Policy

Dear Client, Next week, we will send you a special report published by our Geopolitical Strategy service, authored by my colleague Roukaya Ibrahim. Roukaya will provide her insights on the global shortages of medical equipment as well as the risk of food shortages. A significant portion of the special report focuses on China. We trust you will find her report very useful. Additionally, I will be having three webcasts next week, discussing the economic and financial implications of the COVID-19 pandemic on China. The webcasts will be in both English and Mandarin. Please check out the dates and time on our website. Best regards, Jing Sima China Strategist Highlights China’s official and Caixin manufacturing PMIs in March were weak at best. The indexes underscore that a quick recovery of Chinese and global economic growth is unlikely. A recent re-lockdown of a Chinese county, along with tightened containment measures in other key Asian economies, illustrates the risk of a second wave of infections and a precarious economic “return to normalcy”. Further policy supports announced in the past week suggest that Chinese authorities may be willing to match the size of stimulus from other major economies. In the next three months, risks to Chinese stock prices are still elevated barring a peak in the global pandemic. We maintain a neutral position in both Chinese investable and domestic stocks. Feature Global financial markets are unlikely to sustainably move higher in an environment where it is uncertain whether the COVID-19 virus is abating and business activities can start resuming (Chart 1). China’s economy and stock prices are not insulated from a deep global recession. Price volatility will remain high in Chinese stocks in the next three months and, therefore, we maintain a neutral position in Chinese investable and domestic stocks. Chart 1Close To A Peak In New Cases?

China Macro And Market Review

China Macro And Market Review

In financial markets, cyclical stocks have underperformed defensives since early March. In particular, information technology, materials, industrials and consumer discretionary, all have underperformed the broad market. This reflects a delayed recovery in China’s economic fundamentals. Tables 1 and 2 highlight key developments in China’s economic and financial market performance in the past month. On the growth front, both the official and Caixin PMIs rebounded to above the 50% boom-bust threshold from historic lows in February. However, the indexes suggest that headwinds to China’s economic recovery are not yet subsiding. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review

Chart 2Supply Shock Meets A Collapse In Demand

Supply Shock Meets A Collapse In Demand

Supply Shock Meets A Collapse In Demand

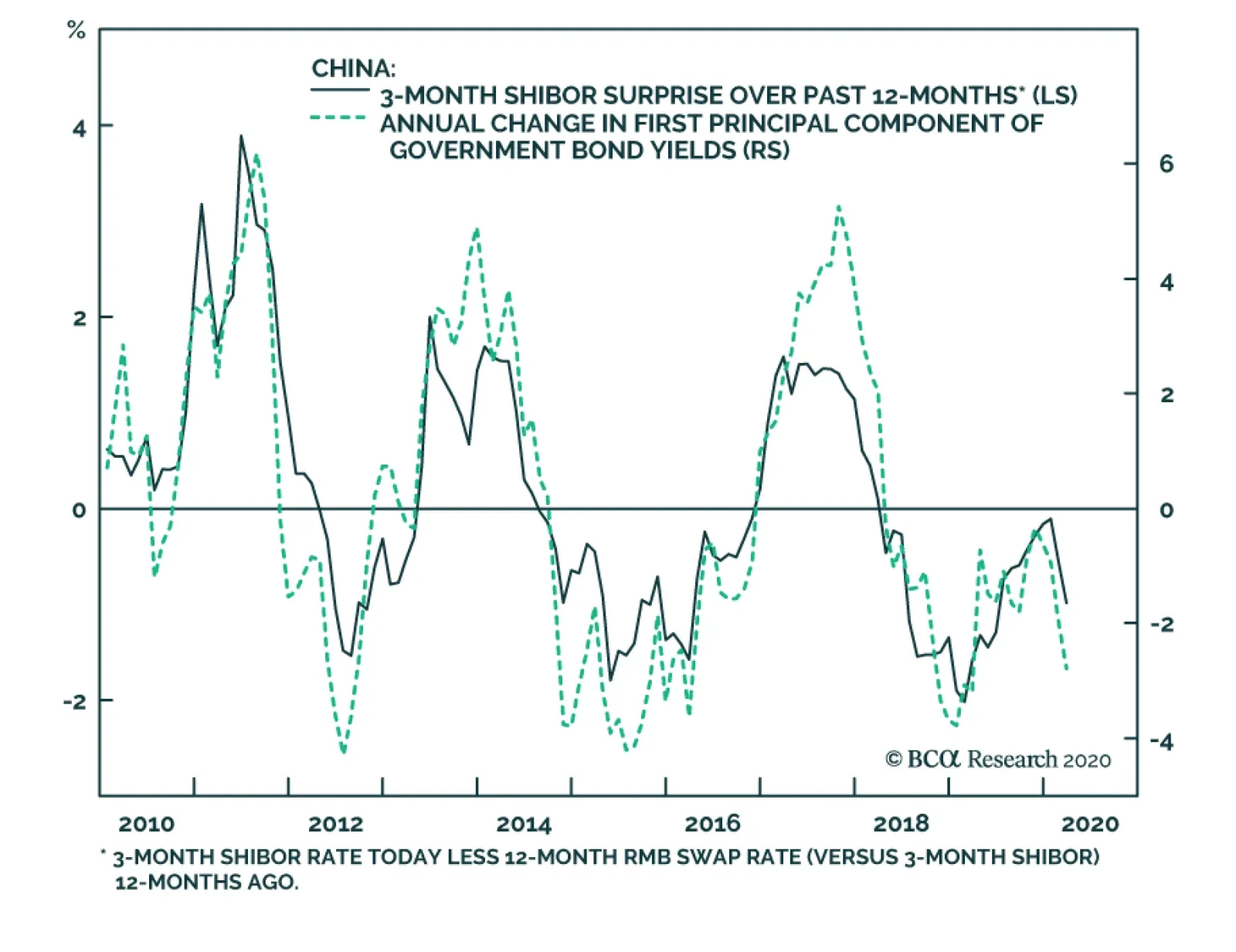

The methodology in calculating PMI indexes reflects the net reported improvement in activity relative to the previous month; a reading of 50 represents no month-over-month change. As such, a 52 reading in March’s official PMI suggests that manufacturing activity in China barely ticked up over February. This is concerning given the extremely depressed level of manufacturing activity in February (Chart 2). Furthermore, two important subcomponents of the PMI remained in contractionary territory even after February’s plunge. While the new orders subcomponent modestly improved in line with the overall index, new export orders and the imports index continued to contract (Chart 2, middle panel). The latter is particularly important for investors who focus on global growth because a modest improvement in Chinese domestic demand that does not translate into import growth is of limited benefit to China's trade partners and global economic activity. In our view, China's March PMI reflects a return to normalcy for the supply side, but it also indicates that domestic demand remains very weak (Chart 2, bottom panel). This is a discouraging result. While March’s economic data in the developed world will likely be uniformly negative, China’s weak PMI readings suggest that its economy may have been impacted by “second-round effects”. This aspect is an ominous sign for developed economies, particularly the US, where the number of new cases continues to escalate. A second wave of infections in China and other Asian nations also underlines the fragility of the rebound, both on the social and economic fronts. Although the pandemic in Asia was largely contained domestically by early March, there is now an increasing number of both imported and domestically transmitted cases. China recently locked down a county of about 600,000 residents and Singapore closed schools and workplaces last week due to a re-emergence of domestic cases.1 There are some encouraging signs in China’s housing market. The monthly real estate sector indicators in Table 1 show the severe impact of the pandemic on China’s property market in the first two months of the year. However, the seasonally adjusted daily data indicate that home sales in China’s 30 large- and medium-sized cities steadily picked up in March (Chart 3). By the end of March, the amount of floor space sold in those cities surpassed the same period of the previous year. A return to normal in housing demand and activity will be crucial for easing property developers’ cash constraints and a recovery in China’s construction sector. On the policy response front, monetary and fiscal stimulus measures continue to roll out. The PBoC chopped its 7-day reverse repo rate by 20bps on March 30, which was the third rate cut in 5 months. It helped to push the 3-month interbank repo rate back to its early-2010 low. We noted in a previous report2 that the 3-month repo rate is China's de facto short-term policy rate and that changes in the rate are strongly linked to average lending rates in the economy (Chart 4). A lowering in the repo rate will help to ease financial conditions and support an eventual rebound in China’s economic activity. Chart 3Signs Of A Gradual Revival In The Housing Market

