Policy

Highlights Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013, and have gravitated to the only available real time estimate of the real neutral rate of interest: the Laubach & Williams (“LW”) “R-star” estimate. With this apparent visualization of secular stagnation as a guide, many investors have concluded that monetary policy ceased to be stimulative last year and that recent Fed rate cuts will be of limited benefit to economic activity even once economic recovery takes hold unless inflation meaningfully accelerates (thus pushing real rates lower for any given nominal Fed funds rate). This report revisits the “LW” R-star estimate in detail, and demonstrates why the estimation is almost certainly wrong, at least over the past two decades. We also outline an inferential approach that investors can use to monitor where the neutral rate is in real time and whether it is rising or falling. The core conclusion for investors is that US Treasury yields reflect a “low rates forever” view with much higher certainty than is analytically warranted and thus appear to be anchored by a false narrative. While bond yields may not rise significantly in the near-term, investors should avoid dogmatic medium-to-longer term views about yields as they may rise meaningfully over a cyclical and secular horizon once a post-COVID-19 expansion takes hold. Feature Over the past several weeks financial markets have moved rapidly to price in a global recession stemming from the COVID-19 outbreak. As financial market participants began to turn to policy makers for support, eyes focused first on the Federal Reserve, and then fiscal authorities. Earlier this week, the ECB joined the party and announced aggressive further measures of its own. When responding to the Fed’s return to the lower bound and its other recent monetary policy decisions, many market participants have expressed the view that the Fed is largely impotent to deal with a global pandemic. There are three elements to this view. The first is that interest rate cuts are ill equipped to stimulate domestic demand if quarantine measures or other forms of “social distancing” are in effect. The second element is that the Fed has only been capable of delivering a fraction of the reduction in interest rates compared to what has occurred in response to previous contractions. The third aspect of this view is that because the neutral rate of interest is so much lower now than it was in the past, Fed rate cuts will not be as stimulative as they were before. Chart II-1Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

While we at least partly agree with the first and second elements of this view, we feel strongly that the third is flawed. Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013,1 and have gravitated to the only available real time estimate of the neutral rate of interest: the Laubach & Williams (“LW”) “R-star” estimate. This time series, which is regularly updated by the New York Fed,2 suggests that the real fed funds rate reached neutral territory in the first quarter of 2019 (Chart II-1). With this apparent visualization of secular stagnation as a guide, many investors have concluded that monetary policy ceased to be stimulative last year and that recent Fed rate cuts will be of limited benefit to economic activity even beyond the near term unless inflation meaningfully accelerates (thus pushing real rates lower for any given nominal Fed funds rate). In this Special Report we revisit the “LW” R-star estimate in detail, and demonstrate why the estimation is almost certainly wrong, at least over the past two decades. Our analysis does not reveal a precise alternative estimate of the neutral rate, although we do provide some inferential perspective on how investors may be able to monitor where the neutral rate is in real time and whether it is rising or falling. However, the core insight emanating from our report, particularly for US fixed income investors, is that US Treasury yields reflect a “low rates forever” view with much higher certainty than is analytically warranted and thus appear to be anchored by a false narrative. While bond yields may not rise significantly in the near-term, this underscores that they have the potential to rise meaningfully over a cyclical and secular horizon once economic activity recovers. As such, we caution fixed-income investors against dogmatic medium-to-longer term views about bond yields, as their potential to rise may be larger than many investors currently expect. Demystifying The LW R-star Estimate The LW estimate of the neutral rate of interest has gained credibility for three reasons. First, as noted above, the evolution of the series fits with the secular stagnation narrative re-popularized by Larry Summers. Second, the series is essentially sponsored by the Federal Reserve even if it is not officially part of the Fed’s forecasting framework, as its two creators are long-time Fed employees (Thomas Laubach is a director of the Fed’s Board of Governors, and John Williams is the current President of the New York Fed). But, in our view, there is a third important reason that global investors have accepted the LW R-star estimate of the neutral rate of interest: the methodology used to generate the estimate is extremely technically complex, and thus is difficult for most investors to penetrate. Much of the technical complexity of the LW estimate is centered around the use of a statistical procedure called a Kalman filter (“KF”). Simply described, the KF is an algorithm that tries to estimate an unobservable variable based on 1) an idea of how the unobservable variable might relate to an observable variable (the “measurement equation”), and 2) an idea of how the unobservable variable might change through time (the “transition equation”). Through a repeated process of simulating the unobserved variable based on a set of assumptions, the KF is able to compare predicted results to actual results on an observation-by-observation basis, and use that information to generate ever more reliable future estimates of the unobserved variable (Chart II-2). Chart II-2A Very Simplified Overview Of The Kalman Filter Algorithm

April 2020

April 2020

We acknowledge that a full technical treatment of the Kalman Filter as it relates to the LW estimate of the neutral rate of interest is beyond the scope of this report, and we provide a more technical overview in Box II-1. But what emerges from a detailed analysis of the model is that the Kalman Filter jointly estimates R-star, potential GDP growth, potential GDP, and the variable “z”, the determinants of R-star that are not explained by potential GDP growth. As we will highlight in the next section, this joint estimation of these four variables is a crucial aspect of the model, because a valid estimate of R-star necessitates a valid estimate of the remaining variables. BOX II-1 A Technical Overview Of The Laubach & Williams R-star Model Chart Box II-1 shows that there are three sets of formulas involved in the LW estimation: the “law of motion” for the neutral rate of interest, two measurement equations, and three transition equations. The law of motion for the neutral rate is fairly simple: R-star is a function of trend real GDP growth, as well as “other factors” represented by the variable “z”. Laubach & Williams note that z “captures factors such as households’ rate of time preference”. The measurement equations are also fairly straightforward. First, the (unobservable) output gap is a function of lagged values of itself as well as the lagged real Fed funds rate gap (relative to the unobservable neutral rate). Second, inflation is a function of lagged values of itself, past values of the output gap, relative core import prices, and lagged relative imported oil prices (the latter two variables are included to capture potential supply shocks to inflation). Note that this second measurement equation is required for the model to work, as it relates the unobservable output gap to observable inflation. As presented in Chart II-2, the three transition equations are present to simulate how the unobservable variables might move through time. Potential growth and potential output are a random walk, and “z” from the law of motion follows either a random walk or an autoregressive process. Chart Box II-1The Laubach & Williams R-star Model

April 2020

April 2020

Debunking The LW R-star Estimate Before criticizing the LW estimate of the neutral rate of interest, it is important for us to note that we have the utmost respect for the Federal Reserve and its research methods. We fully acknowledge that the LW R-star estimation is rooted in solid economic theory, and we have identified no technical errors in the setup of the LW model. Nevertheless, valid analytical efforts sometimes lead to problematic real-world results, and there are two key reasons to believe that the Kalman filter in the LW model is almost certainly misspecifying R-star, at least in terms of its estimate over the past two decades. The first reason relates to the sensitivity of the model to the interval of estimation (the period over which R-star is estimated). Chart II-3 presents the range of quarterly estimates of R-star since 2005, along with the difference between the high and low end of the range in the second panel. The chart shows that while previous estimates of R-star have generally been stable for values ranging between the early-1980s and 2006/2007, pre-1980 estimates have varied quite substantially and we have seen material revisions to the estimates over the past decade. Q1 2018 serves as an excellent example: in that quarter R-star was estimated to be 0.14%; today, the Q1 2018 R-star estimate sits at 0.92%. Chart II-3Since 2005, There Has Been Some Instability In The LW R-star Estimates

Since 2005, There Has Been Some Instability In The LW R-star Estimates

Since 2005, There Has Been Some Instability In The LW R-star Estimates

However, Table II-1 and Chart II-4 highlight the real instability of the Kalman filter estimation by demonstrating the effect of varying the starting point of the model (please see Box II-2 for a brief description of how our estimation of R-star using the LW approach differs slightly from the original procedure). Laubach & Williams originally estimated R-star beginning in Q1 1961; Table II-1 shows what happens to today’s estimate of R-star simply by incrementally varying the starting point of the model from Q1 1958 to Q4 1979. Table II-1Alternative Current LW Estimates Of R-star By Model Starting Point

April 2020

April 2020

Chart II-4Alternative Starting Points Produce Wildly Different Estimates Of R-star Today

