Policy

BCA Research's Geopolitical Strategy service maintains its high conviction call that a new spending bill will be passed, likely by August 10. Fresh fiscal stimulus is more positive for the cyclical outlook than the tactical outlook. Stimulus “hiccups”…

Dear Client, In lieu of our regular report next week, we will be sending you a Special Report from my colleague Garry Evans, Chief Global Asset Allocation Strategist. Garry will be discussing the social and industrial changes that will remain in place even after the COVID-19 pandemic is over, and how investors should tilt their portfolios to take advantage of them. I hope you find his report insightful. Best regards, Peter Berezin, Chief Global Strategist Highlights The number of coronavirus cases in the US appears to have peaked. Negotiations to avert a fiscal cliff continue in Washington. While we expect a deal to be reached, markets could tread nervously until this happens. The US dollar will weaken further over the next 12 months. Narrowing interest rate differentials, a revival in global growth, deteriorating momentum, and pricey valuations all bode poorly for the greenback. Global equities in general, and non-US stocks in particular, tend to fare well in a weak dollar environment. Small cap and value stocks usually outperform when the dollar weakens. Bank shares should start to do better as yield curves steepen and faster economic growth reduces concerns over non-performing loans. US Virus Wave Cresting, But Fiscal Risks Intensifying Chart 1US: Number Of New Cases Seems To Be Peaking

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Last week, we argued that the two biggest near-term threats to stocks and other risky assets were the rising number of coronavirus cases in parts of the US and the looming fiscal cliff.1 Since then, the news on the virus has been broadly positive, while developments on the fiscal front have been mixed. Chart 1 shows that the number of new cases seems to have peaked in the US. In Texas, Florida, California, and Arizona, the share of doctor visits linked to suspected Covid infections is trending lower. This metric leads diagnoses by about one-to-two weeks (Chart 2). Chart 2Doctor Visits, Which Lead Diagnoses, Are Trending Lower

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Over half the US population lives in states that have either suspended or reversed reopening plans (Chart 3). Assuming the number of infections keeps falling and fiscal policy is not unduly tightened, household spending and employment growth – which appear to have stalled out in the second half of July – should begin to pick up. Chart 3Not So Fast

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Unfortunately, the assumption that fiscal policy will remain stimulative looks somewhat shaky. Expanded unemployment benefits for 30 million Americans, consisting mainly of an additional $600 per week for unemployed workers, are set to expire at the end of July. Congressional Republicans have suggested trimming benefits to $200 per week. However, even that would represent a fiscal tightening of nearly 3% of GDP. A Question Of Incentives The Republican position is understandable, given that two-thirds of unemployed workers are currently receiving more in unemployment benefits than they earned while working. Thus, some scaling back of benefits is not only inevitable, but desirable. The question is one of timing. While job openings have risen from their lows, they are still 23% below where they were at the start of the year. According to the NFIB survey, the share of small businesses reporting difficulty in finding qualified workers has also fallen from year-ago levels. When the binding constraint on employment is a shortage of jobs rather than a shortage of workers, higher unemployment benefits will likely boost hiring. This is because increased benefits will increase spending on goods and services across the economy, thus augmenting the demand for labor. Debt, Gold, And The Dollar Chart 4Gold Prices Have Risen On The Back Of Falling Real Yields

Gold Prices Have Risen On The Back Of Falling Real Yields

Gold Prices Have Risen On The Back Of Falling Real Yields

Does the inevitable increase in government debt due to ongoing fiscal stimulus portend disaster down the road? According to many commentators, the recent drop in the dollar and the surge in gold prices is surely telling us that it does. While it is a compelling story, it is mainly false. The yield on the 30-year Treasury bond currently stands at 1.20%, down from 1.5% in mid-June and 2.33% at the start of the year. Bondholders may be many things, but masochistic is not one of them. If they really thought a fiscal crisis was around the corner, yields would be a lot higher. So why is the dollar falling and gold rallying? The answer is inflation expectations have risen off very low levels, which has pushed down real yields. Gold prices are almost perfectly correlated with real interest rates (Chart 4). The Real Reason The Dollar Has Fallen Going into this year, US real yields had a lot more room to decline than rates abroad. For example, at the start of 2019, US real 2-year yields were 221 bps above comparable euro area yields. Today, US real rates are 35 bps lower – a swing of 256 bps. Yield differentials have narrowed against other economies as well, which has pushed down the value of the dollar (Chart 5). In addition, relative growth dynamics have hurt the greenback. The US economy tends to be less cyclical than most of its trading partners. While the US benefits from faster global growth, the rest of the world benefits even more. This causes capital to flow from the US to other countries, leading to a weaker dollar (Chart 6). Chart 5The Greenback Has Been Losing Interest Rate Support

The Greenback Has Been Losing Interest Rate Support

The Greenback Has Been Losing Interest Rate Support

Chart 6The Dollar Usually Weakens When Global Growth Accelerates

The Dollar Usually Weakens When Global Growth Accelerates

The Dollar Usually Weakens When Global Growth Accelerates

Chart 7The Dollar And Cycles

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

BCA Research’s Foreign Exchange Strategist, Chester Ntonifor, has stressed that the dollar typically fares worst in the initial stages of business cycle recoveries (Chart 7). That is the stage we are in today. Indeed, the gap in growth between the US and the rest of the world is likely to be larger than usual over the next few quarters because the pandemic has hit the US harder than most other developed economies. Momentum is also working against the dollar. Being a contrarian is usually a smart investment strategy. That is not the case when it comes to trading the dollar. With the dollar, you want to follow the herd. This is because the dollar is a high momentum currency (Chart 8). A simple trading rule that buys the dollar when it is trading above its 50-day or 200-day moving average, and sells the dollar when it is trading below its respective moving averages, has historically made a lot of money. Likewise, the dollar performs best prospectively when sentiment is bullish and improving (Chart 9). Currently, the dollar is trading below its various moving averages. Sentiment is also poor and deteriorating (Chart 10). Chart 8USD Is A High Momentum Currency

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Chart 9Trading The Dollar: The Trend Is Your Friend

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Chart 10The Dollar Has Started Breaking Down

The Dollar Has Started Breaking Down

The Dollar Has Started Breaking Down

Chart 11The Dollar Is Still Fairly Expensive

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

If the dollar were cheap, all the factors discussed above could be overlooked. But the dollar is not cheap. It is still pricey based on purchasing power parity measures which compare the common-currency cost of identical consumption bundles from one country to the next (Chart 11). A Weaker Dollar is Bullish For Stocks, Especially Non-US Stocks Global equities in general, and non-US stocks in particular, tend to perform well when the dollar is weakening (Chart 12). Chart 12A Weaker Dollar Should Help Global Equities

A Weaker Dollar Should Help Global Equities

A Weaker Dollar Should Help Global Equities

Chart 13Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclicals Tend To Outperform Defensives In A Falling Dollar Environment

Cyclical sectors such as industrials, energy, and materials normally outperform defensives in a weak dollar environment (Chart 13). Relative profit growth in these sectors tends to rise when the dollar depreciates (Chart 14). To the extent that cyclicals are overrepresented in stock market indices outside the US, this gives non-US equities a leg up. Chart 14Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

Relative Profit Growth In Cyclical Sectors Tend To Rise When The USD Depreciates

EM Is The Big Winner From Dollar Weakness A weaker dollar is particularly beneficial to emerging markets. Commodity prices usually rise when the dollar drops (Chart 15). Rising resource prices are good news for many emerging markets. EM debt dynamics also tend to improve when the dollar weakens. EM external debt has grown in recent years (Chart 16). About 80% of EM foreign currency denominated debt is in dollars. A falling dollar reduces the local-currency value of US dollar-denominated liabilities, thus strengthening the balance sheets of many EM companies and governments. Emerging markets with large current account deficits and significant dollar liabilities such as Brazil, Indonesia, Turkey, and Mexico will outperform EMs that generally run current account surpluses and have little in the way of foreign-currency debt. Chart 15Commodity Prices Usually Rise When The Dollar Falls

Commodity Prices Usually Rise When The Dollar Falls

Commodity Prices Usually Rise When The Dollar Falls

Chart 16EM External Debt Has Grown In Recent Years

EM External Debt Has Grown In Recent Years

EM External Debt Has Grown In Recent Years

The Federal Reserve today is trying to engineer an easing in US financial conditions. A weaker dollar is facilitating that goal. Historically, EM stocks have been almost perfectly inversely correlated with US financial conditions (Chart 17). Chart 17EM Equities Benefit From Easier US Financial Conditions

