Policy

An analysis on Ukraine is available below. Highlights A number of liquidity and technical reasons have led us to give benefit of the doubt to the bullish market action and chase this EM rally. We still doubt that the US-China trade truce alone is sufficient to propel a cyclical recovery in global trade and manufacturing. However, it seems the market is operating on a “buy now, ask questions later” principle. Therefore, we are initiating a long position in the EM equity index as of today. Despite the potential for higher EM share prices in absolute terms, we are still reluctant to upgrade EM versus DM stocks. The basis is that EM corporate profits will continue lagging those in DM. Feature We could be in for a replay of the 2012-2014 DM equity rally, where EM stocks rebounded in absolute terms but massively underperformed DM on a relative basis. Chart I-1EM Share Prices: In Absolute Terms And Relative To DM

EM Share Prices: In Absolute Terms And Relative To DM

EM Share Prices: In Absolute Terms And Relative To DM

EM share prices have spiked on the announcement of a trade truce between the US and China. As a result, our buy stop at 1075 on the EM MSCI Equity Index has been triggered, and we are initiating a long position in EM stocks as of today (Chart I-1, top panel). That said, we are still reluctant to upgrade EM versus DM stocks. Regardless of the direction of the market (bull, bear or sideways), EM share prices will likely underperform the global equity benchmark. As we discussed in our report, the primary risk to our view has been that EM share prices get pulled higher as a result of rallying DM markets. Nevertheless, our fundamental assessment remains that EM corporate profits will lag those in DM, heralding EM relative equity underperformance. In fact, we could be in a replay of the 2012-2014 DM equity rally where EM stocks massively underperformed (Chart I-1, bottom panel), as we elaborated in our November 28 report. In this report, we review the indicators that support a bullish stance, the ones that are inconclusive and those that are not confirming the current rally in China-plays in general and EM risk assets in particular. Bullish Liquidity And Technical Settings The following points have led us to give benefit of the doubt to recent market action and to chase this rally: The global liquidity backdrop appears to be conducive for higher share prices. Global narrow and broad money growth have accelerated (Chart I-2). That said, a caveat is in order: These money measures do not always strongly correlate with both global share prices and the global business cycle. There are numerous times when they gave a false signal or were too early or late at turning points. Chart I-2Global Narrow And Broad Money: A Useful But Not Always Reliable Indicator

Global Narrow And Broad Money: A Useful But Not Always Reliable Indicator

Global Narrow And Broad Money: A Useful But Not Always Reliable Indicator

The technical profile of EM equities is rather bullish. As shown on the top panel of Chart I-1 on page 1, EM share prices have found a support at their six-year moving average. When a market fails to break down below its long-term technical support line, odds are that a major bottom has been reached, and the path of the least resistance is up. The reason we look at these long-term (multi-year) moving averages is because they have historically worked very well for key markets like the S&P 500 and 10-year US Treasury bond yields (Chart I-3A & I-3B). Chart I-3AThe Reason Why We Use Multi-Year Moving Averages

The Reason Why We Use Multi-Year Moving Averages

The Reason Why We Use Multi-Year Moving Averages

Chart I-3BThe Reason Why We Use Multi-Year Moving Averages

The Reason Why We Use Multi-Year Moving Averages

The Reason Why We Use Multi-Year Moving Averages

As another positive development, both EM share prices in local currency terms and the EM equity total return index in US dollar terms have bounced from their three-year moving averages (Chart I-4). Chart I-4A Bullish Chart Formation For EM Equities

A Bullish Chart Formation For EM Equities

A Bullish Chart Formation For EM Equities

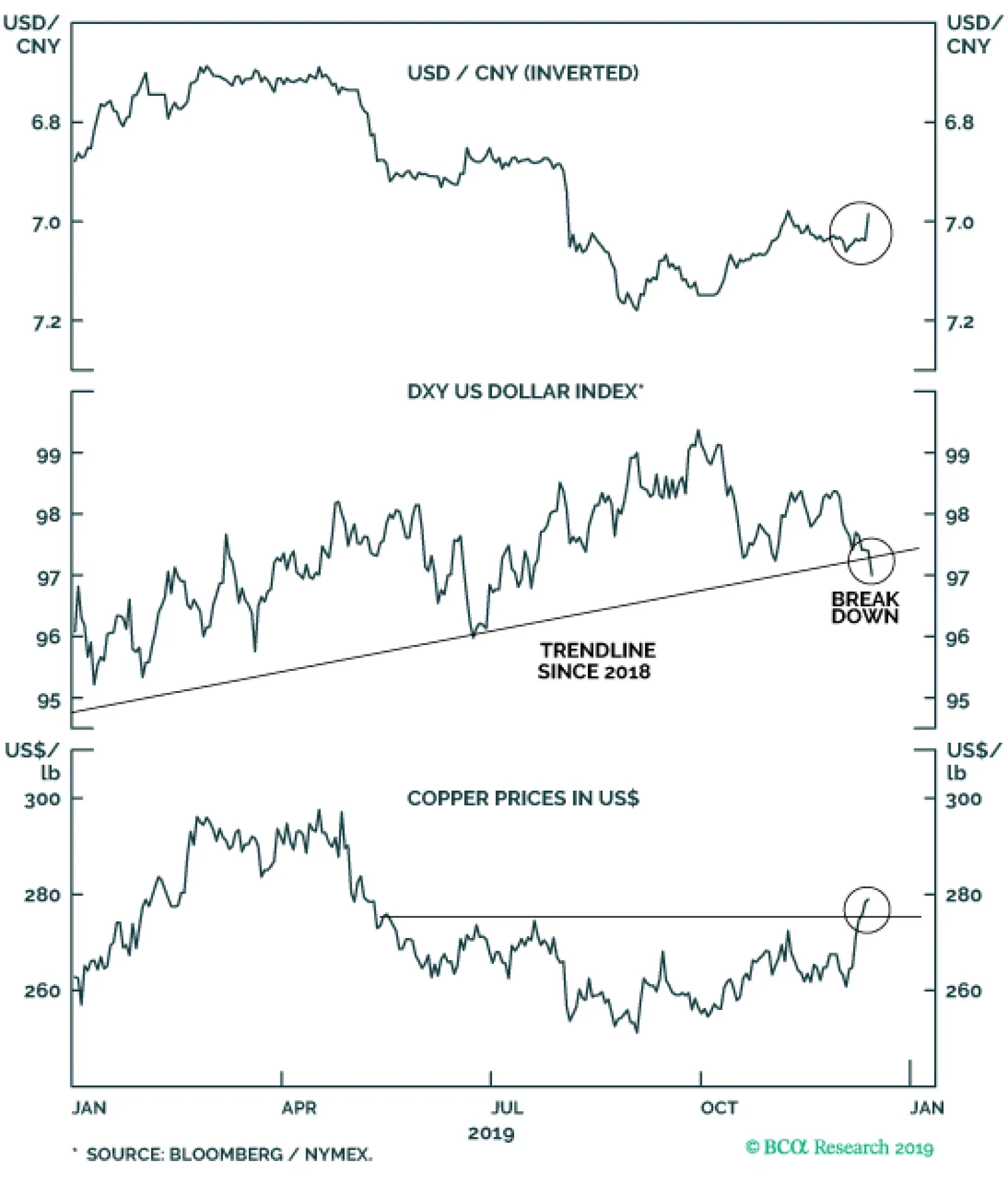

In addition, when a market does not drop below its previous top, this creates a bullish chart configuration (Chart I-4). This seems to be the case with EM share prices currently. Bottom Line: A number of liquidity and technical reasons have led us to give benefit of the doubt to the bullish market action and to chase this rally. Inconclusive Indicators It is rare that all types of indicators – directional market, business cycle, valuation and technical – all line up together to convey the same investment recommendation. Below we present the market indicators and signals that we have been watching to get confirmation of sustainability in the bull market in EM risk assets, commodities and global cyclical equity sectors. They are still inconclusive: The US broad trade-weighted dollar has recently sold off, but it has not broken down technically (Chart I-5). A decisive relapse below its 200-day moving average will signify that the greenback has entered a major bear market. The latter would be consistent with a sustainable and extended bull market in EM risk assets, commodities and global cyclical equity sectors. Chart I-5The US Dollar Has Fallen But Not Broken Down

The US Dollar Has Fallen But Not Broken Down

The US Dollar Has Fallen But Not Broken Down

Chart I-6Indecisive Signals From Commodities And Commodity Currencies

bca.ems_wr_2019_12_19_s1_c6

bca.ems_wr_2019_12_19_s1_c6

Even though copper prices have recently rebounded, they have not yet broken above their three-year moving average (Chart I-6, top panel). The latter can be viewed as the neckline of the head-and-shoulders pattern that has formed in recent years. The same holds true for the overall London Metals Exchange Industrial Metals Price Index, as well as our Risk-On/Safe-Haven currency ratio1 (Chart I-6, middle and bottom panels). Barring a decisive break above their three-year moving averages, the jury is still out on the durability of the rally in commodities prices and EM/China plays. Finally, global industrial share prices and US high-beta stocks have advanced to their 2018 highs, but have not yet broken out (Chart I-7). The same is true for the euro area aggregate stock index in local currency terms (Chart I-8). A decisive breakout above these levels will confirm that global equities in general and cyclical segments in particular are in an enduring bull market. Chart I-7Decisive Breakouts Here Are Needed To Confirm The EM Rally

