Policy

Highlights The Senate will pass the $1.9 trillion American Rescue Plan largely as it stands. Markets will now turn to Biden’s second major reconciliation bill for FY2022 – the one with tax hikes. Democrats will go forward with tax hikes on corporations and the wealthy. But they will spend more than they tax for fear of squandering their term in power. Tax hikes threaten sectors like tech that already face headwinds from rising bond yields. The health sector is also at risk. Stick with cyclicals and value plays. Feature Markets have seesawed as volatility spikes in the face of rapidly rising bond yields. Value stocks such as financials stand to benefit relative to growth stocks as the market comes to grips with the first hint of normal inflation expectations since 2019 (Chart 1). Underlying the trend is a sea change in US fiscal policy. Chart 1Value Stocks To Reignite On Rising Bond Yields

Value Stocks To Reignite On Rising Bond Yields

Value Stocks To Reignite On Rising Bond Yields

The House of Representatives passed the $1.9 trillion American Rescue Plan so it will now go to the Senate for revision, back to the House for approval, and then to President Biden’s desk by around March 14. Investors will now turn to Biden’s second major legislative act prior to the 2022 midterm election cycle: the fiscal year 2022 budget reconciliation process. Before we outline the time frame and tax hikes that that process will entail, we should take a moment to review the current bill. Senate Will Pass American Rescue Plan Largely As Is The House version of the $1.9 trillion American Rescue Plan contains $1,400 household rebates, direct checks via the Internal Revenue Service, for people who make less than $75,000 per year (double those numbers for married couples). Unemployment benefits are supposed to rise from $300 to $400 per week for 73 weeks instead of 50 weeks, with an expiration on August 29 instead of March 14. Those with children or other dependents will receive additional payments. The bill also includes $75 billion for fighting COVID-19, $350 billion for state and local governments, $170 billion for schools and universities, $225 billion for small business, $38 billion for the airline industry and various other tax benefits for families and workers.1 Those who have been let go from their jobs can more easily retain their previous health insurance. Chart 2 provides a visual comparison of the American Rescue Plan with the $900 billion in fiscal relief passed at the end of 2020 prior to House passage and Senate revision. Already the Senate version excludes a hike to the minimum wage, from $7.25 to $15 per hour, as the Senate parliamentarian ruled that does not qualify under the “Byrd rule” because it does not directly impact spending or taxation.2 Vice President Kamala Harris, who is also president of the Senate, could reverse this decision but otherwise the minimum wage will have to be considered in a separate bill later. Chart 2American Rescue Plan

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The Senate could pare back other aspects of the bill – such as state and local aid, given that local government revenues are in much better shape than expected. Chart 2 highlights that the state and local aid component is much larger this time around. Still, the purpose of Senate negotiations is to secure the votes of moderate Democrats, as winning over 10 Republicans is no longer feasible, and moderate senators are not going to sink the first legislative proposal of a president of their own party. The Senate is virtually guaranteed to pass the bill, likely by March 14 when current unemployment benefits expire. The bill’s economic impact will be to speed the vaccination process and provide another infusion of cash into households and various public institutions. Families are just starting to receive the last round of benefits passed in December and they had not exhausted the 14% year-on-year increase in real income that they saw as a result of last year’s CARES Act when the Coronavirus Response and Relief Act sent incomes soaring yet again (Chart 3). Economic growth will be supercharged as economic activity normalizes, consumer confidence recovers, and the service sector revives. Chart 3Washington Lavishes Households With Dole

Washington Lavishes Households With Dole

Washington Lavishes Households With Dole

Biden’s Second Bill Will Pass This Fall The second budget reconciliation procedure, for fiscal year 2022, will begin in mid-April. The formal deadline to adopt a budget resolution is April 15 but the average delay would put the resolution in June.3 The maximum delay would see the resolution passed in October but that is unlikely in today’s context (Diagram 1). After the resolution passes, the House and Senate must reconcile their budgets, pass the same bill, and send it to the president for his signature. Diagram 1Timeline Of Biden Administration’s Second Budget Reconciliation, FY2022

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The average time between Congress adopting a budget resolution and the president signing a reconciliation bill into law is 150 days, putting completion on September 15, 2021. This period could easily extend to November. In the worst-case, judging by history, Democrats could fail to conclude the process until October 2022 – but that is highly unlikely. A delay till December of this year would be a fumble, but a more realistic fumble, say if moderate Democrats must be won over due to controversial provisions. The second reconciliation bill is supposed to consist of investments over a ten-year period rather than emergency relief for the lingering pandemic and economic recovery. Biden’s proposed $2-$3 trillion green infrastructure program is the highlight but we also expect Democrats to prioritize their health care plan, which is estimated to cost $1.7-$1.9 trillion. Hence $4 trillion is a reasonable expectation for new spending but in this case the headline spending figure will be at least partially defrayed by tax hikes, unlike the first reconciliation bill (Charts 4A & 4B). If Biden raises taxes by half as much as he intends, the full price tag would be $2 trillion. Chart 4ABiden Will Spend, Then Tax

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Chart 4BBiden Will Spend, Then Tax

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The precise contours of this bill will remain unknown until Biden presents an outline in April and the House of Representatives drafts a resolution. We test six different scenarios involving different assumptions about Biden’s tax-and-spend proposals, highlighted in Table 1. Generally, we assume that Democrats will much more readily compromise tax hikes rather than spending, given that they want to err on the side of firing up the economic recovery. They are just as capable as Republicans were in 2017 of manipulating the numbers when it comes to the reconciliation requirement that the budget deficit not increase beyond a ten-year time period. Table 1Scenarios For Biden’s Second Reconciliation Bill

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The results are broken down in terms of revenue, expenditure, and net interest costs in Chart 5. The baseline is Biden’s campaign proposal. Scenario 1 assumes that Biden gets all of the spending he wants but is forced to compromise on tax hikes. Scenario 2 is more realistic as it assumes that Biden gets half of what he wants on both spending and taxes. Scenarios 3-6 examine what would happen if Biden were forced to strike out either his green infrastructure plan or his health and social security plan, depending on different revenue assumptions. In Scenarios 5 and 6 we grant Biden only half of his proposed taxes on corporations and wealthy folks, leaving other tax proposals to the side – otherwise the result would be a net tightening of fiscal conditions, which is neither intended nor politically possible. Chart 5Scenarios For Biden’s Second Reconciliation Bill

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The impact on the budget deficit in each scenario is shown in Chart 6. The greatest economic stimulus would occur under Scenario 1, which would soon become a problem for investors as it would hasten inflation and rising interest rates. Chart 6Deficit Scenarios For Biden’s Second Reconciliation Bill

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Scenario 2 is the most realistic policy scenario while being the least inflationary. By contrast, Scenario 4 is realistic but hardly less inflationary than the baseline case. In each of these scenarios it is important to bear in mind that the new government programs would be administered over a ten-year period and therefore the increase to the budget deficit would be more gradual than is the case of the American Rescue Plan, which clearly aims to be disbursed in the first few years. In the case of the Obama administration’s American Recovery and Reinvestment Act (2009) the peak in spending occurred in 2013, four years after the bill was passed (analogous to 2025 today) (Chart 7). Infrastructure and green energy projects are also expected to increase productivity and hence potential growth. Chart 7Infrastructure Spending Could Peak Four Years After Bill’s Passage, As In 2009-13

