Policy

Highlights Portfolio Strategy The trade-weighted U.S. dollar’s appreciation along with the still souring manufacturing data are weighing on SPX profit growth, at a time when heightened geopolitical uncertainty and a looming reversal in financial conditions has the potential to wreak havoc on stock prices. Stay cautious on the prospects of the broad equity market on a cyclical 9-12 month time horizon. Firming operating metrics, the resilient U.S. dollar, compelling valuations and depressed technicals, all signal that there is an exploitable tactical trading opportunity in a long S&P industrials/short S&P tech pair trade, irrespective of the trade war outcome. A tentative tick up in EM and China data along with improving relative operating metrics signal that the time is ripe to initiate a long machinery/short semis pair trade. Recent Changes Initiate a long S&P Industrials/short S&P Tech pair trade on a tactical three-to-six month time horizon, today. Initiate a long S&P Machinery/short S&P Semiconductors pair trade on a tactical three-to-six month time horizon, today.

Follow The Profit Trail

Follow The Profit Trail

Feature The S&P 500 oscillated violently again last week, as the barrage of declining economic data, heightened trade war-related volatility and political upheaval dominated the news flow. While the Fed remains the backstop of last resort, we doubt additional interest rate cuts, which are already aggressively priced in the bond market, will boost lending and entice CEOs to invest in capital expenditure projects. Investors have to stay patient and disciplined, let this economic slowdown play out and allow for the natural healing of the economy. As a reminder, the ISM manufacturing index has been decelerating for twelve months and only been below the boom bust line for two. If history is an accurate guide, an additional three-to-six months of manufacturing pain are in store before a definitive bottom is in place (bottom panel, Chart 1). Such a macro backdrop, still warrants caution on the prospects of the broad equity market. Chart 1Allow Time For Economic Healing

Allow Time For Economic Healing

Allow Time For Economic Healing

Beginning in August, a number of BCA publications became a tad more cautious on risk assets. Following our October editorial view meeting last week, this cautiousness was cemented with a tactical downgrade of global equities to neutral from previously overweight in the BCA House View matrix. While this marks a clear shift toward this publication’s less sanguine view of the U.S. equity market adopted during the summer, BCA's cyclical 12-month House View remains overweight global equities. Worryingly, the majority of the indicators we track continue to emit distress signals and warn that the SPX has further downside (Chart 2), especially absent profit growth. Importantly, we first correctly posited last May that the back half of the year global growth reacceleration was in jeopardy and would go on hiatus courtesy of rising policy uncertainty.1 Such a backdrop would boost the U.S. dollar and simultaneously take a bite out of SPX EPS.2 Chart 2Soft Data Red Flag

Soft Data Red Flag

Soft Data Red Flag

Last week we highlighted that the U.S. dollar is the most important indicator to monitor given its global deflationary/reflationary properties. Were the greenback to maintain its year-to-date gains, it will continue to dent SPX profitability via P&L translation loss effects and likely sustain the profit recession into early 2020 (trade-weighted U.S. dollar shown inverted, bottom panel, Chart 3). Chart 3Greenback Weighing On Profits

Greenback Weighing On Profits

Greenback Weighing On Profits

U.S. Equity Strategy’s S&P 500 four-factor macro EPS growth model remains downbeat (middle panel, Chart 4). Were we to isolate the U.S. dollar as a single variable and re-run the regression it is clear that additional greenback appreciation will further weigh on SPX profit growth (bottom panel, Chart 4). Meanwhile, the easing in financial conditions and drubbing of the 10-year Treasury yield since the Christmas Eve lows is already reflected in the 23% jump in the forward PE multiple, which explains over 90% of the SPX’s rise since the Dec 24, 2018 trough (top & middle panels, Chart 5). In other words, for multiples to expand anew, financial conditions would have to further ease, which in our view is a tall order (bottom panel, Chart 5). Chart 4EPS Model Warrants Caution

EPS Model Warrants Caution

EPS Model Warrants Caution

Chart 5Financial Conditions Are The Forward P/E

Financial Conditions Are The Forward P/E

Financial Conditions Are The Forward P/E

This week we are initiating two related pair trades to exploit the mispricing of the trade war within the deep cyclical sector universe. Thus, we would lean against the narrative that easy financial conditions are not fully reflected into stocks. In contrast, our worry is that junk spreads are on the verge of a breakout and such a backdrop would tighten financial conditions and aggravate an SPX drawdown (junk OAS shown inverted, Chart 6). Adding it all up, the trade-weighted U.S. dollar’s appreciation along with the still souring manufacturing data are weighing on SPX profit growth, at a time when heightened geopolitical uncertainty and a looming reversal in financial conditions has the potential to wreak havoc on stock prices. Stay cautious on the prospects of the broad equity market on a cyclical 9-12 month time horizon. This week we are initiating two related pair trades to exploit the mispricing of the trade war within the deep cyclical sector universe. Chart 6Watch Junk Spreads

Watch Junk Spreads

Watch Junk Spreads

Initiate A Long Industrials/Short Tech Pair Trade… Ever since the Sino-American trade war started in March 2018, the market has punished industrials, but tech has escaped unscathed. While the global growth soft patch preceded the U.S./China trade spat, courtesy of the Fed’s tightening cycle and Chinese policymakers’ slamming on the brakes, the trade war has served as a catalyst to aggressively shed deep cyclical equities except for tech stocks (Chart 7). We think this misalignment presents a playable opportunity to generate alpha by going long industrials/short tech, irrespective of the trade war’s outcome. In other words, this market neutral trade will be in the black either because the trade spat gets resolved or because there will effectively be no “real” deal including intellectual property and the tech sector. If the two sides manage to iron out their differences and strike a deal, industrials stocks should benefit from a greater catch-up phase because they have been depressed over the past two years, while tech stocks are near relative all-time highs. In contrast, a “no deal” scenario, should also re-concentrate investors’ minds and lead to a relative selling in tech stocks versus their already beaten-down deep cyclical peers: industrials. Chart 7Bifurcated Deep Cyclicals Market

Bifurcated Deep Cyclicals Market

Bifurcated Deep Cyclicals Market

Chart 8Lots Of Bad Trade War News Reflected In Prices

Lots Of Bad Trade War News Reflected In Prices

Lots Of Bad Trade War News Reflected In Prices

Chart 8 shows the drubbing in relative share prices as three key macro drivers have felt the trade war’s wrath. In more detail, were a deal to get struck, growth expectations will reverse course and a bond market sell-off will almost immediately reflect such an improvement in the global macro backdrop. Rising interest rates on the back of a reflationary/inflationary impulse are a boon for industrials and a bane for high growth tech stocks (top panel, Chart 8). Similarly, the middle panel of Chart 8 highlights that the ISM manufacturing survey should climb above the boom/bust line and outshine the San Francisco Fed’s Tech Pulse Index (that comprises “coincident indicators of activity in the U.S. information technology sector”3) on news of a successful deal. Finally, relative capital expenditure outlays should also veer in favor of industrials as previously mothballed infrastructure projects will come out of hibernation (bottom panel, Chart 8). In contrast, tech capex has been resilient of late with analytics, security and cloud computing being the most defensive capex corner, leaving little room for additional relative capex gains. Taking the opposite side i.e. a “no deal”, we doubt the metrics we depict in Chart 8 would sink that much further. If anything we believe that there is an element of exhaustion and relative share prices would jump on news of a breakdown in trade talks as tech sector fire sales would trump the sell-off in already depressed industrials. Meanwhile, the U.S. dollar and relative share prices have been steeply diverging recently and this gap will likely narrow via a catch-up phase in the latter (top & middle panels, Chart 9). According to Factset’s latest data the S&P industrials sector garners 37% of its sales from abroad, whereas the S&P information technology sector’s foreign exposure stands at 57% of total revenues.4 Therefore, given this 20% delta, a rising greenback should be beneficial to the more domestically geared industrials stocks (bottom panel, Chart 9). On the operating front, industrials also have the upper hand. The relative wage bill is sinking like a stone (shown inverted, middle panel, Chart 10) at a time when relative selling price inflation is holding its own (top panel, Chart 10). The upshot is that a relative profit margin jump is in store in the coming months which should boost the relative share price ratio (bottom panel, Chart 10). Chart 9Unsustainable Divergence

Unsustainable Divergence

Unsustainable Divergence

Chart 10Industrials Have The Upper Hand

Industrials Have The Upper Hand

Industrials Have The Upper Hand

U.S. Equity Strategy’s proprietary relative Cyclical Macro Indicators and relative profit growth models capture all these drivers and both signal that an industrials versus tech earnings-led outperformance phase looms into year end (Chart 11). Chart 12 shows that the relative earnings breadth and relative net earnings revisions are both deep in negative territory. In terms of technicals, the relative percentage of groups trading with a positive 52-week rate of change has hit the lowest level in the past two decades (second panel, Chart 12) and our composite relative technical indicator is roughly one standard deviation below the historical mean (bottom panel, Chart 11). Chart 11Profit Models And...

Profit Models And...

Profit Models And...

