Policy

Highlights 2021 Model Bond Portfolio Broad Allocations: Translating our 2021 global fixed income Key Views into recommended positioning within our model bond portfolio results in the following conclusions: target a relatively aggressive level of overall portfolio risk, while maintaining a moderately below-benchmark duration exposure alongside overweight allocations to lower-quality global corporate credit, and inflation-linked debt, versus nominal government bonds. Specific Allocation Changes: We are increasing credit spread risk in the US by upgrading our recommended overall US high-yield allocation to overweight, focused on B- and Caa-rated credit tiers, while downgrading US investment grade corporates to neutral. We are also reducing the size of our underweights in euro area corporates and shifting the overall allocation to emerging market USD-denominated credit to overweight. Feature Happy New Year! Just before our holiday break last month, we published our 2021 “Key Views” report, outlining the thematic implications of the BCA 2021 Outlook for global bond markets.1 In this follow-up report, we translate those themes into specific investment recommendations and changes to the allocations in the Global Fixed Income Strategy (GFIS) model bond portfolio. The main takeaways are that the expected global backdrop of improving economic growth momentum, a reduction in coronavirus uncertainty as vaccines are distributed, highly accommodative monetary policy and a weakening US dollar will all provide an additional reflationary lift to global financial markets after a strong H2/2020. That means moderately higher global government bond yields (led by US Treasuries) along with outperformance of growth-related spread product like corporate bonds – specifically in the riskier credit segments like US high-yield and emerging markets (Table 1). Table 1GFIS Model Bond Portfolio Recommended Positioning For The Next Six Months

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

A Review Of The 2020 Model Bond Portfolio Performance Before we look ahead to discuss the details of the changes to our model bond portfolio for 2021, we need to take a final look back at the performance of the portfolio in 2020. Chart 12020 Performance: A Positive Year After A Volatile Start

2020 Performance: A Positive Year After A Volatile Start

2020 Performance: A Positive Year After A Volatile Start

Last year, the model bond portfolio delivered a total return (hedged into US dollars) of 5.9%, which outperformed its custom benchmark index by +20bps (Chart 1).2 That moderately solid return was not delivered without some volatility over the course of the year, particularly during the global market tumult last February and March. Over the full year, the government bond portion of the portfolio underperformed the custom benchmark index by -70bps while the spread product segment outperformed by +90bps. The government bond underperformance occurred entirely in the first quarter of the year, as we began 2020 with a recommended below-benchmark global duration stance and an underweight overall allocation to government bonds versus spread product. For a portfolio that is intended to reflect our strategic investment recommendations, the COVID-19 market volatility in Q1/2020 forced us to change our allocations more frequently and aggressively than usual. In early March, we moved to an overweight recommendation on government bonds and underweight on spread product (particular corporate debt) while also shifting the portfolio duration to above-benchmark. That was a large flip from a pro-risk portfolio construction to a defensive one, but which helped claw back some of the severe underperformance in the month of February as government bonds yields plunged and corporate credit spreads surged higher. After the dramatic easing of monetary policy by the major global central banks in March, most notably the US Federal Reserve’s decision to begin buying corporate bonds, we reverted back to a pro-risk stance by upgrading US investment grade credit and Ba-rated high-yield to overweight – positions that were maintained for the rest of 2021. Those US corporate bond exposures alone accounted for essentially all of the spread product outperformance of our model bond portfolio in 2020 (Table 2). Table 2GFIS Model Bond Portfolio Full Year 2020 Overall Return Attribution

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

In terms of specific country exposures (Chart 2), our underweight stance on US Treasuries (both in allocation and duration exposure) early in 2020 severely hurt the government bond portion of the portfolio (-76bps of underperformance versus the benchmark). This dwarfed the 2020 outperformance from other countries like Italy (+11bps), Japan (+17bps), and the UK (+5bps). Importantly, our move to allocate out of nominal government bonds to inflation-linked debt in the US, Italy and Canada back in June was a positive contributor on the year, boosting the overall portfolio outperformance by a combined +25bps. Chart 2GFIS Model Bond Portfolio Full Year 2020 Government Bond Performance Attribution

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Within spread product (Chart 3), the biggest gains outside of US investment grade came from UK investment grade (+18bps), euro area investment grade (+12bps) and US CMBS (+11bps). The biggest drags on performance came from underweights in euro area high-yield (-23bps) and US B-rated high-yield (-17bps), as we maintained a relatively cautious stance on those sectors even during the sharp rally in the latter half of 2020 given the lingering risks from COVID-19 and US election year uncertainty. In the end, 2020 proved to be an outstanding year for taking any kind of credit risk, as the majority of spread product sectors in our model bond portfolio universe strongly outperformed government debt. Chart 3GFIS Model Bond Portfolio Full Year 2020 Spread Product Performance Attribution By Sector

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

In the end, 2020 proved to be an outstanding year for taking any kind of credit risk, as the majority of spread product sectors in our model bond portfolio universe strongly outperformed government debt (Chart 4). Given our overweight stance toward credit, the year ended on a strong note, with the portfolio delivering +16bps of outperformance in Q4/2020 – the details of which can be found in the Appendix on pages 19-23. Chart 4Ranking The Winners & Losers From The GFIS Model Bond Portfolio Universe In 2020

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Top-Down Bond Market Implications Of Our Key Views As a reminder, the main fixed income investment themes from our 2021 Key Views report were the following: Global growth will accelerate over the course of 2021 as COVID-19 vaccines are distributed and economic confidence improves in response. Longer-term global nominal bond yields should see some upward pressure as growth picks up, with US Treasury yields rising the most. Global real bond yields will stay deeply negative with on-hold central banks actively seeking an inflation overshoot. The US dollar will remain soft in 2021, providing an additional reflationary impulse to the global economy. Lower-quality global credit should outperform against a backdrop that will prove positive for risk assets: easy money policies, improving growth momentum and a reduction in virus-related uncertainty. We now present the specific fixed income investment recommendations that derive from those themes, described along the following lines: overall portfolio risk, overall duration exposure, country allocations within government bonds, yield curve allocations within countries, and corporate credit allocations by country and credit rating. Overall Portfolio Duration Exposure: MODERATELY BELOW BENCHMARK Our Global Duration Indicator, comprised of leading economic growth variables, is already signaling that the direction of global bond yields will be higher in 2021 (Chart 5). Successful distribution of COVID-19 vaccines should eventually add additional upward momentum to global growth as confidence improves later in the year. Even if the vaccine rollout does not go as smoothly as expected, that would put pressure for fiscal stimulus policy responses – especially in the US - that can help sustain economic recoveries. Chart 5Global Bond Yields Will Drift Higher In 2021

Global Bond Yields Will Drift Higher In 2021

Global Bond Yields Will Drift Higher In 2021

Chart 6Stay Below-Benchmark On Overall Duration Exposure

Stay Below-Benchmark On Overall Duration Exposure

Stay Below-Benchmark On Overall Duration Exposure

However, with major central banks like the Fed and ECB likely to keep policy rates unchanged in 2021, so as not to impede a recovery in inflation, any upward lift to bond yields will be moderate and driven overwhelmingly by rising longer-term inflation expectations and not a repricing of future monetary policy tightening. That means developed market yield curves should bearishly steepen, in general, as front-end yields remain anchored. We shifted to a below-benchmark overall portfolio duration stance back at the end of last October, equal to just over 0.5 years of duration versus the custom benchmark index (Chart 6). We are comfortable maintaining that position, in that size, while maintaining a bearish steepening bias to yield curve exposure across all countries in the model portfolio. Government Bond Country Allocation: OVERWEIGHT LOW YIELD BETA MARKETS, OVERWEIGHT PERIPHERAL EUROPE, UNDERWEIGHT THE US In more normal times, we would let our expectations of monetary policy changes guide our recommended government bond country allocations. Yet in 2021, we see almost no chance for any meaningful change in the monetary policy bias of any developed market central bank. Thus, we continue to rely on a “yield beta” framework for making fixed income country allocation decisions in our model bond portfolio. In 2021, we see almost no chance for any meaningful change in the monetary policy bias of any developed market central bank. We expect the largest increase in developed market bond yields in 2021 to occur in the US, thus we recommend favoring countries that have a lower sensitivity to changes in US Treasury yields (i.e. the “yield beta”). The obvious candidates are government bonds in Japan and core Europe, where inflation expectations are likely to see less upward pressure than in the US – especially if the US dollar weakens further (Chart 7). Thus, we begin 2021 by maintaining our existing overweight positions in Germany and France. Chart 7Favor Government Bond Markets Less Correlated To UST Yields In 2021