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The Byrd rule will become even more important with Biden’s second reconciliation bill because the bill will contain a mishmash of Biden’s campaign proposals. Democrats will try to pass as much of their agenda via fast track as possible so as to meet promises ahead of the 2022 midterm election. An advantage of health care spending is that it is unlikely to be struck down by the Senate parliamentarian given that the Obama administration relied on reconciliation to pass a critical second installment to the Affordable Care Act (Obamacare). Biden’s health care plan is more popular than climate change policy, with both the general public and moderate Democrats, and it is guaranteed to pass reconciliation. Infrastructure spending faces greater challenges under reconciliation but they are not insurmountable. Infrastructure is normally handled via the traditional budget process or the Highway Trust Fund and some measures are likely to run afoul of the Byrd rule. Still, workarounds can be found.4 Hence the infrastructure plan is likely to be compromised but not prohibited due to technicalities. Even if infrastructure fails to make it into reconciliation, Biden can use the deadline to top up the exhausted Highway Trust Fund or to reauthorize the Surface Transportation Act as alternative pathways. It is not impossible to get Republican cooperation on infrastructure though the green agenda will meet resistance. The reconciliation process is nominally forbidden from increasing the budget deficit beyond ten years. Short-term spending is exempt, as is the case with the American Rescue Plan and its crisis-response measures, but the purpose of the second reconciliation bill is to invest in long-term, productivity-enhancing programs. A new government health insurance option and/or a green infrastructure buildout will take many years to implement and could increase deficits beyond the ten-year window. But Democrats, like Republicans, will be able to use accounting chicanery and gimmicks to make the budget outlook serve their purposes in passing the legislation. As long as they keep moderate members of the party on their side. Yes, Taxes Will Go Up … But That May Not Be All Bad For Markets Why should Democrats raise taxes at all? Why not focus on stimulus without taking on the political risk of higher taxes? After all, Republicans passed tax cuts via reconciliation without offsetting them by spending cuts. Was it not the higher taxes in Obamacare that greatly fueled resistance from Republicans and their victory in the House of Representatives in 2010? First, on the level of intentions, the Democrats clearly seek to increase taxes on corporations, high-income earners, and capital gains: Both Biden and Harris said they would raise taxes on the campaign trail and in the presidential debates despite the risk to their election prospects. Biden committed only to prevent tax hikes on those making less than $400,000 per year. Harris’s weakest moment in her debate with Mike Pence was her insistence that she would raise taxes but she stuck to her guns. Both factions of the Democratic Party want to raise taxes. Traditional Democrats view tax hikes as a way of paying for a larger government role in addressing social and economic imbalances. Populists view tax hikes as a way of redistributing from the ultra-rich. While budget deficits are not a general concern, combating inequality is a theme shared across the party. Second, on the level of capability, Democrats can get at least some of the tax increases that they want: The US is not overtaxed on the whole. True, Biden’s full tax agenda would push the US back up to the top of the OECD countries in terms of the corporate tax if an “integrated” view of both firm-level taxes and taxes on dividends and capital gains (Chart 8). But this point suggests that Biden will moderate his tax plan rather than abandon it altogether. Popular opinion did not favor Trump for cutting corporate taxes. Chart 8Biden’s Corporate Tax Proposal Would Make US An Outlier Again

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

The macroeconomic impact of raising taxes is manageable in the context of the extraordinary fiscal stimulus that the US is passing. There is no clear relationship between tax rates and economic growth but it is natural for the Democrats to fear that they could squander their term in power by excessive fiscal tightening. Yet the negative economic impact of raising the corporate rate is only 0.8% of GDP over the long run, and half of that if the corporate rate is raised only halfway to what Biden intends (25% instead of 28%) (Table 2), according to the conservative-leaning Tax Policy Foundation. Table 2Economic Impact Of Corporate Tax Not Dramatic

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

President Biden has the political capital early in his term to revise the Trump tax cuts according to Democratic prerogatives. His popularity will not hold up for long (Chart 9). And he only just has enough legislative power. While household sentiment is weak and economic conditions are moderate, both are set to improve as the pandemic fades and fiscal stimulus takes effect (Table 3). While tax hikes will embolden Republican opposition and the Democrats will have lost their chance to affect the tax code if Republicans win in 2022. At the moment, Republicans are divided and unpopular, so Democrats have a window of opportunity (Chart 10). Chart 9Thesis, Antithesis, Synthesis?

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Chart 10Independents Up, Republicans Down

Independents Up, Republicans Down

Independents Up, Republicans Down

Table 3Political Capital Index

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

While Democrats could chuck all the Senate rules out the window in order to pass their spending plans without any offsets, this would anger moderates who tend to uphold Senate rules and norms. The party cannot afford to lose a single vote from their caucus in the Senate. Yet moderate Democrats are not against tax increases in principle. What they would oppose is either excessive tax hikes or a fiscal spending bonanza without any revenue offsets at all.5 It is entirely feasible to back-load tax increases so that they take effect in the latter half of the ten-year budget window, especially after the 2024 election. Treasury Secretary Janet Yellen is advising precisely this course of action and has herself argued that corporate tax hikes will go through.6 There may be some risk that Democrats go full left-wing populist and abandon any semblance of fiscal responsibility so as to supercharge the economy. So far they have agreed to maintain the Senate filibuster and scrap the minimum wage hike but this acceptance of Senate norms may not last as pressure builds. The second reconciliation bill is the last chance to fast-track major initiatives before the midterm. Vice President Harris could overrule the Senate parliamentarian across the board. This scenario is unlikely. The White House and Congress will find a balance that raises some revenue but errs on the fiscally accommodative side, as our scenarios above highlight. Investment Takeaways The market’s concern is that the Democrats will “overdo” the fiscal response and we fully share this concern. The American Rescue Plan alone will plug the output gap by almost three times more than the amount required. The coming tax hikes will not offset the wave of new spending that is coming down the pike. Democrats will partially reverse Trump’s tax cuts in the context of additional pump-priming that constitutes a net increase to the budget deficit. The net effect is inflationary. If Congress were to pass another $2 trillion bill without any substantial revenue offsets then the market would face an even bigger inflationary jolt and an even earlier return to rate hikes by the Fed. But this scenario is unlikely. So the inflationary risk is clear but investors need not panic in the short run. Our infrastructure trade is back on track as the reflation trade rumbles onward (Chart 11). The Democrats will get at least one more major bill passed and it will likely include at least half of Biden’s agenda, including around $2 trillion on green infrastructure. We will discuss the renewable energy portion at length in a forthcoming report. The health care sector faces headwinds from both Biden’s health policies and corporate tax hikes. The sectors that stand to benefit the most from a higher corporate tax rate are those that benefited least from Trump’s Tax Cut and Jobs Act – namely energy, industrials, materials, and financials, in that order (Chart 12A). These are also the cyclical plays that we favor in today’s accommodative policy environment. Chart 11Infrastructure Trade Back On Track

Infrastructure Trade Back On Track

Infrastructure Trade Back On Track

Chart 12ACyclicals Outperforming Health Care

Cyclicals Outperforming Health Care

Cyclicals Outperforming Health Care

Chart 12BCyclicals To Outperform Tech?

Cyclicals To Outperform Tech?

Cyclicals To Outperform Tech?

The same cyclical sectors are also trying to make headway against the tech sector, which stands to suffer from higher interest rates as well as higher taxes, including a minimum tax on book earnings, if that part of Biden’s agenda makes it through the negotiations this fall (Chart 12B). Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Appendix Table A1APolitical Capital: White House And Congress

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Table A1BPolitical Capital: Household And Business Sentiment

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Table A1CPolitical Capital: The Economy And Markets

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Table A2Political Risk Matrix

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Table A3Biden’s Cabinet Position Appointments

Taxes Will Rise But It Is Still A Fiscal Blowout

Taxes Will Rise But It Is Still A Fiscal Blowout

Footnotes 1 See Jeff Drew, “House passes $1.9 trillion stimulus bill with a variety of small business relief,” and Alistair M. Nevius, “Tax provisions in the American Rescue Plan Act,” February 27, 2021, Journal of Accountancy, journalofaccountancy.com. 2 See “The Budget Reconciliation Process: The Senate’s ‘Byrd Rule,’” Congressional Research Service, December 1, 2020, fas.org. 3 The current delay centers on whether the Senate will confirm Biden’s appointee for director of the Office of Management and Budget, Neera Tanden, who lost support from key moderate Democrat Joe Manchin. If she does not receive a compensatory Republican vote then Biden will have to appoint someone else and the Senate will have to confirm. Thus the budget resolution could easily be delayed into May or June. 4 For the difficulties, see Peter Cohn, “Democrats plan a spending blowout, but hurdles remain,” Roll Call, January 11, 2021, rollcall.com. For workarounds, see Zach Moller and Gabe Horwitz, “Reconciliation: How It Works and How to Use It to Help American Workers Recover,” Third Way, February 1, 2021, thirdway.org. 5 See Alexander Bolton, “Democrats hesitant to raise taxes amid pandemic,” The Hill, February 25, 2021, thehill.com. 6 See Saleha Mohsin and Christopher Condon, “Yellen Favors Higher Company Tax, Signals Capital Gains Worth a Look”, Bloomberg, February 22, 2021, Bloomberg.com