Decisive Breakouts Here Are Needed To Confirm The EM Rally

Decisive Breakouts Here Are Needed To Confirm The EM Rally

Chart I-8European Share Prices Are At A Critical Juncture

European Share Prices Are At A Critical Juncture

European Share Prices Are At A Critical Juncture

Bottom Line: Several cyclical and high-beta segments of global financial markets are at a critical juncture. A decisive breakout from these key technical levels is required for us to uphold that EM risk assets and global cyclical plays are in a medium-term bull market. The Eye Of The Storm? There are a number of leading indicators and market signals that do not corroborate the common narrative of a sustainable improvement in global manufacturing/trade in general and China’s industrial cycle in particular: First, China’s narrow and broad money growth appear to be rolling over (Chart I-9). Notably, the money impulses lead the credit impulse, as illustrated in Chart I-10. Consequently, we expect the credit impulse – which is the main indicator currently portraying a revival in the Chinese economy as well as in the global business cycle – to roll over in early 2020. Chart I-9China: Narrow And Broad Money Growth Are Rolling Over

bca.ems_wr_2019_12_19_s1_c9

bca.ems_wr_2019_12_19_s1_c9

Chart I-10China: Money Impulses Are Coincident Or Lead Credit Impulse

bca.ems_wr_2019_12_19_s1_c10

bca.ems_wr_2019_12_19_s1_c10

This entails that the recent tentative improvements in China’s manufacturing, its imports and global trade will not be sustained going forward. Crucially, China’s narrow money (M1) growth point to the lack of a cyclical upturn in EM corporate profits in H1 2020 (Chart I-11). In short, EM listed companies’ profit growth rate stabilizing at around -10% is not a recovery. Second, government bond yields in both China and Korea are not corroborating a revival in their respective business cycles (Chart I-12). Chart I-11EM Corporate Profit Growth To Remain Negative In H1 2020

bca.ems_wr_2019_12_19_s1_c11

bca.ems_wr_2019_12_19_s1_c11

Chart I-12Asian Rates Are Not Confirming A Recovery

Asian Rates Are Not Confirming A Recovery

Asian Rates Are Not Confirming A Recovery

Chinese onshore interest rates have been a reliable compass for both its business cycle as well as EM share prices and currencies as we illustrated in Chart 15 of the November 28 report. For now, the mainland fixed-income market is not predicting an upturn in China’s industrial economy (Chart I-12, top panel). In Korea, exports account for 40% of GDP. Hence, without a considerable export recovery, there cannot be a business cycle revival in Korea. In brief, the latest relapse in local bond yields could be sending a downbeat signal for global trade (Chart I-12, bottom panel). Third, the four-month rise in the Chinese Caixin manufacturing PMI can be partially explained by front-running production and shipments of smartphones, laptops, computers and other electronics ahead of the December 15 round of US tariffs on imports from China. Right after President Trump announced these tariffs in the summer, businesses likely did not take a chance to wait and see. In fact, whether or not these tariffs would have come into effect was unknown till December 13. Manufacturers and US importers of these electronic goods initiated orders, produced and shipped these goods to the US ahead of December 15. Chart I-13Caixin And Taiwanese PMIs Benefited From Front Running

Caixin And Taiwanese PMIs Benefited From Front Running

Caixin And Taiwanese PMIs Benefited From Front Running

Given the focus on that particular round of tariffs was electronics, producers of these goods got a temporary but notable boost from such front-running. Smartphone and electronics manufacturers and their suppliers are predominantly located in Shenzhen and Taiwan. The Caixin manufacturing PMI is a survey of 500 companies, many of which are private enterprises located in Shenzhen. Not surprisingly, the Caixin manufacturing PMI index often fluctuates with Taiwan’s electronics and optical PMI (Chart I-13). In brief, there has been meaningful improvement in China’s and Taiwan’s tech manufacturing. Yet it can be attributed to front-running of production and shipments of electronic products to the US ahead of the December 15 tariff deadline as well as stockpiling of semiconductors by China. The odds are that these measures of manufacturing will slump in early 2020 as the front-running ends. Chart I-14Commodities Prices In China

Commodities Prices In China

Commodities Prices In China

Finally, several commodities prices in China, that troughed in late 2015 ahead of the bottom in global and EM/Chinese equities in early 2016, continue to drift lower or exhibit only a mild uptick. Specifically, these include prices of nickel, steel, iron ore, thermal coal, coke, polyethylene and rubber (Chart I-14). They corroborate that there has been no broad-based amelioration in the mainland’s industrial sector. Bottom Line: In China, narrow and broad money growth has rolled over, onshore interest rates are subsiding and many commodities prices are weak. All of these signify the lack of sustainable growth revival in China in the coming months. Putting It All Together EM risk assets have rallied on the consensus market narrative that the temporary truce between the US and China will lift global growth. We have written at length that China’s domestic demand – not its exports – has been the epicenter of and basis for the global slowdown over the past two years. Without Chinese domestic demand and imports, not exports, staging a material amelioration, global trade and manufacturing are unlikely to experience a cyclical upturn. In short, we doubt that the US-China trade truce is alone sufficient to propel a cyclical recovery in global trade and manufacturing. Yet, when the majority of investors perceive things the same way and act on these perceptions, asset prices can move a lot. We continue to believe that China’s industrial sector, global trade, EM ex-China domestic demand and consequently EM corporate profits will continue to disappoint in the first half of 2020. Nevertheless, we presently concede that we need to give benefit of the doubt to markets. We still doubt that the US-China trade truce alone is sufficient to propel a cyclical recovery in global trade and manufacturing. It could be that the EM equity and currency market rallies are not driven by their fundamentals – i.e., corporate profits/exports do not matter. However, it is rather possible that this rally is only stoked by the worst-kept secret in the investment industry: the search for yield. If that is the case, then there is no dichotomy between our fundamental thesis – that EM/China profits/growth will disappoint in H1 2020 – and the rally in EM markets. It seems the market is operating on a “buy now, ask questions later” principle. We had thought that the ongoing and enduring contraction in EM corporate profits (please refer to Chart I-11 on page 8) amid various structural malaises would overwhelm the impact of the global search for yield. However, it seems the market is operating on a “buy now, ask questions later” principle. Overall, we are initiating a long position in the EM equity index as of today. Provided the high uncertainty over the outlook, we are also instituting a stop point at 1050 for the MSCI EM equity index, 5% below its current level. For global equity investors, we continue recommending favoring DM over EM stocks. Finally, our country equity overweights are Korea, Thailand, Russia, central Europe, Pakistan, Vietnam and Mexico. A basket of these bourses is likely to outperform the EM equity benchmark in any market scenario in terms of EM absolute share price performance. We have been and remain neutral on Chinese, Indian, Taiwanese and Brazilian equities. As always, our list of overweight, underweight and market weight recommendations for EM equities, local and US dollar government bonds and currencies are available at the end of our report on pages 17-18 and on our website. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Ukraine: Buy Local Currency Bonds EM fixed-income investors should buy Ukraine local currency government bonds as well as overweight Ukraine sovereign credit within an EM credit portfolio. The exchange rate is the key for EM fixed-income investors. The Ukrainian hryvnia will be supported by high real interest rates, improving public debt and balance of payment dynamics, as well as abating geopolitical risks. In turn, a stable currency will keep inflation at bay. In such an environment, investors should favor local currency government bonds, as local interest rates will continue falling. Chart II-1Inflation Will Fall Further

Inflation Will Fall Further

Inflation Will Fall Further

In turn, a stable currency will keep inflation at bay (Chart II-1). In such an environment, investors should favor local currency government bonds, as local interest rates will continue falling. The primary risk of owning Ukrainian domestic bonds is a major depreciation in the hryvnia stemming from a risk-off phase in EM. However, as a periphery country, Ukraine’s financial markets might not correlate with their EM peers. Besides, these bonds offer high carry, which protects them against moderate currency depreciation. Overall, the case for buying Ukraine local currency government bonds is based on the following: First, Ukraine satisfies the two prerequisites for public debt sustainability, namely (1) it runs a robust primary fiscal surplus and/or (2) the government’s borrowing costs are below nominal GDP growth. The public debt-to-GDP ratio stands at 56% and will continue to fall so long as the above two conditions are satisfied. The primary consolidated fiscal surplus currently amounts to 1.8% of GDP (Chart II-2). The recently approved 2020 budget projects the primary surplus to be above 1% of GDP and the overall fiscal deficit to be close to 2% of GDP. Local currency interest rates are below nominal GDP growth (Chart II-3). In addition, public debt servicing is at 3.2% and 9% as a share of GDP and total government expenditures, respectively. According to the new budget, the government plans to use close to 12% of total spending for debt repayments in 2020. This will further help reduce the public debt load. Chart II-2A Healthy Fiscal Position

