Policy

The Chinese economic growth model remains reliant on credit formation and capital investment. Therefore, the sustainability of an economic recovery depends on whether Chinese policymakers are willing to keep the stimulus wheel turning. We expect that some…

Feature We spent the past two weeks visiting and exchanging views with our clients in Asia. We presented our view that the ongoing stimulus measures are beginning to bear fruit in terms of stabilizing China’s economic activity, and that we expect the economic slowdown to bottom early next year. In addition, Chinese policymakers are signaling their willingness to accelerate stimulus on both monetary and fiscal fronts, which should mitigate the downside risks and help the economy regain traction in 2020. Interestingly, our view sparked divergent responses: clients outside of China were more upbeat about the state of the Chinese economy than clients from mainland China. While few investors we spoke to showed concerns over an imminent “hard landing” in China’s economy or systemic risk from China’s financial system, our mainland Chinese clients remain skeptical that the ongoing stimulus will be sufficient to revive the economy. They were also worried that financial regulations may be too restrictive to generate the amount of money growth needed for the economy. Another interesting observation was that while being pessimistic about the economy, our mainland Chinese investors share our assessment that Chinese domestic stocks still have some upside in the coming year. On the other hand, global investors, who are more sanguine about China’s economic recovery, prefer to wait on the sidelines before favoring Chinese investable stocks (Chart 1). Chart 1AA Tale Of Two Markets: Onshore Outperforms Global Markets...

A Tale Of Two Markets: Onshore Outperforms Global Markets

A Tale Of Two Markets: Onshore Outperforms Global Markets

Chart 1B...While Offshore Underperforms

...While Offshore Underperforms

...While Offshore Underperforms

Below we present some of the top questions that were posed by investors during our trip, along with our answers. We recap the conclusions of our view, and draw out the investment implications of the differences between the sentiments towards China’s equity markets, in the last question of the report. Q: Recent economic data suggests a weakening Chinese economy. Why do you think the economy will reach a bottom in 2020? Historically, China’s credit formation has consistently led economic activity by about three quarters (Chart 2). Even though credit growth this year has not been as strong as in previous expansionary cycles, a turning point in the credit impulse occurred at the start of 2019. This suggests that economic activity should turn around within the next two quarters. Chart 2Expecting A Turn In Q1 2020

Expecting A Turn In Q1 2020

Expecting A Turn In Q1 2020

Chart 3Emerging Green Shoots

Emerging Green Shoots

Emerging Green Shoots

Furthermore, despite weakening headline economic data, some underlying components indicate promising improvements (Chart 3): Growth in infrastructure investment has ticked up modestly in the past couple months, and is set to improve further. The State Council mandated local governments to allocate the proceeds from special-purpose bond sales to infrastructure projects by the end of October. This, combined with a frontloading of next year’s local government bonds, should lend support to infrastructure spending in the coming months. After fluctuating in and out of contraction for a year, growth in auto manufacturing production picked up in August and remained positive through October. This improvement is due to less contraction in auto sales and a faster reduction in auto inventories. Moreover, electricity output surged in October, which also indicates that growth may be gaining momentum. Chart 4Trade Should Improve Into 2020

Trade Should Improve Into 2020

Trade Should Improve Into 2020

Lastly, global financial conditions have eased significantly and credit growth has picked up worldwide, which should help support global demand. Even though Sino-US trade negotiations are ongoing, our baseline view is that a “Phase One” trade deal will be inked in the next couple months. Eased trade tensions and even some rollbacks in the existing tariffs on Chinese export goods, coupled with improved global demand, should provide some tailwinds to China’s external sector (Chart 4). Q: What is your outlook on China’s economic policy for 2020? The Chinese economic growth model remains reliant on credit formation and capital investment. Therefore, the sustainability of an economic recovery depends on whether Chinese policymakers are willing to keep the stimulus wheel turning. Chart 5A Sign Of A Policy Shift

A Sign Of A Policy Shift

A Sign Of A Policy Shift

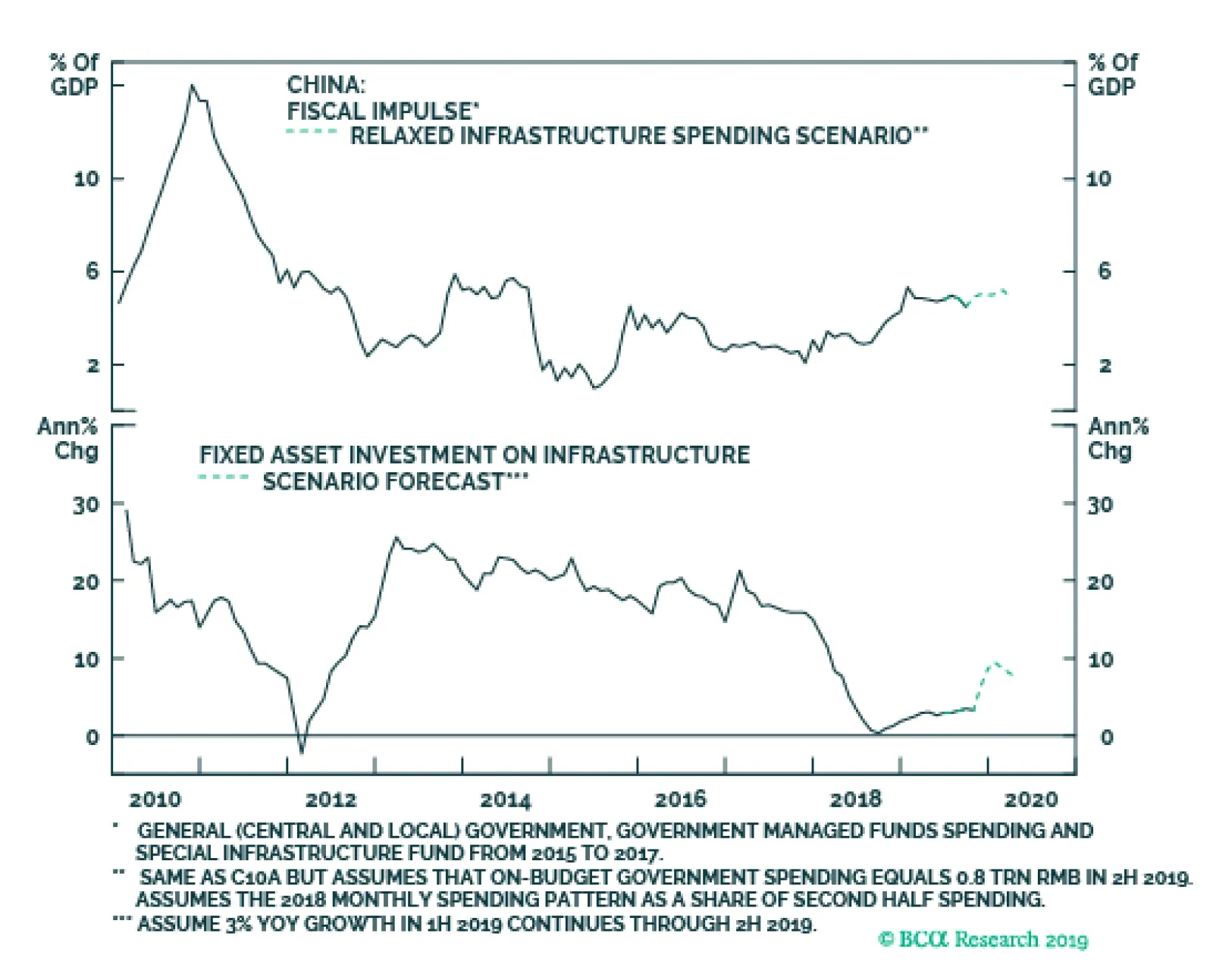

For investors favoring China-related assets, the good news is that there has been an increasing urgency in policymakers’ tone to support economic growth since September. Capex growth from state-owned enterprises (SOEs) has increasingly outpaced the private sector, which is significant: A sustained rotation in the pace of SOE vis-à-vis private sector capex marked a turning point in the 2015-2016 cycle, when Chinese policymakers’ imperative to supporting growth outweighed their desire to continue with structural reforms (Chart 5). We do not expect a 2016-style drastic rise in SOE capex growth next year, because the current economic slowdown is not as severe or prolonged as in 2015. Nonetheless, the rotation in capex growth is an important signal that Chinese policymakers may be more willing to stimulate the economy by again allowing the state sector to upstage the private sector. In the meantime, we expect that some pro-growth “policy adjustments” will be deployed in 2020: Chart 6Infrastructure Investment Likely To Rise