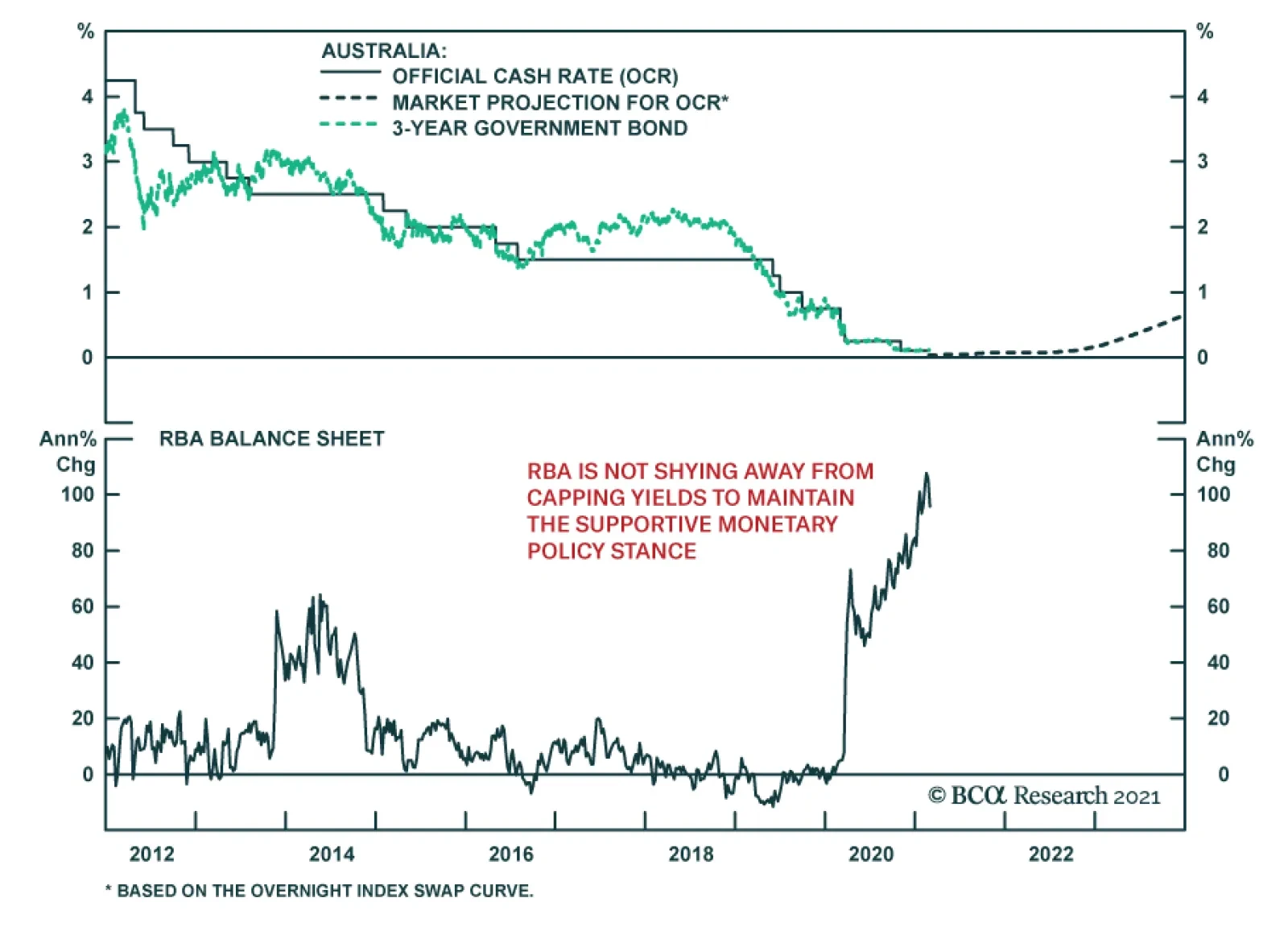

As expected, the Reserve Bank of Australia kept policy unchanged at its Tuesday meeting, maintaining the 10-basis point targets for the cash rate and the yield on the 3-year government bond. The RBA reiterated its commitment to keeping monetary…

Highlights Rising Global Yields: The increased turbulence in global bond markets is part of the adjustment process to a more positive outlook for global economic growth. Rising real yields are now the main driver of nominal yield movements, with stable inflation expectations indicating that investors are not overly concerned about a sustained inflation overshoot. Duration: Central bankers will eventually be forced to shift to less dovish interest rate guidance to reflect the new reality of faster growth and increased inflation pressures, but this is likely to not occur until much later in 2021, starting with the Fed. Maintain a below-benchmark cyclical duration stance in global bond portfolios. UST Yields & Spreads: The selloff in US Treasuries has pushed US yields to levels that are starting to look a bit stretched relative to yields from other major developed economies like Germany and Japan. This is especially true on a volatility-adjusted basis. As a result, we are closing our tactical US-Germany spread widening trade in bond futures at a profit of 1.8%. Feature Chart of the WeekBond Yields Are Rising Because Of Growth

Bond Yields Are Rising Because Of Growth

Bond Yields Are Rising Because Of Growth

The rapid surge in global bond yields seen so far in 2021 has led some commentators to declare that the dreaded “bond vigilantes” have returned to dole out punishment for overly stimulative fiscal and monetary policies (most notably in the US). The rapid pace of the bond selloff, with the 10-year US Treasury yield reaching 1.6% on an intraday basis last week, has raised fears that spiking yields could damage a fragile global economic recovery. This logic is backwards – it is surging growth expectations that are driving bond yields sustainably higher from deeply depressed levels. Global growth is projected to accelerate at a very rapid pace over the rest of this year and 2022. The combination of the Bloomberg consensus real GDP growth and inflation forecasts for the major developed economies suggest that nominal year-over-year GDP growth is expected to climb to 7.2% in the US, 8.4% in the UK and 6.4% in the euro area by year-end (Chart of the Week). Nominal growth in 2022 is expected to grow by another 5-7% across the same regions, suggesting a return to a slightly faster pace than prevailed during the pre-pandemic years of 2017-19 - even after a boom in 2021. Nominal longer-term global government bond yields, which had been priced for a pandemic-stricken economic backdrop, are now playing catch-up to the new reality of a post-pandemic, vaccinated world. Bond investors understand that the need for extreme monetary accommodation is ebbing, especially in the US where there will be an enormous fiscal impulse to growth in 2021 (and beyond). As a result, interest rate expectations are moving higher, fueling a repricing towards higher bond yields around the world. This process has more room to run. A Global Move Higher In Yields, For The Right Reasons Chart 2Reflationary Bear-Steepening Of Global Yield Curves

Reflationary Bear-Steepening Of Global Yield Curves

Reflationary Bear-Steepening Of Global Yield Curves

The cyclical rise in developed market bond yields that began last summer was initially focused on longer-maturity yields boosted by rising inflation expectations (Chart 2). The very front-ends of bond yield curves – which are more sensitive to expectations of changes in central bank policy rates – have remained subdued. The upward pressure on global bond yields is starting to infect some shorter maturities, however. 5-year government bonds yields in the UK, Canada and Australia rose 44bps, 42bps and 35bps, respectively, during the month of February. The latter two represented a near doubling of the level of the 5-year yield. In the case of the UK, the surge in 5-year Gilt yields came from a starting point of negative yields at the end of January. Last week, the 5-year US Treasury yield jumped a massive 22bps on a single day due to a poorly received US Treasury auction. Year-to-date, longer-term global bond yields have been rising more through the real yield component than higher inflation expectations (Charts 3A & 3B). This is a change in the dynamics from the latter half of 2020 when inflation expectations were the dominant force pushing global yields higher. Chart 3AReal Yields Are Driving The Recent Bond Selloff …

Real Yields Are Driving The Recent Bond Selloff...

Real Yields Are Driving The Recent Bond Selloff...

Chart 3B… Even In The Lower-Yielding Markets

...Even In The Lower-Yielding Markets

...Even In The Lower-Yielding Markets

This shift in “leadership” of the global bond market selloff has been broad-based. 10-year real yields from inflation-linked bonds have surged higher in the US (+35bps year-to-date), UK (+40bps), Australia (+44bps) and Canada (+25bps). Real 10-year yields have even inched up in France (+9bps), despite euro area growth suffering because of COVID-19 lockdowns. This coordinated rise in real bond yields comes on the heels of a sharp improvement in overall global economic momentum and improving expectations for future growth. Manufacturing PMIs, a reliable leading indicator of real yields in the developed markets, began a cyclical improvement in the middle of last year and, right on cue, global bond yields bottomed out toward the end of 2020 (Chart 4). The link between that strong growth momentum and real bond yields comes from expected changes in central bank policies. Our Central Bank Monitors for the US, euro area, UK, Japan, Canada and Australia – designed to measure cyclical pressures on monetary policy - have all moved significantly higher since mid-2020 (Chart 5). This suggests a diminished need for additional monetary stimulus because of rebounding economic growth and intensifying inflation pressures. The Monitors have climbed to above pre-pandemic levels in the US and Australia. Chart 4Real Yields Starting To Catch Up To Solid Growth

Real Yields Starting To Catch Up To Solid Growth

Real Yields Starting To Catch Up To Solid Growth

Chart 5Markets Starting To Discount Rate Hikes In 2023

Markets Starting To Discount Rate Hikes In 2023

Markets Starting To Discount Rate Hikes In 2023

Interest rate markets are responding to this cyclical pressure to tighten monetary policies by repricing the expected timing and pace of the next rate hiking cycle. Our 24-month discounters, which derive the amount of interest rate changes priced into overnight index swap (OIS) curves up to two years in the future, are now pricing in higher policy rates in the US (+40bps), the UK (+32bps), Australia (+36bps) and Canada (a whopping +82bps) by the first quarter of 2023. This repricing of interest rate expectations does conflict with current central bank forward guidance, to varying degrees. For example, the Fed continues to signal that there will not be any rate hikes until at least the end of 2023. Policymakers will not be overly concerned about higher government bond yields and shifting interest rate expectations, however, if there is limited spillover into broader financial market performance. In the US, the latest increase in real Treasury yields to date has had minimal impact on US equity market valuations or corporate bond yields (Chart 6A), suggesting no tightening of financial conditions that could impact future US economic growth. A similar situation is playing out in Europe, where higher longer-term real yields have had little impact on equity market valuations or the borrowing rates that the ECB is most concerned about, like Italian BTP yields (Chart 6B). Chart 6ANo Tightening Of Financial Conditions In The US...