Favor Government Bond Markets Less Correlated To UST Yields In 2021

Favor Government Bond Markets Less Correlated To UST Yields In 2021

The UK has been transitioning from a high-beta to low-beta bond market in recent years and we do not see that trend turning in 2021. The Bank of England (BoE) will maintain a dovish policy bias this year as the UK economy begins adjusting to the post-Brexit world and a stronger pound will dampen inflation pressures. We also begin 2021 by staying overweight UK gilts in our model portfolio. We anticipate that the Italy-Germany government bond spread will converge to the lower Spain-Germany spread in 2021. Chart 8Stay Overweight Italian Government Bonds

Stay Overweight Italian Government Bonds

Stay Overweight Italian Government Bonds

Australia and Canada are two countries where a high yield beta to US Treasuries would make them ideal underweight candidates in a global bond portfolio this year. However, the Reserve Bank of Australia (RBA) and Bank of Canada (BoC) have instituted aggressive quantitative easing (QE) programs that are designed to dampen increases in government bond yields. As a result of these opposing forces on Australian and Canadian bond yields, we begin 2021 with a neutral allocation to both countries. However, we may shift either or both to an underweight stance if we sense any wavering of the commitment of the RBA or BoC to their QE programs amid improving economic growth. We also expect further declines in the risk premia for Italian government bond yields in 2021. The combination of aggressive ECB government bond purchases, which includes greater buying of BTPs than in years past, and signs of a somewhat more supportive backdrop of fiscal unity within the European Union (the €750bn Recovery Fund) reduce both the sovereign credit risk and “redenomination risk” of a potential euro breakup. We anticipate that the Italy-Germany government bond spread will converge to the lower Spain-Germany spread in 2021 – an outcome that last occurred in 2016 (Chart 8). We are not only maintaining our long-held overweight stance on Italy in our model portfolio, we are increasing the size of the allocation to begin 2021. Inflation-Linked Bond Allocations: MAINTAIN EXPOSURE IN THE US, ITALY AND CANADA; ADD A NEW ALLOCATION TO FRANCE Chart 9Stay Overweight Global Inflation-Linked Bonds

Stay Overweight Global Inflation-Linked Bonds

Stay Overweight Global Inflation-Linked Bonds

Inflation-linked bonds had a strong relative performance versus nominal government debt across the developed markets during the second half of 2020, with breakevens widening even in countries with low realized inflation like France and Australia. Dovish central banks, the reflationary impacts of rising commodity prices (also fueled by US dollar weakness), and the V-shaped recovery in global economic growth from the 2020 COVID-19 recession have all played a role in helping lift breakevens from the depressed levels seen last spring. None of those factors is expected to change during at least the first half of 2021, thus allocations to inflation-linked bonds are still justified in several countries. We are adding a new position in French inflation-linked bonds versus nominal French bonds with breakevens below our model-implied fair value. Our fair value models for 10-year inflation breakevens show that valuations are no longer unequivocally cheap in most countries, but only in Australia do breakevens look much too high relative to underlying fundamental drivers (Chart 9). US TIPS breakevens are approaching levels that would appear “expensive”, defined as at least one standard deviation above fair value, but we still see additional upside as the model implied fair value is also rising. We currently have recommended allocations to inflation-linked bonds in the US, Italy and Canada in our model portfolio, and we are maintaining those positions as we begin 2021. We are adding a new position in French inflation-linked bonds versus nominal French bonds with breakevens below our model-implied fair value. Spread Product Allocation: OVERWEIGHT GLOBAL CORPORATES VERSUS GOVERNMENT BONDS, FOCUSED ON US HIGH-YIELD AND EM Our expectation of a combination of improving global economic growth and persistent reflationary monetary policies is a very positive backdrop for global spread product, most notably corporate bonds. However, valuations across the global corporate debt spectrum are not universally cheap after the strong H2/2020 performance. Thus, we are maintaining only a moderate overall overweight stance on spread product versus government bonds in our model bond portfolio, equal to 5% of the portfolio (Chart 10). At the same time, we recommend taking more relative spread risk within that moderate overweight allocation. This is the way we are balancing the competing forces of a pro-risk backdrop and increasingly stretched valuations in many sectors. The biggest change we are making to the credit side of our model bond portfolio is downgrading US investment grade corporate exposure to neutral while upgrading US high-yield to overweight. As we discussed in our 2021 Key Views report, spread valuation measures are more stretched for higher-rated US investment grade corporate debt compared to junk bonds. Chart 10A Moderate Recommended Overweight To Global Spread Product In 2021

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Combined with a monetary liquidity backdrop that supports the performance of riskier assets like high-yield (Chart 11), we anticipate that US high-yield will be a relatively strong performer within the US credit markets in 2021. Chart 11Upgrade Lower Rated US High-Yield To Overweight

Upgrade Lower Rated US High-Yield To Overweight

Upgrade Lower Rated US High-Yield To Overweight

When looking at the relationship between spread valuation (using our preferred metric of 12-month breakeven spreads) and risk (using a standard measure like duration-times-spread), the lower rated credit tiers of US high-yield stand out as having the most attractive risk/valuation tradeoff (Chart 12). Thus, we are focusing our shift to an overweight stance on US high-yield in our model bond portfolio by increasing the allocations to the B-rated and Caa-rated tiers. Chart 12Comparing Value (Breakeven Spreads) With Risk (Duration Times Spread)

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Outside the US, we are also adding additional spread product exposure by increasing the weightings to euro area high-yield and emerging market USD-denominated sovereign debt. However, we are still maintaining a relatively higher allocation to US high-yield over euro area equivalents, and emerging market USD-denominated corporate debt over sovereigns. The biggest change we are making to the credit side of our model bond portfolio is downgrading US investment grade corporate exposure to neutral while upgrading US high-yield to overweight. Finally, we are entering 2021 with the same relative tilt within US mortgage-backed securities (MBS) we maintained during the latter half of 2020, with an overweight stance on agency commercial MBS and an underweight on agency residential MBS. Overall Portfolio Risk: AGGRESSIVE The net impact of all the changes made to our portfolio allocations is to boost the estimated tracking error – the relative portfolio volatility versus that of the benchmark – from 31bps to 73bps (Chart 13). This is a significant increase in the usage of our portfolio “risk budget”, but the tracking error is still below our self-imposed limit of 100bps. Chart 13Taking A More Aggressive Posture On Overall Portfolio Risk

Taking A More Aggressive Posture On Overall Portfolio Risk

Taking A More Aggressive Posture On Overall Portfolio Risk

Chart 14Boosting Portfolio Yield Through Selective Overweights

Boosting Portfolio Yield Through Selective Overweights

Boosting Portfolio Yield Through Selective Overweights

After maintaining a cautious stance on overall portfolio risk levels in the latter half of 2020, given the persistent uncertainties over the spread of COVID-19 and the US presidential election, we now deem it appropriate to be more aggressive within our model bond portfolio allocations. The pro-risk positioning changes will also boost the overall yield of the model bond portfolio. The greater allocations to riskier spread product sectors leave the portfolio with a yield that begins 2021 modestly higher than that of the benchmark index (Chart 14). Portfolio Scenario Analysis For The Next Six Months After making the shifts to our model bond portfolio allocations, which can all be seen in the tables on pages 24-25, we now turn to scenario analysis to determine the return expectations for the portfolio for the first half of 2021. Table 2AFactor Regressions Used To Estimate Spread Product Yield Changes

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Table 2BEstimated Government Bond Yield Betas To US Treasuries

