Policy

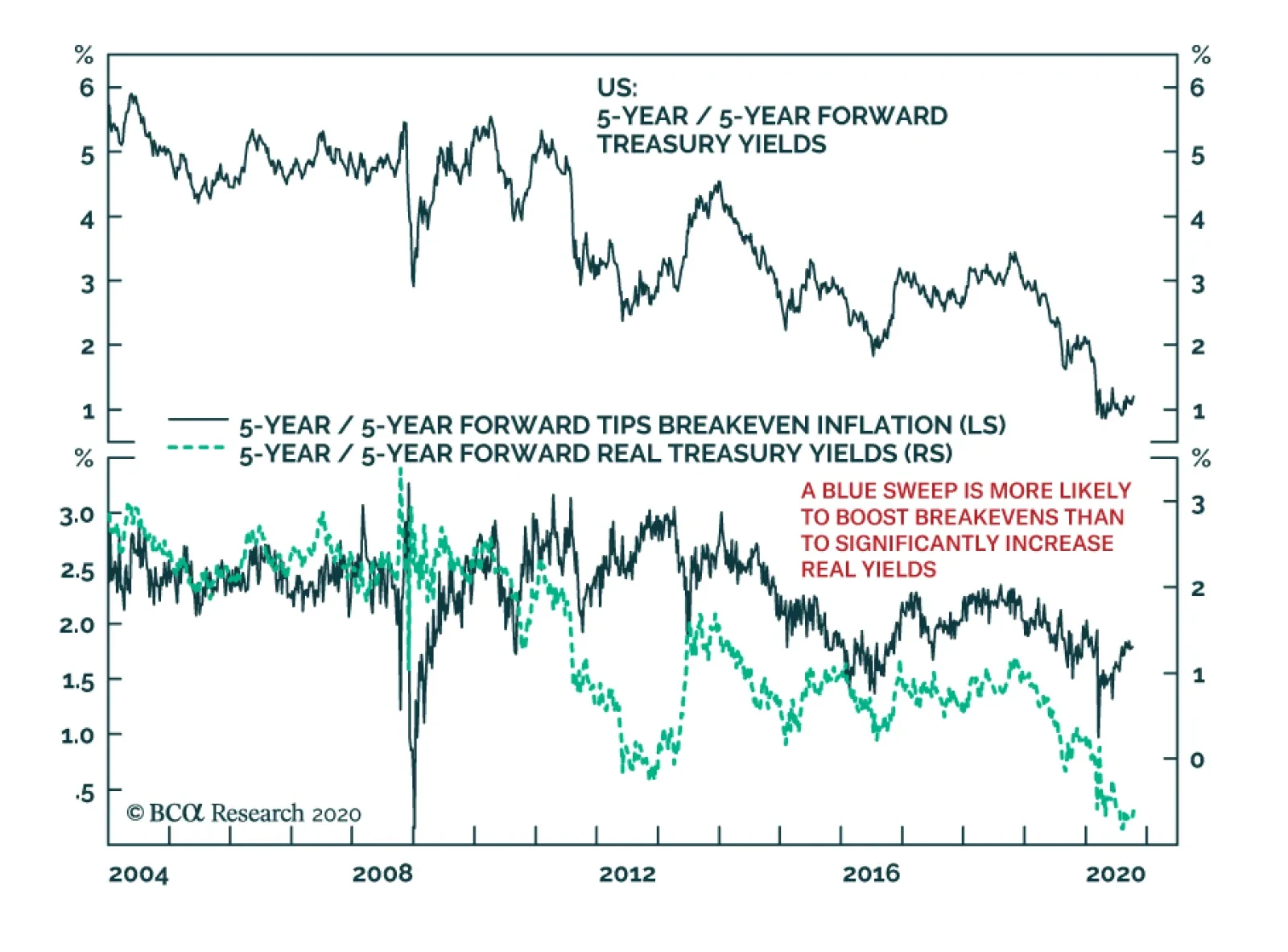

Highlights The US Senate election is as important as the presidency for US politics and markets. Our quantitative Senate election model suggests Democrats will win control – as we have long argued – but there is a 49% chance that they do not, which is higher than consensus. A Republican Senate under a Biden presidency is positive for US stocks relative to global. Corporate taxes will stay put. However, fiscal reflation will have to be earned through tough budget battles, which will raise hurdles for markets. The Democratic sweep scenario is generating excessive enthusiasm in the media, as taxes will rise, but it is ultimately reflationary. It will benefit global stocks more than US stocks. Feature Chart 1Democratic Sweep Favors Global Stocks Versus US

Democratic Sweep Favors Global Stocks Versus US

Democratic Sweep Favors Global Stocks Versus US

Throughout the year we have argued that, as a base case for the US election, investors should expect that the pandemic, recession, and widespread social unrest in the United States would culminate in an anti-incumbent movement among voters. President Trump and the Republicans would lose the White House and Senate in a Democratic sweep. The implication for markets was that, after election volatility, global equities would rally in expectation of less hawkish US foreign and trade policy, while US equities would underperform on the expectation of higher taxes and regulation at home. This view has now become the market consensus (Chart 1). However, our quantitative US election model – which does not rely on head-to-head opinion polling – has recently given President Trump a 49% chance of winning in the latest reading. It is flagging a Biden victory but is essentially “too close to call” (Chart 2). The rapid snapback in the economy provides a basis for Trump to make an eleventh-hour comeback, contrary to optics. Chart 2Quant Model Shows Trump Loss, But 49% Odds Of Winning

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

In this report we present our quant model for the US Senate election, updated for the 2020 cycle. The Senate model is constructed with similar variables, though not exactly the same, and the result is that Democrats are favored to win control but only slightly. The implication is that Democrats are currently overrated by markets and that the election could still go either way. Uncertainty will go up for the remainder of the month. Ultimately we are sticking with our original forecast unless Trump and the Republicans regain momentum in opinion polling, but our models are flagging major risk. Investors should expect volatility to rise in the short term. We will maintain our tactical risk-off trades, since the risk of a contested election and/or a Trump re-election (and hence renewed global trade war) is rising. The Foundations Of Our Senate Model BCA Geopolitical Strategy developed a US Senate election model in September 2018 which quantified the margin of victory for the GOP among several Senate races during the 2018 mid-term election. The beta model focused on modeling individual Senate races, those deemed competitive by BCA’s Geopolitical Strategy at the time, by combining state and national level economic and political variables as well as the latest polling data applicable to each race.1 We are now re-introducing this model, but with a twist: this time we are adopting the same methodology as per our US presidential election model. The result is a state-by-state model that predicts the number of seats the incumbent party will win in the Senate election on November 3, 2020. Like our US election model, our Senate model is based off a probit model that produces a probability that each state will remain under the control of the incumbent party. The dependent variable (classified as “elected”) is stated as 1 = incumbent party wins the Senate election in each state; or 0 = incumbent party does not win the Senate election in each state. This method allows us to measure the probability that a state with certain characteristics will fall into one of these two categories. Therefore we can predict the probability of the incumbent party winning all the Senate seats in each of the 50 states (though, of course, this is only relevant to the one-third of the states that have a Senate seat up for election in 2020). Our model would have predicted the past five Senate election outcomes correctly on an in-sample basis and the past four Senate elections on an out-sample basis. Unlike our presidential election model, which sampled nine elections (1984 to 2016), our sample size for the Senate model is notably larger. That is, our sample consists of 18 Senate elections (1984 to 2018), across 50 states, amounting to 900 observations. While midterm Senate elections are different from those held during a presidential election year, we would not want to exclude the information they provide. The 2018 Senate race has a bearing on our 2020 prediction and this is appropriate. The Senate Model’s Variables Our Senate model includes six explanatory variables: 1. The Federal Reserve Bank of Philadelphia State Coincident Index. The coincident index for each state combines four of the state’s indicators to summarize current economic conditions in a single statistic. The four indicators are nonfarm payroll employment; average hours worked in manufacturing by production workers; the unemployment rate; and wage and salary disbursements plus proprietors' income deflated by the consumer price index (U.S. city average). Like in our US Presidential model, we applied several transformations to the data to obtain meaningful results in the modeling process. We found that using a three-month change of the state coincident index in our Senate model provided the most statistically significant result. Our Senate model suggests that Republican odds of winning are underrated by online betting markets, as with our presidential model. The three-month change of all the monthly state coincident indexes are given heavier weight as we approach the Senate election early in November. However, we only include the preceding year of a Senate election up until September of the election year (i.e. the last data release in October prior to the election itself). Senate elections occur every two years, and we excluded data that has been accounted for in previous elections. As we highlighted in the update of our US Election model we assume that prevailing economic conditions matter most to voters (as future expectations inevitably affect people’s assessment of their current situation), and this bolsters our rationale in using a 3-month change of the state coincident index. 2. The incumbent party’s margin of victory in previous Senate elections in each state Senate race. This is measured as the incumbent party’s share of the popular vote minus the non-incumbent party’s share. If the incumbent party failed to secure a solid win in each state in the previous Senate election, the probability of securing a solid win in the current election becomes smaller. Moreover, the larger the margin of victory in a previous Senate election race, the more likely that incumbent party will win re-election in said state. 3. Net average approval level of the incumbent president in a Senate election year. This is the difference between the incumbent president’s approval and disapproval levels in a Senate election year, from the start of the year up until the end of October of that year – taken as an average. 4. Generic congressional ballot (net support rate). The generic congressional ballot asks people which party they are likely to vote for in Congress. We take the average net support rate in a Senate election year (that being whichever party leads the other in congressional ballot polling). Democrats are usually favored in congressional generic ballot voting, so the net rate is more predictive than the gross rate 5. Dummy variable for congressional ballot. A dummy variable is assigned to variable number four. For example, dummy takes the value of 1 when Democrats have a positive net support rate in generic congressional ballot voting, and 0 when Republicans have a net positive support rate. We assign only one dummy variable to avoid a dummy variable trap.2 6. A “time for change” variable, a categorical variable indicating whether the incumbent party has controlled the Senate for three or more terms (six or more years). If the Senate has been controlled by the incumbent party for three or more terms, the model will “punish” the incumbent party, as we would expect to see a change in control of the Senate the longer one incumbent party controls it. Estimating The Model Since this is a probit model, the coefficients cannot be directly interpreted like in an ordinary regression.3 In Table 1, the sign of the coefficient corresponds to the direction of change in probability. An increase in the State Coincident Index, the incumbent’s margin of victory in previous Senate races, net approval of the incumbent president and generic congressional support ballot, all increase the probability of the incumbent winning a Senate election in a state. Table 1Senate Model Regression Coefficients