April 2020

April 2020

BOX II-2 The Laubach & Williams R-star Model With Simplified Inflation Expectations To proxy inflation expectations in their model, Laubach & Williams use a “forecast of the four-quarter-ahead percentage change in the price index for personal consumption expenditures excluding food and energy (“core PCE prices”) generated from a univariate AR(3) of inflation estimated over the prior 40 quarters”. The authors note that a simplified measure of expectations, a 4-quarter moving average of quarterly annualized core inflation, does not materially alter their results. For the sake of parsimony we use this simplified measure in our analysis. We find that the effect shifts the current estimate of R-star only slightly (+10 basis points), and that the historical differences between our version of the 1961 estimation and the official series are indeed minor. The table highlights that the model fails to even generate a result in a majority of the cases (only 39 out of 88 of the model runs were error-free). In addition, Chart II-4 shows that of the successful estimates of R-star using the LW procedure and alternate starting dates of the model, the estimate of R-star today varies from -2% (in one case) to +2%. Excluding the one extremely negative outlier results in an effective estimate range of 0% to 2%, but the key point for investors is that this range is massive and underscores that the original model’s estimate of R-star today is heavily and unduly influenced by the interval of estimation. Investors should also note that of all of the alternative estimates of R-star today shown in Chart II-4, the estimate using the original interval is very much on the low end of the distribution. The second (and most important) reason to believe that the LW estimate is misspecifying R-star is that the output gap estimate generated by the model is almost certainly invalid, at least over the past two decades. Chart II-5presents the LW output gap estimate alongside an average of the CBO, OECD, and IMF estimates of the gap; panel 1 shows the official current LW output gap estimate, whereas panel 2 shows the range of output gap estimates that are generated using the different estimation intervals highlighted in Table II-1 and Chart II-4. Chart II-5The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

Given that the Kalman filter in the LW model jointly determines R-star and the output gap (by way of estimating potential output via estimating potential GDP growth) and that these estimates are dependent on each other, Chart II-5 highlights that in order to believe the LW R-star estimate investors must believe three things: That the US economy was chronically below potential in the late-1990s when the unemployment rate was below 5%, real GDP growth averaged nearly 5%, and the equity market was booming, That output exceeded potential in 2004/2005 by a magnitude not seen since the late-1970s / early-1980s despite an average unemployment rate, That the 2008/2009 US recession was not particularly noteworthy in terms of its deviation from potential output, and that the economy had returned to potential output by 2010/2011 when the unemployment rate was in the range of 8-9%. Chart II-6The US Economy Was Definitely Not At Full Employment In 2010

The US Economy Was Definitely Not At Full Employment In 2010

The US Economy Was Definitely Not At Full Employment In 2010

While we do not believe any of these three statements, the third is especially unlikely. Chart II-6 highlights that the economic expansion from 2009 – 2020 was the weakest on record in the post-war era in terms of average annual real per capita GDP growth. To us, this is a clear symptom of a chronic deficiency in aggregate demand, and that it is essentially unreasonable to argue that the economy was operating at full employment prior to 2014/2015. This means that the Kalman filter is generating incorrect and unreliable estimates of the output gap, which means in turn that the filter’s estimation of R-star is almost assuredly wrong. How Can Investors Tell What The Neutral Rate Is? An Inferential Approach Table II-2 presents the sensitivity of the original Q1 1961 LW estimate of R-star to a series of counterfactual scenarios for inflation, real GDP growth, nominal interest rates, and import and oil prices since mid-2009. While these scenarios do not in any way improve the validity of the LW R-star estimate, they do help clarify the theoretical basis of the model and they help reveal how investors may infer whether the neutral rate of interest is higher or lower than prevailing market rates, and whether it is rising or falling. Table II-2Sensitivity Of Current LW R-star Estimate To Counterfactual Scenarios (2009 - Present)

April 2020

April 2020

Chart II-7Core Import Price Growth Has Been Weak On Average During This Expansion

Core Import Price Growth Has Been Weak On Average During This Expansion

Core Import Price Growth Has Been Weak On Average During This Expansion

Table II-2 highlights that today’s estimate of R-star using the original LW approach is mostly sensitive to our counterfactual scenarios for growth and interest rates, but not inflation or oil prices. Shifting down import price growth also has a meaningful effect on R-star, but since core import price growth has been particularly weak over the past several years (Chart II-7), it seems unreasonable to suggest that they have been abnormally high and thus “explain” a low R-star estimate today. Table II-2 essentially highlights that the entire question of the neutral rate of interest over the past decade, and the core contradiction that led to the re-emergence of the secular stagnation thesis, can effectively be boiled down to the following simple question: “Why hasn’t US economic growth been stronger this cycle, given that interest rates have been so low?” Based on the (hopefully uncontroversial) view that interest rates influence economic activity and that economic activity influences inflation, we propose the following checklist for investors to ask themselves in order to not only determine the answer to this important question, but to help identify whether R-star in any given country is likely higher or lower than existing policy rates at any given point in time. Are interest rates above or below the prevailing level of economic growth? Are interest rates rising or falling, and how intensely? Are there identifiable non-monetary shocks (positive or negative) that appear to be influencing economic activity? Is private sector credit growth keeping pace with economic growth? Are debt service burdens in the economy high or low? The first question reflects the most basic view of R-star, which is that the real neutral rate of interest should be equal to, or at least closely related to, the potential growth rate of the economy, ceteris paribus. Questions 2 through 5 attempt to determine whether ceteris paribus holds. In terms of how the answers to these questions relate to identifying the neutral rate, consider two economies, “Economy A” and “Economy B” (Chart II-8). Economy A has broadly stable or slightly rising interest rates that are well below prevailing rates of economic growth (questions 1 & 2), no obvious beneficial shocks to domestic demand from fiscal policy or other factors (question 3), and strong private sector credit growth that is perhaps above or strongly above the current pace of GDP growth (question 4). Chart II-8'Economy A', Versus 'Economy B'

April 2020

April 2020

Inferentially, it would seem that interest rates in this hypothetical economy are below R-star today. Question 5 is in our list because the more that active private sector leveraging occurs (thus pushing up debt burdens), the more that we would expect R-star in the future to fall. This is because debt payments as a share of income cannot rise forever, and we would expect that the capacity of economy A’s central bank to raise interest rates in the future are negatively related to economy A’s private sector debt service burden today. Now, imagine another economy (“Economy B”) with interest rates well below average rates of economic growth, an interest rate trend that is flat-to-down, no identifiable non-monetary policy shocks that are restricting aggregate demand, persistently sluggish credit growth, and high private sector debt service burdens in the past. If economy B is growing (even sluggishly) and not in the middle of a recession, it would seem that prevailing interest rates are below R-star, but not significantly so. In this scenario it would seem reasonable to conclude that R-star in economy B has fallen non-trivially below its potential growth rate, and that interest rate increases are likely to move monetary policy into restrictive territory earlier than otherwise would be the case. Is The United States “Economy B”? From the perspective of some investors, our description of economy B above perfectly captures the experience of the US over the past decade: an extremely low Fed funds rate, sluggish to weak growth and inflation, all the result of a huge build-up in leverage and debt service burdens during the last economic cycle. We do not doubt that R-star fell in the US for some period of time during the global financial crisis and in the early phase of the economic recovery. But we doubt that it is as low today as the secular stagnation narrative would imply, in large part because it ignores several important aspects concerning questions 2 through 5 noted above. Chart II-9Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Non-monetary shocks to the US and global economies: Over the past 12 years, there have been at least five deeply impactful non-monetary shocks to both the US and global economies that have contributed to the disconnect between growth and interest rates: 1) a prolonged period of US household deleveraging from 2008-2014, 2) the euro area sovereign debt crisis, 3) fiscal austerity in the US, UK, and euro area from 2010 – 2012/2014 (Chart II-9), 4) the US dollar / oil price shock of 2014, and 5) the recent trade war between the US and China. Several of these shocks have been policy-driven, and in the case of austerity the negative consequences of that policy has led to a lasting change in thinking among fiscal authorities (outside of Japan) that is unlikely to reverse in the near-future. Chart II-10Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Private sector credit growth: Chart II-10 highlights the extent of household deleveraging noted above by showing the growth in total household liabilities over the past decade alongside income growth. Panel 2 shows the leveraging trend of firms, as represented by the nonfinancial corporate sector debt-to-GDP ratio. Chart II-10 underscores two points: the first is that while US household sector credit contracted for several years following the global financial crisis, it is now growing again and has largely closed the gap with income growth. The second point is that the nonfinancial corporate sector has clearly leveraged itself over the course of the expansion, arguing that interest rates have not in any way been restrictive for businesses. While it is true that firms have largely leveraged themselves to buy back stock instead of significantly increasing capital expenditures, in our view this reflects the fact that US consumer demand was impaired for several years due to deleveraging. We doubt that firms would have altered their capital structures to this degree if they did not view interest rates as extremely low. Debt service burdens: Chart II-11 highlights that US household debt service burdens were at very elevated levels prior to the financial crisis, suggesting that the neutral rate did fall for some time following the recession. But today, the debt burden facing households is the lowest it has been in the past 40 years due to both rate reductions and deleveraging, arguing against the view that household debt levels will structurally weigh on interest rates in the years to come. Chart II-12 shows that the picture is different for nonfinancial corporations, as the substantial leveraging noted above has indeed raised debt service burdens for firms. However, the nonfinancial corporate sector debt service ratio remains 400 basis points below early-2000 levels when excess corporate sector liabilities had a clear impact on the economy, suggesting that the Fed’s capacity to raise interest rates still exists following the onset of economic recovery if corporate sector credit growth does not rise sharply relative to GDP over the coming 6-12 months. Chart II-11The Debt Burden Facing US Households Is At A Record Low

