Policy

Highlights If policymakers can neutralize default pressures arising from the lockdowns, the lasting impacts of this recession may not be so bad: As Jay Powell put it on 60 Minutes several weeks ago, policymakers just have to keep people and businesses out of insolvency until health professionals can gain the upper hand over the virus. Fiscal spending caused income and savings to spike, … : Generous transfer payments have left the majority of the unemployed better off than they were when they were working, and April household income and savings soared accordingly. … allowing consumers to meet nearly all of their obligations … : April’s income and savings gains showed up in reduced delinquencies across all categories of consumer loans and in solid April and May rent collections. May’s employment gains suggest that the private sector may not be too far away from taking the baton from Congress: The May employment report blew away expectations and sent risk assets surging, but the positive surprise may derail plans for further fiscal support. Feature Since March, investors have been presented with a simple choice: believe their eyes or believe in the government. They could either focus on horrendous economic data illustrating the crippling effects of widespread lockdowns, or they could trust in policymakers’ ability to shield most citizens and businesses from lasting damage. Our base case has been that policymakers would succeed, for the most part, provided they didn’t have to contend with acute COVID-19 pressures for more than six months. There are as many guesses about the virus’ future path as there are commentators, but it seems reasonably conservative to estimate that the most onerous restrictions will be eased by October. Chart 1DC To The Rescue

D.C. To The Rescue

D.C. To The Rescue

In our view, preventing defaults is the key to mitigating the effects of the virus. If newly vulnerable debtors can be kept from defaulting until the economy can return to something resembling normal, a negatively self-reinforcing dynamic will not take hold, the infection will not spread to the financial system and creditworthy individuals’ and viable businesses’ temporary liquidity issues will not morph into solvency issues. Banking system data to confirm or disprove our thesis will not be available until August, however, as Fed and FDIC data are quarterly, and the shutdowns only began in late March. The unemployment safety net has turned into a trampoline; ... In this report, we have turned to a range of other sources for higher-frequency insights into what is happening in real time. We start with an academic paper showing that most laid-off workers are eligible for benefits comfortably exceeding their previous income, a conclusion reinforced by the April personal income data (Chart 1). We then look at April delinquency data from TransUnion, one of the major credit reporting agencies, and April and May rent-collection data from an apartment trade organization and large-cap publicly traded apartment REITs. We also review the Fed’s Survey of Consumer Finances to get a sense of household indebtedness across the income and wealth spectrums. For now, the data support the conclusion that policymakers have successfully defused credit distress pressures. What Comes In … Unemployment benefits typically fall far short of workers’ regular compensation, averaging about 40% of the median worker’s wage. To cushion the blow of unemployment from COVID-19, the CARES Act included a federal supplement to unemployment benefit payments distributed by the individual states. Added onto the average $400 weekly state benefit, the $600 federal supplement would make the average worker whole (mean earnings are a little less than $1,000 a week). As income inequality has intensified, the compensation distribution for all American workers has come to exhibit a pronounced rightward skew. That skew has pulled mean compensation (the average of all Americans’ earnings) well above median compensation (the earnings of the worker at the exact middle of the earnings distribution).1 By targeting mean compensation, the CARES Act opened the door for a lot of lower-income workers to make more money in unemployment than they did when they were working. According to a recent paper from three Chicago professors, 68% of unemployed workers are eligible to receive benefits that exceed their previous income, while 20% of unemployed workers are eligible for benefits that will at least double it. Overall, they calculate that the median worker is eligible to receive benefits amounting to 134% of his/her previous income.2 ... instead of keeping laid-off employees' incomes from falling below 40 cents on the dollar, it's launched them to $1.30. We offer no judgments about the policy merits of a 134% median replacement rate, but unusually generous benefits should help reduce the drag from unemployment that would otherwise ensue with a 40% replacement rate. Thanks to lower-income households’ higher marginal propensity to consume, consumption should rise at the margin (once activity resumes). Thanks to increased income, lower-income households should be better positioned to meet their financial obligations. We suspect the marginal consumption boost may be hard to see with the naked eye, but auto, credit card and mortgage delinquencies should be appreciably lower than any regression model not adjusted to reflect record replacement rates would predict. … And What Goes Out The Personal Income and Outlays data for April reflected the significant impact on household income of the up-to-$1,200 stimulus checks (economic impact payments) and the supplemental unemployment benefits. Despite an annualized $900 billion decline in employee compensation, personal income rose by nearly $2 trillion in April, thanks to a $3 trillion increase in transfer payments. De-annualizing the components, $250 billion in transfer payments offset a $75 billion decrease in compensation. At about $220 billion, the economic impact payments accounted for the bulk of the transfer payments, and they will fall sharply in May. The IRS did not disclose the amount of economic impact payments it had disbursed by April 30, but it appears that around 80% of the distributions have been made, leaving approximately $55 billion yet to be disbursed. Unemployment insurance receipts will rise in May on an extra week of benefits and an increase in the weekly sums of initial and continuing unemployment claims. We project that employee compensation rose about 3% in May, based on a 2% gain in employment and a 1% increase in average weekly earnings. Aggregating the February-to-May changes, it appears that May personal income ought to exceed February (Table 1). Absent another round of stimulus checks, however, personal income will slide below its pre-shutdown level beginning in June. Table 1May Personal Income Should Exceed Its Pre-Pandemic Level

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

Income is not the sole driver of households’ capacity to service their debt, however. Assets matter, too, and even if the surge in cash flow was a one-off event, it left behind an elevated stock of cash as households slashed consumption in both March and April. Real personal consumption expenditures have fallen 19% from February’s all-time high and are now back to a level they breached in January 2012 (Chart 2). Households saved 33% of their April disposable income, and on a level basis, April savings were up nearly fivefold from their 2019 average. They were a whopping 20 times April interest payments, ex-mortgages (Chart 3). Chart 2Eight Years Of Spending Undone In Two Months

Eight Years Of Spending Undone In Two Months

Eight Years Of Spending Undone In Two Months

Chart 3Consumers' Interest Coverage Ratios Have Soared

Consumers' Interest Coverage Ratios Have Soared

Consumers' Interest Coverage Ratios Have Soared

Household Borrowers Are Staying Current … Table 2Consumer Borrowers Are Hanging In There

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

It is possible to make too much of the April income and outlays data. We had been expecting another round of stimulus checks, but lawmakers’ comments even before the blockbuster employment report suggested one may not be forthcoming. Some of the savings activity was forced on homebound consumers, and some pent-up demand will surely be unleashed as the economy re-opens. Households amassed a mighty savings war chest across March and April, however, and it has left them better-positioned to service their debt obligations going forward. Despite an unemployment rate not seen since FDR, households made their scheduled payments in April. According to TransUnion, delinquency rates fell month-over-month across every major consumer loan category and delinquency rates for mortgages and unsecured personal loans declined on a year-over-year basis (Table 2). The TransUnion data comes from its inaugural Monthly Industry Snapshot, intended to provide a higher-frequency read on headline consumer credit metrics than its typical quarterly releases. In addition to crunching the delinquency numbers, the report noted that forbearance programs have helped ease consumer liquidity pressures, consumers have reduced their outstanding credit card balances and credit scores have slightly improved. None of the factors is decisive on its own, but they contribute to a marginally improved consumer credit outlook. … And Apartment Tenants Are Paying Their Rent It is more common for households in the lower half of the income and net worth distributions to rent their residence than own it. Just one in every five households in the bottom two quintiles of the income distribution (Chart 4, top panel), and one in four in the bottom half of the net worth distribution (Chart 4, bottom panel), have a mortgage. Rent is the single largest recurring expense for these households and the shutdowns made paying it a concern. Several newspaper stories have highlighted the plight of distressed renters while discussing grassroots rent-strike movements, but the National Multifamily Housing Council’s (NMHC) Rent Payment Tracker tells a different story.3 Chart 4Households In The Lower Half Of The Income And Wealth Distributions Rent Their Homes

Households In The Lower Half Of The Income And Wealth Distributions Rent Their Homes

Households In The Lower Half Of The Income And Wealth Distributions Rent Their Homes

The Rent Payment Tracker distills the results of a national survey covering over 11 million professionally managed apartment units. Through May 27th, it reported that 93.3% of renters had made full or partial payments for the month of May. The share of paying tenants was down just 150 basis points year-over-year, and up 160 basis points month-over-month. The six apartment REITs in the S&P 500 reported April and May rent collections that were better than the NMHC data. By the end of May, the REITs had collected 94-99% of the April rent they were due, and 93-96% of their May rents (Table 3). (Equity Residential (EQR) reported its April collections through April 7th and did not provide an end-of-month update; on June 1st, it reported that its May collections through May 7th were in line with April’s.) Essex Property Trust (ESS), which owns a portfolio of apartments in southern California, the Bay Area and greater Seattle, provided a table showing how the economic impact payments and the supplemental unemployment benefit would affect the income of unemployed California and Washington state couples without children. Table 4 expands it to cover four income scenarios, illustrating just how far up the income distribution CARES Act relief stretches. Table 3Residential Tenants Are Paying Their Rent