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Meanwhile occupying the Senate for more than three terms serves as a “punishment” and would decrease the probability of winning a Senate election in a state. The output of our model is the probability of an incumbent win in each state. As in our US Presidential election model, there are two ways of aggregating these probabilities to produce a national-level outcome: Proportional: Allocate the number of Senate seats won by the incumbent proportionally to their probability of victory in each state, and then sum them up across all states. Winner Takes All: As we do in our US Presidential election model, assume a probability threshold of 50%: any state with an incumbent win that is at least 50% likely is fully assigned to the incumbent. The latter, winner takes all, is the aggregation method we base our Senate prediction on. Senate Election Model Prediction Table 2 shows our 2020 prediction. Overall, the Republican Party is expected to win 49 Senate seats, a decrease of four seats from its current 53-seat majority. This means that the Democrats are expected to control the Senate with 51 seats (this includes Independents that caucus with Democrats). Moreover, the model suggests that Republicans have a 49% chance of retaining Senate control. Table 2Predicted 2020 Senate Balance Of Power

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

This is substantially higher than consensus, which has put Republicans at 42% throughout the past month and currently has them at 37% (Chart 3). As with our presidential model, the rapid recovery in the state economic indicators is providing the Republicans with a last-minute boost that contradicts the gloomier picture painted by opinion polls. We do not think they will retain the Senate, but our conviction level is now lower. Chart 3Betting Market Overrates Democratic Odds Of Winning Senate

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

In terms of Senate seats, our model expects Republicans to lose Arizona, Colorado, Maine, Montana, and North Carolina. This is enough for Democrats to obtain 51 seats, a majority, assuming that they lose Alabama. The full list of states that have Senate races in 2020 and the probabilities of a Republican win according to the model are shown in Chart 4. Chart 4Quant Model Shows Democrats Win Senate, But GOP Odds 49%

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Three Senate races are classified as toss-ups, which we define as having a probability between 45% and 55% according to the model. These states are Iowa (54%), Maine (48%) and North Carolina (49%). Montana is close to a toss-up, with a 44% chance of a Republican win. We expect Democrats to win control of the Senate with 51 votes. They need 50, plus the White House, to have a majority. Of these states, if Republicans retain any two, then they will retain their majority, so control of the Senate is on a knife’s edge. Chart 5 shows the odds for each of the 12 swing states in this election. Chart 5Our Senate Odds Compared With The Bookies

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Bear in mind that only 50 seats are needed for the party that wins the White House, since the Vice President is also the President of the Senate and casts the tiebreaking vote. Senate Races Of Interest Our results show that the consensus is underestimating the Republicans, except in Michigan and Montana. The latter could affect overall control of the Senate. The same can be said for Maine, where the Republican challenger may be underrated (Chart 6). The trend of opinion polling in Chart 6 generally shows closer races than the betting markets expect. Our model supports the betting markets on the unlikelihood that Democrats will prevail in several deep red states. Chart 6US Senate Polling And The Betting Odds

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

The presidential race should be the decisive factor. If voters in swing states are sufficiently motivated to vote out the sitting president that they chose only four years ago, which is uncommon in modern US history, then they will likely repudiate the senators who carried that president’s water through a whirlwind of scandals and controversies. Yet with the races so precariously balanced, small or local factors could also decide the outcome. This is an important limitation on our macro method. For example, it is not at all clear that Democrats will win Maine. Our model gives Republicans a 48% chance, while online gamblers put it at 27%. Susan Collins is well-entrenched, having survived again and again since 1996. If Democrats do poach Maine, it is still not clear that they will carry Iowa and Montana, which are more conservative yet saw Democratic victories in 2018. Our model suggests Montana will go Democratic and Iowa will stay Republican. Democrats must win one of these two states (or North Carolina) or they will not take the Senate. A feather could tip the scales. A feather may already be doing that in North Carolina, the other key toss-up state. Democratic candidate Cal Cunningham’s sex scandal has roiled the race. It is not yet clear that voters will abandon Cunningham (see Chart 6, panel 1), but that is likely unless there is an unstoppable Democratic wave.4 If North Carolina stays Republican as a result, then, according to our model, the US Senate would tie at 50-50 and the winner of the White House would turn the balance. Some Democrats have argued that deeper red states may be in contention, such as Georgia, South Carolina, Alaska, Kansas, or Kentucky. Of these, Kansas is notable since no candidate has an incumbent advantage. However, our model rules these races out of play and we tend to agree. Bottom Line: Our model suggests that Democrats will narrowly win control of the Senate as things stand today. With several races extremely close, a trivial event in a single state could turn the balance of power in the US Senate and hence the policy consequences of the entire US election. However, the close contest implies that the party that wins the White House will also win the Senate. Back Testing Our Model Our Senate model performs at an acceptable level during in-sample and out-sample back testing. For in-sample testing, we test our model over our entire sample period (1984 – 2018) and find that 72% of Senate elections (control of the Senate) are correctly predicted, with the model predicting the outcome of the last five Senate elections correctly (Chart 7). Chart 7In-Sample Back Testing Results

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

During out-sample back testing, we look at a sample period of 2000 – 2018, comprising of ten Senate elections, where our model correctly predicts 69% of actual outcomes. The previous four Senate elections are predicted correctly (Chart 8). There is still a roughly 50/50 chance of divided US government in 2021-22. Chart 8Out-Sample Back Testing Results

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Investment Takeaways Our US Senate model is based off a similar methodology as our US Presidential election model. There are however some minor differences. First, we use a weighted maximum likelihood estimate as opposed to a traditional maximum likelihood estimate. This is because of unbalanced binary outcomes in our dependent variable (see Appendix). Chart 9Fair Chance Of Divided Government Still