The Debt Burden Facing US Households Is At A Record Low

The Debt Burden Facing US Households Is At A Record Low

Chart II-12Businesses Have Levered Up Their Balance Sheets, But There Is Still Room For Rates To Rise

Businesses Have Levered Up Their Balance Sheets, But There Is Still Room For Rates To Rise

Businesses Have Levered Up Their Balance Sheets, But There Is Still Room For Rates To Rise

The intensity of recent interest rate changes: Finally, many investors have pointed to sluggish housing activity over the past three years as evidence of a low neutral rate. However, Chart II-13 highlights that the rise in the 30-year US mortgage rate from late-2016 to late-2018 was one of the largest two-year changes in US history, and Chart II-14 shows that the growth in household mortgage credit did not fall below its trend during this period until Q4 2018, when the US stock market fell 20% from its high in response to the economic consequences of the US/China trade war. Chart II-14 also shows that mortgage credit growth responded sharply to a recent reduction in interest rates. All in all, Charts II-13 & II-14 cast doubt on the notion that the level of mortgage rates over the past three years reached restrictive territory. Chart II-13Mortgage Rates Rose Very Significantly From Late-2016 To Late-2018

Mortgage Rates Rose Very Significantly From Late-2016 To Late-2018

Mortgage Rates Rose Very Significantly From Late-2016 To Late-2018

Chart II-14A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

A Record Rise In Mortgage Rates Did Not Crack The Housing Market

Investment Conclusions In the face of a global pandemic and an attendant global recession this year, the idea of eventual Fed rate hikes and the notion that the US economy will be able to tolerate them likely seems preposterous to many investors. We agree that over the coming 6-12 months US Treasury yields are unlikely to rise; even at current levels of the 10-year Treasury yield, we are reluctant to call a trough. Chart II-15US 10-Year Treasurys Are Mostly Priced For A Repeat Of The Past Decade

US 10-Year Treasurys Are Mostly Priced For A Repeat Of The Past Decade

US 10-Year Treasurys Are Mostly Priced For A Repeat Of The Past Decade

However, Chart II-15highlights that over a long-term time horizon, the bond market is now essentially priced for a repeat of the ten-year path of the Fed funds rate following the global financial crisis. While some investors will view this as a reasonable expectation in the face of what they see as a persistent and unexplainable gap between growth and interest rates over the past decade, we think this gap is explainable and we highly doubt that a pandemic with minimal mortality risk to the working age population and the young will cause the US economy to be afflicted with active consumer deleveraging lasting 4 to 6-years, substantial and wide-ranging fiscal austerity, persistently rising trade tariffs, and sharply lower oil prices. So while we agree that the US economy will be substantially cyclically affected by COVID-19, US Treasury yields reflect a “low rates forever” view with much higher certainty than is analytically warranted and thus appear to be anchored by a false narrative. As such, we caution fixed-income investors against dogmatic medium-to-longer term views about bond yields, as their potential to rise following the upcoming recession may be larger than many investors currently believe. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 "IMF Fourteenth Annual Research Conference in Honor of Stanley Fischer," Washington DC, November 8, 2013. 2 "Measuring the Natural Rate of Interest," Federal Reserve Bank of New York.

Highlights The global economy is in the midst of a painful recession. Monetary and fiscal authorities are responding forcefully to the crisis, but the lengths of the lockouts and quarantines remain a major source of downside risk to the economy. Investors should favor stocks over bonds during the next year. The short-term outlook remains fraught with danger, so avoid aggressive bets. Central banks can tackle the global liquidity crunch, thus spreads will narrow and the dollar will weaken. The long-term impact of COVID-19 will be inflationary. Feature “The only thing we have to fear is fear itself.” Franklin Delano Roosevelt 1932 A violent global recession is underway. Last month, we wrote that a deep economic slump would be unavoidable if COVID-19 cases could not be controlled within two to three weeks.1 Since then, the number of new, recorded COVID-19 cases has mounted every day and fear prevails. Consumers are not spending; firms will face a cash crunch and/or bankruptcy, and employment will be slashed. The next few quarters could result in some of the worst GDP prints since the Great Depression. Risk assets have moved to discount this dire scenario. The global stock-to-bond ratio has collapsed by 47% since its peak on January 17th and stands at the 1st decile of it post-1980 distribution. 10-year US bond yields temporarily fell below 0.4%. The dollar has rallied against every currency and even gold traded below $1500 an ounce. Brent crude trades below $30/bbl. In this context, investors must assess if risk asset prices have declined enough to compensate for the economic hazards created by the COVID-19 pandemic. If the massive amount of monetary and fiscal stimulus announced can turn around the economy in the second half of the year, then stocks and risk assets are attractive. Otherwise, they are still not cheap enough and cash remains king. We think it is a good time to begin to parsimoniously deploy capital into risk assets. A Global Recession And An Extraordinary Response The global economy has suffered its worst shock since the Great Financial Crisis (GFC), but policymakers are deploying every tool available. In our base case, GDP will contract more quickly for two quarters than it did during the GFC, and then will recover smartly. It is hard to pinpoint exactly how quickly global GDP will contract in the next six months, but key indicators point to a grim outcome. Chart I-1Global Growth Is Plunging

Global Growth Is Plunging

Global Growth Is Plunging

China’s economy was at the forefront of the COVID-19 pandemic and its trajectory provides a glimpse into what the rest of the world should anticipate. In February, Chinese retail sales contracted by 20.5% annually and industrial production plunged by 13.5%. The German ZEW survey for March paints an equally bleak picture. The growth expectations component for the Eurozone and Germany fell to its lowest level since the GFC. The same indicator, but computed as an average of US, European and Asian subcomponents is also collapsing at an alarming pace (Chart I-1). The European flash PMI for March also points to a deep slowdown, with the services PMI plunging to 28.4, an all-time low. The performance of EM carry trades flashes a somber warning for our Global Industrial Production Nowcast (Chart I-2). Carry trade returns are imploding because global liquidity is incapable of meeting the demand for precautionary money by economic agents. This lack of liquidity is inflicting enormous damage on worldwide growth. Live trackers for US and global economic activity are also melting down. Traffic in some of the US’s largest cities is a fraction of last year's (Chart I-3). Globally, restaurant bookings have dried up and fewer airlines are flying compared to 2008. Initial jobless claims in the US have surged to 3.28 million, rapidly and decisively overtaking the weaknesses seen during the GFC. Chart I-2The Liquidation Of Carry Trade Is A Bad Omen

