GDP growth (Chart 2). On the fiscal front, the target for a budget deficit was cut by less than half percentage point compared with last year. When taking into account both the government’s budgetary and fund expenditures, the broad-measure fiscal deficit will probably be around 8% of GDP (about the same as last year), which implies there will not be any fresh fiscal thrust in 2021 (Chart 3) Chart 2Credit Growth Will Decelerate From Last Year

Credit Growth Will Decelerate From Last Year

Credit Growth Will Decelerate From Last Year

Chart 3Neutral Fiscal Thrust

Neutral Fiscal Thrust

Neutral Fiscal Thrust

The pullback in fiscal impulse is larger than in 2010, 2014, and 2017, following the previous three fiscal expansionary cycles. However, the government's eased budget deficit target this year does not mean government expenditure growth will slow. Government revenues climbed sharply by the end of 2020 and will continue to improve this year (Chart 4). Higher revenues will allow more government spending while keeping the fiscal deficit within its objectives. Chart 4Gov Revenue Is On The mend But Spending Has Yet To Pick Up

Gov Revenue Is On The mend But Spending Has Yet To Pick Up

Gov Revenue Is On The mend But Spending Has Yet To Pick Up

Chart 5A Small Reduction In ##br##LG Bond Quota

National People’s Congress Sets Tone For 2021 Growth

National People’s Congress Sets Tone For 2021 Growth

Furthermore, the quota for local government special purpose bonds was reduced by only 2% from last year. It should help to support a steady growth in China’s infrastructure investment (Chart 5). The data from January and February total social financing shows a noticeable improvement in corporate demand for bank loans, as well as the composition of bank loans. Corporate demand for medium- and long-term loans remains on a strong uptrend, which reflects an ongoing recovery in corporate profits and supports an optimistic view on capital investment in the months ahead (Chart 6). Chart 6More Demand For Longer-Term Loans Reflects Better Investment Propensity

More Demand For Longer-Term Loans Reflects Better Investment Propensity

More Demand For Longer-Term Loans Reflects Better Investment Propensity

Bottom Line: The growth and budget targets set at this year’s NPC suggest only a modest pullback in policy support. Downside Risks To The Economy Chart 7Econ Growth Usually Peaks Six To Nine Months After Credit Expansion Rate Slows

Econ Growth Usually Peaks Six To Nine Months After Credit Expansion Rate Slows

Econ Growth Usually Peaks Six To Nine Months After Credit Expansion Rate Slows

Despite a relatively dovish tone from the NPC, investors should not be complacent about the risk of a policy-tightening overshoot, which could lead to disappointing economic and profit growth this year. In most of the previous policy tightening cycles, China’s economic activities remained resilient in the first 6 to 9 months (Chart 7). One exception was 2014, when nominal GDP growth dropped sharply as soon as credit growth slowed. The reason is that Chinese authorities kept a very disciplined fiscal stance and aggressively tightened monetary policy, while allowing the RMB to soft peg to a rising USD. In other words, macroeconomic policies were too restrictive during the 2013/14 cycle. Although messages from the NPC do not suggest that Chinese authorities are on such an aggressive tightening path this year, investors should watch the following signs that could threaten China's cyclical economic health: Policymakers may keep monetary conditions too tight, by allowing the RMB to rise too fast while lifting bank lending and policy rates. Currently rates are maintained at historically low levels, much lower than in previous policy tightening cycles (Chart 8). However, the trade-weighted RMB has appreciated by 6% since its trough in July last year and has returned to its pre US-China trade war level (Chart 9). The Chairman of China’s Banking and Insurance Regulatory Commission recently signaled that bank lending rates would climb. Although we do not expect the rate to return to its 2014 or 2017 level, China is much more indebted than in previous cycles. Even a small bump in interest rates will place a burden on corporates and local governments’ debt servicing cost, dampening their propensity to invest (Chart 10). Chart 8Aggressive Rate Hikes Are ##br##Unlikely This Year

Aggressive Rate Hikes Are Unlikely This Year

Aggressive Rate Hikes Are Unlikely This Year

Chart 9Rising RMB Should Refrain Chinese Policymakers From Further Tightening Monetary Stance

Rising RMB Should Refrain Chinese Policymakers From Further Tightening Monetary Stance

Rising RMB Should Refrain Chinese Policymakers From Further Tightening Monetary Stance

Chart 10Chinese Private Sector Has Become Much More Sensitive To Rising Interest Rates

