Policy

Highlights BCA’s “Golden Rule of Bond Investing” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, also works in China. The relationship between unexpected changes in China’s de facto short-term policy rate and government bond yields has been surprisingly strong over the past decade. Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The persistent historical gap between economic growth and bond yields in China makes it difficult to forecast the structural outlook for yields using conventional methods. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, we believe that bond yields are more likely to structurally rise than fall. Over the coming 6-12 months, investors should underweight Chinese government bonds versus Chinese equities and onshore corporate bonds. Within a regional government bond portfolio, however, investors should overweight USD-hedged China versus US and developed markets ex-US, as well as in unhedged terms. Feature Last year’s inclusion of Chinese onshore government and policy bank bonds in the Bloomberg Barclays Global Aggregate Index was a significant milestone of China’s journey to internationalize its capital markets. Other bond benchmark providers have since followed suit, highlighting that the trend of increased passive exposure to Chinese assets is likely to continue. Over the past year, the bulk of the market discussion concerning the addition of China to the major bond indices has focused on estimating the size of potential capital inflows that could be triggered and the related impact on onshore bond yields. By contrast, comparatively little work has been done to analyze the core drivers of Chinese government bond yields, and how they compare to the factors that influence yields in the developed markets that dominate the bond indices. This Special Report attempts to fill a hole in the analysis of Chinese bonds. This Special Report attempts to fill that hole in the analysis of Chinese bonds. We look at the predictability of China’s government bond market through the lens of BCA’s “golden rule” framework, and find a surprisingly strong relationship between changes in China’s de facto short-term policy rate and government bond yields. We then present our cyclical (6-12 month) and secular outlooks for government yields given this relationship, and conclude by presenting four specific investment recommendations pertaining to China’s fixed-income market with two audiences in mind: mainland/onshore investors who are focused on returns in unhedged RMB terms, and global fixed-income investors who are primarily focused on hedged US-dollar regional bond exposure. The Golden Rule Of Bond Investing, With Chinese Characteristics In a July 2018 Special Report,1 BCA’s Chief US Bond Strategist, Ryan Swift, elegantly distilled the cyclical US government bond call into a simple question: During the next 12-months, will the Federal Reserve move interest rates by more or less than what is currently priced into the market? Chart 1The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

Ryan argued that a predictive framework for US Treasury returns built around the answer to this question has historically worked so well that it should be referred to as the “Golden Rule of bond investing” (Chart 1). In a follow-up report, our Global Fixed Income Strategy service confirmed that the Golden Rule also largely works in non-US developed market economies, with the exception of Japan due to the absence of any meaningful fluctuation in policy rates over the past two decades.2 The Golden Rule provides a very strong framework to aid fixed-income investors with their cyclical (i.e. 6-12 month) asset allocation decisions, by quantitatively linking government bond returns relative to cash – in other words, the excess return earned by taking duration risk - to policy rate “surprises” compared to what is discounted in shorter-term money markets. The practical application is that a decision to allocate to longer-maturity government bonds is reduced to a bet on whether a central bank will adjust policy rates by more or less than the market expects. The first question we address in this report is to what degree does the Golden Rule apply in China (in yield space rather than in return space), along with an explanation of any differences that may exist. However, we must first note why the Golden Rule of bond investing works, particularly in the US. The first reason is that there is a strong relationship between the US 3-month T-bill rate and Treasury yields of all other maturities. Conceptually, all fixed income investors have a choice when buying US government bonds: they can purchase a 3-month Treasury bill and simply perpetually roll over the position as it matures, or they can purchase a Treasury bond of a longer maturity. This means that yields on longer maturity Treasury bonds simply reflect investor expectations for the average 3-month T-bill rate over the life of the bond, plus some positive risk premium to compensate for the inherent uncertainty of the path and tendency of short-term yields. This helps explain the close link between cyclical changes in 3-month T-bill rates and yields on longer maturity Treasurys. Chart 2In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

The second reason for the Golden Rule’s success is that there is a very tight relationship between the effective Fed funds rate and the 3-month T-bill rate. While it is the (higher) discount rate that is the theoretical no-arbitrage ceiling for the 3-month rate, in practice T-bill rates trade extremely close to the Fed funds rate (Chart 2). This means that Fed funds rate “surprises” (relative to traded market expectations) are akin to surprises in the 3-month rate, which in turn strongly influence the expected future path of short-term interest rates and thus yields on longer maturity Treasurys. In China, we noted in a February 2018 Special Report3 that the 7-day interbank repo rate is now the de jure short-term policy rate in China following the establishment of an interest rate corridor system in 2015. Chart 3 presents our first test of the Golden Rule in China (in yield space rather than in return space), by plotting the annual change in the level of Chinese government bond yields alongside the 7-day repo rate “surprise” over the past year from 2010 to the present. Here, we use the first principal component of zero coupon Chinese government bond yields to represent the average level of yields (rather than selecting a particular maturity), and we use the 12-month RMB swap rate (versus 7-day repo) to represent market expectations for the policy rate. The chart highlights that the fit is good, as measured by a 50% R-squared between the two series. However, deviations in the relationship do exist, with the most notable exception having occurred in 2017: Chinese government bond yields rose considerably more than what the annual surprise in the 7-day repo rate would have suggested. Chart 3In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

Chart 4...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

Chart 4 helps resolve a good portion of the 2017 discrepancy, and clarifies the link between Chinese monetary policy and government bond yields. Chart 4 is similar to Chart 3, except that it replaces the 7-day repo rate surprise with that of 3-month SHIBOR (which trades very closely to the 3-month repo rate). The chart illustrates an even closer fit between the two series (with an R-squared close to 80%), and shows that the 3-month SHIBOR surprise does a meaningfully better job at explaining the 2017 rise in Chinese government bond yields. The Golden Rule of bond investing works surprisingly well in China. The fact that the annual surprise in 3-month SHIBOR has done a better job at predicting changes in bond yields over the past decade underscores that the 3-month repo rate is the de facto short-term policy rate in China, a point that we have made in several previous reports. We have noted that the spike in the 3-month/7-day repo rate spread that occurred in late-2016 and lasted until mid-2018 happened because of China’s crackdown on shadow banking activity. This crackdown caused a funding squeeze for China’s small & medium banks, which caused a material rise in lending rates and government bond yields. This episode highlights that future changes in the 3-month repo rate are likely to reflect both underlying changes in net liquidity provided to large commercial banks (measured by the 7-day repo rate), and any dislocations in the interbank market that have the potential to push up lending rates and government bond yields. Bottom Line: BCA’s “Golden Rule” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, works for China as well – using the correct measure of the PBOC policy rate. This provides a useful investment framework for Chinese government bonds, which are now significant part of major global bond market benchmarks. The Cyclical Outlook For Chinese Government Bond Yields Given the establishment of the relationship between Chinese short-term interbank rates and government bond yields detailed above, we are now able to more precisely discuss the likely cyclical trajectory of Chinese government bond yields as a function of Chinese monetary policy. Two opposing forces have the potential to affect China’s government bond market this year. The first, a stabilization and modest rebound in Chinese economic activity, may exert upward pressure on yields due to expectations of eventual policy tightening. The second, continued attempts by the PBoC to ease corporate lending rates, may exert downward pressure on yields as it will reflect not just easy but easier monetary conditions. Yields at the long-end are likely to move modestly higher this year, at most. For investors, the raises the obvious question of whether Chinese government bond yields are likely to move up, down, or trend sideways this year. In our view, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. Yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. There are two reasons why yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. The first is that the PBoC is generally a reactive central bank and has historically lagged a pickup in economic activity, as illustrated in Chart 5. The chart shows the historical path of 3-month SHIBOR in the year following a bottom in economic activity in 2009, 2012, and 2015, and makes it clear that there has been no precedent for a significant rise in interbank rates in the first nine months of an economic recovery. The 2012 episode did see a very sharp rise in 3-month SHIBOR once the PBoC shifted into tightening mode, but we doubt that this experience will be repeated again unless economic growth accelerates much more aggressively than we expect. The second reason why we expect yields at the short-end of the curve to remain muted this year is because any additional easing by the PBoC is likely to be focused on reducing corporate lending rates, not interbank rates. Chart 6 highlights that while there is a strong correlation between changes in Chinese government bond yields and average lending rates in the economy, the former leads the latter. In the past, this relationship has existed because changes in interbank rates have coincided with reductions in the now obsolete benchmark lending rate, with the former usually occurring earlier than the latter. But in a scenario where the PBoC reduces the loan prime rate (LPR) and keeps net banking sector liquidity roughly constant, the extremely tight relationship shown in Chart 4 suggests that short-term bond yields are unlikely to be affected by a reduction in lending rates. Any meaningful decline in short-term yields below short-term interbank rates would simply prompt banks to stop buying these bonds. Chart 5The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