Infrastructure Investment Likely To Rise

Infrastructure Investment Likely To Rise

Monetary policy will incrementally ease, with one to two 10-15bps loan prime rate (LPR) cuts in the next 3-6 months. At the same time, China’s central bank (PBoC) will keep bank liquidity ample and commercial banks’ funding costs relatively low, by continuing frequent liquidity injections to stabilize the interbank rate. A further cut in the reserve requirement ratio (RRR) is also highly likely. Keeping banks well capitalized will partially mitigate the pressure commercial banks face from falling profit margins and rising credit defaults. Accommodative monetary conditions will also support more stimulus on the fiscal front. We expect that the National People’s Congress in March 2020 will approve higher quotas on the issuing of local government bonds. Chinese state-owned commercial banks will continue to be the main buyers for local government bonds. A portion of 2020 local government special-purpose bond issuance will be frontloaded to the remainder of 2019 and into the first months of next year. Relaxed capital requirements will likely boost local governments’ infrastructure project funding and expenditures. Our model suggests infrastructure spending should pick up from the current 3.3% year-on-year, to close to 7.5% in the second and third quarters next year (Chart 6). There are subtle signs that the government is starting to relax restrictions on the real estate sector. Land sales by local governments have increased since mid-2019, and the trend will continue into 2020 (Chart 7). Income from land sales accounts for 70% of local government revenues, thus allowing more land sales should help fund a larger local government spending budget next year. Declining government subsidies to shantytown renovation (namely the Pledged Supplementary Lending, or PSL) have recently abated and will likely continue to improve (Chart 8). Chart 7Some Improvement To Come In The Real Estate Sector

Some Improvement To Come In The Real Estate Sector

Some Improvement To Come In The Real Estate Sector

Chart 8Government Subsidies Will Continue

Government Subsidies Will Continue

Government Subsidies Will Continue

December’s Central Economic Work Conference (CEWC) will set policy priorities for the following year. We think Chinese policymakers will make economic growth a top priority for 2020. Credit growth swelled in the first quarter of 2019 following the December 2018 CEWC, and we expect a surge in early 2020 as well.Due to the unusually high credit growth in January this year and the seasonal factor next year (Chinese New Year will fall in January 2020), the surge in credit growth, on a year-over-year basis, will more likely be muted until towards the end of the first quarter and into the second quarter. Investors should overweight Chinese investable stocks in the next 6-12 months, but need to watch for more positive signs to upgrade tactical stance. Beyond the second quarter, however, the outlook gets cloudier as tension from the US election heats up and President Trump may change his trade negotiation strategies with China.1 This may have implications on China’s domestic policies. But for now, our baseline view is that Chinese policymakers will incrementally accelerate the pace of economic stimulus throughout next year. Q: Monetary policy has been accommodative for more than a year, but capex this year has fallen below market expectations compared with past cycles. How will further stimulus help to revive investment and economic growth next year? In short, our answer is this: interest rate cuts alone will not be enough to boost economic growth in China. Capex, and growth more generally, will only revive through synchronized policy support from the Chinese authorities. In a previous report2 we discussed that the lack of response to monetary easing has been due to a less effective monetary policy transmission mechanism, a reactive and reluctant central bank, and a debt-loaded corporate sector. More importantly, the “half-measured” stimulus has been preferred by Chinese authorities in this cycle, as they prioritized financial de-risking over growth and have significantly tightened financial regulations since 2016. Given the expected policy pivot to a more pro-growth stance in the coming year, the following underlines our conviction that capex should pick up in 2020. Modern Money Theory (MMT), with Chinese characteristics:3 local governments will ramp up debt again, and this quasi-fiscal stimulus will be a key support to the economy in 2020. During the 2015-2016 cycle, aggressive interest cuts did not result in a significant uptick in credit growth. Bank lending was not the core driver for economic recovery in 2016. The economy only bottomed following an unprecedented issuance of local government bonds after mid-2015 (Chart 9). Chinese authorities will keep a “back door” open: even though overall tight financial regulations will remain intact, we expect the PBoC to allow a more moderate contraction in shadow banking (Chart 10). This will provide smaller banks and enterprises access to tap into bank credit. Importantly, this means the government will acquiesce to local governments in providing extra funding through shadow banking. We already see local government financing vehicles (LGFV) making a comeback in recent months. Chart 9A Chinese Version Of MMT

A Chinese Version Of MMT

A Chinese Version Of MMT

Chart 10The "Back Door" May Open Wider

The "Back Door" May Open Wider

The "Back Door" May Open Wider

Small- and medium-sized enterprises (SMEs) will benefit from lowered financing costs through the new LPR system. As we pointed out in our previous report,4 the new LPR regime is not intended as much to expand bank credit as to help struggling SMEs survive economic hardships. This, along with tax cuts, should provide SMEs some relief from capital constraints. Q. CPI has been rising sharply and is above the government’s inflation target of 3%. Will inflation prevent the PBoC from maintaining an easy monetary policy? Chart 11PBoC Likely To Capitulate To Producer Deflation

PBoC Likely To Capitulate To Producer Deflation

PBoC Likely To Capitulate To Producer Deflation

No. We think deflationary pressure in the industrial sector (measured by producer prices) poses a bigger threat to the economy, and that PBoC is more likely to loosen monetary policy than to tighten (Chart 11). Chart 12 shows that the recent surge in headline consumer prices has almost been entirely driven by soaring pork prices. There is compelling evidence from historical data that, unless core consumer price inflation also rises, climbing food prices alone will have a limited impact on PBoC policy (Chart 13). We think this approach is justified, as the necessity of “core feedthrough” is also what most central banks in the developed world look for when confronted with a detrimental supply shock. Chart 12Rising Pork Prices Have Driven Up Headline Inflation...

Rising Pork Prices Have Driven Up Headline Inflation...

Rising Pork Prices Have Driven Up Headline Inflation...

Chart 13...But Won't Be Driving Up Interest Rates

...But Won't Be Driving Up Interest Rates

...But Won't Be Driving Up Interest Rates

Chart 14A Wild Year For The RMB

A Wild Year For The RMB

A Wild Year For The RMB

Core CPI has been trending downwards since February 2018, and there is no evidence to suggest that food prices will drive up core CPI inflation (Chart 13, bottom panel). This, in combination with deflating producer prices, means that the probability of tighter monetary policy over the coming 6-9 months is extremely low. In fact, we expect, with high conviction, that the PBOC will guide the LPR lower in the coming months. Q: What is your view on the RMB for 2020? The RMB depreciated by 5% against the US dollar from its peak in February this year, mostly driven by market expectations of US tariffs imposed on Chinese export goods. Interest rate differentials, short-term capital flows, and economic fundamentals all have played much smaller roles in the RMB’s value changes (Chart 14). The depreciation in the CNY/USD this year has pushed the RMB close to two sigma below its long-term trend (Chart 15). As we expect a “Phase One” trade deal to be signed and trade tensions abating at least in the near term, the RMB will face upward pressure through the first half of 2020. The appreciation will also be supported by, although to a lesser extent, China’s improved domestic economy, rising demand for RMB-denominated assets, and a weakening US dollar (Chart 16). According to our model, the USD/CNY exchange rate can return to a 6.8-7.0 range, if a significant portion of the existing tariffs is rolled back (Chart 17). This range seems to be within the “fair value” of the RMB, justifiable by the current China-US interest rate differential (Chart 14, bottom panel). Chart 15Has The RMB Gone Too Far?

Has The RMB Gone Too Far?

Has The RMB Gone Too Far?