Chinese Private Sector Has Become Much More Sensitive To Rising Interest Rates

Chinese Private Sector Has Become Much More Sensitive To Rising Interest Rates

Chart 11Bank Lending To Property Sector Has Become Increasingly Restrictive

Bank Lending To Property Sector Has Become Increasingly Restrictive

Bank Lending To Property Sector Has Become Increasingly Restrictive

Policies could become too restrictive in key old-economy industries. Chinese authorities have reiterated their determination to contain price bubbles in the property sector. For the first time since 2017, bank lending to real estate developers grew at a pace far below overall bank loans and continued to trend downward in February this year (Chart 11). Moreover, household mortgage loans have reached their slowest expansion rate since 2013. At 22% of China’s total bank lending, a sharp setback in the property sector’s loan growth will be a significant drag on total credit and the economy. A worsened imbalance in supply and demand could lead to too much buildup in industrial inventory. Manufacturing inventories recovered sharply following last year’s massive stimulus and many sectors have surpassed their pre-pandemic levels (Chart 12). Strong external demand helped to boost China’s production and propensity to restock on raw materials. However, both China’s core CPI and producer prices for consumer goods remain in the doldrums, which indicates that domestic final demand has yet to fully recover (Chart 13). As discussed in last week’s report, reopening the world economy in 2H21 should benefit the service sector more than tradeable goods. China’s inventory buildup, particularly in the upstream industries, could turn excessive when export growth slows and domestic demand fails to pick up the slack. Chart 12How Far Can Chinas Inventory Restocking Cycle Go?

How Far Can Chinas Inventory Restocking Cycle Go?

How Far Can Chinas Inventory Restocking Cycle Go?

Chart 13Final Demand Remains ##br##Weak

Final Demand Remains Weak

Final Demand Remains Weak

The service sector could take longer than expected to recuperate, even though China’s domestic COVID-19 situation is under control. China’s services sector has flourished in recent years and accounted for 54% of the nation’s pre-pandemic economic output. However, about half of the service sector output is tied to real estate and financial services. Increasing pressures from tighter policy regulations targeting both the property and online financial service sectors could dampen their support to the economy more than policymakers anticipated. At the same time, wage and household income growth could remain tame by China’s standards (Chart 14). The NPC’s targeted 7% annual increase in spending for national research and development – far below the 12% annual average reached during the past five years – will not be enough to offset the slowdowns in real estate and financial services (Chart 15). Chart 14Household Income Growth Has Yet To Recover

Household Income Growth Has Yet To Recover

Household Income Growth Has Yet To Recover

Chart 15Chinas Pace Of R&D Investment Has Slowed Along With Econ Growth

Chinas Pace Of R&D Investment Has Slowed Along With Econ Growth

Chinas Pace Of R&D Investment Has Slowed Along With Econ Growth

Bottom Line: The downside risks to China’s cyclical growth trajectory are nontrivial. A tug-of-war between policy tightening and growth support will likely persist throughout this year. Investment Implications We recommend investors to underweight Chinese stocks within a global equity portfolio, in the next 0 to 9 months (Chart 16A and 16B). Chart 16AChinese Stocks Are At Their Technical Resistance

Chinese Stocks Are At Their Technical Resistance

Chinese Stocks Are At Their Technical Resistance

Chart 16BChinese Stocks Are At Their Technical Resistance

Chinese Stocks Are At Their Technical Resistance

Chinese Stocks Are At Their Technical Resistance

On January 13, we tactically downgraded Chinese stocks from overweight to neutral, anticipating that China’s equity markets are sensitive to rising expectations of policy tightening, due to higher corporate debt-servicing costs and lofty valuations. Chinese stock prices peaked in mid-February, but in our view the correction has not yet run its course. In terms of the economy, we maintain our baseline view that China's overall policy environment this year will be more accommodative than in 2017/18. The growth momentum carried over from last year's stimulus should prevent China's economy and corporate profits from slumping by too much this year. However, as policy supports are scaled back, investors will increasingly focus on the intensity of China’s domestic policy tightening and the uncertainties surrounding it. Downside risks are nontrivial and will continue to weigh on investors' sentiment. For investors that are mainly exposed to the Chinese domestic equity market, the near-term setbacks in the A-share market are taking some air out of Chinese equities' frothy valuations, and may pave the way for a more optimistic cyclical outlook beyond the next 9 to 12 months. We recommend domestic investors to stay on the sidelines for now, but will start recommending sector rotations in the next few months when opportunities arise. Jing Sima China Strategist jings@bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

