Policy

Highlights Every year we review our best and worst calls – both in terms of geopolitics and markets. This year our geopolitical forecasting and strategic market recommendations performed well, given the COVID-19 shock, but our tactical trades often went awry. We correctly forecast the presidency, Senate, Democratic nomination, and impeachment outcome. We anticipated “stimulus hiccups” but expected them to be resolved by November 3. The Georgia runoff on January 5 presents a 30% risk to our Senate prediction. In the main, we were right on Chinese politics, EU politics, US-Iran tensions, and Russian politics. US-China tensions kept rising, as expected, but the market ignored it. We missed the Saudi-Russia cartel break-up in Q1. The jury is still out on Brexit. Strategically, we got the big market moves right, but we were too risk-averse during the summer and after the election. Stay long cyber-security stocks in general, but close the pair trade versus Big Tech. Close the 10-year Treasury hedge. Feature Chart 1The Black Swan

The Black Swan

The Black Swan

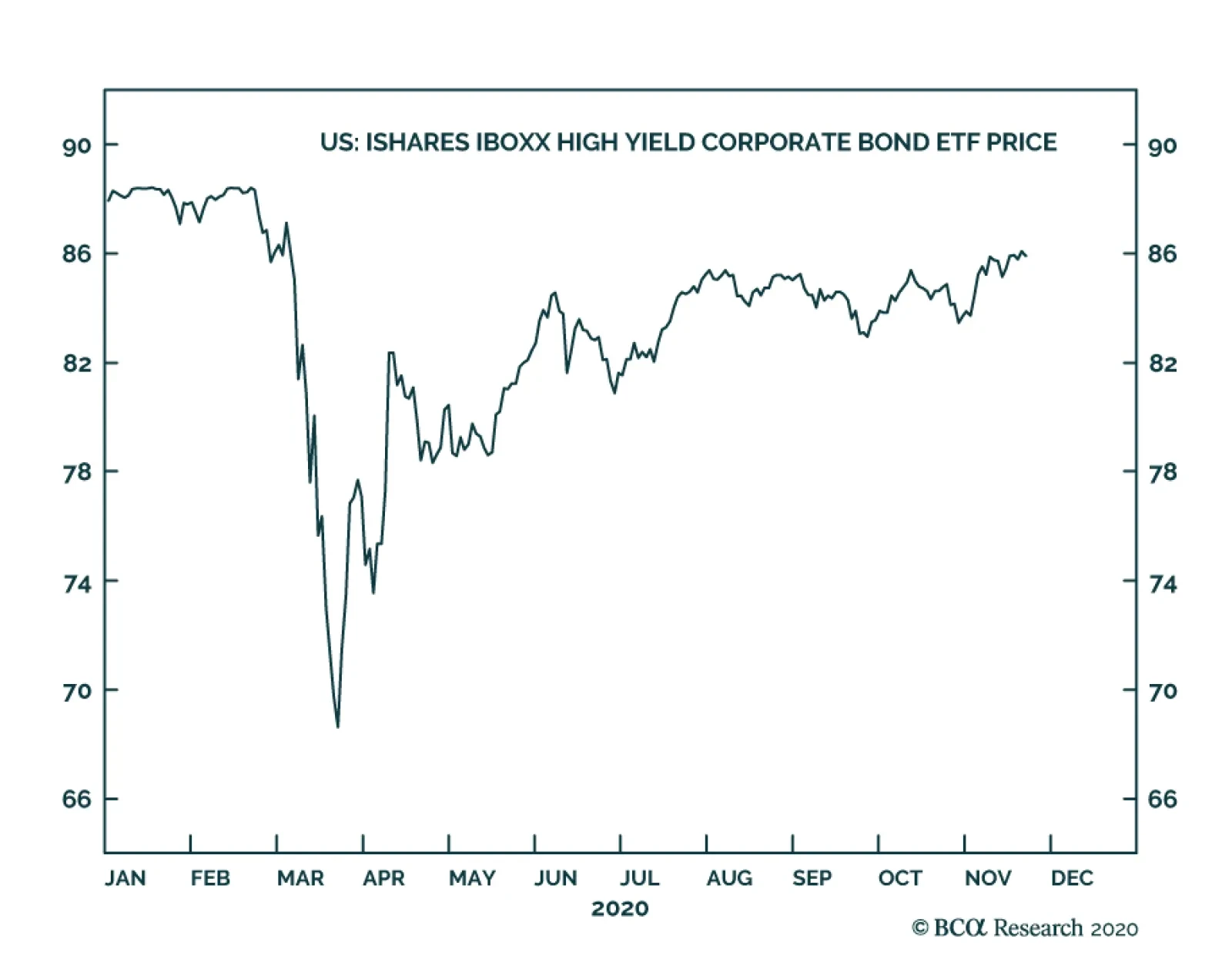

The COVID-19 pandemic took investors by surprise, defined the year 2020, and caused the shortest bear market in history, lasting 33 days (Chart 1). On the whole this year’s crisis illustrates how geopolitical analysis is not primarily concerned with “black swan” events, which are inherently unpredictable. Rather the wholly unexpected pandemic reinforced several of our pre-existing geopolitical themes and trends: de-globalization, American sociopolitical instability, European integration, and US-China conflict. This year our geopolitical forecasting and strategic market recommendations performed well, given the COVID-19 shock, but our tactical trades often went awry. Whether these and other trends will continue in 2021 will be the subject of our strategic outlook due next week. This week we offer our annual report card, which reviews our best and worst calls for the year with a desire to hold ourselves accountable to clients, learn investment lessons from mistakes, and hone our geopolitical method of analysis. Successful Strategy, Debatable Tactics Overall our performance this year was good. Specifically, our political forecasting was on target and our investment recommendations got the big moves correct. But our risk-averse tactical trades were less successful. In last year’s annual outlook, “2020 Key Views: The Anarchic Society,” our main investment recommendation was long gold – based on sky-high geopolitical risk and a shift toward reflationary policy by the Federal Reserve, China, and the European Union (Chart 2). We maintain this trade today, despite its losing some altitude recently, as we expect to see low real rates, reflationary global policy, and rising inflation expectations. Geopolitical risk will also remain elevated despite dropping off from recent peaks, and not only during President Trump’s “lame duck” final days in office. We sounded the alarm for clients in our January 24 report, “Market Hurdles: From Sanders To Iran,” warning that global equities and risk appetite would suffer “in the very near term” due to conventional political risks as well as the new coronavirus, which we feared would explode as a result of Chinese New Year. In retrospect we were not bearish enough even in these reports. In our March 27 report, “No Depression,” we advised that the extraordinary monetary and fiscal response to the crisis would reflate the global economy and thus went long Brent crude oil. From this point onward we gradually added risk to our strategic portfolio, including by going long global equities relative to bonds in June (Chart 3). Chart 2Gold Paid Off When Black Swan Arose

Gold Paid Off When Black Swan Arose

Gold Paid Off When Black Swan Arose

Of course, despite getting these big moves right, we abandoned several of our strategic recommendations during the crisis and some of our tactical trades went awry throughout the year. Chart 3When Crisis Hits, Buy Risk Assets!

When Crisis Hits, Buy Risk Assets!

When Crisis Hits, Buy Risk Assets!