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

On the credit side of the portfolio, we use risk-factor-based regression models to forecast future yield changes for global spread product sectors as a function of four major factors - the VIX, oil prices, the US dollar and the fed funds rate (Table 2A). For the government bond side of the portfolio, we avoid using regression models and instead use a yield-beta driven framework, taking forecasts for changes in US Treasury yields and translating those in changes in non-US bond yields by applying a historical yield beta (Table 2B). For our scenario analysis over the next six months, we use a base case scenario plus two alternate “tail risk” scenarios, based on the following descriptions and inputs: Base Case The current surge of global COVID-19 cases gives way to increased distribution of vaccines. The result is a steady improvement in global growth. Some additional fiscal stimulus is delivered in the US and the larger countries of Europe. Central banks keep their foot on the monetary accelerator with realized inflation moving only modestly higher. The US Treasury curve bear steepens as US inflation expectations continue drifting higher. The VIX index reaches 23, the US dollar depreciates by -5%, oil prices climb +10% and the fed funds rate remains at 0%. Optimistic Scenario The global distribution of COVID-19 vaccines goes smoothly and rapidly, while the current surge in COVID-19 cases fades in the early weeks of 2021. Global growth quickly accelerates on the back of soaring consumer & business confidence. Global fiscal stimulus surprises to upside, while central banks remain super-dovish even as inflation perks up. The US Treasury curve bear-steepens substantially as US inflation expectations steadily increase. The VIX index falls to 18, the US dollar depreciates by -10% in a pro-risk/pro-growth move, oil prices climb +20% and the fed funds rate remains at 0%. Pessimistic Scenario The vaccine rollout is slower than expected, with COVID-19 restrictions remaining in place for longer. Policymakers deliver inadequate new fiscal and monetary stimulus measures to support underwhelming growth. The US Treasury curve bull-flattens as US inflation breakevens plunge. The VIX index soars to 35, the US dollar appreciates by +5%, oil prices plunge -20% and the fed funds rate remains at 0%. The excess return scenarios for the model bond portfolio, using the above inputs in our simple quantitative return forecast framework, are shown in Table 3A. The US Treasury yield assumptions are shown in Table 3B. For the more visually inclined, we present charts showing the model inputs and Treasury yield projections in Chart 15 and Chart 16, respectively. Table 3AGFIS Model Bond Portfolio Scenario Analysis For The Next Six Months

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Table 3BUS Treasury Yield Assumptions For The 6-Month Forward Scenario Analysis

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Chart 15Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Risk Factor Assumptions For The Scenario Analysis

Chart 16US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

US Treasury Yield Assumptions For The Scenario Analysis

The model bond portfolio is expected to deliver an excess return over its performance benchmark during the next six months of +50bps in the base case and +78bps in the optimistic scenario, but is projected to underperform by -37bps in the pessimistic scenario. These are larger expected relative returns than witnessed during the latter half of 2020, consistent with the larger tracking error we are taking entering 2021. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, "2021 Key Views: Vaccination, Reflation, Rotation," dated December 17, 2020, available at gfis.bcarsearch.com. 2 Our model bond portfolio custom benchmark index is the Bloomberg Barclays Global Aggregate Index, but with allocations to global high-yield corporate debt and USD-denominated emerging market debt replacing very high quality spread product (i.e. AA-rated). We believe this to be more indicative of the typical internal benchmark used by global multi-sector fixed income managers. Appendix Appendix Chart 1Q4/2020 GFIS Model Bond Portfolio Performance

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Appendix Table 1GFIS Model Bond Portfolio Q4/2020 Overall Return Attribution

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Appendix Chart 2GFIS Model Bond Portfolio Q4/2020 Government Bond Performance Attribution

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Appendix Chart 3GFIS Model Bond Portfolio Q4/2020 Spread Product Performance Attribution By Sector

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Appendix Chart 4Ranking The Winners & Losers From The GFIS Model Bond Portfolio In Q4/2020

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Our Model Bond Portfolio Strategy For 2021: Leaning Into Reflation

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

According to BCA Research’s Global Asset Allocation Strategy service, a rapid rollout of vaccines means that the economy should be on track to return to near-normality by the second half of 2021. Therefore, the key thing for investors to think about is what…

This is US Bond Strategy’s final report of the year. Our regular publication schedule will resume on January 5th with our Portfolio Allocation Summary for January 2021. We wish you a happy, healthy and prosperous new year. Highlights Interest Rate Policy: The Fed has given us a checklist of three criteria that must be met before it will lift rates off the zero bound. After those criteria are met, the pace of the eventual rate hike cycle will be determined by how quickly inflation expectations move back to “well-anchored” levels. We don’t expect Fed liftoff in 2021. Balance Sheet Policy: The Fed will only increase the pace or lengthen the maturity of its asset purchases if the economy or risk assets undergo a significant negative shock in 2021. Absent that, Fed communications in late-2021 will increasingly focus on the eventual tapering of asset purchases. Given the current vague guidance about when tapering will start, a scaled-down repeat of the 2013 Taper Tantrum is possible in late-2021 or 2022. Emergency Lending Facilities: The Fed will not undertake efforts to subvert Congress and re-establish its emergency lending facilities in 2021. However, the absence of the facilities will not have a negative impact on financial markets. Fiscal/Monetary Coordination: Looking beyond 2021, we see the lines between fiscal and monetary policy continuing to blur. The Fed will be increasingly incentivized to dip its toes into the fiscal arena and fiscal policymakers will let it. Feature Chart 1An Eventful Year

An Eventful Year

An Eventful Year

It would be an understatement to say that 2020 was a busy year for the Federal Reserve. The Fed cut rates to the zero bound when the recession struck in March. It also exploded its balance sheet to fresh all-time highs and rolled out brand-new emergency lending facilities to support flagging credit markets (Chart 1). Then, to top it all off, the Fed concluded a Strategic Review of its monetary policy strategy in August and officially adopted an Average Inflation Target. This report touches on the market implications of 2020’s big Fed moves, but its focus is on what the Fed is likely to do in 2021. The first three sections discuss how we see the Fed’s interest rate policy, balance sheet policy and emergency lending facilities evolving next year. The final section considers a longer time horizon as it discusses what might be the next frontier for monetary policy: increased cooperation between monetary and fiscal authorities. Interest Rate Policy With the fed funds rate at its effective lower bound, bond investors will spend 2021 trying to determine the eventual start date and magnitude of the next tightening cycle. This will be especially complicated because the Fed’s adoption of an Average Inflation Target means that old models of its reaction function must be discarded. We discussed the implications of the move toward Average Inflation Targeting in a September Special Report.1 To quickly recap, the Fed made three main changes that will influence our outlook for interest rate policy in 2021. First, the Fed edited its Statement on Longer-Run Goals and Monetary Policy Strategy to include a new interpretation of its price stability mandate. The new Statement reads: In order to anchor longer-term inflation expectations at [2 percent], the Committee seeks to achieve inflation that averages 2 percent over time, and therefore judges that, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.2 Second, the Fed modified its Statement on Longer-Run Goals and Monetary Policy Strategy to signal that it will rely less on labor market indicators to forecast future inflation. In its old Statement, the Fed talked about minimizing “deviations of employment from the Committee’s assessments of its maximum level.” The revised Statement talks about mitigating “shortfalls of employment from the Committee’s assessment of its maximum level.” In other words, the Fed is saying that it will be less inclined to view an unemployment rate below its estimated natural level (NAIRU) as a signal that inflation is about to accelerate. The Fed’s adoption of an Average Inflation Target means that old models of its reaction function must be discarded. Finally, at the September FOMC meeting, the Fed translated the changes it made to its Statement on Longer-Run Goals and Monetary Policy Strategy into more explicit guidance about when it will consider lifting rates off the zero bound. That guidance is as follows: … it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.3 The Timing Of Liftoff Table 1A Checklist For Liftoff

The Fed In 2021

The Fed In 2021

Digging into the new guidance, we identify three criteria for lifting rates off the zero bound (Table 1). First, the unemployment rate must reach levels consistent with the Committee’s assessments of NAIRU. Currently, those estimates range from 3.5% to 4.5% (Chart 2). Practically, we view this as the least important of the three criteria. NAIRU estimates are revised based on what happens with inflation, and the Fed has already acknowledged that it is now less inclined to view a sub-NAIRU unemployment rate as an inflationary signal. In short, if inflation were to rise sustainably above 2% with the unemployment rate still at 5%, the Fed would simply revise up its NAIRU estimates and begin the rate hike cycle. Chart 2Criteria For Lifting Rates