BCA Research’s US Bond Strategy service concludes that the Fed will revise up its interest rate forecasts at Wednesday’s meeting; nonetheless, the new forecasts will remain more dovish than the current market pricing. The market’s fed funds rate…

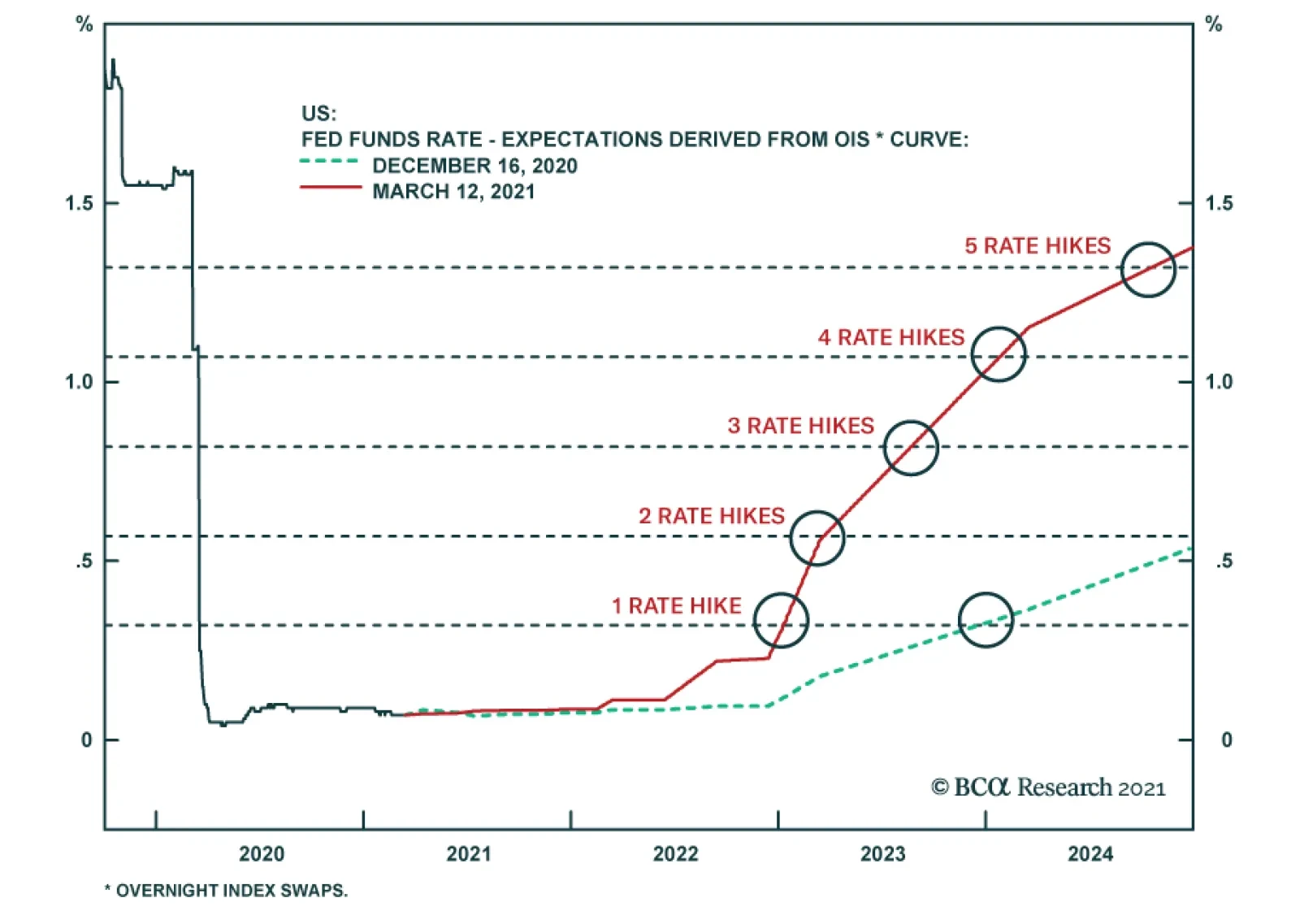

Highlights Duration: The Fed will revise up its interest rate forecasts at this week’s meeting, but the new forecasts will remain dovish compared to current market pricing. This could pressure bond yields down in the near-term. However, any downside in yields could prove temporary given that economic growth continues to beat expectations. Corporates: The macro environment of strong economic growth and accommodative monetary policy will persist for some time yet. In this environment, bond portfolio managers should minimize exposure to interest rate risk and maximize exposure to credit risk. In particular, a strategy of favoring high-yield corporate bonds over investment grade corporate bonds makes a lot of sense. Inflation & TIPS: Core inflation will be relatively strong during the remainder of 2021, with 12-month core PCE likely ending the year close to the Fed’s 2% target. Investors should remain overweight TIPS versus nominal Treasuries and continue to hold inflation curve flatteners and real yield curve steepeners. Expect Some Pushback From The Fed The continuing bond market selloff will be the top item on the agenda at this week’s FOMC meeting. Meeting participants will debate whether the sharp rise in long-maturity bond yields represents a threat to the economic recovery and Chair Powell will no doubt be peppered with questions on the topic at his post-meeting press conference, as he was when he sat down with a Wall Street Journal reporter two weeks ago.1 But for our part, we’ll be focused more on the front-end of the yield curve this week. Specifically, we’ll be looking to see whether the Fed revises up its funds rate forecasts by enough to justify current market pricing or whether it uses its forecasts to push back against the bond bears. The market’s fed funds rate expectations have moved a lot since the Fed last published its own forecasts in December (Chart 1on page 1). In December, the market was priced for fed funds liftoff in December 2023 and then only one more 25 basis point rate hike through the end of 2024. Now, the market is looking for liftoff in January 2023, followed by two more rate hikes before the end of that year. Chart 1Market Priced For 3 Rate Hikes Before The End Of 2023

Market Priced For 3 Rate Hikes Before The End Of 2023

Market Priced For 3 Rate Hikes Before The End Of 2023

As for the Fed, at last December’s meeting only 5 out of 17 FOMC participants anticipated raising rates before the end of 2023. It’s logical to expect the Fed to increase its rate expectations this week as the economic outlook is much brighter than it was at the time of the December FOMC meeting. Back in December, we still didn’t know whether the Democrats would win control of the Senate, enabling passage of President Biden’s $1.9 trillion stimulus bill. Doubts also remained about how quickly COVID vaccination would occur. Chart 2The Data Can't Disappoint