Our Worst Calls Of 2020 We chose a very bad time, last December, to bet heavily on global equity rotation from growth to value and away from tech sector leadership. US equities and tech stocks surged ahead of global equities on the back of the pandemic. Our long energy / short tech trade proved disastrous. Only now, with a vaccine on the horizon, are these recommendations coming to fruition. On the other hand, we should have remained committed to our long EUR-USD position rather than cutting it short when the crisis erupted (Chart 4). Global stimulus and the Fed’s sharp reduction in interest rates and gigantic infusion of US dollar liquidity ensured that the dollar would plummet. Strategically, we got the big market moves right, but we were too risk-averse during the summer and after the election. In some cases our geopolitical forecast proved dead-on while our market recommendation faltered. One of biggest geopolitical forecasts, in September 2019, was that the US and China could well conclude a trade deal but that it would be extremely limited in scope and strategic tensions would continue to rise dangerously. This prediction has proved accurate, judging by US high-tech export controls and China’s suppression of Hong Kong this year. But we misjudged the market response, particularly after China contained the virus: the renminbi saw a tremendous rally this year while we remained short, suffering a 4.96% loss so far (Chart 5). Chart 4Stick With Your Guns...Even Amidst Crisis

Stick With Your Guns...Even Amidst Crisis

Stick With Your Guns...Even Amidst Crisis

Chart 5US-China Tensions Persisted, But The Market Didn't Care

US-China Tensions Persisted, But The Market Didn't Care

US-China Tensions Persisted, But The Market Didn't Care

Along these lines, President-elect Joe Biden’s statement that he will maintain President Trump’s tariffs is another confirmation of one of our most contrarian views over the past year.1 We would expect the People’s Bank to allow the yuan to slip both to deal with lingering deflationary pressures and to build up some poker chips for the coming negotiations with Biden. We also would expect the US dollar to witness a near-term tactical bounce. However, if we are wrong, our short CNY-USD trade will fall further and we will have to cut our losses. Chart 6You Can't Time The Market

You Can't Time The Market

You Can't Time The Market

Other mistakes occurred when solid economic and political views combined with bad market timing. Our long position in cyber-security stocks is well grounded – we remain invested – but once again we jumped the gun on the rotation away from Big Tech, which constituted the short end of two of our pair trades, now closed. Separately, we coupled our long gold bet with a long silver bet that came far too late into the rally – though we remain strategically optimistic on silver due to its industrial uses, which should revive in the post-pandemic context. Lamentably, we ran up against our stop-loss threshold on our structural position in US aerospace and defense stocks not long before the vaccine announcement would have begun the arduous process of recuperating losses (Chart 6). We have reinitiated the latter trade, albeit in global defense stocks rather than just American. The inverse also occurred, in which our political forecasting proved faulty but our market implications worked out quite well. One of our biggest political forecasting failures stemmed from an initial success. Beginning in May, we signaled that the US Congress would experience “stimulus hiccups” in trying to pass additional fiscal relief for the economy. This view proved prescient as negotiations fell through in July and a range of benefits expired. Real rates began to recuperate at this time. The problem is that we also predicted that the fiscal impasse was merely a hiccup, i.e. would be resolved prior to the election. It remains unresolved to this day. Fortunately, our market recommendation – to go long US municipal bonds relative to duration-matched treasuries – was rooted in the principle of “buy what the Fed is buying” and therefore continued to appreciate, along with our similarly justified position in investment grade bonds (Chart 7). Chart 7Stimulus Hiccup Occurred, But Was Not Resolved

Stimulus Hiccup Occurred, But Was Not Resolved

Stimulus Hiccup Occurred, But Was Not Resolved

Our biggest error of political forecasting was the collapse of OPEC 2.0 at the beginning of the year. We signaled to clients in January that Russia was growing internally unstable and that this would result in an external action that would prove market-negative. This was correct, but we failed to anticipate that the most important consequence would be a temporary Russian rejection of Saudi demands for oil production cuts. Still, we advised clients to stay the course, arguing that the Russians and Saudis were geopolitically constrained and would return to their cartel, which proved to be the case, thus hastening the restoration of balance to oil markets. This view supported our long spot oil recommendation in late March, though the idea that US producers might collaborate proved fanciful. Alternatively we suggested that clients go long oil relative to gold, which has performed well. Other mistakes stemmed from our tactical trades. Generally, we were insufficiently bullish both during the summer and after the US election. In both cases we overemphasized the absence of US fiscal stimulus as a risk to the rally. In reality the first stimulus was sufficient and the V-shaped recovery of the private economy reduced the need for additional support over the course of the year. Our long tactical positions in US treasuries, consumer staples, and JPY-EUR did not pan out. The takeaway going forward, given that the market is not pressuring politicians to act, is that the risk of another congressional fiscal failure prior to Christmas is underrated. Lastly, some minor emerging market trades went awry, such as our long positions in Thai and Malay equities and our shorting the South African rand. We wrongly predicted that Michelle Obama would be Joe Biden’s pick for vice president, when in fact that honor went to Senator Kamala Harris. Our Best Calls Of 2020 While we got the big market moves right in 2020, our best calls were political and geopolitical in nature: Joe Biden won the US election. He won through his ability to win back blue-collar workers and compete in the Sun Belt as well as the Rust Belt, which we outlined as a key geographic strength during his run in the Democratic primary election (Map 1). We downgraded Trump from 55% odds of re-election to 35% in March, when the lockdowns occurred, and we upgraded Trump only to 45% in October when he rallied. The thin margins in the swing states confirmed this higher-than-consensus probability of a Trump win. Map 1Joe Biden Won The Rust Belt And The Sun Belt

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Republicans retained the Senate. Beginning in late September, we saw that President Trump was rallying and that this would increase the odds of a Republican Senate even if Trump himself fell short. On October 16 we signaled that the Senate was too close to call, and on October 30 we upgraded the GOP again and argued that a Democratic White House plus a Republican Senate was the most likely scenario (Chart 8). There is a lingering risk to this view: a double Democratic victory in the Georgia runoffs on January 5, 2021. But we put the odds of that at 30% at best. Chart 8Republicans Held The Senate (Pending Georgia Runoffs)

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Chart 9Biden Won The Democratic Primary Nomination

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Biden won the Democratic nomination, which we first highlighted in November 2018 and June 2019 and consistently thereafter, though we never underrated his challengers (Chart 9). Trump was acquitted of impeachment charges, which seems like ages ago. We said from the start that Democrats did not have the votes (Chart 10). China stimulated the economy massively and avoided massive domestic unrest. Investors doubted that Beijing would stimulate enough to lead to a global recovery, given the leadership’s preference to avoid systemic financial risk. We insisted that constraints would prevail over preferences and the stimulus would be gigantic. Our “China Play Index” skyrocketed, though it did not outperform global equities (Chart 11). We also argued that President Xi Jinping would not face significant domestic unrest after the crisis erupted, though we view domestic political risk as underrated for the coming years. Chart 10Impeachment Failed

Geopolitical Report Card: 2020

Geopolitical Report Card: 2020

Long Emerging markets and deep cyclicals recovered. The combination of Chinese stimulus and a US “return to normalcy” led us to go long emerging markets after the election. We articulated this trade by going long Trans-Pacific Partnership countries, on the expectation that Washington will remain hawkish toward China over trade (Chart 12). We also went long deep cyclicals and US infrastructure plays on the basis of Chinese stimulus and the Biden-Trump common denominator on building projects (Chart 13). Chart 11China Stimulated Massively

China Stimulated Massively

China Stimulated Massively

Chart 12Long Trans-Pacific Partnership Worked As EM Play

Long Trans-Pacific Partnership Worked As EM Play

Long Trans-Pacific Partnership Worked As EM Play

The Taiwan Strait was a bigger geopolitical risk than the Korean peninsula, which markets are at last recognizing (Chart 14). Unfortunately for investors Taiwan remains a serious geopolitical risk regardless of Trump’s exit. Hong Kong attracted investors’ attention more than Taiwan in 2020, whereas we have treated Hong Kong as a red herring. Chart 13Long Infrastructure And Cyclicals Paid Off

Long Infrastructure And Cyclicals Paid Off

Long Infrastructure And Cyclicals Paid Off

Chart 14Hong Kong Was A Red Herring, Korea Beat Taiwan

Hong Kong Was A Red Herring, Korea Beat Taiwan

Hong Kong Was A Red Herring, Korea Beat Taiwan

Brexit has been a red herring throughout 2020, as expected, though an end-of-year failure to agree to a UK-EU trade deal would upend our predictions (Chart 15). Chart 15Brexit Was A Sideshow

Brexit Was A Sideshow

Brexit Was A Sideshow

Germany’s shift to more dovish fiscal policy strengthened European solidarity, keeping peripheral bond yields and “break-up risk” contained (Chart 16). In August 2019 we argued that Germany was easing fiscal policy but would not surge spending until a crisis happened – which proved to be the case when the coronavirus prompted Olaf Scholz to wheel out the “bazooka” this year. We also argued that Europe would be willing to mutualize debt, which was officially confirmed when outgoing Chancellor Angela Merkel forged an agreement on an EU Recovery Fund with French President Emmanuel Macron (though not exactly a “Hamiltonian moment”). Chart 16European Solidarity Strengthened