Chart 12...Washed Out Breadth Say Buy Industrials At The Expense Of Tech

...Washed Out Breadth Say Buy Industrials At The Expense Of Tech

...Washed Out Breadth Say Buy Industrials At The Expense Of Tech

Finally, relative valuations are also bombed out. Our relative valuation indicator has been in a six-year uninterrupted drop, falling from two standard deviations above the mean to one standard deviation below the mean (fourth panel, Chart 11). Such entrenched bearishness in relative value is unwarranted. Bottom Line: Firming operating metrics, the resilient U.S. dollar, compelling valuations and depressed technicals, all signal that there is an exploitable tactical trading opportunity in a long S&P industrials/short S&P tech pair trade, irrespective of the trade war outcome. …And A Long Machinery/Short Semis Pair Trade A more speculative and higher octane vehicle to explore this trade war-related mispricing is via a long S&P machinery/short S&P semiconductors pair trade. Most of the drivers mentioned above also hold true in this subsector market-neutral trade. However, in this section we will drill deeper in the China/EM drivers. The Emerging Asia leading economic indicator (EALEI) has plummeted to levels last hit around the 1998 LTCM bailout (top panel, Chart 13). While more pain is likely in the coming months as global trade has ground to a halt, we doubt the carnage in the EALEI can continue indefinitely. In fact, a tentative trough in the Emerging Markets (EM) manufacturing PMI heralds a brighter outlook for relative share prices (bottom panel, Chart 13). Chart 13Same Trade War Theme, Different Vehicles To Play It

Same Trade War Theme, Different Vehicles To Play It

Same Trade War Theme, Different Vehicles To Play It

Chart 14China...

China...

China...

Encouragingly, China’s fiscal and credit impulse also signals that a bottom in relative share prices is likely already in place. If this leading indicator proves accurate in the coming months, then relative share prices can spike 20% near the late-2018 highs (Chart 14). Chinese money supply growth is showing some signs of life and capital committed to infrastructure spending is coming out of hibernation. Goldman Sachs’ China current activity indicator is on a similar upward trajectory, underscoring that the path of least resistance is higher for relative share prices (Chart 15). Chart 15...Holds The Key

...Holds The Key

...Holds The Key

Chart 16Firming Final Demand...

Firming Final Demand...

Firming Final Demand...

On the operating front, relative new orders and relative shipment growth have both ticked higher (top & middle panels, Chart 16). Importantly, our relative demand proxy suggests that the relative end-demand backdrop is also firming. Using Caterpillar’s global sales to dealers data compared with global chip sales reveals that a wide gap has formed between relative share prices and our relative demand gauge (bottom panel, Chart 16). If our thesis pans out in the upcoming three-to-six months then machinery will trounce semis. Finally, relative pricing power corroborates that machinery demand has the upper hand versus semiconductor final demand. The Commodity Research Bureau’s raw industrials index is climbing relative to Asian DRAM prices. The upshot is that the compellingly valued relative share price ratio will gain steam in the months ahead (Chart 17). In sum, a tentative up-tick in EM and China data along with improving relative operating metrics signal that the time is ripe to initiate a long machinery/short semis pair trade. Bottom Line: Initiate a long S&P machinery/short S&P semiconductors pair trade today. The ticker symbols for the stocks in the S&P machinery and S&P semis indexes are: BLBG – S5MACH – CAT, DE, ITW, IR, CMI, PCAR, PH, SWK, FTV, DOV, XYL, IEX, WAB, SNA, PNR, FLS, and BLBG – S5SECO – INTC, TXN, NVDA, AVGO, QCOM, MU, ADI, AMD, XLNX, QRVO, MCHP, MXIM, SWKS, respectively. Chart 17...Is A Boon To Relative Pricing Power

...Is A Boon To Relative Pricing Power

...Is A Boon To Relative Pricing Power

Key Risk To Monitor One important risk to both of our newly recommended market-neutral trades is China. We recently touched base with our ex-Chief Geopolitical Strategist and currently Chief Strategist at the Clocktower Group, Marko Papic. He warned us that all bets would be off because: “I think we will look back at the recession of 2020 and it will be known as the “China recession”. Basically, China just decided to stop playing, pick up its toys, and go home”. If Marko’s wise words were to ring true, then such a Chinese policy shift will truly be a game changer with negative global economic growth implications. With regard to our pair trades, they would both be offside. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA U.S. Equity Strategy Weekly Report, “Consolidation” dated May 21, 2019, available at uses.bcaresearch.com. 2 Please see BCA U.S. Equity Strategy Weekly Report, “On Edge” dated May 13, 2019, available at uses.bcaresearch.com. 3 https://www.frbsf.org/economic-research/indicators-data/tech-pulse/ 4 https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_100419A.pdf Current Recommendations Current Trades Size And Style Views Stay neutral cyclicals over defensives (downgrade alert) Favor value over growth Favor large over small caps (Stop 10%)

Highlights In this Weekly Report, we present our semi-annual chartbook of the BCA Central Bank Monitors. All of the Monitors are now below the zero line, indicating a growing need to ease global monetary policy (Chart of the Week). Central bankers have already gone down that path in several countries over the past few months (the U.S., the euro area, Australia and New Zealand), helping sustain the powerful 2019 rally in global bond markets. Feature With the global manufacturing & trade downturn now threatening to spill over into domestic demand in the major developed markets, policymakers will need to stay dovish to stave off recession. This will keep global bond yields at depressed levels in the near term, at least until widely-followed data like manufacturing PMIs stabilize and/or there is positive news on U.S.-China trade negotiations. Chart of the WeekStrong Pressures To Ease Global Monetary Policy

Strong Pressures To Ease Global Monetary Policy

Strong Pressures To Ease Global Monetary Policy

Yields already discount a lot of bad economic news, however, and there is a ray of hope visible in the bottoming out of our global leading economic indicator. A sustainable bottom in global bond yields, though, will require some change in the current downward growth or inflation momentum highlighted in our Central Bank Monitors. Yields already discount a lot of bad economic news, however, and there is a ray of hope visible in the bottoming out of our global leading economic indicator. A sustainable bottom in global bond yields, though, will require some change in the current downward growth or inflation momentum highlighted in our Central Bank Monitors. An Overview Of The BCA Central Bank Monitors* Chart 2Low Bond Yields Are Consistent With Our CB Monitors

Low Bond Yields Are Consistent With Our CB Monitors

Low Bond Yields Are Consistent With Our CB Monitors

The BCA Central Bank Monitors are composite indicators designed to measure the cyclical growth and inflation pressures that can influence future monetary policy decisions. The economic data series used to construct the Monitors are not the same for every country, but the list of indicators generally measure the same things (i.e. manufacturing cycles, domestic demand strength, commodity prices, labor market conditions, exchange rates, etc). The data series are standardized and combined to form the Monitors. Readings above the zero line for each Monitor indicate pressures for central banks to raise interest rates, and vice versa. Through the nexus between growth, inflation, and market expectations of future interest rate changes, the Monitors do exhibit broad correlations to government bond yields in the Developed Markets (Chart 2). All of the Monitors are currently pointing in a bond-bullish direction, making them less useful as a country allocation tool within global bond portfolios. With easing pressures most intense in the euro area, given that the ECB Monitor has the lowest reading, our recommended overweight stance on core euro area government bonds (hedged into U.S. dollars) remains well supported. In each BCA Central Bank Monitor Chartbook, we include a new chart for each country that we have not shown previously. In this edition, we show the components of the Monitors, grouped into those focusing on economic growth and inflation, plotted against our central bank discounters that indicate the amount of rate cuts/hikes priced into global Overnight Index Swap (OIS) curves. Fed Monitor: Signaling A Need For More Cuts Our Fed Monitor has fallen below the zero line (Chart 3A), indicating that the Fed’s summer rate cuts were justified with more easing still required. The Monitor, however, has not yet fallen to levels seen during U.S. recessions and is more consistent with the below-trend growth periods in 2016 and the late-1990s. The views of the FOMC on U.S. monetary policy are more deeply divided now than has been seen in many years. The doves can point to slumping global growth, persistent trade uncertainty, contracting capital spending and falling inflation expectations as reasons to continue cutting rates. The hawks can look at continued labor market tightness, elevated asset prices and realized inflation rates holding near the Fed’s 2% inflation target (Chart 3B) as reasons to keep monetary policy steady. That mixed picture can be seen in the components of our Fed Monitor, with the growth components showing the biggest pressure for more rate cuts compared to more stable readings from the inflation and financial components (Chart 3C). Chart 3AU.S.: Fed Monitor

U.S.: Fed Monitor

U.S.: Fed Monitor

Chart 3BU.S. Realized Inflation Holding Firm

U.S. Realized Inflation Holding Firm

U.S. Realized Inflation Holding Firm

Chart 3CGreatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

Greatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

Greatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

The U.S. Treasury market may have gotten ahead of itself after the latest decline in yields, which looks stretched versus the Fed Monitor. The U.S. Treasury market may have gotten ahead of itself after the latest decline in yields, which looks stretched versus the Fed Monitor (Chart 3D). We still expect the Fed to deliver just one more rate cut at the FOMC meeting at the end of October, as the “hard” U.S. data is outpeforming the “soft” data like the weak ISM surveys. That leaves Treasury yields vulnerable to some rebound if global growth stabilizes, although that is conditional on no new breakdown of the U.S.-China trade negotiations – a factor that continues to weigh on U.S. business confidence. Chart 3DTreasury Yields More Than Fully Discount Fed Easing Pressures