Chart 6Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Chart 7China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

Additional easing by the PBoC does have the potential to impact the long-end of the government bond curve if investors view these actions as a sign that interbank rates will remain low for some time. This view is reinforced by the fact that China’s yield curve is not particularly flat, and thus has room to move lower. However, Chart 7 also shows that China’s yield curve, defined here as the second principal component of zero coupon Chinese government bond yields, is positively correlated with the relative performance of investable Chinese equities. This suggests that there is a procyclical element to the curve. We suspect that this procyclical element will dominate a potential decline in expectations for future short-term interest rates, but that yields at the long-end are likely to move modestly higher this year, at most. Bottom Line: Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The Secular Outlook For Chinese Government Bond Yields A common approach to forecasting the likely structural trend for nominal government bond yields is to estimate the trajectory of real long-term potential output growth and to add the monetary authority’s inflation target. This framework is based on the idea that interest rates are in equilibrium when the cost of borrowing is roughly equal to nominal income growth, a condition that results in no change in the burden to service existing debt. Chart 8China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

Based on this framework, we would expect Chinese government bond yields to trend down over time, or possibly flat if the PBoC were to tolerate higher inflation over the coming decade. Chart 8 illustrates the IMF’s forecast of falling real potential growth in China over the coming several years, which is consistent with a shift in the composition of growth from investment to consumption as well as China’s looming demographic crisis. But Chart 9highlights an obvious problem with applying this framework to forecast the secular trend in Chinese government bond yields: over the past decade, yields have persistently averaged below actual nominal GDP growth, both in China and in the developed world. In the latter case, it is an open question whether this will continue to be true in the future, but in China’s case it is clear that government bond yields have little connection (in magnitude) to the pace of GDP growth. This reflects the longstanding strategy of Chinese policymakers to promote investment via persistently low interest rates, as has occurred in other manufacturing and export-oriented Asian economies (Chart 10). Chart 9...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

Chart 10In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

The persistent historical gap between economic growth and bond yields in China makes it difficult to forecast the structural outlook for yields using conventional methods, and largely limits us to inference. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, bond yields are more likely to rise than fall over time. This is because as long as interest rates remain well below the pace of income growth, the incentive to excessively borrow (and invest) is likely to persist. Chart 11China Needs Higher Interest Rates, But Only To A Point

China Needs Higher Interest Rates, But Only To A Point

China Needs Higher Interest Rates, But Only To A Point

However, even in a scenario where Chinese government bond yields structurally trend higher, we expect the rise to be modest. Chart 11 highlights that China’s “private sector” debt service ratio is extremely elevated, underscoring that the country’s ability to tolerate significantly higher bond yields is not strong. In addition, since 2015, China’s debt service ratio has been mostly flat despite rising a rising debt-to-GDP ratio, which has been achieved through lower short-term interest rates. To the extent that policymakers fail to make meaningful progress in shifting China’s growth drivers away from investment over the coming few years, lower (potentially sharply lower) bond yields would appear to be all but inevitable to cope with what would become a permanently growing drag on economic activity from the servicing of debt. For now, we would characterize this scenario as a risk to our base case view, but it is a risk that we will be closely monitoring over the coming years. Bottom Line: The persistent gap between Chinese nominal GDP growth and government bond yields is likely contributing to the problem of excessive leveraging. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, bond yields are more likely to structurally rise than fall. Investment Conclusions Our analysis above points to four recommendations for investors over the coming year: Overweight Chinese stocks versus Chinese government bonds in RMB and USD terms Overweight Chinese onshore corporate bonds versus duration-matched Chinese government bonds in RMB terms Overweight 7-10 year USD-hedged Chinese government bonds versus their US and developed market (DM) counterparts For offshore US dollar-based investors, long 7-10 year Chinese government bonds in unhedged terms Regarding the first two recommendations, our view that yields are likely to be flat at the short-end and modestly higher at the long-end suggests that investors can expect total returns on the order of 2-3% from Chinese government bonds this year. Barring a major and lasting economic slowdown from the 2019-nCoV outbreak, we expect Chinese domestic and investable equities to outperform government securities over the coming 6-12 months. Onshore corporate bonds have a similar outlook: onshore spreads are pricing in (massively) higher default losses than we believe is warranted, meaning that they will outperform duration-matched government equivalents without any changes in yield. Chart 12Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Chart 13Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

For global fixed-income investors, Charts 12-14 present USD-hedged 10-year Chinese government yields versus the US and DM/DM ex-US, along with the historical relative return profile of USD-hedged Chinese bonds versus hedged and unhedged returns. In hedged space, Chinese 10-year government bond yields are modestly attractive: 2.2% versus 1.6% in the US and 1.8% in DM ex-US. China’s historically low yield beta to the overall level of global 10-year bond yields (Chart 15) suggests that Chinese yields should perform well in 2020 – a year where we expect global bond yields to drift higher as economic growth rebounds. Combined with relatively attractive valuation, this bodes well for the relative performance of Chinese debt versus DM equivalents. A low yield beta against a backdrop of drifting higher global yields implies that longer-maturity Chinese government bonds will outperform their DM equivalents. Chart 14Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Chart 15China's Yield Beta Has Been Rising, But Is Still Japan-Like

China's Yield Beta Has Been Rising, But Is Still Japan-Like

China's Yield Beta Has Been Rising, But Is Still Japan-Like

We would also recommend longer-maturity Chinese government bonds in unhedged terms versus a USD-hedged global government bond portfolio. Chart 16 highlights that the relative return of this trade is strongly (negatively) linked to USD-CNY, and we expect further (albeit more modest) gains in RMB over the cyclical horizon. Chart 16Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