European Solidarity Strengthened

European Solidarity Strengthened

Chart 17Peak Shinzo Abe' Theme Boosted The Yen

Peak Shinzo Abe' Theme Boosted The Yen

Peak Shinzo Abe' Theme Boosted The Yen

Japan saw “Peak Abenomics,” which was confirmed this year when he handed the helm over to his deputy, Yoshihide Suga, whose policies are continuous. Abe’s late-2019 tax hike was only one of many reasons we anticipated a rally in the yen, which was supercharged by this year’s crisis (Chart 17). Russia’s political risk premium spiked, as we expected, though we did not anticipate that the cause would be a temporary breakdown in OPEC 2.0 (Chart 18). We were more prepared for an event like the poisoning of Alexei Navalny and US sanctions against the Nordstream II pipeline. Our argument that Russia would lie low, for fear of domestic unrest, has so far borne out in the Belarus protests and the conflict in Nagorno-Karabakh. Whether it will continue to do so in the face of what will likely be a pro-democracy assault in eastern Europe from the US Democratic Party remains to be seen. Chart 18Russian Geopolitical Risk Spiked As Predicted

Russian Geopolitical Risk Spiked As Predicted

Russian Geopolitical Risk Spiked As Predicted

India-China tensions were a red herring. India benefited from the western world’s turn against China. Partnerships and alliances were already taking shape before the coronavirus spurred a move in the West to diminish reliance on China’s health care exports. Our long Indian pharmaceuticals trade was highly profitable, though our overweight in Indian bonds was less so (Chart 19). Chart 19India Benefited From West's Anti-China Turn

India Benefited From West's Anti-China Turn

India Benefited From West's Anti-China Turn

Brazilian political risk surged to the highest levels since the 2018 election, and President Jair Bolsonaro suffered a setback in municipal elections, as we expected, especially after witnessing his cavalier attitude toward the pandemic (Chart 20). However, his approval rating rose on the back of fiscal largesse, implying that debt dynamics will continue to trouble this market despite the bullish backdrop for emerging markets in 2021. Chart 20Brazil Remained A Muddle

Brazil Remained A Muddle

Brazil Remained A Muddle

Chart 21Turkish Populism Exacted A Toll

Turkish Populism Exacted A Toll

Turkish Populism Exacted A Toll

Chart 22A Bull Market In Iran Tensions

Bull Market In US-Iran Tensions

Bull Market In US-Iran Tensions

The Turkish lira collapsed, as Turkish President Recep Erdogan maintained reckless domestic economic policies and foreign adventurism (Chart 21). As we go to press, Erdogan appears to be backing down from his aggressive approach to maritime-territorial disputes in the Mediterranean, for fear of European sanctions, which would be a positive surprise, albeit temporary. The “bull market in Iran tensions” continued, with US-Israeli sabotage and assassinations of key Iranian figures bookending the year (Chart 22). With Trump still in office for another 45 days, we would not be surprised to see another move on Iran, where hardliners are ascendant in the unstable advance of the Supreme Leader Ali Khamenei’s eventual succession. So far, Trump has taken market-negative actions in his “lame duck” period on Iran, China, and Big Tech, as we argued, which means more is coming despite the market’s enthusiasm over the partly sunny outlook for 2021. Investment Takeaways Geopolitical analysis is about structural themes and trends – not unpredictable black swans, which may even further entrench structural trends. When a crisis triggers a massive selloff, buy risk assets, then reassess. The gargantuan, coordinated monetary and fiscal response to this year’s crisis presented a clear buy signal. Once the virus was revealed not to be as deadly as first suspected, the rally gained steam. Political and geopolitical forecasts may be dead-on and yet fail to drive the market. There is a constant need to refine the ability to articulate and implement trades that seek to generate alpha from policy insight. Tactical views and attempts at cleverness are a liability when one’s strategic views – geopolitical, macro-economic, financial – are firmly grounded. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Thomas L. Friedman, "Biden Made Sure ‘Trump Is Not Going To Be President For Four More Years,’" New York Times, December 2, 2020, nytimes.com.

The strength in China’s post-pandemic policy support likely peaked in October. Interbank rates have normalized to their pre-pandemic levels and bond yields have risen sharply since May. The renewed emphasis on financial de-risking is evident in China’s recent anti-trust regulations against domestic leading online retail and lending providers, rising corporate bond defaults and readouts from recent PBoC meetings. In the near term, US President-elect Joe Biden will focus on reviving the economy and this may restore some balance to the Sino-US trade relationship. Additionally, China’s economic recovery is on track. The odds are rising that next year the Chinese leadership will accelerate structural reforms and the de-risking campaign, which began in 2017 but was delayed due to the US-China trade war and the COVID pandemic. These policy actions will improve China’s productivity growth and industrial competitiveness in the medium to long term, but they will create short-term headwinds to the economic recovery and the stock market’s performance. The uptrend in China’s business cycle will likely be maintained for another two quarters, propelled by the momentum from this year's massive stimulus. Historically, turning points in China’s business activities lag credit cycles by six to nine months. Given that China’s policy support apexed in Q4 this year, a peak in the country’s business cycle will probably be reached by mid-2021. Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Below is a set of market relevant charts along with our observations: Monetary policy has tightened, but fiscal spending by local governments should pick up in the next two quarters to support the ongoing business cycle expansion into H1 2021. Fiscal spending has been constrained due to shortfalls in revenues this year, despite record sales of special-purpose bonds.1 Government expenditures will gain strength as local governments’ tax revenues start to improve and the proceeds from bond sales are distributed. Chart 1Credit Impulse Has Peaked...

Credit Impulse Has Peaked...

Credit Impulse Has Peaked...

Chart 3Business Cycle Expansion To Continue In 1H21

Business Cycle Expansion To Continue In 1H21

Business Cycle Expansion To Continue In 1H21

Chart 2...But Fiscal Spending Should Pick Up

...But Fiscal Spending Should Pick Up

...But Fiscal Spending Should Pick Up

Part of the buildup in this year’s industrial inventory is due to the solid recovery in domestic demand and proactive restocking by manufacturers. However, the pace of inventory pileup this year has been the highest since 2014, while infrastructure investment and industrial output growth have barely recovered to pre-pandemic levels. The rapid expansion in industrial inventory may be the result of cheap credit and commodity prices and could lead to a period of destocking and slower imports of raw materials in Q1 2021. Chart 4Industrial Inventory Has Run Ahead Of Economic Recovery...

Industrial Inventory Has Run Ahead Of Economic Recovery...

Industrial Inventory Has Run Ahead Of Economic Recovery...

Chart 5...Propelled By Solid Recovery And Cheap Credit

...Propelled By Solid Recovery And Cheap Credit

...Propelled By Solid Recovery And Cheap Credit

Core CPI has reached its weakest level in more than a decade, while the PPI remains in negative territory. A delayed recovery in the household consumption and services sector has been disinflationary to core CPI along with the PPI’s consumer goods price subcomponent.2 Historically, when the growth rate in the PPI outpaces that in the CPI, industrial output and profits tend to improve even if the PPI is in contraction. However, a deflationary PPI is the result of depressed demand for both industrial products and household goods. Hence, neither the widening gap between the PPI and CPI nor the improvement in industrial profits can be sustained on the back of falling consumer prices. Credit impulse tends to lead an increase in both the PPI and CPI by six to nine months. Improving service sector activities and rebounding energy and commodity prices will also be reflationary to both the CPI and the PPI. Meanwhile, the peaking credit impulse coupled with tighter domestic monetary policy and a rapidly rising RMB will limit the upside in both the consumer and producer price indexes. Chart 6Rising Deflation Risks

Rising Deflation Risks

Rising Deflation Risks

Chart 7PPI Has Been Dragged Down By Its Consumer Goods Price Component

PPI Has Been Dragged Down By Its Consumer Goods Price Component

PPI Has Been Dragged Down By Its Consumer Goods Price Component

Chart 8Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Improvement In Industrial Profits Is Unsustainable In A Deflationary Environment

Chart 9While The Economic Recovery Should Support Prices...

While The Economic Recovery Should Support Prices...

While The Economic Recovery Should Support Prices...

Chart 10...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

...A Rapidly Rising RMB Will Limit The Upside In Producer Prices Next Year

Retail sales growth further strengthened in October. However, despite a sharp rebound in auto sales, other consumption segments, such as catering, tourism and consumer durable goods, remain sluggish. Household disposable income and employment have improved from troughs earlier this year, but both continue to lag behind the recovery in the industrial sector. The sluggish household sector has prompted Chinese leaders to take actions. In a State Council executive meeting on November 18, Primer Li Keqiang pledged to promote the consumption of home appliances, catering, and automobiles.3 Stocks of consumer goods and automakers rallied following the pro-consumption stimulus announcement. We continue to favor consumer discretionary stocks in both onshore and offshore markets. Even though the valuations in both sectors are elevated compared with the broad market, their earnings outlook also shows a notable improvement. In the next 6 months, targeted pro-consumption stimulus policies should further boost investors’ sentiment as well as profits in these sectors. Chart 11The Ex-Auto Retail Sales Remain Sluggish

The Ex-Auto Retail Sales Remain Sluggish

The Ex-Auto Retail Sales Remain Sluggish

Chart 12Improving Household Income And Employment Will Support Consumption

Improving Household Income And Employment Will Support Consumption

Improving Household Income And Employment Will Support Consumption

Chart 13Policy Support Will Continue Boosting Auto Sales...