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

Table 4The CARES Act For Essex Property Trust Renters

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

So Far, So Good (How Markets Learned To Stop Worrying And Love Washington, DC)

Who Borrows: Evidence From The Survey Of Consumer Finances Helping the households in the bottom half of the income distribution won’t materially limit credit distress across the economy if those households don’t have access to credit. The latest edition of the Fed’s triennial Survey of Consumer Finances, published in 2017, makes it clear that they do. Those households may be much less likely to carry mortgage debt (Chart 5), but they make up for it by borrowing via other channels. 64% of households in the bottom two quintiles have some debt, and the share grows to 70% when the middle quintile, which qualified for the full $1,200 economic impact payment, is included (Chart 6). Chart 5The Homeownership Income Divide

The Homeownership Income Divide

The Homeownership Income Divide

Chart 6Households In The Lower Two Quintiles Have Debt To Service, Too

Households In The Lower Two Quintiles Have Debt To Service, Too

Households In The Lower Two Quintiles Have Debt To Service, Too

Investment Implications The discussion above focused solely on the consumer, as we discussed the Fed’s efforts to assist lenders and business borrowers in a joint Special Report with our US Bond Strategy colleagues in April.4 Record corporate bond issuance in March and April – before the Fed bought a single corporate bond – testifies to the effectiveness of the Fed’s measures. Its corporate credit facilities bazooka was so large that it was able to soothe the roiled corporate issuance market without firing a single shot. Spreads have narrowed across the spread product spectrum and the primary and secondary markets are once again able to function normally. Too much economic improvement could be self-limiting, and the S&P 500 is trading at an ambitious multiple. We remain equal weight equities over the tactical three-month timeframe. The foregoing review of consumer performance reinforces our view that the SIFI banks should be overweighted relative to the S&P 500. The ongoing data indicate that the SIFI banks will not have to build up their reserves for loan losses as much as investors feared. Our conviction that the SIFI banks are unlikely to face material book value declines has only increased. It has become possible that second- and third-quarter reserve builds may be even less than our optimistic two-times-the-first-quarter view, but the virus will have the final say. The SIFI banks remain our favorite long idea. At the asset allocation level, we remain equal weight equities over the tactical three-month timeframe. We are encouraged by the green shoots visible in the employment report, but stocks are generously valued and the virus outlook is still unclear. The improvement on the ground could prove to be self-limiting if it kills the momentum for further fiscal assistance, or if it encourages officials and individuals to let their guard down regarding the social distancing measures that have been effective in lowering COVID-19 infection rates. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 According to the Census Department’s annual Current Population Survey, mean household income ($90,000) exceeded median household income ($63,000) by 42% in 2018. 2 Ganong, Peter, Noel, Pascal J., Vavra, Joseph S. "US Unemployment Insurance Replacement Rates During the Pandemic," NBER Working Paper No. 27216. 3https://www.nmhc.org/research-insight/nmhc-rent-payment-tracker/ Accessed June 1. 4 Please see the April 14, 2020 US Investment Strategy/US Bond Strategy Special Report, "Alphabet Soup: A Summary Of The Fed’s Anti-Virus Measures," available at usis.bcaresearch.com.

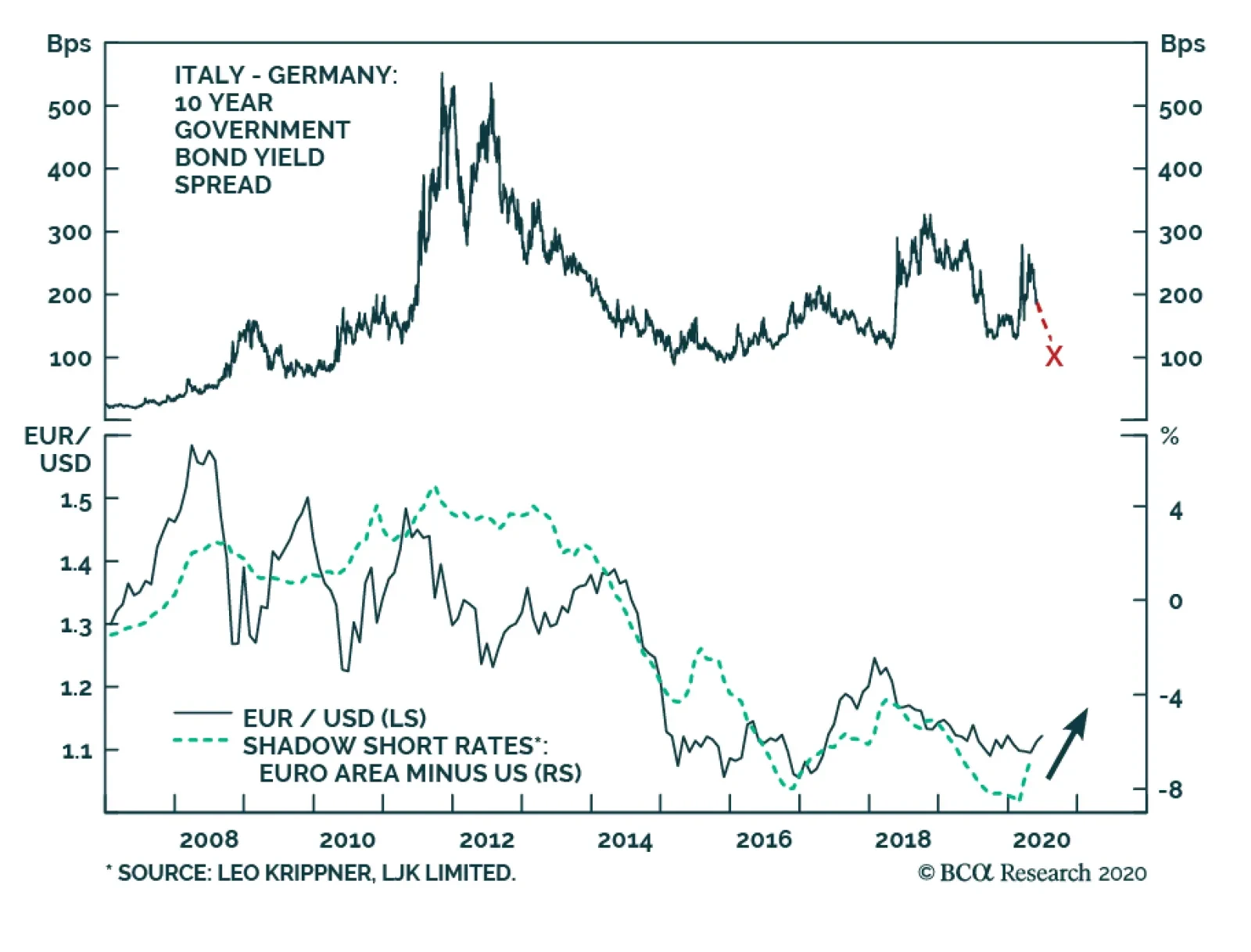

Yesterday, the ECB pleasantly surprised market participants by announcing an additional EUR600 billion of purchases and extending the program to at least June 2021. Investors expected only a further EUR500 billion in buying. The euro strengthened on the…

Highlights Risks assets have entered a FOMO-driven mania phase that could last for a few more weeks. Markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. A weaker than expected global recovery and rising geopolitical tensions between the US and China are the two primary risks that will weigh on EM risk assets after this mania phase runs out of steam. We are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. Within EM, local rates will perform well in both risk-on and risk-off phases. Feature The recovery in global risk assets has entered a fear-of-missing-out, or FOMO, mania phase. Like any mania, this one could last longer and go further than any fundamental analysis could presume. Investors who are long or cannot afford to stay on the sidelines should play this rally with tight stop points. Investors with longer time horizon should wait for a pullback in EM equities and currencies to buy. Within EM, local rates offer the best risk-reward profile. A recovery in global trade and mainland industrial sectors is necessary for EM equities and currencies to rally on a sustainable basis. The global equity rally has taken place amid a shrinking forward EPS. The top panel of Chart I-1 demonstrates that even the ever-bullish bottom-up analysts have been cutting their expectations of the level of corporate 12-month forward earnings per-share. As a result, the global forward P/E ratio has spiked to a 18-year high (Chart I-1, bottom panel). Chart I-1An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

An Unprecedented Divergence: Surging Stocks Prices Amid Plunging Forward EPS Levels