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Secondly, not all our explanatory variables are the same. While we maintain using the State Coincident Index as our one and only economic variable, our suite of political variables has changed to be more geared towards predicting the Senate outcome. Our Senate model predicts Republicans will retain only 49 seats and lose control of the Senate. The Democrats will take control with 51 seats. And yet Republicans have a 49% chance of retaining Senate control. This is equivalent to saying that the race is “too close to call” – which is similar to our presidential model results. The reason is the rapid snapback in the economy. Subjectively, the risk is to the downside for Republicans given the President’s poor polling, particularly on his handling of the pandemic, and the high unemployment rate. The Senate outcome should be determined by the White House race, but obviously there is a fair chance that the winner of the White House still loses control of the Senate (Chart 9). Chart 10Wall Street Expects Divided Government

Wall Street Expects Divided Government

Wall Street Expects Divided Government

Chart 11Trump Protectionism Good For The Dollar

Trump Protectionism Good For The Dollar

Trump Protectionism Good For The Dollar

The stock market is behaving like it expects gridlock, rather than a Democratic sweep – the latter offering greater downside and lesser upside, at least judging by history (Chart 10). So let’s boil this all down to what we know with reasonable certainty: If Trump wins with a Republican Senate, he will still face opposition from House Democrats, so he will be driven to foreign and trade policy in his second term. Protectionism will affect not only China but also Europe and other economies. This is broadly positive for the dollar and US equities relative to global stocks and commodities (Chart 11). Government bond yields would be volatile due to the risk to the cyclical recovery from global trade war. If Biden wins in a Democratic sweep, economies other than China will benefit from lower trade risk and the US will benefit from higher odds of unfettered fiscal stimulus in 2021. But financial markets will simultaneously have to adjust for the negative shock to US corporate earnings from higher taxes and regulation. This outcome is broadly negative for the dollar and US equities relative to global equities and commodities. Government bond yields would rise on the generally reflationary agenda. If Biden wins without the Senate, the market has the most positive outcome of all: less trade war yet no new tax hikes. Both US and global equities would benefit. Bond prices and the dollar would trend downward over time, but not during the occasional fiscal battles that would ensue between the Democratic president and Republican senators. Guy Russell Research Analyst GuyR@bcaresearch.com Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Statistical Appendix A notable property in our dependent variable data requires a brief discussion. Our dependent variable classified as “elected” takes the form of a binary outcome. This data, however, is what’s called “unbalanced,” since incumbent Senators are re-elected approximately 80% of the time. This means that most outcomes in our dependent variable are coded as “1,” with fewer “0’s” because of the strong incumbency effect in Senate races. There are many data sets that exhibit this type of property, such as events like wars, vetoes, cases of political activism, or epidemiological infections, where non-events occur rarely. To alleviate this statistical property in the data, we estimate our model using a weighted maximum likelihood estimate as opposed to the ordinary maximum likelihood estimate usually used in a probit regression.5 This method assigns more weighting to the unbalanced data, or what is known theoretically as “rare event” data, to aid the probit regression in assigning higher probabilities to “0” outcomes. Through this process, we effectively deal with our unbalanced dependent variable data. That said, in developing our quantitative US Senate Election Model, we estimated a suite of probit regressions with several other variables that were theoretically assumed to be relevant and subsequently tested empirically. In Appendix Table 1 below, we only include variables 1, 2, 3 and 6 from our listed variables (we excluded the generic congressional ballot and its corresponding dummy variable). This model suggests that Republicans will hold control of the Senate with 51 seats. Back testing this model revealed that 71% of past Senate elections were correctly predicted, while 67% were correctly predicted in out-sample testing. This is only slightly worse of a track record than our final model. If this model proves more accurate in the event, the implication is that the generic congressional ballot is an unreliable poll. Americans could be shy about stating their support for the Republican Party in the era of Trump. For this outcome, Republicans would only lose Arizona and Colorado. Critical swing states here are Montana (53%) and Arizona (45%). Appendix Table 1Alternative Senate Model Predictions

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

A re-work of the above model, but with a variable that punishes Republicans for holding the Senate for six years or more on average, suggests that Republicans will only win 47 seats in the Senate, giving up six seats (Appendix Table 2). Forecast accuracy is slightly worse off, giving just 68% and 67% predictive accuracy during in and out-sample forecasting of previous Senate elections, respectively. Compared to our primary model, Republicans would lose Arizona, Colorado, Iowa, Maine, Montana, North Carolina and Alabama. Alabama (45%) is the only critical swing state. Appendix Table 2Alternative Senate Model Predictions

Introducing Our Quantitative US Senate Election Model

Introducing Our Quantitative US Senate Election Model

Note: This report has been corrected since publication due to errors in charting. Charts 7 and 8 showed the correct majority party in historical Senate elections but mistakenly attributed to that party the minority party’s number of seats. The changes do not affect the text or the substance of the report: our quantitative model’s accuracy levels remain unchanged, as does the model’s performance relative to historical election results. Footnotes 1 The model was able to predict 14 out of 18 (77%) Senate races flagged as competitive by BCA’s Geopolitical Strategy. Florida, North Dakota, Indiana and Missouri were flagged as Democratic by our model but were won by Republican candidates. 2 A dummy variable trap is a scenario in which the independent variables are multicollinear — a scenario in which two or more variables are highly correlated; or, in simple terms, in which one variable can be predicted from the others. To avoid such a trap, we must exclude one of the categorical variables. Since there are two categorical variables that can be represented here (Republican or Democrat), we use k-1 (where k = the number of categorical variables). 3 The coefficients in a probit regression model measure the change in the Z-score associated to each independent variable for a one-unit change in that variable. 4 See Evie Fordham, "NC Democrat Cal Cunningham faces FEC complaint over California trip amid affair," Fox News, October 13, 2020, foxnews.com. 5 Weighted maximum likelihood estimation is a reasonable approach in dealing with dependent variables that show significant imbalance in their data set. See: King, G. and Zeng, L., 2001. Logistic regression in rare events data. Political analysis, 9(2), pp.137-163.

Highlights Our model suggests that more rate hikes are ahead in 2021; we project a less than 50bps increase in the PBoC policy rate from the current level. Chinese stock prices positively correlate with interest rates and bond yields. The relationship has strengthened since 2015. In the next six to nine months, Chinese stock prices will likely trend up alongside a rising policy rate and an accelerating economic growth. Feature China’s policy rate and bond yields have been rising sharply since May and are breaching their pre-COVID 19 levels. Meanwhile, Chinese stock prices have moved sideways since mid-July, despite a steady recovery in the domestic economy. While some commentators view higher interest rates as a harbinger of an impending equity market weakness, our research shows that the relationship between China’s stock prices and short-term rates has been positive since 2015. A rally in Chinese stocks and outperformance of cyclical stocks relative to defensives positively correlate with rising interest rates and bond yields (Chart 1A and 1B). Chart 1ARising Bond Yields Coincide With Ascending Chinese Stock Prices...

Rising Bond Yields Coincide With Ascending Chinese Stock Prices...

Rising Bond Yields Coincide With Ascending Chinese Stock Prices...

Chart 1B...And Offshore Cyclicals

...And Offshore Cyclicals

...And Offshore Cyclicals

Chart 2Massive Stimulus In 2020 Will Accelerate Economic Growth Into 1H21

Massive Stimulus In 2020 Will Accelerate Economic Growth Into 1H21

Massive Stimulus In 2020 Will Accelerate Economic Growth Into 1H21

China’s massive stimulus this year generated some self-sustaining momentum that will likely push the nation’s output higher in 1H21(Chart 2). The PBoC may raise the policy rate by as much as 50bps in 2021 from its current level, but strong domestic fundamentals should be able to drive up Chinese stock prices, in both absolute term and relative to global equities in the next six to nine months. PBoC Policy Hikes:Still More Ahead While the PBoC’s policy rate has rebounded sharply, it remains at its lowest level since the Global Financial Crisis. Looking forward, will the central bank bring the policy rate (e.g. 3-month SHIBOR) back to its pre-COVID 19 range of 3 – 3.5% or the pre-trade war level near 5%? The acceleration in China’s economic recovery is expected to continue and would boost China’s annual output growth in 1H21 to two to three percentage points above its trend. Based on these estimates, our interest rate model implies more than 200bps in rate increases in 2021 from the current level1 (Chart 3). Chart 3Rising Odds Of PBoC Rate Hikes In 2021