China Macro And Market Review

China Macro And Market Review

Chart 4Lending Rates Bound To Drop Further

Lending Rates Bound To Drop Further

Lending Rates Bound To Drop Further

Further monetary and fiscal stimulus are also pending. The timing and magnitude of these measures suggest that Chinese policymakers may be willing to step up their efforts to match the size of stimulus from other major economies, such as the US.3 If so, it will support our cyclical (i.e. 6-12 months) overweight investment call on Chinese stocks relative to global benchmarks, even though we believe that the short-term risks to Chinese stock prices are still quite elevated. The PBoC adjusted down the interest rate on financial institutions’ central bank excess reserves from 0.72% to 0.35%, effective April 7. The move is significant: the last time that the PBoC reduced the excess reserve rate was in November 2008 during the global financial crisis. The excess reserve rate drop of 0.37% is also larger than the 0.27% dip in 2008. The cut in excess reserves will free up more liquidity for commercial banks and encourage them to lend to businesses. More importantly, the decrease will lower the floor of PBoC’s “interest rate corridor” and pave the way for further reduction in the MLF (the ceiling of the corridor), LPR, and even the benchmark deposit rate which has remained unchanged for the past five years (Chart 5). Last week’s Politburo meeting approved an increase in this year’s quota of local government special purpose bonds (SPBs) along with a bigger fiscal deficit, and the issuance of special treasury bonds (first time since 2007). We believe the fiscal support will help facilitate double-digit growth in infrastructure spending this year. The exact quantity of the SPB quota will be approved at the upcoming National People’s Congress (NPC), but we think the quota will be close to 4 trillion yuan. This amount, which is equivalent of 4% of China’s GDP, will almost double the 2.15 trillion yuan SPBs issued in 2019. Chart 5Lowering The Floor Opens The Door

Lowering The Floor Opens The Door

Lowering The Floor Opens The Door

Chinese stocks have lost more than 10% of their value year-to-date. In addition, cyclical stocks have underperformed defensives in the past month (Chart 6). We noted in our October 30 Special Report4 that historically these cyclical sectors have been positively correlated with pro-cyclical macroeconomic and equity market variables. Therefore, a return to outperformance in both the aggregate Chinese stocks and cyclical sectors will likely require strong evidence of an upturn in China’s business cycle. Chart 6Cyclicals Vs. Defensives Performance Has Reversed Course

Cyclicals Vs. Defensives Performance Has Reversed Course

Cyclicals Vs. Defensives Performance Has Reversed Course

Chart 7RMB Depreciated Due To A Dollar Rally...

RMB Depreciated Due To A Dollar Rally...

RMB Depreciated Due To A Dollar Rally...

The recent devaluation in the RMB against the USD is linked to the dollar’s strength. In the near term, the downward pressure on the RMB against the greenback will persist because the dollar will strengthen from signs that the global economy is entering a more protracted slowdown5 (Chart 7). We think it is unlikely that the PBoC will intervene in the exchange rate market to prop up the RMB; the weakness in the RMB has been benign and limited compared with a collapse in EM currencies (Chart 8). A strong RMB does not bode well either for China’s export price competitiveness or corporate profits (Chart 9). As such, we think that the PBoC will allow the RMB’s value to remain weak against the dollar. The ongoing race-to-the-bottom in interest rates and competitive currency devaluations have indeed provided a window for the PBoC to cut interest rates even more. Chart 8...But Appreciated Against EM Currencies

...But Appreciated Against EM Currencies

...But Appreciated Against EM Currencies

Chart 9A Strong RMB Is Not Desired In The Current Environment

A Strong RMB Is Not Desired In The Current Environment

A Strong RMB Is Not Desired In The Current Environment

Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 https://www.bloomberg.com/news/articles/2020-04-02/chinese-county-back-under-lockdown-after-infection-re-emerges?mc_cid=e33ef3872b&mc_eid=9da16a4859 https://www.scmp.com/week-asia/health-environment/article/3078297/singapore-close-schools-most-workplaces-next-week 2Please see China Investment Strategy Special Report "How To Analyze And Position Towards Chinese Government Bonds," dated January 29, 2020, available at cis.bcaresearch.com 3China has deployed bank re-lending programs and supplementary funds totaling about 1.5% of its 2019 GDP. A 4 trillion yuan local government SPBs will add more than 4% of GDP in fiscal spending. Fiscal deficit is likely to be augmented by 2% of GDP, and the issuance of special treasury bonds and local government general purpose bonds should amount to more than 2% of GDP. 4Please see China Investment Strategy Special Report "A Guide To Chinese Investable Equity Sector Performance," dated October 30, 2019, available at cis.bcaresearch.com 5Please see Foreign Exchange Strategy Weekly Report "Which Are The Most Attractive G10 Currencies?" dated March 27, 2020, available at fes.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Highlights Global shortages of medical equipment – including medicines – are frontloaded until emergency production kicks in. As the crisis abates, political recriminations between the US and China will surge. The US will seek to minimize medical supply exposure to China going forward, a boon for India and Mexico. China has escaped the COVID-19 crisis with minimal impact on food supply. Pork prices are surging due to African Swine Flu, but meat is a luxury. Still, the “Misery Index” is spiking and this will increase social instability. Food insecurity, inflation, and large current account deficits suggest that emerging market currencies will remain under pressure. Turkey and South Africa stand to suffer while we remain overweight Malaysia. Feature Chart 1Collapse In Economic Activity

Collapse In Economic Activity

Collapse In Economic Activity

With a third of the world population under some form of lockdown, general activity in the world’s manufacturing powerhouses has collapsed (Chart 1). The breakdown is a double whammy on market fundamentals. On the supply side, government-mandated containment efforts force workers in non-essential services to stay home while, on the demand side, households confined to their homes are unable to spend. Acute demand for medical supplies is causing shortages, while supply disruptions threaten states that lack food security. While global monetary and fiscal stimulus will soften the blow (Chart 2), the economic shock is estimated to be a 2% contraction in real GDP for every month of strict isolation. If measures are extended beyond April, markets will sell and new stimulus will be applied. Already the US Congress is negotiating the $1-$2 trillion infrastructure package that we discussed in our March 4 report, and cash handouts will be ongoing. When the dust settles the political fallout will be massive. Authoritarian states like China and especially Iran will face greater challenges maintaining domestic stability. Democracies like Italy and the US, which lead the COVID-19 case count, are the most likely to experience a change in leadership (Chart 3). Initially the ruling parties of the democracies are receiving a bump in opinion polling, but this will fade as households will be worse off and will likely vent their grievances at the ballot box.