The Data Can't Disappoint

The Data Can't Disappoint

The Fed will probably respond to these pro-growth developments by revising up its interest rate expectations, but we doubt that these revisions will bridge all of the gap with the market. Employment and inflation both remain far from where the Fed would like them to be, and the Fed will want to send the message that its policy stance remains highly accommodative. We could see the Fed’s median fed funds rate forecast shifting to call for one rate hike by the end of 2023, but not the three currently priced into the yield curve. In this scenario, the Fed’s pushback could prompt some near-term downside in bond yields. The question is how long the Fed’s messaging will impact the market in the current environment of surging economic growth. The Economic Surprise Index shows that the economic data can’t even manage to disappoint expectations, a development that usually coincides with rising yields (Chart 2). Bottom Line: The Fed will revise up its interest rate forecasts at this week’s meeting, but the new forecasts will remain dovish compared to current market pricing. This could pressure bond yields down in the near-term. However, any downside in yields could prove temporary given that economic growth continues to surpass expectations. We maintain below-benchmark portfolio duration and we will continue to use our Checklist (see last week’s report)2 to determine an appropriate time to increase duration. The Spread Buffer In Corporate Credit Treasury yields troughed last August, and since then returns have been hard to come by in the US bond market. This is not too surprising. Fixed income is hardly the ideal asset class for a reflationary economic environment. However, there are steps a bond portfolio manager can take to maximize profits in an economic environment that is characterized by (i) rapid economic growth, (ii) rising inflation expectations and (iii) monetary policy that remains accommodative. Specifically, bond investors should minimize their exposure to interest rate risk (i.e. duration) and maximize exposure to credit risk. That is, shy away from long duration assets with little-to-no credit spread and favor shorter duration assets where the credit spread makes up a large proportion of the yield. This sort of strategy has worked well since the August trough in Treasury yields. The Investment Grade Corporate Bond Index – an index with relatively long duration and a small credit spread – is down 4.08% since August 4th (Chart 3). Notably the worst returns have come from the highest rated credit tiers where the credit spread makes up a smaller proportion of the yield. Notice that Aaa-rated Corporates have lost 9% while Baa-rated bonds are only down 2.52% (Table 1). In contrast, total returns from the High-Yield Index – an index with lower duration where the credit spread makes up a much larger proportion of the yield – have held up nicely. The overall index has returned 6.65% since August 4th with the lowest credit tiers once again performing best. Chart 3Move Down In ##br##Quality