Criteria For Lifting Rates

Criteria For Lifting Rates

The Fed’s second criterion for lifting rates is also the most specific. Inflation must rise to 2 percent before the Fed will consider hiking rates. In a recent speech, Fed Vice-Chair Richard Clarida said he interprets this to mean that 12-month PCE inflation must be at least 2% before the Fed will consider hiking (Chart 2, bottom panel).4 This is helpful for bond investors. We can be certain that no rate hikes will occur at least until 12-month PCE inflation reaches 2%. Finally, the Fed also wants to be certain that inflation is “on track to moderately exceed 2 percent for some time.” This means that the event of 12-month PCE reaching 2% won’t automatically lead to a rate increase. The Fed must also view inflation gains as sustainable. This will likely become an issue in the first half of 2021 when we know that base effects will push 12-month PCE sharply higher, possibly even above 2%. However, we also know that those gains will be short lived.5 Of course, the Fed also knows about the impact of base effects and it will look past any temporary jump in inflation in H1 2021. More generally, while we advise investors to not pay much attention to the Fed’s NAIRU estimates, the unemployment rate will play a role in the Fed’s determination of whether above-2% inflation is sustainable. That is, the Fed is more likely to view above-2% inflation as sustainable if the unemployment rate is 4% than it is if the unemployment rate is 6%. What Does The Market Think? The bond market has been quick to price-in the big shift in the Fed’s interest rate guidance. At present, the overnight index swap curve is priced for a single 25 basis point rate hike in mid-2023 and only one more by mid-2024 (Chart 3). We see a good chance that the Fed’s three liftoff criteria are met before then, a view that forms the basis of our below-benchmark portfolio duration recommendation for 2021.6 In addition, the New York Fed’s Survey of Market Participants shows that only 43% of respondents expect liftoff before the end of 2023 and only 31% before the end of 2022 (Table 2A). This is further evidence that bond yields have room to rise if it looks like the Fed’s three liftoff criteria will be met in 2022 or the first half of 2023. Finally, the New York Fed’s survey shows that market participants understand the Fed’s three liftoff criteria and that differences in opinion about the timing of liftoff reflect differences in views about the economic outlook, not differences in understanding the Fed’s reaction function. The bulk of survey respondents think that the unemployment rate will be between 3.5% and 4.2% (consistent with the Fed’s NAIRU estimates) and that 12-month PCE inflation will be between 2.2% and 2.5% at the time of liftoff (Table 2B). Chart 3The Fed May Lift Rates Sooner Than Markets Expect

The Fed May Lift Rates Sooner Than Markets Expect

The Fed May Lift Rates Sooner Than Markets Expect

Table 2ALiftoff Expectations

The Fed In 2021

The Fed In 2021

Table 2BMarkets Understand The Fed’s Guidance

The Fed In 2021

The Fed In 2021

The Pace Of Tightening And Why We’re Watching Inflation Expectations We’ve seen the three criteria upon which the Fed will condition its decision to hike rates off the zero bound. But the timing of liftoff is not the only thing that bond investors need to consider. We also need to get a sense of how quickly rate hikes will proceed once the next tightening cycle begins. According to the Fed’s interest rate guidance, even after liftoff the Fed will seek to maintain accommodative monetary conditions until it has achieved its price stability goal under its new Average Inflation Target. Recall that this goal is defined as achieving “inflation that averages 2 percent over time”. This is somewhat vaguer than the Fed’s liftoff guidance. Over what time period should we seek to hit average 2% inflation? One option is to start calculating the average when the new regime was adopted in August. In that case, average PCE inflation is running at 0.96%, well below 2%. Alternatively, we could calculate average inflation since the Fed last cut rates to zero in March 2020 (1.50%) or average inflation since the Fed cut rates to zero in December 2008 (1.43%). The point is that the Fed has not given us a clearly defined target. Differences in opinion about the timing of liftoff reflect differences in views about the economic outlook. For this reason, it’s important for bond investors to understand why the Fed has shifted to an Average Inflation Target. The reason has to do with trying to re-anchor inflation expectations. Box 1 shows an example of an Expectations-Augmented Phillips Curve, the Fed’s go-to framework for thinking about inflation. As the accompanying quote from Janet Yellen explains, the Fed thinks about inflation’s long-run trend as being driven by expectations. Shocks to economic slack and import prices can cause inflation to deviate from its long-run trend, but expectations drive the trend itself. This makes it critical for a central bank to keep expectations well anchored near its inflation target. Box 1The Expectations-Augmented Phillips Curve (aka The Fed’s Inflation Model)

