Policy

U.S. monetary conditions will continue to support asset prices and worldwide economic activity for the coming 18 months or so. The Fed will ease policy further and is a long way from tightening. We are still on track for three 25-basis-point rate cuts this…

Highlights The global manufacturing cycle is likely to bottom soon, and consumption and services remain robust. The risk of recession over the next 12 months is low. This suggests that equities will continue to outperform bonds. But the risks to this optimistic scenario are rising. A denting of consumer confidence and worsening of geopolitical tensions could hurt risk assets. We hedge this by overweighting cash. China remains reluctant for now to use aggressive monetary easing. Until it does, the less cyclical U.S. equity market should outperform. We may shift into EM and European equities when China ramps up stimulus and the manufacturing cycle clearly bottoms. To hedge against this upside risk, we go tactically overweight Financials, and reiterate our overweight on Industrials and neutral on Australia. Bond yields should continue their rebound. We recommend an underweight on duration and favor TIPS. Credit should outperform on the cyclical horizon, but high corporate debt is a risk – we recommend a neutral position. Recommendations

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Feature Overview Hedges All Around This is a particularly uncertain time for the global economy – and so a tricky one for asset allocators. Will manufacturing activity bottom soon, or will it drag down the services sector and consumption with it? Will bond yields continue their strong rebound? Is the Fed done cutting rates? Will China now ramp up monetary stimulus? Will Iran escalate a confrontation with Saudi Arabia? What will President Trump tweet about next? This is the sort of environment in which portfolio construction comes into its own. We have our view on all these questions, but our level of conviction is somewhat lower than usual. The way for investors to react is to plan asset allocation in such a way that a portfolio is robust in all the most probable scenarios. We expect the global manufacturing cycle to bottom soon. The Global Leading Economic Indicator is already picking up, and the Global PMI shows some signs of bottoming (Chart 1). The shortest-term lead indicator, the Citigroup Economic Surprise Index, has recently jumped in every region except Europe (Chart 2). (See also What Our Clients Are Asking on page 7 for some more esoteric indicators of cycle bottoms.) The bottoming-out is due to easier financial conditions over the past nine months, a stabilization in Chinese growth, and simply time – the down-leg in manufacturing cycles typically last 18 months, and this one peaked in H1 2018. Chart 1First Signs Of Bottoming

First Signs Of Bottoming

First Signs Of Bottoming

Chart 2Surprisingly Strong Surprises

Surprisingly Strong Surprises

Surprisingly Strong Surprises

At the same time, government bond yields should have further to rise. The Fed may cut rates once more but, given the resilient U.S. economy, no more than that. This is less than the 59 basis points of cuts over the next 12 months priced in by the Fed Fund futures. The recent pick-up in economic surprises suggests that the 10-year U.S. Treasury yield should return at least to where it was six months ago, 2.3-2.4% (Chart 3). This might be delayed, however, if there is an increase in political tensions, for example a break-up of the U.S./China trade talks (Chart 4). Chart 3Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Long-Term Rates To Rebound Further...

Chart 4...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

...But Geopolitical Tensions Remain A Risk

This implies that equities are likely to continue to outperform bonds over the next few quarters, and so we remain overweight global equities and underweight global bonds on the 12-month investment horizon. However, the risks to this rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II, usually about 18 months in advance (Chart 5). The 3-month/10-year curve inverted in the middle of this year. We also worry that the weakness in the manufacturing sector may dent consumer confidence. There are some signs of this in Europe and Japan – but none significant yet in the U.S. (Chart 6). Accordingly last month, as a hedge against an economic downturn, we went overweight cash, which we see as a more attractive hedge, from a risk/reward point-of-view, than bonds. Chart 5Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

Can We Ignore The Message From The Yield Curve?

Chart 6Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

Some Signs Of Weaker Consumer Confidence

We also remain overweight U.S. equities, which are lower-beta and have fewer structural headwinds than equities in other regions. However, we continue to look for an entry point into the more cyclical equity markets which would also be beneficiaries of bolder China stimulus. China’s monetary easing remains more tepid than in previous stimulus episodes. It has probably been enough to stabilize domestic activity (Chart 7) but not to trigger a rally in industrial commodity prices, EM assets, and euro area equities, as it did in 2016. A pick-up in global PMIs and signs of stronger Chinese credit growth would clearly help EM and Europe (Chart 8) but we need higher conviction that these things are indeed happening before making that move. In the meantime, we are hedging the upside risk by raising the global Financials sector tactically to overweight, since it would likely do well if euro area stocks started to outperform. Earlier this year, we raised the Industrials sector to overweight and Australian equities to neutral, also to hedge against the upside risk from more aggressive Chinese stimulus. Chart 7Chinese Stimulus Has Merely Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chinese Stimulus Has Merelyy Stabilized Growth

Chart 8Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Europe And EM Are The Most Cyclical Markets

Chart 9Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

Oil Price Spikes Often Precede Recessions

The biggest geopolitical risk to our sanguine scenario is the situation in the Middle East, after the attacks on Saudi oil refineries. Every recession in the past 50 years has been preceded by a 100% year-on-year spike in the crude oil price (though note that Brent would need to rise to over $100 a barrel by year-end, from $61 today, for that to eventuate (Chart 9)). A short-term oil shortage is not the problem since strategic reserves are ample. But the attack demonstrates the vulnerability of the Saudi installations. And a reprisal attack on Iran could lead it to block the Strait of Hormuz, through which more than 20% of global oil passes. We have an overweight on the Energy sector, partly as a hedge against these risks. BCA’s oil strategists expected Brent crude to rise to $70 this year, and average $74 in 2020, even before the recent attack. They argue that the risk premium in the oil price (the residual in Chart 10) is too low, given not only tensions with Iran, but also other potential supply disruptions in Iraq, Libya, Venezuela and elsewhere. Chart 10Is The Oil Risk Premium Too Low?

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Which Leading Indicators Should Investors Watch To Time The Rebound In Global Growth? Chart 11Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