Move Down In Quality

Move Down In Quality

Table 1Corporate Bond Returns Since The Aug. 4 2020 Trough In Treasury Yields

Limit Rate Risk, Load Up On Credit

Limit Rate Risk, Load Up On Credit

Performance for both the Investment Grade and High-Yield indexes improves if we look at excess returns relative to a duration-matched position in Treasury securities. That is, if we hedge out the interest rate risk and focus purely on spread movements. Though even here, we find that the lowest rated credits with the widest spreads deliver the best returns. If we assume that this reflationary economic environment persists for the next 12 months, can we expect the same low rate risk/high credit risk strategy to succeed? One way to investigate this question is to look at the 12-month breakeven yields and spreads for different segments of the corporate bond market (Table 2). The 12-month breakeven yield is the yield increase that the index can tolerate over the next 12 months before it delivers negative total returns. Similarly, the 12-month breakeven spread is the spread widening that an index can tolerate over the next 12 months before it delivers negative excess returns (where excess returns are measured versus a duration-matched position in Treasury securities). Table 2Corporate Bond 12-Month Breakeven Yields And Spreads

Limit Rate Risk, Load Up On Credit

Limit Rate Risk, Load Up On Credit

The overall Investment Grade Corporate Index, for example, has an average maturity of 12 years and a 12-month breakeven yield of 27 bps. This means that, if we assume that the investment grade corporate bond spread holds steady, then the odds of the index delivering negative total returns over the next 12 months are the same as the odds of a 12-year Treasury yield rising by more than 27 bps. An assumption of flat investment grade corporate bond spreads seems reasonable given that spreads are already historically tight (Chart 4). Moving down in quality within investment grade helps a bit, the Baa credit tier has a 12-month breakeven yield of 30 bps compared to a 12-month breakeven yield of 21 bps for the Aa credit tier. A similar benefit is observed if we look at the 12-month breakeven spread: 14 bps for Baa and only 6 bps for Aa. However, the real improvement comes when we move out of investment grade entirely and into high-yield. To calculate fair breakeven yields and spreads for high-yield bonds we need to incorporate default loss expectations. The current macro environment of strong growth and accommodative monetary policy should lead to relatively low default losses. That being the case, we assume a base case of a 2.5% default rate and 40% recovery rate for the next 12 months. Using this assumption, we calculate a 12-month breakeven yield of 75 bps for the High-Yield Index and a 12-month breakeven spread of 46 bps. This represents a significant extra buffer compared to what is offered by even the lowest investment grade credit tier. Not only that, but the 75 bps 12-month breakeven yield from the High-Yield Index looks even better when we consider that high-yield spreads are not as overvalued relative to history as investment grade spreads, and have more room to tighten as the economic recovery progresses (Chart 5). Chart 4Investment Grade Valuation

Investment Grade Valuation

Investment Grade Valuation

Chart 5High-Yield Valuation

High-Yield Valuation

High-Yield Valuation

Table 2 also presents two other default loss scenarios, and it shows that we need fairly pessimistic default loss expectations to make high-yield breakeven yields and spreads comparable to what is offered by investment grade bonds. Even if we assume a 4.5% default rate and 30% recovery rate for the next 12 months, we still get a 32 bps breakeven yield from the High-Yield Index, comparable to what we get from the Baa credit tier. Bottom Line: The macro environment of strong economic growth and accommodative monetary policy will persist for some time yet. In this environment, bond portfolio managers should minimize exposure to interest rate risk and maximize exposure to credit risk. In particular, a strategy of favoring high-yield corporate bonds over investment grade corporate bonds makes a lot of sense. Inflation & The Inverted TIPS Curve Chart 6Inflation Will Peak In April