No Tightening Of Financial Conditions In The US...

No Tightening Of Financial Conditions In The US...

Chart 6B...Or Europe

...Or Europe

...Or Europe

Currency valuations are a more important indicator of financial conditions for other central banks. For example, the Reserve Bank of Australia (RBA) has been explicit that its current policies – near-zero policy rates, yield curve control to anchor the level of 3-year bond yields and quantitative easing (QE) to moderate the level of longer-term yields – are intended to not only keep borrowing costs low but also dampen the value of the Australian dollar. At the moment, the US dollar is being pulled in different directions by the typical fundamental drivers. Real rate differentials between the US and other major developed economies remain unattractive for the greenback, even with the latest rise in US real yields (Chart 7). At the same time, growth differentials between the US and the other major economies are turning more USD-positive. For now, rate differentials are the more dominant factor for the US dollar and will remain so until the Fed begins to shift to a less dovish policy stance – an outcome that we do not expect until much later this year when the Fed will begin to prepare the market for a tapering of asset purchases in 2022. A sustainable bottoming of the US dollar, fueled by a shift to a less accommodative Fed, will also likely mark the end of the rising trend for global inflation expectations, given the links between the dollar, commodity prices and inflation breakevens (bottom panel). Central banks outside the US will continue to resist any unwelcome appreciation of their own currencies versus the US dollar. That means doing more QE when bond yields rise too quickly, as the RBA did this week and the ECB has threatened to do in recent comments from senior policymakers (Chart 8). Increasing the size of asset purchases is unlikely to sustainably drive non-US bond yields lower, however, in an environment of improving global growth that is causing investors to reassess the future path of interest rates. All more QE can hope to do at this point in the global business cycle is limit how fast bond yields can increase. Chart 7The USD Remains The Critical Reflationary Variable

The USD Remains The Critical Reflationary Variable

The USD Remains The Critical Reflationary Variable

Chart 8More QE Is Less Effective At Capping Bond Yields

More QE Is Less Effective At Capping Bond Yields

More QE Is Less Effective At Capping Bond Yields

Chart 9Markets With A Lower Yield Beta To USTs Are Outperforming

Markets With A Lower Yield Beta To USTs Are Outperforming

Markets With A Lower Yield Beta To USTs Are Outperforming

From an investment strategy perspective, the current growth-fueled move higher in global real bond yields does not change any of our suggested tilts. We continue to recommend a below-benchmark overall duration stance within global bond portfolios. Within our recommended country allocation among developed market government bonds, we continue to prefer a large underweight to US Treasuries and overweights to markets that are less susceptible to changes in US Treasury yields like Germany, France, Japan and the UK (Chart 9). We also continue to recommend only neutral allocations to Canadian and Australian government bonds (with below-benchmark duration exposure within those allocations), although we are on “downgrade alert” for both given their status as higher-beta bond markets with central banks more likely follow the Fed down a less dovish path later this year. Bottom Line: Rising real yields are now the main driver of nominal yield movements, with stable inflation expectations indicating that investors are not overly concerned about a sustained inflation overshoot. Central bankers will eventually be forced to shift to less dovish interest rate guidance to reflect the new reality of faster growth and increased inflation pressures, but this is likely to not occur until much later in 2021, starting with the Fed. Maintain a below-benchmark cyclical duration stance in global bond portfolios, with a large underweight allocation to US Treasuries. The UST-Bund Spread Widening Looks Stretched Chart 10Yield Chasing Has Been A Losing Strategy In 2021

Yield Chasing Has Been A Losing Strategy In 2021

Yield Chasing Has Been A Losing Strategy In 2021

Last August, we published a report discussing how “yield chasing” – a strategy of consistently favoring the highest yielding government bond markets – had become the default strategy for bond investors during the early months of the pandemic.1 We concluded that yield chasing would be a successful strategy for only as long as central banks stuck to their promises to maintain very loose monetary policy for the next few years. Investors would be forced to chase scarce yields in that environment, while worrying less about cyclical economic and inflation factors that could push up bond yields. Yield chasing has performed quite poorly so far in 2021. A basket of higher-yielding markets like the US, Canada and Australia has underperformed a basket of low-yielders like Germany, France and Japan by -1.4 percentage points (Chart 10). Obviously, such a carry-driven strategy would be expected to perform poorly during an environment of rising bond volatility as is currently the case. Markets that have been offering relatively enticing yields, like the US or Australia (Table 1), are actually generating the largest total return losses. Those higher-yielders have suffered more aggressive repricing of interest rate expectations, as discussed in the previous section of this report, leading to losses from duration that are dwarfing the higher yields. This is especially true in the US, where there remains the greater scope for an upward repricing of interest rate and inflation expectations. Table 1Government Bond Yields: Unhedged & Hedged Into USD

Are Central Banks Losing Control Of Bond Yields? No.

Are Central Banks Losing Control Of Bond Yields? No.

This suggests that investors must be cautious on determining when to consider increasing exposure to higher yielders like the US, even after Treasury yields have increased substantially. One way to evaluate that is to look at the spreads between US Treasuries and low yielders like Germany and Japan, relative to US bond volatility. In Chart 11, we show the spread of 10-year US Treasuries to 10-year German Bunds. To facilitate a fair comparison between the two, we hedge the Treasury yield into euros while adjusting the spread for duration difference between the two bonds. The currency-hedged and duration-matched Treasury-Bund spread is shown in the middle panel of the chart. In the bottom panel, we adjust that spread for US interest rate volatility by dividing the spread by the level of the MOVE index of US Treasury option volatility. On an unadjusted basis, the 10-year yield gap now sits at 175bps, +70bps higher than the lows seen in August 2020. That spread is narrower on a currency hedged basis, with the 10-year US Treasury yield hedged into euros +73ps higher than the 10-year German bund yield. Two conclusions stand out from the chart: The currency-hedged and duration-matched spread is still well below the prior peaks dating back to 2000; The volatility-adjusted spread is already one standard deviation above the mean value since 2000. In other words, there is scope for US Treasuries yields to continue rising relative to German Bund yields based on levels reached in past cycles. Yet at the same time, the spread provides a reasonable level of compensation compared to the riskiness (volatility) of Treasuries, also based on past cycles. We show the same chart for the spread between 10-year US Treasuries and 10-year Japanese government bonds (JGBs) in Chart 12. In this case, there is also scope for additional spread widening although the volatility-adjusted spread is still not as attractive as at previous peaks since 2000. Chart 11UST-Bund Spread Looking Stretched Vs UST Vol

UST-Bund Spread Looking Stretched Vs UST Vol

UST-Bund Spread Looking Stretched Vs UST Vol

Chart 12UST-JGB Spread Getting Stretched Vs UST Vol

UST-JGB Spread Getting Stretched Vs UST Vol

UST-JGB Spread Getting Stretched Vs UST Vol

The message from the volatility-adjusted Treasury-Bund spread lines up with that of the momentum measures of the unadjusted spread. The latter is historically stretched relative to its 200-day moving average, while the change in the spread over the past six months has been as rapid as any of the moves seen since the 2008 financial crisis (Chart 13). Adding it all up, positioning for additional widening of the Treasury-Bund spread is a much poorer bet from a risk versus reward perspective than it was even a few months ago. On a fundamental medium-term basis, however, there is still room for the Treasury-Bund spread to widen further. Relative inflation and unemployment (spare capacity) trends both argue for relatively higher US bond yields (Chart 14). In addition, the Fed is almost certainly going to start tightening monetary policy well before the ECB, thus policy rate differentials will underpin a wider bond spread – although that is already largely discounted in the spread on a forward basis (top panel). Chart 13UST-Bund Spread Momentum Looks Stretched