Policy Support Will Continue Boosting Auto Sales...

Policy Support Will Continue Boosting Auto Sales...

Chart 14...And Promote NEV Sales

...And Promote NEV Sales

...And Promote NEV Sales

Chart 15Auto Sector's Outperformance Should Continue

Auto Sector's Outperformance Should Continue

Auto Sector's Outperformance Should Continue

Chart 16Consumer Discretionary Sector Will Also Benefit From More Policy Support

Consumer Discretionary Sector Will Also Benefit From More Policy Support

Consumer Discretionary Sector Will Also Benefit From More Policy Support

Chart 17Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

Housing Demand In Second- And Third-Tier Cities Has Already Rolled Over

In the past four weeks, the high-frequency data show that momentum in housing demand in second- and third-tier cities has quickly abated. Moreover, bank lending to property developers has rolled over, reflecting tighter financing regulations and pressure to deleverage in the property sector. Growth has flattened in medium- and long-term consumer loans while the propensity for home purchase has ticked up slightly. This divergence may be a sign that demand for real estate has not softened, but that home buyers are waiting for more discounts from property developers. As such, the rebound in floor space started in October should be short-lived as property developers’ profit margins continue to narrow and their financing remains constrained. We expect aggregate home sales growth to decelerate slightly in 1H21 from the past six months. However, real estate developers need to complete their existing projects, which will support construction activities into H1 next year. Chart 18Home Buyers May Be Expecting More Home Price Discounts Ahead

Home Buyers May Be Expecting More Home Price Discounts Ahead

Home Buyers May Be Expecting More Home Price Discounts Ahead

Chart 19Financing Constrains Will Limit Investments In New Building Projects

Financing Constrains Will Limit Investments In New Building Projects

Financing Constrains Will Limit Investments In New Building Projects

This year’s strong outperformance in China’s offshore equity prices has been driven by the TMT sector’s stocks (Information Technology, Media & Entertainment, and Internet & Direct Marketing Retail). Since October, however, Chinese stocks excluding the TMT sector have also started to outperform the global benchmarks. Moreover, domestic cyclicals, which do not feature some of China’s leading tech companies such as Alibaba and Tencent, have outpaced onshore defensive stocks. These developments indicate that as the upswing in China’s business cycle continues to strengthen, the outperformance in China’s ex-TMT stocks will likely be sustained into early 2021. Within cyclical sectors, we continue to favor the materials and consumer discretionary sectors aimed at policy dividends and a rebound in commodity prices. Chart 20China's Ex-TMT Stocks Starting To Outperform Global

China's Ex-TMT Stocks Starting To Outperform Global

China's Ex-TMT Stocks Starting To Outperform Global

Chart 21Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Domestic Cyclicals Are Now Breaking Out Relative To Defensives

Chart 22Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Accelerating Economic Recovery Will Continue To Support Chinese Cyclical Stocks

Chart 23Rebounding Commodity Prices Will Bode Well For Material Stocks

Rebounding Commodity Prices Will Bode Well For Material Stocks

Rebounding Commodity Prices Will Bode Well For Material Stocks

Recent bond payment defaults by several SOEs have led to a spike in onshore corporate bond yields. Nonetheless, the ripple effect on China’s financial markets has been limited outside of the corporate bond market; onshore stocks were little changed by news of the defaults. Moreover, the PBoC’s recent liquidity injections helped to stabilize the interbank rate. Historically, corporate bond defaults and rising bond yields have not had an imminent negative impact on China’s domestic stock market performance; none of the defaults in 2015, 2016 or 2019 led to selloffs in the equity market. However, during a business cycle upswing and following a large-scale stimulus, increasing corporate defaults typically mark the onset of tightening in financial regulations and the monetary cycle. We expect the upswing in the business cycle to begin losing momentum as the tightening policy cycle gains further traction in 2021. Prices in the forward-looking equity market will likely peak sooner on the expectation that the rate of economic and corporate earnings growth will slow in 2H21. Chart 24Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Chart 25Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Stress In Chinese Onshore Corporate Bond Market

Chart 26But So Far Negative Impacts On The Stock Market Are Limited

But So Far Negative Impacts On The Stock Market Are Limited

But So Far Negative Impacts On The Stock Market Are Limited

Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Footnotes 1Please see China Investment Strategy Weekly Report "China Macro And Market Review," dated October 7, 2020, available at cis.bcaresearch.com 2Headline PPI is comprised of producer and consumer goods. The weights of producer and consumer goods are roughly 75% and 25%, respectively. As for producer goods by industry, the weight of the manufacturing sector is around 50%, followed by 20% for the raw material sector; the mining sector accounts for only around 5%. 3Pro-auto consumption plans include: providing subsidies to encourage urban car owners to replace older and higher-emission models with newer environmentally friendly ones; encouraging automobile sales and upgrades in rural areas; and promoting New Energy Vehicle (NEV) sales. The plan will also loosen some existing restrictions on auto sales and increase the permits for vehicle license plates. Cyclical Investment Stance Equity Sector Recommendations

Highlights Inflation Breakeven Trades: We are taking profits on our recommended inflation breakeven widening trades in Italy and Canada, as breakevens in both countries are no longer below the fair values implied by our models. We are initiating a new trade this week, going long French 10-year inflation-linked bonds versus French nominal OATs, as French breakevens remain below fair value. Yield Curve Butterfly Trades: We are closing three of our four outstanding government bond yield curve trade recommendations, taking profits in France and Italy and realizing a loss in the UK. We are maintaining our US 5/7/10 butterfly trade, which is the cheapest way to position for an expected steepening of the Treasury curve based on our valuation models. Cross-Country Spread Trades: We are cutting our losses in our New Zealand-UK government bond spread trade, with the odds of the RBNZ shifting to a negative interest rate policy severely curtailed by political pressure over surging New Zealand house prices. We are maintaining our US-Germany spread widening trade, as the spread is too narrow based on our fair value model and we see more scope for US Treasury yields to drift higher in the coming months. Feature Dear Client, Next week, we will be jointly publishing our semi-annual Central Bank Monitor Chartbook along with our colleagues at BCA Research Foreign Exchange Strategy. You will receive that report a few days later than usual on Friday, December 11. We will return to our regular publishing schedule on Tuesday, December 15 with our 2021 Key Views report outlining our main investment themes and ideas for the upcoming year. Best Regards, Rob Robis As we enter the final weeks of an incredibly eventful and (unfortunately) all too memorable 2020, our attention now turns to investment ideas for the coming New Year. This week, all BCA Research clients will receive the 2021 Outlook report, detailing the key themes and recommendations from all our strategists. We will follow that up with our own 2021 Global Fixed Income Strategy outlook report later this month. The waning days of the year also offer a good time to review our more short-term trade recommendations currently in our Tactical Overlay portfolio. In addition, the waning days of the year also offer a good time to review our more short-term trade recommendations currently in our Tactical Overlay portfolio (Table 1). Several of our suggested trades have generated a solid profit (like inflation breakeven wideners) but have now outlived their original rationale. Others, like some of our yield curve trades in Europe, have not gone as we expected and should therefore be closed out. Table 1Changes To Our Tactical Overlay Portfolio

