Policy

Highlights The six-month increase in European bank credit flows amounts to an underwhelming $70 billion, compared to a record high $660 billion in the US and $550 billion in China. Underweight European domestic cyclicals versus their peers in the US and China. Specifically, underweight euro area banks versus US banks. Overweight equities on a long-term (2 years plus) horizon. The mid-single digit return that equities are offering makes them attractive versus ultra-low yielding bonds. But remain neutral equities on a 1-year horizon, until it becomes clear that we can prevent a second wave of the pandemic. Fractal trade: long bitcoin cash, short ethereum. Feature Chart I-1Bank Credit 6-Month Flow Up $70 Bn ##br##In The Euro Area…

Bank Credit 6-Month Flow Up $70 Bn In The Euro Area...

Bank Credit 6-Month Flow Up $70 Bn In The Euro Area...

Chart I-2…But Up $700 Bn ##br##In The US

...But Up $700 Bn In The US

...But Up $700 Bn In The US

Governments and central banks are dishing out an alphabet soup of stimulus. The question is: how much is reaching those that need it? Our preferred approach to assessing monetary stimulus is to focus on the evolution of bank credit flows and bond yields over a six-month period. Bank Credit Flows Have Surged In The US And China, Not In Europe On our preferred assessment, Europe’s monetary stimulus is underwhelming compared with that in the US and China. The six-month increase in US bank credit flows, at $660 billion, is the highest in a decade and not far from the highest ever. In China, the equivalent six-month increase is $550 billion. But in the euro area, the six-month increase in bank credit flows amounts to an underwhelming $70 billion (Charts I-1 - Chart I-4). Chart I-3Bank Credit 6-Month Flow Up $550 Bn In China…

Bank Credit 6-Month Flow Up $550 Bn In China...

Bank Credit 6-Month Flow Up $550 Bn In China...

Chart I-4...And Up ##br##Globally

...And Up Globally

...And Up Globally

Admittedly, US firms are drawing on pre-arranged bank credit lines rather than taking out new loans. Furthermore, the link between bank credit flows and final demand might be compromised during the current economic shutdown. For example, if firms are borrowing to pay workers who are not producing any output, then the transmission of a credit flow acceleration to a GDP acceleration would be weakened. Europe’s monetary stimulus is underwhelming compared with that in the US and China. Nevertheless, some bank credit flows will still reach the real economy. And the US and China are creating more bank credit flows than Europe. Focus On The Deceleration Of The Bond Yield Turning to the bond yield, it is important to focus not on its level, and not on its decline. Instead, it is important to focus on its deceleration. The focus on the deceleration of the bond yield sounds counterintuitive, but it results from a fundamental accounting identity. The next two paragraphs may seem somewhat technical but read them carefully, as they are important for understanding the transmission of stimulus. GDP is a flow. It measures the flow of goods and services produced in a quarter. Hence, GDP receives a contribution from the flow of credit. The flow of credit, in turn, is established by the level of bond yields. When we talk about stimulating the economy, we mean boosting the GDP growth rate from, say, -1 percent to +1 percent, which is an acceleration of GDP. This acceleration in the GDP flow must come from an acceleration in the flow of credit. This acceleration in the flow of credit, in turn, must come from a deceleration of bond yields. In other words, the bond yield decline in the most recent period must be greater than the decline in the previous period. Banks tend to perform better after bond yields have decelerated. The good news is that in the US and China, bond yields have decelerated; the bad news is that in Europe, they have not. Over the past six months, the 10-year bond yield has decelerated by 40 bps in the US and by 65 bps in China. Yet in France, despite the coronavirus crisis, the 10-year bond yield has accelerated by 60 bps (Charts I-5 - Chart I-8).1 Chart I-5The Bond Yield Has Accelerated ##br##In The Euro Area...

The Bond Yield Has Accelerated In The Euro Area... CHART B

The Bond Yield Has Accelerated In The Euro Area... CHART B

Chart I-6...Decelerated ##br##In The US...

...Decelerated In The US...

...Decelerated In The US...

Chart I-7...Decelerated In China...

...Decelerated In China...

...Decelerated In China...

Chart I-8...And Decelerated Globally

...And Decelerated Globally

...And Decelerated Globally

European bond yields are struggling to decelerate because of their proximity to the lower bound to bond yields, at around -1 percent. The inability to decelerate the bond yield constrains the monetary stimulus that Europe can apply compared to the US and China, whose bond yields are much further from the lower bound constraint. Compared to Europe, the US and China have much stronger decelerations in their bond yields and much stronger accelerations in their bank credit flows. This suggests underweighting European domestic cyclicals versus their peers in the US and China. Specifically, banks tend to perform better after bond yields have decelerated; and they tend to perform worse after bond yields have accelerated. On this basis, underweight euro area banks versus US banks (Chart I-9). Chart I-9Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Banks Perform Better After Bond Yields Have Decelerated, Worse After Bond Yields Have Accelerated

Long-Term Asset Allocation Is Straightforward, Shorter-Term Is Not The level of the bond yield, or of so-called ‘financial conditions’, does not drive the short-term oscillations in credit flows. To repeat, it is the acceleration and deceleration of the bond yield that matters. Yet when it comes to the long-term valuation of assets, the level of the bond yield does matter, and when the bond yield is ultra-low it matters enormously. An ultra-low bond yield justifies a much lower prospective return on competing long-duration assets, like equities. The reason is that when bond yields approach their lower bound, bond prices can no longer rise, they can only fall. This higher riskiness of bonds justifies an abnormally low (or zero) ‘risk premium’ on equities. In this world of ultra-low numbers – for both bond yields and equity risk premiums – the low to mid-single digit long-term return that equities are offering makes them attractive versus bonds (Chart I-10). Chart I-10Equities Are Offering Mid-Single Digit Long-Term Returns

Equities Are Offering Mid-Single Digit Long-Term Returns

Equities Are Offering Mid-Single Digit Long-Term Returns

But this long-term valuation argument only works for those with long-term investment horizons. What does long-term mean? There is no clear dividing line, but we would define long-term as two years at the very minimum. For a one-year investment horizon, the much more important question is: what will happen to 12-month forward earnings (profits)? In the stock market recessions of 2008-09 and 2015-16, the stock market reached its low just before forward earnings reached their low. Assuming the same holds true in 2020-21, we must establish whether forward earnings are close to their low or not. In 2008-09, world forward earnings collapsed by 45 percent. In the current recession, which is putatively worse, world forward earnings are down by less than 20 percent to date. To have already reached the cycle low in forward earnings with only half the decline of 2008, the current recession needs to be much shorter than the 2008-09 episode (Chart I-11 and Chart I-12). Chart I-11In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

In The Global Financial Crisis, Forward Earnings Collapsed By 45 Percent

Chart I-12In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

In The Current Crisis, Forward Earnings Are Down 20 Percent. Is That Enough?

Whether this turns out to be the case or not hinges on the pandemic and our response to it. A controlled easing of lockdowns will boost growth as more of the economy comes back to life. But too rapid an easing of lockdowns will unleash a second wave of the pandemic, requiring a second wave of economic shutdowns, a double dip recession and a new low in the stock market. Hence, if you have a long-term (2-year plus) investment horizon, the choice between equities and bonds is very straightforward: overweight equities. On this long-term horizon, German and Swedish equities are especially attractive versus negative-yielding bonds. On a 1-year investment horizon, the key question is: can we avoid a second wave of the pandemic? But if you have a 1-year investment horizon, the choice is less straightforward, because it hinges on whether we can avoid a second wave of the pandemic or not. Until it becomes clear that governments will not reopen economies too quickly, remain neutral equities on the 1-year horizon. Fractal Trading System* This week’s recommended trade is a pair-trade within the cryptocurrency asset-class. Long bitcoin cash / short ethereum. Set the profit target at 21 percent with a symmetrical stop-loss. The 12-month rolling win ratio now stands at 61 percent. Chart I-13Bitcoin Cash Vs. Ethereum

Bitcoin Cash Vs. Ethereum

Bitcoin Cash Vs. Ethereum

When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 In the US, the 10-year bond yield has declined by 120 bps in the past six months compared with 80 bps in the preceding six months, which equals a deceleration of 40 bps; in China, the 10-year bond yield has declined by 73 bps in the past six months compared with 18 bps in the preceding six months, which equals a deceleration of 65 bps; but in France, the 10-year bond yield has increased by 12 bps in the past six months compared with a 48 bps decline in the preceding six months, which equals an acceleration of 60 bps. Fractal Trading System Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