The Fed In 2021

The Fed In 2021

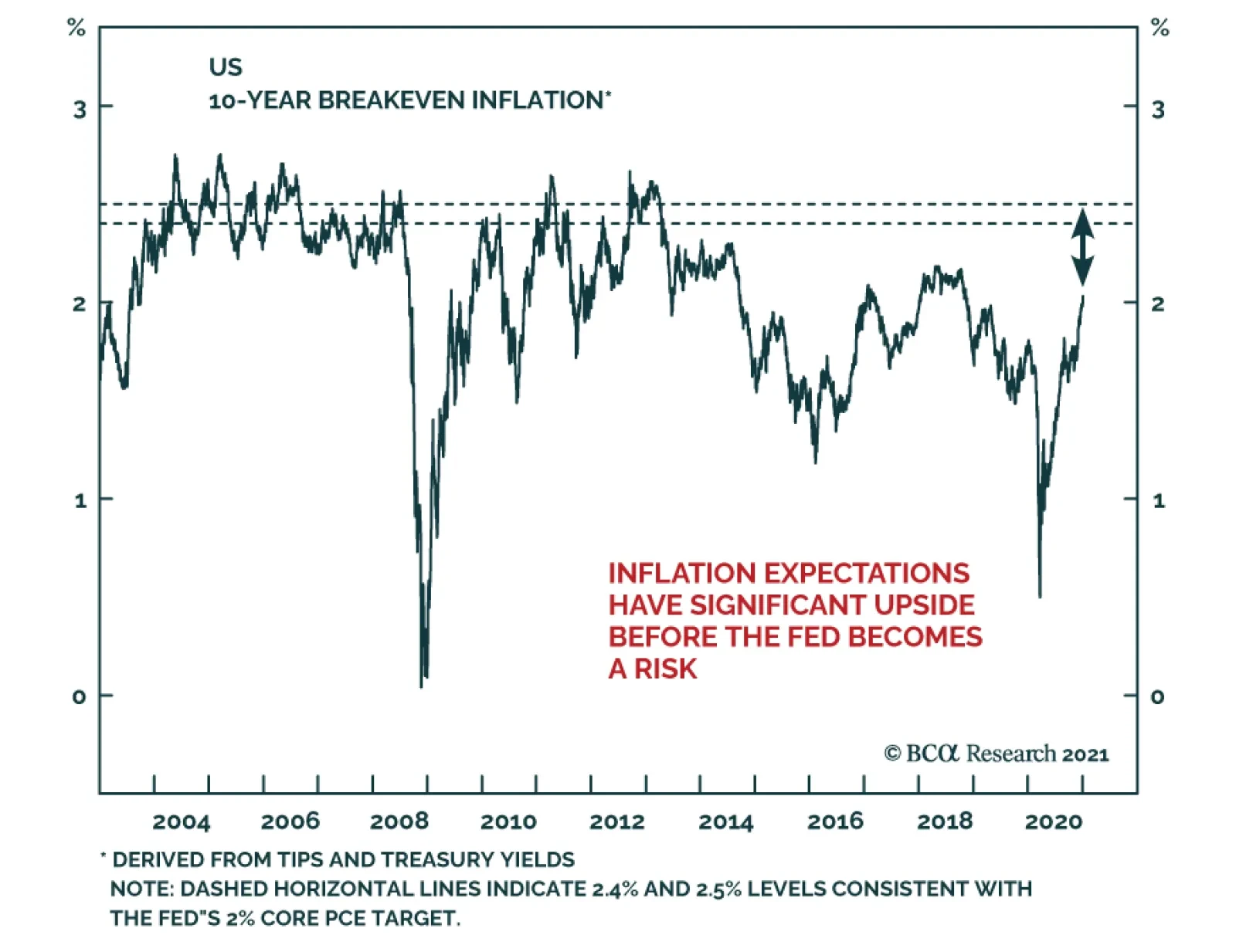

This is the underlying rationale for the Fed’s Average Inflation Target. The Fed has observed that inflation expectations have been too low in recent years. In the Fed’s model, this signals that inflation’s long-run trend has shifted down. In order to get expectations back up to target, the Fed understands that it will probably need to accept a period of above-target inflation. Since economic agents have just experienced a long period of sub-2% inflation, it will probably require a significant period of above-2% inflation before their expectations sustainably shift higher.7 To sum it all up, the Fed will seek to keep monetary conditions accommodative, and thus supportive for risk assets, until inflation expectations are deemed to be re-anchored. At that point, monetary policy will shift to a neutral or restrictive stance and risk asset performance will be challenged. But don’t just take our word for it. Here is what Vice-Chair Clarida said in a recent speech (referenced above): It is important to note, however, that the goal of the new framework is to keep inflation expectations well anchored at 2 percent, and, for this reason, I myself plan to focus more on indicators of inflation expectations themselves – especially survey-based measures – than I will on the calculation of an average rate of inflation over any particular window of time. It is clear that inflation expectations will dictate the eventual pace of Fed tightening. But the question of what measure of inflation expectations to track remains unresolved. Measures of inflation expectations fall into three main categories: Market-based measures Survey measures Trend measures Market-based measures are derived from inflation-linked bonds. Specifically, we derive TIPS breakeven inflation rates for different time horizons by taking the difference between a nominal yield and TIPS yield of the same maturity. In this publication, we often refer to the 10-year and 5-year/5-year forward TIPS breakeven inflation rates and have found that a range of 2.3% to 2.5% has historically been consistent with periods when inflation expectations were deemed “well anchored” (Chart 4A). One potential issue with using market-based measures of inflation expectations is that TIPS prices can sometimes move around for reasons unrelated to changing inflation expectations. That is, regulations or broader portfolio diversification concerns could change the risk premium an investor is willing to accept from TIPS, even if that investor’s underlying inflation view is unchanged. Academics have made attempts to solve this problem by using affine term structure models to decompose yields into various components. Chart 4B presents one such model from D’Amico, Kim and Wei (DKW).8 The DKW model splits the TIPS breakeven inflation rate (or inflation compensation) into an inflation expectation, a liquidity premium that compensates investors for the lower liquidity in TIPS compared to nominal Treasuries and an inflation risk premium that represents the extra compensation investors require to take inflation risk. We are skeptical of the usefulness of affine term structure models. In general, these models have too few inputs to reliably generate the components they purport to measure. However, the Fed clearly pays some attention to the DKW decomposition. If a future increase in TIPS breakeven inflation rates is driven entirely by movement in the liquidity or inflation risk premium components, it would be reasonable to question whether the Fed will react. Chart 4AInflation Expectations: Market-Based Measures

The Fed In 2021

The Fed In 2021

Chart 4BA Decomposition Of TIPS##br## Breakevens

The Fed In 2021

The Fed In 2021

Survey measures of inflation expectations are exactly that: Responses from surveys, usually of professional forecasters or households (Chart 4C). One drawback of survey measures compared to market-based measures is that they are updated less frequently. Another is that survey respondents, particularly households, may only be able to distinguish very large swings in prices. That said, the Fed tracks a wide range of survey measures and they were even singled out by Vice-Chair Clarida as being particularly important in the above quote. Trend inflation measures are statistical measures of the trend in the actual PCE or CPI inflation data. Chart 4D shows both a very simple trend measure, the 10-year annualized rate of change, and a slightly more complex trend measure based on an exponential smoothing rule. Academics have developed even more complex trend inflation measures.9 The logic behind these measures is that expectations tend to adapt only slowly to changes in the actual inflation data. Chart 4CInflation Expectations: Survey Measures

The Fed In 2021

The Fed In 2021

Chart 4DInflation Expectations: Trend Measures

The Fed In 2021

The Fed In 2021

Finally, we should point out a relatively new measure that the Fed will be using to track inflation expectations going forward. It is called the Common Inflation Expectations Index and it is a composite of 21 different survey and market-based inflation measures (Chart 4E), no trend inflation measures are included.10 Chart 4EIntroducing The Common Inflation Expectations Index

The Fed In 2021

The Fed In 2021

To summarize, the Fed has given us a checklist of three criteria that must be met before it will lift rates off the zero bound. After those criteria are met, the pace of the eventual rate hike cycle will be determined by how quickly inflation expectations move back to levels that are considered “well anchored”. Once that happens, the Fed will no longer have an incentive to keep monetary conditions accommodative and risk asset performance will be challenged. Charts 4A-4E in this report provide a wide array of different measures of inflation expectations to monitor. We will keep an eye on all of them, but in particular, we will track the Common Inflation Expectations Index’s progress back to 2.1% and the 5-year/5-year forward TIPS breakeven inflation rate’s progress back to a range of 2.3%-2.5%. While we don’t expect the Fed’s rate hike criteria to be met in 2021, a 2022 liftoff is possible if the COVID vaccine spurs a rapid economic recovery. However, we do expect that, in 2021, the market will start to price-in an earlier liftoff date and quicker pace of tightening than is currently discounted, thus pushing bond yields higher. The Financial Conditions Wildcard Chart 5Financial Conditions

Financial Conditions

Financial Conditions

Our base case view is that the eventual pace of Fed tightening will be determined by inflation expectations. However, there is one wildcard that could cause the Fed to abandon its inflation expectations goal and tighten policy earlier. That wildcard is financial conditions. Presently, financial asset valuations are a mixed bag (Chart 5). Corporate bond spreads are tight, but not at all-time expensive levels. Equity P/E ratios are very elevated, but equities don’t look expensive compared to bonds. If these valuations stay relatively stable, the Fed will continue to rely on inflation expectations to guide the pace of tightening. However, if inflation expectations take a long time to rise, it is conceivable that such a long period of low interest rates could lead to historically stretched financial asset valuations. In short, if inflation doesn’t return within the next couple of years, the Fed may have to tighten policy to take the wind out of an asset bubble that might otherwise burst and lead to an economic recession. We stress that we are not yet close to this point and that the bar for the Fed to abandon its inflation goal will be very high, but we would place financial conditions alongside inflation expectations as the two most important variables to monitor to assess the eventual pace of Fed tightening. Balance Sheet Policy With the funds rate pinned at zero and the Fed’s interest rate guidance essentially set in stone, changes to the pace and composition of asset purchases are the principal tool that the Fed will use to provide more or less immediate monetary accommodation in 2021. The Fed is currently purchasing $80 billion of Treasuries and $40 billion of Agency MBS each month, with Treasury purchases spread out across the yield curve. If this pace and distribution of Treasury purchases is maintained in 2021, the Fed will end up purchasing less and less of the Treasury flow. The Treasury Department has a stated policy goal of increasing the average maturity of the outstanding debt and it has been pursuing that goal by raising the amount of coupon issuance at the expense of bills. The Treasury has already given us its planned coupon issuance schedule for Q4 2020 and Q1 2021. Chart 6 shows that net Fed coupon purchases will gradually decline as a percentage of gross issuance, assuming the Treasury follows through with its plan and the Fed’s balance sheet policy is unchanged. Chart 6The Path For Treasury Supply And Fed Demand

The Fed In 2021

The Fed In 2021

Can The Fed Do More? … Will The Fed Do More? It is possible that the Fed will use its balance sheet to provide more monetary easing in 2021. There are two ways it could do this. First, it could simply increase the monthly pace of asset purchases. Alternatively, it could keep the same pace of purchases but shift Treasury buying toward the long-end of the curve. The idea here would be to prevent long-dated yields from rising too quickly. One or both of these changes could happen in 2021, but only if the economy experiences a negative growth shock or risk asset prices (equities and corporate credit) fall significantly. In that case, the Fed will want to be seen as responding to a negative shock, but absent that, the Committee seems comfortable with its current balance sheet strategy. Chart 7Rate-Sensitive Sectors Have Recovered