Is Eurozone Manufacturing Close To A Bottom? Positive Signals For Global Growth

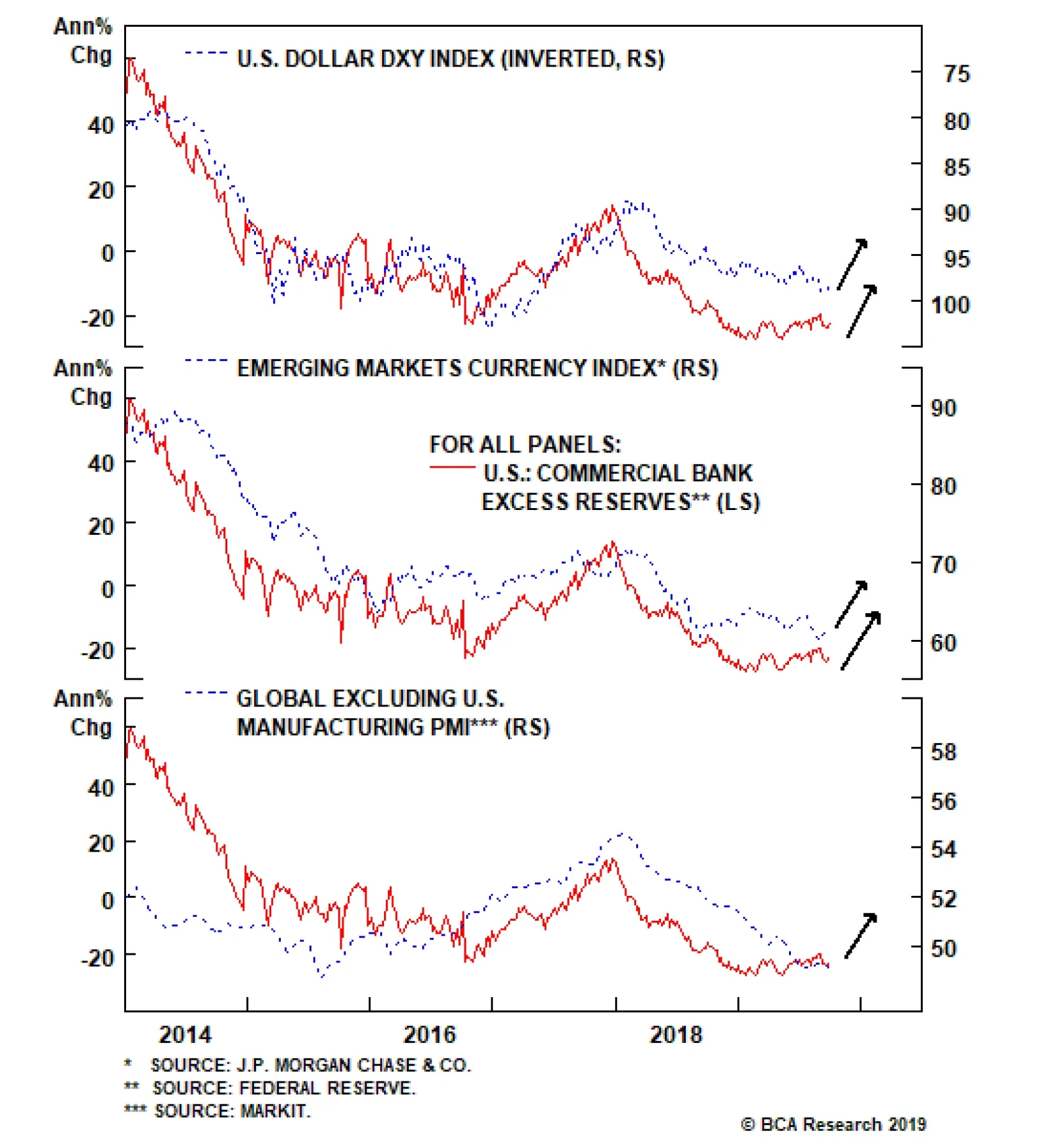

During 2019, the global growth decline was a key driver of the bond rally and the outperformance of defensive assets. Thus, timing when this decline will reverse will be crucial, since it would also result in a change of leadership from defensive to cyclical assets. But how can this be done? Below we list three of our favorite indicators that have provided reliable leading signals on the global economy in the past: Carry-trade performance: The performance of EM currencies with very high carry versus the yen tends to be a leading indicator for global growth (Chart 11, panel 1). In general, carry trades distribute liquidity from countries where funds are plentiful but rates of return are low (like Japan), to places with savings shortfalls and high risk, but where prospective returns are high. Positive performance of these currencies tends to signal a positive shift in global liquidity, which usually fuels global growth. Swedish inventory cycle: The Swedish new-orders-to-inventories ratio is a leading indicator of the global manufacturing cycle (panel 2). Why? Sweden is a small open economy that is very sensitive to global growth dynamics. Moreover, Swedish exports are weighted towards intermediate goods, which sit early in the global supply chain. This makes the Swedish inventory cycle a good early barometer of the health of the global manufacturing cycle. G3 monetary trends: G3 excess money supply – measured as the difference between money supply growth and loan growth – is a leading indicator of global industrial production (panel 3). As base money and deposits become more plentiful in the banking system relative to the pool of existing loans, the liquidity position of commercial banks improves. This provides banks with the necessary fuel to generate more loan growth, a development which eventually provides a boon to economic activity. Importantly, all these leading indicators are sending a positive signal on the global economy. This confirms our view that rates should go up as global growth strengthens. Therefore, investors should remain overweight equities and underweight bonds in their portfolios. Is It Time To Buy Euro Area Banks? In a Special Report on euro area banks in December 2018, we noted that “Historically, when the relative P/B discount hits the lower band and the relative dividend yield hits the upper band, a rebound in relative return performance could be expected”.1 Our recommendation back then was that “long-term investors should avoid banks in the region, but investors with a more tactical mandate and much nimbler style could use the valuation indicators to ‘time’ their entry into and exit out of banks as a short-term trade.” Since then, banks have continued to underperform the overall market by over 10%, further pushing down relative valuation metrics. Currently, both relative P/B and relative dividend yield are at extreme levels that have historically heralded at least a short-term bounce. The euro area PMI is still below 50, but there are signs that the euro area economy could rebound later this year, which should be positive for banks’ relative earnings. Already, forward EPS growth has been stabilizing relative to the broad market (Chart 12, panel 4). In addition, two of the key concerns back in December 2018 were Italian government debt and the unwinding of QE. Now Italian debt is no longer in crisis and the ECB has relaunched QE. As such, investors with a tactical mandate and a nimble style should buy (overweight) banks in the euro area. Long-term investors should still avoid such a short-term trade because structural issues remain. Chart 12Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Tactically Upgrade Euro Area Banks

Is The Gold Rally Over? Spot gold prices have increased 17% year-to-date, on the back of global growth weakness, dovish central banks, and rising political tensions. Should investors now pare back their gold exposure? Common sense would suggest they should. However, these are not ordinary times. In the short term, gold prices might suffer from some profit-taking due to overbought technicals and excessively positive sentiment (Chart 13, panel 1). Moreover, gold prices have moved this year due to increased market expectations of central bank easing (panel 2). We expect that markets will be disappointed going forward by only limited rate cuts, which could put downward pressure on gold. On the other hand, with approximately 27%, or $14.9 trillion, of global debt with negative yields at the moment, investors will continue to shift to the next best asset – zero-yielding gold (panel 3). This is clear from the rise in holdings of gold over the past few years by both central banks and investors (panels 4 & 5). We expect this trend to persist as investors continue their search to avoid negative yields and focus on capital preservation. Geopolitical tensions have intensified since the beginning of the year: ongoing yet inconclusive trade negotiations between the U.S. and China, implementation of further tariffs, Brexit uncertainty, and the recent military attacks in the Middle East (panel 6). This environment should also continue to push gold prices higher. We continue to recommend gold as a hedge against inflation – which we see picking up over the next 12 months – as well as against any further deterioration in global growth and the geopolitical situation. Chart 13Gold: Sell Or Hold?

Gold: Sell Or Hold?

Gold: Sell Or Hold?

Risks to the rosy scenario are rising. We remain concerned about the inverted yield curve, which has accurately forecast every recession since World War II. How Low Can Rates Go? The zero lower bound is a thing of the past. Last month, Denmark’s central bank cut rates to -0.75%, and 10-year government bonds in Switzerland hit a historic low for any major country, -1.12%. In the next recession, how much further could interest rates theoretically fall? For individuals, cash rates might be limited by the cost of storing paper currency, which has a zero yield (unless governments find a way to ban cash or charge an annual fee on it). A bank safety deposit box costs about $300 a year, and a professional-quality safe big enough to store $1 million (which would be a pile of $100 bills 31 x 55 cms, weighing 10 kg) costs $2,000 with installation costs. Amortize the latter over 10 years, and the cost of storing $1 million is about 0.2%-0.3% a year. Swiss franc bills – maximum denomination CHF1,000 – would cost less to store. But storage costs for physical gold are around 2% a year. Since rates have fallen below this, there must be other constraints. Individuals would find storing money in cash possibly dangerous and certainly very inconvenient (imagine having to transport the cash to a bank to pay a tax bill). And the cost for a rich individual or company of storing, say, $1 billion (weighing 10 tonnes) would be much higher. Given the history in even low-rate countries (Chart 14, panel 1), we suspect around -1% is the level at which cashholders would seek alternatives to bank deposits of government bills. Chart 14How Low Can They Go?

How Low Can They Go?

How Low Can They Go?