The Liquidation Of Carry Trade Is A Bad Omen

The Liquidation Of Carry Trade Is A Bad Omen

Chart I-3Live Trackers Are In Free Fall

April 2020

April 2020

Despite the dismal situation, some positive developments are emerging. It has been demonstrated that quarantines contain the spread of the virus. On March 18th, Wuhan recorded no new COVID-19 cases. Moreover, 10 days after its January 24th quarantine began, new cases started to fall off quickly (Chart I-4) in the city. If the recent softening in new cases in Italy’s Lombardy region continues, it will illustrate that democratic regimes can also reduce the pace of infection. Chart I-4Quarantines Do Work

April 2020

April 2020

Most importantly, policymakers around the world have shown their willingness to do “whatever it takes.” Governments are easing fiscal policy with abandon. Germany’s state bank KfW is setting aside EUR550 billion to support the economy. France will spend EUR45 billion and has earmarked EUR300 billion in small business loan guarantees. Spain announced EUR200 billion to protect domestic activity. The White House just passed a stimulus package of $2 trillion, and Canada follows suit with a CAD82 billion relief bill. (Table I-1). As A. Walter and J. Chwieroth showed, the growing financial wealth of the middle class is forcing governments to always provide large bailouts after financial crises and recessions. Otherwise, their political parties suffer extreme repudiation from power.2 Table I-1Massive Stimulus In Response To Pandemic

April 2020

April 2020

Central bankers have also become extreme reflators. Nearly every central bank in advanced economies has cut interest rates to zero or into negative territory. Most importantly, central banks have become lenders of last resort. The US Federal Reserve has announced it will engage in unlimited asset purchases; it has reopened various facilities to provide liquidity to the market and is using the US Department of the Treasury to lend directly to the private sector. Among its many measures, the European Central Bank is scrapping artificial limits on its bond purchases that were its capital keys and has offered a EUR750 billion bond purchase program. The ECB is also looking to open its OMT program. Other central banks are injecting cash directly into their domestic markets (Table I-2). The list and size of actions will expand until the markets are satiated with enough liquidity. Table I-2The Central Banks Still Had Some Options When Crisis Hit

April 2020

April 2020

The impact of these policy measures is threefold. First, the actions are designed to alleviate the global economy’s cash crunch. Secondly, they aim to support growth directly. The private sector needs direct backing to survive the lack of cash inflows that will develop in the coming weeks. If fiscal and monetary authorities can plug that hole, then spending will not have to collapse as deeply nor for as long as would otherwise be the case. Finally, it is imperative that policymakers boost confidence and ease financial conditions to allow “animal spirits” to stabilize. If risk-taking continues to tailspin, then spending will never recover and the demand for cash will only grow, creating the worst liquidity trap since the Great Depression. Policymakers around the world have shown their willingness to do “whatever it takes.” The economy will continue to weaken in the second half of 2020 if quarantines remain in place beyond the summer. Not being epidemiologists, we are not equipped to make this call with any degree of certainty. Much depends on the evolution of the disease and the political decisions taken. We do not yet know if the population will be willing to endure the economic pain of a depression, or if political pressures will rise to force isolation on those over age 60 and those suffering dangerous comorbidities who are at higher risk, and allow everyone else to return to work and school.3 Investment Implications Part 1: Bonds and Stocks Chart I-5The Stock-To-Bond Ratio Has Capitulated

The Stock-To-Bond Ratio Has Capitulated

The Stock-To-Bond Ratio Has Capitulated

While the short-term outlook remains murky for asset markets, investors with a 12-month or longer investment horizon should begin to move capital into equities at the expense of bonds. Beyond the relative technical and valuation backdrops (Chart I-5), the outlook for fiscal and monetary policy favors this allocation decision. US Treasury yields have dropped from 1.9% at the turn of the year to as low as 0.31% on March 9th. According to the bond market, inflation will average less than 1% during the coming 10 years. The OIS curve is pricing in a fed funds rate of only 68 basis points in five years. In response to this extreme pricing, Treasury bonds are exceptionally expensive (Chart I-6). Moreover, using BCA Research’s Golden Rule of Treasury Investing, there is little scope for yields to fall any lower. The Golden Rule states that the return of Treasury bonds is directly linked to the Fed's rate surprises. If over the next year the Fed cuts interest rates more than is currently priced into the OIS curve, then bond yields will fall in the next 12 months (Chart I-7). Given that the fed funds rate is already at its lower limit, the Fed will not be able to deliver such a dovish surprise and yields will have limited downside. Chart I-6Bonds Are Furiously Expensive

Bonds Are Furiously Expensive

Bonds Are Furiously Expensive

Chart I-7The Fed Cannot Pull Another Dovish Surprise Out Of Its Hat

The Fed Cannot Pull Another Dovish Surprise Out Of Its Hat

The Fed Cannot Pull Another Dovish Surprise Out Of Its Hat

The bond market is also vulnerable from a technical perspective. Our Composite Technical Indicator is as overbought today as it was in December 2008 (Chart I-8). Thus, bond prices are vulnerable to good news. Economic activity will be weak for many months, but the recent policy announcements will boost global fiscal deficits by more than $3 trillion in the next 12 to 18 months. Such a large supply of paper is bearish for bonds, especially when they are very expensive. Moreover, global central banks are engaging in large-scale quantitative easing (QE). Globally, monetary authorities have already announced the equivalent of at least $1.9 trillion in asset purchases. The GFC experience showed that QE programs put upward pressure on Treasury yields (Chart I-9). This time will not be different given the combination of QE, supply disruptions caused by quarantines and large fiscal stimulus. Chart I-8A Dire Combination For Bonds

A Dire Combination For Bonds

A Dire Combination For Bonds

Chart I-9QE Pushes Yields Up

QE Pushes Yields Up

QE Pushes Yields Up

Equities offer the opposite risk/reward ratio to bonds. Technical indicators are consistent with maximum pessimism toward equities and imply that most of the selloff is behind us, at least for the time being. The Complacency-Anxiety Indicator developed by BCA Research’s US Equity Strategy service points to widespread pessimism among investors,4 an intuition confirmed by our Sentiment indicator (Chart I-10). Moreover, our Equity Capitulation Index is as depressed as in March 2009. Investors with a 12-month or longer investment horizon should begin to move capital into equities at the expense of bonds. Despite the magnitude of the shock hitting the global economy, equities will rally if they become cheap enough and monetary conditions are accommodative enough. The BCA Valuation indicator has collapsed to “undervalued” territory and our Monetary Indicator has never been more supportive of equities (both variables are shown on page 2 of Section III). The gap between these two indicators is at its lowest level since Q1 2009 or 1982, two points that marked the end of bear markets (Chart I-11). Chart I-10Equities Have Capitulated

Equities Have Capitulated

Equities Have Capitulated

Chart I-11Supportive Combined Valuation And Monetary Backdrop For Equities

Supportive Combined Valuation And Monetary Backdrop For Equities

Supportive Combined Valuation And Monetary Backdrop For Equities

Equity multiples also offer some insight into the risk/reward ratio for stocks. The S&P 500 has collapsed by 34% since its February 19th peak and trades at 13 times forward earnings. True, analysts will revise their forecasts, but the market also only trades at 14 times trailing earnings, which cannot be downgraded. Most importantly, investors are extremely gloomy about expected growth when multiples and risk-free rates are so subdued. Risk assets cannot stabilize durably as long as the demand for dollar liquidity is not satiated. Table I-3Evaluating Where The Floor Lies

April 2020

April 2020

We can use a simple discounted cash flow model to extract the expected growth rate of long-term earnings embedded in the S&P 500. To do so, we assume that the ERP is 300 basis points, close to the long-term outperformance of stocks versus bonds. At current multiples and 10-year yields, investors are pricing in a long-term growth rate of -2% annually for earnings (Table I-3). In comparison, investors were more pessimistic in 1974, 2008 and 2011 when they anticipated long-term earnings contractions of -2.5% annually. If we assume that the long-term growth of expected earnings will fall to that depth, then we can estimate trailing P/E multiples will be under different risk-free rates. If yields fall to zero, then the P/E would be 17.7 or a price level of 2,692; however, if they rise to 1.5%, then the P/E would decline to 13.9 or a price level of 2,115 (Table I-3). Chart I-12Expected Earnings Growth And Interest Rates Are Co-Integrated