Treasury Yields More Than Fully Discount Fed Easing Pressures

Treasury Yields More Than Fully Discount Fed Easing Pressures

BoE Monitor: Easier Policy Needed Our Bank of England (BoE) Monitor, which was in the “tighter money required” zone from 2016-18, has been below the zero line since April of this year (Chart 4A). The market agrees with the message from the Monitor and is now pricing in -12bps of rate cuts over the next twelve months. The relentless uncertainty surrounding Brexit has triggered sharp downgrades of growth expectations and weakened business confidence, which the BoE is now factoring into its own projections. In the August Inflation Report, the BoE lowered its 2020 inflation forecast to below 2% - no surprise given the sharp fall in realized inflation that has already occurred even as economic growth has still not yet fallen substantially below trend (Chart 4B). Chart 4AU.K.: BoE Monitor

U.K.: BoE Monitor

U.K.: BoE Monitor

Chart 4BFalling U.K. Inflation Opens The Door To A BoE Ease

Falling U.K. Inflation Opens The Door To A BoE Ease

Falling U.K. Inflation Opens The Door To A BoE Ease

Still, weakening growth components have been the main driver of the BoE Monitor into rate cut territory (Chart 4C). While a strong jobs market is helping support consumer spending, the Brexit turmoil is having a lasting impact on future growth. Since the 2016 Brexit referendum, business confidence and real business investment have collapsed which, in turn, has hurt productivity growth, as we discussed in a Special Report last month.1 Chart 4CBrexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

Brexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

Brexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

The uncertainty around Brexit dominates the economic outlook and any future BoE decisions. Our Geopolitical Strategy service anticipates that Brexit will be delayed beyond October 31st. As a result, uncertainty will continue to weigh on Gilt yields, even though yields have already fallen in line with our BoE Monitor (Chart 4D). We continue to recommend an overweight stance on U.K. Gilts. Chart 4DGilt Yields Have Fallen In Line With Our BoE Monitor

Gilt Yields Have Fallen In Line With Our BoE Monitor

Gilt Yields Have Fallen In Line With Our BoE Monitor

ECB Monitor: Intense Pressure For Easier Monetary Policy Our European Central Bank (ECB) Monitor is now well below the zero line, signaling a strong need for easier monetary policy (Chart 5A). The global manufacturing downturn has hit the export-dependent economies of the euro area hard, with Germany now likely in a technical recession. Our European Central Bank (ECB) Monitor is now well below the zero line, signaling a strong need for easier monetary policy. Despite the weaker growth momentum, there remains far less spare capacity in the euro area economy than at any time since before the 2009 global recession (Chart 5B). This is keeping realized inflation in positive territory, in contrast to what was seen during the previous downturn in 2015-16. Chart 5AEuro Area: ECB Monitor

Euro Area: ECB Monitor

Euro Area: ECB Monitor

Chart 5BEuro Area Inflation Is Subdued, Despite Tight Labor Markets

Euro Area Inflation Is Subdued, Despite Tight Labor Markets

Euro Area Inflation Is Subdued, Despite Tight Labor Markets

The ECB has already responded to the weakening growth & inflation pressures, introducing a new TLTRO program back in March and then cutting the overnight deposit rate and restarting its Asset Purchase Program in September. The latest policy moves were reported to be more contentious, with the “hard money” northern euro area countries opposed to restarting bond purchases. The new incoming ECB President, Christine Lagarde, will likely have her hands full trying to gain consensus on any further easing measures from here, even as both the growth and inflation components of our ECB Monitor indicate that more stimulus is needed (Chart 5C). Chart 5CA Consistent Message On The Need For Future ECB Easing From Growth & Inflation

A Consistent Message On The Need For Future ECB Easing From Growth & Inflation

A Consistent Message On The Need For Future ECB Easing From Growth & Inflation

The big decline in euro area bond yields, which has pushed large swaths of sovereign yields into negative territory, does not look particularly stretched relative to the plunge in the ECB Monitor (Chart 5D). Without signs that the global manufacturing downturn is ending, however, euro area yields will stay mired at current deeply depressed levels. We recommend a moderate overweight on core European government bonds, on a currency-hedged basis into U.S. dollars. Chart 5DBund Rally Looks In Line With The ECB Monitor

Bund Rally Looks In Line With The ECB Monitor

Bund Rally Looks In Line With The ECB Monitor

BoJ Monitor: A Rate Cut On The Horizon? Our Bank of Japan (BoJ) Monitor has drifted slightly below the zero line into “rate cut required” territory (Chart 6A). Over the past few years, the BoJ’s monetary policy has remained unchanged for the most part and its messaging has grown less dovish, citing an expanding economy. However, recent Japanese economic data shows widespread deterioration in growth momentum, as the nation has been hit hard by the global manufacturing and trade recession. Yet even with weaker growth, Japan’s unemployment rate keeps hitting all-time lows. This has not helped boost inflation much, though, with Japan’s CPI inflation still struggling to reach even the 1% level (Chart 6B). Still, the latest leg lower in our BoJ Monitor has been driven by the growth, rather than inflation, components (Chart 6C). Chart 6AJapan: BoJ Monitor

Japan: BoJ Monitor

Japan: BoJ Monitor

Chart 6BNo Spare Capacity In Japan, But Still No Inflation

No Spare Capacity In Japan, But Still No Inflation

No Spare Capacity In Japan, But Still No Inflation

Weakening confidence has resulted in significant declines in both consumer spending and business investment. Due to the struggling domestic economy, it was expected that the Abe government would postpone the scheduled consumption tax hike, but it was finally initiated on October 1st. The timing could not be worse given the ongoing contraction in global manufacturing and trade activity that has clearly spilled over into Japan’s export and industrially-focused economy. Chart 6CThe Slumping Japanese Economy Could Use Some More BoJ Assistance

The Slumping Japanese Economy Could Use Some More BoJ Assistance

The Slumping Japanese Economy Could Use Some More BoJ Assistance

The BoJ will likely try and deliver some sort of easing in the next few months, but its options are limited after years of already hyper-easy policy. A modest rate cut is likely all that will be delivered, on top of a continuation of the Yield Curve Control policy. That will be enough to keep JGB yields at depressed levels (Chart 6D), even if global yields were to begin climbing. Chart 6DJGB Yields Look Fairly Valued Vs The BoJ Monitor

JGB Yields Look Fairly Valued Vs The BoJ Monitor

JGB Yields Look Fairly Valued Vs The BoJ Monitor

BoC Monitor: Rate Cuts Needed, But Will The BoC Deliver? The Bank of Canada (BoC) Monitor has been below zero since April of this year, indicating a need for easier monetary policy (Chart 7A). Although the BoC has maintained its policy rate at 1.75%, dovish Fed policy and softening domestic economic growth are making it harder for the BoC to continue sitting on its hands Although the Canadian labor market remains solid, household consumption has continued to weaken alongside falling consumer confidence. However, the inflation rate for both headline and core CPI measures is still hovering near the mid-point of BoC 1-3% target range (Chart 7B). Chart 7ACanada: BoC Monitor

Canada: BoC Monitor

Canada: BoC Monitor

Chart 7BRising Inflation Making The BoC’s Job Harder

Rising Inflation Making The BoC's Job Harder

Rising Inflation Making The BoC's Job Harder

At the moment, our BoC Monitor is more influenced by weaker growth components than stabilizing inflation components (Chart 7C). Similar mixed messages are also evident in other data. According to the latest BoC Business Outlook Survey, the overall outlook has edged up to the historical average,2 but real capex growth remains in negative territory and manufacturing new orders are still falling. In contrast, the Canadian labor market remains tight and both wage and price inflation are holding firm. Chart 7CBoC Growth & Inflation Components Signaling Moderate Pressure To Ease

BoC Growth & Inflation Components Signaling Moderate Pressure To Rise

BoC Growth & Inflation Components Signaling Moderate Pressure To Rise

Canadian government bonds have rallied strongly this year, but the yield momentum has appeared to overshoot the decline in our BoC Monitor (Chart 7D). The Canadian OIS curve is discounting -27bps of rate cuts over the next twelve months, but the BoC is not signaling that they will ease. We upgraded our recommended stance on Canadian government bonds to neutral back in May, and we see no need to alter that view without further evidence of more deterioration in Canadian growth or inflation data.3 Chart 7DCanadian Bond Rally Looks A Bit Stretched

Canadian Bond Rally Looks A Bit Stretched

Canadian Bond Rally Looks A Bit Stretched

RBA Monitor: Expect Another Cut The Reserve Bank of Australia (RBA) Monitor has been below the zero line since September 2018, indicating a need for easier monetary policy (Chart 8A). The RBA has already delivered on that signal this year, cutting the Cash Rate twice to an all-time low of 0.75%. Markets are still expecting more, with the Australian OIS curve discounting another -29bps of cuts over the next year, although most of those cuts are expected to occur within the next six months. The signal from our RBA Monitor suggests that Australian bond yields should remain under downward pressure, although the yield momentum has been excessive relative to the fall in the Monitor. Both headline and core CPI inflation remain below the RBA’s 2-3% target range (Chart 8B), and the central bank continues to lower its inflation forecasts, suggesting an entrenched dovish bias. Chart 8AAustralia: RBA Monitor