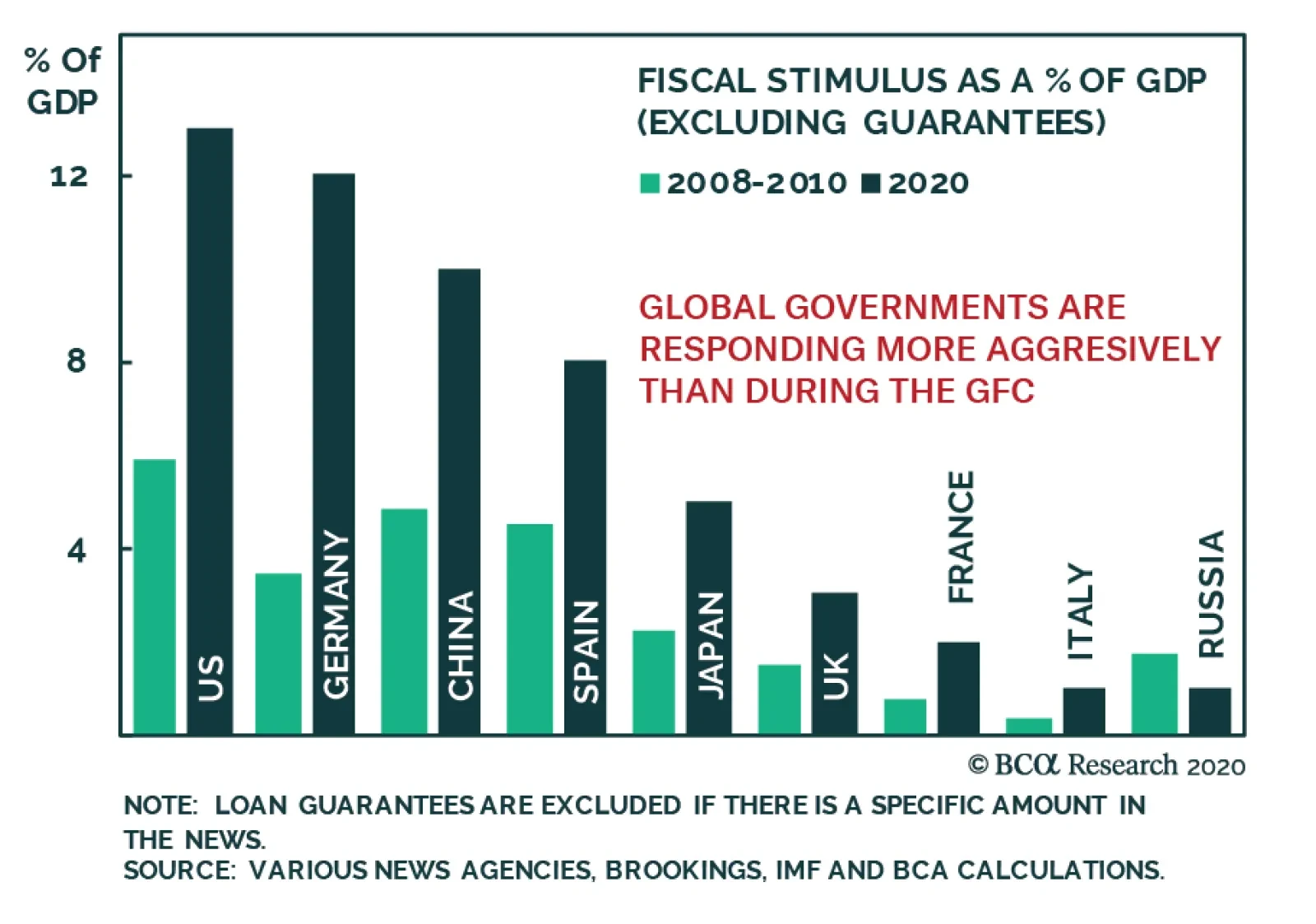

Dear Client, This week, in lieu of our regular report, we are sending you a Special Report from my colleague Jonathan LaBerge. Jonathan discusses the global fiscal response to the COVID-19 pandemic, and provides some perspective on whether the response will be enough to prevent an "L-shaped" economic outcome. I hope you find the report insightful. Last Friday, I participated in a webcast with my fellow BCA Strategists Caroline Miller and Arthur Budaghyan where we discussed the outlook for developed and emerging market equities over the immediate (0-3 month) and cyclical (12 month) horizon. You can access a replay of the webcast here. Please note we will be sending out our regular weekly report next week. Best regards, Peter Berezin, Chief Global Strategist Highlights In this Special Report we explore in detail the fiscal response amongst advanced economies, with the goal of judging whether the response is large enough to prevent an “L-shaped” recession. The crisis remains in its early days and new information about the size and character of the response, as well as the magnitude of the economic shock, continues to emerge on a near-daily basis. As such, our conclusions may change over the coming weeks in line with incoming data. Even when narrowly-defined, the announced (or likely) fiscal response of the US, China, and Germany is quite large and appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event. This is not the case, however, in other euro area economies (France, Italy, and Spain), or in emerging markets. Our analysis also suggests that the global fiscal response will need to increase if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year. This underscores the importance of ensuring that the “Great Lockdown” succeeds at reducing the spread of the disease to a point that does not necessitate widespread renewed restrictions on economic activity. Feature The global economic expansion that began in 2009 has come to an abrupt end due to the COVID-19 pandemic. Aggressive containment measures necessary to control the spread of the disease and prevent the collapse in health care systems around the world have caused a large and sudden stop in global economic activity, which has prompted unprecedented responses from governments around the world. In this Special Report we explore in detail the fiscal response amongst advanced economies, with the goal of judging whether the response is large enough to prevent an “L-shaped” recession (characterized by a very prolonged return to trend growth). The crisis remains in its early days and new information about the size and character of the response, as well as the magnitude of the economic shock, continues to emerge on a near-daily basis. As such, our conclusions may change over the coming weeks in line with incoming data. But for now, we (tentatively) conclude that the fiscal response appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event. However, there are two important caveats. First, while Germany has provided among the strongest fiscal responses globally, measures in France, Italy, and Spain are still lacking and must be stepped up. Second, the announced fiscal measures will not be sufficient if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year – more will have to be done. For policymakers, this underscores the importance of ensuring that the “Great Lockdown” succeeds at reducing the spread of the disease to a point that does not necessitate widespread renewed restrictions on economic activity. In this regard, the gradual re-opening of several US states by early-May, while positive for economic activity in the short-run, is a non-trivial risk to the US and global economic outlooks over the coming 6-12 months. This risk must be closely watched by investors. The Global Fiscal Response: Comparing Across Countries And Across Measures The flurry of policy announcements from national governments over the past six weeks has led to a great degree of confusion about the size and disposition of the global COVID-19 fiscal response. Our analysis is based heavily on the IMF’s tracking of these measures, albeit with a few adjustments. We also rely on analysis from Bruegel, a prominent European macroeconomic think-tank, as well as our own Geopolitical Strategy team and a variety of news reports. Chart 1 presents the IMF’s estimate of the total fiscal response to the crisis across major countries, as of April 23, broken down into “above-the-line” and “below-the-line” measures. Above-the-line measures are those that directly impact government budget balances (direct fiscal spending and revenue measures, usually tax deferrals), whereas below-the-line measures typically involve balance sheet measures to backstop businesses through capital injections and loan guarantees. Chart 1 makes it clear that the fiscal response of advanced economies is enormous when including both above- and below-the-line measures. By this metric, the response of most developed economies is on the order of 10% of GDP, and well above 30% in the case of Italy and Germany. However, using the sum of above- and below-the-line measures to gauge the fiscal response of any country may not be the ideal approach, given that below-the-line measures are contingent either on the triggering of certain conditions or on the provision of credit to households and firms from the financial system. Below-the-line measures also likely increase the liability position of the private sector, thus raising the odds of negative second-round effects. Chart 1The Global Fiscal Response Is Huge When Including All Measures