Rising Odds Of PBoC Rate Hikes In 2021

Rising Odds Of PBoC Rate Hikes In 2021

Historically, our model has successfully captured the major turning points in China's policy rate cycles. This time around, however, the pandemic and the subsequent economic recovery may have complicated the model's predictive power. The model suggests that, in 1H21 the policy rate will return to its pre-trade war range of 4-5%, but we think the rate increases will be capped within 50bps. The model follows a modified version of "Taylor's Rule," in which we assume that the PBoC will target its short-term interest rate based on the deviation between actual and desired inflation rates and the deviation between real GDP growth and China’s trend GDP growth rate. The latest data shows across-the-board strengthening in the economy; most indicators have surprised to the upside, confirming our optimistic assessment.2 However, Taylor's Rule is not able to account for sudden shocks in the economy, such as a pandemic-induced global recession. Thus, the model exaggerates the magnitude of interest rate bumps, based on an economic growth acceleration following a one-off economic shock. In a report earlier this year, we noted that the PBoC has been proactive in normalizing its monetary policy following short-term shocks.3 This is contrary to economic downturns when the PBoC has been a reactive central bank and its decisions often lagged a pickup in economic activity. As such, although interest rates have swiftly rebounded after the pandemic-induced growth contraction in Q1, we expect the pace of rate hikes to be slower in 2021. Chart 4Rapid RMB Appreciation Will Bring Headwinds To Chinese Industrial Profits

Rapid RMB Appreciation Will Bring Headwinds To Chinese Industrial Profits

Rapid RMB Appreciation Will Bring Headwinds To Chinese Industrial Profits

External factors are accounted for in the model, though they may be underestimated. The US Federal Reserve Bank has decisively shifted its monetary policy to broadly accommodative and will stay behind the inflation curve in the next few years. The collapse in interest rate differentials between the US and China has made RMB-denominated assets attractive, boosting strong inflows of foreign capital and rapidly pushing up the value of the RMB (Chart 4, top panel). While we think Chinese policymakers have pivoted to prefer a strong RMB, the recent countermeasures by the PBoC indicate that the central bank will not allow the RMB to climb too rapidly.4 China's drastic tightening in monetary conditions and the sharp rally in the trade-weighted RMB from 2011 to 2014 led to a prolonged economic downturn (Chart 4, bottom panel). Therefore, in the absence of synchronized policy tightening from other central banks, the magnitude of rate hikes by the PBoC will be measured. Bottom Line: The PBoC will continue to push up the policy rate in 2021, but our baseline view is that the magnitude will be capped below 50bps. Interest Rates And Chinese Stocks Chart 5Chinese Stocks/Bond Yields Correlation Became Much More Positive After 2015

Chinese Stocks/Bond Yields Correlation Became Much More Positive After 2015

Chinese Stocks/Bond Yields Correlation Became Much More Positive After 2015

Many investors might think that stock prices tend to react negatively to monetary policy tightening because interest rate upturns and mounting bond yields lead to higher costs of funding for corporations and lower profit growth. However, Chinese stock prices started moving in the same direction with policy rates and bond yields following the burst of the 2014/15 stock market bubble (Chart 5 and Chart 1A and 1B on Page 4 and 2). In general, when China’s economic and profit growth accelerates, share prices can rise with higher interest rates. Share prices can still climb with cuts in interest rates even when economic growth slows but profit growth rate remains in positive territory. However, when profit growth is expected to drop below zero, share prices will drop even if rates are falling (Chart 6A and 6B). In this vein, the most pertinent reason for Chinese stocks to move in tandem with bond yields is that Chinese stocks are increasingly driven by economic fundamentals, which are supported by the volume of total credit creation (measured by total social financing) rather than the price of money in China. Furthermore, the reverse relationship between the volume and price of money in China broke down after 2015; China’s credit creation has become less sensitive to changes in interest rates. Chart 6AWhen Interest Rates Rise...

When Interest Rates Rise...

When Interest Rates Rise...

Chart 6B...Economic Growth Holds The Key For Stock Performance

...Economic Growth Holds The Key For Stock Performance

...Economic Growth Holds The Key For Stock Performance

Since 2015, the PBOC shifted its policy to target interest rates instead of the quantity of money supply (Chart 7). In order to effectively manage the official interbank rates (the 7-day interbank repo rate), the central bank uses tools such as reserve requirement ratio cuts and liquidity injections in the interbank system (Chart 8). In other words, the central bank has forgone its control of the volume of money. Moreover, since late 2016, rather than direct interest rate hikes, the PBoC has been taking monetary policy tightening measures through changes in its macro-prudential assessment (MPA). The changes in the MPA are evident in the 3-month / 1-week repo spread.5 As such, an increase in the 3-month interbank repo rate (and SHIBOR) is often intended to curb shadow-banking activities rather than depress aggregate credit creation and business activities (Chart 9). Chart 7Monetary Policy Regime Shifted In 2015

Monetary Policy Regime Shifted In 2015

Monetary Policy Regime Shifted In 2015

Chart 8More Open Market Operations

Monetary Tightening ≠ Lower Stock Prices

Monetary Tightening ≠ Lower Stock Prices

Chart 9Most Monetary Tightening Has Been Carried Out Through MPA Since 2016

Most Monetary Tightening Has Been Carried Out Through MPA Since 2016

Most Monetary Tightening Has Been Carried Out Through MPA Since 2016

Another idiosyncrasy is China’s fiscal stimulus, which has become a more relevant driver of total social financing since the onset of the 2014/15 economic downcycle (Chart 10). The amount of government bond issuance is specified by the People’s Congress in March each year and is not affected by changes in interest rates or bond yields. Therefore, growth in total social financing can still accelerate despite a higher price of money (Chart 11). Chart 10Fiscal Lever Has Become More Prominent In Driving Business Cycles Since 2015

Fiscal Lever Has Become More Prominent In Driving Business Cycles Since 2015

Fiscal Lever Has Become More Prominent In Driving Business Cycles Since 2015

Chart 11Changes In Interest Rates Have Little Impact On Fiscal And Quasi-Fiscal Borrowing

Changes In Interest Rates Have Little Impact On Fiscal And Quasi-Fiscal Borrowing

Changes In Interest Rates Have Little Impact On Fiscal And Quasi-Fiscal Borrowing

By the same token, a rising 3-month SHIBOR can also be the result of rapid fiscal and quasi-fiscal expansions, as seen in Q3 this year. A flood of central and local government bond issuance drained liquidities from commercial banks, boosting the banks’ needs to borrow money from the interbank system. Nevertheless, the market’s appetite for risk assets increases because fiscal stimulus provides an imminent and powerful reflationary force in China’s business cycles. Chart 12Bank Lending Rates Can Still Trend Downwards Against A Rising Policy Rate

Bank Lending Rates Can Still Trend Downwards Against A Rising Policy Rate

Bank Lending Rates Can Still Trend Downwards Against A Rising Policy Rate

Rising policy rates typically push up corporate bond yields. However, bond yields in China play a relatively small role in driving corporate financing costs on an aggregate level, since commercial banks are still dominant in China’s debt market. Commercial banks' average lending rates closely track the PBoC’s policy rate on a cyclical basis, but Chinese authorities periodically use window guidance to target the Loan Prime Rate (LPR), a reformed bank lending rate. Hence, the direction in both the LPR and the average lending rate can temporarily diverge from the policy rate. These measures can boost bank loan growth even in a rising interest rate environment (Chart 12). Bottom Line: The key driver of Chinese stock performance is the country’s domestic credit, business, and corporate profit growth cycles. Since the 2014/15 cycle, the policy rate has not been the determinant of China’s economic or credit growth. Investment Conclusions We expect that this year’s massive monetary and fiscal stimulus to accelerate the country’s economic recovery into 1H21. Therefore, even if interest rates and bond yields advance, Chinese stock prices can still trend upward. Chinese cyclical stocks should also continue to outperform defensives, in both the onshore and offshore markets (Chart 13A and 13B). Chart 13AStay Invested In Chinese Stocks