UST-Bund Spread Momentum Looks Stretched

UST-Bund Spread Momentum Looks Stretched

Chart 14Fundamentals Still Support A Wider UST-Bund Spread

Fundamentals Still Support A Wider UST-Bund Spread

Fundamentals Still Support A Wider UST-Bund Spread

Chart 15Stay Underweight US Vs. Germany On A Strategic Basis

Stay Underweight US Vs. Germany On A Strategic Basis

Stay Underweight US Vs. Germany On A Strategic Basis

Our fundamental fair value model of the 10-year Treasury-Bund spread shows that the spread is still cheap relative to fair value, which is rising (Chart 15). This suggests more medium-term upside in the spread, perhaps even by more than currently priced into the forwards over the next year. Based on this analysis, we see a case for maintaining a core strategic (6-12 month holding period) underweight position for the US versus Germany in our recommended country allocation within our model bond portfolio. At the same time, with the spread looking a bit stretched on some of the momentum and volatility-adjusted measures, we are taking profits on our tactical (0-6 month holding period) 10-year Treasury-Bund spread widening trade using bond futures, realizing a 1.8% return (see the Tactical Overlay table on page 18). Bottom Line: The selloff in US Treasuries has pushed US yields to levels that are starting to look a bit stretched relative to yields from other major developed economies like Germany and Japan. This is especially true on a volatility-adjusted basis. As a result, we are taking profits on our tactical US-Germany spread widening trade. However, we are maintaining our strategic overweight for Germany versus the US in our model bond portfolio, as fundamentals argue for a wider Treasury-Bund spread on a cyclical and strategic basis. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Report, "We’re All Yield Chasers Now", dated August 11, 2020, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Are Central Banks Losing Control Of Bond Yields? No.

Are Central Banks Losing Control Of Bond Yields? No.

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Chart 1Back To Fair Value

Back To Fair Value

Back To Fair Value

February was a terrible month for the bond market. In fact, the Bloomberg Barclays Treasury Master Index returned -1.8%, its worst month since November 2016. The 5-year/5-year forward Treasury yield rose 37 bps. At 2.19%, it is now fairly valued for the first time since 2019, at least according to survey estimates of the long-run neutral fed funds rates (Chart 1). We outlined a checklist for increasing portfolio duration in our Webcast two weeks ago. So far, only two of the five items on our list have been checked. In particular, dollar sentiment and cyclical economic indicators continue to point toward higher yields, even though the market is now priced for a rate hike cycle that is slightly more hawkish than the Fed’s median forecast from December. We anxiously await this month’s revisions to the Fed’s interest rate forecasts. If the Fed’s forecasts remain unchanged from December, then we may get an opportunity to add some duration back into our recommended portfolio. Stay tuned. Feature Investment Grade: Neutral Chart 2Investment Grade Market Overview

Investment Grade Market Overview

Investment Grade Market Overview

Investment grade corporate bonds outperformed the duration-equivalent Treasury index by 65 basis points in February, bringing year-to-date excess returns up to +68 bps. The combination of above-trend economic growth and accommodative monetary policy supports positive excess returns for spread product versus Treasuries. Though Treasury yields have risen in recent weeks, this does not yet pose a risk for credit spreads. The 5-year/ 5-year forward TIPS breakeven inflation rate remains below 2%. We won’t be concerned about restrictive monetary policy pushing credit spreads wider until it reaches a range of 2.3% to 2.5%. Despite the positive macro backdrop, investment grade corporate valuations are extremely tight. The investment grade corporate index’s 12-month breakeven spread is down to its 2nd percentile (Chart 2). This means that the breakeven spread has only been tighter 2% of the time since 1995. The same measure shows that Baa-rated bonds have only been more expensive 3% of the time (panel 3). We don’t anticipate material underperformance versus Treasuries, but we see better value outside of the investment grade corporate space.1 Specifically, we advise investors to favor tax-exempt municipal bonds over investment grade corporates with the same credit rating and duration. We also prefer USD-denominated Emerging Market Sovereign bonds over investment grade corporates with the same credit rating and duration. Finally, the supportive macro environment means we are comfortable adding credit risk to a portfolio. With that in mind, we encourage investors to pick up the additional spread offered by high-yield corporates. Table 3ACorporate Sector Relative Valuation And Recommended Allocation*

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 3BCorporate Sector Risk Vs. Reward*

Stay Bearish On Bonds

Stay Bearish On Bonds

High-Yield: Overweight Chart 3High-Yield Market Overview

High-Yield Market Overview

High-Yield Market Overview

High-Yield outperformed the duration-equivalent Treasury index by 115 basis points in February, bringing year-to-date excess returns up to +178 bps. Ba-rated credits outperformed duration-matched Treasuries by 111 bps on the month, besting B-rated bonds which outperformed by only 104 bps. The Caa-rated credit tier delivered 138 bps of outperformance versus duration-matched Treasuries. We view Ba-rated junk bonds as the sweet spot within the corporate credit space. The sector is relatively insulated from default risk and yet still offers a sizeable spread pick-up over investment grade corporates (Chart 3). We noted in our 2021 Key Views Special Report that the additional spread earned from moving down in quality below Ba is merely in line with historical averages.2 Assuming a 25% recovery rate on defaulted debt and a minimum required risk premium of 150 bps, we calculate that the junk index is priced for a default rate of 2.3% for the next 12 months (panel 3). This represents a steep drop from the 8.3% default rate observed during the most recent 12-month period. However, only 2 defaults occurred in January, down from a peak of 22 in July. Job cut announcements, an excellent indicator of the default rate, have also fallen dramatically (bottom panel). Overall, we see room for spread compression across all junk credit tiers in 2021 but believe that Ba-rated bonds offer the best opportunity in risk-adjusted terms. MBS: Underweight Chart 4MBS Market Overview

MBS Market Overview

MBS Market Overview

Mortgage-Backed Securities underperformed the duration-equivalent Treasury index by 26 basis points in February, dragging year-to-date excess returns down to -2 bps. The nominal spread between conventional 30-year MBS and equivalent-duration Treasuries widened 6 bps in February, but it remains low relative to the recent pace of mortgage refinancings (Chart 4). The MBS option-adjusted spread (OAS) tightened 1 bp on the month to 24 bps. This is considerably below the 57 bps offered by Aa-rated corporate bonds and the 42 bps offered by Agency CMBS. It is only slightly above the 22 bps offered by Aaa-rated consumer ABS. The plummeting primary mortgage spread was a key reason for the elevated refi activity seen during the past year. However, the spread has now recovered back to more typical levels (bottom panel). The implication is that further increases in Treasury yields will likely be matched by higher mortgage rates. This means that mortgage refinancings are likely close to a peak. A drop in refi activity would be a positive development for MBS returns, but we aren’t yet ready to turn bullish on the sector. First, relative OAS valuation favors Aa-rated corporates and Agency CMBS over MBS. Second, the gap between the nominal MBS spread and the MBA Refinance Index remains wide (panel 2) meaning that we could still see spreads adjust higher. Last year’s spike in the mortgage delinquency rate is alarming (panel 4), but it will have little impact on MBS returns. The increase was driven by household take-up of forbearance granted by the federal government. Our US Investment Strategy service has shown that a considerable majority of households will remain current on their loans once the forbearance period ends, causing the delinquency rate to fall back down.3 Government-Related: Neutral Chart 5Government-Related Market Overview

Government-Related Market Overview

Government-Related Market Overview

The Government-Related index underperformed the duration-equivalent Treasury index by 3 basis points in February, dragging year-to-date excess returns down to +21 bps (Chart 5). Sovereign debt underperformed duration-equivalent Treasuries by 95 bps in February, dragging year-to-date excess returns down to -116 bps. Foreign Agencies outperformed the Treasury benchmark by 31 bps on the month, bringing year-to-date excess returns up to +25 bps. Local Authority bonds outperformed by 63 bps in February, bringing year-to-date excess returns up to +203 bps. Domestic Agency bonds outperformed by 1 bp, bringing year-to-date excess returns up to +16 bps. Supranationals underperformed by 2 bps, dragging year-to-date excess returns down to +5 bps. We recently took a detailed look at valuation for USD-denominated Emerging Market (EM) Sovereigns.4 We found that, on an equivalent-duration basis, EM Sovereigns offer a spread advantage versus US corporates for all credit tiers except Ba. We recommend that investors take advantage of this spread pick-up by favoring investment grade EM Sovereigns over investment grade US corporates. Attractive countries include: Qatar, UAE, Saudi Arabia, Mexico, Russia and Colombia. We prefer US corporates over EM Sovereigns in the high-yield space. Ba-rated high-yield US corporates offer a spread advantage over EM Sovereigns and the extra spread available in B-rated and lower EMs comes from distressed credits in Turkey and Argentina. Municipal Bonds: Overweight Chart 6Municipal Market Overview

