Policy

BCA takes pride in its independence. Strategists publish what they really believe, informed by their framework and analysis. Occasionally, this independence results in strongly diverging views and we currently are in one of those times. Within BCA, two views on the cyclical (six to 12-months) outlook for assets have emerged. One camp expects global growth to rebound in the second half of the year. Along with accelerating growth, they anticipate stock prices and risk assets to remain firm, cyclical equities to outperform defensive ones, safe-haven yields to move up, and the dollar to weaken. Meanwhile, another group foresees a further deterioration in activity or a delayed recovery, additional downside in stocks and risk assets, outperformance of defensives relative to cyclicals, low safe-haven yields, and a generally stronger dollar. For the sake of transparency, we have asked representatives of each camp to make their case in a round-table discussion, allowing our clients to decide for themselves which view is more appealing to them. Global Investment Strategy’s Peter Berezin, U.S. Investment Strategy’s Doug Peta, and Global Fixed Income Strategy’s Rob Robis take the mantle for the bullish camp. U.S. Equity Strategy’s Anastasios Avgeriou, Emerging Market Strategy’s Arthur Budaghyan, and European Investment Strategy’s Dhaval Joshi represent the bearish group.1 The round-table discussion below focuses on the cyclical outlook. For longer investment horizons, most strategists agree that a recession is highly likely by 2022. Moreover, on a long-term basis, valuations in both risk assets and safe-haven bonds are very demanding. In this context, a significant back up in yields could hammer risk assets. The BCA Round Table Mathieu Savary: Yield curve inversions have often been harbingers of recessions. Anastasios, you are amongst those investors troubled by this inversion. Do you not worry that this episode might prove similar to 1998, when the curve only inverted temporarily and did not foreshadow a recession? Moreover, how do you account for the highly variable time lags between the inversion of the yield curve and the occurrence of a recession? Anastasios Avgeriou: The yield curve inverts at or near the peak of the business cycle and it eventually forewarns of upcoming recessions. This past December, parts of the yield curve inverted and now, BCA’s U.S. Equity Strategy service is heeding the signal from this simple indicator, especially given that the SPX has subsequently made all-time highs as our research predicted.2 Chart 1 (ANASTASIOS)The 1998 Episode Revisited

The 1998 Episode Revisited

The 1998 Episode Revisited

The yield curve inversion forecasts a Fed rate cut, and it has never been wrong on that front. It served well investors that heeded the message in June of 1998 as the market soon thereafter fell 20% in a heartbeat. If investors got out at the 1998 peak near 1200 and forwent about 350 points of gains until the March 2000 SPX cycle peak, they still benefited if they held tight as the market ultimately troughed near 777 in October 2002 (Chart 1). With regard to timing the previous seven recessions using the yield curve, if we accept that mid-1998 is the starting point of the inversion, it took 33 months before the recession commenced. Last cycle, the recession began 24 months after the inversion. Consequently, December 2020 is the earliest possible onset of recession and September 2021, the latest. Our forecast calls for SPX EPS to fall 20% in 2021 to $140 with the multiple dropping between 13.5x and 16.5x for an SPX end-2020 target range of 1,890-2,310.3 In other words we are not willing to play a 100-200 point advance for a potential 1,000 point drawdown. The risk/reward tradeoff is to the downside, and we choose to sit this one out. Mathieu: Rob, you take a much more sanguine view of the current curve inversion. Why? Rob Robis: While the four most dangerous words in investing are “this time is different,” this time really does appear to be different. Never before have negative term premia on longer-term Treasury yields and a curve inversion coexisted (Chart 2). Longer-term Treasury yields have therefore been pushed down to extremely low levels by factors beyond just expectations of a lower fed funds rate. The negative Treasury term premium is distorting the economic message of the U.S. yield curve inversion. Chart 2 (ROB)Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Negative Term Premium Distorting The Economic Message Of An Inverted Yield Curve

Term premia are depressed everywhere, as seen in German, Japanese and other yields, reflecting the intense demand for safe assets like government bonds during a period of heightened uncertainty. Global bond markets may also be discounting a higher probability of the ECB restarting its Asset Purchase Program, as term premia typically fall sharply when central banks embark on quantitative easing. This has global spillovers. Prior to previous recessions, U.S. Treasury curve inversions occurred when the Fed was running an unequivocally tight monetary policy. That is not the case today. The real fed funds rate still is not above the Fed’s estimate of the neutral real rate, a.k.a. “r-star,” which was the necessary ingredient for all previous Treasury curve inversions since 1960 (Chart 3). Chart 3 (ROB)Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Fed Policy Is Not Tight Enough For Sustained Curve Inversion