EM Equities Benefit From Easier US Financial Conditions

EM Equities Benefit From Easier US Financial Conditions

What About DM? The impact of a weaker dollar on the stock markets of developed economies is more nuanced. Consider the euro area, for example. On the one hand, a stronger euro hurts the euro area economy, which can ultimately push down domestic profits. A stronger EUR/USD also reduces the profits of European companies with operations in the US when those profits are converted back into euros. That can also hurt European stocks. On the other hand, the overall reflationary effect of a weaker dollar on global growth tends to push up profits. In practice, the latter effect usually dominates the former. Thus, euro area stocks, just like stocks in most other markets, generally outperform the US when the dollar is weakening (Chart 18). Chart 18ANon-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Non-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Non-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Chart 18BNon-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Non-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Non-US Stock Markets Do Well Vis-À-Vis The US When The Dollar Is Weakening

Small Caps And Value Stocks Tend To Outperform When The Dollar Weakens Even though companies in the small cap Russell 2000 index generate less of their sales from abroad than those in the S&P 500, small caps still tend to outperform large caps in weak dollar environments (Chart 19). This is partly because smaller companies are more cyclical in nature. It is also because the US dollar performs best in a risk-off setting when investors are pouring money into the safe-haven Treasury markets. In contrast, small caps excel in a risk-on environment. Value stocks tend to outperform growth stocks in a weaker dollar environment (Chart 20). Like small caps, cyclical equity sectors are overrepresented in value indices. Financials also tend to punch above their weight in value indices. Chart 19Small Caps Tend To Outperform Large Caps During Weak Dollar Environments...

Small Caps Tend To Outperform Large Caps During Weak Dollar Environments...

Small Caps Tend To Outperform Large Caps During Weak Dollar Environments...

Chart 20...The Same Goes For Value Stocks

...The Same Goes For Value Stocks

...The Same Goes For Value Stocks

Small caps and value stocks outperformed between 2000 and 2008, a time when the US dollar was generally weakening. That period saw both a commodity boom and a wave of debt-fueled housing booms. The former lifted commodity prices, while the latter buoyed financials. Commodity prices should rise over the next 12 months thanks to a rebound in global growth and copious Chinese stimulus. Chart 21 shows that the Chinese credit impulse is on track to reach the highest levels since the Global Financial Crisis, while the fiscal deficit will probably hit a record 8% of GDP. The Outlook For Financial Stocks Gauging the outlook for financials is trickier. Credit growth has slowed sharply since the Global Financial Crisis, which has weighed on bank profits. The structural decline in bond yields has also been toxic for bank shares (Chart 22). Lower bond yields tend to translate into flatter yield curves, which can depress net interest margins. Chart 21China Has Opened The Spigots

China Has Opened The Spigots

China Has Opened The Spigots

Chart 22The Structural Decline In Bond Yields Has Been Negative For Bank And Value Stocks

The Structural Decline In Bond Yields Has Been Negative For Bank And Value Stocks

The Structural Decline In Bond Yields Has Been Negative For Bank And Value Stocks

A falling dollar has historically been associated with higher bond yields (Chart 23). As global growth recovers over the next 12 months, bond yields will edge higher. That said, central bank bond purchases, coupled with aggressive forward guidance, will keep bond yields from rising as much as they normally would. And even if nominal yields do rise, inflation expectations will rise even more, implying that real yields will fall further. Falling real yields tend to benefit growth stocks more than they benefit value stocks. Chart 23Bond Yields Tend To Rise When The Dollar Weakens

Bond Yields Tend To Rise When The Dollar Weakens

Bond Yields Tend To Rise When The Dollar Weakens

Still, even a modest steepening of the yield curve will be good for bank earnings. A recovery in economic activity should also dampen concerns about a spike in bad loans. Credit spreads normally fall when economic growth is improving and the dollar is weakening (Chart 24). Banks have significantly increased provisions since the start of the year, which has depressed reported earnings. If some of those provisions are reversed, profits will jump. Chart 24Credit Spreads Tend To Fall When Growth Is Improving And The Dollar Is Weakening

Credit Spreads Tend To Fall When Growth Is Improving And The Dollar Is Weakening Credit Spreads Tend To Fall When Growth Is Improving And The Dollar Is Weakening

Credit Spreads Tend To Fall When Growth Is Improving And The Dollar Is Weakening Credit Spreads Tend To Fall When Growth Is Improving And The Dollar Is Weakening

Chart 25Bank And Value Stocks Are Quite Cheap

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Moreover, bank stocks in particular, and value stocks in general, are extremely cheap by historic standards (Chart 25). Thus, while the case for favoring value over growth is not as clear-cut as it could be, it is strong enough that long term-oriented investors should consider moving capital from high-flying tech stocks to unloved value stocks. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Weekly Report, “Will Bond Yields Ever Go Up?” dated July 24, 2020. Global Investment Strategy View Matrix

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Current MacroQuant Model Scores

The Stock Market Implications Of A Weaker Dollar

The Stock Market Implications Of A Weaker Dollar

Highlights The tech sector faces mounting domestic political and geopolitical risks. We fully expected stimulus hiccups but believe they will give way to large new fiscal support, given that COVID-19 is weighing on consumer confidence. Europe’s relative political stability is a good basis for the euro rally but any comeback in opinion polling by President Trump could give dollar bulls new life. DXY is approaching a critical threshold below which it would break down further. The US could take aggressive actions on Russia and Iran, but China and the Taiwan Strait remain the biggest geopolitical risk. Feature Near-term risks continue to mount against the equity rally, even as governments’ combined monetary and fiscal policies continue to support a cyclical economic rebound. Chart 1Tech Bubble Amid Tech War

Tech Bubble Amid Tech War

Tech Bubble Amid Tech War

Testimony by the chief executives of Facebook, Apple, Amazon, and Alphabet to the US House of Representatives highlighted the major political risks facing the market leaders. There are three reasons not to dismiss these risks despite the theatrical nature of the hearings. First, the tech companies’ concentration of wealth would be conspicuous during any economic bust, but this bust has left pandemic-stricken consumers more reliant on their services. Second, acrimony is bipartisan – conservatives are enraged by the tendency of the tech companies to side with the Democratic Party in policing the range of acceptable political discourse, and they increasingly agree with liberals that the companies have excessive corporate power warranting anti-trust probes. Executive action is the immediate risk, but in the coming one-to-two years congressional majorities will also be mustered to tighten regulation. Third, technology is the root of the great power struggle between the US and China – a struggle that will not go away if Biden wins the election. Indeed Biden was part of the administration that launched the US’s “Pivot to Asia” and will have better success in galvanizing US diplomatic allies behind western alternatives to Chinese state-backed and military-linked tech companies. US tech companies struggle to outperform Chinese tech companies except during episodes of US tariffs, given the latter firms’ state-backed turn toward innovation and privileged capture of the Chinese domestic market (Chart 1). The US government cannot afford to break up these companies without weighing the strategic consequences for America’s international competitiveness. The attempt to coordinate a western pressure campaign against Huawei and other leading Chinese firms will continue over the long run as they are accused of stealing technology, circumventing UN sanctions, violating human rights, and compromising the national security of the democracies. China, for its part, will be forced to take counter-measures. US tech companies will be caught in the middle. Like the threat of executive regulation in the domestic sphere, the threat of state action in the international sphere is difficult to time. It could happen immediately, especially given that the US is having some success in galvanizing an alliance even under President Trump (see the UK decision to bar Huawei) and that President Trump’s falling election prospects remove the chief constraint on tough action against China (the administration will likely revoke Huawei’s general license on August 13 or closer to the election). Massive domestic economic stimulus empowers the US to impose a technological cordon and China to retaliate. Combining this headline risk to the tech sector with other indications that the equity rally is extended – the surge in gold prices, the fall in the 30-year/5-year Treasury slope – tells us that investors should be cautious about deploying fresh capital in the near term. Republicans Will Capitulate To New Stimulus Just as President Trump has ignored bad news on the coronavirus, financial markets have ignored bad news on the economy. Dismal Q2 GDP releases were fully expected – Germany shrank by 10.1% while the US shrank by 9.5% on a quarterly basis, 32.9% annualized. But the resurgence of the virus is threatening new government restrictions on economic activity. US initial unemployment claims have edged up over the past three weeks. US consumer confidence regarding future expectations plummeted from 106.1 in June to 91.5 in July, according to the Conference Board’s index. Chart 2Global Instability Will Follow Recession

A Tech Bubble Amid A Tech War (GeoRisk Update)