Inflation Will Peak In April

Inflation Will Peak In April

February’s Consumer Price Index was released last week, and it showed that core CPI managed only a 0.1% increase on the month. This caught some off guard given that “rising inflation” has become a popular market narrative during the past few months. Our view is that core inflation will rise significantly between now and the end of the year, and that 12-month core PCE inflation will end the year close to the Fed’s 2% target. We arrive at this view for three reasons. First, base effects will lead to a large jump in 12-month inflation measures in March and April. Chart 6 illustrates the paths for both 12-month core PCE and core CPI assuming modest 0.15% monthly gains between now and the end of the year. Because the severely negative inflation prints from last March and April are about to fall out of the rolling 12-month sample, 12-month core inflation is on the cusp of rising to levels considerably above the Fed’s target. This means that after 12-month inflation peaks in April, the question will be how much it declines during the remainder of the year. One reason why we think it might not fall that dramatically is that bottlenecks are already emerging in both the goods and services sectors, and prices will come under upward pressure as the economy re-opens and consumers are encouraged to deploy some of the excess savings they’ve built up during the pandemic. Producer prices are currently surging, as are survey responses about price pressures from the NFIB Small Business Survey and the ISM Manufacturing and Non-Manufacturing Surveys (Chart 7). Finally, shelter is the largest component of core inflation (accounting for almost 40% of core CPI). It would be difficult for overall core inflation to rise significantly without at least some participation from shelter. With that in mind, we now see evidence that shelter inflation will soon put in a trough (Chart 8). Chart 7Price Pressures Are Building

Price Pressures Are Building

Price Pressures Are Building

Chart 8Shelter Inflation About To Bottom

Shelter Inflation About To Bottom

Shelter Inflation About To Bottom

The permanent unemployment rate and Apartment Market Tightness Index are both tightly correlated with shelter inflation. The permanent unemployment rate has stopped climbing and will move lower during the next few months as increased vaccination rates allow for more of the economy to re-open (Chart 8, panel 2). The Apartment Market Tightness Index is also well off its lows, and it will soon jump above the 50 line, joining the Sales Volume Index (Chart 8, panel 3). Consumers are also increasingly seeing signs of rental inflation. A question from the New York Fed’s Survey of Consumer Expectations showed a very sharp increase in expected rents in February (Chart 8, bottom panel). Chart 9Stay Long TIPS

Stay Long TIPS

Stay Long TIPS

As for TIPS strategy, we are hesitant to back away from our overweight TIPS/underweight nominal Treasuries position with inflation on the cusp of a such a significant move higher, especially with the 5-year/5-year forward TIPS breakeven inflation rate still below where the Fed would like it to be (Chart 9). We are also not yet willing to exit the inflation curve flattening and real yield curve steepening positions that we have been recommending since last April, even though the 5/10 TIPS breakeven inflation slope has become inverted (Chart 9, bottom panel).3 With the Fed targeting an overshoot of its 2% inflation target, an inverted inflation curve is more natural than a positively sloped one. This is because the Fed will be trying to hit its inflation target from above, rather than from below. Further, the short-end of the inflation curve is more sensitive to the actual inflation data than the long-end. This means that the curve could flatten even more as inflation rises in the coming months. Bottom Line: Core inflation will be relatively strong during the remainder of 2021, with 12-month core PCE likely ending the year close to the Fed’s 2% target. Investors should remain overweight TIPS versus nominal Treasuries and continue to hold inflation curve flatteners and real yield curve steepeners. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 For more details on the implications of what Powell said in this interview please see US Bond Strategy Weekly Report, “No Panic From Powell”, dated March 9, 2021, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Weekly Report, “No Panic From Powell”, dated March 9, 2021, available at usbs.bcaresearch.com 3 Please see US Bond Strategy Weekly Report, “Negative Oil, The Zero Lower Bound And The Fisher Equation”, dated April 28, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Global Duration: Markets are correctly interpreting the $1.9 trillion US fiscal stimulus package as a factor justifying higher global growth expectations and bond yields. Maintain a below-benchmark stance on overall global duration. Yield Betas & Country Allocation: Within government bond portfolios, overweighting the “lower-beta” countries that have bond yields less sensitive to changes in US yields (Germany, France, Japan) versus the higher-beta markets (Canada, Australia, UK) remains the appropriate strategy during the current bond bear market. Underweights should remain concentrated in the US, though, as it is highly unlikely that any central bank will begin to tighten policy before the Fed. UK Follow-Up: The conclusions from our UK Special Report published last week do not change after adjusting for the difference in the inflation indices used to calculate UK inflation-linked bond yields compared to those of other countries. UK real interest rates are the lowest in the developed economies, while inflation breakevens are the highest. NOTE: There will be no Global Fixed Income Strategy report published next week. Instead, BCA Chief Global Fixed Income Strategist Rob Robis will do a webcast discussing his latest thoughts on global bond markets. Yields Rising Around The World Chart of the WeekPolicy Mix Is Bond-Bearish