Chart I-2EM Forward EPS Level Has Been Falling

EM Forward EPS Level Has Been Falling

EM Forward EPS Level Has Been Falling

Chart I-2 illustrates that the same phenomenon is true for EM equities. Their forward EPS has been contracting and their forward P/E has jumped to a decade high. Any overdrive in asset prices without supporting fundamentals can last for a while but typically ends with a crash. This FOMO-driven mania is unlikely to be any different. It is fair to say that during the March carnage, many investors operated on a “sell now, think later” principle. Since the rally began, they have switched to a “buy now, ask questions later” attitude. As this rally persists, global stocks and credit will become overbought and expensive. At that point, any negative shock could produce a sharp pullback that would likely devolve into another nasty selloff as investors shift back to a “sell now, think later” mentality. The Narratives Driving The Rally The narratives supporting this mania are simple and seem to be both accepted and embraced by a growing number of investors. We agree with some and disagree with others: Economies around the world are opening, which will ensure that an economic recovery will follow. Our interpretation: Surely as confinement policies are eased, activity will improve. However, in our opinion, this should not come as a surprise to investors. This is especially pertinent for the trend-setting US stock market. With US equity valuations not particularly cheap, the market was never pricing in extended lockdowns. Hence, it appears strange to us that markets have so exuberantly cheered the reopening of the economy. Looking forward, the key to the medium-term (six-month) equity outlook is the shape of the recovery following the initial partial normalization. The latter presently looks V-shaped because as stores and businesses reopen economic activity is bound to improve. Yet the odds are that following this initial normalization, the shape of the recovery is most likely to be U-shaped. For what it’s worth, manufacturing PMIs in export-oriented economies like Korea, Japan and Taiwan made new lows in May (Chart I-3). We are not suggesting these indicators will not improve in the months ahead; they surely will. Nevertheless, a marginal rise in diffusion indexes like PMIs from extraordinary depressed levels do not signify a profit recovery. This recession differs from previous ones as the level of business activity has dropped below breakeven points for more businesses than it did in other recessions. When a company operates below its breakeven level, a marginal rise in sales may not be sufficient to improve its debt-servicing capacity, hiring and capital spending intentions. However, it seems markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. This is why we feel risk assets are in a FOMO-driven mania phase, where fundamentals do not matter. Authorities around the world are stimulating, with the US pumping enormous amounts of fiscal and credit stimulus into the economy (Chart I-4, top panel). Chart I-3Asian Manufacturing PMIs Made New Lows In May

Asian Manufacturing PMIs Made New Lows In May

Asian Manufacturing PMIs Made New Lows In May

Chart I-4An Unparalleled Global Money Boom

An Unparalleled Global Money Boom

An Unparalleled Global Money Boom

Chart I-5China Is Ramping Up Stimulus

China Is Ramping Up Stimulus

China Is Ramping Up Stimulus

China has finally embarked on aggressive stimulus. The National People’s Congress has set the monetary policy objective for 2020 as follows: Substantially accelerate the growth of broad money supply and total social financing (Chart I-4, bottom panel). Our interpretation: Indeed, government stimulus worldwide is massive. Yet, it is hard to know if it will be sufficient to produce a V-shaped recovery. The rise in money supply at the moment is being offset by the drop in the velocity of money. As a result, nominal GDP levels are extremely low. That said, last week we upgraded our growth outlook for China because of the above-mentioned aggressive policy stimulus. It is possible that China’s credit and fiscal impulse will reach about 15% of GDP before year-end (Chart I-5). What presently deters us from recommending outright long positions in China-related plays is the escalating US-China confrontation and the risk of a relapse in global stocks. Central banks around the world both in DM and EM are monetizing debt and injecting immense liquidity into the system. Our interpretation: Correct, but equally relevant is investors’ animal spirits. The latter will determine whether and when these liquidity injections leak into risk assets. For now, it seems that once again central banks’ actions have been successful in lifting asset prices, despite poor fundamentals. Equity valuations are cheap, especially outside the US. This is especially true given the low risk-free rate. Our interpretation: We agree that EM equities are cheap, something we have been highlighting since mid-March (Chart I-6). Yet valuations are not a good timing tool, as they can stay depressed so long as profits are not worsening. Meanwhile, US equities are expensive (Chart I-7). Critically, we argued in a recent report that equity multiples depend not only on the risk-free rate but also on the equity risk premium (ERP). Chart I-6EM Equities Are Cheap

EM Equities Are Cheap

EM Equities Are Cheap

Chart I-7US Stocks Are Expensive

US Stocks Are Expensive

US Stocks Are Expensive

Given the immense ambiguities investors are facing with respect to both the business cycle and economic, political and geopolitical trends, the ERP should be at the upper end of its historical range. Hence, the discount factor – the sum of the risk-free rate and the ERP – should be reasonably high. In this context, US equity valuations are rather expensive, despite the very low risk-free rate. In short, the expensive US stock market has until very recently been the locomotive of this rally. If US share prices had not rallied hard in the past two months, EM and other international bourses would not have caught a bid. The Fed’s public debt monetization is a structural, not near-term negative for the greenback. The US dollar is expensive and will depreciate a lot due to unrestrained fiscal and monetary stimulus in the US. Our interpretation: The US dollar is one standard deviation expensive (Chart I-8) and EM currencies have become cheap (Chart I-9). Chart I-8US Dollar Valuations Are Elevated

US Dollar Valuations Are Elevated

US Dollar Valuations Are Elevated

Chart I-9EM Currencies Are Cheap

EM Currencies Are Cheap

EM Currencies Are Cheap

Chart I-10EM Currencies And Stocks Correlate With Industrial Metals

EM Currencies And Stocks Correlate With Industrial Metals

EM Currencies And Stocks Correlate With Industrial Metals

We do not disagree with the view that the US dollar is vulnerable in the long term due to the Federal Reserve’s aggressive debt monetization and that the Fed will eventually fall behind the inflation curve. Yet inflation is not imminent, and the Fed’s public debt monetization is a structural, not near-term negative for the greenback. As such, these potholes for the US dollar may not be pertinent in the next several months. Critically, Chart I-10 illustrates that EM currencies move with industrial metals prices, and EM stocks correlate with global materials stocks. The common driver of all of these markets is global growth in general and China’s industrial sectors in particular. In short, a recovery in global trade and mainland industrial sectors is necessary for EM equities and currencies to rally on a sustainable basis. Investors are underinvested in global equities in general and cyclical plays in particular. Our interpretation: Indeed, we showed last week that institutional equity investors had been skeptical of this rally. What has driven or supercharged this equity rally since late March has been unsophisticated retail investors. They have been opening up broker accounts worldwide and aggressively trading since March lockdowns. We cited a few pieces of anecdotal evidence confirming this phenomenon in last week’s report. However, it seems that institutional investors in recent weeks have capitulated by raising their risk exposure in general and their exposure to cyclical plays in particular. This explains the recent surge in cyclical equities and currencies. Bottom Line: The narratives driving this rally are only partially correct. Markets are ignoring the particularities of this recession and are treating the post-lockdown activity snapback as a V-shaped recovery. A weaker than expected global recovery and rising geopolitical tensions between the US and China are the two primary risks that will weigh on EM risk assets after this FOMO-driven mania phase runs out of steam. Nuances To Beware Of There are several nuances about the market’s internals and characteristics that we would like to draw investors’ attention to: There is mixed evidence as to whether China’s economy in general and its industrial sectors in particular have entered a sustainable recovery. First, examining the Taiwanese manufacturing PMI data could help in assessing the growth outlook for both the mainland economy and for global trade. The basis is that Taiwan has done extremely well by avoiding COVID-19 outbreaks and lockdowns. Therefore, there are no domestic reasons for weak output growth. In addition, its manufacturing sector is very export-oriented, with about 40% of exports destined for mainland China. PMI export orders for Taiwan's aggregate manufacturing and its three key sectors plunged to new lows in May (Chart I-11). This includes both the electronic optical (semiconductor) and basic materials sectors. The latter correlates well with global materials stocks. There has so far not been a bullish signal from this indicator (Chart I-11, second panel). Second, China’s domestic A-share market in general and its cyclical sectors in particular have not yet broken out (Chart I-12). Given China was the first nation to exit from lockdowns, its share prices should be the first to signal a sustainable economic recovery. Yet onshore share prices have been rather subdued. China’s economy will eventually stage a recovery later this year. Our point is that global cyclicals might have run ahead of themselves by pricing in a recovery too early. Chart I-11Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Taiwanese Manufacturing PMIs In May: New Lows Across All Industries

Chart I-12Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Chinese Onshore Share Prices Are Not Flagging An Imminent Recovery

Equity market and sector leadership changes occur during selloffs or at the inception of rallies. Chart I-13 illustrates EM relative stock prices versus DM along with the global equity index. Over the past 25 years, there have been several major leadership changes between EM and DM. And all of them occurred during selloffs in global share prices. Chart I-13EM Versus DM Equity Leadership Rotations Took Place During Selloffs

EM Versus DM Equity Leadership Rotations Took Place During Selloffs

EM Versus DM Equity Leadership Rotations Took Place During Selloffs

Similarly, the relative performance of global growth versus value stocks experiences trend reversals during global bear markets (Chart I-14). Chart I-14Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Global Growth Versus Value Leadership Rotations Occurred During Bear Markets