Chart 2

Chart 3

Until a vaccine or treatment is discovered, medical equipment and social distancing are the only weapons against the pandemic. National production is (rightly) being redirected from clothing and cars to masks and ventilators to meet the spike in demand. Will the supply shock cause shortages in food and medicine – essential goods for humankind? In this report we address the impact of COVID-19 on global supply security and assess the market implications. Medical Equipment Shortages Will Spur Protectionism

Chart

Policymakers are fighting today’s crisis with the tools of the 2008 crisis, but a lasting rebound in financial markets will depend on surmounting the pandemic, which is prerequisite to economic recovery (Table 1). As the US faces the peak of its COVID-19 outbreak, public health officials and doctors are raising the alarm on the shortage of medical supplies. A recent US Conference of Mayors survey reveals that out of the 38% of mayors who say they have received supplies from their state, 84.6% say they are inadequate (Chart 4). Italy serves as a warning: A reported 8% of the COVID-19 cases there are doctors and health professionals, often treating patients without gloves or with compromised protective gear. These workers are irreplaceable and when they succumb the virus cannot be contained. In the US, doctors and nurses are re-using masks and sometimes treating patients behind a mere curtain, highlighting the supply shortage. While the shortages are mainly driven by a surge in demand from both medical institutions and households, they also come from the supply side, particularly China. Factory closures and transportation disruptions in China earlier this year, coupled with Beijing’s government-mandated export curbs, reduced Chinese exports, a major source of US and global supplies (Chart 5).

Chart 4

Chart 5

Other countries have imposed restrictions on exports of products used in combating the spread of COVID-19. Following export restrictions by the French, German, and Czech governments in early March, the European Commission intervened on March 15 to ensure intra-EU trade. It also restricted exports of protective medical gear outside of the EU. At least 54 nations have imposed new export restrictions on medical supplies since the beginning of the year.1 Both European and Chinese measures will reduce supplies in the US, the top destination for most of these halted exports (Chart 6).

Chart 6

Thus it is no wonder that the Trump administration has rushed to cut import duties and boost domestic production. The administration has released strategic stockpiles and cut tariffs on Chinese medical equipment used to treat COVID-19. With the whole nation mobilized, supply kinks should improve greatly in April. After a debacle in rolling out test kits (Chart 7), the US is rapidly increasing its testing capabilities to manage the crisis, with over a million tests completed as of the end of March (Chart 8). Meanwhile a coalition of companies is taking shape to make face masks. The president has invoked the defense production act to force companies to make ventilators.

Chart 7

Chart 8

However, with the pandemic peaking in the US, the hardest-hit regions will continue experiencing shortages in the near term. Shortages are prompting public outcry against the US government for its failure to anticipate and redress supply chain vulnerabilities that were well known and warned against. A report in The New York Times tells how Mike Bowen, owner of Texas-based mask-maker Prestige Ameritech, has advised the past three presidents about the danger in the fact that the US imports 95% of its surgical masks. “Aside from sitting in front of the White House and lighting myself on fire, I feel like I’ve done everything I can,” he said. He is currently inundated with emergency orders from US hospitals. The same report tells of a company called Strong Manufacturers in North Carolina that had to cut production of masks because it depends on raw materials from Wuhan, China, where the virus originated.2 The Trump administration will suffer the initial public uproar, but the US government will also seek to reduce import dependency going forward, and it will likely deflect some of the blame by focusing on the supply risks posed by China. Beijing, for its part, is launching a propaganda campaign against the US to distract from its own failures at home (some officials have even blamed the US for the virus). Meanwhile it is cranking up production and shipping medical supplies to crisis hit areas like Italy to try to repair its global image after having given rise to the virus. In addition, the city of Shenzhen is sending 1.2 million N95 masks to the US on the New England Patriots’ team plane. Even Russia is sending small donations. But these moves work to propagandistic efforts in these countries and will ultimately shame the Americans into taking measures to improve self-sufficiency. Bottom Line: The most important supply shortage amid the global pandemic is that of medical equipment. While these shortages will abate sooner rather than later, the supply chain vulnerabilities they have exposed will trigger new policies of supply redundancy and import substitution. The US in particular will seek to reduce dependency on China. That COVID-19 is aggravating rather than reducing tensions between these states, despite China’s role as a key supplier in a time of need, highlights the secular nature of their rising tensions. The US-China Drug War Shortages of pharmaceuticals are also occurring, despite the fact that the primary pandemic response is necessarily “non-pharmaceutical” (e.g. social distancing). The US Food and Drug Administration (FDA) announced the first COVID-19 related drug shortage in the US on February 27. While the specific drug was not disclosed, the announcement notes that “the shortage is due to an issue with manufacturing of an active pharmaceutical ingredient used in the drug.”3 The FDA is monitoring 20 other (non-critical) drugs potentially at risk of shortages because the sole source is China. The global spread of the pandemic will increase these shortages. On March 3 India announced export restrictions on 26 drugs, including paracetamol and several antibiotics, due to supply disruptions caused by the Chinese shutdown. While Chinese economic activity has since picked up, India is now among the string of countries under a nationwide lockdown. Similar measures enforced across Europe will also hamper the production and transportation of these goods. The implication is that even if Chinese drugs return to market, supplies further down the chain and from alternative suppliers will take a hit. The risk that this will evolve into a drug shortage depends on the intensity of the outbreak. Drug companies generally hold 3-6 months’ worth of inventories. Consequently, while inventories are likely to draw as supplies are disrupted, consumers may not experience an outright shortage immediately. In the US, as with equipment and protective gear, the government’s strategic stockpile will buffer against shortfalls in supplies of critical drugs. COVID-19 is aggravating rather than reducing US-China tensions. Nevertheless the supply chain is getting caught up in the larger US-China strategic conflict. Even before the pandemic, the US-China trade war brought attention to the US’s vulnerabilities to China’s drug exports. This dispute is not limited to illicit drugs, as with China’s production of the opioid fentanyl, but also extends to mainstream medicines, as highlighted in the selection of public statements shown in Table 2.

Chart

Chart 9

How much does the US rely on China for medicine? According to FDA data, just over half of manufacturing facilities producing regulated drugs in finished dosage form for the US market are located abroad, with China’s share at 7% (Chart 9).4 The figures are higher for manufacturing facilities producing active pharmaceutical ingredients, though still not alarming – 72% of the facilities are located abroad, with 13% in China. Of course, high-level data understate China’s influence. The complex nature of global drug supply chains means that the source of finished dosage forms masks dependencies and dominance higher up the supply chain (Figure 1).

Chart

For instance, active pharmaceutical ingredients produced in Chinese facilities are used as intermediate goods by finished dosage facilities in India as well as China. The FDA reports that Indian finished dosage facilities rely on China for three-quarters of the active ingredients in their generic drug formulations, which are then exported to the US and the rest of the world. Any supply disruption in China – or any other major drug producer – will lead to shortages further down the supply chain.