Mathieu: The level of policy accommodation will most likely determine whether Anastasios or Rob is proven right. Peter, you have been steadfastly arguing that policy, in the U.S. at least, remains easy. Can you elaborate why? Peter Berezin: Remember that the neutral rate of interest is the rate that equalizes the level of aggregate demand with the economy’s supply-side potential. Loose fiscal policy and fading deleveraging headwinds are boosting demand in the United States. So is rising wage growth, especially at the bottom of the income distribution. Given that the U.S. does not currently suffer from any major imbalances, I believe that the economy can tolerate higher rates without significant ill-effects. In other words, monetary policy is currently quite easy. Of course, we cannot observe the neutral rate directly. Like a black hole, one can only detect it based on the effect that it has on its surroundings. Housing is by far the most interest rate-sensitive sector of the economy. If history is any guide, the recent decline in mortgage rates will boost housing activity in the remainder of the year (Chart 4). If that relationship breaks down, as it did during the Great Recession, it would suggest that the neutral rate is quite low. Chart 4 (PETER)Declining Mortgage Rates Bode Well For Housing

Declining Mortgage Rates Bode Well For Housing

Declining Mortgage Rates Bode Well For Housing

Given that mortgage underwriting standards have been quite strong and the homeowner vacancy is presently very low, our guess is that housing will hold up well. We should know better in the next few months. Mathieu: Dhaval, you do not agree. Why do you think global rates are not accommodative? Dhaval Joshi: Actually, I think that global rates are accommodative, but that the global bond yield can rise by just 70 bps before conditions become perilously un-accommodative. Here’s where I disagree with Peter: for me, the danger doesn’t come from economics, it comes from the mathematics of ultra-low bond yields. The unprecedented and experimental panacea of our era has been ‘universal QE’ – which has led to ultra-low bond yields everywhere. But what is not understood is that when bond yields reach and remain close to their lower bound, weird things happen to the financial markets.

Chart 5

I refer you to other reports for the details, but in a nutshell, the proximity of the lower bound to yields increases the risk of owning supposedly ‘safe’ bonds to the risk of owning so-called ‘risk-assets’. The result is that the valuation of risk-assets rises exponentially (Chart 5). Because when the riskiness of the asset-classes converges, investors price risk-assets to deliver the same ultra-low nominal return as bonds.4 Comparisons with previous economic cycles miss the current danger. The post-2000 policy easing distorted the global economy by engineering a credit boom – so the subsequent danger emanated from the most credit-sensitive sectors in the economy such as mortgage lending. In contrast, the post-2008 ‘universal QE’ has severely distorted the valuation relationship between bonds and global risk-assets – so this is where the current danger lies. Higher bond yields can suddenly undermine the valuation support of global risk-assets whose $400 trillion worth dwarfs the global economy by five to one. Where is this tipping point? It is when the global 10-year yield – defined as the average of the U.S., euro area,5 and China – approaches 2.5%. Through the past five years, the inability of this yield to remain above 2.5% confirms the hyper-sensitivity of financial conditions to this tipping point (Chart 6). Right now, I agree that bond yields are accommodative. But the scope for yields to move higher is quite limited. Chart 6 (DHAVAL)Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Since 2015, the Global Long Bond Yield Has Struggled To Surpass 2.5 Percent

Mathieu: Monetary policy is important to the outlook, but so is the global manufacturing cycle. The global growth slowdown has been concentrated in the manufacturing sector, tradeable goods in particular. Across advanced economies, the service and consumer sectors have been surprisingly resilient, but this will not last if the industrial sector decelerates further. Arthur, you still do not anticipate any major improvement in global trade and industrial production. Can you elaborate why? Chart 7 (ARTHUR)Global Trade Is Down Due To China Not U.S.

Global Trade Is Down Due To China Not U.S.

Global Trade Is Down Due To China Not U.S.

Arthur Budaghyan: To properly assess the economic outlook, one needs to understand what has caused the ongoing global trade/manufacturing downturn. One thing we know for certain: It originated in China, not the U.S. Chart 7 illustrates that Korean, Japanese, Taiwanese and Singaporean exports to China have been shrinking at an annual rate of 10%, while their shipments to the U.S. have been growing. China’s aggregate imports have also been contracting. This entails that from the perspective of the rest of the world, China has been and remains in recession. U.S. manufacturing is the least exposed to China, which is the main reason why it has been the last shoe to drop. Hence, the U.S. has lagged in this downturn, and one should not be looking to the U.S. for clues about a potential global recovery. We need to gauge what will turn Chinese demand around. In this regard, the rising credit and fiscal spending impulse is positive, but it has so far failed to kick start a recovery (Chart 8). The key reason has been a declining marginal propensity to spend among households and companies. Notably, the marginal propensity to spend of mainland companies leads industrial metals prices by a few months, and it currently continues to point south (Chart 8, bottom panel). The lack of willingness among Chinese consumers and enterprises to spend is due to several factors: (1) the U.S.-China confrontation; (2) high levels of indebtedness among both enterprises and households (Chart 9); (3) ongoing regulatory scrutiny over banks and shadow banking as well as local government debt; and (4) a lack of outright government subsidies for purchases of autos and housing. Chart 8 (ARTHUR)Stimulus Versus Marginal Propensity To Spend