As a final point, investors should note that today’s report is part of a heightened focus on China’s fixed income market, in terms of both forecasting fixed income returns and analyzing the cyclical and structural implications of the increasing investability of China’s financial markets. More research on this topic is likely to come in 2020 and beyond: Stay Tuned! Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 Please see US Bond Strategy Special Report "The Golden Rule Of Bond Investing," dated July 24, 2018, available at usbs.bcaresearch.com 2 Please see Global Fixed Income Strategy Special Report "The Global Golden Rule Of Bond Investing," dated September 25, 2018, available at gfis.bcaresearch.com 3 Please see China Investment Strategy Special Report "Seven Questions About Chinese Monetary Policy," dated February 22, 2018, available at cis.bcaresearch.com

Dear clients, Please note that in next week’s China Macro And Market Review, we will include a section explaining our view on the coronavirus outbreak and its economic as well as financial market implications. We maintain our overweight stance on both Chinese investable and A-share equities, over a tactical (0-3 months) and cyclical (6-12 months) time horizon. Please stay tuned. Jing Sima, China Strategist Highlights BCA’s “Golden Rule of Bond Investing” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, also works in China. The relationship between unexpected changes in China’s de facto short-term policy rate and government bond yields has been surprisingly strong over the past decade. Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The persistent historical gap between economic growth and bond yields in China makes it difficult to forecast the structural outlook for yields using conventional methods. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, we believe that bond yields are more likely to structurally rise than fall. Over the coming 6-12 months, investors should underweight Chinese government bonds versus Chinese equities and onshore corporate bonds. Within a regional government bond portfolio, however, investors should overweight USD-hedged China versus US and developed markets ex-US, as well as in unhedged terms. Feature Last year’s inclusion of Chinese onshore government and policy bank bonds in the Bloomberg Barclays Global Aggregate Index was a significant milestone of China’s journey to internationalize its capital markets. Other bond benchmark providers have since followed suit, highlighting that the trend of increased passive exposure to Chinese assets is likely to continue. Over the past year, the bulk of the market discussion concerning the addition of China to the major bond indices has focused on estimating the size of potential capital inflows that could be triggered and the related impact on onshore bond yields. By contrast, comparatively little work has been done to analyze the core drivers of Chinese government bond yields, and how they compare to the factors that influence yields in the developed markets that dominate the bond indices. This Special Report attempts to fill a hole in the analysis of Chinese bonds. This Special Report attempts to fill that hole in the analysis of Chinese bonds. We look at the predictability of China’s government bond market through the lens of BCA’s “golden rule” framework, and find a surprisingly strong relationship between changes in China’s de facto short-term policy rate and government bond yields. We then present our cyclical (6-12 month) and secular outlooks for government yields given this relationship, and conclude by presenting four specific investment recommendations pertaining to China’s fixed-income market with two audiences in mind: mainland/onshore investors who are focused on returns in unhedged RMB terms, and global fixed-income investors who are primarily focused on hedged US-dollar regional bond exposure. The Golden Rule Of Bond Investing, With Chinese Characteristics In a July 2018 Special Report,1 BCA’s Chief US Bond Strategist, Ryan Swift, elegantly distilled the cyclical US government bond call into a simple question: During the next 12-months, will the Federal Reserve move interest rates by more or less than what is currently priced into the market? Chart 1The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

The (US) Golden Rule Of Bond Investing In Practice

Ryan argued that a predictive framework for US Treasury returns built around the answer to this question has historically worked so well that it should be referred to as the “Golden Rule of bond investing” (Chart 1). In a follow-up report, our Global Fixed Income Strategy service confirmed that the Golden Rule also largely works in non-US developed market economies, with the exception of Japan due to the absence of any meaningful fluctuation in policy rates over the past two decades.2 The Golden Rule provides a very strong framework to aid fixed-income investors with their cyclical (i.e. 6-12 month) asset allocation decisions, by quantitatively linking government bond returns relative to cash – in other words, the excess return earned by taking duration risk - to policy rate “surprises” compared to what is discounted in shorter-term money markets. The practical application is that a decision to allocate to longer-maturity government bonds is reduced to a bet on whether a central bank will adjust policy rates by more or less than the market expects. The first question we address in this report is to what degree does the Golden Rule apply in China (in yield space rather than in return space), along with an explanation of any differences that may exist. However, we must first note why the Golden Rule of bond investing works, particularly in the US. The first reason is that there is a strong relationship between the US 3-month T-bill rate and Treasury yields of all other maturities. Conceptually, all fixed income investors have a choice when buying US government bonds: they can purchase a 3-month Treasury bill and simply perpetually roll over the position as it matures, or they can purchase a Treasury bond of a longer maturity. This means that yields on longer maturity Treasury bonds simply reflect investor expectations for the average 3-month T-bill rate over the life of the bond, plus some positive risk premium to compensate for the inherent uncertainty of the path and tendency of short-term yields. This helps explain the close link between cyclical changes in 3-month T-bill rates and yields on longer maturity Treasurys. Chart 2In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

In The US, The 3-Month T-Bill Rate Perfectly Tracks The Fed Funds Rate

The second reason for the Golden Rule’s success is that there is a very tight relationship between the effective Fed funds rate and the 3-month T-bill rate. While it is the (higher) discount rate that is the theoretical no-arbitrage ceiling for the 3-month rate, in practice T-bill rates trade extremely close to the Fed funds rate (Chart 2). This means that Fed funds rate “surprises” (relative to traded market expectations) are akin to surprises in the 3-month rate, which in turn strongly influence the expected future path of short-term interest rates and thus yields on longer maturity Treasurys. In China, we noted in a February 2018 Special Report3 that the 7-day interbank repo rate is now the de jure short-term policy rate in China following the establishment of an interest rate corridor system in 2015. Chart 3 presents our first test of the Golden Rule in China (in yield space rather than in return space), by plotting the annual change in the level of Chinese government bond yields alongside the 7-day repo rate “surprise” over the past year from 2010 to the present. Here, we use the first principal component of zero coupon Chinese government bond yields to represent the average level of yields (rather than selecting a particular maturity), and we use the 12-month RMB swap rate (versus 7-day repo) to represent market expectations for the policy rate. The chart highlights that the fit is good, as measured by a 50% R-squared between the two series. However, deviations in the relationship do exist, with the most notable exception having occurred in 2017: Chinese government bond yields rose considerably more than what the annual surprise in the 7-day repo rate would have suggested. Chart 3In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

In China, The Golden Rule Works Decently Well Using 7-Day Repo...