Chart 16Demand For RMB Assets On The Rise, Despite The Trade War

Demand For RMB Assets On The Rise, Despite The Trade War

Demand For RMB Assets On The Rise, Despite The Trade War

However, it would not be in the PBoC’s best interests to let the RMB appreciate too rapidly, because an appreciating Chinese currency would act as a deflationary force on China’s export and manufacturing sectors. The large differential in the China-US interest rates would allow PBoC to cut interest and/or RRR rates, to ease upward pressure on the RMB. Chart 17Tariff Rollbacks Will Push Up RMB

Tariff Rollbacks Will Push Up RMB

Tariff Rollbacks Will Push Up RMB

Q: How should equity investors position themselves towards China over the coming year? We are bullish on Chinese investable stocks in the next 6 to 12 months, based on our view that the Chinese economy will bottom in the first quarter next year, policy will be incrementally more supportive, and a “Phase One” trade deal will be signed soon. In the very near term, however, we think downside risks to Chinese equities are not trivial. We remain a neutral tactical stance, but will continue to watch for the following signs before upgrading our tactical call from neutral to overweight.5 Chart 18A (top panel) shows that cyclical stocks remain very depressed relative to defensives, underscoring investors’ lack of confidence in the Chinese economy and trade negotiations. A breakout in cyclicals versus defensives would signify a major improvement in investor sentiment towards Chinese economic growth. An uptick in the relative performance of industrials and consumer staples (Chart 18A, bottom panel). The negative sensitivity of industrials and positive sensitivity of consumer staples to monetary policy suggests that the relative performance between the two sectors may be a reflationary barometer for China’s economy. The relative performance trend remains off its recent low, which suggests that China’s existing policy stance has not yet turned more reflationary. A technical breakdown in the relative performance of healthcare and utility stocks (Chart 18B) would also be a bullish sign. Investable health care and utilities stocks have historically led China’s economic activity, core inflation and stock prices by 1-3 months. A technical breakdown in the relative performance of these sectors would signify that market participants anticipate a bottom in China’s economy. As we mentioned at the outset, we observed an interesting divergence in sentiment among our domestic versus global investors. This divergence is reflected in both the onshore and offshore stock markets; year to date, onshore A shares have outperformed global benchmarks by 5.6% (Chart 1, on page 1 of the report). Chart 18AWaiting For A Telltale Sign...

Waiting For A Telltale Sign...

Waiting For A Telltale Sign...

Chart 18B...Before A Tactical Upgrade

...Before A Tactical Upgrade

...Before A Tactical Upgrade

However, all of the outperformance in A shares occurred before end April, when the trade talks broke down and domestic credit expansion significantly slowed from the first quarter. Since May, the relative performance of A shares in US dollar terms has been mostly flat, reflecting the fact the markets were not expecting a significant stimulus forthcoming. Chinese investable stocks, on the other hand, have been trading heavily on the day-to-day news surrounding the trade negotiations and have significantly underperformed both domestic A shares and global benchmarks. Therefore, our base case view of a trade truce coupled with an improved Chinese economy and more supportive policy near year, warrant a cyclical overweight stance favoring Chinese investable stocks over their domestic peers. Earnings from both onshore and offshore markets will benefit from a modest improvement in economic activity, but we think the investable market will benefit more from the trade truce and more upside growth potential. Stay tuned. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1Please see Geopolitical Strategy Special Report, "Is China Afraid Of The Big Bad Warren?" dated October 25, 2019, available at gps.bcaresearch.com 2Please see China Investment Strategy Weekly Report, " Threading A Stimulus Needle (Part 1): A Reluctant PBoC," dated July 10 2019, available at cis.bcaresearch.com 3We call it a “MMT” because China’s state-owned commercial banks own approximately 80% of local government bonds. The commercial banks are essentially backed by China’s central bank, which has a fiat currency system and can make independent monetary policy decisions. 4Please see China Investment Strategy Weekly Report, "Mild Deflation Means Timid Easing," dated October 9, 2019, available at cis.bcaresearch.com 5Please see China Investment Strategy Special Report, "A Guide To Chinese Investable Equity Sector Performance," dated October 30, 2019, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

Highlights There is little risk that inflation will heat up over the next several months, … : Weak growth is more of a threat to the global economy than inflation. … which means the Fed won’t be in any hurry to take away this year’s rate cuts, … : We expect the Fed to leave the target fed funds rate alone for nearly all of 2020. … giving the economy plenty of opportunity to overheat: If trade tensions move to the back burner, and global manufacturing activity revives, the “insurance” rate cuts executed by the Fed and other central banks may turn out to have been unnecessary. The investment punch line is that accommodative monetary policy is likely to push asset prices and Treasury yields higher: Our revised Rates View Checklist supports going back to a below-benchmark duration stance over the tactical timeframe, in line with our cyclical view. Feature BCA researchers’ latest monthly view meeting opened with a discussion of whether inflation or deflation is the bigger risk to financial markets. Should investors be more concerned about signs of overheating or stalling growth? With inflation unable to get traction in any of the major economies, we all agreed that growth is the more critical unknown. An investor who gets the growth call right has the best chance of getting broad asset class positioning right, along with country, sector, duration, credit and currency tilts. While we continue to believe that there are more inflation pressures beneath the surface of the US economy than most investors realize, they are highly unlikely to manifest themselves any time soon. At today’s low-single-digit levels, inflation’s investment import is limited to its impact on monetary policy. Inflation expectations remain far below the levels that are consistent with the Fed’s inflation target (Chart 1), and the Fed is likely to keep policy easy until they adjust higher. Though it is uncertain just what levels of realized inflation, or inflation expectations, would trigger the Fed’s reaction function, we are confident that inflation will not be an issue in the coming year. Chart 1No Pressure To Remove Accommodation

No Pressure To Remove Accommodation

No Pressure To Remove Accommodation

Chart 2Global Revival Ahead?

Global Revival Ahead?

Global Revival Ahead?

We expect that global growth will surprise to the upside, pulling bond yields and risk asset prices higher. BCA’s global LEI bottomed earlier this year, and the diffusion index that leads directional moves in the LEI has turned sharply higher (Chart 2). The improvement is consistent with the easing in global financial conditions and the tentative détente in the trade war. Although we will not count on a completed “Phase I” agreement until it is signed, financial markets’ allergic reaction to trade tensions seems to have encouraged the White House to back off lest it undermine its re-election prospects. Interest Rates – Looking Back Figure 1Rates View Checklist

Refreshing Our Rates View

Refreshing Our Rates View

We rolled out our Rates View Checklist a little over a year ago to systematize our interest rate analysis and to clarify the rationale underpinning our views1 (Figure 1). Detailing the key series we monitor to anticipate the future direction of rates helps clients think along with us while giving them the chance to adapt the framework for their own purposes. As we were starting from a position of recommending below-benchmark duration, the checklist was aimed at identifying and tracking the factors that could encourage us to become more constructive about Treasury bonds. We never did warm to duration on a cyclical basis, though we did turn tactically neutral in mid-August. Part of the reason was that we did not give enough weight to events outside of the US. Highly-rated, developed-market sovereign bonds are substitutes for one another, and there is a limit to how much currency-adjusted yields can deviate across countries. Very low to negative yields in the UK, France, Germany and Switzerland have exerted a magnetic pull on Treasury yields (Chart 3), and the different sovereigns should move in tandem going forward, with currency-hedged yields observing a tight range. Chart 3Birds Of A Feather

Birds Of A Feather

Birds Of A Feather

The short end of the yield curve exerts considerable influence on rates across all maturities. Our US bond strategists’ golden rule of bond investing homes in on the deviation between actual and expected moves in the fed funds rate as the key determinant of duration positioning outcomes. Following their lead, our checklist is oriented around anticipating the Fed’s reaction to important incoming data. It seems to have done its job over the last year, highlighting the factors that drove the Fed to switch from dialing back accommodation to dialing it up. Although we never checked more than four of the eleven boxes in the checklist – Inverted Yield Curve, Sluggish Rise in Realized Inflation, Sluggish Rise in Inflation Breakevens and International Duress – those four boxes were enough to inspire the Fed’s dovish pivot. That pivot has so far encompassed three quarter-point rate cuts, pruning back the funds rate to 1.75% from 2.5%. It turns out that the key items in the checklist were the orientation of the yield curve; sluggish inflation expectations that the Fed worried could become “unanchored on the downside;” and the shadow of trade tensions that seem to have induced a global manufacturing recession, even if they have yet to infect the DM economies’ larger services sector. They tipped the scales for Fed policy and we will be especially alert to them going forward. Interest Rates – Looking Ahead Figure 2Revised Rates View Checklist

Refreshing Our Rates View

Refreshing Our Rates View

While our interpretation of the checklist left something to be desired, we are convinced that the checklist approach is sound. We return to its framework for insight into the current rates outlook, after making a few tweaks to shore it up (Figure 2). Starting with Fed perceptions, there is still some daylight between our fed funds rate expectations and the market’s, as we think the Fed is done cutting, while the money market assigns a high probability to the possibility of one more cut (Chart 4). The combination of rate cuts and the rally in 10-year Treasury yields got the yield curve back to its typical upward-sloping orientation in October (Chart 5), so we can now uncheck the inverted curve box. We see the five-month inversion as a reason to be more vigilant, but given the unusually negative term premium, we are not treating it as a hard-and-fast sign of looming weakness. The money market has priced out all but one more rate cut, and the yield curve is no longer inverted, suggesting that recession fears are abating. Chart 4Looking For One More Cut

Looking For One More Cut

Looking For One More Cut

Chart 5The Curve Is No Longer Inverted

The Curve Is No Longer Inverted

The Curve Is No Longer Inverted

Chart 6Inflation Is Muted, ...