Chart 10

Chinese influence becomes more apparent when the sample is restricted to generic prescription drugs. These are especially relevant because nearly 70% of Americans are on at least one prescription drug, of which more than 90% are dispensed in the generic form. In this case, 87% of ingredient manufacturers and 60% of finished dosage manufacturers are located outside the US, with 17% of ingredient facilities and 8% of dosage facilities in China (Chart 10). Of all the facilities that manufacture active ingredients that are listed on the World Health Organization’s Essential Medicines List – a compilation of drugs that are considered critical to the health system – 71% are located aboard with 15% located in China (Chart 11). Moreover, manufacturers are relatively inflexible when adapting to market conditions and shortages. Drug manufacturing facilities generally operate at above 80% of their capacity and are thus left with little immediate capacity to ramp up production in reaction to shortages elsewhere. In addition, manufacturers face challenges in changing ingredient suppliers – there is no centralized source of information on them, and additional FDA approvals are required. The US will look to reduce its dependency on China for its drug supplies regardless of 2020 election outcome. China also has overwhelming dominance in specific categories. The Council on Foreign Relations reports that China makes up 97% of the US antibiotics market.5 Other common drugs that are highly dependent on China for supplies include ibuprofen, acetaminophen, hydrocortisone, penicillin, and heparin (Chart 12).

Chart 11

Chart 12

Taking it all together, US vulnerability can be overstated. Consider the following: Of the 370 drugs on the Essential Medicines List that are marketed in the US, only three are produced solely in China. None of these three are used to treat top ten causes of death in the United States. Import substitution is uneconomical. Foreign companies, especially Chinese companies, are attractive due to their lower costs and lax regulations. While China’s influence extends higher up the supply chain, this is true for US markets as well as other consumer markets. While China can cut off the US from the finished dosages it supplies, it cannot do the same for the ingredients that are used by facilities in other countries and eventually make their way to the US in finished dosage form. Americans are demanding that drug prices be reduced and an obvious solution is looser controls on imports. The recent activation of the Defense Production Act shows that the US can take action to boost domestic production in emergencies. Nevertheless, China is growing conspicuous to the American public due to general trade tensions and COVID-19. As it moves up the value chain, it also threatens increasing competition for the US and its allies. Hence the US government will have a strategic reason to cap China’s influence that is also supported by corporate interests and popular opinion. This will lead to tense trade negotiations with China and meanwhile the US will seek alternative suppliers. China will not want to lose market share or leverage over the United States, so it may offer trade concessions at some point to keep the US engaged. Ultimately, however, strategic tensions will catalyze US policy moves to reduce the cost differential with China and promote its rivals. Pressure on China over its currency, regulatory standards, and scientific-technological acquisition will continue regardless of which party wins the White House in 2020. The Democrats would increase focus on China’s transparency and adherence to international standards, including labor and environmental standards. Both Republicans and Democrats will try to boost trade with allies. The key beneficiaries will be India, Southeast Asia, and the Americas. Taiwan’s importance will grow as a middle-man, but so will its vulnerability to strategic tensions. Bottom Line: The US and the rest of the world are suffering shortfalls of equipment necessary to combat COVID-19. There is also a risk of drug shortages stemming from supply disruptions and emergency protectionist policies. These shortages look to be manageable, but they have exposed national vulnerabilities that will be reduced in future via interventionist trade policies. While the US and Europe will ultimately manage the outbreak, the political fallout will be immense. The US will look to reduce its dependency on China. This will increase investment in non-China producers of active pharmaceutical ingredients, such as India and Mexico. The US tactics against China will vary according to the election result, but the strategic direction of diversifying away from China is clear and will have popular impetus in the wake of COVID-19. Food Security In addition to the challenges posed by COVID-19 on medical supplies, food – another essential good – also faces risk of shortages. China is a case in point. Food prices there were on the rise well before the COVID-19 outbreak, averaging 17.3% in the final quarter of 2019. However inflation was limited to pork and its substitutes – beef, lamb and poultry – and reflected a reduction in pork supplies on the back of the African Swine Flu outbreak. While year-on-year increases in the prices of pork and beef averaged 102.8% and 21.0%, respectively, grain, fresh vegetable, and fresh fruit prices averaged 0.6%, 1.5%, and -5.0% in Q42019 (Chart 13). Chart 13Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chinese Inflation Has (Thus far) Been Contained To Pork

Chart 14China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

China's Misery Index Is Spiking - A Political Liability

However China’s COVID-19 containment measures had a more broad-based impact on food supplies, threatening to push up China’s Misery Index (Chart 14). Travel restrictions, roadblocks, quarantined farm laborers, and risk-averse truck drivers introduced challenges not only in ensuring supplies were delivered to consumers, but also to daily farm activity and planting. The absence of farm inputs needed for planting such as seeds and fertilizer, and animal feed for livestock, was especially damaging in regions hardest hit by the pandemic. Livestock farmers already struggling with swine flu-related reductions in herd sizes were forced to prematurely cull starving animals, cutting the stock of chicken and hogs. Now as the country transitions out of its COVID-19 containment phase and moves toward normalizing activity (Chart 15), food security is top of the mind. Authorities are emphasizing the need to ensure sufficient food supplies and adopt policies to encourage production.6 This is especially important for crops due to be planted in the spring. Delayed or reduced plantings would weight on the quality and quantity of the crops, pushing prices up.

Chart 15

With food estimated to account for 19.9% of China’s CPI basket – 12.8% of which goes towards pork (Chart 16) – a prolonged food shortage, or a full-blown food crisis, would be extremely damaging to Chinese families and their pocketbooks.

Chart 16

However, apart from soybeans and to a lesser extent livestock, China’s inventories are well stocked (Chart 17) and are significantly higher than levels amid the 2006-2008 and 2010-2012 food crises. Inventories have been built up specifically to provide ammunition precisely in times of crisis. Corn and rice stocks are capable of covering consumption for nearly three quarters of a year, and wheat stocks exceeding a year’s worth of consumption. Thus, while not completely immune, China today is better able to weather a supply shock. Moreover, with the exception of soybeans, China is not overly dependent on imports for agricultural supplies (Chart 18).

Chart 17

Chart 18

As the COVID-19 epicenter shifts to the US and Europe, farmers there are beginning to face the same challenges. Reports of delays in the arrival of shipments of inputs such as fertilizer and seeds have prompted American farmers to prepare for the worst and order these goods ahead of time.