A Tech Bubble Amid A Tech War (GeoRisk Update)

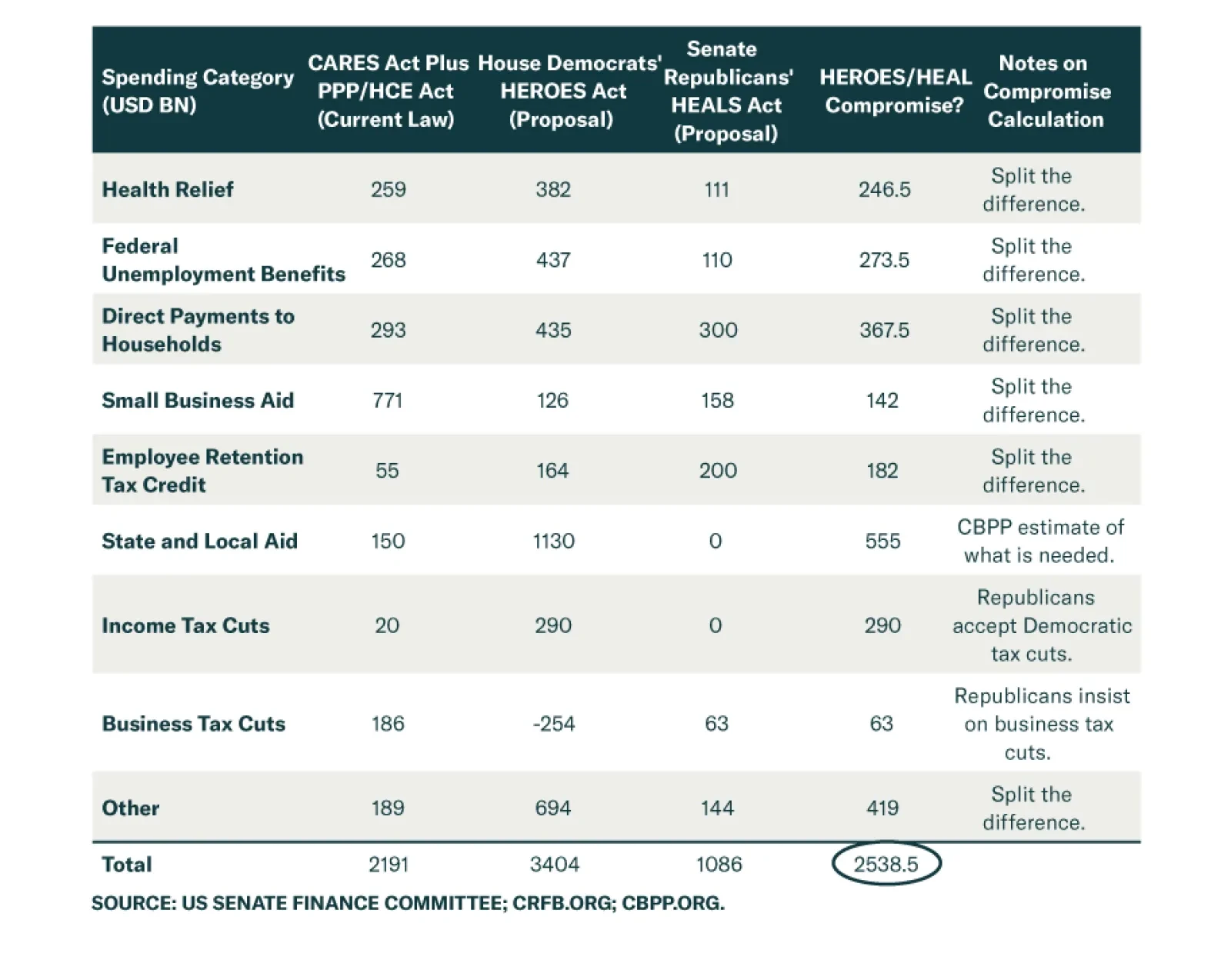

Setbacks in combating the virus will hurt consumers even assuming that governments lack the political will to enforce new lockdowns. The share of countries in recession has surged to levels not seen in 60 years (Chart 2). Financial markets can look past recessions, but the pandemic-driven recession will result in negative surprises and second-order effects that are unforeseen. Yes, fresh fiscal stimulus is coming, but this is more positive for the cyclical outlook than the tactical outlook. Stimulus “hiccups” could precipitate a near-term pullback – such a pullback may be necessary to force politicians to resolve disputes over the size and composition of new stimulus. This risk is immediate in the United States, where House Democrats, Senate Republicans, and the White House have hit an all-too-predictable impasse over the fifth round of stimulus. The bill under negotiation is likely to be President Trump’s last chance to score a legislative victory before the election and the last significant legislative economic relief until early 2021. The Senate Republicans have proposed a $1.1 trillion HEALS Act in response to the House Democrats’ $3.4 trillion HEROES Act, passed in mid-May. As we go to press, the federal unemployment insurance top-up of $600 per week is expiring, with a potential cost of 3% of GDP in fiscal tightening, as well as the moratorium on home evictions. Congress will have to rush through a stop-gap measure to extend these benefits if it cannot resolve the debate on the larger stimulus package. If Democrats and Republicans split the difference then we will get $2.5 trillion in stimulus, likely by August 10. Compromise on the larger package is easy in principle, as Table 1 shows. If the two sides split the difference between their proposals in a commonsense way, as shown in the fourth and fifth columns of Table 1, then the result will be a $2.5 trillion stimulus. This estimate fits with what we have published in the past and likely meets market expectations for the time being. Table 1Outline Of Fifth US COVID Stimulus Package (Estimate)

A Tech Bubble Amid A Tech War (GeoRisk Update)

A Tech Bubble Amid A Tech War (GeoRisk Update)

Whether it is enough for the economy depends on how the virus develops and how governments respond once flu season picks up and combines with the coronavirus to pressure the health system this fall. A back-of-the-envelope estimate of the amount of spending necessary to keep the budget deficit from shrinking in the second half of the year comes much closer to the House Democrats’ $3.4 trillion bill (Table 2), which suggests that what appears to be a massive stimulus today could appear insufficient tomorrow. Nevertheless, $2.5 trillion is not exactly small. It would bring the US total to $5 trillion year-to-date, or 24% of GDP! Table 2Reducing The Budget Deficit On A Quarterly Basis Will Slow Economy

A Tech Bubble Amid A Tech War (GeoRisk Update)

A Tech Bubble Amid A Tech War (GeoRisk Update)

While a compromise bill should come quickly, the Republican Party is more divided over this round of stimulus than earlier this year. Chart 3US Personal Income Looks Good Compared To 2008-09

US Personal Income Looks Good Compared To 2008-09

US Personal Income Looks Good Compared To 2008-09

First, there is some complacency due to the fact that the economy is recovering, not collapsing as was the case back in March. Our US bond strategist, Ryan Swift, has shown that US personal income is much better off, thus far, than it was in the months following the 2008 financial crisis, even though the initial pre-transfer hit to incomes is larger (Chart 3). Second, the Republican Party is reacting to growing unease within its ranks over the yawning budget deficit, now the largest since World War II (Chart 4). Chart 4If Republicans React To Deficit Concerns They Cook Their Own Goose

If Republicans React To Deficit Concerns They Cook Their Own Goose

If Republicans React To Deficit Concerns They Cook Their Own Goose

Chart 5Consumer Confidence Sends Warning Signal To Republicans

A Tech Bubble Amid A Tech War (GeoRisk Update)

A Tech Bubble Amid A Tech War (GeoRisk Update)

If Republicans are guided by complacency and fiscal hawks, they will cook their own goose. A failure to provide government support will cause a financial market selloff, will hurt consumer confidence, and will put the final nail in the coffin of their own chance of re-election as well as President Trump’s. Consumer confidence tracks fairly well with presidential approval rating and election outcomes. A further dip could disqualify Trump, whereas a last-minute boost due to stimulus and an economic surge could line him up for a comeback in the last lap (Chart 5). These constraints are obvious so we maintain our high conviction call that a bill will be passed, likely by August 10. But at these levels on the equity market, we simply have no confidence in the market gyrations leading up to or following the passage of the bill. Our conviction level is on the cyclical, 12-month horizon, in which case we expect US and global stimulus to operate and equities to rise. Bottom Line: Political and economic constraints will force Republicans to join Democrats and pass a new stimulus bill of about $2.5 trillion by around August 10. This is cyclically positive, but hiccups in getting it passed, negative surprises, and other risks tied to US politics discourage us from taking an overtly bullish stance over the next three months. Yes, US-China Tensions Are Still Relevant Chart 6Chinese Politburo"s Bark Worse Than Bite On Stimulus