Inflation Is Muted, ...

Inflation Is Muted, ...

We continue to check both of the sluggish inflation boxes. Realized inflation measures, headline and core, have slumped (Chart 6), and below-target inflation expectations remain a hot-button concern, judging by Fed speakers’ repeated references to them. The Fed has strapped itself to the mast with all its talk about inflation expectations, and it will not begin removing accommodation until inflation expectations revive. We cannot directly observe the output gap, but nearly 3% growth in 2018, and a rip-roaring labor market, offer solid evidence that it has closed and we leave its box unchecked. Labor market indicators unanimously point to the conclusion that monetary accommodation is not necessary. The unemployment rate is a full percentage point below the Fed’s and the CBO’s estimates of NAIRU. Ancillary indicators like the broader definition of unemployment including discouraged workers and involuntary part-time workers (Chart 7, top panel), and the openings (Chart 7, middle panel) and quits rates (Chart 7, bottom panel) from the JOLTS survey, testify to an extremely tight labor market. We expect that the pause in wage acceleration will prove temporary (Chart 8). Chart 7... Despite A Red-Hot Labor Market

... Despite A Red-Hot Labor Market

... Despite A Red-Hot Labor Market

Chart 8Wage Gains Will Pick Up Again

Wage Gains Will Pick Up Again

Wage Gains Will Pick Up Again

Chart 9No Overheating In The Real Economy

No Overheating In The Real Economy

No Overheating In The Real Economy

With cyclical spending well short of past business cycle peaks (Chart 9), the real economy isn’t exerting any pressure on the Fed to intervene to choke off the expansion. (Although a modest pace of Fed hikes would support below-benchmark duration positioning, aggressive tightening to cut off overheating leads to recessions, and would favor long-maturity Treasuries.) We have removed the financial sector imbalances box because there has been no apparent follow through from Governor Brainard’s speech last September, which appeared to set the stage for tightening on the basis of frothy credit conditions. We maintain the international duress box, which is meant to alert us to an overseas crisis or near-crisis that could spark a flight to quality that depresses Treasury yields and/or inspires the Fed to pursue easier policy in an attempt to stave off contagion risks. Green shoots in manufact-uring, here and abroad, support the idea that growth outside the U.S. could be poised to accelerate. Chart 10Global Manufacturing Is Coming Back ...

chart 10

Global Manufacturing Is Coming Back ...

Global Manufacturing Is Coming Back ...

Chart 11... And US Manufacturing May Have Bottomed

... And US Manufacturing May Have Bottomed

... And US Manufacturing May Have Bottomed

We add “Flagging Global Growth” to address the global growth blind spot that undermined our call last year. Our US Bond Strategy colleagues find that the Global Manufacturing PMI, the US ISM Manufacturing PMI and the CRB Raw Industrials Index are the global growth measures that exert the strongest influence on Treasury yields. The Global Manufacturing PMI has risen off its lows over the last three months and is within striking distance of getting back above the 50 contraction/expansion line, led by the US2 and China (Chart 10). The outlook for the US ISM Manufacturing PMI looks good on several counts. First, the comparatively modest manufacturing sector tends to move with the much larger services sector, and the sharp bounce in the Services PMI bodes well for the Manufacturing PMI (Chart 11, top panel). Within the manufacturing survey, New Export Orders’ leap back over 50 suggests that the global economy may have already seen the worst of the manufacturing weakness that has swept the rest of the world (Chart 11, bottom panel). The jury is still out on the CRB Raw Industrials-to-gold ratio (Chart 12, top panel), as industrial commodity prices have yet to show any spunk (Chart 12, bottom panel). Chart 12Commodities Have Yet To Turn

Commodities Have Yet To Turn

Commodities Have Yet To Turn

Chart 13A Weaker Dollar Would Support Higher Rates

A Weaker Dollar Would Support Higher Rates

A Weaker Dollar Would Support Higher Rates

With our trio of indicators mixed-to-positive on balance, we leave the global growth box unchecked. We have also added a dollar box to monitor when Treasury yields are drifting out of alignment with other sovereign yields. If the dollar and Treasury yields rise together, we would view the rise in yields as suspect and at risk of being reversed.3 There doesn’t appear to be any decoupling pressure now, as Treasury yields have risen while the dollar has bumped around in a narrow range (Chart 13, top panel), and bullish sentiment toward the dollar has cooled off, pointing the way to a currency-approved path to higher yields (Chart 13, bottom panel). Bottom Line: We check only two of the boxes in our revised rates checklist (Figure 2), supporting a below-benchmark duration stance. Investment Implications Like all investors, we hate to get anything wrong. We were wrong on rates, though, failing to see the potential for the 10-year Treasury yield to fall to 1.5%. The duration miss undermined results within the fixed income sleeve of our recommendations, as we didn’t take it off until the 10-year Treasury yield had fallen to 1.74% .4 We have modified our rates checklist to force ourselves to be more aware of the world beyond the US, but the available data still support below-benchmark duration positioning, and we now recommend going back to it over the tactical (0-3-month) timeframe. The date when monetary policy turns restrictive has been pushed out, and so have the dates when the bull markets in risk assets will end. We note that our overall asset allocation calls have performed well. Since we upgraded equities in our first 2019 report,5 the S&P 500 Total Return Index has gained 24% while our Treasury underweight, as proxied by the Bloomberg Barclays US Treasury Total Return Index, is up 7% (Chart 14, top panel). Since we upgraded spread product in late January,6 the Bloomberg Barclays US Corporate Investment Grade and High Yield Total Return Indexes are up 12% and 8%, respectively, versus the Treasury Index’s 7% (Chart 14, bottom panel). Chart 14Underweighting Treasuries Has Been The Way To Go

Underweighting Treasuries Has Been The Way To Go

Underweighting Treasuries Has Been The Way To Go

The run-up to the Fed’s series of mid-cycle rate cuts doomed our duration call, but it has fortified the case for overweighting equities and spread product. We still expect the expansion, the equity bull market, and spread product’s long period of generating excess returns to die at the hands of the Fed. Now that the date when monetary policy settings become restrictive has been indefinitely delayed, the end-dates of the equity and credit bull markets have as well. We continue to recommend overweighting equities and spread product, and underweighting Treasuries. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the September 17, 2018 US Investment Strategy Weekly Report, “What Would It Take To Change Our Bearish Rates View?” available at usis.bcaresearch.com. 2 The Global PMI is compiled from Markit’s individual country PMIs, so the chart shows the Markit US PMI instead of the more familiar ISM measure. 3 It the dollar were to rise significantly while Treasury yields rose faster than other DM sovereign yields, currency-adjusted Treasury yields would decouple from peer yields and arbitrage activity would likely bring them back down. 4 Please see the August 12, 2019 US Investment Strategy Weekly Report, “When The Facts Change,” available at usis.bcaresearch.com. 5 Please see the January 7, 2019 US Investment Strategy Weekly Report, “What Now?” available at usis.bcaresearch.com. 6 Please see the January 28, 2019 US Investment Strategy Weekly Report, “Double Breaker,” available at usis.bcaresearch.com.