A Healthy Fiscal Position

A Healthy Fiscal Position

Chart II-3Interest Rates Are Below Nominal GDP Growth And Are Falling

Interest Rates Are Below Nominal GDP Growth And Are Falling

Interest Rates Are Below Nominal GDP Growth And Are Falling

Second, the central bank has more scope to cut interest rates because various measures of inflation will continue falling. Real (adjusted for inflation) interest rates are still very elevated. In particular, the prime lending rate is at 17% for companies and 35% for households, both in nominal terms. Provided core inflation is running at 6%, lending rates are extremely high in real terms. Not surprisingly, narrow and broad money growth are sluggish (Chart II-4). Commercial banks are undergoing major balance sheet deleveraging: their asset growth is in the low single digits in nominal terms, while their value is dropping relative to nominal GDP (Chart II-5). Chart II-4Money Growth Is Sluggish

Money Growth Is Sluggish

Money Growth Is Sluggish

Chart II-5Deleveraging In The Banking Sector

Deleveraging In The Banking Sector

Deleveraging In The Banking Sector

Meanwhile, tighter regulations are forcing banks to recognize bad assets and boost their capital. This has led to a sharp drop in the number of registered banks. Such a structural overhaul of the banking system is cyclically deflationary and warrants lower interest rates. Critically, these reforms are a positive for the exchange rate in the long run. Third, receding foreign funding pressures are helping the balance of payments dynamics and are supportive for the currency. Ukrainian exports have been outperforming global exports since 2017 (Chart II-6). Agricultural exports – which represent 40% of total exports – are an important source of foreign currency revenue for the country. Chart II-6Ukraine Exports Are Outperforming Global Trade

Ukraine Exports Are Outperforming Global Trade

Ukraine Exports Are Outperforming Global Trade

Chart II-7Tight Fiscal And Monetary Policies Are Good For The Current Account Balance

Tight Fiscal And Monetary Policies Are Good For The Current Account Balance

Tight Fiscal And Monetary Policies Are Good For The Current Account Balance

The current account deficit has been narrowing due to slowing domestic demand, arising from tight fiscal and monetary policies (Chart II-7). Foreign ownership of local currency government bonds is $4.6 billion and it makes only 12% of total outstanding amount. Consequently, risk of major foreign portfolio capital outflows due to a risk-off phase in global markets is low. Lastly, Ukraine’s foreign debt obligations – the sum of short-term claims, interest payment and amortization – have been declining and are presently well covered by exports. They comprise 34% of total exports. Finally, geopolitical risks will continue to subside over the coming months. Peace talks between Ukraine and Russia will continue. Importantly, two sets of constraints could force Ukraine and Russia towards resolving the conflict. Specifically: Russia is constrained by its commitment to be a reliable gas supplier to the EU. Half of its gas export capacity passes through Ukraine. European demand for Russian gas is falling and Gazprom gas revenues are decelerating. Cutting transit of gas through Ukraine could now severely jeopardize Russia’s relations with Europe. Therefore, as much as Europe is dependent on Russian gas, Russia is as dependent on European demand for its natural gas. The EU’s support for Ukraine is contingent on reliable transits of Russian gas into EU countries. As such, President Zelensky is under pressure from Europe to assure transmission of Russian gas to Europe. This has led Zelensky into opening a dialogue with Russia and motivated him to seek a new gas transit deal with Gazprom. Given President Zelensky’s high popularity at home, he has political capital to pursue a rapprochement with Russia and attempt to find a resolution to end the conflict in the Donbass. All of these developments have been, and will continue to be, positively perceived by international investors, sustaining the recent stampede into Ukraine’s fixed-income markets. Investment Recommendation We recommend investors purchase 5-year local currency government bonds currently yielding 12%. EM fixed-income investors should also consider overweighting US dollar sovereign bonds in an EM credit portfolio on the back of improving public debt and balance of payments dynamics. Andrija Vesic Research Analyst andrijav@bcaresearch.com Footnotes 1 The Risk-On/Safe-Haven currency ratio is the average of high-beta commodity currencies such as the CAD, AUD, NZD, BRL, CLP and ZAR total return (including carry) indices relative to the average of JPY and CHF total returns (including carry). This ratio is dollar-agnostic. Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights Mega-theme 1: A hypersensitivity to higher interest rates. Overweight equities versus bonds until 10-year bond yields rise 75 bps. At which point, switch into bonds. Mega-theme 2: Europe conquers its disintegration forces. Overweight European currencies, and underweight core European bonds within a fixed income portfolio. Mega-theme 3: Non-China exposed investments outperform structurally. Overweight non-China plays, underweight materials and resources, and underweight commodity currencies. Mega-theme 4: The rise of blockchain and alternative energy. Overweight alternative energy, underweight oil and gas, and underweight financials. Feature Feature ChartUnderweight Materials And Resources In The 2020s

Underweight Materials And Resources In The 2020s

Underweight Materials And Resources In The 2020s

“Study the past if you would divine the future” – Confucius To paraphrase Confucius, we must study the mega-themes of the 2010s if we are to identify the mega-themes of the 2020s. From an economic, financial, and political perspective, the mega-themes of the past decade were: ‘universal QE’; Europe’s threatened disintegration; China becoming the world’s ‘stimulator of last resort’; and the decentralization of information, which threatened the established hierarchies in politics and society. These mega-themes of the 2010s point the way to four mega-themes for the 2020s: A hypersensitivity to higher interest rates. Europe conquers its disintegration forces. Non-China exposed investments outperform structurally. The rise of blockchain and alternative energy. Mega-Theme 1: A Hypersensitivity To Higher Interest Rates The 2010s was the decade of ‘universal QE’. One after another, the world’s major central banks bought trillions of dollars of government bonds (Chart I-2). Yet for all its apparent mystique, QE is nothing more than a signalling mechanism – signalling that central banks intend to keep policy interest rates depressed for a long time. Thereby, QE depresses long-term bond yields – which themselves are nothing more than the expected path of policy interest rates. Chart I-2The 2010s Was The Decade Of 'Universal QE'

The 2010s Was The Decade Of 'Universal QE'

The 2010s Was The Decade Of 'Universal QE'

Something else happens. Close to the lower bound of interest rates, bonds become riskier investments. As holders of Swiss bonds discovered in 2019, low-yielding bonds become a ‘lose-lose’ proposition: prices can no longer rise much, but they can fall a lot. The upshot is that all long-duration assets become risky, and the much higher return required on formerly riskier assets – such as equities – collapses to the feeble return offered on equally-risky bonds. 'Universal QE' has boosted the valuation of all risky assets. Ten years ago, when the global 10-year bond yielded 3.5 percent, equities offered a prospective 10-year return of 9 percent (per annum). Today, when the bond is yielding around 1.5 percent, equities are offering a paltry 3 percent (Chart I-3 and Chart I-4). Meaning that while the present value of the 10-year bond is up around 20 percent, the present value of equities has surged by 60 percent.1 Chart I-3Equities Are Offering A Paltry 3 Percent Return

Equities Are Offering A Paltry 3 Percent Return

Equities Are Offering A Paltry 3 Percent Return

Chart I-4The Return Offered By Equities Has Collapsed To The Feeble Return Offered By Bonds

The Return Offered By Equities Has Collapsed To The Feeble Return Offered By Bonds

The Return Offered By Equities Has Collapsed To The Feeble Return Offered By Bonds

This exponential dynamic has applied to all risky assets in the 2010s. Most notably, real estate prices have sky-rocketed: Shenzhen 325 percent; Beijing 285 percent; Berlin 125 percent; Bangkok 120 percent; San Francisco 90 percent; Los Angeles 85 percent; Sydney 75 percent; and so on. From 2010 to 2020, the value of global real estate surged from an estimated $160 trillion to $300 trillion.2 The market value of equities also doubled from $35 trillion to $70 trillion.3 But global GDP grew by less than a third from $66 trillion to $85 trillion.3 The upshot is that in 2010 the value of real estate plus equities stood at 2.9 times GDP, whereas in 2020 it stands at 4.5 times GDP. Now add in the aforementioned exponentiality of risk-asset valuations at low bond yields. In 2010, a 1 percent rise in yields required a 10 percent decline in present values, whereas in 2020 it might require a 30 percent decline. In 2010, this meant a decline equivalent to 29 percent of global GDP, but in 2020 it means a decline equivalent to a staggering 135 percent of global GDP.4 So mega-theme 1 for the early 2020s is that any monetary policy tightening – in response to, say, wage inflation fears – will unleash a massive deflationary impulse into the economy from falling stock and real estate prices. This deflationary sledgehammer will annihilate the inflationary peanut, and almost certainly trigger the next major recession. But the good news is that it is unlikely to be a 2020 story, as all the major central banks are in ‘wait-and-see’ mode. Structural recommendation: Overweight equities versus bonds until 10-year bond yields rise 75 bps. At which point, switch into bonds. Mega-Theme 2: Europe Conquers Its Disintegration Forces In sub-atomic physics, a nucleus disintegrates when the electrostatic forces pulling it apart becomes stronger than the nuclear forces holding it together. Using the nucleus as a metaphor for Europe, two of the forces pulling it apart have weakened, while one of the forces holding it together has strengthened. We now know that Europe’s biggest rebel – the UK – is leaving the European Union in 2020. In the sub-atomic metaphor, the UK has become a free radical which will try and attach itself to the largest attractive body it can find. But in losing its most wayward member the European nucleus has, by definition, become more cohesive. A second destructive force has been the economic divergences between the ‘core’ and ‘periphery’ European member states. But over the past decade, these divergences have narrowed substantially. Relative to Germany, unit labour costs have declined by 25 percent in Spain, and 15 percent in Italy. More convergence is needed, but the economic forces pulling the European nucleus apart are much weaker in 2020 than they were in 2010 (Chart I-5). Chart I-5The Economic Divergence Between Europe's Core And Periphery Has Narrowed