Municipal Market Overview

Municipal Market Overview

Municipal bonds underperformed the duration-equivalent Treasury index by 6 basis points in February, dragging year-to-date excess returns down to +102 bps (before adjusting for the tax advantage). Municipal bond spreads have tightened dramatically during the past few months and Aaa-rated Munis now look expensive compared to Treasuries, with the exception of the short-end of the curve (Chart 6). That said, if we match the duration and credit rating between the Bloomberg Barclays Municipal bond indexes and the US Credit index, we find that both General Obligation (GO) and Revenue Munis appear attractive compared to US investment grade Credit. Both GO and Revenue Munis offer a before-tax spread pick-up relative to US Credit for maturities above 12 years (bottom panel), the same goes for Revenue bonds in the 8-12 year maturity bucket (panel 3). Revenue bonds in the 6-8 year maturity bucket offer an after-tax yield pick-up versus Credit for investors with an effective tax rate above 0.3%. GO bonds in the 8-12 year and 6-8 year maturity buckets offer breakeven effective tax rates of 1% and 10%, respectively. All in all, municipal bond value has deteriorated markedly in recent months and we downgraded our recommended allocation from “maximum overweight” to “overweight” in January. However, investors should still prefer municipal bonds over investment grade corporate bonds with the same credit rating and duration. Treasury Curve: Buy 5-Year Bullet Versus 2/10 Barbell Chart 7Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury Yield Curve Overview

Treasury yields moved up dramatically in February, with the curve steepening out to the 7-year maturity point and flattening thereafter. The 2/10 Treasury slope steepened 30 bps on the month to reach 130 bps. The 5/30 slope, meanwhile, held steady at 142 bps. Slopes across the entire yield curve traded directionally with yields for the bulk of February. That is, until last Thursday when a surge in bond yields occurred alongside flattening beyond the 5-year maturity point. As a result, the 2/5/10 butterfly spread spiked (Chart 7), moving into positive territory for the first time in a while (panel 4). This curve behavior raises an interesting question. Was last week’s sharp underperformance in the belly a one-off move driven by convexity selling and other technical factors, as many have suggested?5 Or, are we now close enough to a potential Fed liftoff date that we should expect some segments of the yield curve to flatten on days when yields rise? We will be watching the correlations between different yield curve segments and the overall level of yields closely during the next few weeks, but as of today, we think it’s premature to declare that the 5/10 slope has transitioned into a regime where it flattens on days when yields move higher. That being the case, we expect further increases in bond yields to coincide with a falling 2/5/10 butterfly spread, and we retain our recommended position long the 5-year bullet and short a duration-matched 2/10 barbell. TIPS: Overweight Chart 8TIPS Market Overview

TIPS Market Overview

TIPS Market Overview

TIPS outperformed the duration-equivalent nominal Treasury index by 39 basis points in February, bringing year-to-date excess returns up to +183 bps. The 10-year TIPS breakeven inflation rate rose 2 bps on the month to hit 2.17%. The 5-year/5-year forward TIPS breakeven inflation rate fell 15 bps in February to reach 1.91%. February’s TIPS outperformance was concentrated at the front-end of the curve, as investors started to price-in the possibility of higher inflation during the next year or two that eventually subsides. It’s interesting to note that, despite last month’s surge in bond yields, the 5-year/5-year forward TIPS breakeven inflation rate fell, moving further away from the Fed’s 2.3% to 2.5% target range in the process (Chart 8). The Fed will continue to strive for an accommodative policy stance at least until this target is met. Last month’s price action caused our recommended positions in inflation curve flatteners and real yield curve steepeners to perform very well, but we think further gains are possible in the coming months. The 2/10 CPI swap slope has only just dipped into negative territory (panel 4). With the Fed officially targeting a temporary overshoot of its 2% inflation target, this slope should remain inverted for some time yet. With the Fed also continuing to exert more control over short-dated nominal yields than over long-term ones, short-maturity real yields will continue to come under downward pressure relative to the long end (bottom panel). ABS: Overweight Chart 9ABS Market Overview

ABS Market Overview

ABS Market Overview

Asset-Backed Securities outperformed the duration-equivalent Treasury index by 3 basis points in February, bringing year-to-date excess returns up to +20 bps. Aaa-rated ABS outperformed by 2 bps on the month, bringing year-to-date excess returns up to +13 bps. Non-Aaa ABS outperformed by 9 bps on the month, bringing year-to-date excess returns up to +58 bps. The stimulus from last year’s CARES act led to a significant increase in household savings when individual checks were mailed last April. This excess savings has still not been spent, and now another round of checks is pushing the savings rate higher again (Chart 9). The large stock of household savings means that the collateral quality of consumer ABS is very high, with many households using their windfall to pay down debt (bottom panel). Investors should remain overweight consumer ABS and take advantage of strong collateral performance by moving down in credit quality. The Treasury department’s decision to let the Term Asset-Backed Loan Facility (TALF) expire at the end of 2020 does not alter our recommendation. Spreads are already well below the borrowing cost that was offered by TALF, and these tight spread levels are justified by strong household balance sheets. Non-Agency CMBS: Neutral Chart 10CMBS Market Overview

CMBS Market Overview

CMBS Market Overview

Non-Agency Commercial Mortgage-Backed Securities outperformed the duration-equivalent Treasury index by 12 basis points in February, bringing year-to-date excess returns up to +87 bps. Aaa Non-Agency CMBS underperformed Treasuries by 5 bps in February, dragging year-to-date excess returns down to +37 bps. Meanwhile, non-Aaa CMBS outperformed by 75 bps, bringing year-to-date excess returns up to +262 bps (Chart 10). We continue to recommend an overweight allocation to Aaa-rated Non-Agency CMBS and an underweight allocation to non-Aaa CMBS. Even with the expiry of TALF, Aaa CMBS spreads are already well below the cost of borrowing through TALF and thus won’t be negatively impacted. Meanwhile, the structurally challenging environment for commercial real estate could lead to problems for lower-rated CMBS (panels 3 & 4). Agency CMBS: Overweight Agency CMBS outperformed the duration-equivalent Treasury index by 11 basis points in February, bringing year-to-date excess returns up to +39 bps. The average index option-adjusted spread tightened 3 bps on the month to reach 42 bps (bottom panel). Though Agency CMBS spreads have completely recovered back to their pre-COVID lows, they still look attractive compared to other similarly risky spread products. This is especially true when you consider the Fed’s continued pledge to purchase as much Agency CMBS as “needed to sustain smooth market functioning”. Appendix A: Butterfly Strategy Valuations The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: US Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com US Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 4 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 4Butterfly Strategy Valuation: Raw Residuals In Basis Points (As Of February 26TH, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 5 scales the raw residuals in Table 4 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 5Butterfly Strategy Valuation: Standardized Residuals (As Of February 26TH, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Table 6 flips the models on their heads. It shows the change in the slope between the two barbell maturities that must be realized during the next six months to make returns between the bullet and barbell equal. For example, a reading of 39 bps in the 5 over 2/10 cell means that we would only expect the 5-year to outperform the 2/10 if the 2/10 slope steepens by more than 39 bps during the next six months. Otherwise, we would expect the 2/10 barbell to outperform the 5-year bullet. Table 6Discounted Slope Change During Next 6 Months (BPs)

Stay Bearish On Bonds

Stay Bearish On Bonds

Appendix B: Excess Return Bond Map The Excess Return Bond Map is used to assess the relative risk/reward trade-off between different sectors of the US bond market. It is a purely computational exercise and does not impose any macroeconomic view. The Map’s vertical axis shows 12-month expected excess returns. These are proxied by each sector’s option-adjusted spread. Sectors plotting further toward the top of the Map have higher expected returns and vice-versa. Our novel risk measure called the “Risk Of Losing 100 bps” is shown on the Map’s horizontal axis. To calculate it, we first compute the spread widening required on a 12-month horizon for each sector to lose 100 bps or more relative to a duration-matched position in Treasury securities. Then, we divide that amount of spread widening by each sector’s historical spread volatility. The end result is the number of standard deviations of 12-month spread widening required for each sector to lose 100 bps or more versus a position in Treasuries. Lower risk sectors plot further to the right of the Map, and higher risk sectors plot further to the left. Chart 11Excess Return Bond Map (As Of February 26th, 2021)

Stay Bearish On Bonds

Stay Bearish On Bonds

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 For a look at alternatives to investment grade corporates please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 2 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 3 Please see US Investment Strategy Weekly Report, “The Big Bank Beige Book, January 2021”, dated January 25, 2021, available at usis.bcaresearch.com 4 Please see US Bond Strategy Weekly Report, “Searching For Value In Spread Product”, dated January 26, 2021, available at usbs.bcaresearch.com 5 https://www.bloomberg.com/news/articles/2021-02-25/convexity-hedging-haunts-markets-already-reeling-from-bond-rout?sref=Ij5V3tFi Fixed Income Sector Performance Recommended Portfolio Specification Corporate Sector Relative Valuation And Recommended Allocation