Highlights Duration: A survey of the five factors that determine the path for Treasury yields suggests that further upside is likely. We see a clear path to 2.5% for long-maturity Treasury yields as recessionary risk moves to the back burner in the coming months. Credit Cycle: C&I lending standards tightened on net in the third quarter of 2019. But other indicators of monetary conditions point to continued accommodation. We expect lending standards will soon move back into “net easing” territory. Remain overweight Spread Product versus Treasuries. IG Valuation: Investment grade corporate bond spreads for all credit tiers are now below our fair value targets. We recommend only a neutral allocation to the sector. Investors should prefer high-yield bonds, where spreads are more attractive, and Agency MBS, which offer competitive expected returns and much less risk. Feature Chart 1Recession Risk Getting Priced Out

Recession Risk Getting Priced Out

Recession Risk Getting Priced Out

The bond sell-off continued last week, driven by positive developments in US/China trade negotiations and tentative signs of stabilization in some global growth indicators. The renewed sense of economic optimism has reduced the recessionary risk priced into bond markets. The 2/10 Treasury slope has steepened 30 bps since it briefly inverted in late August. During that same period, the 2-year Treasury yield is up 15 bps, the 10-year yield is up 45 bps and the Bloomberg Barclays Treasury index has underperformed a position in cash by 2.7% (Chart 1). These recent developments raise two important questions. First, should investors chase or fade the back-up in Treasury yields? And second, if the sell-off does continue, how high can yields go? To answer these questions we turn to the five macro factors that drive trends in US bond yields. These factors were outlined in our “Bond Kitchen” report from last April, and are listed right here:1 Global growth Policy uncertainty The US dollar The output gap Sentiment Back In The Kitchen Global Growth Chart 2CRB Index Needs To Rebound

CRB Index Needs To Rebound

CRB Index Needs To Rebound

Three global growth indicators are particularly relevant for US Treasury yields. They are the Global Manufacturing PMI, the US ISM Manufacturing PMI and the CRB Raw Industrials index. The latter is especially useful because it updates on a daily basis. Considering the CRB index, we notice that, while it is no longer in a steep downtrend, it has also not rebounded alongside the jump in bond yields (Chart 2). This should give us pause. Continued low readings from the CRB index make it more likely that bond yields will fall back in the coming weeks. We should also note that the ratio between the CRB index and Gold is more highly correlated with the 10-year Treasury yield than the CRB index itself.2 This ratio has bounced off its lows (Chart 2, top panel), but only because Gold has come under downward pressure. With the Fed committed to maintaining an accommodative policy stance until inflation expectations are re-anchored, we expect the Gold price to remain well bid. This means that raw industrials prices must rebound to keep the ratio trending higher. The CRB/Gold ratio has bounced off its lows, but only because Gold has come under downward pressure. More encouraging than the CRB index is the Global Manufacturing PMI, which has moved off its lows during the past three months (Chart 3). The increase has been partially driven by stronger US readings (Chart 3, panel 2), but principally by a significant jump in China’s PMI (Chart 3, bottom panel). Chart 3China Pulling The Global Manufacturing PMI Higher

China Pulling The Global Manufacturing PMI Higher

China Pulling The Global Manufacturing PMI Higher

Somewhat stronger China PMI readings should be expected, given the rebound in our China Investment Strategy’s Li Keqiang Leading Indicator – a composite measure of monetary conditions, money and credit growth (Chart 4).3 We should also expect further modest policy stimulus from China, as long as the labor market remains under pressure (Chart 4, bottom panel). Turning to the US, we have seen three very positive developments in the economic data during the past month. First, the ISM Services PMI jumped from 52.6 to 54.7 in October (Chart 5). A drop in this index to 50 or below would be consistent with a US recession, while the combination of a strong service sector and a depressed manufacturing sector is consistent with our baseline 2015/16 roadmap. This roadmap leads to an eventual rebound in the manufacturing index. Second, the ISM Manufacturing PMI rose a tad in October, but the New Export Orders component jumped significantly from 41 to 50.4 (Chart 5, panel 2). Since the global slowdown began as a non-US phenomenon, a rebound in this export component sends a strong signal that we are at an inflection point. Finally, consumer confidence rose in October following a sharp decline in September. A year-over-year decline in the consumer confidence index is a reasonably strong recession signal, but recent data suggest that this signal is fading (Chart 5, bottom panel). Chart 4Modest Stimulus In China

Modest Stimulus In China

Modest Stimulus In China

Chart 5Three Positive Developments

Three Positive Developments

Three Positive Developments

All in all, the global growth data have turned more positive during the past month. US indicators, in particular, are no longer sending strong recessionary signals. A rebound in the CRB Raw Industrials index would give us more confidence in the durability of the recent rise in Treasury yields. Policy Uncertainty Uncertainty about the US/China trade conflict has eased considerably during the past few weeks, as the two sides appear to be working toward a “phase 1” deal that would prevent the imposition of new tariffs and roll back some that are already in place. Heightened uncertainty about the trade war played a large role in dragging bond yields lower in 2019. This becomes apparent when you notice that survey and sentiment (aka “soft”) data about the economic outlook have been significantly worse than the actual “hard” data on US economic activity.4 It is clear that negative sentiment about the trade war has held survey data and bond yields down, even as underlying US economic activity has been solid. Less bullish dollar sentiment supports a continued uptrend in Treasury yields. We see a continued easing of trade tensions as we head into the first half of next year. President Trump has an incentive to support the economy in an election year, given the historical record of incumbent presidents being re-elected when the economy is strong. However, if this strategy doesn’t work and Trump finds himself behind in the polls by the end of next summer, then he could decide that ramping up the trade war again is the best course of action. In other words, another spike in policy uncertainty in the second half of 2020 is possible if President Trump is trailing in the polls. The US Dollar Chart 6Dollar Sentiment Points To Higher Yields

Dollar Sentiment Points To Higher Yields

Dollar Sentiment Points To Higher Yields

The US dollar is important for the path of US Treasury yields because it signals whether US yields are decoupling from yields in the rest of the world. In other words, if the dollar appreciates significantly alongside rising Treasury yields, then we should view those yields as increasingly out of step with the rest of the world, and thus more likely to fall back down. So far, the dollar has been relatively flat as yields have risen and bullish sentiment toward the US dollar has declined significantly (Chart 6). Less bullish dollar sentiment supports a continued uptrend in Treasury yields. But if yields do in fact continue to rise, it will be important to watch the dollar’s reaction. The Output Gap Chart 7Wage Gains Hurting Margins, Not Raising Prices

Wage Gains Hurting Margins, Not Raising Prices

Wage Gains Hurting Margins, Not Raising Prices

Some sense of the output gap is important for forecasting bond yields. This is because the same amount of global growth will lead to more inflationary pressure and higher bond yields when the output gap is small than when it is large. The fact that the output gap is smaller now than it was in 2016 is probably the reason why the 10-year Treasury yield bottomed 10 bps above its 2016 trough this year, and why the average Treasury index yield bottomed 47 bps above its 2016 trough. We have found wage growth to be an excellent indicator of the output gap, and noted in a recent report that wage growth should continue to accelerate.5 In this vein, another crucial variable to monitor is labor compensation as a percent of national income (Chart 7). The rise in this series indicates that wage gains during the past few years have come at the expense of corporate profit margins, and have not been passed through to higher consumer prices. If this series proves to have a lot more cyclical upside, then it could be some time before wage acceleration translates to higher inflation. Sentiment Chart 8Surprise Index Says Sentiment Is Neutral

Surprise Index Says Sentiment Is Neutral

Surprise Index Says Sentiment Is Neutral

The final factor we consider when forecasting US Treasury yields is sentiment. We have found that the Economic Surprise Index is the single best measure of aggregate market sentiment. That is, when the Surprise index reaches a positive or negative extreme, it usually means that sentiment is too positive or too negative, and will mean-revert in the months ahead. Also, we have observed a strong correlation between the Surprise index and changes in Treasury yields (Chart 8). At present, the Surprise index is roughly neutral, and therefore does not send a strong signal about where sentiment might push bond yields during the next few months. Investment Conclusions To summarize, the outlook from our five macro factors suggests that Treasury yields will rise further in the coming months. Global growth indicators are showing tentative signs of bottoming, and should rise to levels more consistent with the “hard” economic data as policy uncertainty continues to wane. The fact that the US economic data look less recessionary than they did one month ago makes us more confident that our global indicators will rebound. Chart 9A Clear Path To 2.5%