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Instead, Chart 2 compares the countries shown in Chart 1 based only on the IMF’s estimate of above-the-line measures, and with a 4% downward adjustment to Japan’s reported spending to account for previously announced measures.1 The chart shows that countries fall into roughly three categories in terms of the magnitude of their above-the-line response: in excess of 4% of GDP (Australia, the US, Japan, Canada, and Germany), 2-3% (the UK, Brazil, and China), and sub-2% (all other countries shown in the chart, including Spain, Italy, and France). Chart 2The Picture Changes When Excluding Below-The-Line Measures

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Analysis by Bruegel, provides somewhat different estimates of the global COVID-19 fiscal response for select European countries as well as the US (Table 1). Bruegel breaks down discretionary fiscal measures that have been announced into three categories: those involving an immediate fiscal impulse (new spending and foregone revenues), those related to deferred payments, and other liquidity provisions and guarantees. Bruegel distinguishes between the first and second categories because of their differing impact on government budget balances. Deferrals improve the liquidity positions of individuals and companies but do not cancel their obligations, meaning that they result only in a temporary deterioration in budget balances. Table 1 highlights that Bruegel’s estimates of the sum of above- and below-the-line measures are similar to the IMF’s estimates for the US, the UK, and Spain, but are smaller for Italy and larger for France and Germany (particularly the latter). These differences underscore the extreme uncertainty facing investors, who have to contend not only with varying estimates of the magnitude of government policies but also a torrent of news concerning the evolution of the pandemic itself. Table 1The Type Of Fiscal Response Varies Significantly Across Countries

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Chart 3 presents our best current estimate of the above-the-line fiscal response of several countries (the measure we deem to be most likely to result in an immediate fiscal impulse), by excluding loans, guarantees, and non-specified revenue deferrals to the best of our ability.2Chart 3 is based on a combination of data from the IMF, Bruegel analysis, and BCA estimates and news analysis. Chart 3When Narrowly Defined, Several Countries Are Responding Forcefully, But Many Countries Are Not

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Overall, investors can draw the following conclusions from Charts 1 – 3 and Table 1: When measured as the total of above- and below-the-line measures, nearly all large developed market countries have responded with sizeable measures. Emerging market economies are the clear laggards. Excluding below-the-line measures and using our approach, Australia, the US, China, Germany, Japan, and Canada appear to be spending the most relative to the size of their economies. While Japan’s “headline” fiscal number was inflated by including previously-announced spending, it is still decently-sized after adjustment. Outside of Germany, the rest of Europe appears to be providing a middling or poor above-the-line fiscal response. The UK appears to be providing between 4-5% of GDP as a fiscal impulse, whereas the fiscal response in Italy, Spain, and France looks more like that of emerging markets than of advanced economies. Measuring The Stimulus Against The Shock Despite the substantial amount of new information over the past six weeks concerning the evolution of the pandemic and the attendant policy response, it remains extremely difficult to judge what the balance between shock and stimulus will be and what that means for the profile of growth. Nonetheless, below we present a framework that investors can use to approach the question, and that can be updated as new information emerges concerning the impact of the shutdowns and the extent of the response. Our approach involves analyzing four specific questions: What is the size of the initial shock? What are the likely second-round effects on growth? What is the likely multiplier on fiscal spending? Will the composition of fiscal spending alter its effectiveness? The Size Of The Initial Shock Chart 4 presents the OECD’s estimates of the initial impact of partial or complete shutdowns on economic activity in several countries. The OECD first used a sectoral approach to estimating the impact on activity while lockdowns are in effect, assuming a 100% shutdown for manufacturing of transportation equipment and other personal services, a 50% decline in activity for construction and professional services, and a 75% decline for retail trade, wholesale trade, hotels, restaurants, and air travel. Chart 4 illustrates the total impact of this approach for key developed and emerging economies. Chart 4Annual GDP Will Be 1.5%-2.5% Lower For Each Month Lockdowns Are In Effect

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

The OECD’s approach provides a credible estimate of the impact of aggressive containment policies, and implies that annual real GDP is likely to be 1.5-2.5% lower for major countries for each month that lockdown policies are in effect. This implies that output in major economies is likely to fall 3.5% - 6% for the year from the initial shock alone, assuming an aggressive 10-week lockdown followed by a complete return to normal. Estimating Potential Second Round Effects Chart 5 presents projections from the Bank for International Settlements on the spillover and spillback potential of a 5% initial shock to the level of global GDP from the COVID-19 pandemic (equivalent to a 20% impact on an annualized basis). The chart shows that the cumulative impact of the initial shock rises to 7-8% by the end of this year for the US, euro area, and emerging markets, and 6% for other advanced economies. These estimates account for both domestic second round effects of the initial shock, as well as the reverberating impact of the shock on global trade. Chart 5 also shows the devastating effect that a second wave of COVID-19 emerging in the second half of the year would have after including spillover and spillback effects, assuming that only partial lockdowns would be required. In this scenario, the level of GDP would be 10-12% lower at the end of the year depending on the region, suggesting that investors should be more concerned about the possibility of additional lockdown events than they should be about the after-effects of the first wave of infections (more on this below). Chart 5Additional Lockdown Events Are A Greater Risk Than First Wave After-Effects

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Will Fiscal Multipliers Be High Or Low? When examining the academic literature on fiscal multipliers, the first impression is that multipliers are likely to be extremely large in the current environment. Tables 2 and 3 present a range of academic multiplier estimates aggregated by the IMF, categorized by the stage of the business cycle and whether the zero lower bound is in effect. The tables tell a clear story: multipliers are typically meaningfully larger during recessions than during expansions, and extremely large when the zero lower bound (ZLB) is in effect. However, there are at least two reasons to expect that the fiscal multiplier during this crisis will not be as large as Tables 2 and 3 suggest. First, it is obviously the case that the multiplier will be low while full or even partial lockdowns are in effect, as consumers will not have the ability to fully act in response to stimulative measures. This will be partially offset by a burst of spending once lockdowns are removed, but the empirical multiplier estimates during recessions shown in Table 2 have not been measured during a period when constraints to spending have been in effect, and we suspect that this will have at least somewhat of a dampening effect on the efficacy of fiscal spending relative to previous recessions (even once regulations concerning store closures are removed). Table 2Fiscal Multipliers Are Much Larger During Recessions Than Expansions

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Table 3Models Suggest The Multiplier Is Quite High At The Zero Lower Bound

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Second, Table 3 likely overestimates the multiplier at the ZLB. These estimates have been based on models rather than empirical analysis, and appear to be in reference to the prevention of large subsequent declines in output following an initial shock. The modeled finding of a large multiplier at the ZLB occurs because increased deficit spending will not lead to higher policy rates in a scenario where the neutral rate has fallen below zero. But it seems difficult to believe that the fiscal multiplier during ZLB episodes, defined as the impact of fiscal spending on the path of output relative to the initial shock (not relative to a counterfactual additional shock), is larger than the highest empirical estimates of the multiplier during recessions. The only circumstance in which we can envision this being the case is an environment where long-term bond yields are capped and remain at zero, alongside short-term interest rates, as the economy improves. The IMF has provided a simple rule of thumb approach to estimating the fiscal multiplier for a given country. The IMF’s approach involves first estimating the multiplier under normal circumstances based on a series of key structural characteristics that have been shown to influence the economy’s response to fiscal shocks. Then, the “normal” multiplier is adjusted higher or lower depending on the stage of the business cycle, and whether monetary policy is constrained by the ZLB. For the US, the IMF’s approach suggests that a multiplier range of 1.1 – 1.6 is reasonable, assuming the highest cyclical adjustment but no ZLB adjustment (see Box 1 for a description of the calculation). Given the unprecedented nature of this crisis, we are inclined to use the low end of this range (1.1) as a conservative assumption when judging whether fiscal responses to the crisis are sufficient. For investors, this means that governments should be aiming, at a minimum, for fiscal packages that are roughly 90% of the size of the expected shock of their economies, using our US fiscal multiplier assumption as a guide. Box 1The 'Bucket' Approach To Estimating Fiscal Multipliers

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

The Composition Of The Response: Helping Or Hurting? The last of our four questions deals with the issue of composition and whether the form of a country’s fiscal response is likely to alter its effectiveness. We implicitly addressed the first element of composition, whether measures are above-the-line or below-the-line, by comparing Charts 1 - 3 on pages 3-5. Our view is that above-the-line measures are far more important than below-the-line measures, as the former provides direct income and liquidity support. Below-the-line measures are also important, as they are likely to help reduce business failure and household bankruptcies. The fiscal multiplier on these measures has to be above zero, but it is likely to be much lower than that of an above-the-line response. Chart 6Much Of The US Fiscal Response Is Going To Households And Small Businesses