Stimulus Versus Marginal Propensity To Spend

Stimulus Versus Marginal Propensity To Spend

Chart 9 (ARTHUR)Chinese Households Are More Leveraged Than U.S. Ones

Chinese Households Are Leveraged Than U.S. Ones

Chinese Households Are Leveraged Than U.S. Ones

On the whole, the falling marginal propensity to spend will all but ensure that any recovery in mainland household and corporate spending is delayed. Mathieu: Meanwhile, Peter, you have a much more optimistic stance. Why do you differ so profoundly with Arthur’s view? Peter: China’s deleveraging campaign began more than a year before global manufacturing peaked. I have no doubt that slower Chinese credit growth weighed on global capex, but we should not lose sight of the fact there are natural ebbs and flows at work. Most manufactured goods retain some value for a while after they are purchased. If spending on, say, consumer durable goods or business equipment rises to a high level for an extended period, a glut will form, requiring a period of lower production. Chart 10 (PETER)The Global Manufacturing Cycle Has Likely Reached A Bottom

The Global Manufacturing Cycle Has Likely Reached A Bottom

The Global Manufacturing Cycle Has Likely Reached A Bottom

These demand cycles typically last about three years; roughly 18 months on the way up, 18 months on the way down (Chart 10). The last downleg in the global manufacturing cycle began in early 2018, so if history is any guide, we are nearing a trough. The fact that U.S. manufacturing output rose in both May and June, followed by this week’s sharp rebound in the July Philly Fed Manufacturing survey, supports this view. Of course, extraneous forces could complicate matters. If trade tensions ratchet higher, this would weaken my bullish thesis. Nevertheless, with China stimulating its economy again, it would probably take a severe trade war to push the global economy into recession. Mathieu: Dhaval, you are not as negative as Arthur, but nonetheless expect a slowdown in the second half of the year. What is your rationale? Dhaval: To be clear, I am not forecasting a recession or major downturn – unless, as per my previous answer, the global 10-year bond yield approaches 2.5% and triggers a severe dislocation in global risk-assets. In fact, many people get the relationship between recession and financial market dislocation back-to-front: they think that the recession causes the financial market dislocation when, in most cases, the financial market dislocation causes the recession! Nevertheless, I do believe that European and global growth is entering a regular down-oscillation based on the following compelling evidence: From a low last summer, quarter-on-quarter GDP growth rates in the developed economies have already rebounded to the upper end of multi-year ranges. Short-term credit impulses in Europe, the U.S., and China are entering down-oscillations (Chart 11). The best current activity indicators, specifically the ZEW economic sentiment indicators, have rolled over. The outperformance of industrials – the equity sector most exposed to global growth – has also rolled over. Why expect a down-oscillation? Because it is the rate of decline in the bond yield that drove the rebound in growth after its low last summer. Furthermore, it is impossible for the rate of decline in the bond yield to keep increasing, or even stay where it is. Counterintuitively, if bond yields decline, but at a reduced pace, the effect is to slow economic growth. Mathieu: A positive and a negative view of the world logically result in bifurcated outlooks for interest rates and the dollar. Rob, how do you see U.S., German, and Japanese yields evolving over the coming 12 months? Rob: If global growth rebounds, U.S. Treasury yields will have far more upside than Bund or JGB yields. Inflation expectations should recover faster in the U.S., with the Fed taking inflationary risks by cutting rates with a 3.7% unemployment rate and core CPI inflation at 2.1%. The Fed is also likely to disappoint by delivering fewer rate cuts than are currently discounted by markets (90bps over the next 12 months). Treasury yields can therefore increase more than German and Japanese yields, with the ECB and BoJ more likely to deliver the modest rate cuts currently discounted in their yield curves (Chart 12). Chart 11 (DHAVAL)Short-Term Impulses Rebounded... But Are Now Rolling Over