Chinese Politburo"s Bark Worse Than Bite On Stimulus

Chinese Politburo"s Bark Worse Than Bite On Stimulus

Financial markets have shrugged off US-China tensions this year for understandable reasons. The pandemic, recession, and stimulus have overweighed the ongoing US-China conflict. As we have argued, China is undertaking a sweeping fiscal and quasi-fiscal stimulus – despite lingering hawkish rhetoric – and the size is sufficient to assist in global economic recovery as well as domestic Chinese recovery. What the financial market overlooks is that China’s households and firms are still reluctant to spend (Chart 6). China’s Politburo's late July meetings on the economy are frequently important. Initial reports of this year’s meet-up reinforce the stimulus narrative. Hints of hawkishness here and there serve a political purpose in curbing market exuberance, both at home and in the US election context, but China will ultimately remain accommodative because it has already bumped up against its chief constraint of domestic stability. Note that this assessment also leaves space for market jitters in the near-term. The phase one trade deal remains intact as President Trump is counting on it to make the case for re-election while China is looking to avoid antagonizing a loose cannon president who still has a chance of re-election. As long as broad-based tariff rates do not rise, in keeping with Trump’s deal, financial markets can ignore the small fry. We maintain a 40% risk that Trump levels sweeping punitive measures; our base case is that he goes to the election arguing that he gets results through his deal-making while carrying a big stick. At the same time, our view that domestic stimulus removes the economic constraints on conflict, enabling the two countries to escalate tensions, has been vindicated in recent weeks. Chinese political risk continues on a general uptrend, based on market indicators. The market is also starting to price in the immense geopolitical risks embedded in Taiwan’s situation, which we have highlighted consistently since 2016. While North Korea remains on a diplomatic track, refraining from major military provocations, South Korean political risk is still elevated both for domestic and regional reasons (Chart 7). Chart 7China Political Risk Still Trending Upward

China Political Risk Still Trending Upward

China Political Risk Still Trending Upward

The market is gradually pricing in a higher risk premium in the renminbi, Taiwanese dollar, and Korean won, and this pricing accords with our longstanding political assessment. The closure of the US and Chinese consulates in Houston and Chengdu is only the latest example of this escalating dynamic. While the US’s initial sanctions on China over Hong Kong were limited in economic impact, the longer term negative consequences continue to build. Hong Kong was the symbol of the Chinese Communist Party’s compatibility with western liberalism; the removal of Hong Kong’s autonomy strikes a permanent blow against this compatibility. China’s decision to go forward with the imposition of a national security law in Hong Kong – and now to bar pro-democratic candidates from the September 6 Legislative Council elections, which will probably be postponed anyway – has accelerated coalition-building among the western democracies. The UK is now clashing with China more openly, especially after blocking Huawei from its 5G system and welcoming Hong Kong political refugees. Australia and China have fought a miniature trade war of their own over China’s lack of transparency regarding COVID-19, and Canada is implicated in the Huawei affair. Even the EU has taken a more “realist” approach to China. Across the Taiwan Strait, political leaders are assisting fleeing Hong Kongers, crying out against Beijing’s expansion of control in its periphery, rallying support from informal allies in the US and West, and doubling down on their “Silicon Shield” (prowess in semiconductor production) as a source of protection. Intel Corporation’s decision to increase its dependency on TSMC for advanced microchips only heightens the centrality of this island and this company in the power struggle between the US and China. China cannot fulfill its global ambitions if the US succeeds in creating a technological cordon. Taiwan is the key to China’s breaking through that cordon. Therefore Taiwan is at heightened risk of economic or even military conflict. The base case is that Beijing will impose economic sanctions first, to undermine Taiwanese leadership. The uncertainty over the US’s willingness to defend Taiwan is still elevated, even if the US is gradually signaling a higher level of commitment. This uncertainty makes strategic miscalculations more likely than otherwise. But Taiwan’s extreme economic dependence on the mainland gives Beijing a lever to pursue its interests and at present that is the most important factor in keeping war risk contained. By the same token, Taiwanese economic and political diversification increases that risk. A “fourth Taiwan Strait crisis” that involves trade war and sanctions is our base case, but war cannot be ruled out, and any war would be a major war. Thus investors can safely ignore Tik-Tok, Hong Kong LegCo elections, and accusations of human rights violations in Xinjiang. But they cannot ignore concrete deterioration in the Taiwan Strait. Or, for that matter, the South and East China Seas, which are not about fishing and offshore drilling but about China’s strategic depth and positioning around Taiwan. Taiwan is at heightened risk of economic or military conflict. The latest developments have seen the CNY-USD exchange rate roll over after a period of appreciation associated with bilateral deal-keeping (Chart 8). Depreciation makes it more likely that President Trump will take punitive actions, but these will still be consistent with maintaining the phase one deal unless his re-election bid completely collapses, rendering him a lame duck and removing his constraints on more economically significant confrontation. We are perilously close to such an outcome, which is why Trump’s approval rating and head-to-head polling against Joe Biden must be monitored closely. If his budding rebound is dashed, then all bets are off with regard to China and Asian power politics. Chart 8A Warning Of Further US-China Escalation

A Warning Of Further US-China Escalation

A Warning Of Further US-China Escalation

Bottom Line: China’s stimulus, like the US stimulus, is a reason for cyclical optimism regarding risk assets. The phase one trade deal with President Trump is less certain – there is a 40% chance it collapses as stimulus and/or Trump’s political woes remove constraints on conflict. Hong Kong is a red herring except with regard to coalition-building between the US and Europe; the Taiwan Strait is the real geopolitical risk. Maritime conflicts relate to Taiwan and are also market-relevant. Europe, Russia, And Oil Risks Europe has proved a geopolitical opportunity rather than a risk, as we have contended. The passage of joint debt issuance in keeping with the seven-year budget reinforces the point. The Dutch, facing an election early next year, held up the negotiations, but ultimately relented as expected. Emmanuel Macron, who convinced German Chancellor Angela Merkel to embrace this major compromise for European solidarity, is seeing his support bounce in opinion polls at home. He is being rewarded for taking a leadership position in favor of European integration as well as for overseeing a domestic economic rebound. His setback in local elections is overstated as a political risk given that the parties that benefited do not pose a risk to European integration, and will ally with him in 2022 against any populist or anti-establishment challenger. We still refrain from reinitiating our long EUR-USD trade, however, given the immediate risks from the US election cycle (Chart 9). We will reevaluate if Trump’s odds of victory fall further. A Biden victory is very favorable for the euro in our view. Chart 9EUR-USD Gets Boost From EU Solidarity

EUR-USD Gets Boost From EU Solidarity

EUR-USD Gets Boost From EU Solidarity

We are bullish on pound sterling because even a delay or otherwise sub-optimal outcome to trade talks is mostly priced in at current levels (Charts 10A and 10B). Prime Minister Boris Johnson has the raw ability to walk away without a deal, in the context of strong domestic stimulus, but the long-term economic consequences could condemn him to a single term in office. Compromise is better and in both parties’ interests. Chart 10APound Sterling A Buy Over Long Run

Pound Sterling A Buy Over Long Run

Pound Sterling A Buy Over Long Run

Chart 10BPound Sterling A Buy Over Long Run

Pound Sterling A Buy Over Long Run

Pound Sterling A Buy Over Long Run

Two other risks are worth a mention in this month’s GeoRisk Update: Chart 11Russia: GeoRisk Indicator Russian Bonds May Face Sanctions

Russia: GeoRisk Indicator Russian Bonds May Face Sanctions

Russia: GeoRisk Indicator Russian Bonds May Face Sanctions

Russia: In recent reports we have maintained that Russian geopolitical risk is understated by markets. Domestic unrest is rising, the Trump administration could impose penalties over Nordstream 2 or other issues to head off criticism on the campaign trail, and a Biden administration would be outright confrontational toward Putin’s regime. Moscow may intervene in the US elections or conduct larger cyber attacks. US sanctions could ultimately target trading of local currency Russian government bonds, which so far have been spared (Chart 11). Iran: The jury is still out on whether the recent series of mysterious explosions affecting critical infrastructure in Iran are evidence of a clandestine campaign of sabotage (Table 3). The nature of the incidents leaves some room for accident and coincidence.1 But the inclusion of military and nuclear sites in the list leads us to believe that some degree of “wag the dog” is going on. The prime suspect would be Israel and/or the United States during the window of opportunity afforded by the Trump administration, which looks to be closing over the next six months. Trump likely has a high tolerance for conflict with Iran ahead of the election. Even though Americans are war-weary, they will rally to the president’s defense if Iran is seen as the instigator, as opinion polls showed they did in September 2019 and January of this year. Iran is avoiding goading Trump so far but if it suffers too great of damage from sabotage then it may be forced to react. The dynamic is unstable and hence an oil price spike cannot be ruled out. Table 3Wag The Dog Scenario Playing Out In Iran