Rate-Sensitive Sectors Have Recovered

Rate-Sensitive Sectors Have Recovered

Some have suggested that, even if the economic recovery stays on track, the Fed will try to use its balance sheet to lean against rising long-maturity bond yields. We doubt this. First, it is not obvious that the Fed would be able to stop the 10-year Treasury yield from rising to a range of, say, 1.25% to 1.5% by increasing bond purchases in that maturity range by a few billion dollars. As long as the Fed’s interest rate guidance is unchanged, the market’s interest rate expectations will continue to exert a powerful influence on bond yields across the entire curve. Unless the Fed announces a cap on long-dated bond yields, and pledges to buy enough securities to enforce that cap, we are skeptical about the effectiveness of just changing the quantity of asset purchases. Second, it is also not clear that a 10-year Treasury yield between 1.25% and 1.5%, in the context of a steepening yield curve and improving economic growth, would be a problem for either the economy or risk assets. In fact, these sorts of environments tend to be very positive for risk asset performance.11 It is only when the Fed is shifting to a more restrictive monetary policy stance and the yield curve is flattening that bond yields start to exert a negative influence on the economy and risk assets. Even if the Fed is not worried about a moderate bear-steepening of the Treasury curve, a case could be made for providing more easing right now in order to spur a quicker recovery. This question was posed to Chair Powell several times at the last FOMC press conference. In response, Powell noted that the sectors of the economy that are most sensitive to interest rates – residential investment and consumer spending on durable goods – have already recovered (Chart 7). The lagging sectors of the economy – particularly consumer spending on services – cannot recover until the COVID vaccine is widely distributed, irrespective of the level of interest rates. In our view, this is an acknowledgement that the Fed does not see much value in trying to provide further accommodation through the balance sheet channel. All in all, our base case scenario is that the Fed will maintain its current pace and maturity distribution of asset purchases throughout 2021. However, it will increase the pace and/or lengthen the maturity if there is a significant shock to the economy and/or financial markets. Later in 2021, if the recovery stays on track, Fed communications will increasingly take up the issue of when it will be appropriate to taper its pace of asset purchases. The Exit From Asset Purchases And The Possibility Of A Taper Tantrum Chart 8Remember The Taper Tantrum

Remember The Taper Tantrum

Remember The Taper Tantrum

The Fed has already given us a timeline for how it will wind down its asset purchases. According to the minutes from the November FOMC meeting, most participants support a timeline where the Fed will start tapering its pace of asset purchases sometime before the first rate hike. It will then begin lifting interest rates and will stop purchases altogether sometime after that. At the December FOMC meeting, the Fed gave us additional guidance on when it will start the tapering process. Unfortunately, this guidance is quite vague and only confirms the fact that tapering will start before the liftoff date. Specifically, the Fed said that tapering will begin when “substantial further progress has been made toward the Committee’s maximum employment and price stability goals.” Because the guidance around the timing of the tapering process is quite vague, we think it’s possible that it could sneak up on investors and lead to a sharp upward re-adjustment in rate hike expectations, and thus a bond sell-off. In essence, a tamer version of the 2013 Taper Tantrum is possible in late-2021 or 2022. On May 22, 2013, Fed Chair Ben Bernanke explained the Fed’s plan to eventually start tapering its asset purchases. Because investors took this to mean that the rate hike cycle would start much sooner than anticipated, the bond market underwent a sharp re-adjustment. The market quickly went from pricing-in only 35 bps of rate hikes over the next 24 months to 116 bps, and Treasury returns fell precipitously as a result (Chart 8). The Fed has learned a few lessons about communications since then, and it will do its best to keep market expectations aligned with its own strategy. However, unless firmer guidance is provided about when tapering will begin, the risk of a hawkish surprise around the tapering announcement remains. Bottom Line: The Fed will only increase the pace or lengthen the maturity of its asset purchases if the economy or risk assets undergo a significant negative shock in 2021. Absent that, Fed communications in late-2021 will increasingly focus on the eventual tapering of asset purchases. Given the current vague guidance about when tapering will start, a scaled-down repeat of the 2013 Taper Tantrum is possible in late-2021 or 2022. Emergency Lending Facilities In addition to cutting rates to zero and massively scaling up the size of its balance sheet, the Fed also responded to the COVID recession by launching a slew of emergency lending facilities, some re-treads from the financial crisis and some brand new. Facilities to support the corporate bond market (The Primary and Secondary Market Corporate Credit Facilities) and the Municipal Liquidity Facility were particularly successful at capping bond spreads versus Treasuries, even if their actual usage was quite low. In fact, corporate bond spreads peaked on the very day that the Fed announced its corporate credit facilities in March (Chart 1). More recently, however, Treasury Secretary Steve Mnuchin refused to authorize the continuation of most of the Fed’s emergency lending facilities beyond the end of the year. We wrote in November that, even with the Treasury taking back the funds used to set up the facilities, the Fed could re-launch them in 2021 if incoming Treasury Secretary Janet Yellen provides her approval.12 However, a late addition to the recently passed fiscal stimulus package appears to prohibit the re-authorization of the facilities without Congressional approval. At the time of publishing, we have not been able to see the details of the new provision, so there remains some uncertainty about what the Fed can and cannot do in this regard. Credit spreads are no longer trading at distressed levels, primary issuance markets are functioning properly, and the Fed’s facilities have hardly been used at all. Nonetheless, while the new bill raises interesting questions about Fed independence in the long-run, we doubt that markets will respond negatively to the absence of the Fed’s emergency facilities in 2021. Credit spreads are no longer trading at distressed levels, primary issuance markets are functioning properly, and the Fed’s facilities have hardly been used at all (Table 3). Table 3Usage Of The 2020 Federal Reserve Emergency Lending Facilities