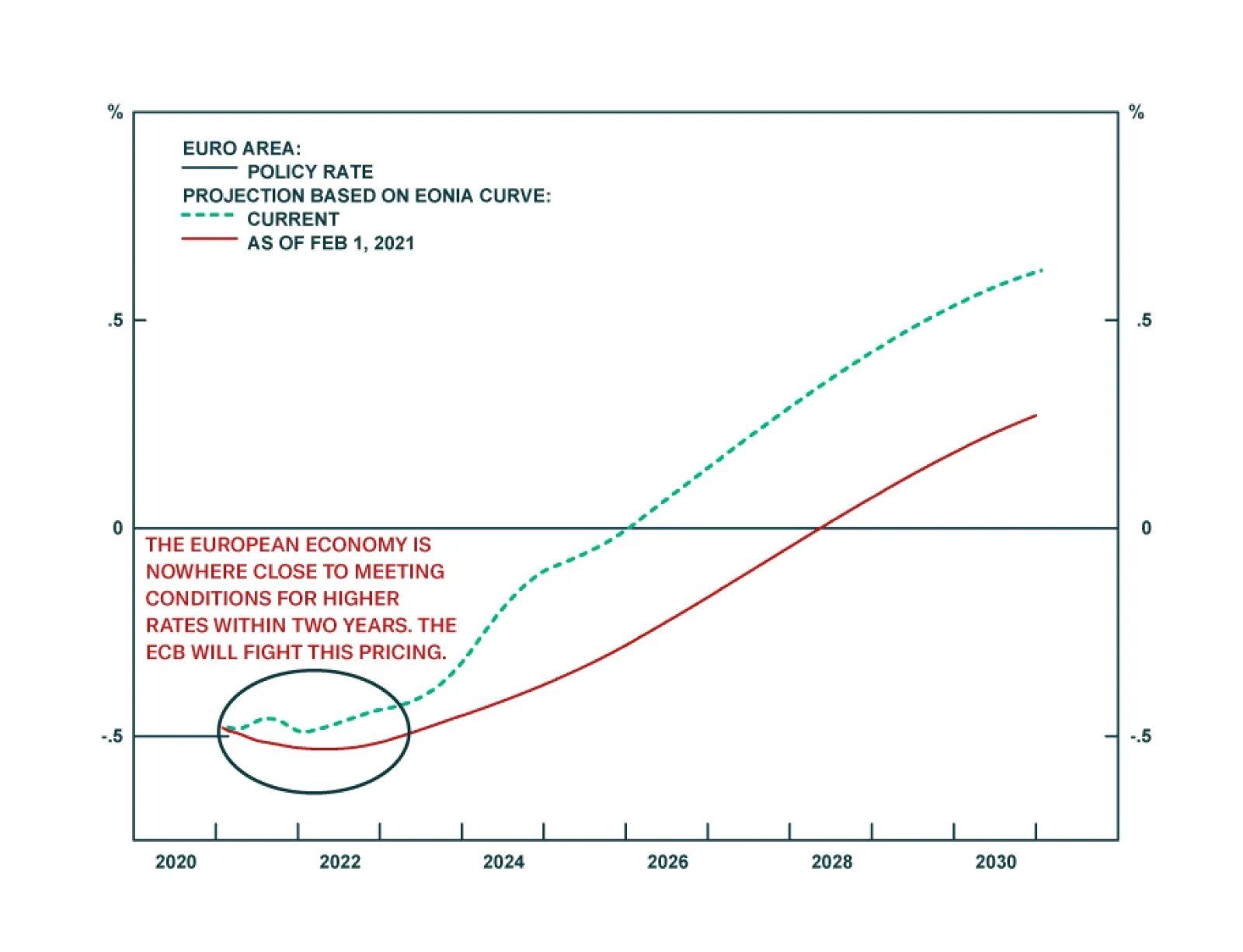

Central banks are becoming uncomfortable with the recent global yield moves. For example, many prominent members of the European Central Bank Governing Council are already suggesting that the ECB could increase the size of its asset purchase to stem the…

Dear Client, In addition to this week’s abbreviated report, we are sending you a Special Report on Bitcoin. I don’t recommend you buy it. Best regards, Peter Berezin Highlights Real government bond yields have increased in recent weeks, which could put further downward pressure on equity prices in the near term. Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. Historically, rising real yields have been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Investors should favor cyclical and value-oriented stocks over defensive and growth-geared plays. Higher Real Yields: A Near-Term Risk For Stocks Chart 1Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Government Bond Yields Have Increased Since Bottoming Last Year

Bond yields have jumped in recent weeks. After bottoming at 0.52% in August, the US 10-year Treasury yield has climbed to 1.54%, up from 0.93% at the beginning of the year. Government bond yields in the other major economies have also risen (Chart 1). While inflation expectations have bounced, the most recent increase in yields has been concentrated in the real component of bond yields (Chart 2). Optimism about a vaccine-led global growth recovery, reinforced by continued fiscal stimulus – especially in the US – has prompted investors to move forward their expectations of how soon and how high policy rates will rise (Chart 3). Chart 2AThe Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (I)

Chart 2BThe Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

The Real Component Has Fueled The Most Recent Rise In Bond Yields (II)

How menacing is the increase in bond yields to stock market investors? Chart 4 shows that there has been a close correlation between real yields and the forward P/E ratio at which the S&P 500 trades. The 5-year/5-year forward real yield, in particular, has moved up sharply, which could put further downward pressure on stocks in the near term. Chart 3Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Path Of Expected Policy Rates Being Revised Upwards

Chart 4Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Rise In Real Rates Is A Headwind For Equity Valuations

Nevertheless, we continue to advocate overweighting equities over a 12-month horizon. As we pointed out two weeks ago, rising real yields have historically been most toxic for stocks when yields have increased in response to hawkish central bank rhetoric. This is manifestly not the case today. In his testimony to Congress this week, Jay Powell downplayed inflation risks, stressing that the US economy was “a long way” from the Fed’s goals. He pledged to tread “carefully and patiently” and give “a lot of advance warning” before beginning the process of normalizing monetary policy. We expect the 10-year Treasury yield to stabilize in the 1.6%-to-1.7% range, still well below the level that would threaten the health of the economy. Favor Cyclical And Value-Oriented Stocks In A Weaker Dollar Environment The Fed’s accommodative stance should limit any near-term upward pressure on the US dollar. Whereas stocks are most sensitive to absolute changes in long-term real bond yields, the dollar is more sensitive to changes in short-term real rate differentials with US trading partners (Chart 5). Since the Fed is unlikely to tighten monetary policy anytime soon, US short-term real rates could fall further as inflation rises. Chart 5The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

The Dollar Is Sensitive To Changes In Short-Term Real Rate Differentials

Chart 6Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical Stocks Tend To Benefit The Most From Stronger Global Growth And A Weaker Dollar

Cyclical stocks, which are overrepresented outside the US, tend to benefit the most from strengthening global growth and a weakening dollar (Chart 6). Value stocks also generally do well in a weak dollar-strong growth environment (Chart 7). Moreover, bank shares – which are concentrated in value indices – typically outperform when long-term bond yields are rising (Chart 8). Chart 7AA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (I)

Chart 7BA Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

A Weaker US Dollar And Stronger Global Growth Should Help Value Stocks (II)

Chart 8Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

Bank Shares Typically Excel When Long-Term Bond Yields Are Rising

In contrast, as relatively long-duration assets, growth stocks often struggle when bond yields go up. The same is true for more speculative plays such as cryptocurrencies. In this week’s Special Report, we discuss the fate of Bitcoin, arguing that investors should resist buying it. Peter Berezin Chief Global Strategist pberezin@bcaresearch.com Global Investment Strategy View Matrix

When Good News Is Bad News

When Good News Is Bad News

Special Trade Recommendations

When Good News Is Bad News

When Good News Is Bad News

Current MacroQuant Model Scores

When Good News Is Bad News

When Good News Is Bad News

Highlights US Treasuries: The uptrend in US Treasury yields has more room to run. However, the primary driver is starting to shift from increased inflation expectations to higher real yields amid greater confidence on the cyclical US economic outlook. Fed Outlook: It is still too soon to expect the Fed to begin signaling a move to turn less accommodative. However, rising realized US inflation amid dwindling spare economic capacity will make the Fed more nervous about its ultra-dovish policy stance in the second half of 2021. This will trigger a repricing of the future path of US interest rates embedded in the Treasury curve, but a Taper Tantrum repeat will be avoided. US Duration: Maintain below-benchmark US duration exposure, with the 10-year Treasury yield likely to soon test the 1.5% level. Feature Chart 1A Cyclical Rise In Global Bond Yields