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

The second element of composition concerns the appropriate distribution of aid among households, businesses, and local governments. On this particular question, it remains extremely challenging to analyze the issue on a global basis, owing to a frequent lack of an explicit breakdown of fiscal measures by recipient. For now, we limit our distributional analysis to the US, and hope to expand our approach to other countries in future research. Chart 6 presents a breakdown of the US fiscal response by recipient, which informs the following observations. Households: Chart 6 highlights that US households will receive approximately $600 billion as part of the CARES Act, roughly half of which will occur through direct payments (i.e. “stimulus checks”) and another 40% from expanded unemployment benefits. In cases where the federal household response has been criticized by members of the public as inadequate, it has often been compared to income support programs of other countries. The Canada Emergency Response Benefit (“CERB”) is a good example of a program that seems, at first blush, to be superior: it provides $2,000 CAD in direct payments to individuals for a 4 week period, for up to 16 weeks (i.e. a maximum of $8,000 CAD), which seems better than a $1,200 USD stimulus check. However, Table 4 highlights that this comparison is mostly spurious. First, the CERB is not universal, in that it is only available to those who have stopped or will stop working due to COVID-19. At a projected cost of $35 billion CAD, the CERB program represents 1.5% of Canadian GDP. By comparison, $600 billion USD in overall household support represents 2.75% of US GDP; this number drops to 1.75% when only considering support to those who have lost their jobs, but this is still higher as a share of the economy than in Canada. Moreover, there is little question that Congress is prepared to pass more stimulus for additional weeks of required assistance. Table 4US Household Relief Is Just As Generous As Seemingly Better Programs

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

The discrepancy between the perception and reality of US household sector support appears to be rooted in the speed of payments. Speed is the one area where Canada’s household sector response appears to have legitimately outperformed the US; CERB payments are received by applicants within three business days for those registered for electronic payment, and in some cases they are received the following day. By contrast, it has taken some time for US States to start paying out the additional $600 USD per week in expanded unemployment benefits, but as of the middle of last week nearly all states had started making these payments. Firms: On April 16 the Small Business Administration announced that the Paycheck Protection Program (“PPP”) had expended its initial budget of $350 billion. While additional funds of $320 billion have subsequently been approved (plus $60 billion in small business emergency loans and grants), the run on PPP funds was, to some investors, an implicit sign that the CARES Act was inadequately structured. Table 5Help For Small Businesses Will Replace A Significant Amount Of Lost Income

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

However, the fact that the initial funds ran out in mid-April simply reflects the reality that social distancing measures had been in place for 3-4 weeks by the time that the program began taking applications. Table 5 highlights that $350 billion was large enough to replace nearly 90% of lost small business income for one month, assuming that overall small business revenue has fallen by 50% and that small businesses account for 44% of total GDP. The table also shows that a combined total of $730 billion is enough to replace almost 80% of lost small business income for 10 weeks, given these assumptions. With loan forgiveness at least partially tied to small businesses retaining employees on payroll for an 8-week period, the PPP is also essentially an indirect form of household income support. State & Local Governments: The magnitude of support for state & local (S&L) governments appears to be the least-well designed element of the US fiscal response. The CARES Act provides for $170 billion in support to S&L, which at first blush seems large as it is approximately 25% of S&L current receipts in Q4 2019 (i.e. it stands to cover a 25% loss in revenue for one quarter). However, this does not account for the significant reported increase in S&L costs to combat the pandemic, nor does it provide S&L governments with any revenue certainty beyond June 30 when most of the assistance from CARES must be spent. Chart 7Persistent State & Local Austerity Must Be Avoided This Time

Persistent State & Local Austerity Must Be Avoided This Time

Persistent State & Local Austerity Must Be Avoided This Time

Unlike households or firms, who also face significant uncertainty, nearly all US states are subject to balanced budget requirements, which prevent them from spending more than they collect in revenue. When faced even with projected revenue losses in the second half of this year and into 2021, states are likely to aggressively and immediately cut costs in order to avoid budgetary shortfalls. Chart 7 highlights that S&L austerity was a significant element of the persistent drag on real GDP growth from overall government expenditure and investment in the first 3-4 years of the post-GFC economic expansion. A repeat of this episode would significantly raise the odds of an “L-type” recession (and thus should certainly be avoided). This is why Congress is moving to pass larger state and local aid. Our Geopolitical Strategy team argues that neither President Trump nor Senate Majority Leader Mitch McConnell will prevent the additional financial assistance that US states will require, despite their rhetoric about states going bankrupt.3 A near-term, temporary standoff may occur, but Washington will almost certainly act to provide at least additional short-term funding if state employment starts to fall due to budget pressure. So while we recognize that the state & local component of the US fiscal response is currently lacking, it does not seem likely to represent a serious threat to an eventual economic recovery in the US. Putting It All Together: Will It Be Enough? Chart 8 reproduces Chart 3 with an assumed fiscal multiplier of 1.1, and with shaded regions denoting the likely initial and total impact on GDP from aggressive containment measures (based on the OECD and BIS’ estimates). Based on our analysis of the US fiscal response, we make no adjustments for the composition of the measures beyond defining the fiscal response on a narrow basis (i.e. excluding loans, guarantees, and non-specified revenue deferrals). The chart highlights that the narrowly-defined fiscal response of three key economies driving global demand, the US, China, and Germany, is either at the upper end or above the total impact range. Thus, for now, we tentatively conclude that the fiscal response that has or will happen appears to be adequate to prevent the direct and indirect effects of the lockdowns from causing an “L-shaped” event, especially since Chart 8 explicitly excludes below-the-line measures. Chart 8Several Important Countries Seem To Be Doing Enough, But More Is Needed In Europe Ex-Germany

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

However, there are two important caveats to this conclusion. First, Chart 8 makes it clear that measures in France, Italy, and Spain are still lacking and must be stepped up. Italy and France have provided a substantial below-the-line response, but it is far from clear that a debt-based response or one that only temporarily improves access to cash for households and businesses will be enough to prevent a prolonged fallout from the sudden stop in economic activity and income. Second, our analysis suggests that the announced fiscal measures will not be sufficient if the global economy faces a W-shaped shock caused by another round of aggressive containment measures later this year or if these measures remain in place at half-strength for many months. This underscores how sensitive the adequacy of announced fiscal measures are to the amount of time economies remain under full or partial lockdown. As such, it is crucial for investors to have some sense of when advanced economies may be able to sustainably end aggressive containment measures. When Can The Lockdowns Sustainably End? Several countries and US states have already announced some reductions in their restrictions, but the question of how comprehensive these measures can be without risking a second period of prolonged stay-at-home orders looms large. Table 6 presents two different methods of estimating sustainable lockdown end dates for several advanced economies. First, we use the “70-day rule” that appears to have succeeded in ending the outbreak in Wuhan, calculated from the first day that either school or work closures took effect in each country.4 Second, using a linear trend from the peak 5-day moving average of confirmed cases and fatalities, we calculate when confirmed cases and fatalities may reach zero. Table 6By Re-Opening Soon, The US May Be Risking A Damaging Second Wave

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

The table highlights that these methods generally prescribe a reopening date of May 31 or earlier, with a few exceptions. The UK’s confirmed case count and fatality trends are still too shallow to suggest an end of May re-opening, as is the case in Canada. In the case of Sweden, no projections can truly be made based on the 70-day rule because closures never formally occurred. But the most problematic point highlighted in Table 6 is that US newly confirmed cases are only currently projected to fall to zero as of February 2021. Chart 9 highlights that while new cases per capita in New York state are much higher than in the rest of the country, they are declining whereas they have yet to clearly peak elsewhere. Cross-country case comparisons can be problematic due to differences in testing, but with several US states having already begun the gradual re-opening process, this underscores that US policymakers may be allowing a dangerous rise in the odds of a secondary infection wave. Chart 9No Clear Downtrend Yet Outside Of New York State