Australia: RBA Monitor

Australia: RBA Monitor

Chart 8BNo Inflation For The RBA To Worry About

No Inflation For The RBA To Worry About

No Inflation For The RBA To Worry About

The latest downturn in our RBA Monitor is related to declines in both the inflation and growth components (Chart 8C). The weakness in the growth components is led by falling exports to Asia, in addition to the sharp drop in house prices in the major cities. The fall in the inflation components reflects both weak inflation expectations and spare capacity in labor markets. Chart 8CA Loud & Clear Message On The Need For RBA Easing

A Loud & Clear Message On The Need For RBA Easing

A Loud & Clear Message On The Need For RBA Easing

The signal from our RBA Monitor suggests that Australian bond yields should remain under downward pressure, although the yield momentum has been excessive relative to the fall in the Monitor (Chart 8D). Australia’s economy will not begin to outperform again, however, until China’s current growth slump starts to bottom out, which is unlikely to occur until the first quarter of 2020 at the earliest. Thus, we expect the RBA to deliver another rate cut before the end of the year, justifying a continued overweight stance on Australian government bonds. Chart 8DA Lot Of Bad News Discounted In Australian Bond Yields

A Lot Of Bad News Discounted In Australian Bond Yields

A Lot Of Bad News Discounted In Australian Bond Yields

RBNZ Monitor: More Easing To Come Our Reserve Bank of New Zealand (RBNZ) monitor remains well below zero, indicating that easier monetary policy is still required (Chart 9A). The central bank has already delivered two rate cuts this year: a -25bps cut in May and, more importantly, a shock rate cut of -50bps in August. Forward guidance remains dovish, with RBNZ Governor Adrian Orr signaling more easing is likely and even hinting at negative rates in the future. This rhetoric is reflected in the NZ OIS curve, which is pricing in a further -42bps of easing over the next twelve months. High inflation is not a constraint for the RBNZ. Both headline and core measures of inflation are currently at 1.7% (Chart 9B). As the RBNZ targets a 1-3% range over the medium term, the prospect of overshooting the 2% longer-term target will not restrict policymakers from acting as appropriate to boost growth. Chart 9ANew Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

Chart 9BNZ Inflation Creeping Higher

NZ Inflation Creeping Higher

NZ Inflation Creeping Higher

Most of the pressure to ease has come from the continued deterioration in the growth component of our RBNZ Monitor (Chart 9C), reflecting weakness in manufacturing and consumption. The manufacturing PMI is currently in contractionary territory at 48.4, having fallen almost five points since February of this year. Annual growth in retail sales has been slowing for the past two years while consumer confidence is at 7-year lows. Chart 9CWeak Growth Is The Reason RBNZ Rate Cuts Are Needed

Weak Growth Is The Reason RBNZ Rate Cuts Are Needed

Weak Growth Is The Reason RBNZ Rate Cuts Are Needed

We feel confident in reiterating our bullish recommendation on NZ government bonds versus U.S. and German sovereign debt. The RBNZ Monitor suggests that policy will stay dovish for some time, while NZ yields still offer a relatively attractive yield, unlike deeply overbought Treasuries and Bunds (Chart 9D). Chart 9DStill A Bullish Case For New Zealand Government Bonds

Still A Bullish Case For New Zealand Government Bonds

Still A Bullish Case For New Zealand Government Bonds

Riksbank Monitor: Watching And Waiting Our Riksbank Monitor remains very slightly below zero and the market is currently priced for -4bps of rate cuts over the next year (Chart 10A). The Riksbank has decided to hold the Repo Rate constant at -0.25% while forecasting a hike towards the end of this year or the beginning of 2020. Given the policy environment, rate cuts remain unlikely. At most, the Riksbank can further delay rate hikes if the data continues to disappoint. The Riksbank noted in its September Monetary Policy Report that the unexpectedly weak development of the labor market indicates that resource utilization will normalize sooner than expected. This is reflected in Chart 10B, where the unemployment gap is now negative. Meanwhile, inflation readings are giving a mixed signal for the central bank. While the headline CPI measure has declined precipitously year-to-date, owing to the dramatic fall in oil prices, core inflation has continued to climb steadily. Chart 10ASweden: Riksbank Monitor

Sweden: Riksbank Monitor

Sweden: Riksbank Monitor

Chart 10BMixed Messages From Swedish Inflation

Mixed Messages From Swedish Inflation

Mixed Messages From Swedish Inflation

As a result, the inflation components of our Riksbank monitor - driven by a spike in the Citigroup Inflation Surprise Index, wage growth hooking upward and inflation expectations holding firm around 2% - are signaling the need for tighter monetary policy (Chart 10C). However, the growth components – led by weak exports, employment, and manufacturing data - are exerting pressure in the opposite direction. This is evident in the Swedish Manufacturing PMI, which tumbled from 51.8 to 46.3 in September, deep into contractionary territory. Chart 10CThere Is A Reason Why The Riksbank Has Been On Hold

There Is A Reason Why The Riksbank Has Been On Hold

There Is A Reason Why The Riksbank Has Been On Hold

Keeping in mind the inflation constraint, it remains unlikely that the Riksbank will cut rates unless the economic data disappoints more significantly to the downside. This should help put a floor under Swedish bond yields in the near term (Chart 10D). Chart 10DSwedish Yields Have Fallen Too Far, Too Fast

Swedish Yields Have Fallen Too Far, Too Fast

Swedish Yields Have Fallen Too Far, Too Fast

Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Shakti Sharma Research Associate shaktis@bcaresearch.com Footnotes * NOTE: All information in this report reflects our knowledge of global events as of Thursday, October 10. 1 Please see BCA Global Fixed Income Strategy Special Report “United Kingdom: Cyclical Slowdown Or Structural Malaise?” dated September 20, 2019, available at gfis.bcaresearch.com. 2https://www.bankofcanada.ca/2019/06/business-outlook-survey-summer-2019/ 3 Please see BCA Global Fixed Income Weekly Report, “Reconcilable Differences” dated May 8, 2019, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

BCA Central Bank Monitor Chartbook: Intensifying Pressure To Ease

BCA Central Bank Monitor Chartbook: Intensifying Pressure To Ease

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Geopolitical risks are starting to abate as a result of material constraints influencing policymakers. China needs to ensure its economy bottoms and a debt-deflationary tendency does not take hold. President Trump needs to avoid further economic deterioration arising from the trade war. The U.K. is looking to prevent a recession induced by leaving the EU without an agreement. Iran and the risk of an oil price shock is the outstanding geopolitical tail risk. Feature Readers of BCA’s Geopolitical Strategy know that what defines our research is our analytical framework – specifically the theory of constraints. Chart 1The Electoral College – An Overlooked Constraint

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

The theory holds that policymakers are trapped by the pressures of their office, their nation’s global position, and the stream of events. These pressures emerge from the material world that we inhabit and as such are measurable. If a leader lacks popular approval, cannot command a majority in the legislature, rides atop a sinking economy, or suffers under stronger or smarter foreign enemies, then his policy preferences will be compromised. He will have to change his preferences to accommodate the constraints, rather than the other way around. Case in point is the U.S. electoral college: it proved an insurmountable political constraint on the Democratic Party in 2016. The college is intended to restrain direct democracy or popular passions; it also restrains the concentration of regional power. In 2012, Barack Obama won a larger share of the electoral college than the popular vote, while in 2016 Hillary Clinton won a smaller share (Chart 1). Clinton’s lack of appeal in the industrial Midwest turned the college and deprived her of the prize. The rest is history. In this report we highlight five key constraints that will shape the direction of the major geopolitical risks in the fourth quarter. We recommend investors remain tactically cautious on risk assets, although we have not yet extended this recommendation to the cyclical, 12-month time frame. China’s Policy: The Debt-Deflation Constraint We have a solid record of pessimism regarding Chinese President Xi Jinping’s willingness and ability to stimulate the economy – but even we were surprised by his tenacity this year. His administration’s effort to contain leverage, while still stimulating the economy, has prevented a quick rebound in the global manufacturing cycle. The constraint limiting this approach is the need to avoid a debt-deflation spiral. This is a condition in which households and firms become pessimistic about the future and cut back their spending and borrowing. The general price level falls and drives up real debt burdens, which motivates further cutbacks. A classic example is Japan, which saw a property bubble burst, destroying corporate balance sheets and forcing the country into a long phase of paying down debt amid falling prices. China has not seen its property bubble burst yet. Prices have continued to rise despite the recent pause in the non-financial debt build-up (Chart 2). Looser monetary and fiscal policy have sustained this precarious balance. But the result is a tug-of-war between the government and the private sector. If the government miscalculates, and the asset bubble bursts, then it will be extremely difficult for the government to change the mindset of households and companies bent on paying down debt. It will be too late to avoid the vicious spiral that Japan experienced – with the critical proviso that Chinese people are less wealthy than the Japanese in 1990 and the country’s political system is less flexible. A Japan-sized economic problem would lead to a China-sized political problem. This is why the recent drop in Chinese producer prices below zero is a worrisome sign (Chart 3). Policymakers have loosened monetary and fiscal policy incrementally since July 2018 and they are signaling that they will continue to do so. This is particularly likely in an environment in which trade tensions are reduced but remain fundamentally unresolved – which is our base case. Chart 2China's Property Bubble Intact