Stay Invested In Chinese Stocks

Stay Invested In Chinese Stocks

Chart 13BCyclicals Still Have Upside Potentials

Cyclicals Still Have Upside Potentials

Cyclicals Still Have Upside Potentials

Rates will begin to climb and fiscal policy will also become more restrictive if China’s output moves above trend growth through 1H21. Government bond quotas and fiscal budget will be determined at the National People’s Congress in March. If the economy is strong, odds are that fiscal stimulus will be scaled back. At that point, investors should start to look for a peak in China’s business cycle linked to monetary and fiscal policy tightening. As growth expectations start to downshift in the equity market, yields on long-dated government bonds will start to decline while yields on the short end will not drop. Additionally, the small-cap ChiNext market has been considered as a speculative segment of the domestic financial market with higher multiples and greater volatility than large-cap A shares. The bourse's trailing price-to-earnings ratio and price-to-book ratio are extremely elevated at 79 and 8.6, respectively, much higher than for broader onshore and offshore Chinese stocks. As such, this market will remain the most vulnerable to domestic liquidity tightening. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 based on our estimates for 1h21: 7.5-8.0% GDP growth, 2.5-2.8% headline CPI, 6.5-6.7 USD/CNY, and the fed holding current fund rate unchanged. 2Please see China Investment Strategy Weekly Report "China Macro And Market Review," dated October 7, 2020, available at cis.bcaresearch.com 3Please see China Investment Strategy Weekly Report "Don’t Chase China’s Bond Yields Lower," dated February 19, 2020, available at cis.bcaresearch.com 4On October 12, the PBoC removed financial institutions’ Forex reserve ratio of 20%, making betting against the RMB cheaper. 5Please see China Investment Strategy Special Report "Seven Questions About Chinese Monetary Policy," dated February 22, 2018, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Highlights Duration: Prospects for more pre-election fiscal stimulus are slim. But with the Democrats gaining ground in the polls, the bond market will stay focused on rising odds of a blue sweep election and greater fiscal stimulus in early 2021. Municipal Bonds: Municipal bonds offer exceptional value relative to both US Treasuries and corporate credit. Not only that, but rising odds of a blue sweep election make state & local government fiscal relief increasingly likely. Investors should overweight municipal bonds in US fixed income portfolios. Economy: The economic recovery continues to roll on, but it will be some time before the output gap is closed and inflation starts to rise. Slow consumer and corporate credit growth suggest that animal spirits have not yet taken hold. Meanwhile, the falling unemployment rate masks a persistent uptrend in the number of permanently unemployed. Feature Chart 1Breakout

Breakout

Breakout

After having been lulled to sleep by several months of stagnant yields, bond investors experienced a minor shockwave in early October. The 10-year Treasury yield and 2/10 slope both broke out of well-established trading ranges and implied interest rate volatility bounced off all-time lows to reach its highest level since June (Chart 1). We suspect this might turn out to be just the first small tremor in a tumultuous month leading up to the US election. Specifically, there are two main political risks that will be resolved within the next month. Both have major implications for the bond market. Bond-Bullish Risk: No More Stimulus Before The Election The first risk is the possibility that the current Congress will not deliver any more fiscal stimulus. This increasingly looks like less of a possibility and more of a likelihood, especially after the president tweeted that he is halting negotiations with House Democrats. While he partially walked those comments back the next day, the fact remains that there is very little time between now and November 3rd, and the two sides remain at loggerheads. We have argued that more household income support from Congress is necessary. Otherwise, consumer spending will massively disappoint during the next year.1 However, it could take a few more months before this becomes apparent in the consumer spending data. Real consumer spending still rose in August, though much less quickly than it did in June and July (Chart 2). Meanwhile, August disposable income remained above pre-COVID levels, as it continued to receive a boost from facilities related to the CARES act (Chart 2, bottom panel). This boost will fade as the CARES act’s money is doled out, pushing spending lower. That is, unless Congress enacts a follow-up bill. There are two main political risks that will be resolved within the next month and both have major implications for the bond market. It looks less and less likely that a bill will be passed this month but, depending on the election outcome, a follow-up stimulus bill could become more likely in January. If consumer spending can hang in for the next couple of months, then the bond market might look past Congress’ near-term failure. This appears to be what is happening so far. The stock market fell 1.4% last Tuesday after Trump tweeted about halting negotiations. The 10-year Treasury yield, however, dropped only 2 bps on the day. More generally, long-dated bond yields rose during the past month, even as stocks sold off and prospects for immediate fiscal relief dimmed (Chart 3). Chart 2September's Consumer Spending Report Is Critical

September's Consumer Spending Report Is Critical

September's Consumer Spending Report Is Critical

Chart 3Bonds Ignore Stock ##br##Market...

Bonds Ignore Stock Market...

Bonds Ignore Stock Market...

With all that in mind, we think September’s consumer spending data – the last month of data we will see before the election – are very important. If spending collapses, it might re-focus the market’s attention on Congress’ failure, sending bond yields down. However, we think the market would see through a modest drop in spending, especially if the election looks poised to bring us a larger bill in 2021. Bond-Bearish Risk: A Blue Sweep Election Chart 4...Take Cues From Election Odds

...Take Cues From Election Odds

...Take Cues From Election Odds

This brings us to the second big political risk that could influence bond yields during the next month: The possibility of a “blue sweep” election where the Democrats win control of the House, Senate and White House. This would clearly be a bearish outcome for bonds, as an unimpeded Democratic party would enact a large stimulus package – likely worth $2.5 to $3.5 trillion – shortly after inauguration. It appears that the bond market is already tentatively pricing-in this outcome. While the recent increase in bond yields is hard to square with weak equity prices and souring expectations for immediate stimulus, it is consistent with rising betting market odds of a blue sweep election (Chart 4). To underscore the bond bearishness of this potential election outcome, consider that not only would a unified Congress be able to quickly deliver another fiscal relief bill, but Joe Biden’s platform calls for even more spending on infrastructure, healthcare, education and other Democratic priorities. In total, Biden is proposing new spending of around 3% of GDP, only about half of which will be offset by tax increases (Table 1). Table 1ABiden Would Raise $4 Trillion In Revenue Over Ten Years

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Table 1BBiden Would Spend $7 Trillion In Programs Over Ten Years

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Political Risk Will Dominate In A Pivotal Month For The Bond Market

How likely is a “blue sweep” election? It is our Geopolitical Strategy service’s base case.2 Also, fivethirtyeight.com’s poll-based forecasting model sees a 68% chance that Democrats win the Senate, a 94% chance that they win the House and an 85% chance that Joe Biden wins the presidency. Investment Strategy These two political risks appear to put bond investors in a bit of a conundrum. On the one hand, if no stimulus bill is passed this month and September’s consumer spending data are weak, then bond yields could fall in the near-term. However, we are inclined to think that if all that occurs against the back-drop of rising odds of a blue sweep election outcome, the bond market will look beyond the near-term and yields will move higher on expectations of larger stimulus coming in January. As such, we retain our relatively pro-reflation investment stance. We recommend owning nominal and real yield curve steepeners, inflation curve flatteners and maintaining an overweight position in TIPS versus nominal Treasuries. All these positions are designed to profit from a rising yield environment.3 Municipal bonds look extremely cheap compared to other US fixed income sectors. We retain an “at benchmark” portfolio duration stance for now, for two reasons. First, while a blue sweep election outcome looks like the most likely scenario, it is not a guarantee. Second, even against the backdrop of greater government stimulus and continued economic recovery, the US economy will still be dealing with a large output gap next year that will temper inflationary pressures. This will keep the Fed on hold, limiting the upside in bond yields. That being said, the odds of another significant downleg in bond yields look increasingly slim. We will likely shift to a more aggressive “below-benchmark” duration stance this month, if our conviction in a blue sweep election outcome continues to rise. A Rare Buying Opportunity In Municipal Bonds No matter how you slice it, municipal bonds look extremely cheap compared to other US fixed income sectors. First, we can look at the spread between Aaa-rated munis and maturity-matched US Treasury yields (Chart 5). When we do this, we find that 2-year and 5-year municipal bonds trade at about the same yields as their Treasury counterparts. This is despite municipal debt’s tax-exempt status. Munis look even more attractive further out the curve, with 10-year and 30-year bonds trading at a before-tax premium relative to Treasuries. Chart 5Aaa Munis Versus ##br##Treasuries

Aaa Munis Versus Treasuries

Aaa Munis Versus Treasuries

Table 2Muni/Corporate Breakeven Effective Tax Rates (%)