Chart 4...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

...And Extremely Well Using 3-Month SHIBOR

Chart 4 helps resolve a good portion of the 2017 discrepancy, and clarifies the link between Chinese monetary policy and government bond yields. Chart 4 is similar to Chart 3, except that it replaces the 7-day repo rate surprise with that of 3-month SHIBOR (which trades very closely to the 3-month repo rate). The chart illustrates an even closer fit between the two series (with an R-squared close to 80%), and shows that the 3-month SHIBOR surprise does a meaningfully better job at explaining the 2017 rise in Chinese government bond yields. The Golden Rule of bond investing works surprisingly well in China. The fact that the annual surprise in 3-month SHIBOR has done a better job at predicting changes in bond yields over the past decade underscores that the 3-month repo rate is the de facto short-term policy rate in China, a point that we have made in several previous reports. We have noted that the spike in the 3-month/7-day repo rate spread that occurred in late-2016 and lasted until mid-2018 happened because of China’s crackdown on shadow banking activity. This crackdown caused a funding squeeze for China’s small & medium banks, which caused a material rise in lending rates and government bond yields. This episode highlights that future changes in the 3-month repo rate are likely to reflect both underlying changes in net liquidity provided to large commercial banks (measured by the 7-day repo rate), and any dislocations in the interbank market that have the potential to push up lending rates and government bond yields. Bottom Line: BCA’s “Golden Rule” framework, which links developed economy government bond returns to central bank policy rate “surprises” versus market expectations, works for China as well – using the correct measure of the PBOC policy rate. This provides a useful investment framework for Chinese government bonds, which are now significant part of major global bond market benchmarks. The Cyclical Outlook For Chinese Government Bond Yields Given the establishment of the relationship between Chinese short-term interbank rates and government bond yields detailed above, we are now able to more precisely discuss the likely cyclical trajectory of Chinese government bond yields as a function of Chinese monetary policy. Two opposing forces have the potential to affect China’s government bond market this year. The first, a stabilization and modest rebound in Chinese economic activity, may exert upward pressure on yields due to expectations of eventual policy tightening. The second, continued attempts by the PBoC to ease corporate lending rates, may exert downward pressure on yields as it will reflect not just easy but easier monetary conditions. Yields at the long-end are likely to move modestly higher this year, at most. For investors, the raises the obvious question of whether Chinese government bond yields are likely to move up, down, or trend sideways this year. In our view, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. Yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. There are two reasons why yields at the short-end of China’s government bond curve are likely to stay flat for most of this year. The first is that the PBoC is generally a reactive central bank and has historically lagged a pickup in economic activity, as illustrated in Chart 5. The chart shows the historical path of 3-month SHIBOR in the year following a bottom in economic activity in 2009, 2012, and 2015, and makes it clear that there has been no precedent for a significant rise in interbank rates in the first nine months of an economic recovery. The 2012 episode did see a very sharp rise in 3-month SHIBOR once the PBoC shifted into tightening mode, but we doubt that this experience will be repeated again unless economic growth accelerates much more aggressively than we expect. The second reason why we expect yields at the short-end of the curve to remain muted this year is because any additional easing by the PBoC is likely to be focused on reducing corporate lending rates, not interbank rates. Chart 6 highlights that while there is a strong correlation between changes in Chinese government bond yields and average lending rates in the economy, the former leads the latter. In the past, this relationship has existed because changes in interbank rates have coincided with reductions in the now obsolete benchmark lending rate, with the former usually occurring earlier than the latter. But in a scenario where the PBoC reduces the loan prime rate (LPR) and keeps net banking sector liquidity roughly constant, the extremely tight relationship shown in Chart 4 suggests that short-term bond yields are unlikely to be affected by a reduction in lending rates. Any meaningful decline in short-term yields below short-term interbank rates would simply prompt banks to stop buying these bonds. Chart 5The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

The PBoC Is Generally A Reactive Central Bank

Chart 6Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Average Lending Rates Lag Short-Term Bond Yields

Chart 7China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

China's Yield Curve Is Generally Pro-Cyclical

Additional easing by the PBoC does have the potential to impact the long-end of the government bond curve if investors view these actions as a sign that interbank rates will remain low for some time. This view is reinforced by the fact that China’s yield curve is not particularly flat, and thus has room to move lower. However, Chart 7 also shows that China’s yield curve, defined here as the second principal component of zero coupon Chinese government bond yields, is positively correlated with the relative performance of investable Chinese equities. This suggests that there is a procyclical element to the curve. We suspect that this procyclical element will dominate a potential decline in expectations for future short-term interest rates, but that yields at the long-end are likely to move modestly higher this year, at most. Bottom Line: Any additional easing by the PBoC this year is likely to be focused on reducing lending rates to the real economy, not interbank rates (which drive government bond yields). As such, yields at the short-end are likely to be flat until later this year at the earliest, whereas yields at the long-end are likely to move modestly higher, at most. The Secular Outlook For Chinese Government Bond Yields A common approach to forecasting the likely structural trend for nominal government bond yields is to estimate the trajectory of real long-term potential output growth and to add the monetary authority’s inflation target. This framework is based on the idea that interest rates are in equilibrium when the cost of borrowing is roughly equal to nominal income growth, a condition that results in no change in the burden to service existing debt. Chart 8China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

China's Potential Growth Is Likely To Trend Lower...

Based on this framework, we would expect Chinese government bond yields to trend down over time, or possibly flat if the PBoC were to tolerate higher inflation over the coming decade. Chart 8 illustrates the IMF’s forecast of falling real potential growth in China over the coming several years, which is consistent with a shift in the composition of growth from investment to consumption as well as China’s looming demographic crisis. But Chart 9highlights an obvious problem with applying this framework to forecast the secular trend in Chinese government bond yields: over the past decade, yields have persistently averaged below actual nominal GDP growth, both in China and in the developed world. In the latter case, it is an open question whether this will continue to be true in the future, but in China’s case it is clear that government bond yields have little connection (in magnitude) to the pace of GDP growth. This reflects the longstanding strategy of Chinese policymakers to promote investment via persistently low interest rates, as has occurred in other manufacturing and export-oriented Asian economies (Chart 10). Chart 9...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

...But Bond Yields Are Well Below GDP Growth, Just Like In Developed Markets

Chart 10In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

In Industrial Asian Economies, Low Bond Yields Are A Policy Choice

The persistent historical gap between economic growth and bond yields in China makes it difficult to forecast the structural outlook for yields using conventional methods, and largely limits us to inference. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, bond yields are more likely to rise than fall over time. This is because as long as interest rates remain well below the pace of income growth, the incentive to excessively borrow (and invest) is likely to persist. Chart 11China Needs Higher Interest Rates, But Only To A Point

China Needs Higher Interest Rates, But Only To A Point

China Needs Higher Interest Rates, But Only To A Point

However, even in a scenario where Chinese government bond yields structurally trend higher, we expect the rise to be modest. Chart 11 highlights that China’s “private sector” debt service ratio is extremely elevated, underscoring that the country’s ability to tolerate significantly higher bond yields is not strong. In addition, since 2015, China’s debt service ratio has been mostly flat despite rising a rising debt-to-GDP ratio, which has been achieved through lower short-term interest rates. To the extent that policymakers fail to make meaningful progress in shifting China’s growth drivers away from investment over the coming few years, lower (potentially sharply lower) bond yields would appear to be all but inevitable to cope with what would become a permanently growing drag on economic activity from the servicing of debt. For now, we would characterize this scenario as a risk to our base case view, but it is a risk that we will be closely monitoring over the coming years. Bottom Line: The persistent gap between Chinese nominal GDP growth and government bond yields is likely contributing to the problem of excessive leveraging. To the extent that Chinese policymakers succeed at shifting the drivers of growth from investment to consumption, bond yields are more likely to structurally rise than fall. Investment Conclusions Our analysis above points to four recommendations for investors over the coming year: Overweight Chinese stocks versus Chinese government bonds in RMB and USD terms Overweight Chinese onshore corporate bonds versus duration-matched Chinese government bonds in RMB terms Overweight 7-10 year USD-hedged Chinese government bonds versus their US and developed market (DM) counterparts For offshore US dollar-based investors, long 7-10 year Chinese government bonds in unhedged terms Regarding the first two recommendations, our view that yields are likely to be flat at the short-end and modestly higher at the long-end suggests that investors can expect total returns on the order of 2-3% from Chinese government bonds this year. Barring a major and lasting economic slowdown from the 2019-nCoV outbreak, we expect Chinese domestic and investable equities to outperform government securities over the coming 6-12 months. Onshore corporate bonds have a similar outlook: onshore spreads are pricing in (massively) higher default losses than we believe is warranted, meaning that they will outperform duration-matched government equivalents without any changes in yield. Chart 12Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Within Global Fixed-Income, Hedged Chinese 10-Year Yields Are Relatively Attractive