China's Property Bubble Intact

China's Property Bubble Intact

Chart 3China's Constraint Is Debt-Deflation

China's Constraint Is Debt-Deflation

China's Constraint Is Debt-Deflation

Are policymakers aware of this constraint? Absolutely. If the trade talks collapse, or the global economy slumps regardless, then China will have to stimulate more aggressively. Xi Jinping is not truly a Chairman Mao, willing to impose extreme austerity. He oversaw the 2015-16 stimulus and would do it again if he came face to face with the debt-deflation constraint. Is China still capable of stimulating? High debt levels, the reassertion of centralized state power, and the trade war have all rendered traditional stimulus levers less effective by dampening animal spirits. Yet policymakers are visibly “riding the brake,” so they can remove restraints and increase reflation if necessary. Most obviously, authorities can inject larger fiscal stimulus. They have insisted that they will prevent easy monetary and credit policies from feeding into property prices – and this could change. They could also pick up the pace when it comes to reducing average bank lending rates for small and medium-sized businesses.1 In short, stimulus is less effective, but the government is also preferring to save dry powder. This preference will be thrown by the wayside if it hits the critical constraint. The implication is that Chinese stimulus will continue to pick up over a cyclical, 12-month horizon. There is impetus to reduce trade tensions with the U.S., discussed below, but a lack of final resolution will ensure that policy tightening is not called for. Bottom Line: China’s chief economic constraint is a debt-deflation trap. This would engender long-term economic difficulties that would eventually translate into political difficulties for Communist Party rule. If a trade deal is reached, it is unlikely alone to require a shift to tighter policy. If the trade talks collapse, stimulus will overshoot to the upside. Trade War: The Electoral Constraint The U.S. and China are holding the thirteenth round of trade negotiations this week after a summer replete with punitive measures, threats, and failed restarts. Tensions spiked just ahead of the talks, as expected. Immediately thereafter President Trump declared he will meet with Chinese negotiators to give a boost to the process and reassure the markets.2 Trump’s major constraint in waging the trade war is economic, not political. Americans are generally sympathetic to his pressure campaign against China. Public opinion polls show that a strong majority believes it is necessary to confront China even though the bulk of the economic pain will be borne by consumers themselves (Chart 4). Yet Americans could lose faith in Trump’s approach once the economic pain fully materializes. Critically, the decline in wage growth that is occurring as a result of the global and manufacturing slowdown is concentrated in the states that are most likely to swing the 2020 election, e.g. the “purple” or battleground states (Chart 5). Chart 4Americans To Confront China Despite The Costs?

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

Chart 5Trump Faces Pressure To Stage A Tactical Trade Retreat

Trump Faces Pressure To Stage A Tactical Trade Retreat

Trump Faces Pressure To Stage A Tactical Trade Retreat

Furthermore, a rise in unemployment, which is implied by the recent decline in the University of Michigan’s survey of consumer confidence regarding the purchase of large household goods, would devastate voters’ willingness to give Trump’s tariff strategy the benefit of the doubt (Chart 6). Wisconsin and Pennsylvania, two critical states, have seen a net loss of manufacturing jobs on the year. The fear of an uptick in U.S. unemployment will prevent Trump from escalating the trade war. An uptick in unemployment would be a major constraint on Trump’s trade war – he cannot escalate further until the economy has stabilized. And that may very well require tariff rollback while trade talks “make progress.” We expect that Trump is willing to do this in the interest of staying in power. As highlighted above, the Xi administration is not without its own constraints. Our proxies for China’s marginal propensity to consume show that Chinese animal spirits are still vulnerable, particularly on the household side, which has not responded to stimulus thus far (Chart 7). Since this constraint is less immediate than Trump’s election date, Xi cannot be expected to capitulate to Trump’s biggest demands. Hence a ceasefire or détente is more likely than a full bilateral trade agreement. Chart 6Waning Consumer Confidence On Big Ticket Items Foreshadows Rise In Unemployment

Waning Consumer Confidence On Big Ticket Items Foreshadows Rise In Unemployment

Waning Consumer Confidence On Big Ticket Items Foreshadows Rise In Unemployment

Trump’s electoral constraint also suggests that he needs to remove trade risks such as car tariffs on Europe and Japan (which we expect he will do). We have been optimistic on the passage of the USMCA trade deal but impeachment puts this forecast in jeopardy. Chart 7China's Trade War Constraint? Animal Spirits

China's Trade War Constraint? Animal Spirits

China's Trade War Constraint? Animal Spirits

Bottom Line: Trump will stage a tactical retreat on trade in order to soften the negative impact on the economy and reduce the chances of a recession prior to the November 3, 2020 election. China’s economic constraints are less immediate and it is unlikely to make major structural concessions. Hence we expect a ceasefire that temporarily reduces tensions and boosts sentiment rather than a bilateral trade agreement that initiates a fundamental deepening of U.S.-China economic engagement. U.S. Policy: The Economic Constraint The 2020 U.S. election is a critical political risk both because of the volatility it will engender and because of what we see as a 45% chance that it will lead to a change in the ruling party governing the world’s largest economy. Will Trump be the candidate? Yes. If Trump’s approval among Republicans breaks beneath the lows plumbed during the Charlottesville incident in 2017 (Chart 8A), then Trump has an impeachment problem, but otherwise he is safe from removal. Judging by the Republican-leaning pollster Rasmussen, which should reflect the party’s mood, Trump’s approval rating has not broken beneath its floor and may already be bouncing back from the initial hit of the impeachment inquiry (Chart 8B). The rise in support for impeachment and removal in opinion polls is notable, but it is also along party lines and will fade if the Democrats are seen as dragging on the process or trying to circumvent an election that is just around the corner. Chart 8ARepublican Opinion Precludes Trump’s Removal

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

Chart 8BRepublican-Leaning Pollster Shows Support Holding Thus Far

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

How will all of this bear on the 2020 election? Turnout will be high so everything depends on which side will be more passionate. A critical factor will be the Democratic nominee. Former Vice President Joe Biden, the establishment pick, has broken beneath his floor in the polling. His rambling debate performances have reinforced the narrative that he is too old, while the impeachment of Trump will fuel counteraccusations of corruption that will detract from Biden’s greatest asset: his electability. According to a Harvard-Harris poll from late September, 61% of voters believe it was inappropriate for Biden to withhold aid from Ukraine to encourage the firing of a Ukrainian prosecutor even when the polling question makes no mention of any connection with Biden’s son’s business interest there. Moreover, 77% believe it is inappropriate that Biden’s son Hunter traveled with his father to China while soliciting investments there. With Vermont Senator Bernie Sanders’s candidacy now defunct as a result of his heart attack and old age, Elizabeth Warren, the progressive senator from Massachusetts, will become the indisputable front runner (which she is not yet). In the fourth primary debate on October 15, she will face attacks from all sides reflecting this new status. Given her debate performances thus far, she will sustain the heightened scrutiny and come out stronger. This is not to say that Warren is already the Democratic candidate. Biden is still polling like a traditional Democratic primary front runner (Chart 9), while Warren has some clear weaknesses in electability, as reflected in her smaller lead over Trump in head-to-head polls in swing states. Nevertheless Warren is likely to become the front runner. Chart 9Biden Polling About Average Relative To Previous Democratic Primary Front Runners

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

The recession call remains the U.S. election call. Two further considerations: Impeachment and removal of President Trump ensure a Democratic victory. There are hopes in some quarters that President Trump could be impeached and removed and yet his Vice President Mike Pence could go on to win the 2020 election, preserving the pro-business policy status quo. The problem with this logic is that Trump cannot be removed unless Republican opinion shifts. This will require an earthquake as a result of some wrongdoing by Trump. Such an earthquake will blacken Pence’s and the GOP’s name and render them toxic in the general election. Not to mention that Pence’s only act as president in the brief interim would likely be to pardon Trump and his accomplices. He would suffer Gerald Ford’s fate in 1976. Which means that a significant slide in Trump’s approval among Republicans will translate to higher odds of a Democratic win in 2020 and hence higher taxes and regulation, i.e. a hit to corporate earnings expectations. We expect this approval to hold up, but the market can sell off anyway because … The market is overrating the Senate as a check on Warren in the event she wins the White House. It is true that relative to Biden, Warren is less likely to carry the Senate. Democrats need to retain their Senate seat in Alabama, while capturing Maine, Colorado, and Arizona (or Georgia) in addition to the White House in order to control the Senate. Biden is more competitive in Arizona and Georgia than Warren. But this is a flimsy basis to feel reassured that a Warren presidency will be constrained. In fact, it is very difficult to unseat a sitting president. If the Democrats can muster enough votes to kick out an incumbent and elect an outspoken left-wing progressive from the northeast, they most likely will have mustered enough votes to take the Senate as well. For instance, unemployment could be rising or Trump’s risky foreign policy could have backfired. Chart 10Business Sentiment Threatens Trump Re-Election