Chart I-15EM Could Outperform DM For A Few Weeks

EM Could Outperform DM For A Few Weeks

EM Could Outperform DM For A Few Weeks

Leadership of US equities and global growth stocks did not change during the March crash nor during the following two-month rally from the bottom. Only in the past week or so have US equities and global growth stocks begun to lag EM bourses and global value, respectively (Chart I-15). In brief, the latest leadership rotation from US to EM did not occur during the selloff or at inception of the rally – i.e., it does not fit the typical profile of sustainable leadership reversal. As such, it may not be enduring. The internals of this rally are consistent with the fact that it might already be at a late stage. During rallies, laggards are the last to catch a bid. Contrarily, during selloffs, outperformers are the last to be liquidated. For example, US growth stocks were the last ones to be liquidated in both the 2015-early-2016 and 2018 selloffs. When the decade-long leaders – US growth stocks – were finally stamped out, it marked the bottom of those selloffs. We are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. The Fed’s purchases of US bonds will likely continue pushing investors into EM credit markets. Using an analogous framework for this rally, the latest extraordinary spike in the laggards such as EM, Europe and both value and cyclical stocks could be a sign of bear capitulation, and could signify the final phase of this equity rally. Bottom Line: There are several nuances to the current equity market rally, but investors seem reluctant to consider them amid a FOMO-driven mania. Investment Considerations The FOMO-driven rally could last for several more weeks. Afterwards it will be followed by a major setback. Investors who are long or cannot afford to stay on the sidelines should play this rally with tight stop points. Investors with longer time horizon should wait for a pullback in EM equities and currencies to buy. Chart I-16EM Local Rates Offer Value

EM Local Rates Offer Value

EM Local Rates Offer Value

We are making the following adjustments and changes to our strategy and trade recommendations: In regard to our EM versus DM asset allocation strategy, we are making one change: we are upgrading EM sovereign and corporate credit from underweight to neutral within a global credit portfolio. The Fed’s purchases of US bonds will likely continue pushing investors into EM credit markets. Consistently, we are closing two positions: (1) our short EM corporate and sovereign credit / long US investment-grade corporate bond trade; and (2) our long Asian investment-grade /short high-yield corporate bond trade. Within the EM credit space, we continue to favor sovereigns versus corporates – a strategy recommended on April 23. We are still reluctant to strategically upgrade EM stocks versus DM ones even though odds of EM outperforming DM stocks are high in the coming weeks. In light of the potential FOMO-driven rally, to protect profits we are closing the following two currency positions: Take profits on short BRL/long USD trade. It was initiated on November 29, 2019 and has produced a 19% gain. Book profits on short SGD/long JPY position. This recommendation has generated a 2.3% gain since its initiation on June 8, 2018. We are still maintaining shorts in the following EM currencies: CLP, ZAR, TRY, IDR, PHP and KRW. They could continue rallying in the near term but will relapse afterwards. We are also structurally short low beta currencies: the RMB and the Saudi riyal. Within EM, local rates offer the best risk-reward profile: they will perform well in both risk-on and risk-off phases. Real bond yields remain somewhat elevated in many EMs, as shown in Chart I-16. We continue to receive long-term rates in Mexico, Colombia, Russia, Ukraine, India, Pakistan, Malaysia, China and Korea, as well as 2-year rates in South Africa. Their central banks will reduce policy rates much further. In addition, several of these local bond markets will benefit from ongoing quantitative easing by their central banks. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights The Chinese economy continues to recover, albeit less quickly than the first two months following a re-opening of the economy. The demand side of the Chinese economic recovery in May marginally outpaced the supply side, with a notable improvement concentrated in the construction sector. We are initiating two new trades: long material sector stocks versus the broad indices, in both onshore and offshore equity markets. Feature The recovery in China’s economy and asset prices has entered a “tapering phase”, in which the speed of the recovery is normalizing from a rapid rebound two months after the economy re-opened. The direction of the ultra-accommodative monetary and fiscal stance has not changed, but the aggressiveness in the stimulus impulse is abating as the recovery continues. As we highlighted in last week’s report, the announced stimulus at this year's NPC was less than meets the eye of investors.1 Chart 1A Quick Reversal In The Outperformance Of Chinese Stocks

A Quick Reversal In The Outperformance Of Chinese Stocks

A Quick Reversal In The Outperformance Of Chinese Stocks

Near-term downside risks in Chinese stocks were highlighted by last week’s quick reversal in the outperformance of Chinese equities relative to global benchmarks (Chart 1). As the US and European economies re-open and the stimulus impulse in major developed markets (DMs) is at peak intensity, Chinese stocks will underperform those in DMs, particularly US stocks. The re-escalation in Sino-US tensions will also add to the near-term volatility in Chinese equities. Therefore, we maintain our tactical (0-3 months) neutral view on aggregate Chinese equity indexes, in both domestic and offshore markets. Beyond Q2, however, our baseline view still supports an outperformance in Chinese stocks. The stepped-up stimulus measures since March should start to trickle down into the broader economy. Global business activities and demand will slowly normalize in the summer, helping to revive China’s exports. Moreover, an intensified pressure on employment, indicated in this month’s employment subcomponents in manufacturing and non-manufacturing PMIs, should prompt policymakers to roll out more growth-supporting measures in Q3. Tables 1 and 2 below highlight key developments in China’s economic and financial market performance in the past month. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Chart 2ASpeed Of Manufacturing Activity Recovery Has Moderated

Speed Of Manufacturing Activity Recovery Has Moderated

Speed Of Manufacturing Activity Recovery Has Moderated

China’s official manufacturing PMI slipped to 50.6 in May from 50.8 a month earlier (Chart 2A). While the reading suggests that manufacturing activities are still in an expansionary mode, the speed of the expansion has moderated compared with April and March. The supply side of manufacturing activities and employment were the biggest drags on May’s official PMI. The production subcomponent in the PMI decelerated whereas new orders increased from April (Chart 2A, bottom panel). The net result is an improved supply-demand balance in the manufacturing sector, however, the improvement is marginal. It also differs from the V-shaped recovery in 2008/09, when both new orders and production subcomponents grew simultaneously (Chart 2B). The demand side of the economy is still concentrated in the policy-driven construction sector. The rebound in construction PMI continues to significantly outpace that in manufacturing and non-manufacturing PMIs (Chart 2C, top panel). The construction employment sub-index ticked up by 1.7 percentage points in May, compared with a slowdown of 0.8 percentage points in manufacturing and 0.1 percentage points in non-manufacturing employment PMIs (Chart 2C, bottom panel). Chart 2BDemand Struggles To Outpace Supply

Demand Struggles To Outpace Supply

Demand Struggles To Outpace Supply

Chart 2CDemand Recovery Is Concentrated In Construction

Demand Recovery Is Concentrated In Construction

Demand Recovery Is Concentrated In Construction

While a buoyant construction sector should provide a strong tailwind to raw material prices and related machinery sales, a laggard recovery from other sectors means the upside potential in aggregate producer prices (PPI) will be limited in the current quarter. In May, there was a rebound in the PMI sub-indices measuring raw material purchase prices and ex-factory prices, which heralds easing in the contraction of PPI in Q2 (Chart 3). However, neither of the PMI price sub-indices has returned to levels reached in January, when PPI growth was last positive. Moreover, weaker readings in the purchases and raw material inventory subcomponents suggest that manufacturers may be reluctant to restock due to sluggish global trade and a lagging rebound in domestic demand (Chart 3, bottom panel). This month’s PMI shows that the employment subcomponents in both the manufacturing and non-manufacturing PMIs are contracting (Chart 4). Because demand for Chinese export goods remains sluggish, we expect unemployment in China’s labor-intensive export manufacturing sector to rise in Q2 and even into Q3. The intensified pressure on employment will likely prompt Chinese policymakers to roll out more demand-supporting measures. Chart 3PPI Contraction Will Ease But Upside Limited In Q2/Q3

PPI Contraction Will Ease But Upside Limited In Q2/Q3

PPI Contraction Will Ease But Upside Limited In Q2/Q3

Chart 4Employment In Trouble, A Catalyst For More Easing

Employment In Trouble, A Catalyst For More Easing

Employment In Trouble, A Catalyst For More Easing

The BCA Li Keqiang Leading Indicator rose moderately in April. A plunge in the Monetary Conditions Index (MCI) limited the magnitude of the indicator's increase, offsetting an uptick in money supply and credit growth (Chart 5). A rapid disinflation in headline consumer prices (CPI) since the beginning of this year has pushed up the real savings deposit rate, which contributed to the MCI’s nose-dive. In our view, the MCI’s sharp drop is idiosyncratic and does not signify a tightening in the PBoC’s monetary stance or overall monetary conditions. Huge fluctuations in food prices have been driving the headline CPI since March 2019, while the core CPI remains stable. While food prices historically have very little correlation with the PBoC's monetary policy actions, a disinflationary environment will provide the central bank more room for easing. Odds are high that the PBoC will cut the savings deposit rate for the first time since 2015. Chart 5Monetary Conditions Are Not As Tight As The Indicator Suggests