A Tech Bubble Amid A Tech War (GeoRisk Update)

A Tech Bubble Amid A Tech War (GeoRisk Update)

Chart 12Oil Supply Risks Stem From Iran/Iraq, But COVID Threat To Demand Persists

Oil Supply Risks Stem From Iran/Iraq, But COVID Threat To Demand Persists

Oil Supply Risks Stem From Iran/Iraq, But COVID Threat To Demand Persists

Oil markets have the capacity and the large inventories necessary to absorb supply disruptions caused by a single Iranian incident (Chart 12). Only a chain reaction or major conflict would add to upward pressure. This would also require global demand to stay firm. The threat from COVID-19 suggests that volatility is the only thing one can count on in the near-term. Over the long run we remain bullish crude oil due to the unfettered commitment by world governments to reflation. Bottom Line: The euro rally is fundamentally supported but faces exogenous risks in the short run. We would steer clear of Russian currency and local currency bonds over the US election campaign and aftermath, particularly if Trump’s polling upturn becomes a dead cat bounce. Iran is a “gray swan” geopolitical risk, hiding in plain sight, but its impact on oil markets will be limited unless a major war occurs. Investment Implications The US dollar is at a critical juncture. Our Foreign Exchange Strategist Chester Ntonifor argues that if the DXY index breaks beneath the 93-94 then the greenback has entered a structural bear market. The most recent close was 93.45 and it has hovered below 94 since Monday. Failure to pass US stimulus quickly could result in a dollar bounce along with other safe havens. Over the short run, investors should be prepared for this and other negative surprises relating to the US election and significant geopolitical risks, especially involving China, the tech war, and the Taiwan Strait. Over the long run, investors should position for more fiscal support to combine with ultra-easy monetary policy for as far as the eye can see. The Federal Reserve is not even “thinking about thinking about raising rates.” This combination ultimately entails rising commodity prices, a weakening dollar, and international equity outperformance relative to both US equities and government bonds. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 See Raz Zimmt, "When it comes to Iran, not everything that goes boom in the night is sabotage," Atlantic Council, July 30, 2020. Section II: Appendix : GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Section III: Geopolitical Calendar

Highlights The decade-long US equity market outperformance versus the rest of the world could be nearing its end. We are upgrading EM stocks from underweight to neutral within a global equity portfolio. We reiterate the change in our US dollar outlook from bullish to bearish. The concentration risk in EM (specifically in North Asia) mega-cap stocks, poor fundamentals in EM outside North Asia, and a potential flare-up in US-China tensions are the reasons why we are reluctant to be overweight EM stocks. Feature We recommended the short EM equities / long S&P 500 position in late 2010,1 and have reiterated this strategy consistently over the past decade. Since its inception, this trade has produced a 193% gain with extremely low volatility (Chart 1). We recommend taking profits on this position for the reasons elaborated in this report. Chart 1Book Profits On Our Short EM Stocks / Long S&P 500 Strategy

Book Profits On Our Short EM Stocks / Long S&P 500 Strategy

Book Profits On Our Short EM Stocks / Long S&P 500 Strategy

Chart 2Equity Strategy Of the Decade: The Risk-Reward Is No Longer Attractive

Equity Strategy Of the Decade: The Risk-Reward Is No Longer Attractive

Equity Strategy Of the Decade: The Risk-Reward Is No Longer Attractive

Consistently, we are upgrading EM stocks from underweight to neutral within a global equity portfolio. Our decade-long equity sector theme – introduced in our June 8, 2010 report2 – has been to underweight resources and overweight technology and healthcare (Chart 2). This sector strategy has been one of the reasons for underweighting EM and favoring the US market in a global equity portfolio over the past decade. Going forward, the risk-reward of this sector strategy is no longer attractive. Regarding EM absolute performance, we recommend that absolute-return investors remain on standby for a correction before going long the EM equity benchmark. The End Of US Equity Outperformance The decade-long US equity market outperformance versus the rest of the world could be nearing its end.It is widely known that this decade’s US equity outperformance was largely due to FAANGM stocks (Facebook, Amazon, Apple, Netflix, Google and Microsoft). The FAANGM rally meets many of the criteria for a bubble, as we elaborated in our July 16 report. Our FAANGM equity index – an equal-weighted average of the six stocks – has increased almost 20-fold in real (inflation-adjusted) terms since January 2010 (Chart 3). Chart 3Each Decade = One Mania

Take Profits On The Short EM / Long S&P 500 Position

Take Profits On The Short EM / Long S&P 500 Position

Its rise is on par with the magnitude of the bull market in the Nasdaq 100 index through the 1990s, or of Walt Disney. through the 1960s, and it well exceeds other bubbles, as illustrated on Chart 3. All price indexes are shown in real (inflation-adjusted) terms. FAANGM stocks have greatly benefited from the recent “work from home” and other societal shifts and have been outperforming through the March financial carnage. It has made them unassailable in the eyes of investors. Yet, even great companies have a fair price, and considerable price overshoots will not be sustainable in the long term. We sense that a growing number of investors deem the US FAANGM and EM mega-cap stocks to be invincible. When some stocks are regarded as unbeatable, their top is not far. Therefore, it is highly unlikely that the FAANGM will outperform in the next selloff. Rather, the odds are that they will underperform because these stocks are extremely expensive, overbought, over-hyped and over-owned. The decade-long US equity market outperformance versus the rest of the world could be nearing its end. Apart from technology and FAANGM, US equities are facing a mediocre profit outlook. As long as the pandemic is not contained, America’s consumer and business confidence will remain lackluster, and, as a result, a recovery in their spending will be subdued. Chart 4US Stocks Are Not Cheap After Removing Market-Cap Bias

US Stocks Are Not Cheap After Removing Market-Cap Bias

US Stocks Are Not Cheap After Removing Market-Cap Bias

Notably, the broad US equity market is also expensive. The equal-weighted US equity index is trading at a 12-month forward P/E ratio of 21 (Chart 4, top panel). The risks associated with domestic politics are rising in the US. Social, political and economic divisions have been magnified by both the pandemic and the economic downtrend. Social and political tensions will likely flare up around the November elections. Our colleagues from the Geopolitical team argue that a contested election is possible and could lead to a crisis of presidential legitimacy in the US. Finally, the US equity market cap has reached 58% of the global market cap, the highest on record. Gravity forces are likely to kick in sooner than later, capping US equity outperformance. Bottom Line: The tailwinds supporting the US equity outperformance are fading. We are booking gains on the short EM stocks / long S&P 500 strategy. Consistently, we are also closing the short EM banks / long US banks and short Chinese banks / long US banks positions. They have produced a 75% gain and an 11% loss, respectively. Downgrading The US Dollar Outlook = Upgrading The EM View We had been bullish on the US dollar and bearish on EM currencies since early 2011 (Chart 5, top panel), but on July 9 made a major change in our currency strategy: we switched our shorts in EM currencies away from the US dollar to against an equal-weighted basket of the euro, Swiss franc and the yen. Since then, the EM ex-China equal-weighted currency index has rebounded versus the US dollar, but has depreciated against the basket of the euro, CHF and JPY (Chart 5, bottom panel). Chart 5EM Currencies Have Bottomed Versus The US Dollar But Not Against Other Safe-Heavens

EM Currencies Have Bottomed Versus The US Dollar But Not Against Other Safe-Heavens

EM Currencies Have Bottomed Versus The US Dollar But Not Against Other Safe-Heavens