Chart 15Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

Yield Curves When Rates Are At Zero Or Below

At the long end, the yield curve does not typically invert much when short-term rates are zero or negative (Chart 15). The biggest 3-month/10-year inversion was in Switzerland earlier this year, -0.05%. This points then to the absolute lowest level for 10-year bonds anywhere, even in the middle of a nasty recession, at around -1.1%. That is a worry for asset allocators. It means that the maximum mathematical upside for Swiss government bonds from their current level (-0.8%) is 3% while it is 5% for German bonds (currently -0.5%). This is not much of a hedge. Only the U.S. looks better: if the 10-year Treasury yield falls to 0%, the total return is 18%. Global Economy Chart 16U.S. Growth Remains Solid

U.S. Growth Remains Solid

U.S. Growth Remains Solid

Overview: Industrial-sector growth globally has been weak, with the manufacturing PMI in most countries falling below 50. But consumption and services almost everywhere have remained resilient, even in the manufacturing-heavy euro area. And there are tentative signs of a bottoming-out in manufacturing. However, a full-scale rebound will depend on further monetary stimulus in China, where the authorities still seem cautious about rolling out easing on the scale of what was done in 2016. U.S.: U.S. manufacturing has now followed the rest of the world into contraction, with the ISM manufacturing index slipping below 50 in August (Chart 16, panel 2). However, consumption and services are holding up well. Employment continues to expand (albeit at a slightly slower pace than last year, perhaps because of a lack of jobseekers), there is no sign of a rise in layoffs, and consumer confidence remains close to a historical high (though it slipped slightly in September). Housing has recovered after last year’s slowdown, and the recent congressional budgetary agreement means fiscal policy will be mildly expansionary over the coming 12 months. Only capex (panel 5) has slowed, as companies postpone investment decisions due to uncertainty surrounding the trade war. The consensus expects U.S. real GDP growth of 2.2% this year, above most estimates of trend growth. Euro Area: Given its higher concentration in manufacturing, European growth is weaker than in the U.S. The manufacturing PMI has been below 50 since February, and fell further to 45.6 in August. Industrial production is shrinking by 2% year-on-year. Italy has experienced two negative quarters of growth, and Germany may also enter a technical recession in Q3 (GDP shrank by 0.1% in Q2). However, there are some tentative signs that manufacturing is bottoming: the ZEW survey in September, for example, surprised on the upside. And, like the U.S., consumption remains strong. Even in manufacturing-heavy Germany, employment continues to grow, and retail sales in July were up 4.4% year-on-year. In the U.K., however, uncertainty surrounding Brexit has damaged business investment, though employment has been strong.2 Chart 17First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

First Signs Of A Rebound In The Rest Of The World?

Japan: Consumption has already slipped, even before the consumption tax hike scheduled in October. Retail sales in July fell 2% year-on-year, due to negative wage growth and consumer sentiment falling to a five-year low. Manufacturing continues to suffer from China’s slowdown and the strong yen (up 6% over the past 12 months), with exports falling 6% and industrial production down 2% year-on-year over the past three months. The effect of the consumption tax hike may be cushioned by government measures (lowering taxes on autos and making high-school education free, for example). And a pickup in Chinese growth would boost exports. But there are scant signs yet of a bottoming in activity. Emerging Markets: China’s growth appears to have stabilized, with both manufacturing and non-manufacturing PMIs above 50 (Chart 17, panel 3). But confidence remains fragile, with retail sales growth slowing to a 20-year low and car sales down 7% in August, despite the introduction of cars compliant with new emissions standards. The authorities have responded with further easing measures (including a further cut in the reserve requirement in September) but seem reluctant to launch a full-scale monetary stimulus, similar to what they did in 2016. Elsewhere in EM, growth has slowed in countries with structural issues (latest year-on-year real GDP growth in Argentina is -5.7%, in Turkey -1.5% and in Mexico -0.8%) but remains fairly resilient elsewhere (India 5%, Indonesia 5%, Poland 4.2%, Colombia 3.4%). Interest Rates: Central banks almost everywhere have turned dovish, with the Fed cutting rates for a second time, the ECB restarting asset purchases, and the Bank of Japan signaling it will ease in October. But further monetary accommodation will probably be less than the market expects. The Fed signaled that its cuts were just a mid-cycle correction and that further easing is unlikely. And the ECB and BoJ have little ammunition left. With signs of growth bottoming, and the market understanding that central banks’ dovish turn is reaching its end, long-term rates, which have already risen in the U.S. from 1.45% to 1.72% in September, are likely to move higher. Investors should also carefully watch U.S. inflation, which is showing signs of underlying strength, with core CPI inflation rising 2.4% year-on-year in August (and as much as 3.4% annualized over the past three months). Global Equities Chart 18Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Has Earnings Growth Bottomed?

Still Cautious, But Adding An Upside Hedge: Global equities registered a small loss of 8 basis points in Q3 (Chart 18) despite all the headline risks from geopolitics and weakening economic data. Overall, our defensive country allocation worked well in Q3, since DM equities outperformed EM by 4.5%, and the U.S. outperformed the euro area by 2.8%. Our sector positioning did not do as well since underweights in Utilities and Consumer Staples and overweights in Industrials, Energy and Health Care all went in the wrong direction, even though the underweight in Materials did help to offset the loss. During the quarter, however, both sector and country rotations were evident within the global equity universe, in line with the wild swings in bond yields. September saw some reversals in DM/EM, U.S./euro area and cyclical/defensives. Going forward, BCA’s House View remains that global economic growth will begin to recover over the coming months, albeit a little later than we previously expected. As such, our defensive country allocation remains appropriate. We did put euro area and EM equities on upgrade watch in April,3 but the delay in the global recovery also implies that it is still not the time to trigger this call. With our view that bond yields have hit bottom,4 we are making one adjustment in our global sector allocation by upgrading Financials to overweight from neutral. We are financing this by cutting in half the double overweight in Health Care to overweight (see next page for more details). This adjustment also acts as a hedge against two possible outcomes: 1) that the euro area outperforms the U.S., and 2) that Elizabeth Warren wins in the upcoming U.S. presidential election.5 Upgrade Global Financials To Overweight From Neutral Chart 19Upgrade Global Financials

Upgrade Global Financials

Upgrade Global Financials

The relative performance of global Financials to the overall equity market has been hugely affected by the movements in global bond yields (Chart 19, panel 1). As bond yields made a sharp reversal in September, so did the relative performance of Financials, even though it is barely evident on the chart given how much Financials have underperformed the broad market over recent years. It’s not clear how sustainable the sharp reversal in bond yields will be, but BCA’s House View is that bond yields will move higher over the next 9-12 months. As such, we are upgrading Financials to overweight from neutral, for the following additional reasons: Valuations are extremely attractive as shown in panel 2. More importantly, the relative valuation is now at an extreme level that historically heralded a bounce in Financials’ relative performance. Loan quality has improved. The U.S. non-performing loan (NPL) ratio is nearing the lows reached before the Global Financial Crisis (GFC). Even in Spain and Italy, NPL ratios have fallen significantly, though they remain higher than they were prior to the GFC (panel 3). U.S. consumption has been strong, housing has rebounded, and demand for loans is getting stronger (panel 4), in line with data such as the Citi Economic Surprise Index, suggesting that economic data may have hit bottom. To finance this upgrade, we cut the double overweight of Health Care to overweight, as a hedge against Elizabeth Warren winning next year’s U.S. presidential election and tightening rules on drug pricing. Government Bonds Maintain Slight Underweight On Duration. Our below-benchmark duration call was severely challenged by the global bond markets in the first two months of the third quarter. The U.S. 10-year Treasury yield hit 1.43% on September 3 in response to the weaker-than-expected ISM manufacturing index in the U.S., 57 bps lower than the level at the end of previous quarter, and just a touch higher than the historical low of 1.32% reached on July 6, 2016. The rebound in bond yields since September 5, however, was driven not only by the ebb and flow in the U.S./China trade policy dynamics, but also by the positive surprises in economic data releases, as shown in Chart 20. BCA’s Global Duration Indicator, constructed by our Global Fixed Income Strategy team using various leading economic indicators, is also pointing to higher yields globally going forward. Investors should maintain a slight underweight on duration over the next 9-12 months. Favor Linkers Vs. Nominal Bonds. Global inflation expectations have also rebounded after continuing their downtrend in the first two months of the quarter. This largely reflects the acceleration in August in realized inflation measures such as core CPI, core PCE, and average hourly earnings. In addition, historically, the change in the crude oil price tends to have a good correlation with inflation expectations. The oil price jumped initially by 20% following the attack on the Saudi Arabian oil production facilities. While it’s not clear how the geopolitical tensions will evolve in the Middle East, a conservative assumption of a flat oil price until the end of the year still points to much higher inflation expectations, supporting our preference for inflation-linked bonds over nominal bonds. We also favor linkers in Japan and Australia over their respective nominal bonds (Chart 21). Chart 20Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Bond Yields Have Hit Bottom