Business Sentiment Threatens Trump Re-Election

Business Sentiment Threatens Trump Re-Election

In our estimation the Democrats have about a 45% chance of winning the presidency, and Warren does not significantly reduce this chance. The resilient U.S. economy is Trump’s base case for success. But Trump’s trade policy and the global slowdown are rapidly eating away at the prospect that voters see improvement (Chart 10). This speaks to the constraint driving a ceasefire with China above, but it also speaks to the broader probability of policy continuity in the U.S. As Warren’s path to the White House widens, there is a clear basis for equities to sell off in the near term. Bottom Line: Trump’s approval among Republicans is a constraint on his removal via impeachment. But the status of the economy is the greater constraint. The recession call remains the election call. While we expect downside in the near term, we are still constructive on U.S. equities on a cyclical basis. War With Iran: The Oil Price Constraint The Senate will remain President Trump’s bulwark amid impeachment, notwithstanding the controversial news that Trump is moving forward with the withdrawal of troops from Syria, specifically from the so-called “safe zone” agreed with Turkey, giving Ankara license to stage a larger military offensive in Syria. This abandonment of the U.S.’s Kurdish allies at the behest of Turkey (which is a NATO ally but has been at odds with Washington) has provoked flak from Republican senators. However, it is well supported in U.S. public opinion (Chart 11). Trump is threatening to impose economic sanctions on Turkey if it engages in ethnic cleansing. The Turkish lira is the marginal loser, Trump’s approval rating is the marginal winner. The withdrawal sends a signal to the world that the U.S. is continuing to deleverage from the Middle East – a corollary with the return of focus on Asia Pacific. While the Iranians are key beneficiaries of this pivot, the Trump administration is maintaining maximum sanctions pressure on the Iranians. The firing of hawkish National Security Adviser John Bolton did not lead to a détente, as President Rouhani has too much to risk from negotiating with Trump. Instead the Iranians smelled U.S. weakness and went on the attack in Saudi Arabia, briefly shuttering 6 million barrels of oil per day. The response to the attack – from both Saudi Arabia and the U.S. – revealed an extreme aversion to military conflict and escalation. Instead the U.S. has tightened its sanctions regime – China is reportedly withdrawing from its interest in the South Pars natural gas project, a potentially serious blow to Iran, which had been hyping its strategic partnership with China. This reinforces the prospect for a U.S.-China ceasefire even as it redoubles the economic pressure on Iran. As long as the U.S. maintains the crippling sanctions on Iran, there is no guarantee that Tehran will not strike out again in an effort to weaken President Trump’s resolve. The fact that about 18% of global oil supply flows through the critical chokepoint of the Strait of Hormuz is Iran’s ace in the hole (Chart 12). It is the chief constraint on Trump’s foreign policy, as greater oil supply disruptions could shock the U.S. economy ahead of the election. Trump can benefit from minor or ephemeral disruptions but he is likely to get into trouble if a serious shock weakens the economy at this juncture. Chart 11U.S. Opinion Constrains Foreign Policy

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

Chart 12Oil Price Constrains U.S. Policy Toward Iran

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

An oil shock does not have to originate in Hormuz shipping or sneak attacks on regional oil infrastructure. Iran is uniquely capable of fomenting the anti-government protests that have erupted in southern Iraq. The restoration of stability in Iraq has resulted in around 2 million barrels of oil per day coming onto international markets (Chart 13). If this process is reversed through political instability or sabotage, it will rapidly push up against global spare oil capacity and exert an upward pressure on oil prices that would come at an awkward time for a global economy experiencing a manufacturing recession (Chart 14). Chart 13Iran's Leverage Over Iraq

Iran's Leverage Over Iraq

Iran's Leverage Over Iraq

Chart 14Global Oil Spare Capacity Constrains Response To Crisis

Five Constraints For The Fourth Quarter

Five Constraints For The Fourth Quarter

Bottom Line: Iran’s power over regional oil production is the biggest constraint on Trump’s foreign policy in the region, yet Trump is apparently tightening rather than easing the sanctions regime. The failure of the Abqaiq attack to generate a lasting impact on oil prices amid weak global demand suggests that Iran could feel emboldened. The U.S. preference to withdraw from Middle Eastern conflicts could also encourage Iran, while the tightening of the sanctions regime could make it desperate. An oil shock emanating from the conflict with Iran is still a significant risk to the global bull market. Brexit: The No-Deal Constraint The fifth and final constraint to discuss in this report pertains to the U.K. and Brexit. We do not consider the October 31 deadline a no-deal exit risk. Parliament will prevail over a prime minister who lacks a majority. Nevertheless the expected election can revive no-deal risk, especially if Boris Johnson is returned to power with a weak minority government. Chart 15U.K.: Public Opinion Constrains Parliament And No-Deal Brexit

U.K.: Public Opinion Constrains Parliament And No-Deal Brexit

U.K.: Public Opinion Constrains Parliament And No-Deal Brexit

While parliament is the constraint on the prime minister, the public is the constraint on parliament. From this point of view, support for Brexit has weakened and the Conservative Party is less popular than in the lead up to the 2015 and 2017 general elections. The public is aware that no-deal exit is likely to cause significant economic pain and that is why a majority rejects no-deal, as opposed to a soft Brexit. Unless the Tory rally in opinion polling produces another coalition with the Northern Irish, albeit with Boris Johnson at the helm, these points make it likely that a no-deal Brexit will become untenable when all is said and done (Chart 15). If Johnson achieves a single party majority the EU will be more likely to grant concessions enabling him to get a withdrawal deal over the line. We remain long GBP-USD but will turn sellers at the $1.30 mark. Investment Implications The path of least resistance is for China’s stimulus efforts to increase – incrementally if trade tensions are contained, and sharply if not. This should help put a floor beneath growth, but the Q1 timing of this floor means that global risk assets face additional downside in the near term. We continue to recommend going long our “China Play” index. U.S.-China trade tensions should decline as President Trump looks to prevent higher unemployment ahead of his election. China has reason to follow through on small concessions to encourage Trump’s tactical trade retreat, but it does not face pressure to make new structural concessions. We expect a ceasefire – with some tariff rollback likely – but not a big bang agreement that removes all tariffs or deepens the overall bilateral economic engagement. Stay long our “China Play” index. We remain short CNY-USD on a strategic basis but recognize that a ceasefire presents a short term (maximum 12-month) risk to this view, so clients with a shorter-term horizon should close that trade. We are long European equities relative to Chinese equities as a result of the view that China will stimulate but that a trade ceasefire will leave lingering uncertainties over Chinese corporates. U.S. politics are highly unpredictable but constraint-based analysis indicates that while the House may impeach, the Senate will not remove. This, combined with Warren’s likely ascent to the head of the pack in the Democratic primary race, means that Trump remains favored to win reelection, albeit with low conviction (55% chance) due to a weak general approval rating and economic risks. The risk to U.S. equities is immediate, but should dissipate. The U.S. is rotating its strategic focus from the Middle East to Asia Pacific, which entails a continued rotation of geopolitical risk. However, recent developments reinforce our argument in July that Iranian geopolitical risk is frontloaded relative to the China risk. This is true as long as Trump maintains crippling sanctions. Iran may be emboldened by its successes so far and has various mechanisms – including Iraqi instability – by which it can threaten oil supply to pressure Trump. This is a tail risk, but it does support our position of being long EM energy producers. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 Please see BCA Research, China Investment Strategy Weekly Report, “Mild Deflation Means Timid Easing,” October 9, 2019, available at cis.bcaresearch.com. 2 China knows that Trump wants to seal a deal prior to November 2020 to aid his reelection campaign, while Trump needs to try to convince China that he does not care about election, the stock market, or anything other than structural concessions from China. Hence the U.S. blacklisted several artificial intelligence companies and sanctioned Chinese officials in advance of the talks. The U.S. opened a new front in the conflict by invoking China’s human rights abuses in Xinjiang, which is also an implicit warning not to create a humanitarian incident in Hong Kong where protests continue to rage. These are pressure tactics but have not yet derailed the attempt to seal a deal in Q4.