Expected Earnings Growth And Interest Rates Are Co-Integrated

Expected Earnings Growth And Interest Rates Are Co-Integrated

This method suggests that 2200 is the S&P 500’s likely floor. Risk-free rates and the expected growth rate of long-term earnings are correlated series because the anticipated evolution of economic activity drives both real interest rates and earnings (Chart I-12). Thus, it is unlikely that yields will climb if expected earnings growth falls. Instead, if the expected growth rate of long-term earnings drops to -2.5%, then yields should stand between 1% and 0.5%, implying equilibrium trailing P/Es of 15 to 16.3 times, or prices levels of 2,278 to 2,468. P/E will only fall much further if the dollar scramble lasts longer. As investors seek cash and liquidate all assets, the process can push anticipated growth rates lower while pulling bond yields higher (see next section). Investment Implications Part 2: The Uncontrolled Liquidity Crunch Is Still An Immediate Risk Risk assets cannot stabilize durably as long as the demand for dollar liquidity is not satiated. The large programs announced around the world seem to be calming this liquidity crunch. However, the situation is fluid and the crunch can come back at a moment's notice. Despite the magnitude of the shock hitting the global economy, equities will rally if they become cheap enough and monetary conditions are accommodative enough. Credit spreads blew up as investors priced in the inevitable increase in defaults that accompanies recessions (Chart I-13). Junk spreads moved to as high as 1100 basis points, their highest level since 2009. If we assume that next year, US EBITDA contracts by its average post-war magnitude (a timid assumption), then the interest coverage ratio will deteriorate to readings not seen since the S&L crisis, which will force default rates higher (Chart I-14). Chart I-13Defaults Will Rise

Defaults Will Rise

Defaults Will Rise

Chart I-14Corporate Fundamentals Will Deteriorate

Corporate Fundamentals Will Deteriorate

Corporate Fundamentals Will Deteriorate

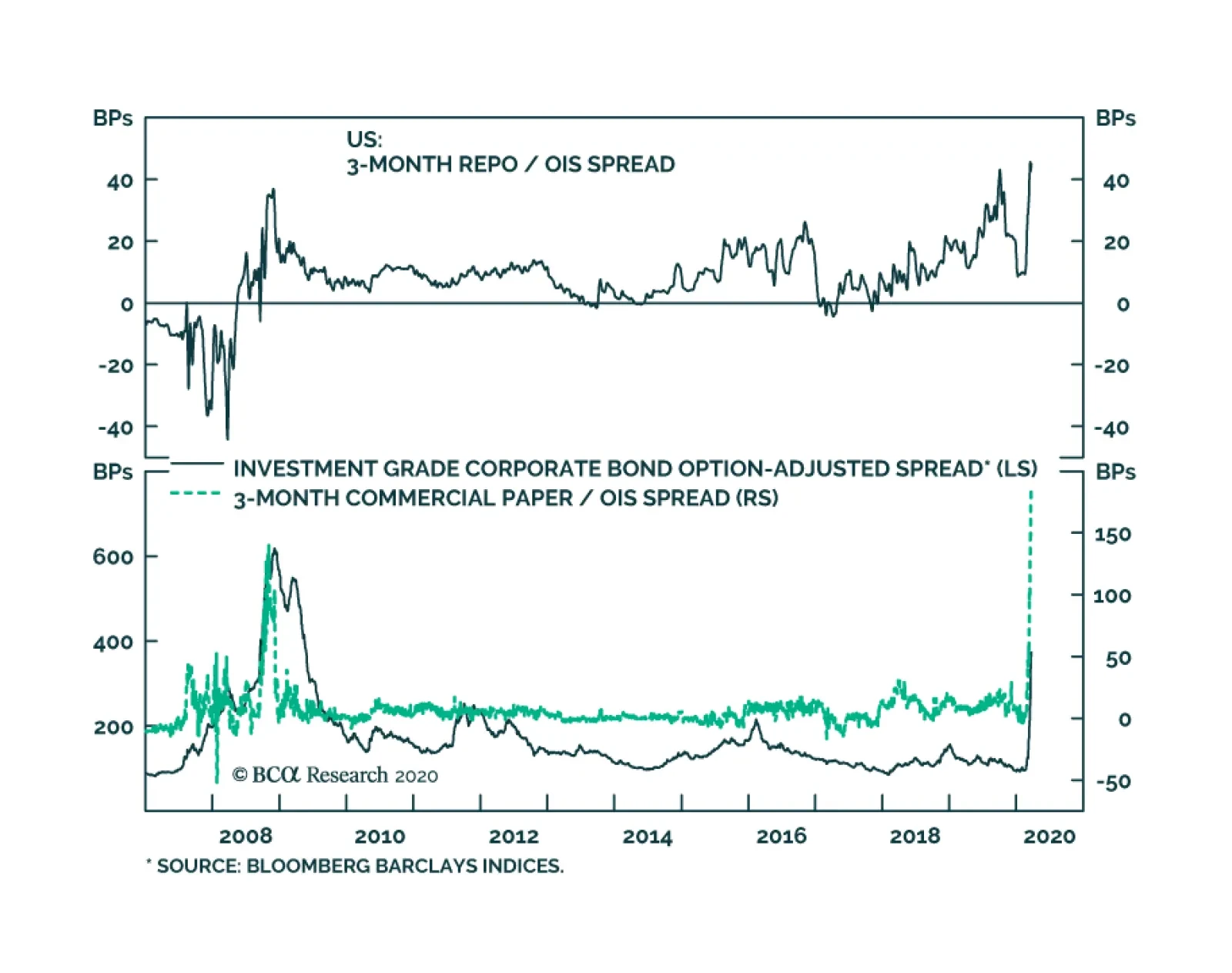

The anticipated contraction in cash flows creates another more pernicious and dangerous consequence: an insatiable demand for dollar liquidity by the private sector. Companies are worried they may not generate the necessary cash flows to service their debt. This is especially worrisome for foreign borrowers who have loans in US dollars. The BIS estimates that foreign currency debt denominated in USDs stands at $12 trillion. Meanwhile, these foreign borrowers are hoarding dollars. The risk aversion of US-based companies is accentuating the dollar crunch. US companies have pulled on their credit lines en masse. US commercial banks must provide this cash to their clients. However, US banks must still meet liquidity requirements imposed by the Basel III rules. As a result, the banks are also hoarding as much cash as possible in the form of excess reserves and curtailed their capital market lending, especially in the repo market. Repos are the lifeblood of capital markets and without repos, market liquidity (the ability to sell and buy securities) quickly deteriorates. This chain of events has caused a sharp widening in Treasury bid-ask spreads, LIBOR-OIS spreads and commercial paper-T-Bill spreads, and has fueled weaknesses in mortgage and municipal bond markets (Chart I-15). The evaporation of the repo market accentuates the foreign liquidity crunch. Without functioning repo markets, dollar funding in offshore markets becomes more onerous, as highlighted by the widening in global cross-currency basis swap spreads (Chart I-16). Borrowers are buying dollars at any cost. This has led to the surge in the dollar from March 9th, which forced the collapse of risky currencies such as the NOK, the BRL or the MXN, but also of safe-haven currencies such as the JPY and the CHF. Chart I-15Symptoms Of A Liquidity Crunch

Symptoms Of A Liquidity Crunch

Symptoms Of A Liquidity Crunch

Chart I-16Offshore Funding Pressures Point To A Dollar Shortage

Offshore Funding Pressures Point To A Dollar Shortage

Offshore Funding Pressures Point To A Dollar Shortage

The strength in the dollar is problematic. As a symptom of the liquidity crunch, it accompanies forced selling of assets by investors seeking to acquire cash. Moreover, the USD is a funding currency, hence a strong dollar also tightens the global cost of capital for all foreign borrowers who have tapped into US capital markets. For US firms, it also accentuates deflationary pressures and the resulting lower price of goods sold increases the risk of bankruptcies. Thus, a strong dollar would feed the weakness in asset prices and further widen credit spreads. Moreover, because the liquidity crunch hurts growth and can concurrently push yields higher, it could pull P/Es below 15 and drive equity prices far below our 2,200 floor. On the positive side, central banks worldwide are keenly aware of the danger created by the liquidity crunch. The Fed has started and restarted a long list of liquidity facilities (Table I-2). Its unlimited QE program also addresses the dollar shortage directly by expanding the supply of money. Crucially, the Fed has re-opened dollar swap lines with other central banks, including emerging markets such as Korea, Singapore, Mexico and Brazil. Even the ECB and the Bank of England are relaxing liquidity ratios for their banks, which at the margin will alleviate the supply of liquidity in their domestic economies. The Fed will likely follow its European counterparts, which could play a large role in alleviating the global dollar shortage. Investors seeking to assess if the supply of liquidity is large enough should pay close attention to gold prices. The global, large-scale fiscal stimulus programs will also address the dollar liquidity crisis. When investors judge there is sufficient fiscal stimulus to put a floor under global economic activity, the markets will take a more sanguine view of the risk of default. If large enough, government spending will support corporate cash flows and, therefore, limit corporate bankruptcies. Consequently, demand for liquidity will also decline and mass asset liquidations will ebb. Chart I-17Gold Is The Ultimate Liquidity Gauge