Chart 21Favor Inflation Linkers

Favor Linkers

Favor Linkers

We continue to look for an entry point into more cyclical markets which would benefit from a bolder Chinese stimulus. Corporate Bonds Since we turned cyclically overweight on credit within a fixed-income portfolio, investment-grade bonds and high-yield bonds have produced 220 and 73 basis points, respectively, of excess return over duration-matched government bonds. We remain bullish on the outlook for credit over the next 12 months, as we expect global growth to accelerate before the end of the year. Historically, improving global growth has resulted in sustained outperformance of credit over government bonds. Moreover, default rates should remain subdued over the next year given that lending standards continue to ease (Chart 22, panel 1). How long will we remain overweight credit? High levels of leverage, declining interest coverage ratios, and the high share of Baa-rated debt in the U.S. corporate debt market continue to make credit a risky proposition on a structural basis. However, with inflation expectations still very low, the Fed has a strong incentive to keep monetary policy easy. This dovish monetary policy should keep interest costs at bay, helping credit outperform over the next year. That said, we believe that there are some credit categories that are more attractive than others. Specifically, we recommend investors favor Baa-rated and high yield securities, given that there is still room for further credit compression in these credit buckets (panel 2 and panel 3). On the other hand, investors should stay away from the highest credit categories, as they no longer offer value (panel 4). Chart 22Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Baa-rated And High-Yield Credit Offer The Most Value

Commodities Chart 23No Supply Shock In The Oil Market

Quarterly Portfolio Outlook: Hedges All Around

Quarterly Portfolio Outlook: Hedges All Around

Energy (Overweight): September’s drone attack on Saudi crude facilities sent oil prices soaring as much as 20% in the days following, before falling back to pre-attack levels. Initial estimates estimated the supply disruption at 5.7 million barrels a day – approximately 5.5% of global supply – making it the largest crude supply outage in history. However, assuming the Saudis can return 70% of the lost output back online as they claim, OPEC’s spare capacity, approximately 1.8 million barrels a day, should be able to balance the market and cover the remaining lost production.6,7 In the longer-term, a pick-up in global oil demand, as economic growth rebounds, plus supply tightness should keep oil price elevated, with Brent reaching $70 this year and averaging $74 in 2020 (Chart 23, panels 1 & 2). Industrial Metals (Neutral): A combination of half-hearted year-to-date stimulus by Chinese authorities and a stronger USD in the second and third quarters of 2019 have driven industrial metals spot prices lower. However, the Chinese government announced additional stimulus in September, with further bond issuance to finance infrastructure projects and an easing of monetary policy (panel 3). This should give some upside for industrial metal prices over the coming six-to-12 months. Precious Metals (Neutral): We remain positive on gold, despite its strong performance year-to-date, since we see it as a good hedge against recession, inflation, and geopolitical risks. We discuss gold in detail in the What Our Clients Are Asking section on page 9. Silver also looks attractive in the short term. The nature of the use of silver has changed over the past two decades, from being mostly a base metal for industrial fabrication to becoming more of a precious metal viewed as a safe haven. The correlation between gold and silver prices has increased since the Global Financial Crisis from an average of 0.5 pre-crisis to 0.8 post-crisis (panels 4 & 5). Global growth and political uncertainty should support silver prices in the coming months. Currencies U.S. Dollar: The trade-weighted dollar has appreciated by 2.5% since we turned neutral in April. We expect that the steep drop in yields will continue to ease financial conditions and help global growth in the last quarter of the year. Given that the dollar is a counter-cyclical currency, an environment where global growth rallies have historically been negative for the greenback. Euro: Since we turned bullish in April, EUR/USD has depreciated by 2.7%. Overall, we continue to be positive on EUR/USD on a cyclical timeframe. After the ECB cut rates by 10 basis points and announced further rounds of quantitative easing, there is not much room left for the euro area to keep easing relative to the U.S. (Chart 24, panel 1). Moreover, improving expectations of profit growth in the euro area vis-à-vis the U.S. will drive money flows towards Europe, pushing EUR/USD up in the process (panel 2). Emerging Market Currencies: We remain bearish on emerging market currencies for the time being. That being said, they remain on upgrade watch for the end of the year. There are multiple signs that global growth is turning up, a consequence of the easy financial conditions caused by some of the lowest bond yields on record. Moreover, the marginal propensity to spend (proxied by M1 growth relative to M2 growth) in China, the main engine of EM growth, continues to point to further appreciation in emerging market currencies (panel 3). Chart 24Interest Rate And Profit Expectation Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

The Euro Might Soon Pop Interest Rate And Profit Expectations Differentials Favor The Euro

Alternatives Chart 25Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Favor Hedge Funds Untill Global Growth Bottoms

Return Enhancers: Over the past 12 months, we have recommended investors pare back on private equity and increase allocations to hedge funds – macro hedge funds in particular. This was due to our judgement that we are late in the economic cycle. While we expect growth to pick up over the coming months, this is not yet clear in the data (Chart 25, panel 1). This uncertain macro outlook will prove tough for private equity funds, especially given an environment of rising multiples and increasing competition for deals. We continue to see global macro hedge funds as the best hedge ahead of the next recession and would advise investors to allocate funds now, given the time it takes to move allocations in the illiquid space. Inflation Hedges: In the current environment, TIPS are likely a better inflation hedge than illiquid alternative assets. Our May 2019 Special Report 8 showed that TIPS produce a particularly attractive risk-adjusted return during times when inflation is rising, but still fairly low (below 2.3%). TIPS should do well, therefore, in the environment we expect over the next few months, where the Fed remains dovish, cutting rates perhaps once more, while condoning a moderate acceleration of inflation (panel 2). Volatility Dampeners: Structured products – mostly Mortgage-Backed Securities (MBS) – have had an excellent record of reducing portfolio volatility (panel 3). Despite that, we do not recommend more than a neutral allocation to MBS currently due to a less-than-attractive valuation picture. Despite Treasury yields falling by more than 100 basis points this year and refinancing activity picking up, nominal MBS spreads remained near their all-time lows. However, as Treasury yields bottom, we expect refinancing to slow, putting downward pressure on spreads. Risks To Our View The most likely upside risk comes from the Fed being too dovish and falling behind the curve. Underlying inflation pressures in the U.S. remain strong (with core CPI up 3.4% annualized over the past three months). After two rate cuts, the Fed Funds rate is now comfortably below the neutral rate: 0.1% in real terms compared to a Laubach-Williams r* of 0.8% (Chart 26). Tightness in the money markets have pushed the Fed to start expanding its balance sheet again. If manufacturing growth accelerates next year, and wages and profits begin to rise, a stock market melt-up, similar to that in 1999, would be possible. Eventually, though, the Fed would need to raise rates (perhaps sharply) to kill inflation, which could usher in the next recession. There are a broader range of possible downside risks. As argued throughout this Quarterly, there are various possible triggers of recession: failure of China to stimulate, and a loss of confidence by consumers, in particular. Some models of recession put the risk over the next 12 months as high as 30% (Chart 27). Structurally, the biggest risk is probably the high level of corporate debt in the U.S. (Chart 28). A breakdown in the junk bond market, as seen briefly last December, could lead to companies failing to refinance the large amount of debt maturing over the next 18 months. Geopolitical risks also remain elevated and are, by nature, hard to forecast. The outcome of Brexit remains highly uncertain – though we see low risk of a no-deal exit. We expect trade talks between the U.S. and China to drag on, without a comprehensive deal, while a clear breakdown would be negative. Impeachment of President Trump is probably not a significant market event, but might hurt market sentiment briefly (particularly if it makes the election of Elizabeth Warren more likely). The Iran/Saudi conflict could escalate. Risk premiums may need to rise to take into account these threats. Chart 26Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Is The Fed Turning Too Dovish?

Chart 27What Risk Of Recession?

What Risk Of Recession?

What Risk Of Recession?

Chart 28Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Is Corporate Debt The Biggest Risk?