A Year-End Review Of Our Tactical Overlay Trades

A Year-End Review Of Our Tactical Overlay Trades

As a reminder to our regular readers, our Tactical Overlay is a portfolio of individual trade ideas within the global fixed income space with an investment horizon of six months or less. These differ from our more typical strategic (6-12 month) recommendations that also populate our model bond portfolio. Ideas for our Tactical Overlay trades often stem from our fair value models, but can also be plays on events that we expect will be market relevant on a near-term basis, like central bank meetings. All recommended trades are implemented using specific securities, rather than generic Bloomberg tickers or bond indices. This allows for a more transparent process where clients can follow along with the performance of our trades. Evaluating Our Tactical Inflation-Linked Breakeven Trades We currently have two open tactical trade recommendations involving inflation-linked bonds: Long 10-year Italian inflation-linked bonds vs short 10-year Italian bond futures Long 10-year Canadian inflation-linked bonds vs short 10-year Canadian bond futures We initiated both of these trades back in June of this year, as well as an additional trade involving US TIPS, based on the output of our inflation breakeven fair value framework. In our models, we regress 10-year inflation breakevens on the annual rate of change of oil prices in local currency terms and a multi-year moving average of realized headline inflation.1 At the time of our mid-year report, inflation breakevens were too low on our models in the majority of developed market countries with inflation-linked bonds – a lingering after-effect of the COVID-19 shock to global growth in the second quarter of 2020 (Chart 1). Since then, 10-year inflation breakevens have caught up to fair value in the US, Germany, Italy and Canada, and have even moved above fair value in the UK and Australia. Chart 1A Big Shift In Inflation Breakeven Valuations

A Year-End Review Of Our Tactical Overlay Trades

A Year-End Review Of Our Tactical Overlay Trades

In June, we also entered into a US 10-year TIPS breakeven widening trade, but we took profits on the trade once US breakevens returned back to our model fair value estimate in September. We now see a similar situation in Canada (Chart 2) and Italy (Chart 3) where breakevens have converged to our model-implied fair value. Chart 2Canadian 10-Year Inflation Breakeven Model

Canadian 10-Year Inflation Breakeven Model

Canadian 10-Year Inflation Breakeven Model

A move above fair value is possible, but could be harder to achieve with the Canadian dollar and euro steadily trending higher which could weigh on the market’s view on future inflation in Canada and Italy. We are taking profits on our Canada and Italy 10-year breakeven trades, realizing profits of 4.7% and 5.6% respectively. Thus, we are taking profits on our Canada and Italy 10-year breakeven trades, realizing profits of 4.7% and 5.6% respectively. The Italian returns were boosted considerably by the long side of this trade, as we entered the position when the 10-year real yield was +1.05% and which has since collapsed to -0.05% on the back of the massive rally in Italian bonds. One place where breakevens still look attractively cheap, trading close to one standard deviation below our model fair value, is in France (Chart 4). This contrasts with the breakevens in Italy and Germany that have fully converged to fair value. Thus, we are entering a new trade this week, going long the on-the-run 10yr French inflation-linked bond (OATi) and shorting French bond futures (Euro-OATs). The hedge ratio used for this trade to keep both legs duration matched, given the much shorter duration of the OATi relative to nominal French bonds, is 0.49 (see the Tactical Overlay table on page 17 for specific details on the securities used in the trade). Chart 3Italian 10-Year Inflation Breakeven Model

Italian 10-Year Inflation Breakeven Model

Italian 10-Year Inflation Breakeven Model

Chart 4French 10-Year Inflation Breakeven Model

French 10-Year Inflation Breakeven Model

French 10-Year Inflation Breakeven Model

Bottom Line: We are taking profits on our recommended inflation breakeven widening trades in Italy and Canada, while initiating a new breakeven widening position in France, based on the output of our breakeven fair value models. Evaluating Our Yield Curve/Butterfly Spread Trades Back in July, we initiated a series of yield curve butterfly spread trades in the US, UK, Italy and France.2 Butterfly spreads compare the yield of a single bond (bullets) to that of a duration-neutral combination of bonds with shorter and longer maturities relative to the bullet (barbells). Our valuation models produce fair value estimates of various butterfly combinations based on the relation of the butterfly spreads to the slope of the yield curve. We then combine those valuations with our own macro views on the future slope of yield curves to come up with potential value-based curve trades.3 We now evaluate our four existing curve trades in turn. Long UK 3/20 Barbell vs. 10-Year Bullet Our original rationale for entering this trade was two-fold. Firstly, this position was the most attractive butterfly combination in terms of the standardized deviation of the spread from its model-implied fair value. Secondly, there was a relatively low correlation between nominal UK bond yields and inflation breakevens--meaning that we could see a rise in long-dated inflation expectations that did not also push up nominal bond yields by a proportional amount. This made the trade consistent with our overall macro view back in July that the Gilt curve would flatten (the same rationale applies to the other two long barbell versus short bullet trades, or “flatteners”, in France and Italy that we discuss below). Unfortunately, our rationale did not play out as expected (Chart 5). Instead of reverting to fair value, the butterfly spread was mostly flat while the bullet grew more expensive relative to the barbell, driven by a rise in the model fair value. This in turn was due to significant steepening in the underlying 3/20 curve, contrary to our expectations. We also saw a significant overall upward shift in the overall UK Gilt curve, which generated losses on our long barbell position (which has a higher interest rate convexity) that overwhelmed the profits on our short bullet position. Going forward, there are good technical and strategic reasons to exit this trade. The butterfly spread is not yet at levels where it tends to mean-revert (second panel). In addition, Joe Biden’s US election victory has also increased the odds of a Brexit deal, which would put bear-steepening pressure on the UK Gilt curve. With that in mind, we are closing our Long UK 3/20 Barbell vs. 10-Year Bullet for a loss of -0.17%. Long France 2/30 Barbell vs. 5-Year Bullet Our rationale for entering this flattener was the same as in the UK. However, we fared quite a bit better here. The underlying 2/30 curve did flatten, as we expected, however, the butterfly spread itself moved further away from fair value, with the bullet component becoming relatively more expensive (Chart 6). So, as with the UK, the returns on this trade can be largely explained by the relative outperformance of the barbell component due to its higher convexity. In France, however, the effect worked to our favor as the yield curve shifted downwards significantly. The positive returns on the long French 30-year OAT component, where yields have been nearly slashed in half since July, dominated the other parts of the trade - even with the 30-year bond only being a small piece (11%) of the duration-weighted barbell Chart 5UK 3/10/20 Spread Fair Value Model

UK 3/10/20 Spread Fair Value Model

UK 3/10/20 Spread Fair Value Model

Chart 6France 2/5/30 Spread Fair Value Model

France 2/5/30 Spread Fair Value Model

France 2/5/30 Spread Fair Value Model

Although we did make profits on the flattener, it turned into a convexity bet that was not our original intention. Seeing as our underlying logic did not work out as expected, we are not comfortable remaining in this position. Thus, we are closing our France butterfly trade for a profit of 0.56%. Long Italy 5/30 Barbell vs. 10-Year Bullet As with the UK and France, we entered this trade based on its attractive model-based valuation and the relatively low correlation between inflation breakevens and nominal yields in France. Our expectation of flattening in the underlying 5/30 curve did not bear out as it remained mostly flat (Chart 7). We did see some reversion in the butterfly spread towards our model-implied fair value, which helped us make profits on our trade. Again, we cannot ignore the effect of convexity when looking at the outperformance of the barbell component. Yields fell dramatically across the Italian curve in one of the clearest examples of the yield-chasing behavior we have been describing this year.4 As Italian yields continue their race to the bottom, supported by ECB asset purchases and perceptions of more fiscal co-operation between the countries of Europe, there is a chance that this trade will continue to perform by virtue of its exposure to the long end of the Italian curve. However, as our original bias towards curve flattening did not play out, we prefer to maintain our exposure to Italian government debt via an overweight allocation in our model bond portfolio instead. We therefore close our Long Italy 5/30 Barbell vs. 10-Year Bullet for a profit of 0.83% Long US 7-Year Bullet vs. 5/10 Barbell The US was the only region where we initiated a “steepener” trade, with a long bullet versus short barbell combination that does well when the yield curve steepens. We chose this particular 5/7/10 butterfly as it was the most attractive steepener available based on our model-implied valuation that also fit our fundamental macro bias back in July towards US Treasury curve steepening – a view that we still hold today. With signs pointing towards further bear steepening of the Treasury curve, we feel comfortable keeping this US 5/7/10 butterfly spread trade open. Our rationale for initiating the trade was borne out, with the underlying 5/10 Treasury curve steepening and the butterfly spread tightening towards fair value (Chart 8). Our trade was supported by a continued rebound in long-dated US inflation expectations as well as the US election result, the most bond-bearish event of the year. Chart 7Italy 5/10/30 Spread Fair Value Model