Gold Is The Ultimate Liquidity Gauge

Gold Is The Ultimate Liquidity Gauge

Investors seeking to assess if the supply of liquidity is large enough should look for some key market signals. We pay close attention to gold prices; after March 9th they fell despite the global spike in risk aversion due to gold's extreme sensitivity to global liquidity conditions. Both today and in the fall of 2008, gold prices fell when illiquidity grew. Our gold fair-value model shows that the precious metal is extremely sensitive to inflation expectations and real bond yields (Chart I-17). As illiquidity grows and the dollar appreciates, inflation breakevens collapse and real yields spike. Thus, the recent gold rebound suggests that the Fed and other major central banks have expanded the supply of liquidity sufficiently to meet demand, the price of money will fall (real interest rates) and inflation expectations will rebound. Monitor whether gold can remain well bid. Investment Implications Part 3: FX And Commodity Markets Chart I-18China's Stimulus Will Once Again Be Paramount

China's Stimulus Will Once Again Be Paramount

China's Stimulus Will Once Again Be Paramount

China’s stimulus will be a key driver of the FX market in the post-liquidity-crunch world. Historically, because Chinese reflation has lifted the global manufacturing cycle, it possesses a large influence on the dollar’s trend (Chart I-18). We believe that China’s stimulus will be comparable to the one implemented in 2008 and will boost global growth. Moreover, the interest rate advantage of the US has declined and global macro volatility will not remain at current extremes for an extended time. These three factors (Chinese stimulus, lower interest rate differentials and declining volatility) will weigh on the USD in the coming 18 months (Chart I-18, bottom panel). EM currencies and the AUD will benefit most from the dollar depreciation later this year. In the short term, these currencies remain exposed to any flare up in the liquidity crunch and can cheapen further. But, as Chart I-19 highlights, investing in those currencies will likely generate long-term excess returns because they have cheapened significantly. Commodities, too, are becoming attractive at current valuations. Industrial metals such as copper will benefit greatly from China’s stimulus. A rising Chinese credit and fiscal impulse lifts the price of base metals because it pushes up Chinese infrastructure spending as well as residential and capex investment (Chart I-20). Moreover, a lower dollar and accommodative global monetary policy will further boost the appeal of industrial metals. Chart I-19EM FX Is Cheap

EM FX Is Cheap

EM FX Is Cheap

Chart I-20China Will Drive Metal Prices Higher

China Will Drive Metal Prices Higher

China Will Drive Metal Prices Higher

China’s stimulus will be a key driver of the FX market in the post-liquidity-crunch world. The oil outlook is particularly unclear as both demand and supply factors are in flux. At $27/bbl, Brent is cheap enough to compensate investors for the decline in demand that will emerge between now and the end of the second quarter. However, the market-share war between Saudi Arabia and Russia layers on the problem of supply risk. Saudi Aramco is set to increase production to 12.3 million barrels by April and Saudi’s GCC allies have announced they are increasing output as well. According to BCA Research’s Commodity and Energy Strategy service, the oil market is already oversupplied by 1.6 million barrels per day, a number that will expand if the KSA and its allies fulfill their production pledges. If this situation persists, oil will lag behind industrial metals when global risk aversion recedes. Nonetheless, our commodity strategists believe that the collapse in oil prices is more painful for Russia than for KSA. We believe there will be a compromise between OPEC and Russia in the coming weeks that will push supply lower.5 Additionally, the Texas Railroad Commission is preparing to impose limitations on Texas oil production, which has not been done since the 1970s. Such a decision would magnify any rebound in oil prices. Thinking Long-Term: The Return Of Stagflation? The COVID-19 outbreak will likely be viewed as an epoch-defining moment. The policy response to the outbreak will be far reaching and the disease will change the way firms manage supply chains for decades to come. There will be a substantial pullback in globalization. COVID-19 has generated an inflationary shock in the medium term. Chart I-21War Spending Is Always Inflationary

War Spending Is Always Inflationary

War Spending Is Always Inflationary

COVID-19 has generated an inflationary shock in the medium term. Governments have suddenly abandoned their preferences for fiscal rectitude. The US deficit will reach a peacetime record of 15% of GDP. These are war-like spending measures. In history, gold standard or not, wars were the main reason for inflationary outbreaks as they involved massive budgetary expansions (Chart I-21). The large monetary easing accompanying the current fiscal expansion will only add to this inflationary impulse. Many of the proposals discussed by governments involve funneling cash directly to households, while central banks buy bonds issued by the same government. This is very close to helicopter money. These policies will increase the velocity of money, which is structurally inflationary (Chart I-22). Naysayers may point to the lack of inflation created by QE programs in the direct aftermath of the GFC. However, at that time, households and commercial banks were much sicker. Today, capital ratios in the US and the Eurozone are 60% and 33% higher than in 2007, respectively (Chart I-23). Thus, banks are much more likely to add to money creation instead of retracting from it as they did in the last cycle. Chart I-22If Velocity Rises, So Will Inflation

If Velocity Rises, So Will Inflation

If Velocity Rises, So Will Inflation

Chart I-23Banks Are Much Healthier Than In 2008

April 2020

April 2020

Chart I-24Financial Assets Have No Inflation Cushion

Financial Assets Have No Inflation Cushion

Financial Assets Have No Inflation Cushion

Markets are not ready for higher inflation. The 5-year/5-year forward CPI swaps in the US and the euro area stand at only 1.6% and 0.7%, respectively. Household long-term inflation expectations are also at all-time lows (Chart I-24). Therefore, an increase in inflation will have a deep impact on asset prices. The first implication is that gold prices have probably begun a new structural bull market. Inflation will surprise on the upside and keep real interest rates lower. Both these factors are highly bullish for the yellow metal. Additionally, easy fiscal policy and money printing will devalue currencies versus hard assets, which will benefit all precious metals, including gold. EM central banks have recently been diversifying aggressively in gold, which will add another impetuous to its rally. The second implication is that the stock-to-bond ratio has structural upside. Equities are not a perfect inflation hedge, but their profits can rise when selling prices accelerate. However, bonds display rock bottom real yields, inflation protection and term premia. Moreover, their low-running yields are below the dividend yields of equities, which has also boosted bond duration to record levels. Therefore, bonds offer even less protection against higher inflation. Hence, the stock-to-bond ratio will probably follow the historical experience of the 20th century structural bull market and inflect higher (Chart I-25). However, this outperformance will not stem from the superior performance of stocks in real terms; rather, it will emerge from a very poor performance by bonds. Chart I-25The Stock-To-Bond Ratio Will Follow The 20th Century Road Map