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Investment Conclusions Our core conclusion that an “L-shaped” global recession is likely to be avoided is generally bullish for equities on a 12-month horizon. However, uncertainty remains extremely elevated, and the recent rise in stock prices in the US (and globally) has been at least partially based on the expectation that lockdowns will sustainably end soon, which at least in the case of the US appears to be a premature conclusion given the current lack of large-scale virus testing capacity. As such, we are less optimistic towards risky assets tactically, and would recommend a neutral stance over a 0-3 month horizon. As noted above, our cross-country comparison of narrowly-defined fiscal measures suggested that euro area countries (excluding Germany) will likely have to do more in order to prevent a long period of below-trend growth. In the case of highly-indebted countries like Italy, this raises the additional question of whether a significantly increased debt-to-GDP ratio stemming from an aggressive fiscal impulse will cause another euro area sovereign debt crisis similar to what occurred from 2010-2014. Chart 10Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Italy's Debt Sustainability Hurdle Is Lower Than It Used To Be

Government debts are sustainable as long as interest rates remain below economic growth, and from this vantage point Italy should spend as much as needed in order to ensure that nominal growth remains above current long-term government bond yields. Chart 10 highlights that, despite a widening spread versus German bunds, Italian 10-year yields are much lower today than they were during the worst of the euro area crisis, meaning that the debt sustainability hurdle is technically lower. However, we have also noted in previous reports that high-debt countries often face multiple government debt equilibria; if global investors become fearful that that high-debt countries may not be able to repay their obligations without defaulting or devaluing, then a self-fulfilling prophecy will occur via sharply higher interest rates (Chart 11). Chart 11Multiple Equilibria In Debt Markets Are Possible Without A Lender Of Last Resort

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

For now, we view the risk of a renewed Italian debt crisis from significantly increased spending related to COVID-19 as minimal, and it is certainly lower than the status quo as the latter risks causing a sharp gap between nominal growth and bond yields like what occurred from 2010 – 2014. First, Chart 12 highlights that Italy has succeeded in somewhat reducing its structural balance, which averaged -4% for many years prior to the euro area crisis. Assuming an adequate global response to the crisis and that economic recovery ensues, it is not clear why global bond investors would be concerned that Italian structural deficits would persistently widen. Second, the ECB is purchasing Italian government bonds as part of its new Pandemic Emergency Purchase Program, which will help cap the level of Italian yields. Third, Chart 13 shows what will occur to Italy’s government debt service ratio (general government net interest payments as a percent of GDP) in a scenario where Italy’s gross debt to GDP rises a full 20 percentage points and the ratio of net interest payments to debt remains unchanged. The chart shows that while debt service will rise, it will still be lower than at any point prior to 2015. Chart 12Italy's Structural Budget Balance Has Improved

Italy's Structural Budget Balance Has Improved

Italy's Structural Budget Balance Has Improved

Chart 13Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

Italy's Debt Service Ratio Won't Go Up Much, If Yields Are Unchanged

So not only should Italy spend significantly more to combat the severely damaging nature of the pandemic, we would expect that Italian spreads would fall, not rise, in such an outcome. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 “Skeptical economists call Japan’s largest-ever stimulus package ‘puffed-up’, Keita Nakamura, The Japan Times, April 8, 2020. 2 Please note that Chart 3 differs somewhat from a chart that has been frequently shown by our Geopolitical Strategy service. Both charts are accurate; they simply employ different definitions of the fiscal response to the pandemic. 3 Indeed, McConnell has already walked back his comments that states should consider bankruptcy. President Trump is constrained by the election, as are Senate Republicans, and the House Democrats control the purse strings. Hence more state and local funding is forthcoming. At best for the Republicans, there may be provisions to ensure it goes to the COVID-19 crisis rather than states’ unfunded pension obligations. See Geopolitical Strategy, “Drowning In Oil (GeoRisk Update),” April 24, 2020, available at gps.bcaresearch.com. 4 School and work closure dates have been sources from the Oxford COVID-19 Government Response Tracker. Global Investment Strategy View Matrix

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

Current MacroQuant Model Scores

The Global COVID-19 Fiscal Response: Is It Enough?

The Global COVID-19 Fiscal Response: Is It Enough?

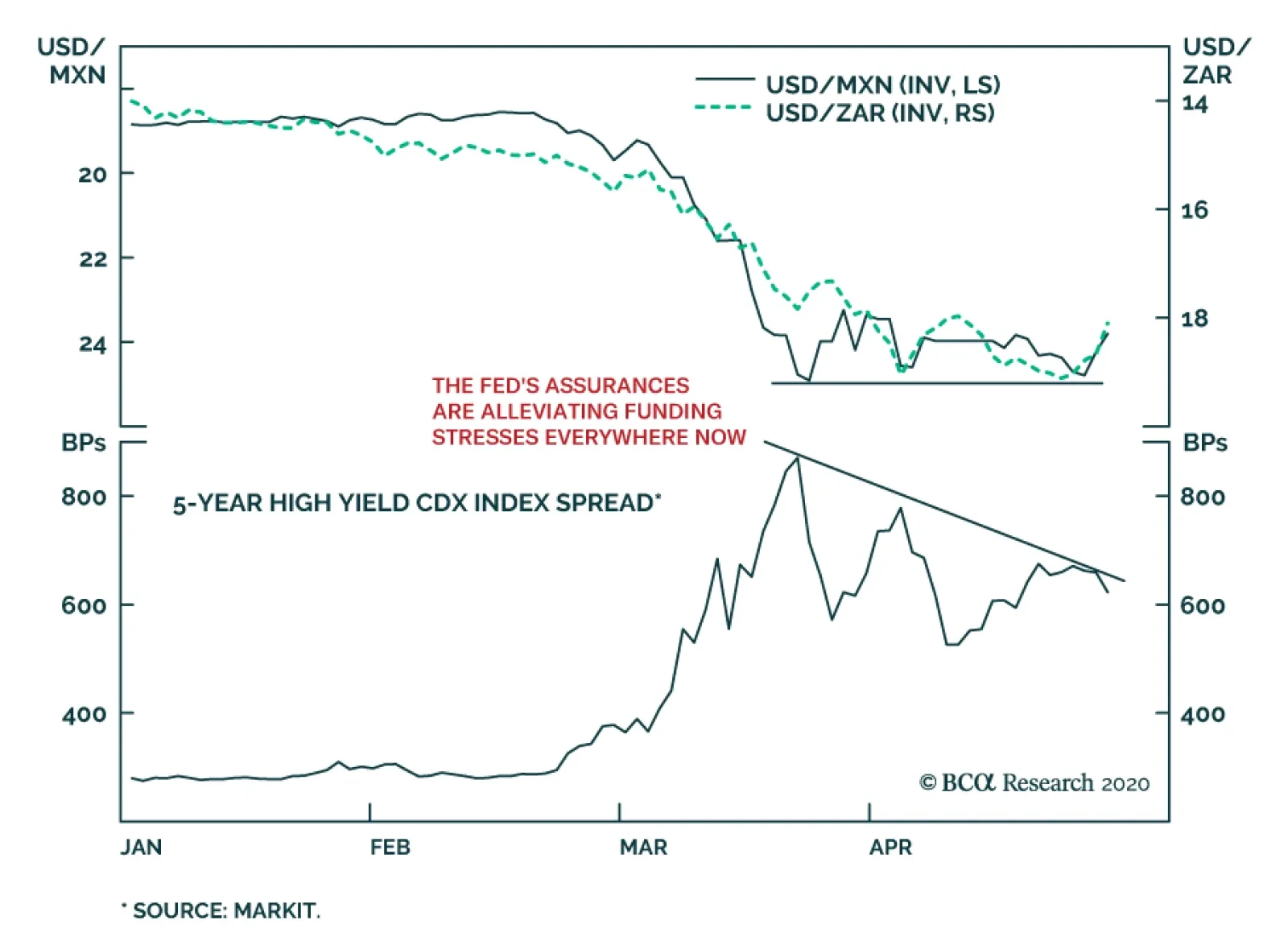

The Fed did not adjust policy yesterday. This is not much of a surprise, the FOMC announced a flurry of programs since March 15th which have allowed funding stress to fall, risk assets to stabilize, and stocks to rally sharply. Nonetheless, Chairman…

Highlights The collapse in oil prices supercharges the geopolitical risks stemming from the global pandemic and recession. Low oil prices should discourage petro-states from waging war, but Iran may be an important exception. Russian instability is one of the most important secular geopolitical consequences of this year’s crisis. President Trump’s precarious status this election year raises the possibility of provocations or reactions on his part. Europe faces instability on its eastern and southern borders in coming years, but integration rather than breakup is the response. Over a strategic time frame, go long AAA-rated municipal bonds, cyber security stocks, infrastructure stocks, and China reflation plays. Feature Chart 1Someone Took Physical Delivery!