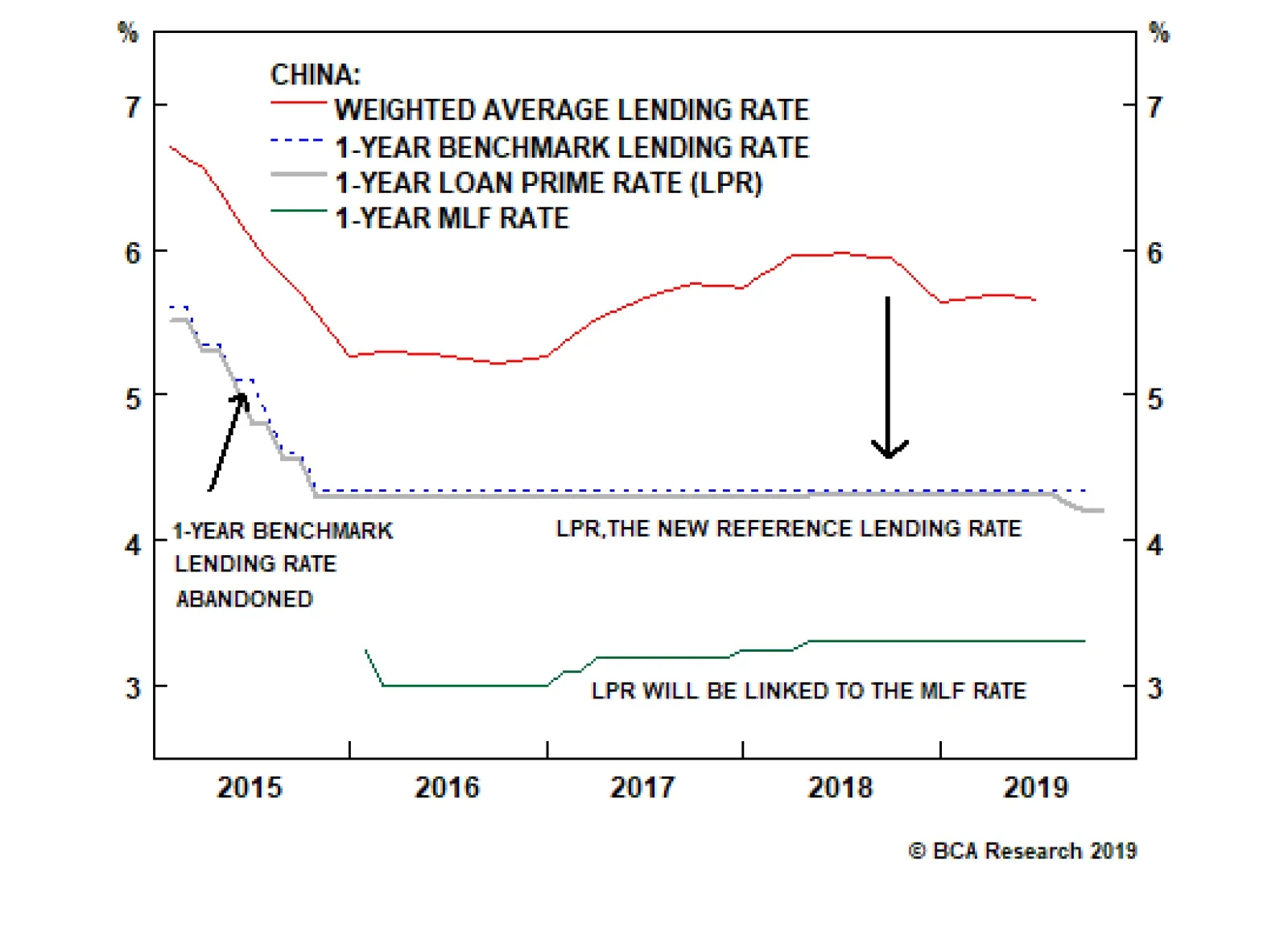

The LPR rate is essentially the MLF rate plus bank profit margins. The market will guide the top line lending rate, while the PBoC will have control over the floor rate (MLF) through open market operations. The fact that the PBoC is keeping the MLF rate…

On August 20th, the PBoC launched a new loan prime rate (LPR) system, a revamped reference regime for setting bank loan interest rates. In September, the new LPR rate for one-year bank loans was lowered by five basis points. The new LPR reform is designed…

Highlights The Chinese economy is still slowing, and there is not yet enough evidence from forward-looking economic data to suggest a turnaround is imminent. Deflation has returned to China’s industrial sector. Even though overall price deceleration has been relatively mild, it is further squeezing already deteriorating industrial profit growth. We do not expect deflation to spiral into a 2015/2016-style episode, which removes at least one risk to our growth outlook. At the same time, a mild deceleration in prices will not provide enough incentive for Chinese policymakers to hit the stimulus button. The People’s Bank of China’s new interest rate-setting regime, the LPR, will not provide much in the way of stimulus over the next few months. But it has the potential to improve China’s monetary policy transmission mechanism over the coming year, increasing the odds that policymakers will succeed in stabilizing economic activity. Short-term downside risks to growth have not abated, and we remain tactically bearish on Chinese stocks. Cyclically, we continue to recommend an overweight stance, on the basis of an eventual reacceleration in economic activity. Feature Chart 1The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing

China’s economy is at a critical juncture: “Half-measured” stimulus so far has been able to keep the domestic economy in better shape than in the 2015-2016 down cycle, but overall economic activity has not bottomed (Chart 1). The Sino-America trade talk has resumed at the moment, but the two sides have yet to make any substantive progress towards a deal. In the meantime, the global economy has also reached a critical point where the degree of economic weakness has the potential to feed on itself, possibly triggering a recession.1 This underscores our tactically bearish stance towards Chinese stocks versus the global equity benchmark. Barring more forceful stimulus or resolution on the trade front, any external shock and/or internal policy missteps could easily tip the Chinese economy into a deeper growth slowdown. Hence, downside risks remain elevated for Chinese stocks over the next 3- to 6-months. The “D” Word Returns, But Won’t Spur Aggressive Further Easing Chart 2Industrial Price Deflation Returns

Industrial Price Deflation Returns

Industrial Price Deflation Returns

Economic data over the past two months have provided mixed signals. Readings from both China’s National Bureau of Statistics (NBS) PMI and from the Caixin PMI show an improvement in the manufacturing sector. However, industrial deflation has returned to China: Three years after the country declared victory against a prolonged industrial destocking cycle, producer price inflation (PPI) relapsed into negative territory in July and declined further in August (Chart 2). While prices are typically lagging indicators and reflect lingering effects from past economic conditions, there is not enough evidence in forward-looking economic data right now to suggest a turnaround in the economy is imminent.2 A deflationary PPI is not a trivial source of concern for Chinese policymakers. Last time growth in China’s PPI turned negative, it took policymakers four and a half years and an annualized 28% of GDP worth of credit expansion to pull the industrial sector out of its deflationary cycle. Chart 3Deflation Threatens Recovery In Industrial Profit Growth

Deflation Threatens Recovery In Industrial Profit Growth

Deflation Threatens Recovery In Industrial Profit Growth

For investors, deflation has pernicious effects on profits, and we have received several client inquiries concerning the topic since PPI growth turned negative. The historical relationship suggests profit growth for both the A-share and investable markets is highly linked to fluctuations in producer prices (Chart 3), and China’s industrial sector profit growth has already been rapidly deteriorating over the past 12 months. The good news is that we do not expect the current episode of PPI deflation to become as protracted as it did in 2012-2016, or as severe as in 2015-2016. Two reasons underpin our view: Since early-2018, monetary policy has been much easier than during past deflationary episodes. Monetary policy in the past year and half has been much more accommodative than in the three years leading to the deep industrial deflationary cycle in 2015, particularly on the exchange rate front. The RMB was soft-pegged to a rising U.S. dollar before it was decoupled by the PBoC in August 2015, and was appreciating against its trading partners throughout most of 2012-2015. Bank lending rates were also kept at historically high levels during this period (Chart 4). This time, even though money and credit growth has not returned to the same pace as in 2015-2016, current ultra-loose monetary conditions should spur enough credit growth to keep prices from deflating aggressively. Chart 4Monetary Conditions Easier Than Last Cycle

Monetary Conditions Easier Than Last Cycle

Monetary Conditions Easier Than Last Cycle

Inventory levels are low, and capacity levels do not appear to be overly excessive. After years of industrial consolidation, China’s industrial capacity does not appear to be particularly excessive compared to the past cycle. This is distinctively different from the prolonged contraction in PPI between 2012 and 2016, when China’s industrial inventories were coming off a five-year-long destocking cycle, and capacity utilization fell markedly (Chart 5). This is not the case today. Moreover, even though final demand has been weak, production has retrenched even more, drawing down inventories to the point where the pace of inventory destocking may have reached a cyclical bottom (Chart 6). A re-stocking of industrial goods should boost producers’ pricing power. Chart 5Capacity Is Not Excessively Underutilized

Capacity Is Not Excessively Underutilized

Capacity Is Not Excessively Underutilized

Chart 6Inventory Destocking May Be Bottoming Out

Inventory Destocking May Be Bottoming Out

Inventory Destocking May Be Bottoming Out

But the bad news (for investors), is that contained, or mild producer price deflation will not be reason alone to spur aggressive further easing from policymakers. This means that the re-emergence of price deflation, even mild and short-lived, will weigh on earnings and investor sentiment. Bottom Line: This episode of producer price deflation is unlikely to become as pernicious as occurred in the past, but policymakers are thus unlikely to act aggressively to counter it. While this removes some of the downside risks for Chinese stocks, even mild deflation will weigh on earnings growth (and thus sentiment) which underscores our tactically bearish stance on Chinese stocks. Demystifying China’s New Loan Prime Rate: Not The Stimulus You Are Looking For On August 20th, the PBoC launched a new loan prime rate (LPR) system, a revamped reference regime for setting bank loan interest rates3 (Chart 7). In September, the new LPR rate for one-year bank loans was lowered by five basis points. Since then, the market has been fixated on predicting whether the PBoC will cut the Medium-Lending Facility (MLF) rate next, which would be perceived as a change in China’s monetary stance. Chart 7China's New LPR: A Shadow 'Tax Cut'