Footnotes 1Please see Global Asset Allocation Special Report, titled "Euro Area Banks: Value Play Or Value Trap?" dated December 14, 2018, available at gaa.bcaresearch.com. 2 Please see Foreign Exchange Strategy Special Report, “United Kingdom: Cyclical Slowdown Or Structural Malaise?”, dated 20 September 2019, available at fes.bcaresearch.com. 3Please see Global Asset Allocation Quarterly, titled "Quarterly - April 2019" dated April 1, 2019, available at gaa.bcaresearch.com. 4Please see Global Investment Strategy Weekly Report, titled "Bond Yields Have Hit Bottom," dated September 6, 2019, available at gis.bcaresearch.com. 5Please see Global Investment Strategy Weekly Report, titled "Elizabeth Warren And The Markets," dated September 13, 2019, available at gis.bcaresearch.com. 6Dmitry Zhdannikov and Alex Lawler “Exclusive: Saudi oil output to return faster than first thought - sources,” Reuters, dated Sepetmber 17, 2019. 7Please see Geopolitical Strategy Special Alert titled, “Attacks On Critical Infrastructure In KSA Raises Questions About U.S. Response,” dated September 16, 2019, available at gps.bcaresearch.com. 8Please see Global Asset Allocation Special Report, titled “Investors’ Guide To Inflation Hedging: How To Invest When Inflation Rises,” dated May 22, 2019, available at gaa.bcaresearch.com GAA Asset Allocation

Highlights The fundamentals of the U.S. economy remain strong but investors’ skittishness has caused stocks to fluctuate with the ebb and flow of news headlines. With investor sentiment playing a leading role, we introduce a simple framework for tracking the course of animal spirits. Earnings expectations are undemanding, risk appetite remains robust and the monetary policy backdrop is supportive of the expansion. However, geopolitical unpredictability and potential irrational exuberance send warning signals. We continue to believe that recession worries are overblown, but there is no rule that says bear markets can only occur alongside recessions. Although there are some areas of concern, our overall assessment of other potential bear market triggers does not suggest that trouble is at hand. Feature A bear can find plenty to worry about these days. The trade war is still casting a shadow over global trade prospects, global manufacturing activity is slowing, the U.K. and German economies contracted in the second quarter and recent attacks demonstrated that Middle Eastern oil facilities were more vulnerable than investors realized. The R-word has abounded in the financial press all summer and the number of Google searches for the term “recession” surged to levels last reached in the months leading to the Great Financial Crisis. The summer anxiety did not last, though. Powered by a perceived cooling of trade tensions and monetary support from the Fed, the S&P 500 has already recouped all of its summer losses. The market swings were not driven by the domestic macroeconomic backdrop, which remained largely unremarkable. The U.S. economy is slowing after 2018’s sugar rush, but is still getting enough fiscal support to grow at or above trend despite the global slowdown. To this point, the slowdown has been confined to manufacturing, and the history of past industrial production cycles suggests it has almost run its course. The service sector is resilient across the developed world and the fundamentals for U.S. consumption remain strong. Fundamentals are not the whole story, however, and they have lately taken a backseat to politicians’ whims. The resulting anxiety has made it relatively easy to surpass downwardly revised expectations (Chart 1), and we have little concern that the bottom is about to drop out of S&P 500 earnings. But earnings are only half of the equation. The multiple investors are willing to pay for those earnings is the other half, and they could be the key swing factor if earnings growth is going to remain in the low single digits. Chart 1Markets And Economic Data Are Out Of Sync

Markets And Economic Data Are Out Of Sync

Markets And Economic Data Are Out Of Sync

We introduce a simple framework for tracking animal spirits. Multiples are largely a function of investor enthusiasm, and we attempt to track it via the Ex-Recession Bear Market Checklist developed by our sister Global ETF Strategy service (Table 1). It seeks to measure animal spirits across six dimensions: expectations, prices, appetite, euphoria, policy and geopolitics. Constructing the checklist is necessarily subjective, and as such we consider it a welcome complement to our fundamental analysis. We remain deeply invested in searching out the coming equity market inflection point, and delving into animal spirits allows us to track a wider range of potential catalysts. Table 1Ex-Recession Bear Market Checklist

Euphoric Angst

Euphoric Angst

Expectations Chart 2Back To Sustainable Levels...

Back To Sustainable Levels...

Back To Sustainable Levels...

After calling for unusually strong late-cycle profits growth last year on the back of the cut in corporate tax rates, earnings expectations are undemanding relative to history (Chart 2). Consensus S&P 500 earnings estimates for the full year project just 1.5% growth over 2018. As of the beginning of last week, analysts had penciled in a 3% year-over-year decline in 3Q earnings for the S&P 500. Those estimates are likely to be revised even lower as corporations make sure they’ve underpromised in the final two weeks before 3Q earnings season kicks off. Perhaps the consensus is a bit too conservative. Even though the year-over-year benefits of corporate tax cuts are gone, the dovish pivots by the Fed and other major central banks will support earnings growth. In the U.S. in particular, where the economy is still strong, easier financial conditions should help extend the shelf life of the current expansion through 2020. Bottom Line: Earnings growth is not going to blast higher, but profits are unlikely to contract as long as the Fed continues to support the expansion. The earnings bar has been set very low, and it will be rather easy for S&P 500 companies to exceed it. Prices We keep close tabs on valuation metrics, though we try not to get too wrapped up in them. Expensive (cheap) stocks can get more expensive (cheaper) as investors can remain irrational for a while. Valuations only become prone to mean-revert when they reach extreme levels. Chart 3Restored Normal Mirror-Image Relationship

Restored Normal Mirror-Image Relationship

Restored Normal Mirror-Image Relationship

Forward multiples offer greater insight when considered in conjunction with forward earnings estimates. It is unusual for both earnings estimates and forward multiples to be extended at the same time, as they were in 2018, because investors are typically unwilling to pay high multiples when they suspect that earnings may be peaking. The more normal mirror-image relationship has restored itself this year, as projected earnings growth has slipped below its mean level, balancing out the above-mean forward multiple (Chart 3). Chart 4Definitely Elevated, But Not Problematic Yet

Definitely Elevated, But Not Problematic Yet

Definitely Elevated, But Not Problematic Yet

Other conventional valuation measures remain elevated but valuations within one standard deviation of the mean are far from extreme (Chart 4). The S&P 500 price-to-sales ratio is the only metric nearing the two-standard-deviation level that marks what we view as the beginning of extreme territory. It is worth noting valuations have only eroded modestly in the current global geopolitical backdrop. Though they slid in the wake of the first tariff announcement, they have mostly recovered and have seemed somewhat inured to subsequent escalations, which may suggest that investors are becoming complacent about trade threats. Bottom Line: Stocks are fully priced and the fact that valuations were only modestly affected by tariff uncertainty has gotten our attention. One-sigma deviations do not point to an immediate reversal, however, so we will wait for more metrics to approach the two-sigma threshold before raising a red flag on valuations. Appetite IPO activity is a proxy for animal spirits. Well-received IPOs are a sign that investors still have a hearty appetite for what the future might hold and suggests that they do not fear the imminent end of the bull market. If new issues are too well received, however, IPO appetite becomes a contrary indicator. When an IPO frenzy takes hold, it’s a sign that optimism has reached unsustainable levels and the end of the cycle must be near. For now, we judge that the IPO market is healthy but not too healthy. Chart 5Improved Corporate Health Or Heightened Risk Appetite?

Improved Corporate Health Or Heightened Risk Appetite?

Improved Corporate Health Or Heightened Risk Appetite?