Chart 19

While these proactive measures will help reduce risks to supply, farmers in Europe and parts of the US who typically rely on migrant laborers will need to search for alternative laborers as the planting season nears. Just last week France’s agriculture minister asked hairdressers, waiters, florists, and others that find themselves unemployed to take up work in farms to ensure food security. As countries become increasingly aware of the risks to food supplies, some have already introduced protectionist measures, especially in the former Soviet Union: The Russian agriculture ministry proposed setting up a quota for Russian grain exports and has already announced that it is suspending exports of processed grains from March 20 for 10 days. Kazakhstan suspended exports of several agricultural goods including wheat flour and sugar until at least April 15. On March 27, Ukraine’s economy ministry announced that it was monitoring wheat export and would take measures necessary to ensure domestic supplies are adequate. Vietnam temporarily suspended rice contracts until March 28 as it checked if it had sufficient domestic supplies. The challenge is that, unlike China, inventories in the rest of the world are not any higher than during the previous food crisis and do not provide much of a buffer against supply shortfalls (Chart 19). Higher food prices would be especially painful to lower income countries where food makes up a larger share of household spending (Chart 20). In addition to using their strategic food stockpiles, governments will attempt to mitigate the impact of higher food prices by implementing a slew of policies:

Chart 20

Trade policies: Producing countries will want to protect domestic supplies by restricting exports – either through complete bans or export quotas. Importing countries will attempt to reduce the burden of higher prices on consumers by cutting tariffs on the affected goods. Consumer-oriented policies: Importing countries will provide direct support to consumers in the form of food subsidies, social safety nets, tax reductions, and price controls. Producer-oriented policies: Governments will provide support to farmers to encourage greater production using measures such as input subsidies, producer price support, or tax exemptions on goods used in production. While these policies will help alleviate the pressure on consumers, they also result in greater government expenditures and lower revenues. Thus, subsidizing the import bill of a food price shock can weigh on public finances, debt levels, and FX reserves. Currencies already facing pressure due to the recessionary environment, such as Turkey, South Africa and Chile will come under even greater downward pressure. Food inventories ex-China are insufficient to protect against supply shortages. Bottom Line: COVID-19’s logistical disruptions are challenging farm output. This is especially true when transporting goods and individuals across borders rather than within countries. This will be especially challenging for food importing countries, as some producers have already started erecting protectionist measures and this will result in an added burden on government budgets that are already extended in efforts to contain the economic repercussions of the pandemic. Investment Implications Chart 21Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

Ag Prices Inversely Correlated With USD

China will continue trying to maximize its market share and move up the value chain in drug production. At the same time, the US is likely to diversify away from China and try to cap China’s market share. This will result in tense trade negotiations regardless of the outcome of the US election. The COVID-19 experience with medical shortages and newfound public awareness of potential medical supply chain vulnerabilities means that another round of the trade war is likely. Stay long USD-CNY. Regarding agriculture, demand for agricultural commodities is relatively inelastic. This inelasticity should prevent a complete collapse in prices even amid a weak demand environment. Thus given the risk on supplies, prices face upward pressure. However, not all crops are facing these same market dynamics. While wheat and rice prices have started to move in line with the dynamics described above, soybeans and to a greater extent corn prices have not reacted as such (Chart 21). In the case of soybeans, we expect demand to be relatively muted. China accounts for a third of the world’s soybean consumption. 80% of Chinese soybeans are crushed to produce meal to feed China’s massive pork industry. However, the 21% y/y decline in pork output in 2019 on the back of the African Swine Flu outbreak will weigh on demand and mute upward pressures on supplies. Demand for corn will also likely come in weak. The COVID-19 containment measures and the resulting halt in economic activity reduce demand for gasoline and, as a consequence, reduce demand for corn-based ethanol, which is blended with gasoline. In addition to the above fundamentals, ag prices have been weighed down by a strong USD which makes ex-US exporters relatively better off, incentivizing them to raise exports and increase global supplies. A weaker USD – which we do not see in the near term – would help support ag prices. It is worth noting that if there is broad enforcement of protectionist measures, then producers will not be able to benefit from a stronger dollar. In that case we may witness a breakdown in the relationship between ag prices and the dollar. In light of these supply/demand dynamics, we expect rice and wheat prices to be well supported going forward and to outperform corn and soybeans. Roukaya Ibrahim Editor/Strategist Geopolitical Strategy RoukayaI@bcaresearch.com Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See "Tackling COVID-19 Together: The Trade Policy Dimension," Global Trade Alert, University of St. Gallen, Switzerland, March 23, 2020. 2 See Rachel Abrams et al, "Governments and Companies Race to Make Masks Vital to Virus Fight," The New York Times, March 21, 2020. 3 The announcement also notes that there are other alternatives that can be used by patients. See "Coronavirus (COVID-19) Supply Chain Update," US FDA, February 27, 2020. 4 All regulated drugs include prescription (brand and generic), over the counter, and compounded drugs. 5 Please see Huang, Yanzhong, "The Coronavirus Outbreak Could Disrupt The US Drug Supply," Council on Foreign Relations, March 5, 2020. 6 The central government ordered local authorities to allow animal feed to pass through checkpoints amid the lockdowns. In addition, Beijing has relaxed import restrictions by lifting a ban on US poultry products and announcing that importers could apply for waivers on goods tariffed during the trade war such as pork and soybeans. The lifting of these restrictions also serves to help China meet its phase one trade deal commitments. Please see "Coronavirus hits China’s farms and food supply chain, with further spike in meat prices ahead," South China Morning Post, dated February 21, 2020.

Highlights The Federal Reserve’s temporary FIMA repo facility will go a long way in helping ease dollar-funding stress outside the US. However, with the duration of the lockdown highly uncertain, a liquidity crisis could rapidly evolve into a solvency one. If the containment measures prove successful by summer, then the global economy will be awash with much stimulus, which will be fertile ground for pro-cyclical currencies. However, in the event that we receive indications of a more malignant outcome, we could retest and break above the recent highs in the DXY. We assign a one-third probability to this outcome. For now, a barbell strategy is warranted. Hold a basket of the cheapest currencies, along with some safe-havens. Crude oil has approached capitulation lows, but conditions are not yet in place for a durable bottom. Stand aside on petrocurrencies for now. Feature Chart I-1The Fed's Liquidity Injections Are Working

The Fed's Liquidity Injections Are Working

The Fed's Liquidity Injections Are Working

The DXY index has once again broken above the psychological 100 level. This has occurred alongside the backdrop of very generous swap lines offered by the Federal Reserve to foreign central banks, as well as a temporary repo facility for foreign and international monetary authorities (FIMA). In fact, the euro-dollar cross-currency basis swap is now in positive territory, suggesting that a key funnel for offshore dollar liquidity has now significantly widened (Chart I-1). Why then has the dollar continued to strengthen, despite a concerted effort by the Fed to flood the global system with dollars? We offer and explore three reasons: The Fed’s actions are still insufficient. The dollar crisis is evolving from a liquidity one to a solvency one. The liquidity-to-growth transmission mechanism needs time. The Fed’s Actions Are Still Insufficient The Fed’s actions so far to ease the offshore dollar funding stress have been to: Offer unlimited funding through swap lines to five major central banks at the overnight index swap + 25 basis points.1 This was effective the week of March 16. Extend the swap lines to nine more central banks, with a cap of US$60 billion and a maturity of 84 days.2 This was announced March 19. Allow FIMA account holders to temporarily exchange their Treasury securities held with the Fed for US dollars. This was announced on Tuesday. Have these actions been sufficient? For most developed market currencies, yes. Chart I-2 shows that the currencies that have been most hit in the first quarter were of the countries initially excluded from the swap agreement such as Australia, Norway and New Zealand. Since the March 19 agreement, these currencies have staged significant rallies. Chart I-2Very Few Winners In Q1

Capitulation?

Capitulation?