A Clear Path To 2.5%

A Clear Path To 2.5%

We would become concerned about a renewed downtick in yields if the CRB Raw Industrials index fails to rebound, or if the dollar strengthens significantly in the coming weeks. At the beginning of this report, we asked how high Treasury yields can go if the global growth rebound proves durable. To answer that question we refer to current estimates of the long-run neutral fed funds rate. The FOMC’s median estimate of the long-run neutral fed funds rate is 2.5% and the median estimate from the New York Fed’s Survey of Market Participants is 2.48%, with an interquartile range of 2.25% - 2.5%. If recessionary fears move to the back burner, it would be logical for long-dated yields to converge toward those levels. That is in fact what happened in recent years, with the 5-year/5-year forward Treasury yield peaking several times at levels close to the Fed’s median neutral rate estimate (Chart 9). With this in mind, we see a clear path to 2.5% on the 5-year/5-year forward Treasury yield, with the 10-year yield reaching similar levels since the 5/10 Treasury slope is likely to remain flat (Chart 9, bottom panel). For yields to eventually move above 2.5%, the market would have to re-consider its outlook for the long-run neutral fed funds rate. We discussed what factors to monitor in this regard in a recent report.6 Bottom Line: Treasury yields have moved significantly higher in recent weeks, but a survey of the five factors that determine the path for Treasury yields suggests that further upside is likely. We see a clear path to 2.5% for long-maturity Treasury yields as recessionary risk moves to the back burner in the coming months. Checking In On The Credit Cycle In previous reports, we mentioned that three factors drive our view of corporate bond spreads and the credit cycle: Balance sheet health Monetary conditions Valuation We last presented a detailed examination of these factors in a report from mid-September, concluding that accommodative monetary conditions will support corporate bond excess returns, despite deteriorating balance sheet health.7 Three factors drive our view of corporate bond spreads and the credit cycle: Balance sheet health, monetary conditions,and valuation. But since then, C&I lending standards – an important indicator of monetary conditions – moved into “net tightening” territory for the third quarter of 2019 (Chart 10). Tightening C&I lending standards, if they persist, would put significant upward pressure on corporate defaults and credit spreads. Chart 10Credit Cycle Checklist: Monetary Conditions

Credit Cycle Checklist: Monetary Conditions

Credit Cycle Checklist: Monetary Conditions

While the recent move in lending standards is concerning, we expect it to reverse in the near future. The yield curve, another indicator of monetary conditions, has steepened in recent months, suggesting that conditions are becoming more accommodative. Also, loan officers reported that the terms on C&I loans continued to ease in Q3, even as overall standards tightened (Chart 10, panel 3). Most importantly, inflation expectations remain extremely low (Chart 10, bottom panel). This gives the Fed every incentive to maintain accommodative monetary conditions. This should give lenders the confidence to ease lending standards, leading to tight credit spreads and a low corporate default rate. Bottom Line: C&I lending standards tightened on net in the third quarter of 2019. But other indicators of monetary conditions point to continued accommodation. We expect lending standards will soon move back into “net easing” territory. Remain overweight Spread Product versus Treasuries. Downgrade Investment Grade Corporates To Neutral Last week, we downgraded our recommended allocation to investment grade corporate bonds from overweight to neutral.8 We maintain a positive view of the credit cycle, and expect that corporate bonds will continue to outperform Treasuries. However, investment grade corporate spreads no longer provide adequate compensation for their level of risk. We maintain an overweight allocation to high-yield corporates, where spreads remain attractive. Chart 11 shows that investment grade corporate spreads have tightened somewhat in recent months, but that they remain well above the tights seen in early 2018. However, the chart also shows that average index duration has increased considerably this year. All else equal, higher index duration justifies a wider spread. In contrast, notice that high-yield index duration fell this year (Chart 11, bottom panel). This is because high-yield bonds usually carry embedded call options, making them negatively convex. All else equal, lower index duration makes the spread offered by the high-yield index more attractive. Because changes in spread and duration are both important, we prefer to use the 12-month breakeven spread as our main valuation tool. This measure is the spread widening required on a 12-month investment horizon to underperform a duration-matched position in Treasuries. It can be approximated by dividing the option-adjusted spread by duration. Chart 12 shows investment grade 12-month breakeven spreads as a percentile rank since 1995. The overall message is that spreads have rarely been lower. Chart 11Higher Durations Makes IG Spreads Look Too Tight

Higher Durations Makes IG Spreads Look Too Tight

Higher Durations Makes IG Spreads Look Too Tight

Chart 12Investment Grade Corporate Spreads Have Rarely Been Lower

Investment Grade Corporate Spreads Have Rarely Been Lower

Investment Grade Corporate Spreads Have Rarely Been Lower

Finally, we can also recognize that spreads tend to be tight in the middle and late stages of the credit cycle. In the current environment, that means we should expect spreads to be near the bottom of their historical ranges. To control for this fact, we re-calculate our breakeven spread percentile ranks using only mid-cycle periods when the slope of the yield curve is between 0 bps and 50 bps. We can then back-out spread targets for each credit tier based on the median 12-month breakeven spreads seen in similar macro environments. Chart 13 shows that spreads for all investment grade credit tiers have moved below our targets. High-yield spreads are not shown, but they remain well above target levels.9 Chart 13Spreads For All IG Credit Tiers Are Below Target

Spreads For All IG Credit Tiers Are Below Target

Spreads For All IG Credit Tiers Are Below Target

In place of investment grade corporates, which have become expensive, we recommend upgrading Agency MBS. MBS now offer expected returns that are comparable with corporate bonds rated A or higher, with considerably less risk.10 Bottom Line: Investment grade corporate bond spreads for all credit tiers are now below our fair value targets. We recommend only a neutral allocation to the sector. Investors should prefer high-yield bonds, where spreads are more attractive, and Agency MBS, which offer competitive expected returns and much less risk. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “Bond Kitchen”, dated April 9, 2019, available at usbs.bcaresearch.com 2 For details on why the ratio between the CRB Raw Industrials index and Gold tracks the 10-year Treasury yield please see US Bond Strategy Portfolio Allocation Summary, “The Sequence Of Reflation”, dated March 5, 2019, available at usbs.bcaresearch.com 3 Please see China Investment Strategy Special Report, “The Data Lab: Testing The Predictability Of China’s Business Cycle”, dated November 30, 2017, available at cis.bcaresearch.com 4 For more details on the divergence between “soft” and “hard” data please see US Bond Strategy Weekly Report, “Crisis Of Confidence”, dated October 22, 2019, available at usbs.bcaresearch.com 5 Please see US Bond Strategy Weekly Report, “Position For Modest Curve Steepening”, dated October 29, 2019, available at usbs.bcaresearch.com 6 Please see US Bond Strategy Weekly Report, “Position For Modest Curve Steepening”, dated October 29, 2019, available at usbs.bcaresearch.com 7 Please see US Bond Strategy Weekly Report, “Corporate Bond Investors Should Not Fight The Fed”, dated September 17, 2019, available at usbs.bcaresearch.com 8 Please see US Bond Strategy Portfolio Allocation Summary, “The Fed Will Stay Supportive”, dated November 5, 2019, available at usbs.bcaresearch.com 9 For details on how we calculate our spread targets please see US Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 10 For more details on the positive outlook for MBS please see US Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights All the steps in the earnings dance are well known: Company management teams guide Wall Street analysts to lower their expectations in the weeks leading up to the beginning of earnings season, and their companies’ results then comfortably clear the lowered bar. Given the lack of true suspense, the S&P 500 largely ignores quarterly results: In the near term, moves in the S&P 500 have little to no relationship with either earnings growth or the magnitude of earnings beats. Over time, however, index prices and earnings move together: If earnings multiples mean-revert, earnings and prices have to converge over the long run. The equity bull market isn’t finished yet: The monetary policy backdrop will support earnings growth well into 2021, though it will not promote multiple expansion for much more than a year. Feature Chart 1We've Seen This Movie Before

Why Bother With Earnings?

Why Bother With Earnings?

Taking a turn chairing BCA’s daily meeting last week, we duly updated our colleagues on the progress of earnings season. At the time, over 75% of the S&P 500’s constituents had reported, and the index was on its way to surpassing consensus analyst expectations by a few percentage points. We then showed charts tracking the course of expectations across each of this year’s three quarters to show that the “surprise” wasn’t actually very surprising (Chart 1). We included the charts to add a bit of levity, but a fellow strategist asked an incisive question: If earnings season follows the same pattern every quarter, why pay attention to it at all? Earnings season surely has its elements of Kabuki theater, but earnings are the fundamental basis for purchasing an ownership stake in a company. A share of stock is a claim on a company’s aggregate future earnings. To the extent that quarterly earnings reports provide a window into the trajectory of a company’s future earnings path, they contain relevant information about the fair value of its shares. Quarterly earnings offer more insight at the individual stock level than at the index level, as individual stocks are subject to idiosyncratic factors, while index earnings tend to reflect overall economic performance, and we therefore view them as a check on the other real-time indicators we examine to gauge the health of the economy. A review of how S&P 500 prices interact with S&P 500 earnings suggests that earnings have little to no impact on near-term index performance. They do move together in the long term, though, as they must if earnings multiples are a mean-reverting series. In the near term, when multiples are oscillating, anticipating stock market moves is a function of anticipating earnings growth and swings in multiples, which move independently of one another. The fed funds rate cycle has historically provided a good high-level guide to earnings and multiples trends. S&P 500 Performance During Earnings Season To test the S&P 500’s sensitivity to earnings surprises, we dug through weekly earnings updates going back to the beginning of 2012 (4Q11 earnings season) to compare expected index earnings per share (EPS) with reported index EPS.1 I/B/E/S has long been recognized as the earnings-estimates authority, so we use its estimates in conjunction with its compilation of reported earnings to ensure our analysis really is apples-for-apples.2 We track S&P 500 performance in three-month segments, beginning with the Monday following the second Friday of the new quarter, since that is the week that the banks typically get earnings season rolling. Earnings beats are stable and predictable, but the S&P 500's reaction to them is anything but. The empirical record over the last 31 quarters supports our colleague’s intuition. Over the 13 weeks following the major banks’ releases, S&P 500 performance exhibits no consistent link with earnings surprises (Chart 2). The best-fit line through a simple scatterplot shows that the relationship, such as it is, has been inverse and weak (Chart 3). The link with the year-over-year change in S&P 500 earnings is even weaker (Charts 4 and 5). Chart 2Earnings Surprises Don't Move The S&P 500 …

Why Bother With Earnings?