Monetary Conditions Are Not As Tight As The Indicator Suggests

Monetary Conditions Are Not As Tight As The Indicator Suggests

The yield curve in Chinese government bonds quickly flattened around the time of the National People’s Congress (NPC), with the short end of the curve rising faster than the long end (Chart 6). This is in keeping with our assessment that while the market is expecting the recovery to continue in China, it is unimpressed with the intensity of upcoming stimulus and monetary easing. Monetary easing seems to be taking a pause, but we do not think this indicates a change in the PBoC’s policy stance (Chart 7). Instead, weak global demand, slow recovery in the domestic economy and intensified pressure on domestic employment, all will incentivize policymakers to up their game by mid-year. As such, we expect the yield curve to steepen again in H2, with the short-end of the curve fluctuating at a low level and the 10-year government bond yield picking up when the economy gains traction. Chart 6The Bond Market May Be Incorrectly Pricing In A Monetary Tightening

The Bond Market May Be Incorrectly Pricing In A Monetary Tightening

The Bond Market May Be Incorrectly Pricing In A Monetary Tightening

Chart 7A Pause Before More Easing In June

A Pause Before More Easing In June

A Pause Before More Easing In June

The spread in Chinese corporate bond yields has dropped by more than 30bps from its peak in April. This is in line with that of major DM countries and a reflection of the easier liquidity conditions globally (Chart 8). We anticipate that the yield spreads in Chinese corporate bonds will continue to normalize. However, a flare in US-China tensions will put upward pressure on the financing costs of lower-rated corporations (Chart 8, bottom panel). The default rate among Chinese corporate bonds is unlikely to rise meaningfully this year, in light of ultra-accommodative monetary conditions and the Chinese government’s bailout programs to backstop corporate defaults. Chinese corporate bond defaults and non-performing loans historically have correlated with periods of financial sector de-leveraging and de-risking, other than during economic downturns. We continue to recommend investors hold China’s corporate bonds in the coming 6-12 months in a USD-CNH hedged term. Chart 8Financing Costs May Rise For Lower-Rated Corporations

Financing Costs May Rise For Lower-Rated Corporations

Financing Costs May Rise For Lower-Rated Corporations

Chart 9Cyclicals Are Struggling To Break Out

Cyclicals Are Struggling To Break Out

Cyclicals Are Struggling To Break Out

Among Chinese equities, cyclical sectors have struggled to outperform defensives in both onshore and offshore markets (Chart 9). This reflects investors’ concerns over the slow recovery in domestic demand and heightened geopolitical risk between the US and China. As such, we continue to favor domestic, demand-driven sectors among the cyclical stocks, such as consumer discretionary and construction-related materials. We upgraded consumer discretionary stocks from neutral to overweight on May 20, and we are now initiating two trades to long material sector stocks versus the broad markets in both the domestic and investable markets. The constituents of both China’s investable and domestic material sectors are highly concentrated in the metal and mining subsectors, which roughly account for half of the material sectors’ weight in the MSCI and MSCI A Onshore Indexes, respectively. Chart 10 highlights that the material sectors’ relative performance is highly correlated with CRB raw materials in both domestic and investable markets. Given that China’s credit cycles historically lead the CRB material index by about six months, China’s massive credit stimulus will boost CRB raw materials by end-Q2 and thus, the outperformance of the material sectors. The RMB has depreciated by almost 3% in the wake of a re-escalation in US-China frictions. The CNY/USD spot rate is approaching its weakest point reached in September 2019 (Chart 11). Furthermore, on May 29, the PBoC set the CNY/USD reference rate at its lowest level since 2008, a move that suggests defending the RMB is no longer in China’s interest. Downward pressure on the RMB will persist in the months leading up to the November US presidential election. The US economy is in a much more fragile state than in 2018/19, which may hinder President Trump’s willingness to resort to tariffs between now and November. However, we cannot completely roll out the probability that Trump will impose further tariffs on Chinese exports, if he is losing the election through weak public support and is removed from his financial and economic constraints. In any case, in the coming months CNY/USD exchange rate will likely continue to decouple from the economic fundamentals such as interest rate differentials (Chart 11, bottom panel). Instead, the exchange rate will be largely driven by market sentiment surrounding the US-China frictions. Volatility in CNY/USD will increase, but the overall trend in the CNY/USD will continue downwards as long as the escalation in US-China tensions persists. On a 6- to 12-month horizon, however, we expect that the depreciation trend in the RMB to moderately reverse as the Chinese economy continues to strengthen. Chart 10Material Sectors Should Benefit From The Stimulus And Construction Boom

Material Sectors Should Benefit From The Stimulus And Construction Boom

Material Sectors Should Benefit From The Stimulus And Construction Boom

Chart 11The CNY/USD Will Continue To Decouple From Interest Rate Differentials

The CNY/USD Will Continue To Decouple From Interest Rate Differentials

The CNY/USD Will Continue To Decouple From Interest Rate Differentials

Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 Please see China Investment Strategy Weekly Report "Taking The Pulse Of The People’s Congress," dated May 28, 2020, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

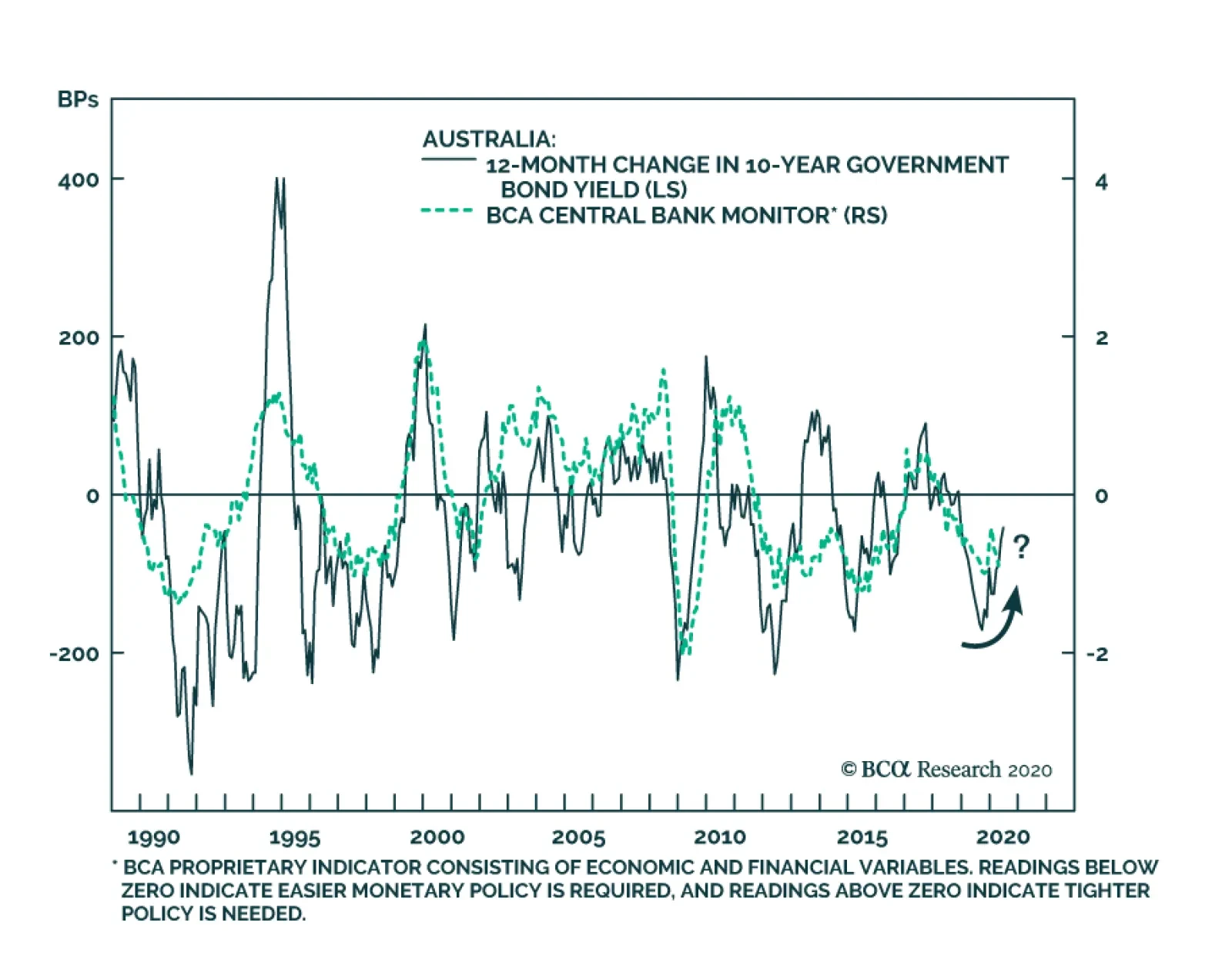

BCA Research's Global Fixed Income Strategy service's Reserve Bank of Australia (RBA) monitor may be turning the corner after Australia delivered 125bps of stimulus since June 2019. The Australian unemployment gap has widened dramatically, owing to job…