We consider it healthy that the number of IPO deals has remained stable since 2017, though the fact that their average value has more than doubled over that time could be a sign that investors are willing to grant increasingly higher values to private and newly-public companies (Chart 5). The fact that a steadily increasing share of the companies commanding larger valuations have yet to turn a profit is somewhat unsettling (please see the “Euphoria” section, below). We are therefore encouraged that investors pushed back so vigorously against the IPO of We Work’s parent company. Media reports suggesting that the sub-lessor of office space may be valued around a quarter of management’s initial estimates indicates that institutional investors are not blindly chasing the next hot deal. The companies that have completed offerings this year have fared well. 60% of the U.S. companies that have gone public so far this year are trading above their initial offering price. The median “successful” IPO in 2019 has returned 50% since inception, while the median “unsuccessful” IPO lost 23%. This asymmetry and the larger number of “successful” IPOs suggests that IPOs continue to be generally well-received. Bottom Line: Investors’ appetite for new issues has held up despite a challenging geopolitical and global growth backdrop, while We Work’s struggles to attract a public ownership base suggests they have maintained some healthy skepticism. As it relates to the near-term outlook, we rate investor appetites as light green. Euphoria IPO activity can also offer a window into investor euphoria. The share of companies going public with negative earnings has reached levels last observed in the years preceding the dot-com crash. The fact that profitless IPOs are currently better received by investors than IPOs of profitable companies is a concern (Chart 6). Chart 6Getting Carried Away

Getting Carried Away

Getting Carried Away

While we noted that aggregate S&P 500 valuations are within normal ranges, valuations among the most highly valued stocks suggest that some exuberance has broken out. Using the backtest functionality of BCA’s Equity Trading Strategy platform,1 we devised baskets of the top deciles of stocks ranked by Price-to-Earnings, Forward Price-to-Earnings, Price-to-Tangible Book Value, Price-to-Sales and Price-to-Operating Cash Flow. Chart 7The Most Expensive Stocks Are Getting More Expensive

The Most Expensive Stocks Are Getting More Expensive

The Most Expensive Stocks Are Getting More Expensive

The rising median P/E ratio of the top-decile P/E stocks suggests that investors continue to support the highest valuations by piling into the most richly valued firms. The same pattern prevails for the top deciles of stocks ranked on the four other multiples (Chart 7). Four out of the five metrics we track are now at or above two standard deviations from their mean. Bottom Line: Demand for unprofitable companies’ IPOs and the extreme valuations of the highest-valued companies on a range of metrics suggest that investors have gotten a little carried away. We rate this dimension orange. Policy We previously noted that restrictive monetary policy has been a precondition for every recession in the last 50 years. Consistent with its repeated pledge to sustain the expansion as long as possible, the Fed delivered its second rate cut earlier this month, and central banks around the world have embarked on what is turning into a synchronized dovish pivot. Despite unanimous expectations of easier policy at its September meeting, the ECB managed to surprise somewhat dovishly with the announcement of an open-ended bond purchase program, dubbed “QE Infinity”. Other developed-economy central banks like the already accommodative Reserve Bank of New Zealand have been delivering dovish surprises in the form of larger-than-expected rate cuts. Bottom Line: Uber-dovish U.S. and global central banks should prolong the shelf life of the expansion. Geopolitics The U.S.-China trade war continues to loom as the biggest risk to the global economy and the main source of investor angst. The Iranian attack on critical Saudi Arabian infrastructure also has the potential to destabilize markets and exacerbate investor concerns. Our Geopolitical Strategy service could see U.S.-China tensions receding in the near term, but fear that Iran will be an ongoing irritant. The motivations on the U.S. side are straightforward: first and foremost, the current administration wants to be re-elected next November. It is way too early to call the election – we won’t know who will face off until next summer – but one ironclad law of presidential elections is surely on the administration’s mind. The incumbent party always loses the White House if a recession occurs during the campaign (Chart 8). If hard-nosed trade policy appeared to be pushing the economy in the direction of a recession, it is likely the administration would dial down its aggressiveness. Chart 8A 2020 Recession Is The Biggest Threat To Trump's Reelection Prospects

A 2020 Recession Is The Biggest Threat To Trump's Reelection Prospects

A 2020 Recession Is The Biggest Threat To Trump's Reelection Prospects

Enter the Iranians. Their (apparent) attack on critical Saudi oil facilities2 signals that Middle Eastern tensions could intensify and crude prices could blast higher. As we wrote last week, the U.S. economy is far less exposed to an oil price shock than it was in the ‘70s, due mainly to its emergence as the world’s largest oil producer, but the rest of the world is vulnerable. An oil price shock could induce a global ex-U.S. recession. The U.S. is a comparatively closed economy, and it regularly responds to global forces with a longer lag than other economies. It does eventually respond to them, however, and if an oil price shock leads to recessions in major economies in the rest of the world, it will ultimately threaten the U.S. economy. Keeping the expansion going through November 2020 may require U.S. policymakers to focus carefully on the Middle East to defuse the potential implications of Iranian belligerence. The administration may need to cool tensions with China to free up the bandwidth to deal with Iran, and also to prevent trade tensions’ marginal pressure on global growth from making the global economy more vulnerable to an oil price spike. Our overall assessment of bear market triggers does not suggest that trouble is imminent. The U.S.-China pause our geopolitical colleagues have been calling for would not be as beneficial for markets as a holistic trade settlement, but it appears to be materializing. In deference to China’s National Day celebrations, the U.S. will delay the tariff hike that was supposed to begin October 1st (from 25% to 30% on $250 billion worth of Chinese imports). China, for its part, has issued waivers for tariffs and promised to increase purchases of U.S. farm goods. A trade deal with Japan has also been agreed in principle and is slated to be signed any day, while U.S. relations with Europe are marginally improving.3 Bottom Line: The latest pause in trade tensions is boosting investor sentiment and risk-asset performance but the unpredictability of the current administration’s actions and public communications still have the potential to rattle markets. We rate this dimension orange. Investment implications We continue to believe that worries of a recession are overblown, but it might also take time for investors to overcome all of their concerns. A lot of fear is already discounted in the 2019 earnings estimates correction, bringing the bar quite low for corporate earnings to beat expectations. Coupled with an accommodative policy backdrop and still-robust investor appetites, the expansion still has room to run. Equities are not a slam dunk at this point in the cycle. Valuations are full, global growth is uncertain, and geopolitics are a wild card. Volatility is likely to be elevated and subject to sporadic spikes. We remain positive on the U.S. economy and continue to expect global growth will pick up later this year, however, so we continue to recommend that investors remain at least equal weight equities in balanced portfolios. Jennifer Lacombe, Senior Analyst jenniferl@bcaresearch.com Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Available at https://ets.bcaresearch.com/ 2 Abqaiq is the most important oil-processing facility in the world, and the Khurais oil field is adjacent to the Ghawar oil field, the world’s largest. 3 Please see BCA Research Geopolitical Strategy Weekly Report “Trump’s Tactical Retreat”, published September 13, 2019. Available at gps.bcaresearch.com.

Highlights The world remains mired in a manufacturing recession. As such, it is still too early to put on fresh pro-cyclical trades. Focus on the crosses rather than outright U.S. dollar bets. Two new trade ideas: sell EUR/NOK and buy GBP/JPY. Also consider selling the gold/silver ratio. Feature Currency markets tend to trade into and out of various regimes. This means that to be an effective FX manager, you have to be extremely fluid. For example, interest rate differentials might dominate FX moves during a particular period, pivoting your job to a central bank monitor. Other times, flows dominate, perhaps even equity flows, like when a disruptive technology is developed in a specific market. The outperformance of U.S. equities, specifically technology stocks, is a case in point. Balance-of-payments dynamics usually matter mostly at critical turning points, making them not very useful as timing indicators. The exorbitant privilege of the U.S. dollar we discussed a fortnight ago is also a case in point. But more often than not, being able to identify whether the investment climate is about to become more hostile or not could be the key difference between being a successful FX manager or a relic. There has been no shortage of news for investors to digest over the last few days, from the Brexit imbroglio, to the Fed, to the drone attacks in Saudi Arabia and finally to U.S. President Donald Trump’s possible impeachment. But the most perplexing (and perhaps the most important) has been the German manufacturing flash PMI print for the month of September of 41.4, the lowest in over a decade (Chart I-1). If the country with the “cheapest currency” cannot manage to pull itself out of a manufacturing recession, then the message to the periphery is clearly that they have an impending problem. In short, our contention that the euro was close to a bottom might be offside by a few months, based on the latest manufacturing data release (Chart I-2). Chart I-1A Eurozone Manufacturing Recession