Why Bother With Earnings?

Chart 3… Which Is Slightly Negatively Correlated With Them

Why Bother With Earnings?

Why Bother With Earnings?

Chart 4Earnings Growth Doesn't Move The S&P 500 …

Why Bother With Earnings?

Why Bother With Earnings?

Chart 5… Which Has No Short-Term Relationship With It

Why Bother With Earnings?

Why Bother With Earnings?

Earnings data support our colleague’s contention that earnings season, at least as it relates to expectations, is something of a charade. Companies, which heavily influence analyst estimates with their guidance, have beaten expectations every quarter for at least eight years. As Charts 2 and 3 show, earnings beat expectations by an average of 3.7%, nearly the midpoint of the 1-6% range. The S&P 500 shouldn’t be expected to react to “surprises” that are more or less pre-ordained. Bottom Line: Earnings season has no observable impact on the S&P 500. Earnings attract a lot of attention, but they do not influence index-level performance in the near term. The S&P 500 And Earnings Over Longer Periods Anything can happen over short periods, but stock prices have to track earnings over the long term. If the idea that an ownership share represents a proportional stake in company earnings is too abstract, consider the equity equation. Equity prices, P, can be viewed as the product of earnings, E, and the multiple investors are willing to pay for each dollar of earnings, P/E. P = E * (P/E) The market P/E ratio is subject to mean reversion, making changes in earnings the key long-term driver of S&P 500 performance. Since 1966, the S&P 500 index (Chart 6, top panel) has appreciated at the same rate as its trailing four-quarter operating earnings (Chart 6, middle panel), given that its trailing multiple is not far from where it started (Chart 6, bottom panel). Growth in forward earnings expectations (Chart 7, middle panel) has lagged S&P 500 growth (Chart 7, top panel) since expectations data began to be compiled in 1979 because the forward multiple has more than doubled from late ‘70s trough levels (Chart 7, bottom panel). In any extended period not bookended by an outlier multiple, however, one should expect S&P 500 appreciation to track earnings estimate growth. Chart 6S&P 500 Earnings And Prices Will Converge Over Time ...

S&P 500 Earnings And Prices Will Converge Over Time ...

S&P 500 Earnings And Prices Will Converge Over Time ...

Chart 7... As Long As The Starting Or Ending Multiple Isn't An Outlier

... As Long As The Starting Or Ending Multiple Isn't An Outlier

... As Long As The Starting Or Ending Multiple Isn't An Outlier

Bottom Line: Stock price gains and earnings growth will converge over the long run as long as the earnings multiple mean-reverts. Earnings do matter in the long run. Where Do We Go From Here? There are several earnings growth models within BCA. Like all regression models, they often work well in stretches, but are susceptible to unanticipated inflections and changes in correlations. Since the crisis, the difference between year-over-year growth in industrial production and year-over-year growth in the money supply has aligned closely with earnings growth (Chart 8). If we (and global equity markets) are correct in sniffing out a bottoming in global manufacturing activity, and loan growth is unlikely to accelerate much as banks are pulling in their horns in commercial real estate and selected consumer categories, earnings growth could pull out of its funk. Chart 8Earnings Growth Will Revive Once Global Manufacturing Pressure Abates

Earnings Growth Will Revive Once Global Manufacturing Pressure Abates

Earnings Growth Will Revive Once Global Manufacturing Pressure Abates

We have found that earnings growth and multiple re-rating or de-rating is reliably influenced by the monetary policy backdrop. While the level of the fed funds rate goes a long way to explaining overall index moves, earnings growth and multiple expansion/compression are a function of its direction. Broadly, forward estimates grow at a rapid rate when the Fed is hiking rates (the economy is expanding) and slump when it’s cutting them (the economy needs a hand). Forward multiples are the mirror image of earnings estimates, contracting when the Fed is hiking and expanding at a robust clip when the Fed is cutting. Earnings grow at a rapid clip when the Fed is leaning against a too-strong economy, but they slump when the Fed is trying to nurse it back to health. Viewed through the lens of the fed funds rate cycle (Figure 1), policy had been in Phase I from December 2015, when the Fed began hiking rates, until the end of July, when the Fed began cutting, transitioning into Phase IV. Phase IV has been characterized by solid multiple expansion and, ex-2008-9, decent earnings growth. It will remain in force until the Fed returns to hiking rates, which we do not expect until the second half of 2020 at the earliest. Once the Fed does resume hiking, it will likely take some time for it to raise the fed funds rate above its equilibrium level (Phase II). Figure 1The Fed Funds Rate Cycle

Why Bother With Earnings?

Why Bother With Earnings?

Our base case is that the Fed will not turn restrictive until 2021. Easy monetary policy is a tailwind for earnings growth, which remains strong in Phase II, so we expect that earnings growth will shake loose of 2019’s doldrums across the next two years. Stocks should benefit from re-rating until the Fed resumes hiking rates (Phase I), cutting off multiple expansion. They will de-rate once monetary policy becomes restrictive (Phase II), as it must once the Fed perceives a need to cool the economy. The bottom line is that the monetary policy backdrop should be earnings-friendly well into 2021, even if multiple expansion isn’t likely to persist beyond the next nine to twelve months. Investment Implications Investors should not look to quarterly earnings reports to inform asset allocation decisions. Quarterly releases may be telling for individual companies’ longer-run profit potential, but they do not shed much light on the S&P 500’s future earnings. The long-run index earnings profile is much more likely to be influenced by broad themes than real-time data points. We devote our focus to the cyclical forces affecting asset-class-level returns, and find that the monetary policy cycle offers useful insight into future moves in earnings and multiples. The Fed's dovish pivot will help keep the expansion going, ... That insight is favorable for equities, and for spread product as well. We are in the latter stages of both the business cycle and the credit cycle, but new injections of monetary accommodation and the postponement of the shift to restrictive monetary policy settings will extend the longevity of the expansion and the period over which credit generates positive excess returns. Investors have different objectives and risk tolerances, but we think all of them should remain at least equal weight equities in balanced portfolios, and overweight spread product (and underweight Treasuries) within fixed-income sleeves. It is too soon to de-risk investment portfolios. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 All data cited in this section comes from Refinitiv’s (formerly Thomson Reuters’) This Week in Earnings publication. 2 Earnings estimates compiled by other vendors may differ from I/B/E/S estimates, and other measures of reported earnings, like Standard & Poor’s, regularly diverge from I/B/E/S’.