Highlights In this Weekly Report, we present our semi-annual chartbook of the BCA Central Bank Monitors. All of the Monitors are now below the zero line, indicating the need for continued easy global monetary policy to help mitigate the COVID-19 recession (Chart of the Week). Central bankers have already responded in an intense and rapid fashion to the crisis, delivering a series of rate cuts, increased asset purchase programs and measures to support bank lending to businesses suffering under quarantines. All of these vehicles have helped trigger a powerful rally in global bond markets that helped revitalize risk assets as well. After the coordinated global easing response of the past few months, the optimal policy choices now differ from country to country. This creates opportunities to benefit from country allocation decisions even in a world of puny government bond yields. The overall signal from our Central Bank Monitors is still bond bullish, however – at least over the next few months until there is evidence of how fast global growth is rebounding from the COVID-19 lockdowns. An Overview Of The BCA Central Bank Monitors Chart of the WeekUltra-Accommodative Monetary Policies Are Still Required

Ultra-Accommodative Monetary Policies Are Still Required

Ultra-Accommodative Monetary Policies Are Still Required

Chart 2A Bond-Bullish Message From Our CB Monitors

A Bond-Bullish Message From Our CB Monitors

A Bond-Bullish Message From Our CB Monitors

The BCA Central Bank Monitors are composite indicators designed to measure the cyclical growth and inflation pressures that can influence future monetary policy decisions. The economic data series used to construct the Monitors are not the same for every country, but the list of indicators generally measure the same things (i.e. manufacturing cycles, domestic demand strength, commodity prices, labor market conditions, exchange rates, etc). The data series are standardized and combined to form the Monitors. Readings above the zero line for each Monitor indicate pressures for central banks to raise interest rates, and vice versa. Through the nexus between growth, inflation, and market expectations of future interest rate changes, the Monitors do exhibit broad correlations to government bond yields in the Developed Markets (Chart 2). All of the Monitors are indicating intense pressure to maintain very easy monetary policies in response to the global COVID-19 recession. While the bad economic and inflation news is largely discounted in the depressed level of bond yields worldwide, there are still opportunities to position country allocations within a government bond portfolio based on the message from our Monitors (overweighting the US, the UK and Canada, underweighting Germany and Japan). All of the Monitors are indicating intense pressure to maintain very easy monetary policies in response to the global COVID-19 recession. In each BCA Central Bank Monitor Chartbook, we include a new chart for each country that we have not shown previously. In this edition, we show the components of the Monitors, grouped into those focusing on economic growth and inflation, plotted alongside our estimate of the appropriate level of central bank policy interest rates derived using a Taylor Rule. Fed Monitor: Policy Must Stay Accommodative Our Fed Monitor has collapsed below the zero line to recessionary levels (Chart 3A) in response to the coronavirus crisis. The Fed has already delivered a series of aggressive policy responses since March to help support an economy ravaged by the virus, including: interest rate cuts; quantitative easing (QE), including buying corporate and municipal debt; and setting up lending schemes for small businesses. The lockdown of almost the entire country has helped “flatten the curve” of the spread of COVID-19, but at a painful economic cost. The unemployment rate rose to 14.7% in April, the highest level since the Great Depression, and is expected to peak at levels above 20%. The result is unsurprising: a massive increase in spare economic capacity with a threat of deflation as headline CPI inflation plummeted to 0.3% in April (Chart 3B). Chart 3AUS: Fed Monitor

US: Fed Monitor

US: Fed Monitor

Chart 3BUS Realized Inflation Flirting With 0%

US Realized Inflation Flirting With 0%

US Realized Inflation Flirting With 0%

Within the components of our Fed Monitor, weakening growth has been the main driver of the decline (Chart 3C). Our Taylor Rule estimate suggests a deeply negative fed funds rate is “appropriate”, although the Fed is likely to pursue other avenues of easing like yield curve control before ever attempting a sub-0% policy rate. Chart 3CNegative Rates Are 'Required' In The US, But The Fed Has Other Options

Negative Rates Are 'Required' In The US, But The Fed Has Other Options

Negative Rates Are 'Required' In The US, But The Fed Has Other Options

The fall in US Treasury yields over the past few months has been in line with the decline in our Fed Monitor (Chart 3D). While the US economy is slowly awakening from lockdowns, consumer and business confidence are likely to remain fragile given the numerous risks from a second wave of COVID-19, worsening US-China relations and, more recently, social unrest. Thus, we continue to recommend an overweight strategic allocation to the US within global government bond portfolios. The fall in US Treasury yields over the past few months has been in line with the decline in our Fed Monitor Chart 3DTreasury Yields Fully Reflect Pressure For More Fed Easing

Treasury Yields Fully Reflect Pressure For More Fed Easing

Treasury Yields Fully Reflect Pressure For More Fed Easing

BoE Monitor: Negative Rates On The Horizon? Our Bank of England (BoE) Monitor has collapsed to the lowest level in its history on the back of the severe COVID-19 recession (Chart 4A). The BoE already cut the Bank Rate to 0.1% in March, ramped up asset purchases, and introduced a Term Funding scheme to support business lending. Any additional easing from here might entail negative policy rates, which markets are already discounting. The UK unemployment rate is expected to peak around 8%, with the BoE projecting the economy to shrink by -14% this year, which would be the worst recession in modern history. Inflation has dropped sharply on the back of the dual collapse of energy prices and economic growth, ending a period of currency-fueled inflation increases (Chart 4B). Chart 4AUK: BoE Monitor

UK: BoE Monitor

UK: BoE Monitor

Chart 4BUK Realized Inflation Is Slowing Rapidly

UK Realized Inflation Is Slowing Rapidly

UK Realized Inflation Is Slowing Rapidly

The components of our BoE Monitor fully reflect the dire economic situation (Chart 4C), with weak growth – led by sharp falls in business confidence – driving the collapse of the Monitor more than falling inflation pressures. Our Taylor Rule estimate of the policy rate is not yet calling for negative rates, but that is because we are using the New York Fed’s estimate of r* as the neutral real rate, which is a relatively high 1.4% (by comparison, r* in the US is estimated to be 0.5%). Chart 4CNegative Rates Are Not Yet Required In The UK

Negative Rates Are Not Yet Required In The UK

Negative Rates Are Not Yet Required In The UK

The sharp fall in the BoE Monitor suggests that Gilt yields will remain under downward pressure in the coming months (Chart 4D). New BoE Governor Andrew Bailey has stated that a move to negative rates is not imminent, but markets will continue to flirt with the notion of sub-0% interest rates until the economy and inflation stabilize. We maintain an overweight stance on UK Gilts. Chart 4DBoE Monitor Suggests Continued Downward Pressure On Gilt Yields

BoE Monitor Suggests Continued Downward Pressure On Gilt Yields

BoE Monitor Suggests Continued Downward Pressure On Gilt Yields

ECB Monitor: Continued Monetary Support Is Needed Our European Central Bank (ECB) Monitor is now well below the zero line, signaling a strong need for easier monetary policy to fight the COVID-19 downturn (Chart 5A). The ECB has delivered multiple measures to ease monetary conditions, including a new €750bn bond-buying vehicle and liquidity operations to help banks maintain lending to European businesses. The recession has hit the region hard, with real GDP declining by -3.8% in Q1, the sharpest fall since records began in 1995. Unemployment rates have climbed higher, although to much lower levels than seen in the US thanks to more generous government labor support programs that have helped to limit layoffs. The sharp downturn has resulted in both a surge in spare economic capacity and plunge in headline inflation to 0.3% in April (Chart 5B). Chart 5AEuro Area: ECB Monitor

Euro Area: ECB Monitor

Euro Area: ECB Monitor

Chart 5BEurope Is On The Edge Of Deflation

Europe Is On The Edge Of Deflation

Europe Is On The Edge Of Deflation

Within the individual components of our ECB Monitor, both weaker growth and near-0% inflation have both contributed to the Monitor’s decline (Chart 5C). Our Taylor Rule measure shows that the ECB’s current stance of having policy rates modestly below 0% is appropriate. Chart 5CThe ECB Needs To Keep Its Foot On The Monetary Accelerator

The ECB Needs To Keep Its Foot On The Monetary Accelerator

The ECB Needs To Keep Its Foot On The Monetary Accelerator

Despite the ECB’s easing measures, and in contrast to the message from our ECB Monitor, the downward momentum in core European bond yields has been fading (Chart 5D). With the ECB reluctant to push policy rates deeper into negative territory, and with reliable cyclical indicators like the German ZEW and IFO surveys showing signs that euro area growth is starting to recover from the lockdowns, the case for even lower core European yields in the coming months is not strong. We maintain our recommended underweight stance on German and French government bonds. We maintain our recommended underweight stance on German and French government bonds. Chart 5DNo Pressure For Higher German Bund Yields

No Pressure For Higher German Bund Yields

No Pressure For Higher German Bund Yields

BoJ Monitor: What More Can Be Done? Our Bank of Japan (BoJ) Monitor has fallen further below zero, indicating easier policy is required (Chart 6A). The BoJ has already introduced additional easing measures in the past couple of months: extending forward guidance (inflation is projected to remain below the BoJ’s 2% target for the next three years), increasing asset purchases and enhancing loan programs to small and medium sized companies. New cases of COVID-19 have slowed sharply in Japan, prompting an end to the national state of emergency last week. Importantly, the virus did not hit Japan's labor market as severely as in other developed countries. The unemployment rate did reach a two-year high in April, but is still only 2.6% (Chart 6B). Fiscal stimulus and measures to protect job losses have played a major role in preventing a bigger spike in joblessness. Even with those measures, growth remains weak and realized inflation is heading back towards deflation. Chart 6AJapan: BoJ Monitor