The Stock-To-Bond Ratio Will Follow The 20th Century Road Map

The Stock-To-Bond Ratio Will Follow The 20th Century Road Map

Thirdly, the structural relative bear market in EM equities will likely end soon. EM equities will enjoy strong real asset prices and EM assets have much more appealing valuations than DM stocks. This is an imbedded inflation protection. The world is witnessing a fiscal and monetary push that will result in lower productivity growth and profit margins, along with feared inflation. The next decade could increasingly look like the stagflationary 1970s. Mathieu Savary Vice President The Bank Credit Analyst March 26, 2020 Next Report: April 30, 2020 II. Revisiting The Neutral Rate Of Interest: A Contrarian View In A Time Of Crisis Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013, and have gravitated to the only available real time estimate of the real neutral rate of interest: the Laubach & Williams (“LW”) “R-star” estimate. With this apparent visualization of secular stagnation as a guide, many investors have concluded that monetary policy ceased to be stimulative last year and that recent Fed rate cuts will be of limited benefit to economic activity even once economic recovery takes hold unless inflation meaningfully accelerates (thus pushing real rates lower for any given nominal Fed funds rate). This report revisits the “LW” R-star estimate in detail, and demonstrates why the estimation is almost certainly wrong, at least over the past two decades. We also outline an inferential approach that investors can use to monitor where the neutral rate is in real time and whether it is rising or falling. The core conclusion for investors is that US Treasury yields reflect a “low rates forever” view with much higher certainty than is analytically warranted and thus appear to be anchored by a false narrative. While bond yields may not rise significantly in the near-term, investors should avoid dogmatic medium-to-longer term views about yields as they may rise meaningfully over a cyclical and secular horizon once a post-COVID-19 expansion takes hold. Over the past several weeks financial markets have moved rapidly to price in a global recession stemming from the COVID-19 outbreak. As financial market participants began to turn to policy makers for support, eyes focused first on the Federal Reserve, and then fiscal authorities. Earlier this week, the ECB joined the party and announced aggressive further measures of its own. When responding to the Fed’s return to the lower bound and its other recent monetary policy decisions, many market participants have expressed the view that the Fed is largely impotent to deal with a global pandemic. There are three elements to this view. The first is that interest rate cuts are ill equipped to stimulate domestic demand if quarantine measures or other forms of “social distancing” are in effect. The second element is that the Fed has only been capable of delivering a fraction of the reduction in interest rates compared to what has occurred in response to previous contractions. The third aspect of this view is that because the neutral rate of interest is so much lower now than it was in the past, Fed rate cuts will not be as stimulative as they were before. Chart II-1Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

Monetary Policy Ceased To Be Stimulative Last Year, According To The LW R-star Estimate

While we at least partly agree with the first and second elements of this view, we feel strongly that the third is flawed. Global investors have come to accept the secular stagnation narrative as described by Larry Summers in November 2013,6 and have gravitated to the only available real time estimate of the neutral rate of interest: the Laubach & Williams (“LW”) “R-star” estimate. This time series, which is regularly updated by the New York Fed,7 suggests that the real fed funds rate reached neutral territory in the first quarter of 2019 (Chart II-1). With this apparent visualization of secular stagnation as a guide, many investors have concluded that monetary policy ceased to be stimulative last year and that recent Fed rate cuts will be of limited benefit to economic activity even beyond the near term unless inflation meaningfully accelerates (thus pushing real rates lower for any given nominal Fed funds rate). In this Special Report we revisit the “LW” R-star estimate in detail, and demonstrate why the estimation is almost certainly wrong, at least over the past two decades. Our analysis does not reveal a precise alternative estimate of the neutral rate, although we do provide some inferential perspective on how investors may be able to monitor where the neutral rate is in real time and whether it is rising or falling. However, the core insight emanating from our report, particularly for US fixed income investors, is that US Treasury yields reflect a “low rates forever” view with much higher certainty than is analytically warranted and thus appear to be anchored by a false narrative. While bond yields may not rise significantly in the near-term, this underscores that they have the potential to rise meaningfully over a cyclical and secular horizon once economic activity recovers. As such, we caution fixed-income investors against dogmatic medium-to-longer term views about bond yields, as their potential to rise may be larger than many investors currently expect. Demystifying The LW R-star Estimate The LW estimate of the neutral rate of interest has gained credibility for three reasons. First, as noted above, the evolution of the series fits with the secular stagnation narrative re-popularized by Larry Summers. Second, the series is essentially sponsored by the Federal Reserve even if it is not officially part of the Fed’s forecasting framework, as its two creators are long-time Fed employees (Thomas Laubach is a director of the Fed’s Board of Governors, and John Williams is the current President of the New York Fed). But, in our view, there is a third important reason that global investors have accepted the LW R-star estimate of the neutral rate of interest: the methodology used to generate the estimate is extremely technically complex, and thus is difficult for most investors to penetrate. Much of the technical complexity of the LW estimate is centered around the use of a statistical procedure called a Kalman filter (“KF”). Simply described, the KF is an algorithm that tries to estimate an unobservable variable based on 1) an idea of how the unobservable variable might relate to an observable variable (the “measurement equation”), and 2) an idea of how the unobservable variable might change through time (the “transition equation”). Through a repeated process of simulating the unobserved variable based on a set of assumptions, the KF is able to compare predicted results to actual results on an observation-by-observation basis, and use that information to generate ever more reliable future estimates of the unobserved variable (Chart II-2). Chart II-2A Very Simplified Overview Of The Kalman Filter Algorithm

April 2020

April 2020

We acknowledge that a full technical treatment of the Kalman Filter as it relates to the LW estimate of the neutral rate of interest is beyond the scope of this report, and we provide a more technical overview in Box II-1. But what emerges from a detailed analysis of the model is that the Kalman Filter jointly estimates R-star, potential GDP growth, potential GDP, and the variable “z”, the determinants of R-star that are not explained by potential GDP growth. As we will highlight in the next section, this joint estimation of these four variables is a crucial aspect of the model, because a valid estimate of R-star necessitates a valid estimate of the remaining variables. BOX II-1 A Technical Overview Of The Laubach & Williams R-star Model Chart Box II-1 shows that there are three sets of formulas involved in the LW estimation: the “law of motion” for the neutral rate of interest, two measurement equations, and three transition equations. The law of motion for the neutral rate is fairly simple: R-star is a function of trend real GDP growth, as well as “other factors” represented by the variable “z”. Laubach & Williams note that z “captures factors such as households’ rate of time preference”. The measurement equations are also fairly straightforward. First, the (unobservable) output gap is a function of lagged values of itself as well as the lagged real Fed funds rate gap (relative to the unobservable neutral rate). Second, inflation is a function of lagged values of itself, past values of the output gap, relative core import prices, and lagged relative imported oil prices (the latter two variables are included to capture potential supply shocks to inflation). Note that this second measurement equation is required for the model to work, as it relates the unobservable output gap to observable inflation. As presented in Chart II-2, the three transition equations are present to simulate how the unobservable variables might move through time. Potential growth and potential output are a random walk, and “z” from the law of motion follows either a random walk or an autoregressive process. Chart Box II-1The Laubach & Williams R-star Model

April 2020

April 2020

Debunking The LW R-star Estimate Before criticizing the LW estimate of the neutral rate of interest, it is important for us to note that we have the utmost respect for the Federal Reserve and its research methods. We fully acknowledge that the LW R-star estimation is rooted in solid economic theory, and we have identified no technical errors in the setup of the LW model. Nevertheless, valid analytical efforts sometimes lead to problematic real-world results, and there are two key reasons to believe that the Kalman filter in the LW model is almost certainly misspecifying R-star, at least in terms of its estimate over the past two decades. The first reason relates to the sensitivity of the model to the interval of estimation (the period over which R-star is estimated). Chart II-3 presents the range of quarterly estimates of R-star since 2005, along with the difference between the high and low end of the range in the second panel. The chart shows that while previous estimates of R-star have generally been stable for values ranging between the early-1980s and 2006/2007, pre-1980 estimates have varied quite substantially and we have seen material revisions to the estimates over the past decade. Q1 2018 serves as an excellent example: in that quarter R-star was estimated to be 0.14%; today, the Q1 2018 R-star estimate sits at 0.92%. Chart II-3Since 2005, There Has Been Some Instability In The LW R-star Estimates

Since 2005, There Has Been Some Instability In The LW R-star Estimates

Since 2005, There Has Been Some Instability In The LW R-star Estimates

However, Table II-1 and Chart II-4 highlight the real instability of the Kalman filter estimation by demonstrating the effect of varying the starting point of the model (please see Box II-2 for a brief description of how our estimation of R-star using the LW approach differs slightly from the original procedure). Laubach & Williams originally estimated R-star beginning in Q1 1961; Table II-1 shows what happens to today’s estimate of R-star simply by incrementally varying the starting point of the model from Q1 1958 to Q4 1979. Table II-1Alternative Current LW Estimates Of R-star By Model Starting Point

April 2020

April 2020

Chart II-4Alternative Starting Points Produce Wildly Different Estimates Of R-star Today