The Economic Divergence Between Europe's Core And Periphery Has Narrowed

The Economic Divergence Between Europe's Core And Periphery Has Narrowed

Meanwhile, a force holding the European nucleus together has strengthened. In 2010, the Target2 banking imbalance stood at €0.3 trillion; in 2020, it stands close to €1.5 trillion. In simple terms, this means Germany’s exposure to ‘Italian euro’ assets has surged via the ECB’s massive purchases of Italian BTPs. At the same time, Italian investors have parked their cash in German banks, meaning they are owed ‘German euros’ (Chart I-6). Chart I-6Europe’s Target2 Banking Imbalance Stands Close To €1.5 Trillion

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

With such a massive Target2 imbalance, the biggest casualty of the euro’s disintegration would be Germany, whose 2008 recession would look like a stroll in the park. Giving Germany a huge incentive to become more conciliatory to its partners, for example on the use of fiscal stimulus. The best way to play mega-theme 2 is through the currency and bond markets. European equity markets are plays on their dominant sectors, and as we are about to see, many of the sectors over-weighted in Europe face structural headwinds. Structural recommendation: Overweight European currencies, and underweight core European bonds within a fixed income portfolio. Mega-Theme 3: Non-China Exposed Investments Outperform Structurally The 2010s was the decade when China became the global ‘stimulator of last resort’. Prior to the 2010s, the credit impulse in China was inconsequential compared to the credit impulses in the US and Europe. But in the 2010s the tables turned. The credit impulses in the US and Europe became inconsequential, as the amplitude of China’s waves of stimulus swamped all others (Chart I-7). Chart I-7In The 2010s, China Became The Global 'Stimulator Of Last Resort'

In The 2010s, China Became The Global 'Stimulator Of Last Resort'

In The 2010s, China Became The Global 'Stimulator Of Last Resort'

China became the global stimulator of last resort because in 2010 its indebtedness was significantly less than in other major economies. But today, China’s indebtedness has overtaken the others, and is levelling off at a point that has proved to be a reliable upper bound (Chart I-8). Chart I-8China's Indebtedness Is Reaching Its Upper Bound

China's Indebtedness Is Reaching Its Upper Bound

China's Indebtedness Is Reaching Its Upper Bound

An upper bound to indebtedness exists because further debt creates mal-investments whose returns are lower than the cost of the debt. And as indebtedness approaches the upper bound, each wave of stimulus loses potency compared to the preceding wave. For example, in 2011 China’s nominal GDP growth accelerated to 20 percent, but in 2017 it accelerated to 10 percent. In the financial markets, China’s waves of stimulus enabled short bursts of countertrend outperformance within the structural bear market in materials and resources – sectors which feature large in European markets. However, as Chinese stimulus loses its potency in the 2020, the structural bear markets in China-exposed investments will re-establish (Chart I-1). Structural recommendation: Overweight non-China plays, underweight materials and resources, and underweight commodity currencies. Mega Theme 4: The Rise Of Blockchain And Alternative Energy Historian Niall Ferguson describes history as a perpetual oscillation between periods dominated by centralized hierarchies and periods dominated by decentralized networks. And quite often, he says, the switch is enabled by a revolutionary new technology. For example, the advent of the printing press in the mid-15th century catalysed the Protestant Reformation and turbocharged the Renaissance by unleashing a decentralization of knowledge, information, and news. Sound familiar? In the early-21st century the internet has similarly decentralized the production and consumption of knowledge, information, and news. And the new networked age has threatened the established hierarchies in politics and society, fuelled populism, and disrupted many sectors in the economy. Yet Ferguson points out that it is futile (as well as Luddite) to resist such shifts from hierarchical structures towards decentralized networks. In the 2020s the decentralization baton will pass from the internet to the blockchain. Just as the internet decentralizes information, the blockchain decentralizes intermediation and trust functions. Hence, the blockchain will be maximally disruptive to any economic sector whose raison d’être is intermediation and trust – most notably finance and law. The blockchain will be maximally disruptive to any economic sector whose raison d’être is intermediation and trust – most notably finance and law. By the end of the decade, you will no longer need a bank to intermediate your excess savings to a borrower. And you will no longer need a lawyer to oversee a change of ownership. The blockchain will do these for you just as securely and much more cost effectively. One consequence is that the nature of the world’s energy requirements will change. The blockchain is very energy intensive, but unlike the internal combustion engine, the energy does not have to be portable. Hence, there will be a structural shift towards energy in the form of ‘moving electrons’ and away from energy in the form of the ‘chemical bonds’ in fossil fuels. This will be a boon for the alternative energy sector at the expense of oil and gas (Chart I-9). Chart I-9Underweight Oil And Gas In The 2020s

Underweight Oil And Gas In The 2020s

Underweight Oil And Gas In The 2020s

We will cover this mega-theme in more detail in a Special Report next year. Structural recommendation: Overweight alternative energy, underweight oil and gas, underweight financials. And with that, it’s time to sign off for this year and for this decade. I do hope that you have found the past decade’s reports insightful, sometimes provocative, but always enjoyable. We promise to continue in the same vein in the 2020s. It just remains for me and the team to wish you a happy new year and a happy new decade! Fractal Trading System* The Conservatives won a surprise landslide victory in the UK election last week, but fractal structures suggest that some of the market euphoria is now overdone. Specifically, the 30 percent rally in UK homebuilders through the last 65 days is vulnerable to a short-term countertrend move. Accordingly, this week’s recommended trade is short UK homebuilders / long UK oil and gas. Set the profit target at 9 percent with a symmetrical stop-loss. Chart I-10UK: Homebuilders Vs. Oil and Gas

UK: Homebuilders Vs. Oil and Gas

UK: Homebuilders Vs. Oil and Gas

In other trades, short MSCI AC World versus the global 10-year bond was closed at its 2.5 percent stop-loss, leaving three trades in comfortable profit, one neutral, and one in loss. When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 In simple terms, if the 10-year yield declines by 2 percent, a 2 percent a year lower return for 10 years requires the present value to rise by 2 percent times 10, which equals 20 percent. In the case of equities, the equivalent calculation is 6 percent times 10, which equals 60 percent. 2 Source: Savills 3 Source: Thomson Reuters 4 2.9 times 10 percent equals 29 percent, 4.5 times 30 percent equals 135 percent. Fractal Trading System

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

Cyclical Recommendations Structural Recommendations

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

2020s Key Views: Four Mega-Themes For The 2020s

Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity

Highlights OPEC 2.0 production discipline and the capital markets’ parsimony in re funding US shale-oil producers will restrain oil supply growth. Monetary and fiscal stimulus will revive EM demand. These fundamentals will push inventories lower, further backwardating forward curves. Base metals demand will pick up as EM income growth revives. Demand also will get a boost from the ceasefire in the Sino-US trade war. Gold will remain range-bound for most of next year: A weaker USD and rising inflation expectations are bullish, but rising bond yields and reduced trade tensions will be headwinds. Grain markets will drift, although dry conditions in Argentina and the trade-war ceasefire could provide short-term price support, along with a weaker USD. Risk to our view: Continued elevated global policy uncertainty would support a stronger USD and stymie central bank efforts to revive global growth in 2020. Feature Dear Client, We present our key views for 2020 in this issue of Commodity & Energy Strategy. This will be our last publication of 2019, and we would like to take the opportunity to thank you for your on-going interest in the commodity markets and in our publication. It has been our privilege to serve you. We wish you and your loved ones all the best of this beautiful Christmas season and a prosperous New Year in 2020! Robert Ryan Chief Commodity & Energy Strategist Going into 2020, policy uncertainty again will be a key driver of commodity demand, the Sino-US trade-war ceasefire and UK election results notwithstanding.1 As uncertainty has increased, demand for safe havens like the USD and gold have increased. The principal impact of this uncertainty shows up in FX markets. As uncertainty has increased, demand for safe havens like the USD and gold has increased. Indeed, the Fed’s Broad Trade-Weighted USD index for goods (TWIBG) has become highly correlated with the Global Economic Policy Uncertainty index (GEPU). The three-year rolling correlation between these indexes reached a record high in November 2019 (Chart of the Week).2 Individually, the record for the TWIBG was posted in September 2019, while the GEPU record was hit in August 2019. Chart of the WeekGlobal Economic Policy Uncertainty Highly Correlated With USD