Italy 5/10/30 Spread Fair Value Model

Italy 5/10/30 Spread Fair Value Model

Chart 8US 5/7/10 Spread Fair Value Model

US 5/7/10 Spread Fair Value Model

US 5/7/10 Spread Fair Value Model

Going forward, we see good reasons to maintain this trade. The butterfly spread, after briefly reaching expensive levels, is back to being attractively valued. Even if the residual were to dip back below zero, it would still have room to become more expensive, shoring up our trade. This trade also remains the most attractive of all the steepener trades on a model-implied valuation basis, removing any incentive to rotate towards another part of the curve. The odds favor more reflationary Treasury curve steepening after the US election. President-elect Biden has a stated goal of more fiscal stimulus, while his selection of Janet Yellen as Treasury Secretary signaling increased cooperation between monetary and fiscal authorities. With signs pointing towards further bear steepening of the Treasury curve, we feel comfortable keeping this US 5/7/10 butterfly spread trade open. Bottom Line: We are closing three of our four outstanding government bond yield curve trade recommendations, taking profits in France and Italy and realizing a loss in the UK. We are maintaining our US 5/7/10 butterfly trade, which is the cheapest way to position for an expected steepening of the Treasury curve based on our valuation models. Evaluating Our Cross-Country Yield Spread Trades We currently have two recommended trades involving plays on the spread between government bonds: Long 5-year New Zealand government bonds versus short 5-year UK Gilts, currency-hedged into GBP We initiated this trade on August 25, and to date the trade is severely underwater with a total return of -1.8%.5 That loss comes from the long New Zealand leg of the trade, as the 5-year NZ bond yield has increased by 34bps from our entry level. Chart 9A Rapid Shift Upward In NZ Rate Expectations

A Rapid Shift Upward In NZ Rate Expectations

A Rapid Shift Upward In NZ Rate Expectations

The rationale for this trade was based on our assessment of the relative probability of the Bank of England (BoE) and Reserve Bank of New Zealand (RBNZ) moving to a negative interest rate policy. Both central banks hinted strongly at such a move throughout the summer months as part of their efforts to support pandemic-stricken economies. Our view back in late August was that it was more likely that the RBNZ would choose negative rates, as New Zealand had far lower inflation expectations than the UK and, unlike the British pound, the New Zealand dollar was not undervalued. This trade was initially profitable, but all that changed rapidly during the month of November. The RBNZ disappointed investor expectations on a move to negative rates at the November 11 monetary policy meeting. The central bank elected instead to increase the size of its existing quantitative easing program, while giving no hint that negative rates were coming soon. The response was a sharp move higher in both New Zealand bond yields and the New Zealand dollar (Chart 9). There was an even more violent adjustment in yields and the currency last week, after New Zealand Finance Minister Grant Robertson wrote a letter to RBNZ Governor Adrian Orr asking the central bank to change its policy remit to include controlling New Zealand house price inflation. Markets interpreted this blatant political pressure on the central bank as the end of any hopes of negative rates in New Zealand, with bond yields and the currency spiking higher once again. House prices have surged after the RBNZ aggressively cut interest rates earlier this year, with a rapidly rising share of new mortgages having higher loan-to-value ratios (Chart 10). House price inflation is now running at 19.8%, and Finance Minister Robertson did cite deteriorating housing affordability and inequality as the basis for his letter to the RBNZ. It is clear that a move to negative interest rates – which could further fuel the explosion in house prices – is now very difficult for the RBNZ to pull off without facing intense criticism. It is clear that a move to negative interest rates – which could further fuel the explosion in house prices – is now very difficult for the RBNZ to pull off without facing intense criticism. This shatters the underlying rationale for our long New Zealand/short UK yield spread trade (Chart 11). Chart 10RBNZ-Fueled Boom In House Prices

RBNZ-Fueled Boom In House Prices

RBNZ-Fueled Boom In House Prices

Thus, we are choosing to cut our losses and close out our recommended trade. Long 10-year German Bunds versus short 10-year US Treasuries Chart 11Time To Cut Our Losses On The NZ-UK Trade

Time To Cut Our Losses On The NZ-UK Trade

Time To Cut Our Losses On The NZ-UK Trade

We initiated this recommendation on October 27, and to date the trade is running a small loss of -0.17%.6 The rationale behind the trade was two-fold: Our valuation model for the 10-year UST-Bund yield spread showed that the spread was far below fair value; We turned more bearish on US Treasuries just before the US presidential election, downgrading our recommended allocation to underweight while also upgrading more defensive Germany – with its low yield-beta to US Treasuries - to overweight. The trade initially performed well, driven by faster growth and inflation in the US versus the euro area (Chart 12). The Treasury selloff has stalled of late, but we view this as more a consolidative pause than a near-term peak in yields. Chart 12Fundamentals Justify A Wider UST-Bund Spread

Fundamentals Justify A Wider UST-Bund Spread

Fundamentals Justify A Wider UST-Bund Spread

With our Treasury-Bund valuation model still showing that the spread is too tight, and with the spread not looking overly stretched versus its 200-day moving average (Chart 13), we are keeping our US versus Germany trade in our Tactical Overlay portfolio. Chart 13Valuation & Momentum Point To A Wider UST-Bund Spread

Valuation & Momentum Point To A Wider UST-Bund Spread

Valuation & Momentum Point To A Wider UST-Bund Spread

Bottom Line: We are cutting our losses in our New Zealand-UK government bond spread trade, with the odds of the RBNZ shifting to a negative interest rate policy severely curtailed by political pressure over surging New Zealand house prices. We are maintaining our US-Germany spread widening trade, as the spread is too narrow based on our fair value model and we see more scope for US Treasury yields to drift higher in the coming months Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Shakti Sharma Research Associate ShaktiS@bcaresearch.com Footnotes 1 Please see BCA Research Global Fixed Income Strategy Weekly Report, " How To Play The Revival Of Global Inflation Expectations", dated June 23, 2020, available at gfis.bcaresearch.com. 2 Please see BCA Research Global Fixed Income Strategy Weekly Report, "Global Yield Curve Trades: Netting Returns With Butterflies", dated July 7, 2020, available at gfis.bcaresearch.com. 3 Readers looking for more detailed background on butterfly trades and our yield curve modelling framework should refer to the July 7, 2020 Strategy Report where we initiated these trades. 4 Please see BCA Research Global Fixed Income Strategy Weekly Report, "We’re All Yield Chasers Now", dated August 11, 2020, available at gfis.bcaresearch.com. 5 Please see BCA Research Global Fixed Income Strategy Weekly Report, "Assessing The Leading Candidates To Join The Negative Rates Club", dated August 26, 2020, available at gfis.bcaresearch.com. 6 Please see BCA Research Global Fixed Income Strategy Weekly Report, "The Global Bond Implications Of Rising Treasury Yields", dated October 27, 2020 available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

A Year-End Review Of Our Tactical Overlay Trades

A Year-End Review Of Our Tactical Overlay Trades

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Dear Client, Instead of our regular report next week, we will be sending you BCA Research’s Annual Outlook, featuring long-time BCA client Mr. X, who visits towards the end of each year to discuss the economic and financial market outlook for the year ahead. We will be back the week after with the GIS quarterly Strategy Outlook, where we will explore the major investment themes and views we see playing out in 2021. Best regards, Peter Berezin, Chief Global Strategist Highlights While a vaccine, ironically, could dampen economic activity in the near term, it will pave the way for faster growth in the medium-to-long term. Inflation is unlikely to rise much over the next two-to-three years. However, it could gallop higher later this decade as unemployment falls below pre-pandemic levels and policymakers keep both monetary and fiscal policy accommodative. Many of the structural factors that have depressed inflation are going into reverse: Baby boomers are leaving the labor force, globalization is on the back foot, and social cohesion is fraying. The lackluster pace of productivity growth suggests that innovation is not occurring as fast as many people think. Rather, what seems to be happening is that the nature of innovation is changing in ways that are a lot more favorable to Wall Street than Main Street. Monopoly power has grown, especially in the tech sector. This has had a deflationary effect in the past but could take a more inflationary tone in the future. Investors should remain overweight stocks for the next 12 months, while shifting equity allocation away from growth companies towards value companies and away from the US towards the rest of the world. The Waiting Game This week brought some further good news on the pandemic front. The number of reported daily cases continues to trend lower in Europe. The 7-day average has now fallen by 30% from its November 8th peak (Chart 1). In the US, there are faint indications that the number of new cases is stabilizing, especially in the hard-hit Midwest (Chart 2). Chart 1Covid Cases In Europe: Past The Worst

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Chart 2Covid Cases In The US: Approaching The Peak Of The Third Wave?