Japan: BoJ Monitor

Japan: BoJ Monitor

Chart 6BJapan Nearing Deflation Once Again

Japan Nearing Deflation Once Again

Japan Nearing Deflation Once Again

Looking at the components of our BoJ Monitor, contracting growth, more than weakening inflation pressures, is the bigger driver of the fall in the Monitor below zero (Chart 6C). However, our Taylor Rule estimate does not suggest that the current level of the policy rate is out of line. Chart 6CBoJ Needs More Easing (Somehow) Until The Economy Revives

BoJ Needs More Easing (Somehow) Until The Economy Revives

BoJ Needs More Easing (Somehow) Until The Economy Revives

The BoJ’s current combined policies of negative rates, QE and yield curve control are keeping JGB yields at near-0% levels. Those policies are also suppressing yield volatility and preventing an even bigger fall in JGB yields (with larger capital gains) as suggested by our BoJ Monitor (Chart 6D). We continue to recommend a maximum underweight in Japanese government bonds in a yield-starved world. Chart 6DJGB Yields Will Be Anchored For Some Time

JGB Yields Will Be Anchored For Some Time

JGB Yields Will Be Anchored For Some Time

BoC Monitor: Deflationary Pressures Intensifying Our Bank of Canada (BoC) Monitor has collapsed into “easier policy required” territory, reaching levels last seen during the 2009 recession (Chart 7A). The central bank has already introduced several easing measures to help boost the virus-stricken economy, including cutting the Bank Rate to a mere 0.25% and starting a QE program to buy government bonds for the first time ever. Before the COVID-19 outbreak, some softening of the economy was already underway. Now, after the imposition of nationwide lockdowns to limit the spread of the virus, the unemployment rate has spiked to 13% - a level last seen in the early 1980s. The result is a massive deflationary output gap has opened up (Chart 7B), with realized headline CPI inflation printing at -0.2% in April. Chart 7ACanada: BoC Monitor

Canada: BoC Monitor

Canada: BoC Monitor

Chart 7BOutright Headline CPI Deflation In Canada

Outright Headline CPI Deflation In Canada

Outright Headline CPI Deflation In Canada

The fall in our BoC Monitor has been driven by both collapsing economic growth and weakening inflation pressures (Chart 7C). Our Taylor Rule estimate suggests that one of new BoC Governor Tiff Macklem’s first policy decisions may need to be a move to negative interest rates. Macklem and other BoC officials have not played up the possibility of cutting rates below 0%. However, the fact that the BoC provided no economic growth forecasts in the most recent Monetary Policy Report highlights the extreme uncertainties surrounding the economic impact from COVID-19 – even with the Canadian government providing a large fiscal response to the pandemic. Chart 7CBoC Monitor Plunging Due To High Unemployment & Low Inflation

BoC Monitor Plunging Due To High Unemployment & Low Inflation

BoC Monitor Plunging Due To High Unemployment & Low Inflation

We upgraded our recommended stance on Canadian government debt to overweight back in March, and the collapse of the BoC Monitor suggests continued downward pressure on Canadian yields (Chart 7D). Stay overweight. The collapse of the BoC Monitor suggests continued downward pressure on Canadian yields. Chart 7DCanadian Yield Momentum In Line With The BoC Monitor

Canadian Yield Momentum In Line With The BoC Monitor

Canadian Yield Momentum In Line With The BoC Monitor

RBA Monitor: Rate Cutting Cycle Is Done Due to a slump in export demand and a weakening housing market, our Reserve Bank of Australia (RBA) monitor has been consistently calling for rate cuts since April 2018 (Chart 8A). Australia began its easing cycle early, having delivered a total of 125bps of stimulus since June 2019, with the two most recent cuts coming directly in response to the COVID-19 crisis. As in other developed markets, the unemployment gap in Australia has widened dramatically, owing to job losses concentrated in tourism, entertainment, and dining out (Chart 8B). Although inflation briefly breached the low end of the RBA’s 2-3% target band in Q1, this will not be a lasting development. The RBA sees headline CPI deflating by -1% year-on-year in Q2/2020 and, even as far as 2022, only sees it growing at 1.5%. Chart 8AAustralia: RBA Monitor

Australia: RBA Monitor

Australia: RBA Monitor

Chart 8BInflation Will Remain Stuck Below RBA 2-3% Target

Inflation Will Remain Stuck Below RBA 2-3% Target

Inflation Will Remain Stuck Below RBA 2-3% Target

Although both the growth and inflation components of our RBA Monitor are below zero, the former drove the most recent decline (Chart 8C) led by consumer confidence almost touching the 2008 lows. The RBA has already responded by cutting rates to near 0%, well below the Taylor Rule implied estimate, and initiating yield curve control with a cap on 3-year government bond yields at 0.25%. Chart 8CNo Pressure For The RBA To Go To Negative Rates

No Pressure For The RBA To Go To Negative Rates

No Pressure For The RBA To Go To Negative Rates

Overall, Australian bond yields have accurately priced in the dovish signal from our RBA Monitor (Chart 8D). With COVID-19 relatively well contained in Australia, there is less pressure on the RBA to ease further. Governor Lowe has also ruled out negative rates, which will put a floor under yields. Owing to these factors, we confidently reiterate our neutral stance on Australian government debt within global fixed income portfolios. Australian bond yields have accurately priced in the dovish signal from our RBA Monitor. Chart 8DAustralian Bond Yields Are Unlikely To Move Much Lower

Australian Bond Yields Are Unlikely To Move Much Lower

Australian Bond Yields Are Unlikely To Move Much Lower

RBNZ Monitor: Cause For Concern After a resurgence late last year, our Reserve Bank of New Zealand (RBNZ) Monitor has declined to a level slightly below zero (Chart 9A). The RBNZ responded to the pandemic by delivering a massive -75bps cut in March, but has since left the policy rate untouched, preferring to deliver further stimulus by doubling the size of its QE program. Forward guidance is signaling that the policy rate will remain at 0.25% until 2021, but the central bank has not ruled out negative rates in the future. Although the actual unemployment numbers do not yet capture the impact of the pandemic, both consensus and RBNZ forecasts call for a blowout in the unemployment gap (Chart 9B). The RBNZ expects the steady improvement in inflation seen up to Q1/2020 to be wiped out, with headline CPI projected to remain below the 1-3% target range until mid-2022. Chart 9ANew Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

Chart 9BRealized NZ Inflation Was Drifting Higher, Pre-Virus

Realized NZ Inflation Was Drifting Higher, Pre-Virus

Realized NZ Inflation Was Drifting Higher, Pre-Virus

Surprisingly, the inflation component of our RBNZ Monitor is actually calling for tighter monetary policy, owing to significant strength in the housing market (Chart 9C). However, this trend is likely to reverse - the RBNZ foresees a -9% decline in house prices over the remainder of 2020. Meanwhile, growth components such as consumer confidence and employment will remain depressed, holding down our RBNZ monitor. Chart 9CGrowth, Now Inflation, Has Driven The RBNZ Monitor Lower

Growth, Now Inflation, Has Driven The RBNZ Monitor Lower

Growth, Now Inflation, Has Driven The RBNZ Monitor Lower

Overall, the momentum in New Zealand bond yields seems to have overshot the message from our RBNZ Monitor (Chart 9D). However, with so much uncertainty about business investment and cash flows from key sectors such as tourism and education, it is too early to bet on an improvement in yields. We therefore maintain a neutral recommendation on NZ sovereign debt. Chart 9DNZ Bond Yields Are Unlikely To Move Lower

NZ Bond Yields Are Unlikely To Move Lower

NZ Bond Yields Are Unlikely To Move Lower

Riksbank Monitor: Worries For The Coronavirus Mavericks Amid the global pandemic, our Riksbank Monitor has collapsed to all-time lows (Chart 10A). In its April monetary policy decision, the Riksbank opted for continued asset purchases and liquidity measures to support bank lending to companies over a move to negative rates. One of the primary concerns for the Riksbank is headline CPI inflation, which fell into mild deflation (-0.4% year-over-year) in April on the back of lower energy prices and weaker domestic demand (Chart 10B). This could spill over into a lasting decline in long-term inflation expectations if the economy does not quickly improve. Chart 10ASweden: Riksbank Monitor

Sweden: Riksbank Monitor

Sweden: Riksbank Monitor

Chart 10BSwedish Realized Inflation Back To 0%

Swedish Realized Inflation Back To 0%

Swedish Realized Inflation Back To 0%

Both the growth and inflation components of our Riksbank Monitor are calling for further easing, with the growth component now at post-crisis lows (Chart 10C). The collapse on the growth side can be attributed to historic falls in retail confidence, the manufacturing PMI and employment while the inflation component remains depressed due to low headline numbers and inflation expectations. Chart 10CThe Riksbank Hates Negative Rates, But Could Still Need Them If The Economy Worsens