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

A strong USD affects commodity demand directly, because it slows income growth in EM economies – the engine-house of commodity demand. A stronger USD raises the local-currency cost of consuming commodities – an important driver of EM demand – and reduces the local-currency cost of producing commodities. So, at the margin, demand is pressured lower and supply growth is incentivized – together, these effects combine to push prices lower. Economic policy uncertainty likely will diminish in early 2020, following the Sino-US trade-war ceasefire, the decisive UK election results and continued central-bank signaling – particularly from the Fed – that rates policy will remain accommodative for the foreseeable future. That said, the ceasefire does not mark the end of the Sino-US trade war, and many issues – ongoing US-China tensions, US election uncertainty, global populism and nationalism, rising geopolitical tensions in the Persian Gulf, ad hoc monetary policy globally – still are to be resolved. Terra Incognita The GEPU index does not measure uncertainty per se, as uncertainty per se cannot be measured.3 The index picks up word usage connected with the word “uncertainty.” So, it is more the perception of uncertainty that is being reported by Economic Policy Uncertainty in its data. Nonetheless, this is a good way to measure such sentiment, as research from the St. Louis Fed found: “Increases in the economic uncertainty index tend to be associated with declines (or slower growth) in real GDP and in real business fixed investment.” In past three years, increased policy uncertainty also has been fueling demand for safe havens, chiefly the USD and gold. This is a highly unusual coincidence – i.e., a rising USD accompanied by a rising gold price. Typically, a weaker USD puts a bid under gold prices. Indeed, this relationship is one of the primary drivers of our gold model, which suggests the effect of the heightened policy uncertainty dominates the USD impact on gold prices in the current environment (Chart 2). Chart 2Gold Typically Rallies When the USD Weakens

Gold Typically Rallies When the USD Weakens

Gold Typically Rallies When the USD Weakens

The flip-side of the deleterious effects of higher economic policy uncertainty is its resolution: Growing cash balances and a higher capacity to lever balance sheets of households, firms and investor accounts means there is a lot of dry powder available to recharge growth in the real and financial economies globally.4 Chart 3BCA's Grwowth Gauges Indicate Global Economy Rebounding

BCA's Grwowth Gauges Indicate Global Economy Rebounding

BCA's Grwowth Gauges Indicate Global Economy Rebounding

Our commodity-driven economic activity gauges are picking up growth impulses, most likely in response to the global monetary stimulus that has been deployed this year (Chart 3). In addition, systemically important central banks have given no indication they are going to be reversing this stimulus. A meaningful reduction in uncertainty could turbo-charge global growth prospects. Below, we provide our key views for each of the commodity complexes we cover. Oil Outlook Energy: Overweight. The oil market is poised to move higher on the back of OPEC 2.0’s deepening of production cuts to 1.7mm b/d, mostly because of actions by the Kingdom of Saudi Arabia (KSA) to cut output deeper, to a total of close to 900k b/d vs. its October 2018 production levels.5 Combined with the loss of ~ 1.9mm b/d of production in Iran and Venezuela due to US sanctions, the supply side can be expected to tighten next year (Chart 4). The Vienna meeting – which ended December 6, 2019 – demonstrated commitment to OPEC 2.0’s production-restraint strategy, and we expect member states will deliver. At least they will reduce the incidence of free riding at KSA’s expense – there were subtle hints from the Saudis they will not tolerate such behavior. KSA’s threats in this regard are credible, given its follow-through in 1986 when they surged production and briefly drove WTI prices below $10/bbl to send a message to free riders in the OPEC cartel. The Saudis acted similarly during the 2014 – 2016 market share war. US shale-oil production growth will slow next year to 800k b/d y/y, vs. the 1.35mm b/d we expect for this year. US lower 48 crude production will increase to 10.7mm b/d in 2020, taking total US production to 13.1mm b/d, a ~ 850k b/d increase y/y. On the demand side, we lowered our expectation for 2019 growth to 1.0mm b/d, given the continued downgrades of historical consumption estimates this year from the EIA, IEA and OPEC. Nonetheless, we continue to expect 2020 growth of 1.4mm b/d, on the back of continued easing of global financial conditions, led by central-bank accommodation. Given our view, we remain long oil exposures in several ways. First, we remain long WTI futures outright going into 2020; this position is up 30% from January 3, 2019 when it was initiated. Second, we recommended getting long 2H20 vs. short 2H21 Brent futures, expecting crude oil forward curves to backwardate further as tighter supply and stronger demand force refiners to draw inventories harder next year (Chart 5). Chart 4Markets Will Tighten In 2020

Markets Will Tighten In 2020

Markets Will Tighten In 2020

Chart 5Oil Inventories Will Draw Harder In 2020

Oil Inventories Will Draw Harder In 2020

Oil Inventories Will Draw Harder In 2020

We expect Brent crude oil to average $67/bbl next year, given the fundamentals outlined above. We also expect a weaker dollar to be supportive of demand ex-US. WTI will trade at a $4/bbl discount to Brent next year, based on our modeling (Chart 6). Chart 6Brent, WTI Will Trade Higher

Brent, WTI Will Trade Higher

Brent, WTI Will Trade Higher

We remain overweight energy, crude oil in particular, given our expectation markets will tighten on the supply side and demand growth, particularly in EM economies, will revive. Bottom Line: We remain overweight energy, crude oil in particular, given our expectation markets will tighten on the supply side and demand growth, particularly in EM economies, will revive. This expectation will be challenged by continued economic policy uncertainty. On the flip side, however, a meaningful resolution to this uncertainty could turbo-charge growth as real economic activity picks up and the USD weakens. Base Metals Outlook Base Metals: Neutral. We remain strategically neutral base metals going into 2020, but tactically bullish, carrying a long LMEX and iron-ore spread position into the new year.6 The behavior of base metals prices – used by economists as proxies for EM growth – is indicating industrial demand is picking up (Chart 7). This aligns well with our proprietary indicators of commodity demand and global industrial activity (Chart 8). Base metals prices are more sensitive to changes in global growth than other commodities. For this reason, we use these prices to confirm the signals coming from the proprietary models we use to gauge EM growth. Chart 7Base Metals Prices Signaling EM Growth Revival

Base Metals Prices Signaling EM Growth Revival

Base Metals Prices Signaling EM Growth Revival

The so-called phase-one agreement to reduce tariffs in the Sino-US trade war will support global demand at the margin for base metals. This is a ceasefire in the trade war not a resolution, so we are not expecting a surge in demand. Chart 8BCA Proprietary Indicators Also Signaling Growth Revival

BCA Proprietary Indicators Also Signaling Growth Revival

BCA Proprietary Indicators Also Signaling Growth Revival

That said, base metals – aluminum and copper, in particular – have a tailwind in the form of global monetary accommodation by central banks. This was undertaken to reverse the negative effect on global financial conditions brought about by the Fed’s rates normalization policy last year and China’s 2017-18 deleveraging campaign. In addition, our China strategists expect modest fiscal and monetary stimulus from Beijing, which also will be supportive of demand.7 Aluminium and copper comprise 75% of the LMEX index. These are primary industrial markets, in which China accounts for ~ 50% of global demand, and EM ex-China demand remains stout. Even with a trade war raging for most of 2019, the supply and demand of aluminum and copper – the largest components of the LMEX index – was diverging: Consumption outpaced production – a multi-year trend – which forced inventories to draw hard (Charts 9A and 9B). Chart 9AGlobal Aluminum Markets Getting Tighter …

Global Aluminum Markets Getting Tighter ...

Global Aluminum Markets Getting Tighter ...