Chart 13Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

Unhedged Yield Spreads Predict Hedged Relative Performance Versus The US

For global fixed-income investors, Charts 12-14 present USD-hedged 10-year Chinese government yields versus the US and DM/DM ex-US, along with the historical relative return profile of USD-hedged Chinese bonds versus hedged and unhedged returns. In hedged space, Chinese 10-year government bond yields are modestly attractive: 2.2% versus 1.6% in the US and 1.8% in DM ex-US. China’s historically low yield beta to the overall level of global 10-year bond yields (Chart 15) suggests that Chinese yields should perform well in 2020 – a year where we expect global bond yields to drift higher as economic growth rebounds. Combined with relatively attractive valuation, this bodes well for the relative performance of Chinese debt versus DM equivalents. A low yield beta against a backdrop of drifting higher global yields implies that longer-maturity Chinese government bonds will outperform their DM equivalents. Chart 14Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Unhedged Yield Spreads Predict Hedged Relative Performance Versus DM

Chart 15China's Yield Beta Has Been Rising, But Is Still Japan-Like

China's Yield Beta Has Been Rising, But Is Still Japan-Like

China's Yield Beta Has Been Rising, But Is Still Japan-Like

We would also recommend longer-maturity Chinese government bonds in unhedged terms versus a USD-hedged global government bond portfolio. Chart 16 highlights that the relative return of this trade is strongly (negatively) linked to USD-CNY, and we expect further (albeit more modest) gains in RMB over the cyclical horizon. Chart 16Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

Modest Further RMB Upside Means Unhedged Chinese Bonds Will Outperform

As a final point, investors should note that today’s report is part of a heightened focus on China’s fixed income market, in terms of both forecasting fixed income returns and analyzing the cyclical and structural implications of the increasing investability of China’s financial markets. More research on this topic is likely to come in 2020 and beyond: Stay Tuned! Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 Please see US Bond Strategy Special Report "The Golden Rule Of Bond Investing," dated July 24, 2018, available at usbs.bcaresearch.com 2 Please see Global Fixed Income Strategy Special Report "The Global Golden Rule Of Bond Investing," dated September 25, 2018, available at gfis.bcaresearch.com 3 Please see China Investment Strategy Special Report "Seven Questions About Chinese Monetary Policy," dated February 22, 2018, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

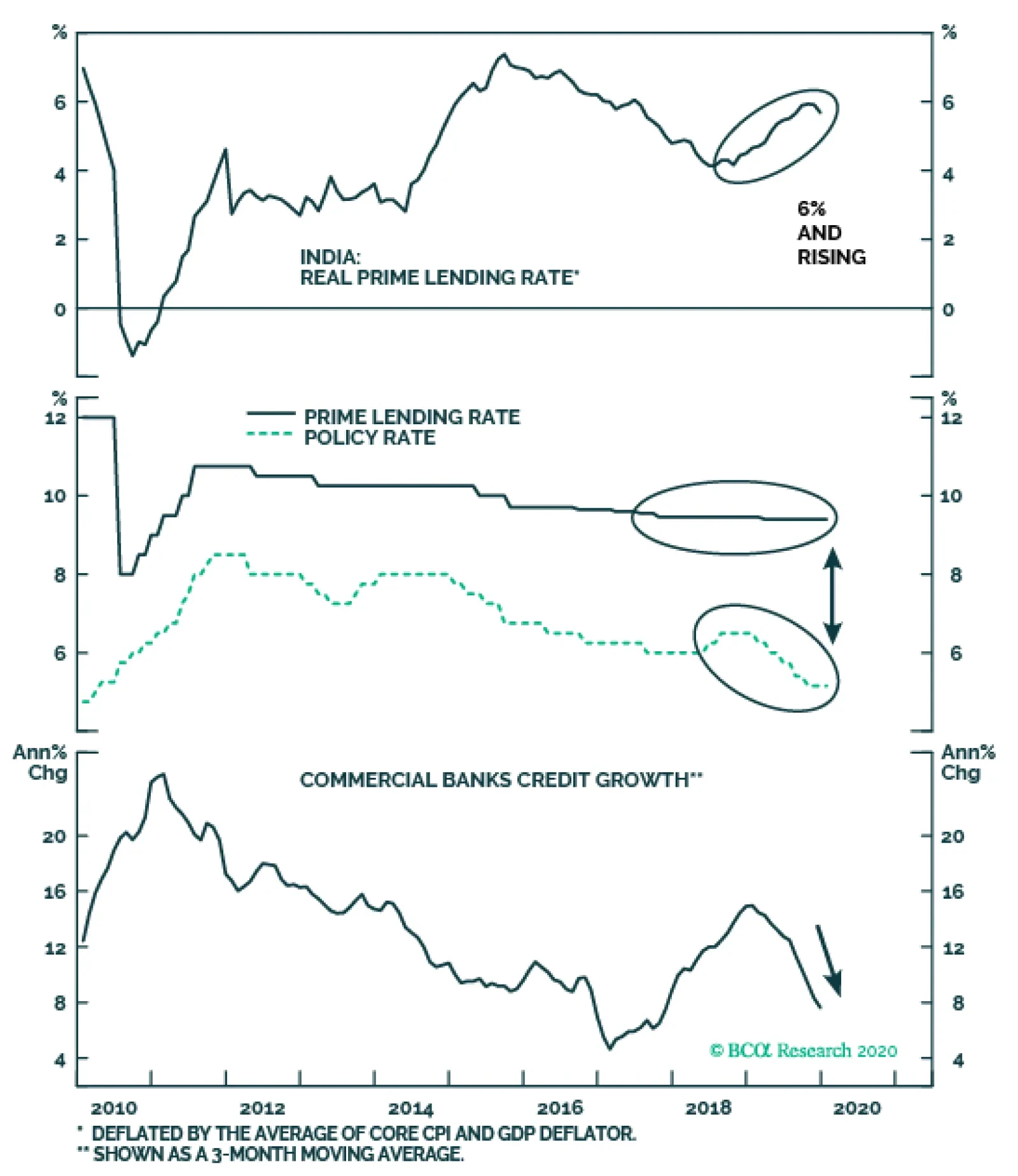

The entire Indian economy is suffering from high real borrowing costs. The monetary policy transmission mechanism has not been working effectively in India. Even though the central bank has cut its policy rate by 135 basis points in 2019, the prime lending…