Short-Term Impulses Rebounded... But Are Now Rolling Over

Short-Term Impulses Rebounded... But Are Now Rolling Over

Chart 12 (ROB)U.S. Treasuries Will Underperform Bunds & JGBs

U.S. Treasuries Will Underperform Bunds & JGBs

U.S. Treasuries Will Underperform Bunds & JGBs

Japanese yields will remain mired at or below zero over the next 6-12 months, as wage growth and core inflation remain too anemic for the BoJ to alter its 0% target on 10-year JGB yields. German yields have a bit more potential to rise if European growth begins to recover, but will lag any move higher in Treasury yields. That means that the Treasury-Bund and Treasury-JGB spreads will move higher over the next year. Negative German and Japanese yields may look completely unappetizing compared to +2% U.S. Treasury yields, but this handicap vanishes when all three yields are expressed in U.S. dollar terms. Hedging a 10-year German Bund or JGB into higher-yielding U.S. dollars creates yields that are 50-60bps higher than a 10-year U.S. Treasury. It is abundantly clear that German and Japanese bonds will outperform Treasuries over the next year if global growth recovers. Mathieu: Peter, your positive view on global growth means that the Fed will cut rates less than what is currently priced into the OIS curve. So why do you expect the dollar to weaken in the second half of 2019? Peter: What the Fed does affects interest rate differentials, but just as important is what other central banks do. The ECB is not going to raise rates over the next 12 months. However, if euro area growth surprises on the upside later this year, investors will begin to question the need for the ECB to keep policy rates in negative territory until mid-2024. The market’s expectation of where policy rates will be five years out tends to correlate well with today’s exchange rate. By that measure, there is scope for interest rate differentials to narrow against the U.S. dollar (Chart 13). Chart 13A (PETER)Interest Rate Expectations Against The U.S. Should Narrow (I)

Interest Rate Expectations Against The U.S. Should Narrow (I)

Interest Rate Expectations Against The U.S. Should Narrow (I)

Chart 13B (PETER)Interest Rate Expectations Against The U.S. Should Narrow (II)

Interest Rate Expectations Against The U.S. Should Narrow (II)

Interest Rate Expectations Against The U.S. Should Narrow (II)

Keep in mind that the U.S. dollar is a countercyclical currency, meaning that it moves in the opposite direction of global growth (Chart 14). This countercyclicality stems from the fact that the U.S. economy is more geared towards services than manufacturing compared with the rest of the world. Chart 14 (PETER)The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

As such, when global growth accelerates, capital tends to flow from the U.S. to the rest of the world, translating into more demand for foreign currency and less demand for dollars. If global growth picks up in the remainder of the year, as I expect, the dollar will weaken. Mathieu: Arthur, as you are significantly more negative on growth than either Rob or Peter, how do you see the dollar and global yields evolving over the coming six to 12 months? Arthur: I am positive on the trade-weighted U.S. dollar for the following reasons: The U.S. dollar is a countercyclical currency – it exhibits a negative correlation with the global business cycle. Persistent weakness in the global economy emanating from China/EM is positive for the dollar because the U.S. economy is the major economic block least exposed to a China/EM slowdown. Meanwhile, the greenback is only loosely correlated with U.S. interest rates. Thereby, the argument that lower U.S. rates will drive the value of the U.S. currency much lower is overemphasized. The Federal Reserve will cut rates by more than what is currently priced into the market only in a scenario of a complete collapse in global growth. Yet this scenario would be dollar bullish. In this case, the dollar’s strong inverse relationship with global growth will outweigh its weak positive relationship with interest rates. Contrary to consensus views, the U.S. dollar is not very expensive. According to unit labor costs based on the real effective exchange rate – the best currency valuation measure – the greenback is only one standard deviation above its fair value. Often, financial markets tend to overshoot to 1.5 or 2 standard deviations below or above their historical mean before reversing their trend. One of the oft-cited headwinds facing the dollar is positioning, yet there is a major discrepancy between positioning in DM and EM currencies versus the U.S. dollar. In aggregate, investors – asset managers and leveraged funds – have neutral exposure to DM currencies, but they are very long liquid EM exchange rates such as the BRL, MXN, ZAR and RUB versus the greenback. The dollar strength will occur mostly versus EM and commodities currencies. In other words, the euro, other European currencies and the yen will outperform EM exchange rates. I have less conviction on global bond yields. While global growth will disappoint, yields have already fallen a lot and the U.S. economy is currently not weak enough to justify around 90 basis points of rate cuts over the next 12 months. Mathieu: Before we move on to investment recommendations, Anastasios, you have done a lot of interesting work on the outlook for U.S. profits. What is the message of your analysis? Chart 15 (ANASTASIOS)Gravitational Pull