Someone Took Physical Delivery!

Someone Took Physical Delivery!

Oil markets melted this week. Oil volatility measured by the Crude Oil ETF Volatility Index surpassed 300% as WTI futures for May 2020 delivery fell into a black hole, bottoming at -$40.40 per barrel (Chart 1). Our own long Brent trade, initiated on 27 March 2020 at $24.92 per barrel, is down 17.9% as we go to press. Strategically we are putting cash to work acquiring risk assets and we remain long Brent. The forward curve implies that prices will rise to $35 and $31 per barrel for Brent and WTI by April 2021. We initiated this trade because we assessed that: The US and EU would gradually reopen their economies (they are doing so). Oil production would be destroyed (more on this below). Russia and Saudi Arabia would agree to production cuts (they did). Monetary and fiscal stimulus would take effect (the tsunami of stimulus is still growing). Global demand would start the long process of recovery (no turn yet, unknown timing). On a shorter time horizon, we are defensively positioned but things are starting to look up on COVID-19 – New York Governor Andrew Cuomo has released results of a study showing that 15% of New Yorkers have antibodies, implying a death rate of only 0.5%. The US dollar and global policy uncertainty may be peaking as we go to press (Chart 2). However, second-order effects still pose risks that keep us wary. Chart 2Dollar And Policy Uncertainty Roaring

Dollar And Policy Uncertainty Roaring

Dollar And Policy Uncertainty Roaring

Geopolitics is the “next shoe to drop” – and it is already dropping. A host of risks are flying under the radar as the world focuses on the virus. Taken alone, not every risk warrants a risk-off positioning. But combined, these risks reveal extreme global uncertainty which does warrant a risk-off position in the near term. This week’s threats between the US and Iran, in particular, show that the political and geopolitical fallout from COVID-19 begins now, it will not “wait” until the pandemic crisis subsides. In this report we focus on the risks from oil-producing economies, but we first we update our fiscal stimulus tally. Stimulus Tsunami Chart 3Stimulus Tsunami Still Building

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Policymakers responded to COVID-19 by doing “whatever it takes” to prop up demand (Chart 3). Please see the Appendix for our latest update of our global fiscal stimulus table. The latest fiscal and monetary measures show that countries are still adding stimulus – i.e. there is not yet a substantial shift away from providing stimulus: China has increased its measures to a total of 10% of GDP for the year so far, according to BCA Research China Investment Strategy. This includes a general increase in credit growth, a big increase in government spending (2% of GDP), a bank re-lending scheme (1.5% of GDP), an increase in general purpose local government bonds (2% of GDP), plus special purpose bonds (4% of GDP) and other measures. On the political front, the government has rolled out a new slogan, “the Six Stabilities and the Six Guarantees,” and President Xi Jinping said on an inspection tour to Shaanxi that the state will increase investments to ensure that employment is stabilized. This is the maximum reflationary signal from China that we have long expected. The US agreed to a $484 billion “fourth phase” stimulus package, bringing its total to 13% of GDP. President Trump is already pushing for a fifth phase involving bailouts of state and local governments and infrastructure, which we fully expect to take place even if it takes a bit longer than packages that have been passed so far this year. German Chancellor Angela Merkel has opened the way for the EU to issue Eurobonds, in keeping with our expectations. Germany is spending 12% of GDP in total – which can go much higher depending on how many corporate loans are tapped – while Italy is increasing its stimulus to 3% of GDP. As deficits rise to astronomical sums, and economies gradually reopen, will legislatures balk at passing new stimulus? Yes, eventually. Financial markets will have to put more pressure on policymakers to get them to pass more stimulus. This can lead to volatility. In the US the pandemic is coinciding with “peak polarization” over the 2020 election. Lack of coordination between federal and state governments is increasing uncertainty. Currently disputes center on the timing of economic reopening and the provisioning bailout funds for state and local governments. Senate Majority Leader Mitch McConnell is threatening to deny bailouts for American states with large, unfunded public pension benefits (Chart 4A). He is insisting that the Senate “push the pause button” on coronavirus relief measures; specifically that nothing new be passed until the Senate convenes in Washington on May 4. He may then lead a charge in the Republican Senate to try to require structural reforms from states in exchange for bailouts. Estimates of the total state budget shortfall due to the crisis stand at $500 billion over the next three years, which is almost certainly an understatement (Chart 4B). Chart 4AUS States Have Unfunded Liabilities

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Chart 4BUS States Face Funding Shortfalls

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Could a local government or state declare bankruptcy? Not anytime soon. Technically there is no provision for states to declare bankruptcy. A constitutional challenge to such a declaration would go to the Supreme Court. One commonly cited precedent, Arkansas in 1933, ended up with a federal bailout.1 A unilateral declaration could conceivably become a kind of “Lehman moment” in the public sector, but state governors will ask their legislatures to provide more fiscal flexibility and will seek bailouts from the federal government first. The Federal Reserve is already committed to buying state and local bonds and can expand these purchases to keep interest rates low. Washington would be forced to provide at least short-term funding if state workers started getting fired in the midst of the crisis because of straightened state finances – another $500 billion for the states is entirely feasible in today’s climate. Constraints will prevail on the GOP Senate to provide state bailout funds. This conflict over state finances could have a negative impact on US equities in the near term, but it is largely a bluff – McConnell will lose this battle. The fundamental dynamic in Washington is that of populism combined with a pandemic that neutralizes arguments about moral hazard. Big-spending Democrats in the House of Representatives control the purse strings while big-spending President Trump faces an election. Senate Republicans are cornered on all sides – and their fate is tied to the President’s – so they will eventually capitulate. Bottom Line: The global fiscal and monetary policy tsunami is still building. But there are plenty of chances for near-term debacles. Over the long run the gargantuan stimulus is the signal while the rest is noise. Over the long run we expect the reflationary efforts to prevail and therefore we are long Treasury inflation-protected securities and US investment grade corporate bonds. We recommend going strategically long AAA-rated US municipal bonds relative to 10-year Treasuries. Petro-State Meltdown Since March we have highlighted that the collapse in oil prices will destabilize oil producers above and beyond the pandemic and recession. This leaves Iran in danger, but even threatens the stability of great powers like Russia. Normally there is something of a correlation between the global oil price and the willingness of petro-states to engage in war (Chart 5). Chart 5Petro-States Cease Fire When Oil Drops

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

When prices fall, revenues dry up and governments have to prioritize domestic stability. This tends to defer inter-state conflict. We can loosely corroborate this evidence by showing that global defense stocks tend to be correlated with oil prices (Chart 6). Global growth is the obvious driver of both of these indicators. But states whose budgets are closely tied to the commodity cycle are the most likely to cut defense spending. Chart 6Global Growth Drives Oil And Guns

Global Growth Drives Oil And Guns

Global Growth Drives Oil And Guns

Russia is case in point. Revenues from Rostec, one of Russia’s largest arms firms, rise and fall with the Urals crude oil price (Chart 7). The Russians launch into foreign adventures during oil bull markets, when state coffers are flush with cash. They have an uncanny way of calling the top of the cycle by invading countries (Chart 8). Chart 7Oil Correlates With Russian Arms Sales

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Chart 8Russian Invasions Call Peak In Oil Bull Markets

Russian Invasions Call Peak In Oil Bull Markets

Russian Invasions Call Peak In Oil Bull Markets

Chart 9Turkish Political Risk On The Rise

Turkish Political Risk On The Rise

Turkish Political Risk On The Rise

In the current oil rout, there is already some evidence of hostilities dying down in this way. For instance, after years of dogged fighting in Yemen, Saudi Arabia is finally declaring a ceasefire there. Turkey, which benefits from low oil prices, has temporarily gotten the upper hand in Libya vis-à-vis Khalifa Haftar and the Libyan National Army, which depends on oil revenues and backing from petro-states like Russia and the GCC. Of course, Turkey’s deepening involvement in foreign conflicts is evidence of populism at home so it does not bode well for the lira or Turkish assets (Chart 9). But it does highlight the impact of weak oil on petro-players such as Haftar. However, the tendency of petro-states to cease fire amid low prices is merely a rule of thumb, not a law of physics. Past performance is no guarantee of future results. Already we are seeing that Iran is defying this dynamic by engaging in provocative saber-rattling with the United States. Iran And Iraq The US and Iran are rattling sabers again. One would think that Iran, deep in the throes of recession and COVID-19, would eschew a conflict with the US at a time when a vulnerable and anti-Iranian US president is only seven months away from an election. Chart 10US Maximum Pressure On Iran