Policy Mix Is Bond-Bearish

Policy Mix Is Bond-Bearish

The path of least resistance for global bond yields remains biased upward. Optimism on future economic growth remains ebullient with consumer and business confidence indices surging in much of the developed world. The epicenter of the global bond bear market remains the US, where pandemic related economic restrictions are being unwound with 21.4% of the US population now having received at least one dose of a vaccine. Fiscal policy in the US is also supporting the positive vibes on future growth after the $1.9 trillion stimulus package was signed into law by President Biden last week. The 10-year US Treasury yield climbed back to the 2021 high of 1.63% on the back of that announcement. The US stimulus package changes the trajectory of the 2021 US fiscal impulse from a $0.8 trillion contraction to a $0.3 trillion expansion, according to estimates from the US Committee for a Responsible Federal Budget (Chart of the Week). This, combined with ongoing quantitative easing from global central banks eager to keep bond yields as low as possible until inflation expectations sustainably return to policymaker targets, is providing a bond-bearish lift to both inflation expectations and real yields – most notably in the US. Central bankers can try to fight back against the speed of the increase in bond yields by maintaining their commitment to current policy settings, as the European Central Bank (ECB) and Bank of Canada (BoC) did last week. The Fed, Bank of England (BoE) and Bank of Japan (BoJ) will all get the chance to do the same this at this week’s policy meetings. The likely message from all will be one of staying the course and not reflexively responding to higher bond yields, which have not triggered a broad-based selloff in global risk assets that would pre-emptively tighten financial conditions. The S&P 500 index hit an all-time high last week, while equity markets in Europe and Japan have returned to pre-pandemic levels (Chart 2). Global corporate credit spreads have remained calm, consistent with a positive growth backdrop that diminishes the potential for credit downgrades and defaults. The US dollar has gotten a lift from improving US growth expectations and relatively higher US Treasury yields, which has had some negative spillover effect into emerging market equities and currencies. The dollar rebound has been relatively modest to date, however, with the DXY index up only 3% from the early 2021 lows. A major reason why global equity and credit markets have absorbed higher bond yields so well is because the sheer scope of the new US fiscal stimulus will have a major impact on growth momentum both in the US and outside the US. This comes on top of the boost to optimism from the speed of the US and UK vaccine rollouts. In an update to its December 2020 economic outlook published last week, the OECD estimated that the $1.9 trillion US stimulus will boost US real GDP growth by 3.8 percentage points versus its original forecast over the next year (Chart 3). Other countries will also benefit from the implied surge in US demand spilling over from that stimulus package, with the OECD projecting a 1.1 percentage point increase to world real GDP growth. Chart 2Risk Assets Ignoring Rising Global Bond Yields

Risk Assets Ignoring Rising Global Bond Yields

Risk Assets Ignoring Rising Global Bond Yields

Chart 3Big Growth Spillovers From US Fiscal Stimulus

Harder, Better, Faster, Stronger

Harder, Better, Faster, Stronger

Countries that have the greater exposure to US demand, like Canada and Mexico, are expected to benefit a bit more than the rest of the world, but the expected boost to growth is consistent (around one half of a percentage point) from China to Europe to Japan to major emerging market countries like Brazil. That US-fueled pickup in global economic activity will help absorb some of the spare capacity that opened up during the COVID-19 pandemic. In Chart 4 and Chart 5, we show the estimates taken from the December 2020 OECD Economic Outlook for the output gaps in the US, euro area, UK, Japan, Canada and Australia for 2021 and 2022. We adjust those projections by the OECD’s estimate of the impact of the US fiscal stimulus in 2021, as well as by the additional upward revisions to the OECD growth projections in 2021 and 2022 that were published last week. Chart 4The $1.9 Trillion Stimulus Will Close The US Output Gap …

Harder, Better, Faster, Stronger

Harder, Better, Faster, Stronger

Chart 5… And Help Narrow Output Gaps Elsewhere

Harder, Better, Faster, Stronger

Harder, Better, Faster, Stronger

Chart 6Maintain Below-Benchmark Duration

Maintain Below-Benchmark Duration

Maintain Below-Benchmark Duration