While the US dollar could rebound in the short term, especially versus EM currencies, any rebound will likely prove to be short-lived. From now on, the strategy for the greenback should be selling into strength. Here is why: As US inflation rises in the coming years and the Fed refuses to raise interest rates, US real rates will drop further and, as a result, the US dollar will depreciate. A central bank that is behind the inflation curve is bearish for a nation’s currency. The main reason for turning negative on the US dollar structurally is the rising determination by the Federal Reserve to stay behind the inflation curve in the years to come. This strategy will instigate an inflation outbreak. Falling real interest rates have caused a plunge in the US dollar, as well as a surge in precious metal prices, in recent weeks. In fact, risk-on currencies have lately underperformed safe-haven currencies, such as the CHF and JPY (Chart 6). This market move confirms that the dollar’s recent plunge is due to fears of its debasement, not to robust growth in the world economy and in EM/China. As US inflation rises in the coming years and the Fed refuses to raise interest rates, US real rates will drop further and, as a result, the US dollar will depreciate. Colossal debt monetization. The Fed is undertaking an immense monetization of public and private debt. The current situation, involving the Fed’s purchases of securities, is different from the one following the Lehman crisis. Back in 2008-2014, the Fed’s QE program did not produce an exponential rise in money supply. The US broad money supply (M2) was rising at a single-digit rate between 2009 and 2014 (Chart 7). Presently, US M2 growth has exploded to 24% from a year ago. Chart 6Risk-On Currencies Are Underperforming Safe-Heaven Ones

Risk-On Currencies Are Underperforming Safe-Heaven Ones

Risk-On Currencies Are Underperforming Safe-Heaven Ones

Chart 7Helicopter' Money in the US

Helicopter' Money in the US

Helicopter' Money in the US

The pace of US broad money growth is much higher than that of many advanced and developing economies. Chart 8 shows new money creation as a share of GDP across various economies. It demonstrates that Japan and the US are now experiencing the quickest rate of new money creation in the world. In short, even though debt monetization is occurring in many advanced and EM economies, the US is doing it on an unprecedented scale. Chart 8Money Creation As % Of GDP In 2Q2020

Take Profits On The Short EM / Long S&P 500 Position

Take Profits On The Short EM / Long S&P 500 Position

“Helicopter” money will eventually lift inflation. The latest surge in the US money supply has only partially offset the collapse in its velocity. Consequently, America’s nominal GDP has plunged. This stems from the following identity: Nominal GDP = Price Level x Output Volume = Velocity of Money x Money Supply Solving the above equation for inflation, we get: Price Level = (Velocity of Money x Money Supply) / (Output Volume) Going forward, the velocity of US money will likely recover, for it is closely associated with consumers’ and businesses’ willingness to spend. At that point, rising velocity of money and greater money supply will work together to exert upward pressure on nominal GDP. Meantime, the pandemic will probably reduce potential output. The outcome of higher nominal spending and reduced potential productive capacity will be higher inflation. In sum, US inflation will rise well above 2% in the coming years. Yet, the Fed will stay put amid rising inflation. The upshot will be a structural downtrend in the US dollar. Whilst there are many arguments against rising inflation, we are leaning toward the view that US inflation will begin rising as of next year. We will elaborate on this inflation outlook in our future reports. Rising political and social uncertainty in the US will weigh on the greenback. The failure by the US authorities to contain the spread of the pandemic will continue fueling political and social upheavals. This could culminate in a harshly contested presidential election and a reduction in the US dollar’s allure for foreign investors. Portfolio inflows into the US will turn into outflows. The stellar performance of US equities attracted portfolio inflows into the US over the last 10 years. These capital inflows, in turn, boosted the greenback. But these dynamics are about to be reversed. Chart 9The US's Net International Investment Position Is At A Record Low

The US's Net International Investment Position Is At A Record Low

The US's Net International Investment Position Is At A Record Low

The top panel of Chart 9 shows that the US’s net international investment position in equities is at its lowest point since 1986. This means that foreign ownership of US stocks exceeds US resident ownership of foreign equities by a record amount. This reflects the fact that investors have by a large margin favored the US versus other bourses. As American share prices outperformed their international peers, both domestic and foreign investors have poured more capital into US equities. As the US relative equity performance reverses, equity capital will flow out of the US, thus dragging down the US dollar. Chart 10 shows that the trade-weighted dollar tracks the relative performance of the S&P500 versus the global equity benchmark in local currency terms. Regarding debt securities, the US’s net international investment position has widened to - US$8.5 trillion (Chart 9, bottom panel). Not all fixed-income investors hedge currency risk. As the dollar slides, there will be growing pressure on foreign fixed-income investors to hedge their dollar exposure or sell US and buy non-US debt securities. Chart 10A Top In The US$ = The End Of The US Equity Outperformance?

A Top In The US$ = The End Of The US Equity Outperformance?

A Top In The US$ = The End Of The US Equity Outperformance?

Bottom Line: Immense public debt monetization leading to higher inflation down the road and the Fed falling behind the curve, will produce a lasting and considerable downtrend in the US dollar in the coming years. Why Not Overweight EM Stocks? There are a number of reasons why – for now – we are only upgrading EM equities to neutral, rather than to overweight within a global equity portfolio, and why we are still reluctant to recommend buying EM stocks for absolute-return investors: Concentration risk in EM mega-cap stocks. As US FAANGM share prices come under selling pressure, contagion will spill over to EM mega-cap stocks. The latter have been responsible for a large share of gains in the EM equity index and, conversely, their pullback will considerably impact the EM benchmark’s performance. The top six companies combined account for about 24% of the MSCI EM equity market cap. To compare, US FAANGM (Facebook, Apple, Amazon, Netflix, Google and Microsoft) also account for 24% of the S&P 500 market cap. Hence, the concentration risk in EM equity space is as high as in the US. Geopolitical risk. A potential flare up in in geopolitical tensions will weigh on Chinese, South Korean and Taiwanese stocks. Given that they make up about 65% of the MSCI EM index equity market cap, the EM benchmark will suffer in absolute terms and be unlikely to outperform the global equity index. Faced with decreased approval in regard to his handling of the pandemic, and to a lesser extent, the economy and other social issues, President Trump could well resort to geopolitics to “rally Americans behind the flag.” He may, for example, ramp up tensions with China in an attempt to make geopolitics and China the focal points of the forthcoming presidential election. China will certainly retaliate. The South China Sea, Taiwan, technology transfers, treatment of multinational companies in both China and the US, as well as North Korea, could be focal points of a confrontation. This will weigh on business confidence in Asia and on capital spending. In our opinion, markets are vulnerable to such geopolitical risks. Poor domestic fundamentals in EM outside China, Korea and Taiwan. Fundamental backdrops remain inferior in many EM economies outside the North Asian ones. The number of new infections continues to rise in India, Indonesia, The Philippines, Brazil, Mexico, Colombia and Peru. Many EM economies will only slowly return to normalcy. In certain countries, banking systems were already in poor health, and things have gotten much worse after the crash in economic activity. As to the positives for EM, they are as follows: Rising Chinese demand will boost EM exports to China and help revive their growth. EM equity valuations are very appealing versus the S&P 500 (Chart 11). The bottom panel of Chart 11 shows that EM’s cyclically-adjusted P/E ratio relative to that in the US is over one standard deviation below its mean. Based on the 12-month forward P/E ratio for an equal-weighted index, EM stocks are cheaper than US ones (please refer to Chart 4 on page 4). EM currencies are also cheap (Chart 12). While they might experience a short-term setback, as a global risk-off phase takes place, EM exchange rates have probably seen their lows versus the US dollar. Chart 11EM Stocks Offer Value Versus The S&P 500

EM Stocks Offer Value Versus The S&P 500

EM Stocks Offer Value Versus The S&P 500

Chart 12EM Currencies Are Cheap

EM Currencies Are Cheap

EM Currencies Are Cheap

The US dollar’s weakness will mitigate risks for EM issuers of US dollar bonds and, thereby, induce more flows into EM sovereign and corporate credit markets. In short, EM local currency bonds will assuredly benefit from the US dollar’s slide. We have been neutral on both EM local currency bonds and EM sovereign and corporate credit, and are waiting for a correction before upgrading to overweight. In nutshell, little or no stress in EM fixed-income markets bodes well for EM share prices. Bottom Line: Risks to EM equity relative performance are presently balanced. A neutral allocation is warranted for now. EM relative equity performance versus DM is only slightly above its recent low (Chart 13, top panel). It is, therefore, a good juncture to move the EM equity allocation from underweight to neutral. In addition, both the EM equal-weighted and small-cap equity indexes are not yet signaling a broad-based and sustainable outperformance (Chart 13, middle and bottom panels). Chart 13EM Relative Equity Performance Is In A Bottom-Out Phase