China's New LPR: A Shadow "Tax Cut"

China's New LPR: A Shadow "Tax Cut"

PBoC will increase its control of the pricing of credit, while tight financial regulations will restrict the size and speed of credit growth. The new LPR reform, in our view, is designed to force state-owned (and better-capitalized) commercial banks to hand out a “tax cut” to struggling small- and medium-sized enterprises (SMEs) by lowering bank lending rates. At the same time, it allows the PBoC to take back control of the pricing of credit from commercial banks, “killing two birds with one stone.” There are three main market implications from this approach: The new LPR is likely to gradually narrow the gap between corporate bond yields (i.e. “market rates”) and bank lending rates; A cut in the MLF rate in the near term should be interpreted as a “reward” to commercial banks rather than a stimulus for the economy; Most importantly, the new LPR system does not mean rapid credit expansion is in the cards. Quite the opposite, in the near term, banks may tighten their lending. The wide spread between the 3-month interbank repo rate and average bank lending rate illustrates the reason why the PBoC has introduced the LPR.4 This gap is also evident when comparing the yield of AAA-rated corporate bonds and the average bank lending rate (Chart 8). These gaps exist because Chinese commercial banks have largely manipulated the 1-year bank lending rate set by the PBoC when lending to their “preferred customers,” usually state-owned enterprises and real estate developers, by offering significantly discounted loan rates. Banks then charge substantial “risk premiums” on loans to the private sector, mostly SMEs, to make up for the narrower profit margins on loans to SOEs (Chart 9). Chart 8An Impaired Monetary Policy Transmission Mechanism

An Impaired Monetary Policy Transmission Mechanism

An Impaired Monetary Policy Transmission Mechanism

Chart 9Evidence Of Asymmetrical Lending Practices

Evidence Of Asymmetrical Lending Practices

Evidence Of Asymmetrical Lending Practices

The new LPR system is designed to minimize this discrepancy, since the new LPRs are more market based and are quoted based on the price of loans banks charge their prime clients. By design, the new LPR system should force the average bank lending rate closer to the rate companies borrow in the bond market. This means bank lending rates will be guided lower, including lending rates for SMEs. However, the new system will be implemented in phases, and the PBoC is likely to gradually guide LPRs lower to allow banks to readjust their pricing models. The LPR rate is essentially the MLF rate plus bank profit margins (the added basis points above the MLF rate). The market will guide the top line lending rate, while the PBoC will have control over the floor rate (MLF) through open market operations. The fact that the PBoC is keeping the MLF rate unchanged while allowing the LPR to drop (albeit slightly) sends an explicit message: The PBoC is forcing banks to lower lending rates first before boosting their now-narrowed profit margins by lowering the MLF rate. In contrast to expectations of market participants that the LPR system will ease credit conditions, banks may actually tighten their lending in the coming months. While the PBoC will increase its control of the pricing of bank loans by the rate reform plan, the strengthening in financial regulations that has occurred over the past year will restrict the size and speed of credit growth. This combination has created more room for monetary easing without unleashing “animal spirits.” Borrowing costs to risky institutions have been higher since the Baoshang Bank takeover and are likely to remain elevated even if interest rates are lower (Chart 10). More importantly, mortgage and real estate developer loans together account for nearly 30% of total bank credit. Unless policymakers ease the brakes on lending restrictions to the property sector, bank lending growth is unlikely to pick up meaningfully (Chart 11). In fact, the PBoC has explicitly excluded mortgage and property-related lending from benefitting from the LPR rate cut.5 Barring a significant worsening in economic data, we do not expect the PBoC to lower mortgage lending and real estate-related loan rates in the coming months. Chart 10Tightened Financial Regulations Will Keep Cost Of Risky Lending High

Tightened Financial Regulations Will Keep Cost Of Risky Lending High

Tightened Financial Regulations Will Keep Cost Of Risky Lending High

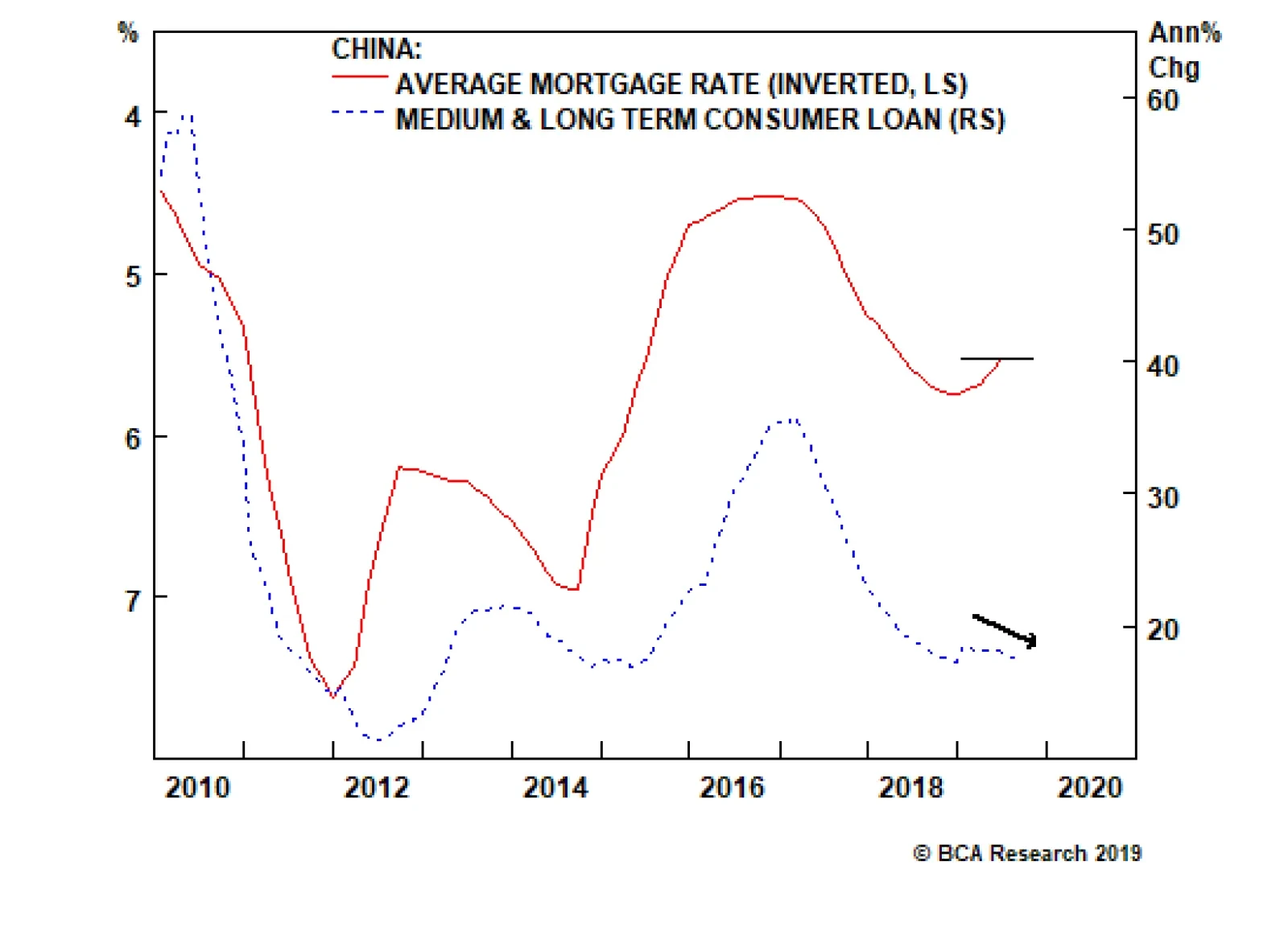

Chart 11Mortgage Rate Unlikely To Return To Its 2016 Low

Mortgage Rate Unlikely To Return To Its 2016 Low

Mortgage Rate Unlikely To Return To Its 2016 Low

Finally, in the next two- to three-quarter mandatory implementation period, banks will be readjusting their pricing and credit risk-assessing models. During the transition, we expect more cautious sentiment among both lenders and borrowers. Hence, in the short term, bank loan growth may actually moderate. Bottom Line: The new LPR system may lower China’s banking sector profits in the short term. But in the next 6- to 12-months, we expect the PBoC to compensate commercial banks by keeping ample liquidity in the interbank system and by eventually lowering the MLF rate. The new LPR system may slow bank credit growth in the next few months, but after its full implementation (by the second quarter of 2020), it will have the potential to make PBoC’s policy more effective. Investment Conclusions We expect two phases of Chinese equity relative performance over the coming year: one phase of flat-to-potentially seriously down performance to last from now until sometime in the first quarter of 2020 when the economy bottoms, and then a phase of outperformance. Our expectation that the economy will bottom in Q1 2020 rests on the existing reflationary response by Chinese policymakers and an improved monetary transmission mechanism. Chart 12We Expect The Chinese Economy To Bottom In Q1 2020

We Expect The Chinese Economy To Bottom In Q1 2020

We Expect The Chinese Economy To Bottom In Q1 2020