The Fed In 2021

The Fed In 2021

In short, we don’t see the Fed going out of its way to re-establish the facilities in 2021 because it will become clear that they are no longer needed. The Next Regime Shift In Fed Policy: Fiscal/Monetary Coordination The adoption of an Average Inflation Target represents a major regime shift in Federal Reserve policy. In the final section of this report, we expand our horizon beyond 2021 and speculate about what the next major regime shift for the Fed might be. The 2020 recession made two things crystal clear. First, traditional fiscal policy becomes essentially impotent once interest have been reduced to the zero-lower-bound. Once there, Fed policy is most impactful when it focuses on lending to the private sector. Lending to the private sector through an emergency lending facility is an act that blurs the distinction between monetary and fiscal policy. This was made abundantly clear by Congress’ recent push to legislate the Fed’s activities in this arena. Second, it is difficult for fiscal policy to act quickly enough during an economic downturn. While the CARES act was delivered in a timely manner, it has taken many months to pass a follow-up bill. The Fed’s independence allows it to act immediately when it is economically necessary, while Congress’ increasing polarization makes swift action a challenge. If we take these two observations to their logical conclusion, and throw in the strong chance that the traditional channels of monetary policy will be increasingly blocked in the future as rates bump up against zero, it seems to us that the strict separation of responsibilities between fiscal and monetary policymakers will fade over time. More specifically, greater time spent at the zero-lower-bound will incentivize the Fed to get more and more creative with its quasi-fiscal private lending facilities. Further, Congress will be more than happy to allow this encroachment as it finds itself unable to respond effectively in times of crisis. Of course, this will also lead to periodic push-back as some members of Congress fret about the Fed’s over-reach, but we expect this push-back will be the exception rather than the rule. Greater time spent at the zero-lower-bound will incentivize the Fed to get more and more creative with its quasi-fiscal private lending facilities. In fact, the best idea might be for fiscal and monetary policymakers to join together proactively to craft programs that can be deployed during the next recession. One example of such an idea was recently presented by Julia Coronado and Simon Potter.13 Coronado and Potter’s idea relies on the use of instant payment processing technology (which the Fed is already working on) to create digital accounts at the Federal Reserve for every household. Once those accounts are in place, the federal government could issue Recession Insurance Bonds, zero coupon bonds with some pre-determined face value, and grant one bond to every household in the country. Then, during the next economic downturn, the Fed could decide to do a “people’s QE” where it buys all the Recession Insurance Bonds leaving every household with a direct cash payment equal to the face value of the bond. This scheme directly addresses the two main problems we named earlier. It is fiscal policy, not monetary policy, so it can still be effective at the zero-lower-bound. Also, Congress can take its time to deliberate on the bill that authorizes the creation of the Recession Insurance Bonds, as this can be done proactively during a period of economic recovery. Then, the Fed can use its ability to move quickly during the next downturn to “activate” the bonds and deliver the fiscal stimulus that Congress actually passed years earlier. While likely not a story for 2021, we see increased cooperation between monetary and fiscal policymakers as the next big regime shift for the Fed. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy / Global Fixed Income Strategy Special Report, “A New Dawn For US Monetary Policy”, dated September 1, 2020, available at usbs.bcaresearch.com 2 https://www.federalreserve.gov/monetarypolicy/guide-to-changes-in-statement-on-longer-run-goals-monetary-policy-strategy.htm 3 https://www.federalreserve.gov/monetarypolicy/files/monetary20200916a1.pdf 4 https://www.federalreserve.gov/newsevents/speech/clarida20201116a.htm 5 For a more complete discussion of our 2021 inflation outlook please see “BCA Outlook 2021: A Brave New World”, dated November 30, 2020, available at bca.bcaresearch.com 6 Please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 7 This is the theory of adaptive expectations and we use it to model changes in the 10-year TIPS breakeven inflation rate. For further details please see US Bond Strategy Weekly Report, “How Are Inflation Expectations Adapting?”, dated February 11, 2020, available at usbs.bcaresearch.com 8 https://www.federalreserve.gov/econres/notes/feds-notes/tips-from-tips-update-and-discussions-20190521.htm 9 Fed Governor Lael Brainard references several of these trend measures in this recent speech: https://www.federalreserve.gov/newsevents/speech/brainard20201021a.htm&…; 10 More details on how this aggregate measure is constructed can be found here: https://www.federalreserve.gov/econres/notes/feds-notes/index-of-common-inflation-expectations-20200902.htm 11 For more details on how corporate credit performs during different yield curve environments please see US Bond Strategy Special Report, “2021 Key Views: US Fixed Income”, dated December 15, 2020, available at usbs.bcaresearch.com 12 Please see US Bond Strategy Weekly Report, “Preparing For A Dark Winter … But Do Markets Care?”, dated November 24, 2020, available at usbs.bcaresearch.com 13 https://www.piie.com/publications/policy-briefs/reviving-potency-monetary-policy-recession-insurance-bonds

Highlights The ongoing pandemic underscores the need for fiscal and monetary policymakers to continue to provide a reflationary “bridge” until vaccination ends the threat to the health care system. The pending deal being discussed between US congressional negotiators is not perfect, but it is likely to be a credible extension of the US fiscal bridge and it clarifies the path from the near-term growth outlook (which is negative), to the cyclical outlook (which is positive). The surprisingly strong euro area flash services PMI in December likely reflects the quick removal of restrictions that may soon need to be reimposed. European leaders will either need to provide additional fiscal support to their economies if the strain on the health care system does not soon relent, or economic activity will have to become increasingly dependent on external demand. China’s credit impulse has likely peaked, but economic activity will continue to accelerate in the first half of 2021 and will positively contribute to global growth. Our baseline view is that credit tightening in China will not lead to a meaningful drag on global growth in the second half of next year, but the history of policy “oversteering” in China means that the risks of a policy overkill cannot be ruled out. A likely extension of the reflationary bridge in the US coupled with strengthening Chinese demand has meaningfully reduced the odds of a deflationary outcome over the next year. Extreme technical conditions suggest that a moderate correction in stocks is possible in the first quarter, but the next significant episode of risk-off sentiment should be bought rather than sold. Investors should position in favor of risky assets over a 6-12 month horizon. Feature Our recently published 2021 Outlook report laid out the main macroeconomic themes that we see driving markets next year, as well as our cyclical investment recommendations. In this month’s report we briefly discuss the nearer-term outlook for growth through the lens of fiscal policy. Still Some Way To Go Chart I-1Slowing Economic Activity In Developed Economies

Slowing Economic Activity In Developed Economies

Slowing Economic Activity In Developed Economies

Over the very near term, growth will remain unavoidably linked to the dynamics of the COVID-19 pandemic. The second/third wave of infections that began in September has forced the re-imposition of restrictions in most European countries, as well as in some US states. High-frequency economic indicators clearly show that the European economy contracted in Q4 (Chart I-1), whereas in the US the slowdown has so far been less pronounced. The US economy continued to expand in the fourth quarter with the Atlanta Fed GDPNow model projecting 11% annualized growth, driven heavily by a sizeable change in private inventories (Chart I-2). Chart I-2US Q4 Growth Is Set To Be Large, But Driven Mostly By Inventories

January 2021

January 2021

The relationship between the pandemic and the economy has shifted since the spring. Back then, the rapid spread of the disease and the mostly unknown nature of the virus triggered a forceful response from policymakers. Widespread restrictions on movement and economic activity were imposed to stem the spread. However, those measures came at a high economic and social cost. With economic activity still running far below pre-pandemic levels and an increasingly weary and resistant public, policymakers have become highly reluctant to re-impose aggressive measures. As a driver of policy, the key consideration is the extent of pressure on medical systems. Chart I-3 highlights the situation in Europe. Daily ICU occupancy exploded in several European countries in October, which led to the new restrictions at the end of that month. In the US, COVID-19 hospitalizations are now nearly twice as high as they were in April and July, and for now many new state-level restrictions are not mandatory. But New York City’s mayor noted earlier this week that a “full shutdown” was likely following Christmas, highlighting that many parts of the US may be facing meaningfully tighter restrictions in the weeks ahead if the pace of new infections does not level off. Chart I-4 presents an estimate of the COVID-19 reproduction value (“R-naught”) in the US and in advanced economies outside the US, which highlights that it is too soon to confidently project a peak. Even outside the US, where restrictions have recently been tighter and progress has been made at reducing the number of intensive care patients, the reproduction number has crept back above one after some restrictions were loosened. Chart I-3Europe Reintroduced Lockdowns Because Of Pressure On The Medical System

Europe Reintroduced Lockdowns Because Of Pressure On The Medical System

Europe Reintroduced Lockdowns Because Of Pressure On The Medical System

Chart I-4Too Soon To Project A Peak In Cases

Too Soon To Project A Peak In Cases

Too Soon To Project A Peak In Cases

A Credible Extension Of The US Reflationary Bridge The ongoing pandemic underscores the need for fiscal and monetary policymakers to continue to provide a reflationary “bridge” until vaccination ends the threat to the health care system. Currently, health experts project that this is unlikely to occur before late spring or mid-year. Earlier this year, fiscal authorities around the world built a massive reflationary bridge to support household income while stay-at-home orders were in place. However, the effect of that stimulus has waned – at least for some income groups. In the US, Chart I-5 highlights that unemployment insurance payments have fallen by more than suggested by the decline in continuing jobless claims. Post-election surveys have suggested that a vast majority of Americans felt another economic assistance package was needed, with most reporting that it should occur before inauguration.1 Overall income remains higher than its pre-pandemic baseline (Chart I-6), but aggregate figures mask white collar/blue collar divergences. Many white-collar employees saw a substantial increase in their savings this year as their spending declined and income held up (due to their ability to work from home), whereas blue-collar and low-wage service workers found themselves dependent on government assistance. While the deployment of white-collar savings is likely to eventually support blue-collar and low-wage worker income, it is unlikely that this will occur while significant pandemic restrictions remain in place. Chart I-5The Stimulative Effect Of The CARES Act Has Waned

The Stimulative Effect Of The CARES Act Has Waned

The Stimulative Effect Of The CARES Act Has Waned

Chart I-6Overall Income Is ''Normal'', But This Masks Large Differences Across The Income Spectrum

Overall Income Is ''Normal'', But This Masks Large Differences Across The Income Spectrum

Overall Income Is ''Normal'', But This Masks Large Differences Across The Income Spectrum