A Eurozone Manufacturing Recession

A Eurozone Manufacturing Recession

Chart I-2The Euro Needs Stronger Growth

The Euro Needs Stronger Growth

The Euro Needs Stronger Growth

Which FX Regime? Chart I-3A Recession Will Be Dollar Bullish

A Few Trade Ideas

A Few Trade Ideas

The performance of the dollar since the 10/2 yield curve inverted is instructive. So far, we are tracking both the 2005 and 1998 roadmaps, meaning the window for cautious optimism on risk assets could still pan out (Chart I-3). Specifically, the dollar tends to rally during recessions but the window before the dollar bull market takes hold can be quite long. In both 2006 and 1998, the dollar eventually catapulted higher, but it took longer than 12 months. Having an accurate recession probability-timing model is therefore crucial for strategy. Historically, domestic flows have been a very timely indicator, since repatriation by residents occurs during episodes of severe capital flight. In 2005, domestic individuals were deploying funds outside the U.S., which suggested patience before positioning for dollar strength. This made sense, since the return on capital was higher outside the U.S. with the EM and commodity bull market in full swing. More often than not, FX markets tend to favor regions with the highest return on capital. These tend to be the most difficult to bet against, but potentially the most potent blindside at turning points. If economic data continues to deteriorate due to much larger endogenous factors, a defensive strategy is clearly warranted. One way to tell will be an emerging divergence between our leading indicators and actual underlying data as is occurring so far in September. On the flip side, any specter of positive news could light a fire under sectors, currencies and countries that have borne the brunt of the slowdown. Both are highly risky bets. For now, we prefer to focus on the crosses rather than outright U.S. dollar bets. Sell EUR/NOK Sometimes, the best ideas are the simplest ones. The Norges bank is the most hawkish G-10 central bank, while the European Central Bank restarted QE at its latest meeting. This is a powerful catalyst for a short EUR/NOK trade: The dollar tends to rally during recessions but the window before the dollar bull market takes hold can be quite long. The slowdown in the euro zone has been concentrated in the manufacturing sector, but the deflationary impulse is starting to shift to other parts of the economy. Euro area overall core CPI continues to blast downwards, which has historically been a bad omen for the euro (Chart I-4). We expect euro zone inflation expectations to eventually rise, in part helped by the recovery in oil prices (Chart I-5), but this will also benefit the Norwegian krone. EUR/NOK has historically tracked the performance of relative stock prices between Europe and Norway, but a gaping wedge opened up in 2018 (Chart I-6). This divergence is unsustainable. In short, it is a bet on oil fields in Norway versus European banks. The ECB’s tiering of reserves might prevent euro zone banks from teetering over the edge, but unless the manufacturing recession ends soon and firms start to borrow to invest, banks will continue to have a demand problem. Meanwhile, the flareup in the Middle East means that oil prices will remain bid in the near term. This should favor Norwegian equities over those in the euro zone, and be negative for EUR/NOK (Chart I-7). 10-year German bunds are yielding -0.57% while the yield pickup on Norwegian bonds is a positive carry of 1.8%, despite liquidity concerns. In their latest policy meeting, Central Bank Governor Øystein Olsen stressed that Norway had much more fiscal room to maneuver in the event of a downturn, meaning the supply of Norwegian paper could increase, easing the liquidity premium. Chart I-4Deflation Remains Predominant In The Eurozone

Deflation Remains Predominant In The Eurozone

Deflation Remains Predominant In The Eurozone

Chart I-5A Rise In Oil Prices Will Help Inflation Expectations

A Rise In Oil Prices Will Help Inflation Expectations

A Rise In Oil Prices Will Help Inflation Expectations

Chart I-6Stocks And Currencies: An Unsustainable Divergence

Stocks And Currencies: An Unsustainable Divergence

Stocks And Currencies: An Unsustainable Divergence

Chart I-7Higher Oil is Negative ##br##For EUR/NOK

Higher Oil is Negative For EUR/NOK

Higher Oil is Negative For EUR/NOK

Bottom Line: Sell EUR/NOK at 9.937. Buy GBP/JPY Last week’s Special Report made the case for a cyclical recovery in the U.K., even though structural factors remain a headwind. This week, we are re-attempting to buy cable versus the yen: Most importantly, the Bank of England stood pat at its latest policy meeting while the Bank of Japan is likely to introduce more stimulus or stronger guidance. Real interest rate differentials favor a stronger pound. Most importantly, the Bank of England stood pat at its latest policy meeting while the Bank of Japan is likely to introduce more stimulus or stronger guidance (Chart I-8). Chart i-8A Tactical Bounce In GBP/JPY Is Likely

A Tactical Bounce In GBP/JPY Is Likely

A Tactical Bounce In GBP/JPY Is Likely

Chart I-9The Benefit Of A Weaker Pound

The Benefit Of A Weaker Pound

The Benefit Of A Weaker Pound

Speculators are very short the pound while they have been covering their short bets on the yen, as the investment environment has become more uncertain. The fall in the pound should begin to improve the U.K.’s balance-of-payment dynamics relative to Japan (Chart I-9). Bottom Line: Buy GBP/JPY at 132.6. Concluding Thoughts We continue to track various indicators for the dollar, from interest rate differentials, balance-of-payment dynamics, valuations, portfolio flows and positioning – and none of them are sending a bullish signal at the moment. Global growth remains in a funk, which has been supercharging dollar bulls. However, long-dollar bets remain susceptible should global growth stabilize. Our strategy is to continue focusing on the crosses until categorical evidence emerges that global growth has bottomed. In our trading portfolio, we continue to favor the NOK, SEK, petrocurrencies and the AUD. So far, these trades have been implemented at the crosses to limit downside risk, should our view on the dollar be offside. We intend to eventually start placing outright dollar bets once evidence emerges that global growth has bottomed and the world has skidded a recession. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been relatively strong: The Markit flash manufacturing PMI rebounded to 51 in September from 50.3. Flash services PMI increased to 50.9. The Chicago Fed national activity index increased to 0.1 from -0.4 in August. The Richmond Fed manufacturing index fell to -9 in September from 1. The Conference Board consumer confidence fell to 125.1 in September from 135.1. On the housing front, home prices grew by 0.4% month-on-month in July. Mortgage applications decreased by 10% for the week ended September 20th, but new home sales increased by 7% month-on-month in August. Initial jobless claims increased to 213,000 for the week ended September 20th. Annualized GDP growth was unchanged at 2% quarter-on-quarter in Q2. Trade deficit of goods was little changed at $72.8 billion. Headline and core PCE increased to 2.4% and 1.9% quarter-on-quarter, respectively in Q2. The DXY index appreciated by 0.6% this week. The recent data from the U.S. have been holding up quite well compared with the rest of the world. Net speculative positions on the greenback remain elevated due to U.S. relative strength. While we see dollar resilience in the near term, declining net foreign purchases of U.S. securities, diminishing interest rate differentials and the plunging bond-to-gold ratio all suggest the path of least resistance for the dollar is down. Report Links: Preserving Capital During Riot Points - September 6, 2019 Has The Currency Landscape Shifted? - August 16, 2019 USD/CNY And Market Turbulence - August 9, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area continue to deteriorate: The Markit flash manufacturing and services PMIs for the euro area both fell to 45.6 and 52, respectively in September. In France, the Markit flash manufacturing PMI fell to 50.3; services PMI decreased to 51.6. In Germany, the manufacturing PMI collapsed to 41.4; services PMI fell to 52.5. German IFO current assessment increased to 98.5 in September. However, the IFO expectations fell to 90.8. Monetary supply (M3) grew by 5.7% year-on-year in August. German Gfk consumer confidence nudged up to 9.9 in October. The EUR/USD fell by 0.8% this week. The recent data from the euro area has unfortunately showed no signs of global growth bottoming. The manufacturing PMI in Germany is now at its lowest level since the Great Financial Crisis. A major concern faced by investors is that weak activity in manufacturing may have already begun to infiltrate the service sectors. That said, the services PMIs in major economies, though falling, still remain in expansionary territory above 50. Report Links: Battle Of The Central Banks - June 21, 2019 EUR/USD And The Neutral Rate Of Interest - June 14, 2019 Take Out Some Insurance - May 3, 2019 Japense Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: National headline inflation fell from 0.5% year-on-year to 0.3% year-on-year in August. Core inflation was unchanged at 0.6% year-on-year. The Markit flash manufacturing PMI fell to 48.9 in September from 49.3. Services PMI also fell to 52.8 from 53.3. The leading index and coincident index were both little changed at 93.7 and 99.7, respectively, in July. The USD/JPY has been flat this week. Japanese exports have been weak, weighed by the global trade war and manufacturing slowdown. However, accordingly to the BoJ, domestic demand has remained firm, and capex also continues to increase. Moreover, the consumption tax hike next month will probably have a marginal impact compared with previous tax hikes. In a speech this week, BoJ Governor Haruhiko Kuroda emphasized that the central bank will ease without hesitation if the economy loses momentum. Report Links: Has The Currency Landscape Shifted? - August 16, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 Battle Of The Central Banks - June 21, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