Highlights Most central banks still consider economic risks asymmetrical to the downside. This means that even if global growth rebounds in earnest, policy is likely to stay pat over the next three to six months. The conclusion is that relative growth fundamentals rather than central bank policy will likely drive FX price action in the next few months. Our bias remains that the growth impulse will be strongest outside the US during the first half of this year. Stay short the DXY index. The BoJ’s inaction this week makes long yen bets cheap insurance against a rise in FX volatility. Remain short USD/JPY and go short CHF/JPY. The pound remains a buy on dips but will likely underperform the euro over the next few months. EUR/GBP should touch 0.88. The BoC kept rates on hold, but erred on the dovish side, in line with our expectations. Stay short CAD/NOK and long AUD/CAD. We were stopped out of our long NOK/SEK trade for a profit of 1.8%. We will look to rebuy the cross at lower levels. Feature Chart I-1Currency Markets Have Priced In A Benign Recovery

Currency Markets Have Priced In A Benign Recovery

Currency Markets Have Priced In A Benign Recovery

The powerful bounce in global equity markets since the August lows has pushed many stock indices into overbought territory. Chart I-1 shows that the rise in global stocks has already discounted an improvement in global manufacturing in order of magnitude similar to the 2012 and 2016 episodes. However, currency markets have been discounting a much more benign outcome (bottom panel). The divergence between currency and equity performance is a marked change from what has prevailed during past cycles. For example, trough to peak, AUD/JPY, a key barometer of greed versus fear in currency markets, appreciated 40% during the 2012 episode, and 25% in 2016-2017, along with rising equity prices. The performance of even more high-octane currency pairs such as the RUB/JPY, the ZAR/JPY, or even the BRL/JPY, was explosive. More muted currency action this time around therefore calls into question the durability of this recovery. Perhaps given that equities are long-duration assets, it is quite plausible that the drop in interest rates in 2019 has increased their relative appeal, boosting nominal values. While that makes sense, most bond markets have also seen higher yields over the past few months, making this explanation questionable. Alternatively, the easing in trade tensions and/or the Federal Reserve’s liquidity injections may have rekindled animal spirits among domestic investors. Or perhaps, a synchronized recovery has narrowed G10 growth differentials, muting currency performance in the process but boosting share prices. The rise in global stocks has already discounted an improvement in global manufacturing. However, currency markets have been discounting a much more benign outcome. Either way, the resolution to this dissonance will be either through marked improvement in global economic data in the coming months (which will support pro-cyclical currencies), or a period of indigestion for stock markets (which will lift volatility) – or a combination of both. At a minimum, this suggests tweaking currency portfolios in anticipation of these dynamics. On Volatility And The Dollar Everyone understands that currency markets are about relative trends. Therefore, the implicit assumption that the dollar will weaken as global growth picks up is that the epicenter of this recovery will be outside the US. Chart I-2 shows that economic data is not yet surprising to the upside outside the US, even though there has been marked improvement on a rate-of-change basis. Beneath the surface, the strongest data surprises have been in the euro area, Switzerland, New Zealand and Australia, while disappointments have been in Canada and the UK. In hindsight, the chart also highlights why the Canadian dollar was the best performing G10 currency in 2019, while the Swedish krona was the weakest. Chart I-2Growth Dispersion Has Fallen

Growth Dispersion Has Fallen

Growth Dispersion Has Fallen

The drop in economic dispersion has pushed currency volatility near record lows (Chart I-3). Every seasoned investor does and should pay attention to low volatility. This is because what destroys portfolios is not exuberance, but complacency. This might sound like a tautology, but during the last three episodes of volatility dropping to these levels, the dollar soared and pro-cyclical currencies suffered severe losses. Everyone remembers 1997-1998, 2007-2008 and 2014-2015. Will this time be the same? While a rise in volatility is usually associated with a higher dollar, there are three key differences this time around. First, real rates turned positive in the US relative to its G10 counterparts in 2014 (Chart I-4). This meant the US dollar, which has typically been a funding currency (not least because it is a reserve currency), became the object of carry trades. It is a fair contention that any capital that wanted to find its way into US Treasurys has had more than five years of positive real carry to do so. With real relative yields in the US now rolling over, which way will capital gravitate? Chart I-3Volatility Near Record Lows

Volatility Near Record Lows

Volatility Near Record Lows

Chart I-4Real Rates Lower In The US

Real Rates Lower In The US

Real Rates Lower In The US

The dollar has been in a bull market since 2011, which has shifted valuations towards expensive quartiles. This is a key difference from previous low-volatility episodes when the dollar was much earlier into bull-market territory (Chart I-5). The dollar tends to run in long cycles, and a spike in volatility can either mark the beginning or the end of a cycle. As we have emphasized numerous times in previous reports, being long the US dollar is a consensus trade. Our primary basis for this is CFTC positioning data. However, a timelier leading indicator to watch is the gold-to-bond ratio. Currencies are about confidence, and a key measure of confidence in the US dollar is the total return in the US 10-year Treasury compared to gold bullion, which has collapsed (Chart I-6). The budget deficit in the US is about to explode, while it was low and falling during prior dollar riot points. Chart I-5The Dollar Is Expensive

The Dollar Is Expensive

The Dollar Is Expensive

Chart I-6Tug Of War Between US Bonds And Gold

Tug Of War Between US Bonds And Gold

Tug Of War Between US Bonds And Gold

More importantly, currency markets are likely to gyrate with relative fundamentals. The slowdown in the global economy was driven by the manufacturing sector, so it is fair to assume that this is the part of the economy that is ripe for mean reversion. Historically, cyclical swings in most economies tend to be driven by manufacturing and exports rather than services (and consumption). More specifically, the currencies that have borne the brunt of the manufacturing slowdown should logically be the ones to experience the quickest reversals. This is already being manifested in a very steep rise in their bond yields vis-à-vis those in the US. For example, yields in Norway, Sweden, Switzerland and Japan have risen significantly versus those in the US since the bottom. A synchronized recovery in global growth will go a long way in further eroding the US’ yield advantage. Currencies are about confidence, and a key measure of confidence in the US dollar is the total return in the US 10-year Treasury compared to gold bullion. Bottom Line: Remain short the DXY index with an initial target of 90 and a stop loss at 100. The Yen As Portfolio Insurance Should our thesis that the dollar is in a downtrend for 2020 be correct, it is unlikely to occur in a straight line. This argues for having some portfolio insurance. The Bank of Japan’s inaction this week may have been a red herring, since one of the most potent moves in asset markets in recent months has been the +130-basis-point move in favor of Japanese yields (Chart I-7). The gap between the USD/JPY and real rates has opened up a rare arbitrage opportunity. Should a selloff in global risk assets materialize, the yen will strengthen. On the other hand, if global growth does eventually accelerate, the yen could weaken on its crosses but strengthen vis-à-vis the dollar. This keeps short USD/JPY bets in an enviable “heads I win, tails I do not lose too much” position. The rise in Japanese yields has been driven by three key pivotal developments: For most of the past five years, the BoJ was one of the most aggressive central banks in terms of asset purchases. This was a huge catalyst for a downturn in the trade-weighted yen (Chart I-8). With a renewed expansion in the Fed’s balance sheet, monetary policy is tightening on a relative basis in Japan. Total annual asset purchases by the BoJ are currently running at about ¥20 trillion, while JGB purchases are running at ¥15 trillion. This is a far cry from the central bank’s soft target of ¥80 trillion, and unlikely to change anytime soon. Chart I-7Japanese Bond Yields Have Surged