However, there are three reasons why the Fed’s actions are still insufficient. First, they are limited to only 14 central banks, and need to be expanded further. While currencies such as the Brazilian real and Mexican peso have stabilized, others like the Turkish lira or South African rand continue their freefall. In short, many emerging market central banks do not have swap agreements with the US. These are countries with huge dollar liabilities that could continue to see their currencies fall, pushing up the aggregate dollar index. Developed market commodity currencies tend to be highly correlated to emerging market currencies (Chart I-3). There is a huge pool within the financial architecture unable to access funding through central bank swap lines. The second reason is that the pool of Treasury securities available to swap for US dollars has shrunk significantly. This has been on the back of slowing global trade, which sapped the current account surpluses of many countries, dampening their foreign exchange reserves. Thus, while the Fed’s latest actions may prevent an international dumping of US Treasurys, it may be insufficient to completely assuage funding stresses (Chart I-4). Chart I-3Commodity Currencies Still At Risk

Commodity Currencies Still At Risk

Commodity Currencies Still At Risk

Chart I-4A Smaller Pool Of Treasurys To Sell

A Smaller Pool Of Treasurys To Sell

A Smaller Pool Of Treasurys To Sell

Finally, a recent report by the Bank of International Settlements3 showed that of the US$86 trillion in outstanding foreign exchange swaps/forwards, about 60% is among non-bank financial and other institutions. This suggests there is a huge pool within the financial architecture unable to access funding through central bank swap lines. Given that hedge funds are included in this group, this category entails a lot more credit risk than any central bank will be willing to bear (Chart I-5). Chart I-5Can The Fed Bail Out Non-Banks?

Capitulation?

Capitulation?

Bottom Line: While the Fed’s injection of dollar liquidity has been massive and significant, access to these funds may be limited to entities that have significant credit risk. There is not much the Fed can do about this. But at the same time, it also suggests the Fed’s actions have been insufficient to quench the global thirst for dollar liquidity. From A Liquidity To A Solvency Crisis If the containment measures prove successful by summer, then the global economy will be awash with much stimulus, which will be fertile ground for pro-cyclical currencies. As a counter-cyclical currency, the dollar will buckle, lighting a fire under our favorites such as the Norwegian krone and the Swedish krona. The euro will be the most liquid beneficiary of this move. However, the DXY index has effortlessly broken above the psychological 100 level, suggesting we could catapult to new highs. When massive amounts of stimulus are injected into markets but prices keep falling (and the dollar keeps rallying), this portends a liquidity crisis morphing into a solvency one. What ensues is a liquidation phase where the only guiding signposts are technical indicators and valuation extremes. There are a few indications we could be stepping into this phase: During recessions, the dollar rally has tended to occur in two phases. The first phase prompts the US authorities to act, usually by dropping interest rates, which dampens the rally. The next phase epitomizes indiscriminate liquidation by financial markets (Chart I-6). Enter 2008. The US first introduced swap lines with a few central banks in December 2007. But from March to October 2008, the dollar soared by about 25%. This prompted the Fed to expand its swap lines to include even some emerging markets. Despite the knee-jerk fall in the dollar of 11%, we eventually made new highs by rallying 15%. While the Fed’s injection of dollar liquidity has been massive and significant, access to these funds may be limited. As the dollar rises, it takes time for economies to implode due to strong monetary and fiscal frameworks. The implosion of the euro area economy only surfaced well after the 2008 crisis. Specifically, there has been an epic rise in global nonfinancial corporate debt. As a result, credit default swaps across many countries are surging (Chart I-7). High-yield spreads are blowing out. Our bond strategists believe that even though there is value in investment-grade debt, high-yield paper remains at risk.4 Historically, whenever the default rate has breached 4% (as is the case now), a self-reinforcing feedback loop of higher refinancing rates and defaults ensues (Chart I-8). With a recovery rate that is going to be much lower than historical standards due to bloated balance sheets, this is worrisome. Chart I-6The Dollar Rally Occurs In Two Phases

The Dollar Rally Occurs In Two Phases

The Dollar Rally Occurs In Two Phases

Chart I-7CDS Spreads Are Widening Significantly

CDS Spreads Are Widening Significantly

CDS Spreads Are Widening Significantly

Chart I-8Large Defaults Are Ahead

Large Defaults Are Ahead

Large Defaults Are Ahead

It is difficult to pinpoint where the epicenter of the potential default wave will be. The energy sector looks like a prime candidate, putting many commodity currencies at risk. Bottom Line: There is a non-negligible risk that the liquidity crisis evolves into a solvency one. Though this is not our base case, we assign a one-third probability to this outcome. Liquidity To Growth Transmission Channel Monetary stimulus only affects the economy with a lag, and fiscal stimulus is so far unlikely to completely plug the hole from economic disruption. This leaves currency technicals and valuation as among the only few guiding signposts towards a peak in the DXY. There is usually a significant lag between easing in offshore dollar funding costs and a respective bottom in the domestic currency (Chart I-1). The AUD/JPY cross has broken below the key support zone of 70-72. This defensive line held notably during the European debt crisis, China’s industrial recession and, more recently, the global trade war. This pins the next level of support in the 55-57 zone, on par with the recessions of 2001 and 2008. The USD/JPY is weakening again and will likely hit 100. A rising yen is usually accompanied by a dollar rally against other procyclical currencies. Outside of the Fukushima crisis, this has been a key indicator that the investment environment is becoming precarious (Chart I-9). Chart I-9The Yen Could Touch 100

The Yen Could Touch 100

The Yen Could Touch 100

Some high-beta currencies such as the USD/TRY, USD/ZAR, and USD/IDR are still in freefall. These currencies are usually good at sniffing out a change in the investment landscape, specifically one becoming perilous for carry trades. Similarly, the USD/CNY has tested and has failed to break above 7.12. This will be a key level to watch since a break above will send Asian currencies into the abyss. “Doctor” copper has failed to stage a meaningful rebound. In fact, the copper-to-gold and oil-to-gold ratios continue to head lower from oversold levels. Whenever cyclical sectors are underperforming defensives at the same time as non-US markets underperforming US ones, this has signaled that the marginal dollar is rotating towards the US. This is usually dollar bullish (Chart I-10A and Chart I-10B). “Doctor” copper has failed to stage a meaningful rebound. In fact, the copper-to-gold and oil-to-gold ratios continue to head lower from oversold levels. This signifies impairment in the liquidity-to-growth transmission mechanism (Chart I-11). Earnings revisions continue to head lower across all markets. Chart I-10ACyclical Markets Are Not Confirming A Dollar Top

Cyclical Markets Are Not Confirming A Dollar Top

Cyclical Markets Are Not Confirming A Dollar Top

Chart I-10BCyclical Markets Are Not Confirming A Dollar Top

Cyclical Markets Are Not Confirming A Dollar Top

Cyclical Markets Are Not Confirming A Dollar Top

Chart I-11Dr Copper Is Sick

Dr Copper Is Sick

Dr Copper Is Sick

Bottom Line: Historically, signs of capitulation can usually be observed by paying close attention to market internals and currency technicals. While we have had some marginal improvement, we are not out of the woods yet. Portfolio Strategy Chart I-12Go Short CAD/NOK