April 2020

April 2020

BOX II-2 The Laubach & Williams R-star Model With Simplified Inflation Expectations To proxy inflation expectations in their model, Laubach & Williams use a “forecast of the four-quarter-ahead percentage change in the price index for personal consumption expenditures excluding food and energy (“core PCE prices”) generated from a univariate AR(3) of inflation estimated over the prior 40 quarters”. The authors note that a simplified measure of expectations, a 4-quarter moving average of quarterly annualized core inflation, does not materially alter their results. For the sake of parsimony we use this simplified measure in our analysis. We find that the effect shifts the current estimate of R-star only slightly (+10 basis points), and that the historical differences between our version of the 1961 estimation and the official series are indeed minor. The table highlights that the model fails to even generate a result in a majority of the cases (only 39 out of 88 of the model runs were error-free). In addition, Chart II-4 shows that of the successful estimates of R-star using the LW procedure and alternate starting dates of the model, the estimate of R-star today varies from -2% (in one case) to +2%. Excluding the one extremely negative outlier results in an effective estimate range of 0% to 2%, but the key point for investors is that this range is massive and underscores that the original model’s estimate of R-star today is heavily and unduly influenced by the interval of estimation. Investors should also note that of all of the alternative estimates of R-star today shown in Chart II-4, the estimate using the original interval is very much on the low end of the distribution. The second (and most important) reason to believe that the LW estimate is misspecifying R-star is that the output gap estimate generated by the model is almost certainly invalid, at least over the past two decades. Chart II-5presents the LW output gap estimate alongside an average of the CBO, OECD, and IMF estimates of the gap; panel 1 shows the official current LW output gap estimate, whereas panel 2 shows the range of output gap estimates that are generated using the different estimation intervals highlighted in Table II-1 and Chart II-4. Chart II-5The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

The LW Output Gap Estimates, Upon Which R-star Depends, Have Been Wrong For Two Decades

Given that the Kalman filter in the LW model jointly determines R-star and the output gap (by way of estimating potential output via estimating potential GDP growth) and that these estimates are dependent on each other, Chart II-5 highlights that in order to believe the LW R-star estimate investors must believe three things: That the US economy was chronically below potential in the late-1990s when the unemployment rate was below 5%, real GDP growth averaged nearly 5%, and the equity market was booming, That output exceeded potential in 2004/2005 by a magnitude not seen since the late-1970s / early-1980s despite an average unemployment rate, That the 2008/2009 US recession was not particularly noteworthy in terms of its deviation from potential output, and that the economy had returned to potential output by 2010/2011 when the unemployment rate was in the range of 8-9%. Chart II-6The US Economy Was Definitely Not At Full Employment In 2010

The US Economy Was Definitely Not At Full Employment In 2010

The US Economy Was Definitely Not At Full Employment In 2010

While we do not believe any of these three statements, the third is especially unlikely. Chart II-6 highlights that the economic expansion from 2009 – 2020 was the weakest on record in the post-war era in terms of average annual real per capita GDP growth. To us, this is a clear symptom of a chronic deficiency in aggregate demand, and that it is essentially unreasonable to argue that the economy was operating at full employment prior to 2014/2015. This means that the Kalman filter is generating incorrect and unreliable estimates of the output gap, which means in turn that the filter’s estimation of R-star is almost assuredly wrong. How Can Investors Tell What The Neutral Rate Is? An Inferential Approach Table II-2 presents the sensitivity of the original Q1 1961 LW estimate of R-star to a series of counterfactual scenarios for inflation, real GDP growth, nominal interest rates, and import and oil prices since mid-2009. While these scenarios do not in any way improve the validity of the LW R-star estimate, they do help clarify the theoretical basis of the model and they help reveal how investors may infer whether the neutral rate of interest is higher or lower than prevailing market rates, and whether it is rising or falling. Table II-2Sensitivity Of Current LW R-star Estimate To Counterfactual Scenarios (2009 - Present)

April 2020

April 2020

Chart II-7Core Import Price Growth Has Been Weak On Average During This Expansion

Core Import Price Growth Has Been Weak On Average During This Expansion

Core Import Price Growth Has Been Weak On Average During This Expansion

Table II-2 highlights that today’s estimate of R-star using the original LW approach is mostly sensitive to our counterfactual scenarios for growth and interest rates, but not inflation or oil prices. Shifting down import price growth also has a meaningful effect on R-star, but since core import price growth has been particularly weak over the past several years (Chart II-7), it seems unreasonable to suggest that they have been abnormally high and thus “explain” a low R-star estimate today. Table II-2 essentially highlights that the entire question of the neutral rate of interest over the past decade, and the core contradiction that led to the re-emergence of the secular stagnation thesis, can effectively be boiled down to the following simple question: “Why hasn’t US economic growth been stronger this cycle, given that interest rates have been so low?” Based on the (hopefully uncontroversial) view that interest rates influence economic activity and that economic activity influences inflation, we propose the following checklist for investors to ask themselves in order to not only determine the answer to this important question, but to help identify whether R-star in any given country is likely higher or lower than existing policy rates at any given point in time. Are interest rates above or below the prevailing level of economic growth? Are interest rates rising or falling, and how intensely? Are there identifiable non-monetary shocks (positive or negative) that appear to be influencing economic activity? Is private sector credit growth keeping pace with economic growth? Are debt service burdens in the economy high or low? The first question reflects the most basic view of R-star, which is that the real neutral rate of interest should be equal to, or at least closely related to, the potential growth rate of the economy, ceteris paribus. Questions 2 through 5 attempt to determine whether ceteris paribus holds. In terms of how the answers to these questions relate to identifying the neutral rate, consider two economies, “Economy A” and “Economy B” (Chart II-8). Economy A has broadly stable or slightly rising interest rates that are well below prevailing rates of economic growth (questions 1 & 2), no obvious beneficial shocks to domestic demand from fiscal policy or other factors (question 3), and strong private sector credit growth that is perhaps above or strongly above the current pace of GDP growth (question 4). Chart II-8'Economy A', Versus 'Economy B'

April 2020

April 2020

Inferentially, it would seem that interest rates in this hypothetical economy are below R-star today. Question 5 is in our list because the more that active private sector leveraging occurs (thus pushing up debt burdens), the more that we would expect R-star in the future to fall. This is because debt payments as a share of income cannot rise forever, and we would expect that the capacity of economy A’s central bank to raise interest rates in the future are negatively related to economy A’s private sector debt service burden today. Now, imagine another economy (“Economy B”) with interest rates well below average rates of economic growth, an interest rate trend that is flat-to-down, no identifiable non-monetary policy shocks that are restricting aggregate demand, persistently sluggish credit growth, and high private sector debt service burdens in the past. If economy B is growing (even sluggishly) and not in the middle of a recession, it would seem that prevailing interest rates are below R-star, but not significantly so. In this scenario it would seem reasonable to conclude that R-star in economy B has fallen non-trivially below its potential growth rate, and that interest rate increases are likely to move monetary policy into restrictive territory earlier than otherwise would be the case. Is The United States “Economy B”? From the perspective of some investors, our description of economy B above perfectly captures the experience of the US over the past decade: an extremely low Fed funds rate, sluggish to weak growth and inflation, all the result of a huge build-up in leverage and debt service burdens during the last economic cycle. We do not doubt that R-star fell in the US for some period of time during the global financial crisis and in the early phase of the economic recovery. But we doubt that it is as low today as the secular stagnation narrative would imply, in large part because it ignores several important aspects concerning questions 2 through 5 noted above. Chart II-9Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Fiscal Austerity Has Been A Serious Non-Monetary Shock To Aggregate Demand

Non-monetary shocks to the US and global economies: Over the past 12 years, there have been at least five deeply impactful non-monetary shocks to both the US and global economies that have contributed to the disconnect between growth and interest rates: 1) a prolonged period of US household deleveraging from 2008-2014, 2) the euro area sovereign debt crisis, 3) fiscal austerity in the US, UK, and euro area from 2010 – 2012/2014 (Chart II-9), 4) the US dollar / oil price shock of 2014, and 5) the recent trade war between the US and China. Several of these shocks have been policy-driven, and in the case of austerity the negative consequences of that policy has led to a lasting change in thinking among fiscal authorities (outside of Japan) that is unlikely to reverse in the near-future. Chart II-10Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low

Recent Trends In US Private Sector Leverage Do Not Suggest R-star Is Very Low