Japanese Bond Yields Have Surged

Japanese Bond Yields Have Surged

Chart I-8The Yen And QE

The Yen And QE

The Yen And QE

Movements in the yen are as influenced by external conditions as what is happening domestically, given Japan’s huge export sector. Credit default swap spreads of cyclical sectors are collapsing to new lows, symptomatic of an improving profit outlook (Chart I-9). This suggests it is the growth component driving Japanese yields higher (Japanese CPI swaps have indeed been flat). This also mirrors the recent outperformance of Asian cyclical sectors relative to defensive ones. The Abe government announced a huge fiscal package last year, in part driven by the disastrous typhoons as well as the upcoming Olympics. This allowed the BoJ to upgrade its growth forecasts in its latest policy minutes. The relative performance of construction and engineering stocks are an important barometer for when the funds are flowing into the economy (Chart I-10). Chart I-9Default Risk Easing In Japan

Default Risk Easing In Japan

Default Risk Easing In Japan

Chart I-10Fiscal Stimulus And Construction Stocks

Fiscal Stimulus And Construction Stocks

Fiscal Stimulus And Construction Stocks

As a defensive currency, the yen tends to weaken as global growth improves, given it is usually used to fund carry trades. That said, our contention is that the yen will surely weaken at the crosses, but could still strengthen versus the dollar. As mentioned above, one catalyst is the divergence from the traditional relationship with real rates. More importantly, the USD/JPY and the DXY tend to have a positive correlation, because the dollar drives the yen most of the time. Meanwhile, net short positioning in the yen versus the dollar makes it attractive from a contrarian standpoint (Chart I-11). Given extremely low volatility, this places short USD/JPY bets as an attractive vehicle to play a rise in volatility. Chart I-11Investors Are Short The Yen

Investors Are Short The Yen

Investors Are Short The Yen

More conservative investors could go short CHF/JPY. The recent rise in the Swiss franc threatens the nascent recovery in inflation (Chart I-12), while weakness in the Japanese yen will help lift domestic tradeable goods prices. This puts more pressure on the Swiss National Bank rather than the BoJ. Meanwhile, as a safe haven, the yen is cheaper than the franc. This is confirmed by many of our in-house models. In simple terms, relative inflation with the US has been lower in Japan over the last several decades, but the franc has been stronger. In simple terms, relative inflation with the US has been lower in Japan over the last several decades, but the franc has been stronger (Chart I-13). Meanwhile, over the last two years, a rise in volatility has benefited the yen more than the franc. Chart I-12Strong Franc Is A Headwind For Swiss Inflation

Strong Franc Is A Headwind For Swiss Inflation

Strong Franc Is A Headwind For Swiss Inflation

Chart I-13The Yen Is Cheaper ##br##Insurance

The Yen Is Cheaper Insurance

The Yen Is Cheaper Insurance

Bottom Line: The yen is the most attractive safe-haven currency at the moment. Remain short USD/JPY and sell CHF/JPY. Housekeeping We were stopped out of our long NOK/SEK trade for a profit of 1.8%. We will look to rebuy this cross at lower levels. The trade is mostly about carry, and we are both positive on the NOK and SEK. This makes market timing important. NOK/SEK at 1.04 will be attractive. There were no new insights from the Norges bank this week, in the context of all the central bank meetings. We will also be looking to opportunistically buy the pound, but buying EUR or GBP volatility might be a better bet. For now, despite the robust labor report, economic surprises in the UK remain negative (Chart I-14). Stay tuned. Chart I-14GBP Is Vulnerable

GBP Is Vulnerable

GBP Is Vulnerable

Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been mixed: Industrial production fell by 1% year-on-year in December. The preliminary Michigan consumer sentiment index fell slightly to 99.1 in January. MBA mortgage applications fell by 1.2% for the week ended January 17th. However, existing home sales surprised to the upside, rising 3.6% month-on-month in December. Chicago Fed national activity index fell to -0.35 from 0.41 in December. Initial jobless claims increased to 211K for the week ended January 17th, better than expectations. The DXY index increased by 0.4% this week. There are growing concerns over whether China's coronavirus would significantly drag down global growth. While this is a hiccup in the short term, we remain positive and believe that global growth will accelerate this year on easy financial conditions and faded trade war risks. Report Links: On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been mostly positive: The current account balance came in at €33.9 billion in November. Headline and core inflation were both unchanged at 1.3% year-on-year respectively in December. The ZEW economic sentiment survey soared to 25.6 from 11.2 in January. The euro fell by 0.8% against the US dollar this week. On Thursday, the ECB maintained interest rates at -0.5%. The key takeaway from the ECB is that they are grappling with a review of their monetary policy objective in a manner that might increase accommodation. A switch to an explicit 2% inflation target and/or including a climate change objective into quantitative easing decisions heralds a much more dovish ECB. We are tightening our stop on long EUR/CAD to 1.42. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 On Money Velocity, EUR/USD And Silver - October 11, 2019 A Few Trade Ideas - Sept. 27, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: Industrial production fell by 8.2% year-on-year in November. The trade deficit widened to ¥152.5 billion in December. Imports and exports both fell by 4.9% and 6.3% year-on-year, respectively. All industry activity index increased by 0.9% month-on-month in November. Both the coincident index and the leading economic index fell to 94.7 and 90.8, respectively in November. The Japanese yen appreciated by 0.3% against the US dollar this week. The BoJ kept interest rates unchanged, in line with expectations. More importantly, the outlook report revised the growth forecast upward to 0.9% from 0.7% for the fiscal year 2020. Moreover, the BoJ revised down the inflation forecast by 10 bps due to lower crude oil prices. Please refer to our front section this week for a more in-depth analysis on the Japanese yen. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Signposts For A Reversal In The Dollar Bull Market - November 1, 2019 A Few Trade Ideas - Sept. 27, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the UK have been positive: Retail sales grew by 0.9% year-on-year in December. The Rightmove house price index increased by 2.7% year-on-year in January. The ILO unemployment rate was unchanged at 3.8% in November. Average earnings grew by 3.2% year-on-year in November. This followed a 3-month improvement in employment of 208K, after what had been a dismal employment report for most of 2019. The British pound appreciated by 0.7% against the US dollar this week. The biggest volatility in European currencies in the next few weeks is likely to emerge in the EUR/GBP cross. European economic data has had the best positive surprises in the last few weeks, in part due to base effects. However, the ECB’s transcript this week suggests leaning against any currency strength. In the UK, the pound will still trade partly on politics for now. Buying GBP and EUR volatility looks like a good bet. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 A Few Trade Ideas - Sept. 27, 2019 United Kingdom: Cyclical Slowdown Or Structural Malaise? - Sept. 20, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been positive: The Westpac consumer confidence index fell by 1.8% in January. Consumer inflation expectations increased to 4.7% from 4% in January. 28.9K new jobs were created in December, above consensus. This was a combination of 29.2K part-time jobs but a loss of 0.3K full-time jobs. The participation rate was unchanged at 66% in December, while the unemployment rate fell further to 5.1%. The Australian dollar fell by 0.6% against the US dollar this week. The positive jobs report placed a bid under AUD, but that quickly dissipated as the coronavirus scare started to dominate headlines. We discussed AUD in depth last week and are buyers at 68 cents. Our primary rationale is that this is a potent contrarian bet. Report Links: On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Visitor arrivals fell by 3.5% year-on-year in November. Net migration fell to 2610 from 3400 in November. The performance services index fell to 51.9 from 52.9 in December. The New Zealand dollar fell by 0.5% against the US dollar this week. While we believe that the kiwi dollar will outperform the US dollar this year amid improving global growth, domestic constraints including decreasing net migration might limit upside potential. Stay long AUD/NZD and SEK/NZD. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 USD/CNY And Market Turbulence - August 9, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been soft: Manufacturing sales fell by 0.6% month-on-month in November. Headline inflation was unchanged at 2.2% year-on-year in December. Core inflation however, fell to 1.7% from 1.9% in December. New house prices grew by 0.1% year-on-year in December. The Canadian dollar fell by 0.8% against the US dollar this week. On Wednesday, the BoC decided to put interest rates on hold, while opening the door for possible rate cuts later this year if the Canadian data disappointed. In short, like most other central banks, the BoC is data dependent. Our story for CAD is simple – if the epicenter of a growth rebound is outside the US, CAD will underperform its antipodean counterparts. Stay long AUD/CAD. Report Links: The Loonie: Upside Versus The Dollar, But Downside At The Crosses Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