Go Short CAD/NOK

Go Short CAD/NOK

We recommend maintaining a barbell strategy – a basket of the cheapest currencies, along with some safe-havens such as the yen and Swiss franc. Overall, investors should maintain a small upward bias in the dollar in the near term. Meanwhile, short USD/JPY positions make sense. Oil plays are becoming attractive, but conditions for a durable bottom are not yet in place. The strong rebound in the NOK/SEK cross is just an unwinding of the flash crash. If the dollar and oil have been at the epicenter of these moves, then the cross is still at risk of relapsing in the near term. We were stopped out of a long position in this cross, and will discuss oil and petrocurrencies next week. That said, a short CAD/NOK position is a much safer way to express a longer-term bearish view on the dollar (Chart I-12). We are going short this cross today with a stop-loss at 7.5. Finally, the pound remains extremely cheap versus the dollar, but the rally in recent days has eroded the potential for tactical upside. We will await better opportunities to own sterling. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 These include the Bank Of Canada, Bank Of Japan, Bank Of England, European Central Bank, and the Swiss National Bank. 2 These include the Reserve Bank of Australia, the Banco Central do Brasil, the Danmarks Nationalbank (Denmark), the Bank of Korea, the Banco de Mexico, the Norges Bank, the Reserve Bank of New Zealand, the Monetary Authority of Singapore, and the Sveriges Riksbank. 3 Stefan Avdjiev, Egemen Eren and Patrick McGuire, “Dollar Funding Costs during the Covid-19 Crisis through the Lens of the FX Swap Market,” BIS Bulletin, dated April 1, 2020. 4 Please see US Bond Strategy and Global Fixed Income Strategy Joint Special Report, “Trading The US Corporate Bond Market In A Time Of Crisis,” dated March 31, 2020, available at usbs.bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been negative: The University of Michigan's consumer sentiment index plunged to 89.1 in March from 101 the previous month, the fourth largest monthly decline over the past half a century. ADP employment recorded a loss of 27K jobs in total nonfarm private sector, including a 90K decrease in small businesses payroll which was offset by the 48K increase in healthcare. Initial jobless claims surged to 6.6 million for the week ended March 27. The ISM manufacturing index came in at a relatively benign 49.1, but this was boosted by supplier deliveries. The DXY index appreciated by 1.1% this week amid growing concerns over COVID-19 and disappointing data releases. Shortly after the $2 trillion coronavirus rescue package last week, President Trump is now calling for another "very big and bold" $2 trillion "Phase 4" package on infrastructure spending. Report Links: The Dollar Funding Crisis - March 19, 2020 Are Competitive Devaluations Next? - March 6, 2020 The Near-Term Bull Case For The Dollar - February 28, 2020 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been negative: The business climate indicator dropped to -0.28 from -0.06 in March, as the COVID-19 crisis deepens. The March consumer price inflation fell across the euro area: headline inflation fell from 1.2% to 0.7% year-on-year and core inflation decreased from 1.2% to 1%. EUR/USD depreciated by 1.1% this week. Euro zone countries have until April 9 to design another stimulus package to support the economy which might consist of financial loans and a short-term work scheme. The biggest challenge being faced is that while some member countries (including France, Italy and Spain) are calling for joint debt issuance, others (including Germany and Austria) are fiercely against it. Report Links: On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 On Money Velocity, EUR/USD And Silver - October 11, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: The jobs-to-applicants ratio dropped from 1.49 to 1.45 in February. Industrial production contracted by 4.7% year-on-year in February, down from -2.3% the previous month. Housing starts fell by 12.3% year-on-year in February. The Japanese yen appreciated by 1.6% against the US dollar this week, supported by growing concerns over COVID-19 and a global recession. The quarterly Tankan Survey shows that the sentiment index fell to a 7-year low of -8 in Q1 among large manufacturers, and dived to 8 from 20 among non-manufacturers. Besides, the survey points to a further deterioration of confidence over the next three months. Report Links: The Near-Term Bull Case For The Dollar - February 28, 2020 Building A Protector Currency Portfolio - February 7, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the UK have been negative, despite some positive releases for Q4: Consumer confidence dropped from -7 to -9 in March. Markit manufacturing PMI slipped from 48 to 47.8 in March. The current account deficit narrowed from £15.9 billion to £5.6 billion in Q4. Annualized GDP growth was unchanged at 1.1% year-on-year in Q4. The British pound soared by 2% against the US dollar this week. To preserve cash during the pandemic, the BoE's Prudential Regulation Authority (PRA) suggested commercial banks to suspend dividends and buybacks until the end of this year in addition to cancelling outstanding 2019 dividends. Moreover, the PRA also expects banks not to pay any cash bonuses to senior staff. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 A Few Trade Ideas - Sept. 27, 2019 United Kingdom: Cyclical Slowdown Or Structural Malaise? - Sept. 20, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mixed: Consumer confidence dropped from 72.2 to 65.3 in March. Manufacturing PMI slipped from 50.1 to 49.7 in March. New home sales increased by 6.2% month-on-month in February, up from 5.7% the previous month. Building permits grew by 20% month-on-month in February. However, we expect housing activities to slow down in March. The Australian dollar fell further by 0.4% against the US dollar this week. In the minutes released this Wednesday, the RBA warned that a "very material contraction" in economic activity was ahead. While the RBA said it was not possible to provide an update of the macro forecast given the "fluidity of the situation", it also expressed concerns that the contraction might linger beyond the June quarter. Report Links: On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Building permits grew by 4.7% month-on-month in February. However, business confidence plunged from -19.4 to -63.5 in March. The activity outlook index also dived from 12 to -26.7 in March. The New Zealand dollar fell by 0.8% against the US dollar this week. Similar to the BoE, the RBNZ is now restricting all locally-incorporated banks from paying dividends on ordinary shares until the economy has sufficiently recovered in order to preserve cash and support the stability of the financial system. The RBNZ is also taking measures to help support banks to lend to businesses. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 USD/CNY And Market Turbulence - August 9, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been negative: Bloomberg Nanos confidence dropped from 51.3 to 46.9 for the week ended March 27. Markit manufacturing PMI fell below 50 for the first time since last September to 46.1 in March. The Canadian dollar fell by 1.2% against the US dollar this week, weighed down by the sharp decline in oil prices. The BoC lowered the overnight target rate by another 50 bps in an emergency meeting last Friday. It also joined the QE club by launching the Commercial Paper Purchase Program (CPPP) which aims to ease short-term funding stress. Report Links: The Loonie: Upside Versus The Dollar, But Downside At The Crosses Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been negative: KOF leading indicator dropped from 100.9 to 92.9 in March. Total sight deposits increased from CHF 609 billion to CHF 621 billion for the week ended March 27. The manufacturing PMI plunged from 49.5 to 43.7 in March. Headline consumer prices fell by 0.5% year-on-year in March, further down from the 0.1% decline in February. The Swiss franc fell by 1.5% against the US dollar this week. The SNB is not only battling a weaker economic backdrop, but also strong demand for safe-haven currencies. While the SNB has less room to further lower interest rates, it is taking part in easing funding stress from the pandemic. Report Links: On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Currency Market Signals From Gold, Equities And Flows - January 31, 2020 Portfolio Tweaks Before The Chinese New Year - January 24, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been negative: Retail sales increased by 2% month-on-month in February, up from 0.5% the previous month. Manufacturing PMI fell to 41.9 from 51.6 in March, the lowest since the Great Financial Crisis. The new orders, production and employment components all plunged below 40, while suppliers' delivery index soared to 74. The Norwegian krone rebounded by 2% against the US dollar this week, following the brutal selloff in recent weeks weighed by the sharp decline in oil prices. The Norges Bank is stepping up in currency intervention to reduce volatility including buying the krone in exchange for the US dollar. We believe there is now tremendous value in the krone once oil prices stabilize. Report Links: Building A Protector Currency Portfolio - February 7, 2020 On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been negative: Retail sales grew by 2.8% year-on-year in February. Manufacturing PMI crashed to 43.2 in March from 52.7. The Swedish krona fell by 0.5% against the US dollar this week. In the Swedish Economy Report released on Wednesday, the NIER (Swedish National Institute of Economic Research) estimates that Sweden's GDP will fall by just over 6% in the second quarter. While the NIER believes that the current central bank measures are appropriate in supporting the economy in a wave of bankruptcies and mass unemployment, Sweden has more room to act with relatively lower government debt to its advantage. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Making predictions about the economic and market outlook seems a futile exercise in the midst of such massive uncertainty. The deluge of articles about COVID-19 merely serves to highlight that nobody really knows how things will play out in the year ahead. Much depends on whether an effective vaccine or treatment becomes available within a reasonable timescale and that remains an open question. Social and economic disruption will continue to intensify until the spread of the virus starts to abate. One thing is certain. Economic activity around the world faces its biggest contraction in modern times. Declines in second quarter GDP will be mind-numbingly bad in a wide range of countries, especially those that have instituted lockdowns and the closure of non-essential businesses. According to the OECD, the median economy faces an initial output decline of around 25% as a result of shutdowns and restrictions.1 Chart 1A Meltdown In Economic Activity