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Nevertheless, it is too early to breathe a sigh of relief. As with other coronaviruses, SARS-CoV-2 spreads more easily in colder temperatures. Moreover, this week is Thanksgiving in the US, and with the holiday season approaching in the wider world, there will be more opportunities for the virus to propagate. Chart 3The US May Have To Follow Europe In Tightening Lockdown Measures

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Despite the cresting in new cases, the absolute number of confirmed daily infections remains extremely high. The 7-day average currently stands at about 175,000 in the US. Adjusting for the typical three-week lag between new cases and deaths, the case-fatality rate is approximately 1.8%. The CDC estimates the “true” fatality rate is 0.7%.1 This implies that for every one person who tests positive for Covid-19, 1.5 people go undetected. Thus, around 450,000 Americans are catching Covid every day. That is 3.2 million per week or about 1% of the US population. Other estimates from the CDC suggest that the true number of new infections may now be even greater, perhaps as high as 11 million per week.2 Unlike in Europe, where governments have implemented a series of stringent lockdown measures, the US has taken a more relaxed approach (Chart 3). If the number of new infections fails to fall much from current levels, more US states will have to tighten social distancing rules. The availability of vaccines will pave the way for stronger growth in the medium-to-long term. Ironically however, as we pointed out two weeks ago, vaccine optimism could dampen economic activity in the near term. With the light clearly visible at the end of the tunnel, more people may choose to hunker down to avoid being infected. After all, how frustrating would it be to contract the virus just a few months before one can be vaccinated? It is like being the last guy shot on the battlefield in a war that is drawing to an end. The Outlook For Inflation Could inflation make a comeback once a vaccine is widely available? The pandemic put significant downward pressure on prices in a number of areas, particularly air transport, accommodation, apparel, and gasoline. While prices in some categories, such as used cars, meats and eggs, and certain toiletries did rise briskly, the net effect was still a substantial decline in overall inflation (Chart 4). Chart 4The Impact Of Covid On US Inflation

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Core PCE inflation stood at 1.4% in October, well below the Fed’s target. As Chart 5 illustrates, core inflation is below central bank targets in most other economies as well. A bounce back in prices in the most pandemic-afflicted sectors should lift inflation over the next six months. Our US bond strategists expect core PCE inflation to peak at 2¼% in the second quarter of next year, before falling back below 2% by the end of 2021. Chart 5Core Inflation Below Central Bank Targets

Core Inflation Below Central Bank Targets

Core Inflation Below Central Bank Targets

Chart 6Unemployment Rate Is Projected To Decline Towards Pre-Covid Lows In The Coming Years

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Ignoring the temporary oscillations in inflation due to base effects, a more sustained increase in inflation would require that labor market slack be fully absorbed. In its October 2020 World Economic Outlook, the IMF projected that the unemployment rate in the major economies would fall back to its full employment level by around 2025 (Chart 6). While a vaccine will expedite the healing of labor markets, it is probable that unemployment will remain too high to generate an overheated economy for the next three years. What about beyond then? The fact that long-term bond yields are so low today implies that most investors think that inflation will remain subdued for many years to come (Chart 7). This is confirmed by CPI swaps, which in some countries go out as far as 50 years. For the most part, they are all trading at levels below official central bank inflation targets (Chart 8). Chart 7Long-Term Bond Yields Are Depressed...

Long-Term Bond Yields Are Depressed...

Long-Term Bond Yields Are Depressed...

Chart 8… As Are Long-Term Inflation Expectations

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Heading Towards The Kink Is inflation really dead, or is it just dormant? We think it is the latter. Contrary to the claim that the Phillips curve has become defunct, Chart 9 shows that the wage version of the Phillips curve – which compares wage growth with the unemployment rate – is very much alive and well. What is true is that rising wage growth has failed to translate into higher price inflation in most economies since the early 1980s. However, this may have simply been due to happenstance: Every time the global economy was starting to heat up to the point that a price-wage spiral could develop, something would happen to break it. In 2019, the unemployment rate in the G7 hit a 46-year low. Perhaps inflation would have accelerated this year had it not been for the pandemic? Likewise, inflation might have risen in 2008 had it not been for the financial crisis, and in 2001 had it not been for the dotcom bust. Chart 9Is The Phillips Curve Really Dead?

Is The Phillips Curve Really Dead?

Is The Phillips Curve Really Dead?

Chart 10Inflation Reached The ''Kink'' In 1966

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Rather than being defunct, the price-version of the Phillips curve may turn out to be kinked at a very low level of the unemployment rate. Such was the case during the 1960s (Chart 10). US core inflation remained steady at around 1.5% in the first half of that decade, even as the unemployment rate drifted lower and lower. In 1966, with the unemployment rate nearly two percentage points below NAIRU, inflation blasted off, doubling to more than 3% within a span of six months. Core inflation would go on to increase to 6% by 1969, setting the stage for the stagflationary 1970s. A Less Deflationary Structural Backdrop Many pundits argue that the structural backdrop for inflation is vastly different today than it was during the 1960s, making any comparison with that decade next to worthless. They point out that unions had a lot more power back then, global supply chains were underdeveloped, and rapid population growth was creating more demand for goods and services than the economy could supply. We have addressed these arguments in the past and will not belabor the point this week other than to note that all three of these structural forces are now in retreat.3 Chart 11The Heyday Of Globalization Is Behind Us

The Heyday Of Globalization Is Behind Us

The Heyday Of Globalization Is Behind Us

Granted, unions are not as powerful as they were in the 1960s. However, public policy is still moving in a more worker-friendly direction. Witness the fact that Florida voters, despite handing the state to President Trump, voted 61%-to-39% to raise the state minimum wage in increments from $8.56 an hour to $15 by 2026. Joe Biden has also pledged to hike the federal minimum wage to $15 from its current level of $7.25. Meanwhile, globalization is on the back foot, with the ratio of trade-to-output moving sideways for more than a decade (Chart 11). At the same time, baby boomers are departing the labor force en masse. Rather than remaining net savers, these retiring workers will become dissavers. This means that the global savings glut, which has suppressed interest rates and inflation, could begin to dry up. Perhaps most ominously, social stability is at risk of breaking down. Homicides in the US have risen by nearly 30% so far this year compared to the same period a year ago.4 Historically, the institutionalization rate has tracked the homicide rate quite closely (Chart 12). As was the case in the 1960s, a lot of the well-meaning discussion about criminal justice reform today could turn out to be counterproductive. Perhaps it was just a coincidence, but it is worth remembering that inflation exploded in the 1960s at exactly the same time that the murder rate shot up (Chart 13). Chart 12Dramatic Drop In Institutionalization Rate During The 1960s Corresponded With A Sharp Increase In The Homicide Rate

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Chart 13Social Unrest Can Fuel Inflation

Social Unrest Can Fuel Inflation

Social Unrest Can Fuel Inflation

The Role Of Innovation Technological innovation has been routinely cited as a driver of falling inflation. In many ways, this is rather odd. Economic theory states that faster innovation should lead to higher real income. It does not say whether the increase in real income should come via rising nominal income or falling inflation. Indeed, to the extent that faster innovation leads to higher potential GDP growth, it could fuel inflation. This is because stronger trend growth will tend to raise the neutral rate of interest, implying that monetary policy will become more stimulative for any given policy rate. Moreover, the fixation on technology as a deflationary force is a bit strange considering that measured productivity growth has been exceptionally weak in most advanced economies over the past 15 years – weaker, in fact, than it was in the 1970s (Chart 14). Chart 14US Productivity Has Been Exceptionally Weak Over The Past Ten Years

US Productivity Has Been Exceptionally Weak Over The Past Ten Years

US Productivity Has Been Exceptionally Weak Over The Past Ten Years

How, then, does one explain why tech stocks have fared so well? One often-heard answer is that productivity growth is mismeasured. We examined this argument carefully in our report entitled Weak Productivity Growth: Don't Blame The Statisticians, concluding that this does not appear to be the case. A more plausible answer is that while the pace of innovation has not sped up, the nature of innovation has changed dramatically in ways that have helped Wall Street a lot more than Main Street. The True Nature Of Corporate Profits Standard economics textbooks regard profit as a return on capital. This implies that if the price of capital goes down, firms should respond by increasing investment spending in order to further boost profits. In practice, that has not occurred. For example, the Trump Administration promised that corporate tax cuts would produce an investment boom. While business investment did rise in 2018, this was all due to a rebound in energy spending. Outside of the oil and mining sector, business investment grew more slowly between Q4 of 2016 and Q4 of 2019 than it did over the preceding three years (Chart 15). Likewise, neither falling interest rates nor rising stock prices – two factors that should produce a lower cost of capital – have done much to buoy investment spending in recent years. Chart 15Overall Capex In 2017-2019 Was Boosted By The Oil And Mining Sector