A Cyclical Rise In Global Bond Yields

A Cyclical Rise In Global Bond Yields

The selloff in global government bond markets that began in the final few months of 2020 has gained momentum over the past few weeks. The benchmark 10-year US Treasury yield now sits at 1.37%, up 45bps so far in 2021, while the 30-year Treasury yield is at a six-year high of 2.22%. Yields are on the move in other countries, as well, with longer-maturity yields moving higher in the UK, Canada, Australia, New Zealand – even Germany, where the 30yr is now back in positive yield territory at 0.20%, a 34bp increase over the past month alone. The main reason for this move higher in yields can be summed up in one word: “optimism”. Economic growth expectations are improving according to investor surveys like the global ZEW, which is a reliable leading indicator of global bond yields (Chart 1). Falling global COVID-19 case numbers with rising vaccination rates, combined with very large US fiscal stimulus measures proposed by the Biden administration, have given investors hope that a return to some form of pre-pandemic economic normalcy can be achieved later this year. That means faster global growth and a risk of higher inflation, both of which must be reflected in higher bond yields. With the 10-year US Treasury yield now already in the middle of our 2021 year-end target range of 1.25-1.5%, and the macro backdrop remaining bond-bearish, we think it is timely to discuss the possibility that our yield target is too conservative Good Cyclical News Is Bad News For Treasuries The more recent move higher in US Treasury yields is notable because it has not been all about higher inflation breakevens, as has been the case since yields bottomed in mid-2020; real yields are finally starting to inch higher. The 30-year TIPS yield now sits in positive territory at +0.09%, ending a period of negative real yields dating back to the pandemic-induced market shock of last spring (Chart 2). Real yields across the rest of the TIPS curve are also starting to stir, even at the 2-year point, yet remain negative. Thus, the price action has supported one of US Bond Strategy’s Key Views for 2021 that the real yield curve will steepen.1 This uptick in US real yields has occurred alongside a string of positive developments on the US economy, suggesting that improved growth prospects – and what that means for future US inflation and Fed policy - are the key driver. Improving US domestic demand US economic data is not only showing resilience but gaining positive momentum. The preliminary US Markit composite PMI (combining both manufacturing and services industries) for February rose to the highest level in six years (Chart 3). Retail sales in January rose by an eye-popping 5.3% versus the month prior, due in no small part to the impact of government stimulus checks issued in the December pandemic relief package. The Conference Board measure of consumer confidence also picked up in January. The improving trend in US data so far in 2021 is pointing to some potentially big GDP numbers – the New York Fed’s “Nowcast” is calling for Q1 real GDP growth of 8.3%. Chart 2US Real Yields Starting Are Stirring

US Real Yields Starting Are Stirring

US Real Yields Starting Are Stirring

Chart 3US Growing Faster Than Lockdown-Stricken Europe

US Growing Faster Than Lockdown-Stricken Europe

US Growing Faster Than Lockdown-Stricken Europe

Vaccine rollout success After a sloppy start to the COVID-19 vaccination program in the US, the numbers are starting to improve with 19% of the US population having received at least one dose (Chart 4). Numbers of new cases and hospitalizations due to the virus have been collapsing as well, a sign that new lockdowns can be avoided, particularly in the larger US coastal cities. The vaccination numbers are even higher in the UK, where Prime Minister Boris Johnson this week revealed an ambitious plan to fully reopen the UK economy by June. While the pace of inoculation has been far slower within the euro area and other developed countries like Canada, developments in the US and UK are a hopeful sign that the vaccines can help free the world economy from the shackles of COVID-19. Chart 4The US & UK Leading The Way On The Vaccine Rollout

Optimism Reigns Supreme

Optimism Reigns Supreme

Even more fiscal stimulus Our US political strategists expect the Biden Administration’s $1.9 trillion pandemic relief package (the “American Rescue Plan”) to be passed by the US Senate in mid-March via a simple majority through a reconciliation bill.2 A second bill is likely to be passed this autumn or next spring with a much larger number, potentially up to $8 trillion worth of spending on infrastructure, health care, child care and green projects over the next ten years (Chart 5). These are big numbers for a $21 trillion US economy that will increasingly need less stimulus as lockdowns ease. Chart 5Biden’s Agenda AFTER The American Rescue Plan

Optimism Reigns Supreme

Optimism Reigns Supreme

Chart 6Welcome Back, Inflation?

Welcome Back, Inflation?

Welcome Back, Inflation?

Chart 7Price Pressures From US Manufacturing Bottlenecks

Price Pressures From US Manufacturing Bottlenecks

Price Pressures From US Manufacturing Bottlenecks

The combined impact of fiscal stimulus, accommodative monetary policy, easy financial conditions and fewer pandemic related economic restrictions has the potential to boost US economic growth quite sharply this year. If US GDP growth follows the Bloomberg consensus forecasts, the US output gap will be fully closed by Q1/2022 (Chart 6).That would be a much faster elimination of the spare capacity created by the 2020 recession compared to the post-2009 experience, raising the risk of upside inflation surprises later this year and in 2022. Signs of growing inflation pressures will make many FOMC members increasingly uncomfortable, even under the Fed’s new Average Inflation Targeting strategy where inflation overshoots will be more tolerated. Already, there are signs of sharply increased price pressures in the US economy stemming from factory bottlenecks (Chart 7). US manufacturers have had to deal with pandemic-induced disruptions to supply chains, in addition to the unexpectedly fast recovery of US consumer demand from last year’s recession that left companies short of inventory.3 The ISM Manufacturing Prices Paid index hit a 10-year high in January, fueled by surging commodity prices, which is already showing up in some inflation data. The US Producer Price Index for finished goods jumped 1.3% in January – the largest monthly surge since 2009 – boosting the annual inflation rate to 1.7% from 0.8% the prior month. Chart 8A Boost To US Inflation Coming Soon From Base Effects

A Boost To US Inflation Coming Soon From Base Effects

A Boost To US Inflation Coming Soon From Base Effects

Chart 9Additional Upside US Inflation Risks

Additional Upside US Inflation Risks

Additional Upside US Inflation Risks

Chart 10US Shelter Inflation Set To Bottom Out

US Shelter Inflation Set To Bottom Out

US Shelter Inflation Set To Bottom Out

A pickup in US annual inflation rates over the next few months was already essentially a done deal because of base effect comparisons versus the collapse in inflation during the 2020 COVID-19 recession (Chart 8). Additional inflation pressures stemming from factory bottlenecks could provide an additional lift to realized inflation rates. When looking at the main components of the US inflation data, there is scope for a broad-based pickup that goes beyond simple base effect moves. Core Goods CPI inflation is now rising at a 1.7% year-over-year rate, the highest since 2012, with more to come based on the acceleration of growth in US non-oil import prices (Chart 9). Core Services CPI inflation has plunged during the pandemic and is now growing at a 0.5% annual rate. As the US economy reopens from pandemic restrictions, services inflation should begin to recover and add to the rising trend of goods inflation. This will especially be true if the Shelter component of US inflation also begins to recover in response to a tightening demand/supply balance for US housing (Chart 10). Bottom Line: US Treasury yields are rising in response to positive upward momentum in US economic growth, the likelihood of some pickup in inflation over the next 6-12 months and, most importantly, shifting expectations that the Fed will turn less dovish later this year. Evaluating The Fed’s Next Moves Fed officials have continued to signal that they are not yet ready to consider any change to monetary policy settings or forward guidance on future rate moves. In his semi-annual testimony before US Congress this week, Fed Chair Jerome Powell reiterated that the pace of the Fed’s asset purchases would only begin to slow once “substantial progress” has been made towards the Fed’s inflation and unemployment objectives. Powell also stuck to his previous messaging that the Fed would “continue to clearly communicate our assessment of progress toward our goals well in advance of any change in the pace of purchases”.4 According to the New York Fed’s Primary Dealer and Market Participant surveys for January, however, the Fed is not expected to stay silent on the topic of tapering for much longer. According to the surveys, the Fed is expected to begin tapering its purchases of Treasuries and Agency MBS in the first quarter of 2022 (Chart 11). A full tapering to zero (net of rollovers of maturing debt) is expected by the first quarter of 2023. Clearly, bond traders and asset managers believe that US growth and inflation dynamics will both improve over the course of this year such that the Fed will have little choice but to begin the signaling of tapering sometime before the end of 2021. Chart 11Fed Surveys Expect A Full QE Tapering In 2022

Optimism Reigns Supreme

Optimism Reigns Supreme