There is little data from the U.K. this week: Mortgage approvals decreased slightly to 42,576 in August from 43,303 in July. The GBP/USD fell by 1.4% this week. British Prime Minister Boris Johnson has now lost his majority in Westminster after large profile defections from the so-called rebels, thus another election is highly likely by year-end. Besides, a further delay of Brexit is almost certain. We have downgraded the probability for a no-deal Brexit. We remain positive on the pound and are buying GBP/JPY this week. Report Links: United Kingdon: Cyclical Slowdown Or Structural Malaise? - September 20, 2019 Battle Of The Central Banks - June 21, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mixed: The preliminary commonwealth manufacturing PMI fell to 49.4 in September from 50.9 in August. On the other hand, the services PMI rebounded to 52.5 from 49.1, back to above-50 expansionary territory. Consumer confidence increased to 110.1 from 109.3 this week. The AUD/USD fell by 1% this week. Reserve Bank of Australia Governor Philip Lowe commented on Tuesday that the Australian economy is picking up, and is now at a “gentle turning point.” The previous rate cuts have allowed the property markets in big cities like Sydney and Melbourne to regain some strength, but will likely take longer to flow through the whole economy. In terms of monetary policy, Governor Lowe reiterated his commitment to ease monetary conditions when needed, though he did not signal an imminent move for next week. Australia has a large beta to global shifts as a small, open economy. Should the global manufacturing recession come to an end, the positive fundamentals will continue to lift the Australian economy through the rest of the year and into 2020. Report Links: A Contrarian View On The Australian Dollar - May 24, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Imports increased by NZ$30 million to NZ$5.69 billion in August, while exports fell by NZ$830 million to NZ$4.13 billion. The total trade deficit widened from NZ$700 million to NZ$1.57 billion. The NZD/USD appreciated by 1% initially, then plunged after the Reserve Bank of New Zealand’s policy meeting, returning flat this week. As widely expected, the RBNZ kept its official cash rate unchanged at 1% this Wednesday while signaling that there is more scope to ease if necessary amid a global slowdown. The market is currently pricing an 80% probability of a rate cut for the next policy meeting in November, reflecting weak business confidence. We are playing the kiwi weakness through the Australian dollar and Swedish krona, which are 1.9% and 1.95% in the money, respectively. Report Links: USD/CNY And Market Turbulence - August 9, 2019 Where To Next For The U.S. Dollar? - June 7, 2019 Not Out Of The Woods Yet - April 5, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been resilient: Bloomberg Nanos confidence increased to 57.4 this week from 56.7. Retail sales increased by 0.4% month-on-month in July, lower than the expectations of a 0.6% monthly growth. The USD/CAD has been flat this week. Oil prices have been on a wild ride this year. Since the drone attack a fortnight ago, Saudi Arabia has claimed that it is recovering faster than expected, beating its own targets. Brent crude oil spot prices have fallen by 6% from their September 16th peak, while Western Canada Select (WCS) oil prices have dropped by 12.3%, dampening the loonie’s upside potential. Report Links: Preserving Capital During Riot Points - September 6, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been mostly negative: The trade balance narrowed to CHF 1.2 billion in August from CHF 2.6 billion in July. Credit Suisse survey expectations came in at -15.4 in September, up from the last reading of -37.5 in August. The USD/CHF has been flat this week. As a small, open economy, Switzerland belongs to those countries with highest foreign trade-to-GDP share. The trade balance in August has been the lowest since January 2018, with lower exports of main goods including chemical and pharmaceutical products. Among trading partners, exports to Germany, Italy, and France all declined, reflecting the recent manufacturing slowdown in Europe. That said, we remain positive on the safe-haven Swiss franc during the risk-off period amid trade war uncertainties, Brexit chaos, Middle-East tensions, and more recently, the Trump Impeachment imbroglio. Report Links: What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

There is scant data from Norway this week: The unemployment rate increased to 3.8% in July, 0.6 percentage points higher than in April, accordingly to the recent Labour Force Survey. The USD/NOK appreciated by 0.5% this week. The Norges Bank, the one and only hawkish central bank among the G-10, raised its interest rate by 25 basis points to 1.5% last week. Since last September, the Norges Bank has hiked rates four times in total, resulting in a one-percentage-point increase in rates. The central bank stated that “the Norwegian economy has been solid; Employment has risen; Capacity utilization appears to be somewhat above a normal level; Inflation is close to target.” A higher interest rate would also help take the wind out of skyrocketing house prices and household debt levels. In addition, the central bank lowered its projection path for the krone, stating that the factors it outlined, including weaker activity in the petroleum sector, would probably keep weighing on the krone in the years ahead. Report Links: Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Currency Complacency Amid A Global Dovish Shift - April 26, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been negative: Consumer confidence fell to 90.6 in September. PPI yearly growth fell from 2% in July to 1.4% in August. Trade balance shifted to a deficit of SEK 5.4 billion in August. USD/SEK has been flat this week. We are closely monitoring the Swedish foreign trade as a leading indicator for global growth. The Swedish trade balance has shifted to a deficit for the first time this year. However, compared to last August, the deficit was narrowed by SEK 2.6 billion. Year to date, the Swedish trade surplus amounted to SEK 27 billion. Notably, the trade in goods with non-EU countries resulted in a surplus of SEK 6.6 billion, while the trade with EU resulted in a deficit of SEK 12 billion. Report Links: Where To Next For The U.S. Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

The Indian government resorted to an unexpected large corporate income tax cut last week. The government reduced the effective corporate tax rate from 35% to around 25%. If domestic bond yields rise materially in response to this fiscal stimulus, share…

The market is priced for roughly one more 25 bps rate cut before the end of the year. More specifically, the fed funds futures market is split 50/50 on whether that rate cut occurs at the October or December FOMC meeting. The market currently sees only a 4%…

Fed Chairman Jerome Powell had his work cut out for him at last week’s FOMC press conference. First, he had to craft a coherent message about the Fed’s reaction function following a meeting where three voting members dissented from the committee’s decision to…

Highlights Pension reform in Brazil is pushing through. The upcoming 12-18 months offer a window of opportunity, most notably on the privatization and tax reform front. Ongoing efforts should sustain an improvement in “animal spirits” in the short term and create some potential for structural improvements over the long term. Nevertheless, Brazil’s slow grinding economic recovery remains vulnerable to a negative external or domestic shock that could cause it to “stall speed”. If structural reforms or the business cycle hit stall speed, financial markets will sell off. Weighing the pros and cons, we are upgrading Brazil from underweight to neutral. Feature Pension Reform Will (Eventually) Pass, But What Next? Recent progress on Brazil’s economic reform agenda is market-positive but is clearly at risk of “stall speed”1 if reform momentum is not sustained after the likely passage of social security cuts. Having cleared the Chamber of Deputies, the pension reform bill is now likely to pass the senate. The first round of voting is expected any day now and the government’s senate leader, Fernando Bezerra, expects the bill to pass the second round by mid-October (Diagram I-1). Diagram I-1Brazil: Pension Reform Timeline

Brazil: Just Above "Stall Speed"

Brazil: Just Above "Stall Speed"

Chart I-1Pension Bill Will See The Light Of Day

Brazil: Just Above "Stall Speed"

Brazil: Just Above "Stall Speed"