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Chart 16A Winner-Takes-All Economy

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Why did the standard economic relationship between investment and the cost of capital break down? The answer is that the traditional approach does not take into account what has become an increasingly important driver of corporate profits: monopoly power. A recent study by Grullon, Larkin, and Michaely found that market concentration has increased in 75% of all US industries since 1997.5 Furman and Orszag have shown that the dispersion in the rate of return on capital across firms has widened sharply since the early 1990s. In the last year of their analysis, firms at the 90th percentile of profitability had a rate of return on capital that was five times that of the median firm, a massive increase from the historic average of two times (Chart 16). The dispersion in performance has been particularly stark within the tech sector. According to BCA Research’s proprietary Equity Analyzer, the shares of “value tech” companies – that is, companies trading in the bottom quartile of price-to-earnings, price-to-operating cash flow, price-to-free cash flow, price-to-book, and price-to-sales – have not only lagged the shares of other tech companies, but they have also lagged the shares of similarly valued financial companies (Chart 17). This underscores the point that the outperformance of growth stocks over the past 12 years has not just been a story about technology. Rather, it has primarily been a story about some tech companies doing much better than other tech companies. Chart 17Value Tech Lagged Value Financials

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

The Winner-Take-All Economy What explains the bifurcation in performance within the tech sector? Two reasons come to mind. First, tech companies are particularly susceptible to network effects: The more people who use a particular tech platform, the more attractive it is for others to use it. Facebook is a classic example. Second, tech companies benefit significantly from scale economies. Once a piece of software has been written, creating additional copies costs almost nothing. Even in the hardware realm, the marginal cost of producing an additional chip is tiny compared to the fixed cost of designing it. All of this creates a winner take-all environment where success begets further success. The role played by winner-take-all markets explains how a handful of companies were able to become mega-cap tech titans. Chart 18 and Chart 19 show that increased monopoly power, as reflected in rising profit margins and higher relative P/E ratios, has played a greater role in driving tech share outperformance since the mid-1990s than faster revenue growth. Chart 18Decomposing Tech Outperformance (I)

Decomposing Tech Outperformance (I)

Decomposing Tech Outperformance (I)

Chart 19Decomposing Tech Outperformance (II)

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Reaching Adulthood History suggests that monopolists tend to experience an initial rapid growth phase in which they capture ever-more market share, followed by a mature phase where they effectively function as utilities – cranking out stable cash flows to shareholders without experiencing much further growth. While it is impossible to say how far along most of today’s tech leaders are in this cycle, it does appear that the period of rapid growth for many of them may be drawing to a close. As it is, close to three-quarters of US households already have an Amazon Prime account. Slightly over half have a Netflix account. Nearly 70% have a Facebook account. Google commands 92% of the internet search market. The shift away from “growth status” towards “utility status” for some tech monopolists could prompt investors to trim the valuation premium they assign to these stocks. In addition, it could lead to increased regulation by governments to ensure that monopoly power is not abused. This could further depress valuations. Monopolies And Inflation What about the implications for inflation? Unlike firms in a perfectly competitive industry, monopolistic firms have to contend with the fact that higher output could depress selling prices, thus leading to lower profit margins. As my colleague Mathieu Savary has emphasized,6 this implies that rising market power could simultaneously increase profits while reducing investment in new capacity. At least initially, this could be deflationary in two ways: First, lower investment spending will reduce aggregate demand. Second, greater market power will shift income towards wealthy owners of capital, who tend to save more than regular workers. This helps explain why falling real interest rates and rising profits have failed to trigger an investment boom. Further down the road, the impact of monopoly power on inflation could turn on its head. Less investment spending will curb potential GDP growth, making it easier for economies to run up against capacity constraints. Low real interest rates could also induce governments to run larger budget deficits, boosting aggregate demand in the process. Finally, an economy where monopoly power runs unchecked will eventually spur a populist backlash, leading to reflationary policies that favor workers over business oligarchs. Investment Conclusions Equities have run up a lot since the start of November. Bullish sentiment has surged in the American Association of Individual Investors weekly bull-bear poll, while the put-to-call ratio has fallen to multi-year lows (Chart 20). Given the likelihood that economic growth could surprise on the downside in the near term, equities are vulnerable to a short-term correction. Nevertheless, rising odds of an effective vaccine and continued easy monetary policy keep us bullish on stocks over a 12-month horizon. Chart 20A Lot Of Bullishness

A Lot Of Bullishness

A Lot Of Bullishness

Chart 21European Banks: A Low Bar For Success

European Banks: A Low Bar For Success

European Banks: A Low Bar For Success

Equity investors should shift their allocation away from growth stocks towards value stocks and away from the US towards the rest of the world. We like European banks in particular. They currently trade at 0.6-times tangible book value and 7.2-times 2019 earnings. Earnings estimates for 2021 have been slashed but should rebound on the expectation of a vaccine-driven growth recovery later next year (Chart 21). Faster growth should produce a modest steepening in yield curves, boosting net interest margins in the process. Faster growth should also lead to stronger credit demand while reducing bad loans. Looking further out, this week’s report argues that inflation could accelerate meaningfully once unemployment returns to pre-pandemic levels in about two-to-three years. The departure of baby boomers from the labor market, sluggish productivity growth, fraying social cohesion, and a backlash against monopoly power could all push up inflation. These forces could also create a more challenging environment for stocks, particularly today’s mega-cap tech names. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 A recent systematic review of literature found that the Covid-19 infection fatality rate (IFR) stood at 0.7%. Similarly, in September, the Centers for Disease Control and Prevention (CDC) published age-specific IFRs in its Covid-19 Planning Scenarios. The population-weighted average of the CDC’s “best estimate” suggests a 0.7% IFR. Please see “COVID-19 Pandemic Planning Scenarios,” Centers for Disease Control and Prevention, updated September 10, 2020; and Gideon Meyerowitz-Katz, and Lea Merone, “A systematic review and meta-analysis of published research data on COVID-19 infection fatality rates,” International Journal of Infectious Diseases, September 29, 2020. 2 Please see “Covid live updates: CDC estimates only eighth of infections counted,” NBC News Live Blog, November 25, 2020; and “The Latest: South Korea has most daily cases in 8 months,” Associated Press, November 26, 2020. 3 Please see Global Investment Strategy Special Report, “Is The Entire World Heading For Negative Rates?” October 25, 2019; Special Reports “1970s-Style Inflation: Could It Happen Again? (Part 1),” and “1970s-Style Inflation: Could It Happen Again? (Part 2),”dated August 10 and 24, 2018; and Weekly Report, “Is The Phillips Curve Dead Or Dormant?” dated September 22, 2017. 4 Please see this Twitter thread on the latest data from the 100 largest US cities by Patrick Sharkey, Professor of Sociology and Public Affairs at Princeton University. 5 Gustavo Grullon, Yelena Larkin, and Roni Michaely, “Are US Industries Becoming More Concentrated?” Oxford Academic, Review of Finance (23:4), July 2019. 6 Please see The Bank Credit Analyst Special Report, “The Productivity Puzzle: Competition Is The Missing Ingredient,” dated June 27, 2019. Global Investment Strategy View Matrix

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Current MacroQuant Model Scores

Inflation, Innovation, And The Value/Growth Debate

Inflation, Innovation, And The Value/Growth Debate

Highlights President Trump’s final actions and the US fiscal impasse pose non-trivial risks to the rally. Biden’s foreign policy cabinet picks have limited impact but are mildly positive for now. Biden’s multilateralism will eventually conflict with the need to get things done. Continuities with Trump foreign policy are underrated. The RCEP trade agreement is not a game changer but a pro-trade shift in the US would be. Europe is a clear winner of the US election but continental politics risk will pick up next year from today’s lows. Book profits on select risk-on trades, but go strategically long GBP-EUR. Feature Global financial markets are surging on a raft of good news. We are booking some gains as we expect the rally to be capped in the near term either by Trump’s final actions as president or by the US fiscal impasse. First, the good news. The US power transition is officially under way, reducing US policy uncertainty. The popular vote within the critical battleground states acted as a restraint on the Republican Party’s ability to dispute the results or appoint Republican electors to the Electoral College.1 Chart 1US And Global Policy Uncertainty Falling

US And Global Policy Uncertainty Falling