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Next, we can look at how municipal bonds stack up compared to corporates. We do this in a couple different ways. In Table 2, we start with the Bloomberg Barclays Investment Grade Corporate Index split by credit tier. We then find the General Obligation (GO) municipal bond that matches each corporate index’s credit rating and maturity and calculate the breakeven effective tax rate between the two yields. The breakeven effective tax rate is the effective tax rate that would make an investor indifferent between owning the municipal bond and the corporate bond. For example, if an investor faces an effective tax rate of 7%, they will observe the same after-tax yield in a 12-year A-rated GO municipal bond as they do in a 12-year A-rated corporate bond. If their effective tax rate is more than 7%, the muni offers an after-tax yield advantage. Alternatively, we can look at the relative value between munis and credit using the Bloomberg Barclays Municipal Indexes. In Chart 6A, we start with the average yield on the Bloomberg Barclays General Obligation indexes by maturity. We then find the US Credit index that matches the credit rating and duration of the municipal index and calculate the yield differential.4 We find that in all cases, for GO bonds ranging from 6 years to maturity and higher, the muni offers a before-tax yield advantage compared to the Credit Index. This is also true when we perform the same exercise using municipal revenue bonds instead of GOs (Chart 6B). Chart 6AGO Munis Versus Credit

GO Munis Versus Credit

GO Munis Versus Credit

Chart 6BRevenue Munis Versus Credit

Revenue Munis Versus Credit

Revenue Munis Versus Credit

You may notice that municipal bonds trade at a before-tax premium to credit in Charts 6A and 6B, but at a discount in Table 2. This is because we compare bonds by maturity in Table 2 and by duration in Charts 6A and 6B. Unlike investment grade corporates, municipal bonds often carry call options making them negatively convex and giving them a duration that is much shorter than their maturity. Cheap For A Reason, Or Just Plain Cheap? Chart 7State & Local Balance Sheets Will Weather The Storm

State & Local Balance Sheets Will Weather The Storm

State & Local Balance Sheets Will Weather The Storm

We have effectively demonstrated that municipal bonds offer value relative to both Treasuries and corporate credit. But attractive value is not enough to warrant an overweight allocation. Ideally, we would also like some degree of confidence that wide spreads won’t eventually be justified by a wave of downgrades and defaults. While state & local government balance sheets are certainly stressed, we see strong odds that the muni market will emerge from the COVID recession relatively unscathed. For starters, state & local governments were experiencing strong revenue growth prior to the pandemic (Chart 7, top panel). This allowed them to build rainy day funds up to all-time highs (Chart 7, panel 4). Second, income support for households from the CARES act helped prop up state & local income tax revenues in the second quarter (Chart 7, panel 2), though sales tax revenues took a significant hit (Chart 7, panel 3). Going forward, a blue sweep election scenario would not only provide more income support for households – helping income tax revenues – but a Democratic controlled Congress would also quickly deliver fiscal aid directly to state & local governments. In fact, it is this aid for state & local governments that is currently the key sticking point in fiscal negotiations. In the meantime, state & local governments will continue to clamp down on spending. This can already be seen in the massive drop in state & local government employment (Chart 7, bottom panel). This is obviously a drag on economic growth, but the combination of austerity measures and high rainy day fund balances will help municipal bonds avoid downgrades and defaults, at least until a fiscal relief bill is passed next year. While state & local government balance sheets are certainly stressed, we see strong odds that the muni market will emerge from the COVID recession relatively unscathed. Bottom Line: Municipal bonds offer exceptional value relative to both US Treasuries and corporate credit. Not only that, but rising odds of a blue sweep election make state & local government fiscal relief increasingly likely. Investors should overweight municipal bonds in US fixed income portfolios. Economy: Credit Growth & The Labor Market Credit Growth Slowing Chart 8No Animal Spirits

No Animal Spirits

No Animal Spirits

Of notable economic data releases during the past two weeks, we find it particularly interesting that both consumer credit and Commercial & Industrial (C&I) bank lending continue to slow (Chart 8). On the consumer side, massive income support from the CARES act and few spending opportunities caused households to pay down debt this spring. Then, after two months of modest gains, consumer credit fell again in August (Chart 8, top panel). This strongly suggests that, even as lockdown restrictions have eased, consumers aren’t yet ready to open up the spending taps. On the corporate side, firms received much less of a direct cash injection from Congress and were forced to take on massive amounts of debt to get through the spring and early summer months. But as of the second quarter, we recently observed that nonfinancial corporate retained earnings now exceed capital expenditures.5 This strongly suggests that firms have taken out enough new debt and that C&I bank lending will remain slow in the coming months. Cracks Showing In The Labor Market Chart 9Far From Full Employment

Far From Full Employment

Far From Full Employment

Finally, we should mention September’s employment report that was released two weeks ago (Chart 9). It is certainly positive that the unemployment rate continues to fall, but the main takeaway for bond investors should be that the US economy remains far from full employment, and therefore far away from generating meaningful inflationary pressure. While the unemployment rate fell for the fifth consecutive month, it is now dropping much less quickly than it did early in the summer (Chart 9, panel 2). Also, we continue to note that labor market gains are entirely concentrated in temporarily unemployed people returning to work. The number of permanently unemployed continues to rise (Chart 9, bottom panel). Bottom Line: The economic recovery continues to roll on, but it will be some time before the output gap is closed and inflation starts to rise. Slow consumer and corporate credit growth suggest that animal spirits have not yet taken hold. Meanwhile, the falling unemployment rate masks a persistent uptrend in the number of permanently unemployed. Appendix The Fed rolled out a number of aggressive lending facilities on March 23. These facilities focused on different specific sectors of the US bond market. The fact that the Fed has decided to support some parts of the market and not others has caused some traditional bond market correlations to break down. It has also led us to adopt of a strategy of “Buy What The Fed Is Buying”. That is, we favor those sectors that offer attractive spreads and that benefit from Fed support. The below Table tracks the performance of different bond sectors since the March 23 announcement. We will use this to monitor bond market correlations and evaluate our strategy’s success. Table 3Performance Since March 23 Announcement Of Emergency Fed Facilities

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Political Risk Will Dominate In A Pivotal Month For The Bond Market

Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “More Stimulus Needed”, dated September 15, 2020, available at usbs.bcaresearch.com 2 Please see Geopolitical Strategy Weekly Report, “It Ain’t Over Till It’s Over”, dated October 9, 2020, available at gps.bcaresearch.com 3 For more details on these recommended positions please see US Bond Strategy Weekly Report, “Positioning For Reflation And Avoiding Deflation”, dated August 11, 2020, available at usbs.bcaresearch.com 4 Note that we use the US Credit Index in Charts 6A and 6B. This index includes the entire US corporate bond index but also some non-corporate credit sectors like Sovereigns and Foreign Agency bonds. 5 Please see US Bond Strategy Weekly Report, “Out Of Bullets”, dated September 29, 2020, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Both public opinion polls and betting markets suggest that Joe Biden will become President, with the Democrats gaining control of the Senate and retaining the House of Representatives. Such a “blue wave” would have mixed effects on the value of the S&P 500. On the one hand, corporate taxes would rise under a Biden administration. On the other hand, trade relations with China would improve. The Democrats would also push for more fiscal stimulus, which the stock market would welcome. The odds of Republicans and Democrats agreeing on a major new stimulus deal before the November elections look increasingly slim. In a blue wave scenario, the Democrats will enact $2.5-to-$3.5 trillion in pandemic relief shortly after Inauguration Day. Joe Biden‘s platform also calls for around 3% of GDP in additional spending on infrastructure, health care, education, climate, housing, and other Democratic priorities. Unlike in late 2016, the Fed is in no mood to raise interest rates. Large-scale fiscal easing will push down the value of the US dollar, while giving bond yields a modest boost. Non-US stocks will outperform their US peers. Value stocks will outperform growth stocks. Looking further out, Republicans will move to the left on economic issues, leaving corporate America with no clear backer among the two major parties. As such, while we are constructive on equities over the next 12 months, we see grave dangers ahead later this decade. Look, Here's The Deal: Joe Biden Is In The Lead With four weeks remaining until the US presidential election, Joe Biden remains on course to become the 46th president of the United States. According to recent public opinion polls, the former vice president leads Donald Trump by 10 percentage points nationwide, and by 4 points in battleground states (Chart 1). Far fewer voters are undecided today compared to 2016. This suggests that there is less scope for President Trump to narrow his deficit in the polls. Betting markets give Biden a 68% chance of prevailing in the race for the White House (Chart 2). They also assign a 67% probability that the Democrats will take control of the Senate and 89% odds that they will retain their majority in the House of Representatives. Chart 1Opinion Polls Favor Biden ...