Highlights Maintaining an adequate level of aggregate demand has proven to be one of the biggest macroeconomic challenges of the modern era. Yet, in principle, it should not be difficult to increase demand. After all, people like to consume. If households are not spending enough, governments can just give them money or increase spending directly on public infrastructure and other worthwhile endeavors. Various explanations have been proposed for why these solutions either won’t work or are bad ideas even if they do work. These include Ricardian Equivalence-type arguments; claims that periods of high unemployment may be necessary to cleanse financial and economic imbalances; and concerns about excessive levels of government debt. None of these explanations are particularly persuasive, which suggests that politics, rather than economics, may be at the heart of the demand-side secular stagnation problem. Bondholders benefit from low inflation, which has often led them to oppose meaningful fiscal stimulus. Looking out, the influence of bondholders is likely to wane as populism proliferates. Investors should favor “real assets” such as equities, real estate, and commodities over “nominal assets” such as bonds and cash. A Rather Peculiar Problem Some problems are hard to solve. Curing cancer is hard. Reconciling quantum mechanics with general relativity is hard. But why should getting people to spend more be so difficult? After all, people like to consume. It is getting them to save that should be challenging. And yet, the most pressing macroeconomic problem in many countries over the past decade (and much longer in Japan) has been generating enough spending to achieve full employment, which is a precondition for allowing central banks to move away from extreme measures such as quantitative easing and negative rates. It would be one thing if secular stagnation were primarily a problem of inadequate supply. Increasing supply is difficult. While some economists such as Robert Gordon have focused on the poor prospects for potential GDP growth in developed economies (sluggish productivity and labor force growth being among the key culprits), the Larry Summers characterization of secular stagnation is first and foremost about inadequate demand. If people are not spending enough, why can’t the government simply increase transfers to households or spend money directly on public infrastructure, scientific exploration, or other worthwhile endeavors? Three arguments have been advanced as to why this strategy either will not work or is a bad idea even if it does work: 1) Ricardian Equivalence-type theories claiming that the private sector will increase savings by enough to counter larger budget deficits, thus leaving overall demand unchanged; 2) claims that periods of high unemployment are both necessary and desirable for shifting resources to more productive uses; and 3) concerns that higher government debt levels stemming from larger budget deficits will impose long-term costs that swamp the short-term growth benefits of fiscal stimulus. As we discuss below, none of these arguments are particularly persuasive. This suggests that politics, rather than economics, explains why there has been so much reluctance towards fiscal easing. Ricardian Equivalence Ricardian Equivalence stipulates that the lifetime present value of after-tax income determines household consumption. This implies that if a government issues each person a check for $1 million, everybody will just save the money in anticipation of higher taxes down the road. If that sounds a tad implausible, this is because the theory assumes, among other things, that everyone is perfectly rational, can borrow as much as they want, and lives forever (or at least values their heirs’ or beneficiaries’ welfare as much as their own). The theory is even less convincing when applied to government spending. Only in the extreme scenario where the government permanently increases spending would rational, infinitely-lived households cut their spending by exactly enough to offset the rise in government expenditures. If the increase in government spending were perceived to be temporary, aggregate demand would still rise, even if everyone is completely rational. To see this, consider a case where the government increases spending by $1 billion per year for three years. The “rational” response would be for households to cut their own expenditures by the annual carrying cost of the additional $3 billion in debt. Assuming an interest rate of 2%, this would amount to a reduction in annual consumption of about $60 million, leaving a net annual fiscal boost of $940 billion. The example above almost certainly overstates the negative impact on consumption in situations where the economy is operating below potential. This is because raising government spending in a depressed economy will boost output, thus increasing the present value of lifetime incomes. The expectation of higher income will lift consumption. The bottom line is that Ricardian Equivalence applies only in a very narrow range of circumstances, none of which are relevant in the real world. Indeed, as Box 1 discusses, the empirical evidence clearly suggests that fiscal multipliers are positive, especially in economies grappling with high unemployment. The Urge To Purge One popular view, often associated with the Austrian School of economics, is that recessions cleanse the economy and the financial system of excesses, paving the way for faster growth. The main problem with this view is that it assumes that resources will only shift to more worthwhile uses if many people are unemployed. In practice, this is not the case. In any given month, about five million US workers will either quit or lose their job, while a slightly higher number will find new work (Chart 1). Chart 1Labor Market Churn Tends To Increase As Unemployment Falls

Labor Market Churn Tends To Increase As Unemployment Falls

Labor Market Churn Tends To Increase As Unemployment Falls

Chart 2Residential Construction Accounted For Only 20% Of The Job Losses During The Great Recession

Secular Stagnation: The Easiest Problem In The World?

Secular Stagnation: The Easiest Problem In The World?

The small difference between gross inflows and outflows is the net change in employment. This is the number investors focus on every month when the payroll report is released; it is usually less than 5% of gross flows. Strikingly, gross separations usually rise when the unemployment rate falls, implying that labor market churn increases when the economy strengthens. This occurs because more people tend to quit their jobs when the labor market is tight and job openings are plentiful. The pro-cyclicality of the quits rate dominates the counter-cyclicality of the discharge rate. The Great Recession demonstrated that most of the job losses during severe downturns are gratuitous in the sense that they impose needless suffering on workers without making the economy more productive. Chart 2 shows that only 20% of US job losses between 2007 and 2009 took place in the residential building sector and related financial activities where excesses were plainly evident. The rest of the losses were in parts of the economy that had little to do with the housing bubble. Too Much Debt? Opponents of loose fiscal policy often point to rising government debt levels as an unwelcome side effect of larger budget deficits. Worries about high debt levels are certainly justified for countries that do not print their own currencies. When a country lacks a buyer of last resort for its debt, a self-fulfilling crisis can develop where rising bond yields make it more difficult for the government to service its obligations, leading to even higher bond yields (Chart 3). Chart 3Multiple Equilibria In Debt Markets Are Possible Without A Lender Of Last Resort

Secular Stagnation: The Easiest Problem In The World?

Secular Stagnation: The Easiest Problem In The World?

In contrast, central banks in countries that are able to issue debt in their own currencies can always purchase their own government’s bonds with newly issued cash. They can also set short-term interest rates at whatever level they want, thus ensuring that the government has a reliable source of financing. The “golden rule” for debt sustainability says that a country’s debt-to-GDP ratio will stabilize as long as the interest rate the government pays on its debt is less than the growth rate of the economy. This is true regardless of how big a primary budget deficit the government runs (Chart 4).1 Chart 4Debt Dynamics When r Is Less Than g

Secular Stagnation: The Easiest Problem In The World?

Secular Stagnation: The Easiest Problem In The World?

In fact, the higher the debt-to-GDP ratio is, the larger the sustainable level of the budget deficit that the government can achieve. For example, if nominal GDP growth is 4% and the target debt-to-GDP ratio is 50%, the government can run a budget deficit of 2% of GDP in perpetuity; in contrast, if the target debt-to-GDP ratio is 250%, the government can run a budget deficit of 10% of GDP. The catch is that this magic only works if the interest rate stays below the growth rate of the economy. When there is a lot of spare capacity, this is not a major issue since interest rates can be kept low without the worry that inflation will accelerate. Things get trickier once the economy reaches full employment. At that point, if the budget deficit remains high, inflation could rise as aggregate demand begins to outstrip the economy’s productive capacity. This may cause the central bank to raise interest rates, which could be a vexing problem for a highly indebted government. One might argue that the government could preempt the central bank from having to raise rates simply by tightening fiscal policy once the economy begins to overheat. In many cases, this would indeed be the correct response. However, there may be some occasions where tightening fiscal policy is politically impossible. In such cases, the preferred political response may be to allow inflation to rise. Higher inflation would push up nominal income, thus putting downward pressure on the debt-to-GDP ratio. Once the real value of the debt has been inflated away, the central bank could raise rates in order to cool the economy. Would such an inflationary strategy be preferable to not running a large budget deficit to begin with? It depends on who you ask! If you ask bondholders, they would certainly say no. If anything, bondholders might prefer a deflationary environment since falling prices would increase the purchasing power of their bonds. In contrast, workers and businesses may prefer more stimulus. For them, higher inflation down the road is a price worth paying if it means continued low unemployment and rising profits. How do these competing interests balance out? In most cases, the economy would be better off following the bigger budget deficit/higher inflation strategy. This is partly because deflation is generally a greater risk to the financial system and the broader economy than inflation. It is also because the capital stock is likely to grow more quickly in an economy that is able to stay close to full employment than one that suffers from deficient demand (firms generally invest more when unemployment is low). Hence, not only can fiscal stimulus provide short-term support to employment and consumption during the period when demand is depressed, it can even generate longer-term gains in the form of higher labor productivity and lower structural unemployment compared to what would have happened in the absence of any fiscal easing. The Political Economy Of Debt And Inflation The discussion above suggests that political forces, rather than economic logic, explain why some countries fail to take the necessary steps to solve what should be an elementary problem: increasing demand. In particular, demand-side secular stagnation is likely to be a bigger threat in countries where the preferences of bondholders and others who benefit from very low inflation hold sway. The appreciation of this fact helps explain some key developments in economic history, while shedding light on what the future may hold. Chart 5Universal Suffrage Made Inflation Politically More Palatable Than Deflation

Universal Suffrage Made Inflation Politically More Palatable Than Deflation

Universal Suffrage Made Inflation Politically More Palatable Than Deflation