US Maximum Pressure On Iran

US Maximum Pressure On Iran

Iran has survived nearly two years of “maximum pressure” from President Trump (Chart 10), and previous US sanction regimes, and has a fair chance of seeing the Democrats retake Washington. The Democrats would restart negotiations to restore the 2015 nuclear deal, which was favorable to Iran. Therefore risking air strikes from President Trump is counterproductive and potentially disastrous. Yet this logic only holds if the Iranian regime is capable of sustaining the pain of a pandemic and global recession on top of its already collapsing economy. Iran’s ability to circumvent sanctions to acquire funds depended on the economy outside of Iran doing fine. Now Iran’s illicit funds are drying up. This could lead to a pullback in funding for militant proxies across the region as Iran cuts costs. But it also removes the constraint on Iran taking bolder actions. If the economy is collapsing anyway then Iran can take bigger risks. Furthermore if Iran is teetering, there may be an incentive to initiate foreign conflicts to refocus domestic angst. This could be done without crossing Trump’s red lines by attacking Iraq or Saudi Arabia. With weak oil demand, Iran’s leverage declines. But a major attack would reduce oil production and accelerate the global supply-demand rebalance. Iran’s attack on the Saudi Abqaiq refinery last September took six million barrels per day offline briefly, but it was clearly not intended to shut down that production permanently. Threats against shipping in the Persian Gulf bring about 14 million barrels per day into jeopardy (Chart 11). Chart 11Closing Hormuz Would Be The Biggest Oil Shock Ever

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Iran-backed militias in Iraq have continued to attack American assets and have provoked American air strikes over the past month, despite the near-war scenario that erupted just before COVID. Iranian ships have harassed US naval ships in recent days. President Trump has ordered the navy to destroy ships that threaten it; Iranian commander has warned that Iran will sink US warships that threaten its ships in the Gulf. There is a 20% chance of armed hostilities between the US and Iran. Why would Iran be willing to confront the United States? First, Iran rightly believes that the US is war-weary and that Trump is committed to withdrawing from the Middle East. But this could prompt a fateful mistake. The equation changes if the US public is incensed and Trump’s election campaign could benefit from conflict. Chart 12Youth Pose Stability Risk To Iran

Youth Pose Stability Risk To Iran

Youth Pose Stability Risk To Iran

Second, the US is never going to engage in a ground invasion of Iran. Airstrikes would not easily dislodge the regime. They could have the opposite effect and convert an entire generation of young, modernizing Iranians into battle-hardened supporters of the Islamic revolution (Chart 12). This is a dire calculation that the Iranian leaders would only make if they believed their regime was about to collapse. But they are quite possibly the closest to collapse that they have been since the 1980s and nobody knows where their pain threshold lies. They are especially vulnerable as the regime approaches the uncharted succession of Supreme Leader Ali Khamanei. Since early 2018 we have argued that there is a 20% chance of armed hostilities between the US and Iran. We upgraded this to 40% in June 2019 and downgraded it back to 20% after the Iranians shied from direct conflict this January. Our position remains the same 20%. This is still a major understated risk at a time when the global focus is entirely elsewhere. It will persist into 2021 if Trump is reelected. If the Democrats win the US election, this war risk will abate. The Iranians will play hard to get but they are politically prohibited from pursuing confrontation with the US when a 2015-type deal is available. This would open up the possibility for greater oil supply to be unlocked in the future, but sanctions are not likely to be lifted till 2022 at earliest. Russia Russia may not be on the verge of invading anyone, but it is internally vulnerable and fully capable of striking out against foreign opponents. Cyberattacks, election interference, or disinformation campaigns would sow confusion or heighten tensions among the great powers. The Russian state is suffering a triple whammy of pandemic, recession, and oil collapse. President Vladimir Putin’s approval rating has fallen this year so far, whereas other leaders in the western world have all seen polling bounces (even President Trump, slightly) (Chart 13). Putin postponed a referendum designed to keep him in office through 2036 due to the COVID crisis. In other words, the pandemic has already disrupted his carefully laid succession plans. While Putin can bypass a referendum, he would have been better off in the long run with the public mandate. Generally it is Putin’s administration, not his personal popularity, that is at risk, but the looming impact on Russian health and livelihoods puts both in jeopardy (Chart 14) and requires larger fiscal outlays to try to stabilize approval (Chart 15). Chart 13Putin Saw No COVID Popularity Bump

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Chart 14Russian Regime Faces Political Discontent

Russian Regime Faces Political Discontent

Russian Regime Faces Political Discontent

Moreover, regardless of popular opinion, Putin is likely to settle scores with the oligarchs. The fateful decision to clash with the Saudis in March, which led to the oil collapse, will fall on Igor Sechin, Chief Executive of Rosneft, and his faction. An extensive political purge may well ensue that would jeopardize domestic stability (Chart 16). Chart 15Russia To Focus On Domestic Stability

Russia To Focus On Domestic Stability

Russia To Focus On Domestic Stability

Chart 16Russian Political Risk Will Rise

Russian Political Risk Will Rise

Russian Political Risk Will Rise

Russian tensions with the US will rise over the US election in November. The Democrats would seek to make Russia pay for interfering in US politics to help President Trump win in 2016. But even President Trump may no longer be a reliable “ally” of Putin given that Putin’s oil tactics have bankrupted the US shale industry during Trump’s reelection campaign. The American and Russian air forces are currently sparring in the air space over Syria and the Mediterranean. The US has also warned against a malign actor threatening to hack the health care system of the Czech Republic, which could be Russia or another actor like North Korea or Iran. These issues have taken place off the radar due to the coronavirus but they are no less real for that. Venezuela We have predicted Venezuela’s regime change for several years but the oil meltdown, pandemic, and insufficient Russian and Chinese support should put the final nail in the regime’s coffin. Hugo Chavez’s rise to power, the last “regime change,” occurred as oil prices bottomed in 1998. Historically the Venezuelan armed forces have frequently overthrown civilian authorities, but in several cases not until oil prices recovered (Chart 17). Chart 17Venezuelan Coups Follow Oil Rebounds

Venezuelan Coups Follow Oil Rebounds

Venezuelan Coups Follow Oil Rebounds

The US decision to designate Nicolas Maduro as a “narco-terrorist,” to deploy greater naval and coast guard assets around Venezuela, to reassert the Monroe Doctrine and Roosevelt Corollary, and to pull Chevron from the country all suggest that Washington is preparing for regime change. Such a change may or may not involve any American orchestration. Venezuela is an easy punching-bag for President Trump if he seeks to “wag the dog” ahead of the election. Venezuela would be a strategic prize and yet it cannot hurt the US economy or financial markets substantially, giving limited downside to President Trump if he pursues such a strategy. Obviously any conflict with Venezuela this year is far less relevant to global investors than one with Iran, North Korea, China, or Russia. Regime change would be positive for oil supply and negative for prices over the long run. But that is a story for the next cycle of energy development, as it would take years for government and oil industry change in Venezuela to increase production. The US election cycle is a critical aggravating factor for all of these petro-state risks. Shale producers are going bankrupt, putting pressure on the economy and some swing states. The risk of a conflict arises not only from Trump playing “wag the dog” after the crisis abates, but also from other states provoking the president, causing him to react or overreact. The “Other Guys” Oil producers outside the US, Canada, gulf OPEC, and Russia – the “other guys” – are extremely vulnerable to this year’s global crisis and price collapse. Comprising half of global production, they were already seeing production declines and a falling global market share over the past decade when they should have benefited from a global economic expansion. They never recovered from the 2014-15 oil plunge and market share war (Chart 18). Angola (1.4 million barrels per day), Algeria (one million barrels per day), and Nigeria (1.8 million barrels per day) are relatively sizable producers whose domestic stability is in question in the coming years as they cut budgets and deplete limited forex reserves to adjust to the lower oil price. This means fewer fiscal resources to keep political and regional factions cooperating and provide basic services. Algeria is particularly vulnerable. President Abdelaziz Bouteflika, who ruled as a strongman from 1999, was forced out last year, leaving a power vacuum that persists under Prime Minister Abdelaziz Djerad, in the wake of the low-participation elections in December. An active popular protest movement, Hirak, already exists and is under police suppression. Unemployment is high, especially among the youth. Neighboring Libya is in the midst of a war and extremist militants within Libya and North Africa would like to expand their range of operations in a destabilized Algeria. Instability would send immigrants north to Europe. Oil production will be reduced involuntarily as well as voluntarily this year due to regime failures. Brazil is not facing the risk of state failure like Algeria, but it is facing a deteriorating domestic political outlook (Chart 19). President Jair Bolsonaro’s popularity was already low relative to most previous presidents before COVID. His narrow base in the Chamber of Deputies got narrower when he abandoned his political party. He has defied the pandemic, refused to endorse social distancing or lockdown orders by local governments, and fired his Health Minister Luiz Henrique Mandetta. Chart 18Petro-States: 'Other Guys' Face Instability