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Chart 2.... As Do Betting Markets

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Mixed Impact On The S&P 500 What would the market implications of a “blue wave” be? Our sense is that the overall impact on the value of the S&P 500 would be small, largely because some negative repercussions from a Democratic sweep would be offset by positive repercussions. On the negative side, Biden has pledged to raise the corporate income tax rate from 21% to 28%, bringing it halfway back to the 35% rate that prevailed in 2017. He has also promised to introduce a minimum of 15% tax on the income that companies report in their financial statements to shareholders, raise taxes on overseas profits, and lift payroll taxes on households with annual earnings in excess of $400,000. Together, these measures would reduce S&P 500 earnings-per-share by 9%-to-10%. On the positive side, while geopolitical tensions will persist, US trade relations with China would likely improve if Joe Biden were to become the president. Biden has roundly criticized Trump’s tariffs, saying that they are “crushing farmers” and “hitting a lot of American manufacturing… choking it to within an inch of its life.”1 He has pledged to honor multilateral agreements. The World Trade Organization concluded on September 15 that Trump’s tariffs violated international trade rules. This judgement and the desire to turn the page on the Trump era could give Biden the impetus to eventually roll back some of the tariffs. In contrast, having been stricken by what he has called the “China virus,” Trump could take things personally and retaliate with a flurry of new punitive measures. Fiscal policy would be further loosened in a blue wave scenario, an outcome that the stock market would welcome. Voters would also applaud more pandemic relief. Table 1 shows that 72% of Americans, including the majority of Republicans, support the broader contours of the $2 trillion stimulus package that President Trump has rejected. Table 1Voters Support A New $2 Trillion Coronavirus Stimulus Package By A Fairly Wide Margin

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

At this point, the odds of Republicans and Democrats agreeing on a major new stimulus deal before the November elections look increasingly slim. If Biden wins and the Republicans lose control of the senate, the Democrats would likely enact a stimulus package worth $2.5-to-$3.5 trillion shortly after Inauguration Day on January 20. In addition to pandemic-related stimulus, Joe Biden has called for around 3% of GDP in spending on infrastructure, health care, education, climate, housing, and other Democratic priorities. Only about half of those expenditures would be matched by higher taxes, implying substantial net stimulus for the economy. A Weaker Dollar And Modestly Higher Bond Yields The greenback jumped on Tuesday after President Trump said he is breaking off negotiations with the Democrats over a new stimulus bill. This suggests that the dollar will weaken if fiscal policy is loosened. If that were to happen, it would be different from what transpired following Trump’s victory in 2016 when the dollar strengthened. Why the disconnect between now and then? The answer has to do with the outlook for monetary policy. Back then, the Fed was primed to start raising rates again – it hiked rates eight times beginning in December 2016, ultimately bringing the fed funds rate to 2.5% by end-2018 (Chart 3). This time around, the Fed is firmly on hold, with the vast majority of FOMC members expecting policy rates to stay at rock-bottom levels until at least 2023. This suggests that nominal bond yields will rise less than they did in late 2016. Since inflation expectations will likely move up in response to more stimulative fiscal policy, real yields will rise even less than nominal yields. Over the past 18 months, US real rates have fallen a lot more in relation to rates abroad than what one would have expected based on the fairly modest depreciation in the US dollar (Chart 4). If US real rates remain entrenched deep in negative territory, while the US current account deficit widens further on the back of strong domestic demand, the dollar will continue to weaken. Chart 3Trump Victory Was Followed By Rising Interest Rates

Trump Victory Was Followed By Rising Interest Rates

Trump Victory Was Followed By Rising Interest Rates

Chart 4A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

A Relatively Muted Decline In The Dollar Given The Move In Real Yield Differentials

Favor Non-US And Value Stocks Non-US stocks typically outperform their US peers when the dollar is weakening (Chart 5). This partly stems from the fact that cyclical stocks are overrepresented in stock markets outside of the United States. It also reflects the fact that cash flows denominated in say, euros or yen, are worth more in dollars if the value of the dollar declines. Chart 5A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

A Weaker Dollar Tends To Benefit Cyclical And Non-US Stocks

Financial stocks are overrepresented outside the US (Table 2). They are also overrepresented in value indices (Table 3). While a Biden administration would subject the largest US banks to additional regulatory scrutiny, the impact on their bottom lines would likely be small. US banks have been living under the shadows of the Dodd-Frank Act for over a decade. Today, banks operate more as stable utilities than as cavalier casinos. Table 2Financials Are Overrepresented In Ex-US Indexes, While Tech Dominates The US Market

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Table 3Financials Are Overrepresented In Value, While Tech Dominates Growth Indexes

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Stronger stimulus-induced growth next year will allow many banks to release some of the hefty provisions against bad loans that they built up this year, while modestly steeper yields curves will boost net interest margins. Tech stocks are overrepresented in growth indices. Better trade relations would help US tech companies, as would a weaker dollar. That said, Joe Biden’s plan to increase taxes on overseas profits would hit tech companies disproportionately hard since the tech sector derives over half its revenue from outside the United States. Stepped up antitrust enforcement and more stringent privacy rules could also weigh on tech profits. On balance, while there are many moving parts, a Democratic sweep would favor non-US equities over US equities, and value stocks over growth stocks. Trumpism Transcends Trump Chart 6Trump Targeted Socially Conservative Voters

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

In 2016, we bucked the consensus view that Hillary Clinton would win the election. On September 30, 2016, we predicted that “Trump will win and the dollar will rally,” noting that “Trump has seen a huge (yuge?) increase in support among working-class whites. If the so-called “likely voters” backing Clinton are, in fact, less likely to turn out at the polls than those backing Trump, this could skew the final outcome in Trump's favor.”2 Right-wing populism was the $1 trillion bill lying on the sidewalk that no mainstream Republican politician seemed eager to pick up. According to the Voter Study Group, only 4% of the US electorate identified as socially liberal and fiscally conservative in 2016, compared to 29% who saw themselves as fiscally liberal and socially conservative (Chart 6). The latter group had no political home, at least until Donald Trump came along. Rather than waxing poetically about small government conservatism – as most establishment Republicans were wont to do – Trump railed against mass immigration, unfair trade deals, rising crime, never-ending wars, and what he described as out-of-control political correctness. While Trump was able to carry out parts of his protectionist agenda, most of his other actions fell well short of what he had promised. His only major legislative achievement was a massive tax cut for corporations and wealthy individuals – something that the vast majority of his base never asked for. The Rich Are Flocking To The Democratic Party How did corporations and wealthy Americans reward Trump for lowering their taxes? By shifting their allegiances towards the Democrats, that’s how. According to the Pew Research Center, households earning more than $150,000 favored Democrats by 20 percentage points during the 2018 Congressional elections, a 13-point jump from 2016. Households earning between $30,000 and $149,999 favored Democrats by only 6 points in 2018. The only other income group that strongly favored Democrats were those earning less than $30,000 per year (Table 4). Table 4Democratic Candidates Had Wide Advantages Among The Highest-And-Lowest Income Voters

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Chart 7Democratic Districts Have Fared Better Over The Past Decade