Chart 9B… As Are Copper Markets

... As Are Copper Markets

... As Are Copper Markets

Bottom Line: Inventories in industrial-metals markets have been drawing hard for years – particularly in aluminum – as metals' demand remained above supply. Given this, we are long the LMEX index: Even a marginal growth pick-up could rally prices. Precious Metals Outlook Precious Metals: Neutral. Going into 2020, gold’s outlook could be volatile – especially in 1H20 – as the metal’s key drivers will send conflicting signals (Table 1). Table 1Fundamental And Technical Gold-Price Drivers

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

Gold prices are holding up above $1,450/oz. Our latest fair-value estimate indicates gold will hover around $1,475/Oz over the short-term (Chart 10). We break next year’s gold forecast into two parts: Phase 1: Growth revival and uncertainty respite. These two factors are closely intertwined; the magnitude of global growth’s rebound is conditional on a reduction of global economic policy uncertainty. We expect this relief will come from a ceasefire in the US-China trade war. Combined, accelerating economic activity – mainly driven by EM economies – and falling uncertainty will push the US dollar lower.8 For gold prices, this phase will be characterized by two contrasting forces: A falling USD (bullish gold) vs. lower safe-haven demand and rising US interest rates (bearish gold). US rates will increase early next year as global uncertainty is reduced and bond markets price-out Fed rates cuts. The current unusually high correlation between gold and US rates implies gold will face selling pressures during this period (Chart 11). Nonetheless, we expect the Fed will stay on hold and not start raising rates next year, which will cap price risks to gold. Chart 10High USD Correlation Throws Off Fair-Value Model Gold Prices Will Rise 4Q20

High USD Correlation Throws Off Fair-Value Model Gold Prices Will Rise 4Q20

High USD Correlation Throws Off Fair-Value Model Gold Prices Will Rise 4Q20

Chart 11US Rates Could Hurt Gold Prices In 1H20

US Rates Could Hurt Gold Prices In 1H20

US Rates Could Hurt Gold Prices In 1H20

Phase 2: EM wealth effect and inflation rebound. As income growth accelerates, EM households will slowly accumulate jewelry, coins, and bars – of which China and India are the largest consumers. Demand pressure from these consumers will manifest itself in 2H20, adding to buoyant central-banks purchases of gold. The upside in bond yields will be limited by major central banks’ dovish stance until inflation is well-established above target. Closely monitoring the evolution of inflation will become increasingly important in 2020, given inflation pressures are building in the US and globally (Chart 12). A lower USD – supporting stronger commodity demand – will magnify global inflation trends (Chart 13). There is a very real risk inflation shoots up in 4Q20, keeping real rates low. This differs from our BCA House view, which does not see inflation pressures building until 2021. Chart 12Inflationary Pressures Are Building Up In The US And Globally

Inflationary Pressures Are Building Up In The US And Globally

Inflationary Pressures Are Building Up In The US And Globally

Political uncertainty likely will return ahead of the 2020 US election. A resurgence in popular support for one of the progressive Democratic candidates – Elizabeth Warren or Bernie Sanders – could disrupt US stock markets. Gold would advance in such an environment. Chart 13No Inflation Without A Weaker USD

No Inflation Without A Weaker USD

No Inflation Without A Weaker USD

Progressive populists would lead to domestic policy uncertainty and larger budget deficits, yet would not remove the threat of trade protectionism. We expect the Fed will stay on hold and not start raising rates next year, which will cap price risks to gold. Bottom Line: Gold prices will move sideways in 1H20 and will drift higher in 4Q20 supported by depressed real rates, a lower dollar, and US election uncertainty. Silver Market Chart 14Silver Prices Will Move Higher With Gold Prices

Silver Prices Will Move Higher With Gold Prices

Silver Prices Will Move Higher With Gold Prices

Silver prices have traded closely with gold since the Global Financial Crisis (GFC), moreso than with industrial metals (Chart 14). Prior to the GFC, silver traded like a base metal, owing to the high growth rates in EM economies undergoing rapid industrialization. Post-GFC, the evolution of silver’s price more closely tracked gold prices, following the massive injections of money and credit by central banks globally. Thus, we expect it will continue to follow the evolution of gold prices outlined above. Nonetheless, industrial applications still represent ~ 50% of silver’s physical demand and its supply-demand balance is estimated to have been tight this year. Silver likely will outperform gold next year as global growth and industrial activity rebound. PGM Markets The palladium market will remain tight in 2020. According to Johnson Matthey, the 10-year-long supply deficit is expected to widen massively this year, when all’s said and done. Prices surpassed $1,900/oz in December, forcing inventory liquidation (Chart 15). We believe the platinum-to-palladium ratio is at a level that would incentivize substitution in the pollution-control technology in gasoline-powered engines, and supports higher platinum content in diesel catalyzers (Chart 16).9 Nonetheless, swapping palladium for platinum is complex and requires a redesign of the production process. A lot will depend on how much the added cost of the more expensive palladium affects new-car buyers’ demand.10 To date, there are no signs car makers have already – or are willing to – initiate this process on a significant scale. Chart 15Palladium Inventories Are Depleted

Palladium Inventories Are Depleted

Palladium Inventories Are Depleted

A few factors need to align to incentivize substitution of palladium for platinum. The price ratio between the two metals should reach extreme levels; the price divergence should be expected to last for a prolonged period of time, and concerns over supply security of platinum should be low. Chart 16Relative Inventory levels Drive The Palladium To Platinum Price Ratio

Relative Inventory levels Drive The Palladium To Platinum Price Ratio

Relative Inventory levels Drive The Palladium To Platinum Price Ratio

In today’s context, this last condition could slow substitution. South African platinum supply – which represents close to 73% of the world primary supply – is projected to fall by close to 3% next year. Automakers need stable platinum supplies as they increase their demand for the metal and with persistent power-supply issues in South Africa – exacerbated by recent flooding – this condition will be hard to meet. No market has been harder hit by the Sino-US trade war than grains and ags generally. Thus, palladium holds an advantage over platinum on that front. Its supply sources are more diversified, and with 15% comes from stable North American countries and 40% comes from Russia. We believe substitution will commence, but this is a gradual process and will only slowly affect the metals’ price ratio.11 For 2020, we expect palladium prices to continue increasing due to stricter pollution regulation in China, India, and Europe.12 Ag Outlook Chart 17Sino-US Trade War, USD Hammer Grain Prices

Sino-US Trade War, USD Hammer Grain Prices

Sino-US Trade War, USD Hammer Grain Prices

Ags/Softs: Underweight. The final form of the ceasefire in the Sino-US trade war – i.e., the “phase one” deal between China and the US to roll back tariffs – has yet to show itself. Last Friday, US Trade Representative Robert Lighthizer stated China has agreed to buy $32 billion – over the next two years – of US ag products as part of a “phase one” deal. This news moved corn, wheat and beans prices up 6.3%, 3.2%, and 3.4% respectively as of Tuesday’s close. Another positive news for US farmers was an announcement from the USDA that the final $3.6 billion of the $14.5 billion budgeted for farm subsidies this year to offset the trade war impact on US farmers most likely would be made in the near future by the Trump administration.13 No market has been harder hit by the Sino-US trade war than grains and ags generally. Severe weather across much of the US Midwest should have produced a rally, as offshore demand competed for available supply, which likely would have been lower at the margin last year absent a trade war. Instead, corn, wheat and beans are going into 2020 pretty much at the same price levels they went into 2019. In addition to the deleterious effect of the US-China trade war, ag markets have been particularly hard hit by the strong USD, which makes exports from the US expensive relative to alternative suppliers – e.g., Argentina and Brazil, which are posing serious challenges to US farmers (Chart 17). Global inventories are, nonetheless, being whittled away, which is good news for farmers generally (Chart 18). And, this likely will continue in 2020, given the physical deficits expected this year (Chart 19). Chart 18GLOBAL GRAIN STOCKS BEING WHITTLED DOWN ...

GLOBAL GRAIN STOCKS BEING WHITTLED DOWN ...

GLOBAL GRAIN STOCKS BEING WHITTLED DOWN ...