That reality motivated the COVID relief deal that is reportedly under discussion between US congressional negotiators. The deal – as described in the financial media as we go to press – likely excludes state & local support, but it also likely includes a new round of stimulus checks, some funding for unemployment insurance recipients, and cash for small businesses, health-care providers, and schools. The deal, which we expect to be passed over the course of the next week, is not perfect but it is a credible extension of the US fiscal bridge and it clarifies the path from the near-term growth outlook (which is negative), to the cyclical outlook (which is positive). Chart I-7State & Local Government Support Is Needed In The New Year

State & Local Government Support Is Needed In The New Year

State & Local Government Support Is Needed In The New Year

The issue of state & local funding will be important to return to in the new year following Joe Biden’s inauguration. Persistent state & local government austerity following the global financial crisis acted as a significant drag on US economic growth (Chart I-7). Nonetheless, one-month delay to state & local government fiscal assistance is less problematic than a delay in extending unemployment insurance payments, given the pending expiry of the remaining CARES act unemployment programs on Dec. 26. Europe’s Bridge Is Shakier In Europe, the need for additional fiscal support is higher than in the US, given that activity contracted this quarter. While the December flash euro area services PMI showed surprising strength, this likely reflects the quick removal of restrictions that we noted may soon need to be reimposed. European economies responded very forcefully this year to the pandemic when all response measures are considered, but less so in many important economies when focusing only above-the-line measures – i.e., new spending and foregone government revenue – to the exclusion of equity injections, loans, and guarantees. Based on this metric, Chart I-8 shows that the UK and Germany have provided a response that is in line with the advanced economy average, whereas most other European countries have lagged. Chart I-9 highlights that this year’s economic rebound in Spain and Italy has been aided by Germany’s stronger fiscal response, as evidenced by intra-euro area trade balances. Chart I-8The Fiscal Response Of Many European Countries Has Lagged

January 2021

January 2021

Chart I-9Germany's Fiscal Stimulus Supported The Euro Area's Recovery

Germany's Fiscal Stimulus Supported The Euro Area's Recovery

Germany's Fiscal Stimulus Supported The Euro Area's Recovery

Funds from the European Recovery and Resilience Facility (“RRF”) have yet to be deployed and they will eventually act to support euro area economic activity. However, outlays from the fund next year are expected to be small. Given that this month’s ECB actions were aimed at simply maintaining easy financial conditions,2 European leaders will either need to provide additional fiscal support to their economies if the strain on the health care system does not soon relent, or economic activity will have to become increasingly dependent on external demand. China: Adding To Global Growth, For Now Chart I-10China Will Boost Euro Area Economic Activity Next Year

China Will Boost Euro Area Economic Activity Next Year

China Will Boost Euro Area Economic Activity Next Year

Fortunately for Europe (and advanced economies more generally), the external demand outlook is bright – for now. Euro area exports to China are strongly predicted by China’s credit impulse lagged by 9 months, and are set to rise materially (Chart I-10). China’s aggressive – and comparatively early – response to the pandemic will thus contribute meaningfully to global growth in the first half of 2021, and could obviate the need for further European fiscal stimulus if restrictions there are not reinstituted. China is likely to provide a significantly smaller boost to global growth in the second half of next year, as policymakers have already begun to mop up excess liquidity. Chart I-11 highlights that China’s credit impulse has consistently followed a 3½-year cycle since 2010, and this year has been no different. This cycle is not exogenous or mystical; it has been caused by the repeated “oversteering” of activity by Chinese policymakers who frequently oscillate between the need to fight deflation and the strong desire to curb additional private-sector leveraging. The chart suggests that an inflection point in this cycle’s upswing has been reached, which is consistent with the view of BCA’s China strategists that the credit cycle has peaked. A peak in China’s credit impulse does not mean that China’s contribution to global growth is about to slow. Global industrial production continued to accelerate following a peak in China’s credit impulse for at least six months in the lead-up to the last two global economic slowdowns (Chart I-12). But the chart also shows that a slowdown in global activity did occur following China’s impulse peak in both cases, especially when the impulse fell below its average of 28½% of GDP. Chart I-11China's Credit Cycle Has Peaked, Right On Schedule

China's Credit Cycle Has Peaked, Right On Schedule

China's Credit Cycle Has Peaked, Right On Schedule

Chart I-12DM Economies Continue To Grow Following A Peak In China's Credit Cycle

DM Economies Continue To Grow Following A Peak In China's Credit Cycle

DM Economies Continue To Grow Following A Peak In China's Credit Cycle

Our baseline view is that credit tightening in China will bring the impulse down to approximately 30% of GDP in 2021, which is still above its average of the past decade. This suggests that China will not contribute as much to global demand in the second half of the year, but will not be an actual drag. Still, the history of policy “oversteering” in China means that the risk of a policy overkill cannot be ruled out. Investors should closely watch for signs of increased hawkishness emanating from China’s National People’s Congress in March. Conclusions And Portfolio Recommendations Cyclically, as we highlighted in our 2021 Outlook, developed market (DM) economies are likely to experience above-trend growth, low inflation, and accommodative monetary policy next year. China’s economic cycle is running ahead of the DM world and Chinese growth will eventually moderate, but is still set to accelerate in the first half of the year. A likely extension of the reflationary bridge in the US coupled with strengthening Chinese demand meaningfully reduces the odds of a deflationary outcome over the next year, in the sense that consumers, businesses, and investors are much more likely to view any near-term lockdown-driven impacts on growth as necessarily temporary. This de-risks the path to a post-pandemic economy and increases our conviction in a cyclically-bullish stance towards risk assets. We continue to recommend that in 2021 global investors should: Favor stocks versus bonds; Maintain below-benchmark portfolio duration; Position for corporate bond spread tightening; Favor commodities; and Expect a continued decline in the US dollar. Chart I-13US Equities Are Vulnerable To A Moderate Correction

US Equities Are Vulnerable To A Moderate Correction

US Equities Are Vulnerable To A Moderate Correction

Over the very near-term, Chart I-13 shows that US equities are potentially vulnerable to a moderate tactical correction. US stocks are very richly valued, and investors may use signs of modest delays in the immunization campaign, a failure of the US Congress to provide support for state & local governments, or inadequate fiscal support in Europe as an excuse to sell. A moderate correction, on the order of 5-7%, is possible in the first quarter. The question for investors is whether the next significant episode of risk-off sentiment should be bought or sold. Given the ongoing impact of very easy monetary policy on equity multiples and the high likelihood of a significant earnings recovery, we are strongly inclined towards the former, barring any substantial shift in the timeline to mass vaccination. Equity returns will be lower in 2021 than in 2020, but are very likely to be positive and beat those offered by government securities. Jonathan LaBerge, CFA Vice President The Bank Credit Analyst December 18, 2020 Next Report: January 28, 2021 II. The Modern-Day Phillips Curve, Future Inflation, And What To Do About It Many investors feel that the Phillips Curve has failed to predict weak inflation over the past decade. But this perception is due to a singular focus on the economic slack component of the modern-day version of the curve to the exclusion of inflation expectations, and a failure to fully consider the lasting impact of sustained periods of a negative output gap on those expectations. In addition, many investors tend to downplay the long-term balance sheet impact of two episodes of excesses and savings/capital misallocations on the relationship between the stance of monetary policy and the output gap, via a persistently negative shock to aggregate demand and a reduced sensitivity of economic activity to interest rates. The COVID-19 pandemic was certainly a major economic shock. But for now, it seems like this was a sharp income statement recession, not a balance-sheet recession. This fact, along with lower odds of negative supply-side shocks and several structural factors, suggest that inflation will be higher over the next ten years than it has over the past decade. Investors looking to protect against potentially higher inflation should look primarily to commodities, cyclical stocks, and US farmland. Gold is likely to remain well supported over the coming few years, but rich valuation suggests the long-term outlook for the yellow metal is poor. A hybrid TIPS/currency portfolio has historically been strongly correlated with the price of gold, and may provide investors with long-term protection against inflation – at a better price. Introduction Chart II-1A Surge In Long-Dated Inflation Expectations

A Surge In Long-Dated Inflation Expectations

A Surge In Long-Dated Inflation Expectations