Petro-States: 'Other Guys' Face Instability

Petro-States: 'Other Guys' Face Instability

Chart 19Brazilian Political Risk Rising Again

Brazilian Political Risk Rising Again

Brazilian Political Risk Rising Again

Brazil has a high number of coronavirus deaths per million people relative to other emerging markets with similar health capacity and susceptibility to the disease. This, combined with sharply rising unemployment, could prove toxic for Bolsonaro, who has not received a bounce in popular opinion from the crisis like most other world leaders. Thus on balance we expect the October local elections to mark a comeback for the Worker’s Party. The limited fiscal gains of Bolsonaro’s pension reform are already wiped out by the global recession, which will set back the country’s frail recovery from its biggest recession in a century. The country is still on an unsustainable fiscal path. Bolsonaro does not have a strong personal commitment to neoliberal structural reform, which has been put aside anyway due to the need for government fiscal spending amid the crisis. Unless Bolsonaro’s popularity increases in the wake of the crisis – due to backlash against the state-level lockdowns – the economic shock is negative for Brazil’s political stability and economic policy orthodoxy. Bottom Line: Our rule of thumb about petro-states suggests that they will generally act less aggressive amid a historic oil price collapse, but Iran may prove a critical exception. Investors should not underestimate the risk of a US-Iran conflict this year. Beyond that, the US election will have a decisive impact as the Democrats will seek to resume the Iranian nuclear deal and Iran would eventually play ball. Venezuela is less globally relevant this year – although a “wag the dog” scenario is a distinct possibility – but it may well be a major oil supply surprise in the 2020s. More broadly the takeaway is that oil production will be reduced involuntarily as well as voluntarily this year due to regime failures. Investment Takeaways Obviously any conflict with Iran could affect the range of Middle Eastern OPEC supply, not just the portion already shuttered due to sanctions on Iran itself. Any Iran war risk is entirely separate from the risk of supply destruction from more routine state failures in Africa. These shortages have been far less consequential lately and have plenty of room to grow in significance (Chart 20). The extreme lows in oil prices today will create the conditions for higher oil prices later when demand recovers, via supply destruction. Chart 20More Unplanned Outages To Come

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Chart 21European Political Risk No Longer Underrated

European Political Risk No Longer Underrated

European Political Risk No Longer Underrated

An important implication – to be explored in future reports – is that Europe’s neighborhood is about to get a lot more dangerous in the coming years, as the Middle East and Russia will become less stable. Middle East instability will result in new waves of immigration and terrorism after a lull since 2015-16. These waves would fuel right-wing political sentiment in parts of Europe that are the most vulnerable in today’ crisis: Italy, Spain, and France (Chart 21). This should not be equated with the EU breaking apart, however, as the populist parties in these countries are pursuing soft rather than hard Euroskepticism. Unless that changes the risk is to the Euro Area’s policy coherence rather than its existence. Finally Russian domestic instability is one of the major secular consequences of the pandemic and recession and its consequences could be far-reaching, particularly in its great power struggle with the United States. We are reinitiating a strategic long in cyber security stocks, the ISE Cyber Security Index, relative to the S&P500 Info Tech sector. Cyberattacks are a form of asymmetrical warfare that we expect to ramp up with the general increase in global geopolitical tensions. The US’s recent official warning against an unknown actor that apparently intended to attack the health system of the Czech Republic highlights the way in which malign actors could attempt to capitalize on the chaos of the pandemic. We also recommend strategic investors reinitiate our “China Play Index” – commodities and equities sensitive to China’s reflation – and our BCA Infrastructure Basket, which will benefit from Chinese reflation as well as US deficit spending. China’s reflation will help industrial metals more so than oil, but it is positive for the latter as well. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 John Mauldin, "Don't Be So Sure That States Can't Go Bankrupt," Forbes, July 28, 2016, forbes.com. Section II: Appendix : GeoRisk Indicator China

China: GeoRisk Indicator

China: GeoRisk Indicator

Russia

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

UK

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Germany

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Canada

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Spain

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Taiwan

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Turkey

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Brazil

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Appendix Table 1 The Global Fiscal Stimulus Response To COVID-19

Drowning In Oil (GeoRisk Update)

Drowning In Oil (GeoRisk Update)

Section III: Geopolitical Calendar

Highlights Yesterday we published a Special Report titled EM: Foreign Currency Debt Strains. We are upgrading our stance on EM local currency bonds from negative to neutral. Before upgrading to a bullish stance, we would first need to upgrade our stance on EM currencies. We recommend receiving long-term swap rates in Russia, Mexico, Colombia, China and India. EM central banks’ swap lines with the Fed could be used to fend off short-term speculative attacks on EM currencies. Nevertheless, they cannot prevent EM exchange rates from depreciation when fundamental pressures warrant weaker EM currencies. For the rampant expansion of US money supply to produce a lasting greenback depreciation, US dollars should be recycled abroad. This is not yet occurring. Domestic Bonds: A New Normal Chart I-1Performance Of EM Domestic Bonds In The Last Decade

Performance Of EM Domestic Bonds In The Last Decade

Performance Of EM Domestic Bonds In The Last Decade

In recent years, our strategy has favored the US dollar and, by extension, US Treasurys over EM domestic bonds. Chart I-1 demonstrates that the EM GBI local currency bond total return index in US dollar terms is at the same level as it was in 2011, and has massively underperformed 5-year US Treasurys. We are now upgrading our stance on EM local currency bonds from negative to neutral. Consistently, we recommend investors seek longer duration in EM domestic bonds while remaining cautious on the majority of EM currencies. Before upgrading to a bullish stance on EM local bonds, we would first need to upgrade our stance on EM currencies. Still, long-term investors who can tolerate volatility should begin accumulating EM local bonds on any further currency weakness. Our upgrade is based on the following reasons: First, there has been a fundamental shift in EM central banks’ policies. In past global downturns, many EM central banks hiked interest rates to defend their currencies. Presently, they are cutting rates aggressively despite large currency depreciation. This is the right policy action to fight the epic deflationary shock that EM economies are presently facing. There has been a fundamental shift in EM central banks’ policies. They are cutting rates aggressively despite large currency depreciation. Historically, EM local bond yields were often negatively correlated with exchange rates (Chart I-2, top panel). Similarly, when EM currencies began plunging two months ago, EM local bond yields initially spiked. However, following the brief spike, bond yields have begun dropping, even though EM currencies have not rallied (Chart I-2, bottom panel). This represents a new normal, which we discussed in detail in our October 24 report. Overall, even if EM currencies continue to depreciate, EM domestic bond yields will drop as they price in lower EM policy rates. Second, the monetary policy transmission mechanism in many EMs was broken before the COVID-19 outbreak. Even though central banks in many developing countries were reducing their policy rates before the pandemic, commercial banks’ corresponding lending rates were not dropping much (Chart I-3, top panel). Chart II-2EM Local Bond Yields And EM Currencies

EM Local Bond Yields And EM Currencies

EM Local Bond Yields And EM Currencies

Chart I-3EM ex-China: Monetary Transmission Has Been Impaired

EM ex-China: Monetary Transmission Has Been Impaired

EM ex-China: Monetary Transmission Has Been Impaired