Chart 19... Physical Deficits Will Whittle Stocks Further Next Year

... Physical Deficits Will Whittle Stocks Further Next Year

... Physical Deficits Will Whittle Stocks Further Next Year

Markets are still awaiting final details of the ceasefire in the Sino-US trade war. The deal is expected to be signed in the first week of January. 2020 could be the year the global ag markets come more into balance, with stocks-to-use levels falling and normal trade resuming. We are not inclined to take a view on this possibility and are therefore remaining underweight the ag complex. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Footnotes 1 Our outlook last year was entitled 2019 Key Views: Policy-Induced Volatility Will Drive Markets. It was published December 13, 2018, and is available at ces.bcaresearch.com. This year’s outlook again reflects our House view, which was published in the Bank Credit Analyst on November 28, 2019, entitled OUTLOOK 2020: Heading Into The End Game. It was sent to all clients last month and is available at bca.bcaresearch.com. 2 Uncertainty is measured using the Baker-Bloom-Davis Global Economic Policy Uncertainty (GEPU) index. GEPU is a monthly GDP-weighted index of newspaper headlines containing a list of words related to three categories – “economy,” “policy” and “uncertainty.” Newspapers from 20 countries representing almost 80% of global GDP (on an exchange rates-weighted basis) are scoured monthly to create the index. Please see Economic Policy Uncertainty for additional information. We use the Fed's USD broad trade-weighted index for goods (TWIBG) reported by the St. Louis Fed to track the USD. Please see the St. Louis Fed’s FRED website at Trade Weighted U.S. Dollar Index: Broad, Goods. 3In a June 2011 interview with the Minneapolis Fed, Ricardo Caballero, a professor of economics at MIT, provided a succinct description of risk and uncertainty, paraphrasing former US Defense Secretary under President George W. Bush Donald Rumsfeld: “(W)hen he talked about the difference between known unknowns and unknown unknowns. The former is risk; the latter is uncertainty. Risk has a more or less well-defined set of outcomes and probabilities associated with them. Uncertainty does not—things are much less clear.” Kevin L. Kliesen of the St. Louis Fed explores the link between rising uncertainty and slower economic growth in Uncertainty and the Economy (April 2013), observing, “If the business and financial community believes the near-term outlook is murkier than usual, then the pace of hiring and outlays for capital spending projects may be unnecessarily constrained, thereby slowing the overall pace of economic activity.” 4The Wall Street Journal reported investors have accumulated a $3.4 trillion cash position, a decade-high level; this is consistent with the risk aversion that can be expected when economic uncertainty is high. Please see Ready to Boost Stocks: Investors’ Multitrillion Cash Hoard, published by The Wall Street Journal November 5, 2019. 5 Accounting for Saudi Arabia's 400k b/d of additional voluntary cuts. 6 The LMEX no long trades on the LME, but we are using the index as a proxy for a position. In iron ore, we are long December 2020 65% Fe futures vs. short 62% Fe futures on the Singapore Exchange, expecting steelmakers will favor the high-grade material in the new mills they’ve brought on line. 7 Our China strategists expect “Chinese policymakers will roll out more stimulus to secure an economic recovery in 2020, and external demand will improve. But we expect growth in both the domestic economy and exports to only modestly accelerate.” Please see 2020 Key Views: Four Themes For China In The Coming Year, published by BCA Research’s China Investment Strategy December 11, 2019. It is available at cis.bcareserach.com. 8 The US dollar is a countercyclical – i.e. it is inversely correlated with the global business cycle – due to the fact that the US economy is driven more by services than manufacturing. 9 Palladium is used mostly in pollution-abatement catalysts in gasoline-powered cars, while Platinum is favored in diesel-engine cars (along with a small amount of palladium). Catalysts production represents close to 80% and 45% of palladium's and platinum's total demand. 10 Considering there’s ~ 3.5g of palladium in a new car and palladium trades at ~ $1,900/oz, close to $240 is added to the cost of a new gasoline-powered car by using this metal in pollution-abatement technology. 11 Please see South African Mines Grind To Halt As Floods Deepen Power Crisis, published by reuters.com on December 10, 2019. 12 Stricter emissions standards in the car industry – mainly in China where China 6 emissions legislation is taking effect – are increasing the PGMs loadings in each car, supporting demand growth. 13 Please see China May Agree to Buy U.S. Ag Exports, But a Final Tranche of Cash to Farmers is Still Likely, published by agriculture.com’s Successful Farming news service. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q3

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Trades Closed

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

2020 Key Views: Policy Uncertainty Continues To Drive Commodity Markets

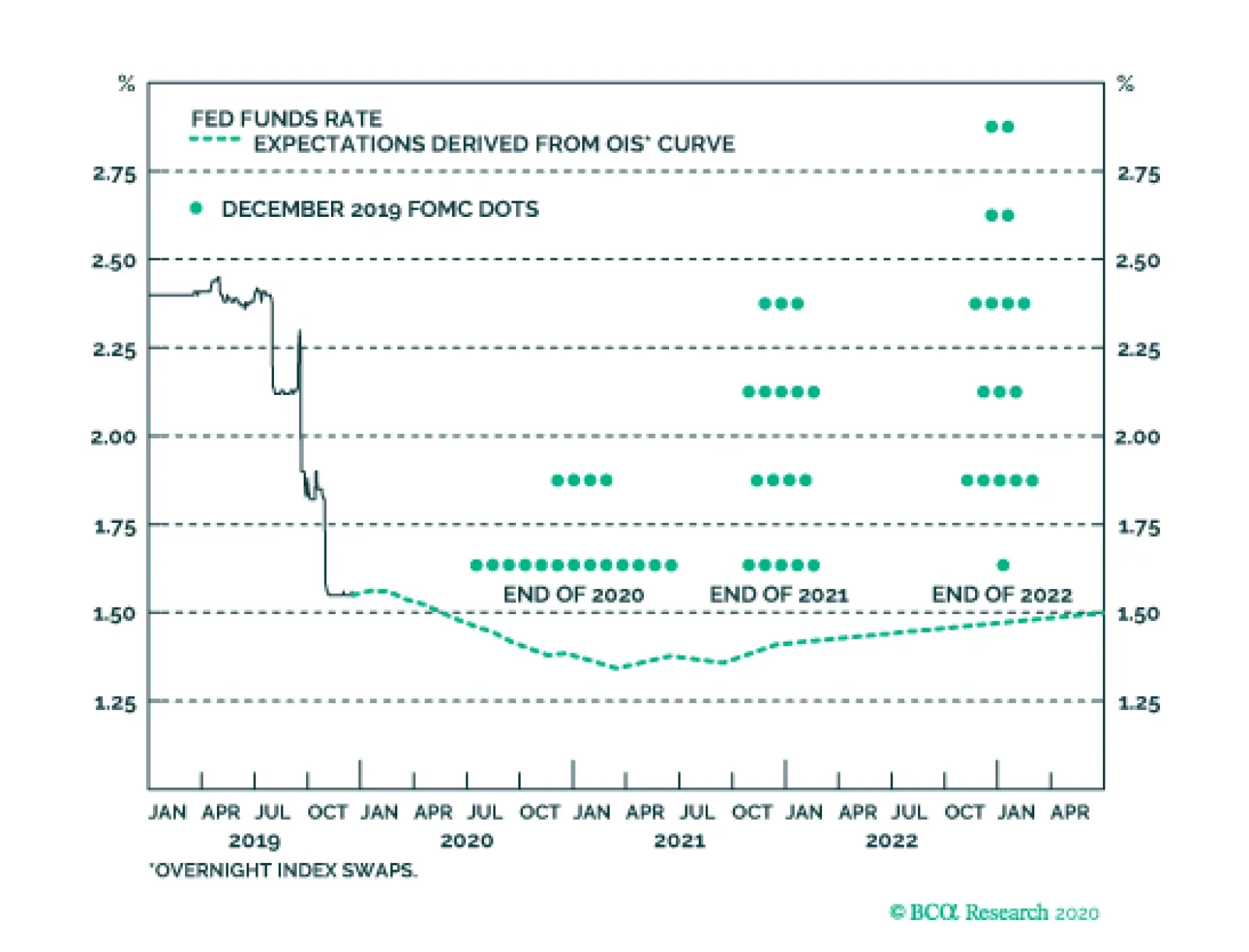

At last week’s FOMC meeting, the Fed’s reaction function underwent a significant dovish shift. Currently, only four FOMC participants expect to lift rates in 2020 while the remaining 13 expect the funds rate to stay between 1.5% and 1.75%. Back in…

Dear Clients, In our final publication of the year, we bring you a recap of this past week’s significant events in Sino-US relations and the key messages from the Central Economic Work Conference. Accordingly, we are upgrading our tactical stance towards Chinese stocks from neutral to overweight. Our publishing schedule will resume on January 9, 2020 with our monthly Macro and Market Review. Our China Investment Strategy team wishes you a happy holiday season and a prosperous New Year! Best regards, Jing Sima, China Investment Strategist Highlights We are upgrading our tactical call on Chinese stocks from neutral to overweight. Recent developments in the Chinese investable equity market point to a risk-on sentiment. The fact the US and China have reached an agreement likely marks the beginning of a truce, which could potentially last through the US presidential election in November 2020. The CEWC statement from last week reinforces our view that China's leadership feels the urgency to stabilize the economy now outweighs the desire to continue financial deleveraging. Feature Signals from the Chinese investable equity market have titled in a bullish direction. This shift is accompanied by two modestly bullish developments: First, the annual China Economic Work Conference (CEWC) concluded on December 12 with support for a more reflationary stance for the coming year. Then, a day later, the US and Chinese officials confirmed they have agreed on a Phase One trade deal. The combination of these developments provides a sufficient basis to upgrade our tactical (0-3 month) stance on Chinese stocks from neutral to overweight (within a global equity portfolio), to be consistent with our bullish cyclical (6-12 month) stance. Equity Market Signals Have Become Bullish In our previous reports, we highlighted that the relative performance of some sectors in the Chinese investable equity market reflects China’s policy direction and financial market conditions, supporting our bullish/bearish calls on Chinese stocks. Recently, two of the three equity market telltale signs that we have been watching have turned favorable for a bullish view on Chinese stocks (Chart 1A and 1B): Chart 1ACountercyclical Sector Stock Performance Points To Improvement In Economic Activity

Countercyclical Sector Stock Performance Points To Improvement In Economic Activity

Countercyclical Sector Stock Performance Points To Improvement In Economic Activity

Chart 1BThe Breakdown Of Defensive Stocks Suggests A Return Of Risk-On Sentiment

The Breakdown Of Defensive Stocks Suggests A Return Of Risk-On Sentiment

The Breakdown Of Defensive Stocks Suggests A Return Of Risk-On Sentiment

Chart 1A (top panel) shows that the relative performance of investable utility stocks have broken down, signifying that market participants anticipate the slowdown in China’s economy will soon bottom. Investable healthcare stocks have not breached their 200-day trend, but are headed in that direction (Chart 1A, bottom panel). Key equity market signs have turned supportive for a bullish tactical call on Chinese stocks. Cyclical stocks are outperforming defensives in both China’s onshore and offshore markets, reflecting improved investor sentiment towards China’s economic outlook (Chart 1B). Bottom Line: Key equity market signs have turned supportive for a bullish call on Chinese stocks for the next 0 to 3 months. Phase One Trade Deal: Unimpressive But Pragmatic Adding to this bullish shift in equity market signals was the first of two positive fundamental improvements over the past week. The US and China reached agreement on a Phase One deal just a few days before the 15% tariff increase on $160 billion of Chinese export goods to the US was scheduled to come into effect. Reportedly, the two sides agreed to pause the 15% tariff scheduled for December 15 and lower the tariff on about $120 billion of Chinese imports to 7.5%. However, the 25% tariffs on the first $250 billion of Chinese imports will remain in place (Chart 2). Chart 2Tariff Rollbacks Unimpressive...