A Meltdown In Economic Activity

A Meltdown In Economic Activity

Estimates for the drop in US real GDP in the second quarter range as high as 50% at an annual rate. To put this into perspective, the peak-to-trough decline in US real GDP in the 2007-09 recession was a mere 4% over six quarters, and that felt catastrophic at the time. The New York Fed’s weekly economic index2 has already fallen to the lows of 2008 and worse is still to come (Chart 1). Could things be as bad as the 1930s Great Depression when US real GDP contracted by 25% over a three-year period? That would require an extreme apocalyptic view about the progression of the virus and does not bear thinking about. I am not that gloomy. Policymakers are acting aggressively to limit the economic damage. Central banks are flooding the system with liquidity and the cost of money is negligible. Meanwhile, fiscal caution has been thrown to the wind with massive government stimulus in many countries. While this will not prevent a deep recession, it will minimize the downside risks and support the eventual rebound. Markets are understandably in a deep funk because it is hard to price unknown risks. If this is no more than a two-quarter economic downturn followed by a sharp recovery, then a good buying opportunity in risk assets is in place given that monetary policy will stay hyper accommodative for a considerable time. If the downturn lingers much longer than that, then equities remain at risk. While loath to make a prediction, I am uncharacteristically tending to the more optimistic side. Let’s make the heroic assumption that we are not in an end of days scenario and that this crisis will pass at some point in the next year- hopefully sooner than later. What are some of the longer-run implications? A few come to mind. The backlash against globalization will gather impetus. Public sector debt will rise to unimaginable peacetime levels. Meanwhile, the crisis puts the final nail in the coffin of the private sector Debt Supercycle. Monetary policy will err on the side of ease for a very long time. The way that companies and other institutions have been forced to adapt to the crisis could trigger lasting changes in how they operate. Globalization In Full Retreat Chart 2A Retreat From Globalization

A Retreat From Globalization

A Retreat From Globalization

The peak of globalization has been a central part of the BCA view for several years.3 Long before the current crisis, it was clear that anti-globalization forces were gathering strength, illustrated by increased trade barriers, a backlash against inward migration in many countries, and reduced flows of foreign direct investment (Chart 2). The Trump Administration’s imposition of tariffs and the Brexit vote were two of the more obvious examples of the change in attitudes. The supply-chain interruptions caused by factory shutdowns in China will reinforce the view that shifting production to cheaper-cost countries overseas went too far. At a minimum, it seems inevitable that many companies will seek to reduce their reliance on a single producer for critical components. On the medical front, one striking fact to emerge was that China supplies around 80% of US antibiotics. There will be massive pressure to develop greater homegrown supplies of medical supplies and other products deemed critical for economic and national security. The crisis also has led to a breakdown of the Schengen Area of open borders within the European Union (EU). Many member countries have reinstituted border controls and it is unclear when these might be removed. The free movement of people is a core principle of the EU. Meanwhile, the Maastricht Treaty rules on fiscal discipline, a key element of economic union, have been thrown out of the window. Even Germany has bowed to the pressure of relaxing fiscal constraints. Finally, a worsening situation for the already troubled Italian banking system will threaten EU financial stability. Overall, the crisis will leave a huge question mark over the long-term viability of the EU. Globalization was a major force behind disinflation as production shifted to low-cost producers. A reversal of this trend will thus be inflationary, at the margin. For many, this will be a price worth paying if it means increased job security and reduced vulnerability of supply chains. But the shift away from globalization will not be the only trend that threatens an eventual resurgence of inflation. The Explosion In Government Debt: Last Gasp Of The Debt Supercycle BCA introduced the concept of the Debt Supercycle more than 40 years ago to describe the actions of policymakers to pump up demand rather than allow financial imbalances to be fully unwound during economic downturns. This inevitably meant that each new cycle began with a higher level of financial imbalances. As indebtedness rose, the economic costs of a financial cleansing increased, requiring ever-more desperate policy measures to shore things up. Unfortunately, such actions merely created the conditions for greater excesses and imbalances down the road. For example, the Federal Reserve’s aggressive response to the bursting of the tech bubble in 2000 helped set the scene for the even bigger housing bubble later in the decade. In that sense, the Debt Supercycle was a self-reinforcing trap that was bound to end badly, and that occurred in 2007. Chart 3The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

The US Household Love Affair With Debt Died A Decade Ago

Our discussion of the US Debt Supercycle was focused largely on the private sector because that is where rising imbalances posed the greatest threat to economic and financial stability. Rising public sector imbalances were less of a concern because governments do not finance themselves through the banking sector. Moreover, unlike the private sector, taxes can always be raised to boost revenues or, in extremis, the authorities can resort to the printing press. At the end of 2014, we wrote that the Debt Supercycle was dead. By that, we meant that easing policy would no longer be able to encourage a new cycle of leverage-financed private-sector spending. The downturn of 2007-09 was a turning point in attitudes toward debt, much in the way that those who lived through the Great Depression were financially conservative for the rest of their lives. Our view has been vindicated by the fact the ratio of household debt to income has decisively broken its pre-housing bubble uptrend and has failed to revive in the face of record-low interest rates (Chart 3). Corporate borrowing has been strong, but largely to finance stock buybacks and M&A activity. Capital spending has been disappointing this cycle, despite strong profits and margins. The current deep downturn will add a further nail in the coffin of the private sector Debt Supercycle. The shock of the recession and destruction of wealth will leave a legacy of increased financial caution with households wanting to build precautionary savings and companies striving to repair damaged balance sheets. It would not be a surprise to see the US personal saving rate head back to the double-digit levels of the early 1980s. While the private sector embraces greater financial conservatism, we are witnessing the start of an extraordinary surge in public sector deficits and debt from already high levels. Chart 4A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit

A Bad Starting Point For A Surge In The Federal Deficit