The Riksbank Hates Negative Rates, But Could Still Need Them If The Economy Worsens

The Riksbank Hates Negative Rates, But Could Still Need Them If The Economy Worsens

The sharp downward move in our Riksbank Monitor suggests Swedish bond yields should remain under downward pressure in the coming months (Chart 10D). The key factor for yields will be the effect of the relatively lax measures implemented by Sweden to combat the pandemic. Sweden saw positive GDP growth in Q1/2020 due to fewer restrictions on the economy. However, infection and mortality rates are much higher in Sweden than in neighboring countries and, as a result, Denmark and Norway excluded Sweden from their open border agreement. Continued restrictions of the sort are bearish for growth – and bullish for bonds – in this trade-dependent economy. Chart 10DSwedish Bond Yields Will Remain Under Downward Pressure

Swedish Bond Yields Will Remain Under Downward Pressure

Swedish Bond Yields Will Remain Under Downward Pressure

Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Shakti Sharma Research Associate ShaktiS@bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

BCA Central Bank Monitor Chartbook: Collapse

BCA Central Bank Monitor Chartbook: Collapse

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

The COVID-19 induced recession has accelerated several paradigm shifts that were already afoot. Populism, anti-immigrant sentiment, deglobalization, and fiscal profligacy were replete – particularly in the US – even before the pandemic. For the first time since WWII, the US budget deficit significantly expanded for three years running at a time when the unemployment rate was declining, late in the cycle. We fear that the Washington Consensus – a catchall term for fiscal prudence, laissez-faire economics, free trade, and unfettered capital flows – is being replaced by economic populism, by a Buenos Aires Consensus, as our geopolitical strategists have posited in the past. Buenos Aires Consensus is our catchall term for everything that is opposite of the Washington Consensus: less globalization, fiscal stimulus as far as the eyes can see, erosion of central bank independence, and a dirigiste (as opposed to laissez-faire) approach to economics that seeks to protect “state champions,” stifles innovation, and ultimately curbs productivity growth. The most important long-term consequence of the Buenos Aires Consensus will be higher inflation. And we are not talking just the asset price kind – which investors have enjoyed over the past decade – but of the more traditional flavor: consumer price inflation (Chart 1). Chart 1Inflation Is Coming

Inflation Is Coming

Inflation Is Coming

A profligate US government where $3 trillion + fiscal packages are passed with a strong bipartisan consensus, rising odds of increased defense and infrastructure spending, a renewed focus on protecting America’s industrial champions from competition (foreign or domestic), and a robust protectionist agenda (again, on both sides of the aisle), are all inherently inflationary and negative for bonds, ceteris paribus. A whiff of inflation would be a positive for the broad equity market, further fueling the “risk on”, liquidity-driven, melt-up phase. However, historically when inflation has entered the 3.7%-4% zone in the past, the broad equity market has stumbled (Chart 2). Despite these powerful longer-term inflationary forces, our working assumption is that, in the next 9-12 months, headline CPI inflation will only renormalize, rather than surge, as the coronavirus-induced deficient demand and excess supply dynamic will take time to reach a new equilibrium (Chart 3). Chart 2Only A Whiff Of Inflation Is Good For Stocks

Only A Whiff Of Inflation Is Good For Stocks

Only A Whiff Of Inflation Is Good For Stocks

Importantly, the magnitude of the economic damage, the likelihood that a “second wave” requires renewed lockdowns, and a new steady state of the apparent “square root” type of recovery remain unknown. This means that “deflationistas” may continue to have an upper hand on the “inflationistas”, as witnessed by the subdued inflation expectations (Chart 3). Chart 3In The Near-Term Disinflation Looms

In The Near-Term Disinflation Looms

In The Near-Term Disinflation Looms

The Federal Reserve’s Function As The Lender Of Last Resort What is certain is the Fed’s resolve to keep things gelled together and allow businesses and the economy enough time to heal and overcome the coronavirus shock. Simply put, there are high odds that the Fed will remain accommodative and take inflation risk “sitting down” for quite some time, certainly for the next year, and likely longer (Chart 4). While early on, the Powell-led Fed had been ambivalent, the FOMC’s swift and immense response to the coronavirus calamity with unorthodox monetary policies has been appropriate and unprecedented (Chart 5). Clearly, the sloshing liquidity cannot cure the coronavirus, but providing the credit needed in parts of the financial markets and select business sectors that had completely dried up was the proper policy response. The Fed acted promptly as a lender of last resort. Unlike the difficulty in defeating deflation – look no further than Japan – ending inflation is easy. The great Paul Volcker has taught the Fed and the world how to break the back of inflation. The Fed, therefore, has the credible tools to deal with a possible inflationary impulse. Chart 4Do Not Fight The Mighty Fed

Do Not Fight The Mighty Fed

Do Not Fight The Mighty Fed

Chart 5Joined At The Hip

Joined At The Hip

Joined At The Hip

Until economic growth regains its footing and climbs to its post-GFC steady 2-2.5% real GDP growth profile, the probability is high that the Fed will take some inflation risk (Chart 6). Chart 6The Fed Can Afford To Take Inflation Risk

The Fed Can Afford To Take Inflation Risk

The Fed Can Afford To Take Inflation Risk

This is especially the case given that political risk in the US is tilted to the downside. With income inequality at nose bleeds levels, US policymakers (both fiscal and monetary authorities) will hesitate to act on the inflation mandate with gusto and objectivity (Chart 7). Chart 7The Apex Of Globalization And Income Inequality

The Apex Of Globalization And Income Inequality

The Apex Of Globalization And Income Inequality

The Fed will therefore not rush to abruptly tighten monetary policy, a view confirmed by the bond market: fed funds futures are penciling a negative fed funds rate in mid-2021 and ZIRP as far as the eye can see (Chart 8). A sustainable breakout in bond yields would require inflation (and to a lesser extent real GDP growth) to significantly surprise to the upside, which would compel the Fed to aggressively raise the fed funds rate. But that is not on the immediate horizon especially given the recent coronavirus-related blow to unit labor costs (please see Appendix below). Even if there were an inflationary backup in longer term Treasury yields, yield curve control is a tool the Fed is considering, something it first tried on the Treasury’s orders during and following WWII for a nine year period. Chart 8ZIRP As Far As The Eye Can See

ZIRP As Far As The Eye Can See

ZIRP As Far As The Eye Can See

Dollar And The Inflationary Valve Importantly, the US dollar’s direction will be critical in determining whether any lasting inflation acceleration occurs. The top panel of Chart 9 shows that inflation accelerates during U.S. dollar bear markets. A depreciating greenback greases the wheels of the global financial system and also serves as a global growth locomotive given that trade is largely conducted in US dollars (bottom panel, Chart 9). Thus, the Fed’s recent US dollar swap lines to other Central Banks, along with its FIMA facility, were instrumental in unclogging the global financial system. Sloshing US dollar liquidity restored a semblance of normality to asset prices (Chart 10). Chart 9Inversely Correlated

Inversely Correlated

Inversely Correlated

Chart 10Ample Liquidity To Debase The Greenback

Ample Liquidity To Debase The Greenback

Ample Liquidity To Debase The Greenback

As we highlighted in our December 16 Special Report titled “Top US Sector Investment Ideas For The Next Decade” ,1 there are rising odds that a US dollar bear market takes root this decade. Eventually, the steeper the greenback’s fall, the higher the chance of a longer lasting inflationary spurt as US import price inflation will rear its ugly head (Chart 11). Chart 11US Dollar Bear Markets Are Synonymous With Inflation

US Dollar Bear Markets Are Synonymous With Inflation

US Dollar Bear Markets Are Synonymous With Inflation

So What? While, in the near-term, accelerating inflation is a negligible risk owing to excess economic slack, in the intermediate-term, it is a rising probability outcome. BCA’s long-held de-globalization theme,2 the US/Sino trade war that is here to stay irrespective of the next electoral outcome and excessive US government fiscal largesse will likely, in the next two-to-three years, swing the global deflation/inflation pendulum toward sustained inflation (Chart 12). For investors that are worried about the prospect of higher inflation, the purpose of this Special Report is to serve as an equity sector positioning roadmap, especially if inflationary pressures become more acute sooner than we anticipate. Chart 12Deglobalization Will Result In Inflation

Deglobalization Will Result In Inflation

Deglobalization Will Result In Inflation

Historically, inflation has been synonymous with an aggressive Fed and hard asset outperformance, suggesting that deep cyclical sectors would be the primary beneficiaries. Table 1 shows that over the last six major inflationary cycles, energy, materials, real estate and health care have been consistent outperformers. On the flip side, utilities, tech and telecom have been clear underperformers. The remaining sectors have been a mixed bag. Table 1S&P 500 Sector Performance During Inflationary Periods

Revisiting Equity Sector Winners And Losers When Inflation Climbs

Revisiting Equity Sector Winners And Losers When Inflation Climbs