There have been scant data from Switzerland this week: Producer prices fell by 1.7% year-on-year in December, compared with a decrease of 2.5% the previous month. Money supply (M3) grew by 0.7% year-on-year in December. The Swiss franc has been more or less flat against the US dollar this week. We continue to favor the Swiss franc as global risks persist, including concerns about the coronavirus. However, as discussed in the front section of this report, the yen is a better hedge than the franc at the current juncture. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Notes On The SNB - October 4, 2019 What To Do About The Swiss Franc? - May 17, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There was scant data out of Norway this week: The Labor Force Survey recorded an increase in the unemployment rate to 4% in November. The Norwegian krone fell by 1.3% against the US dollar this week amid lower energy prices. On Thursday, the Norges Bank kept interest rates on hold at 1.5%, as widely expected. Moreover, the Bank Governor Øystein Olsen said that "The Committee’s current assessment of the outlook and the balance of risks suggests that the policy rate will most likely remain at the present level in the coming period," implying no change in the policy rate in the near-term. This suggests that going forward, relative fundamentals rather than policy decisions will dictate NOK’s path. Our bias is that a valuation cushion offers a margin of safety for long NOK positions. Remain short USD/NOK and CAD/NOK. Report Links: On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

There was scant data out of Sweden this week: After rising from 6% to 6.8% in November, the unemployment rate fell back to 6% in December. The Swedish krona fell by 0.2% against the US dollar this week. Going forward, improving global growth, diminished trade tensions, and fewer concerns about a near-term recession all underpin the Swedish economy and the krona. SEK is the most potent G10 cross to play a global manufacturing rebound. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Today, the major development of the ECB’s policy meeting was the announcement of the new monetary strategy policy review. Following the press conference where the program was announced, the euro fell 0.6% and bunds outperformed Treasury Notes. The policy…

As expected, the BoC kept interest rates at 1.75%. While the BoC highlighted that the economy possesses more slack than originally estimated, it refrained from committing policy to any path this year. After all, while the Canadian economy continues to suffer…

As tensions from the US-China trade war abate, investors are starting to refocus on economic fundamentals. This year, Chinese policymakers will maintain their tight grip on local government spending and bank lending, and will continue to fine-tune policies…

Highlights The recently signed Phase One deal is positive for China and global equity markets as it brings a temporary truce to the trade war. However, China is unlikely to change its current policy trajectory to create additional domestic demand to consume $200 billion in new imports from the US. China is likely to meet the commitment only half way in the next two years, and meet the 2020 import target from the US by a redistribution of its purchases overseas. The RMB will modestly appreciate in the next three to six months. On the monetary policy front, there is no sign of further monetary easing from the PBoC. We continue to recommend an overweight stance towards Chinese stocks in the next six months, relative to the global benchmark. Feature Economic data released last week, including Q4 GDP growth, December industrial production, fixed-asset investment and trade data, all suggest that the Chinese economy bottomed before the end of 2019. The Phase One trade deal between China and the US marks a significant de-escalation in a two-year trade war. The RMB appreciated by 1.4% against the greenback since the beginning of the year, pushing USD-CNY firmly below the key psychological 7 mark. The performance of equities in China’s onshore and offshore markets confirms that the economy has bottomed. Since December 11, 2019, Chinese cyclical sectors have outperformed defensives and both the investable and domestic markets have broken above their respective 200-day moving averages versus global stocks (Chart 1A and 1B). Chart 1ABoth Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Chart 1BCyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

We continue to recommend a cyclical long stance on Chinese stocks. We expect pro-growth policy support to accelerate in the first quarter, economic recovery to further solidify, and the Phase One trade deal to reduce economic and financial market volatility until the November 2020 US presidential election. All of these factors should support an outperformance in Chinese stocks relative to their global peers. Some Inconvenient Truth To The Truce China’s commitment to purchase an additional $200 billion in goods from the US was more than market participants anticipated. We do not think China will honor this commitment to its full extent. Moreover, we also do not think this will change China’s domestic economic policy trajectory for 2020. Details in Chapter 6 of the Phase One trade agreement titled “Expanding Trade”1 include: In the next 2 years, China is committed to purchase an additional $200 billion worth of goods and services from the US, from the 2017 baseline. The additional $200 billion amount is split over the next two years: China will need to add no less than $77 billion of imports from the US in 2020, and $123 billion in 2021. This amounts to a 41% increase in 2020 and a 66% increase in 2021, from the 2017 baseline of $186 billion (Chart 2). The text from Chapter 6 of the Phase One deal also specifies that, between January 2020 and December 2021, China will add a total of $77.7 billion in purchases of manufactured goods (including aircraft components), $32 billion in agricultural products, $52.4 billion in energy and $37.9 billion in services from the US (Chart 3). Chart 2Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Chart 3Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

China’s annual import growth from the US in 2017 was the highest one in the past ten years. If we assume that China will simply add $200 billion of new imports in the next two years from the US to this high starting point, it will need to boost domestic demand to accommodate at least a 4-6% increase in total imports in the next two years from 2019.2 In contrast, growth in China’s total imports in 2019 contracted by 3% from 2018, and averaged at only 2% in the last five years. In other words, in 2020 and 2021, even if China does not increase imports from other countries, just the commitment from purchases of US goods alone would require a sizable boost in China’s domestic demand. However, the assumption above is overly simplified and optimistic. Even though Chinese leadership may have shifted their policy priority from financial deleveraging to supporting economic growth this year, we do not think they will fully abandon the battle against systemic risks in the financial sector. Therefore, China is unlikely to significantly deviate from its current policy trajectory and stimulate aggressively to create additional domestic demand to consume the agreed $200 billion in new imports from the US. It is equally unlikely that China will absorb the $200 billion additional imports from the US, at the expense of its domestic production. A more plausible approach, which is our base case scenario, is that China will meet a large portion of the 2020 import target before November, to show good faith. After the US presidential election, China will face the challenge of either a re-escalation from the Phase Two trade talk with a re-elected President Trump, or a new US president with his/her own political agenda. In either case, at this point China is unlikely to have the intention to meet the import target for 2021. Chart 4China Likely To Shift Agro And Energy Import Suppliers To The US

Managing Expectations

Managing Expectations