EM Relative Equity Performance Is In A Bottom-Out Phase

EM Relative Equity Performance Is In A Bottom-Out Phase

Some FAQs Question: Wouldn’t the US dollar rally if global stocks sell off? The greenback will likely attempt to rebound from current oversold levels when and as a global risk-off phase sets in. EM high-beta currencies could experience a non-trivial setback but will remain above their March lows. Yet, any rebound in the US dollar versus European currencies and the Japanese yen will be fleeting and moderate. On July 9, in anticipation of US dollar weakness, we booked profits on the short EM currencies/long US dollar strategy and recommended shorting several EM currencies versus an equal-weighted basket of the euro, CHF and JPY. This strategy remains intact for now. Our short list of EM currencies includes: BRL, CLP, ZAR, TRY, IDR, PHP and KRW. Odds are that EM stocks will likely be broadly flattish relative to those in DM amid the next sell off. Chart 14EM Stocks Have Been Low Beta

EM Stocks Have Been Low Beta

EM Stocks Have Been Low Beta

Question: Aren’t EM stocks high-beta and won’t they underperform if, and as, global stocks sell off? The EM equity index has had a beta lower than one since 2013 (Chart 14). Odds are that EM stocks will likely be broadly flattish relative to those in DM amid the next sell off. Within the DM equity space, the US will likely underperform both Europe and Japan in common currency terms. Question: Which equity markets do you favor within the EM space? Our current overweights are China, Thailand, Russia, Peru, Pakistan and Mexico. Our underweights are Indonesia, India, Hong Kong, the Philippines, Turkey, South Africa, Chile and Brazil. Question: Which currencies and local currency bond markets do you recommend overweighting for dedicated EM managers? We recommended going long the Czech koruna versus the US dollar last week. Other currencies that we favor within the EM space are SGD, TWD, THB, MXN and RUB. As for local currency bonds or swap rates, our top picks are Mexico, Russia, Korea, India, China, Malaysia, Thailand, Peru, Ukraine and Pakistan. As always, the list of country recommendations for equities, fixed-income and currencies is available at the end of our reports (please refer to pages 14-15) or on the website. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1Please see Emerging Markets Strategy Weekly Reports "Inflation, Overheating And The Stampede Into Bonds," dated November 30, 2010, and "Emerging Markets In 2011: Not The Best Play In Town," dated December 14, 2010. 2Please see Emerging Markets Strategy Special Report "How To Play Emerging Market Growth In The Coming Decade," dated June 8, 2010 Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

At the press conference following the FOMC decision, Fed Chair Powell reinforced the extremely dovish forward guidance of the Fed by asserting once again that the committee “is not thinking about thinking about raising rates”. He also highlighted that…

Highlights The Fed’s emergency lending facilities have successfully stabilized markets … : Credit spreads have tightened dramatically since March and liquidity has been restored to the US Treasury market. … at very little cost to the central bank: Just the announcement of Fed lending facilities has been enough to push spreads lower in most cases. The facilities themselves have seen very little actual uptake. The only cost borne by the Fed has been a dramatic expansion of its balance sheet due to purchases of Treasury securities. We still want to “buy what the Fed is buying”: In US fixed income, we want to favor those sectors that are eligible for Fed support. This includes corporate bonds rated Ba and higher, municipal bonds and Aaa-rated securitizations. Keep portfolio duration at neutral: The Fed will be much more cautious about raising interest rates than in the past, and could wait until inflation is above its target before lifting off zero. Feature Back in April, we published a detailed explainer of the extraordinary actions taken by the Federal Reserve to combat the pandemic-induced recession.1 This week, we re-visit that Special Report to assess what the Fed has accomplished during the past three months and to speculate about what lies ahead. Overall, the Fed’s response has been highly effective. Stability was restored to financial markets almost immediately after the most dramatic policy interventions were announced, and it turns out that the announcements themselves did most of the work. The ultimate usage of the Fed’s Section 13(3) emergency lending facilities has been extremely low relative to their stated maximum capacities (Table 1). If you are the Fed, it is apparently enough to marshal overwhelming force and announce your willingness to deploy it. Like the ECB demonstrated in the fraught Eurozone summer of 2012, a bazooka can restore order without being fired.2 Table 1Usage Of The 2020 Federal Reserve Emergency Lending Facilities

Alphabet Soup, Part 2: Shocked And Awed

Alphabet Soup, Part 2: Shocked And Awed

The only possible cost borne by the Fed has been an explosion in the size of its balance sheet, mostly attributable to purchases of Treasury securities. The ultimate usage of the Fed’s facilities has been extremely low relative to their stated maximum capacities. This report looks at how the Fed’s actions have influenced (and will influence) interest rates, Treasury market liquidity, the corporate bond market and other fixed income spread products. It also considers the potential impact of the size of the Fed’s balance sheet on the economy and financial markets. Interest Rates The Fed dropped the funds rate to a range of 0% to 0.25% on March 15, and since then it has aggressively signaled that rates will stay pinned at the zero-lower-bound for a long time. Investors quickly took this message on board (Chart 1). The median estimate from the New York Fed’s Survey of Market Participants has the funds rate holding steady at least through the end of 2022. Meanwhile, the overnight index swap curve isn’t pricing-in a rate hike until 2024. Chart 1The Fed And Market Agree: No Hikes Through 2022

The Fed And Market Agree: No Hikes Through 2022

The Fed And Market Agree: No Hikes Through 2022

Chart 2Better Signaling From The Fed

Better Signaling From The Fed

Better Signaling From The Fed

The market adjusted much more quickly to the Fed’s zero interest rate policy this year than it did during the last zero-lower-bound episode (Chart 2). The MOVE index of Treasury yield volatility has already plunged to below 50. It took several years for it to reach those levels after the Fed cut rates to zero at the end of 2008. Similarly, the yield curve is much flatter today than it was during the last zero-lower-bound episode. This partly reflects the market’s expectation that rates will stay at zero for longer and partly the downward revisions to estimates of the long-run neutral fed funds rate that have occurred during the past few years. The bottom line is that the Fed has successfully achieved its goal on interest rate policy. The funds rate is at its effective lower bound and the entire term structure is priced for it to stay there for a very long time. There are two main reasons for this success. First, the Fed’s forward guidance has been more dovish this year than at any point during the last zero-lower-bound episode, with many FOMC participants calling for the Fed to target a temporary overshoot of the 2% inflation target. Second, the market is more skeptical about inflation ever returning to that target, as evidenced by much lower long-dated inflation expectations (Chart 2, bottom panel). What’s Next? The Fed has already made it clear that it won’t pursue negative interest rates. With those off the table, the next step will be for the Fed to make its forward rate guidance more explicit. In all likelihood this will involve the return of some form of the Evans Rule that was in place between 2012 and 2014. The Evans Rule was a commitment to not lift rates at least until the unemployment rate moved below 6.5% or inflation moved above 2.5%.3 The new version of the Evans Rule will be much more dovish. In a recent speech, Governor Lael Brainard favorably cited research suggesting that the Fed should refrain from liftoff until inflation reaches the 2% target.4 That may very well be the rule that ends up becoming official Fed guidance. If the Fed wants to strengthen its commitment to low rates even more, it could follow the Reserve Bank of Australia’s lead and implement a Yield Curve Control policy. This policy would involve setting caps for Treasury yields out to a 2-year or 3-year maturity. The Fed would pledge to buy as many securities as necessary to enforce the caps and would only lift the caps when the criteria of its new Evans Rule are met. While spreads have tightened across all credit tiers, investment grade corporates have become much more expensive than high-yield. For the time being, there is no rush for the Fed to deliver more explicit forward guidance and/or Yield Curve Control. As we noted above, bond yields are already pricing-in an extremely lengthy period of zero rates. But these policies will become more important as the economic recovery progresses and market participants start to speculate about an eventual exit from the zero bound. Explicit forward guidance and/or Yield Curve Control would then prevent a premature rise in bond yields and tightening of financial conditions. With all that in mind, we would not be surprised to see more explicit (Evans Rule-style) forward guidance rolled out at some point this year, but unless bonds sell off significantly beforehand, it probably won’t have an immediate impact on yields. The same is true for Yield Curve Control, though the odds of that being announced this year are lower as it is a tool with which the Fed is less comfortable. Treasury Market Liquidity Chart 3When Treasury Market Liquidity Evaporated