Tariff Rollbacks Unimpressive...

Tariff Rollbacks Unimpressive...

Chart 3...But China's Promise To Buy American Goods Helps Trump Claim Victory

...But China's Promise To Buy American Goods Helps Trump Claim Victory

...But China's Promise To Buy American Goods Helps Trump Claim Victory

In return, China agrees to, in the next two years, boost imports of American goods and services by a total of $200 billion from their levels in 2017 (Chart 3). While no specific number has been confirmed from the Chinese side, in a news conference, Chinese officials said that China “will expand imports of some agriculture products currently in urgent need, such as pork and poultry.” Given that both sides picked low hanging fruit in the Phase One deal, the tougher issues to be discussed in Phase Two could lead to a breakdown in negotiations, which potentially could unravel the Phase One tariff rollbacks. Nevertheless, the agreement serves an interim purpose for both President Trump and President Xi: it allows Trump to claim a short-term political victory on his trade negotiations with China, and gives Xi some breathing space to focus on domestic economic challenges. Bottom Line: While the Phase Two negotiations, when commencing, will be a risk to the Phase One trade deal, the current agreement likely marks the beginning of a truce, which could potentially last through the November’s presidential election in 2020. CEWC: Reinforcing Reflationary Bias For 2020 In addition to the trade deal, another bullish factor for stocks is the fact that Chinese policymakers will proactively fine-tune economic policy to mitigate the impact from the US tariffs that remain in effect and to ensure stable economic growth in the coming year. President Xi at last week’s Central Economic Work Conference (CEWC) urged that Chinese policymakers must “make contingency plans” to combat challenges from both domestic and external environment. At the three-day annual CEWC this year, Chinese central and local government officials set the direction and strategy of China’s economic policy for the coming year. The meeting also reveals the challenges Chinese policymakers are facing, and the areas they will likely mobilize monetary resources to tackle. Investors can therefore benefit from insights into both the direction and constraints of China’s near-term policy framework. We highlight four investment-relevant messages from this year’s CEWC: A Greater Emphasis On Growth Stability The tone from this year’s CEWC reflects an urgency to stabilize the economy and meet growth targets. The tone from this year’s CEWC reflects an urgency to stabilize the economy and meet growth targets. The statement from the meeting mentioned “stability” 31 times, compared with 22 in 2018.1 The statement also reiterated the importance of doubling GDP and per capita income by 2020. This suggests that a growth imperative remains the top priority and reinforces the leadership’s reflationary policy stance for next year. We previously projected that the Chinese government would allow a lower GDP growth target for 2020, between 5.5 and 6.0%. However, we think growth targets to be set at next March’s National People’s Congress (NPC) are more likely to be in a “reasonable range” (verbiage used in the CEWC statement) between 5.8 and 6.2%. As noted in our December 11 report,2 the Chinese economy needs to increase by 6% in 2020 to double its size from the 2010 level in real terms. While China’s real GDP statistics are suspiciously smooth and largely invalid when it comes to equity market pricing, the deviation between market expectations and the actual GDP growth target range set at NPC can help investors gauge how much more (or less) ammunition Chinese policymakers are willing to deploy to support the economy in that year. China is falling short of its target to double real urban per capita income next year from 10 years ago (Chart 4). Nominal wage and salary per capita growth has experienced a sharp drop since the third quarter of 2018 and probably contributed to the subdued appetite for consumption (Chart 5). Chart 4Household Income: Rural Overshooting; Urban Falling Short

Household Income: Rural Overshooting; Urban Falling Short

Household Income: Rural Overshooting; Urban Falling Short

Chart 5Wage Growth Only Started Stabilizing Recently

Wage Growth Only Started Stabilizing Recently

Wage Growth Only Started Stabilizing Recently

To meet the target, urban per capita income will need to grow at an above-real GDP rate of 10% in 2020, almost doubling the growth in 2018 and 2019. Given the still weak domestic economic conditions, we are not optimistic that China will be able to double the growth rate of urban income per capita in 2020 from 2019. Additionally, income typically lags economic activity. Even if China’s economic slowdown bottoms in the first quarter of 2020, it is unlikely we will see significant improvement in income until a few quarters later. Therefore, we think policymakers will likely focus on overall economic and employment growth stability, and poverty reduction through improving rural income in 2020 (Chart 4, top panel). A Shift In Policy Priorities The new year marks the final year of the “Three Major Battles” against financial deleveraging, poverty elimination, and pollution. In this year’s CEWC statement, for the first time in three years, the order of the battles has been rearranged with financial deleveraging ranked behind poverty reduction and environment protection. The PBoC will stay on a mild rate-cutting cycle throughout next year. The shift in policy priorities suggests that the pressure to deleverage has greatly eased. Banks’ asset balance sheets will expand at a faster rate, while the pace of reduction in shadow banking will likely continue to moderate (Chart 6). The description of monetary policy stance was amended to “maintaining a flexible and appropriate monetary policy” from last year’s “appropriately loose or tight.” The change points to a more dovish tone, confirming our assessment that the PBoC will stay on a mild rate-cutting cycle to lower corporate funding costs throughout the next year3 (Chart 7). Chart 6In 2020, Expect Faster Bank Balance Sheet Expansion

In 2020, Expect Faster Bank Balance Sheet Expansion

In 2020, Expect Faster Bank Balance Sheet Expansion

Chart 7The PBoC's Rate-Cutting Cycle Will Continue Next Year

The PBoC's Rate-Cutting Cycle Will Continue Next Year

The PBoC's Rate-Cutting Cycle Will Continue Next Year

At this stage, we do not anticipate the Chinese policymakers will entirely abandon financial risk containment or significantly loosen financial regulations. Rather, we think the reduced pressure on deleveraging and lowering of funding costs will provide moderate support for the private sector, specifically small- and medium-sized enterprises. A slew of new policies announced before the CEWC, including an adjustment to some of the parameters in the Macro-Prudential Assessment (MPA) framework to encourage lending to the private sector,4 will help strengthen the impact of PBoC’s countercyclical measures. A Bigger Fiscal Push This year’s CEWC statement indicated policymakers will continue to fine-tune a proactive fiscal policy, but unlike last year, the meeting did not specify further cuts to taxes. The statement suggests fiscal support to the economy will mainly focus on infrastructure, and listed transportation, urban and rural development, and the 5G networks to be the government’s main investment projects next year. Chart 8Local Governments Have Borrowed More Than They Spent

Local Governments Have Borrowed More Than They Spent

Local Governments Have Borrowed More Than They Spent

In 2019, infrastructure investment was subdued, despite increased quotas for local government special-purpose bond issuance. Our research shows that local government infrastructure expenditures in 2019 have consistently lagged behind their borrowing (Chart 8). The gap between local government infrastructure funding deficit and borrowing has only started flattening in the third quarter of this year. The delayed conversion from borrowing to spending means local governments have accumulated more spending power for 2020. In order to encourage local governments to speed up spending, the central government is also likely to further loosen up project restrictions. A bigger fiscal push by the central government, coupled with a frontloading of 2020 local government special-purpose bond issuance, will likely boost infrastructure spending to around 10% in the first two quarters, doubling the growth in the first eleven months of 2019.5 More robust fiscal stimulus will lead to an increase in the debt load of local governments, but Chinese policymakers are caught between a rock and a hard place and therefore must choose the least risky tools to stimulate the economy. In our view, local government bonds are still a better option over local government financing vehicles (LGFVs) or other illicit channels. Social Housing Gets Another Boost Surprisingly,6 last week’s CEWC statement again emphasized the importance of shantytown renovation (Chart 9). While this implies there would likely be a significant monetary boost to social housing in the coming year, the statement also indicated that policymakers would not want property prices to dramatically change in either direction. Even though local governments have been granted more flexibility to fine-tune their local housing policies, we think the possibility of a broad-based regulatory easing in the housing market remains low in 2020. Therefore, government subsidies in social housing in 2020 will unlikely to lead to another property market boom like that of 2016. Chart 9Social Housing Gets Another Fiscal Boost

Social Housing Gets Another Fiscal Boost

Social Housing Gets Another Fiscal Boost