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Other data tell a similar story. Median household income in Democratic congressional districts rose by 13% between 2008 and 2017. It fell by 4% in Republican districts. Today, on average, Republican districts have a median income that is 13% below Democratic districts (Chart 7). Campaign donations have shifted towards the Democrats. The latest monthly fundraising data shows that the Biden campaign received three times more large-dollar contributions in total than the Trump campaign. The nation’s CEOs have not been immune from this transformation. Seventy-seven percent of the business leaders surveyed by the Yale School of Management on September 23 said they would be voting for Joe Biden.3 As elites desert the Republican Party, will the Democratic Party start championing lower taxes and less regulation? That seems unlikely. According to the Voter Study Group, higher-income Democrats are actually more likely to support raising taxes on families earning more than $200,000 per year than lower-income Democrats (83% versus 79%). Among Republicans, the opposite is true: 45% of lower-income Republicans are in favor of raising taxes, compared to only 23% of higher-income Republicans.4 There used to be a time when companies tried to steer clear of the political limelight. This is starting to change. As the relative purchasing power of Democratic voters has risen, many companies have become emboldened to adopt overtly political stances on a variety of hot-button social and cultural issues, even if those stances alienate many conservative customers. What does this imply for investors? If big business abandons conservative voters, conservative voters will abandon big business. Corporate America will be left with no clear backer among the two major parties. Over the long haul, this is likely to be bad news for equity investors. As such, while we are constructive on equities over the next 12 months, we see grave dangers ahead later this decade. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 “Biden Takes On ‘Trump’s Tariffs’,” The Wall Street Journal, June 12, 2019. 2 Please see Global Investment Strategy Special Report, “Three (New) Controversial Calls,” dated September 30, 2016. 3 “CEO Caucus Survey: Business Leaders Fault Trump Administration on COVID and China,” Yale School of Management, September 24, 2020. 4 Lee Drutman, Vanessa Williamson, Felicia Wong, “On the Money: How Americans’ Economic Views Define — and Defy — Party Lines,” votersstudygroup.org, June 2019. Global Investment Strategy View Matrix

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Current MacroQuant Model Scores

Market Implications Of A Blue Wave

Market Implications Of A Blue Wave

Highlights President Trump is waffling on fiscal relief. Our constraints-based framework still points to a deal, but the odds have clearly fallen. US and global stocks have rallied despite the fiscal failure. Markets evidently believe stimulus is coming regardless, particularly if Democrats win a blue sweep – our base case election scenario. However, our quantitative election model has boosted Republican odds, flagging a major risk to the blue sweep scenario. Moreover a blue sweep will remove checks and balances on the new administration and thus bring negative surprises that the market is underrating. We maintain our tactical risk-off positioning on the expectation of another leg of election-related volatility. Over a 12-month time horizon we remain invested in reflation plays. Feature Financial markets came around to our “blue sweep” base case for the US election this week. Betting markets shifted sharply after the first presidential debate (Chart 1). Support for Biden surged in national opinion polls while Trump dropped off, albeit to a lesser extent in swing states. Worryingly for the White House, the few polls taken since Trump took ill with COVID-19 on October 2 do not show a sympathy bounce for the president (Chart 2). Chart 1Consensus Forms Around ‘Blue Sweep’ Base Case

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Chart 2Trump Takes A Dive With Little Time On Clock

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

In a very dangerous turn for the president’s re-election chances, Trump discontinued negotiations with House Democrats over a fiscal relief bill, promising to pass a large new stimulus after the election. Partially walking back those comments, he said he would sign any targeted stimulus bills that Congress sends him in the meantime (such as a new round of $1,200 rebates for households). House Speaker Nancy Pelosi shot down the option of a skinny bill, as we have argued she would. Now they are going back and forth. While the S&P 500 rallied on the news, other reflation trades like US cyclicals, oil, and silver show the risk of premature fiscal tightening (Chart 3). Investors may have to wait until late January until getting a new infusion of government support. Chart 3Lack Of Stimulus Still A Risk To Reflation Trades

Lack Of Stimulus Still A Risk To Reflation Trades

Lack Of Stimulus Still A Risk To Reflation Trades

Chart 4Market Rally Not Based On Blue Sweep Odds

Market Rally Not Based On Blue Sweep Odds

Market Rally Not Based On Blue Sweep Odds

True, a fiscal deal could be passed in the lame duck session in November or December, but Republican Senators unwilling to pony up around $500 billion to bail out blue states – when they face a possible wipeout in a historic election – will be even less willing if they lose the election. They will be more hawkish since they will want to pin deficits on the Democrats in future. If Republicans retain control of the Senate despite the latest news – which is possible, especially given the Democratic candidate’s new vulnerability in the North Carolina race due to a sex scandal – then investors have two years of fiscal hawkishness to contend with. Diagram 1 highlights the market implications of this Senate risk. Diagram 1Scenarios For US Election Outcomes And Market Impacts

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

So we need to look elsewhere to explain why the market rallied when odds of a fiscal deal fell. The above reasoning leaves us with the following options: The economy is recovering so robustly that new fiscal stimulus is unnecessary. This is not the view of Federal Reserve Chairman Jay Powell, who all but pleaded for Congress to conclude a deal to secure the recovery, or of other mainstream economists. Stimulus is coming regardless of election outcome. Congress will be forced to support the country during a slump. Debt monetization is the relevant point, even if there is a month-or-two delay in stimulus. Financial markets are cheering the higher odds of a Democratic clean sweep of Congress and the White House since it implies fiscal largesse. The market may already have discounted some of the impending tax hikes over the past month. The second explanation is the best but the third is rapidly becoming the new consensus on Wall Street. Chart 4 suggests there is no connection between the S&P rally and the odds of a blue sweep. With the Fed pursuing “maximum employment” and average inflation targeting, it makes sense that the real mover in the macro landscape has become fiscal policy. Hence the outcome that produces the most proactive fiscal policy is positive for financial markets. A blue sweep is verification of the shift toward debt monetization, which is missing from option two above. The problem is that a blue sweep also brings downside risks. Domestic policy uncertainty will only fall temporarily after the election if there is a blue sweep. Checks and balances will vanish. Eventually Democrats will become overweening in their policy agenda, delivering negative surprises to financial markets. A “New Deal”-style policy agenda would weigh on the corporate earnings outlook. For example, Democrats have refused to forswear removing the filibuster or stacking the Supreme Court, both of which would lie in their power and either of which would enable them to pass an ambitious “New Deal”-style policy agenda that would bring unforeseen consequences – largely in the direction of wealth redistribution away from corporations. Table 1What EPS Hit To Expect?

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Redistribution would start to correct US social and economic imbalances, improve middle class spending power, and boost consumption – but it would first weigh on the corporate earnings outlook. Net profit growth, which grew by 16% above what was otherwise expected due to the Trump tax cuts (Chart 5), could suffer more than the expected 11% one-off contraction (Table 1), as our US equity strategist Anastasios Avgeriou has shown. Chart 5Partial Repeal Of Trump Tax Cut Bad For Earnings

Partial Repeal Of Trump Tax Cut Bad For Earnings

Partial Repeal Of Trump Tax Cut Bad For Earnings

New proposals will also emerge that the market is not taking account of. To take just the latest example, former Fed Chair Janet Yellen recently stated that the US could adopt a $40 per ton tax on carbon emissions under a Biden administration.1This proposal is not part of Biden’s official plan, hence not priced by markets along with Biden’s expected tax hikes (Table 2). But control of the Senate would make it a real option given Biden’s ambitious climate goals. Table 2Biden Needs Senate To Raise Taxes

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

Consumer confidence in the US will suffer from political polarization. Recall that in 2016, the economy was in fine shape but Republicans did not believe it, weighing down the average until President Trump won the election. Today the economy is in a slump but Republicans may not recognize the bad news until President Trump loses. Democrats, for their part, will suddenly abandon their doom and gloom if Biden wins the election. Applying a comparable partisan shock to consumer confidence for 2021 would suggest that overall confidence will be lackluster (Chart 6). At least this is true until the passage of new stimulus and an advancing recovery outweigh the partisan effect. Chart 6Biden Will Not Recreate Trump Confidence Boost

It Ain’t Over Till It’s Over

It Ain’t Over Till It’s Over

A similar case can be made that small business sentiment will worsen in a blue sweep scenario. Fear of higher regulation and taxes will spike and weigh on animal spirits (Chart 7). Historically the first year after an election sees smaller equity upside and larger downside with unified government as opposed to divided government (Chart 8). If this time is different it is because of the sea change in the US to embrace debt monetization. But that sea change occurred under a Republican administration and is likely to persist due to the output gap. Chart 7SMEs Will Fear Blue Wave

SMEs Will Fear Blue Wave

SMEs Will Fear Blue Wave

Chart 8Stock Market Profile Fits Divided Government, Which Has More Upside

Stock Market Profile Fits Divided Government, Which Has More Upside

Stock Market Profile Fits Divided Government, Which Has More Upside