When Treasury Market Liquidity Evaporated

When Treasury Market Liquidity Evaporated

As the COVID-19 crisis flared in March, there were several tense days when liquidity in the US Treasury market evaporated. Bond yields jumped even as the equity market plunged (Chart 3). Meanwhile, liquidity markers showed that it had become much more difficult to transact in US Treasuries. Treasury Bid/Ask spreads widened dramatically and the iShares 20+ Year Treasury ETF (TLT) traded at a huge discount to its net asset value (Chart 3, panel 3). During the past four months, researchers have identified hedge fund selling of Treasuries to meet margin calls and foreign bank selling of Treasuries to meet demands for US dollar funding as the proximate causes of March’s Treasury rout. However, it is clearly a failure of market structure that the Treasury market was unable to accommodate that selling pressure without liquidity disappearing. In a recent paper from The Brookings Institution, Darrell Duffie explains why the Treasury market was unable to maintain its liquidity during this tumultuous period.5 Essentially, he argues that it is the combination of rising Treasury supply and post-2008 regulations imposed on dealer banks that has led to an environment where there is a large and growing amount of Treasury supply, but where dealers have less balance sheet capacity to intermediate trading. To illustrate, Chart 4 shows the ratio between the outstanding supply of Treasury securities and the quantity of Treasury inventories for which primary dealers obtained financing. Quite obviously, the dealers’ intermediation activities have not kept pace with the expanding size of the market. Chart 4Primary Dealers Have Not Kept Up With Treasury Issuance

Primary Dealers Have Not Kept Up With Treasury Issuance

Primary Dealers Have Not Kept Up With Treasury Issuance

What’s Next? Without changes to Treasury market structure or bank capital requirements (Duffie recommends abandoning the system of competing dealer banks altogether and moving all Treasury trades through one central clearinghouse), we are likely to see more episodes like March where a spate of Treasury selling leads to an evaporation of market liquidity. When that happens, the Fed will be forced to step in and buy Treasuries, as it did in March (Chart 3, bottom panel). The goal of that intervention is simply to remove enough supply from the market so that the remaining trading volume can be handled by the dealers. As this pattern repeats itself over time, it will cause the Fed’s presence in the Treasury market to grow. Bottom Line: Unless structural changes are made to the Treasury market or bank capital regulations are rolled back, we should expect more episodes of Treasury market illiquidity like we saw in March. We should also expect the Fed to respond to those episodes with aggressive Treasury purchases, and for the Fed’s presence in the Treasury market to grow over time. Corporate Bonds The Fed’s intervention in the corporate bond market consists of three lending facilities: The Secondary Market Corporate Credit Facility (SMCCF) where the Fed purchases investment grade corporate bonds and recent Ba-rated fallen angels in the secondary market. This facility also purchases investment grade and high-yield ETFs. The Primary Market Corporate Credit Facility (PMCCF) where the Fed buys new issuance from investment grade-rated issuers (and recent fallen angels) in the primary market. The Main Street Lending Facility (MSLF) where the Fed purchases loans off of bank balance sheets. The loans must be made to small or medium-sized firms with Debt-to-EBITDA ratios below 6.0. Chart 5Corporate Issuance Surged Following The Fed's Announcements

Corporate Issuance Surged Following The Fed's Announcements

Corporate Issuance Surged Following The Fed's Announcements

As mentioned above, these facilities have barely been tapped. As of July 1, the Fed had purchased $1.5 billion of corporate bonds and just under $8 billion of ETFs through the SMCCF, while the PMCCF had not been used at all. However, the impact of the Fed’s promise to back-stop such a large portion of the corporate debt market has been immense. Corporate bond issuance surged following the announcement of the Fed’s facilities, and set monthly post-2008 records in March, April and May (Chart 5). The effect on corporate bond spreads has been just as dramatic. Spreads peaked on March 23, the day that the SMCCF and PMCCF were announced, and have tightened significantly since then. Further underscoring the importance of the SMCCF, PMCCF and MSLF announcements is that those segments of the corporate bond market most likely to have access to the Fed’s lending facilities have seen the most spread compression. Recall that investment grade issuers and recent fallen angels have access to the SMCCF and PMCCF, while the MSLF will benefit most issuers rated Ba or higher. Some B-rated issuers are able to tap the MSLF, but not the majority. Issuers rated Caa or below are much less likely to benefit from any of the Fed’s programs. Table 2 shows how the impact of the Fed’s facilities has played out across the different corporate credit tiers. It shows each credit tier’s option-adjusted spread and 12-month breakeven spread as of March 23 and today. It also shows the percentile rank of those spreads since 2010 (100% indicating the widest spread since 2010 and 0% indicating the tightest). While spreads have tightened across all credit tiers, investment grade corporates have become much more expensive than high-yield. The B-rated and below credit tiers are particularly cheap, with 12-month breakeven spreads all above their 80th percentiles since 2010. Table 2The Fed's Impact On Corporate Spreads

Alphabet Soup, Part 2: Shocked And Awed

Alphabet Soup, Part 2: Shocked And Awed

Chart 6Spread Curve Back To Normal

Spread Curve Back To Normal

Spread Curve Back To Normal

The market impact of the Fed’s corporate lending facilities is also apparent across the corporate bond term structure. In March, the investment grade corporate bond spread slope inverted, as 1-5 year maturity corporate bond spreads widened relative to spreads of securities with more than 5 years to maturity (Chart 6).6 The Fed concentrated its lending facilities on securities with less than 5 years to maturity, and it has successfully re-steepened the corporate spread curve. But the Fed’s corporate lending facilities are not all powerful. As Chair Powell likes to say: “the Fed has lending powers, not spending powers”. So while the promise of Fed lending is a big help, it still means that troubled firms will have to increase their debt loads to survive the economic downturn. Those firms that take on debt may still see their credit ratings downgraded as their balance sheet health deteriorates. Indeed, this is exactly what has happened. Ratings downgrades have jumped during the past few months, as have defaults (Chart 7). There has also been a spike in the number of fallen angels – firms downgraded out of investment grade – but not as big a jump as was seen during the last recession (Chart 7, panel 2). The Fed’s emergency lending facilities have likely prevented some downgrades, but not all. Chart 7Fed Can't Prevent Downgrades

Fed Can't Prevent Downgrades

Fed Can't Prevent Downgrades

What’s Next? The Fed’s lending facilities are responsible for a huge portion of the spread compression we’ve seen since late March. That said, it is a potential problem for corporate bonds that those facilities are scheduled to expire at the end of September. Our sense is that the expiry date will be extended, and that the facilities will only be wound down after a significant period of time where they see zero usage. At that point, the Fed should be able to halt the facilities without unduly impacting markets. In terms of investment implications, we think that the Fed’s back-stop will continue to be the most important driver of corporate bond spreads during the next few months. This means we would avoid chasing the attractive valuations in bonds rated B & below, and would continue to focus our corporate bond exposure on bonds rated Ba and above. We make an exception to our “buy what the Fed is buying” rule when it comes to positioning across the corporate bond term structure. Here, we are inclined to grab the extra spread offered by longer-maturity securities even though Fed secondary market purchases are concentrated at the front-end. Our rationale is that the Fed’s secondary market purchases are already low and will likely decline as time goes on. Meanwhile, if firms with long-maturity debt outstanding need help they can still access the PMCCF if needed. Other Fed Lending Facilities & Fixed Income Sectors Outside of the three programs geared toward the corporate bond market, the Fed also rolled out emergency lending facilities meant to back-stop: money market mutual funds (MMLF), the commercial paper market (CPFF), the asset-backed securities market (TALF), the municipal bond market (MLF) and the federal government’s new Paycheck Protection Program (PPPLF). Once again, the announcement effect did most of the work for all of these facilities and the Fed managed to quickly restore stability to each targeted market without doing much actual lending. For starters, the MMLF successfully halted a flight out of prime money market funds with a relatively modest $53 billion in loans (Chart 8). The CPFF caused the commercial paper/T-bill spread to normalize with only $4 billion of lending, and the LIBOR/OIS spread also tightened soon after the Fed rolled out its facilities (Chart 8, bottom panel). The Fed has dramatically expanded the size of its balance sheet through purchases of Treasury securities and agency MBS. In the asset-backed securities market, the Fed decided that only Aaa-rated securitizations are eligible for TALF. With that in mind, Aaa-rated consumer ABS and CMBS spreads have tightened considerably since TALF’s announcement (Chart 9). Non-Aaa consumer ABS spreads have tightened modestly despite the lack of Fed support. This is because fiscal stimulus has, so far, kept households flush with cash and prevented a wave of consumer bankruptcies. Non-Aaa CMBS, on the other hand, have struggled due to lack of Fed support and a sharp increase in commercial real estate delinquencies. Chart 8Stability Restored

Stability Restored

Stability Restored

Chart 9Consumer ABS & CMBS Spreads Tightened Considerably...

Consumer ABS & CMBS Spreads Tightened Considerably...

Consumer ABS & CMBS Spreads Tightened Considerably...