Gravitational Pull

Gravitational Pull

Anastasios: While markets cheered the trade truce following the recent G-20 meeting, no tariff rollback was agreed. Since the tariff rate on $200bn of Chinese imports went up from 10% to 25% on May 10, odds are high that manufacturing will remain in the doldrums. This will likely continue to weigh on profits for the remainder of the year. Profit growth should weaken further in the coming six months. Periods of falling manufacturing PMIs result in larger negative earnings growth surprises as market forecasters rarely anticipate the full breadth and depth of slowdowns. Absent profit growth, equity markets lack the necessary ‘oxygen’ for a durable high-quality rally. Until global growth momentum turns, investors should fade rallies. Our four-factor SPX EPS growth model is flirting with the contraction zone. In addition, our corporate pricing power proxy and Goldman Sachs’ Current Activity Indicator both send a distress signal for SPX profits (Chart 15). Already, more than half of the S&P 500 GICS1 sectors’ profits are estimated to have contracted in Q2, and three sectors could see declining revenues on a year-over-year basis, according to I/B/E/S data. Q3 depicts an equally grim profit picture that will also spill over to Q4. Adding it all up, profits will underwhelm into year-end. Mathieu: Doug, you do not share Anastasios’s anxiety. What offsets do you foresee? Moreover, you are not concerned by the U.S. corporate balance sheets. Can you share why? Doug Peta: As it relates to earnings, we foresee offsets from a revival in the rest of the world. Increasingly accommodative global monetary policy and reviving Chinese growth will give global ex-U.S. economies a boost. That inflection may go largely unnoticed in U.S. GDP, but it will help the S&P 500, as U.S.-based multinationals’ earnings benefit from increased overseas demand and a weaker dollar. When it comes to corporate balance sheets, shifting some of the funding burden to debt from equity when interest rates are at generational lows is a no-brainer. Even so, non-financial corporates have not added all that much leverage (Chart 16). Low interest rates, wide profit margins and conservative capex have left them with ample free cash flow to service their obligations (Chart 17). Chart 16 (DOUG)Corporations Have Not Added Much Leverage ...

Corporations Have Not Added Much Leverage ...

Corporations Have Not Added Much Leverage ...

Chart 17 (DOUG)...Though They Have Ample Cash Flow To Service It

...Though They Have Ample Cash Flow To Service It

...Though They Have Ample Cash Flow To Service It

Every single viable corporate entity with an effective federal tax rate above 21% became a better credit when the top marginal rate was cut from 35% to 21%. Every such corporation now has more net income with which to service debt, and will have that income unless the tax code is revised. You can’t see it in EBITDA multiples, but it will show up in reduced defaults. Mathieu: The last, and most important question. What are each of your main investment recommendations to capitalize on the economic trends you anticipate over the coming 6-12 months? Let’s start with the pessimists: Arthur: First, the rally in global cyclicals and China plays since December has been premature and is at risk of unwinding as global growth and cyclical profits disappoint. Historical evidence suggests that global share prices have not led but have actually been coincident with the global manufacturing PMI (Chart 18). The recent divergence is unprecedented. Chart 18 (ARTHUR)Global Stocks Historically Did Not Lead PMIs

Global Stocks Historically Did Not Lead PMIs

Global Stocks Historically Did Not Lead PMIs

Second, EM risk assets and currencies remain vulnerable. EM and Chinese earnings per share are shrinking. The leading indicators signal that the rate of contraction will deepen, at least the end of this year (Chart 19). Asset allocators should continue underweighting EM versus DM equities. Finally, my strongest-conviction, market-neutral trade is to short EM or Chinese banks and go long U.S. banks. The latter are much healthier than EM/Chinese ones, as we discussed in our recent report.6 Anastasios: The U.S. Equity Strategy team is shifting away from a cyclical and toward a more defensive portfolio bent. Our highest conviction view is to overweight mega caps versus small caps. Small caps are saddled with debt and are suffering a margin squeeze. Moreover, approximately 600 constituents of the Russell 2000 have no forward profits. Only one S&P 500 company has negative forward EPS. Given that both the S&P and the Russell omit these figures from the forward P/E calculation, this is masking the small cap expensiveness. When adjusted for this discrepancy, small caps are trading at a hefty premium versus large caps (Chart 20). Chart 19 (ARTHUR)China And EM Profits Are Contracting

China And EM Profits Are Contracting

China And EM Profits Are Contracting

Chart 20 (ANASTASIOS)Continue To Avoid Small Caps

Continue To Avoid Small Caps

Continue To Avoid Small Caps

We have also upgraded the S&P managed health care and the S&P hypermarkets groups. If the economic slowdown persists into early 2020, both of these defensive subgroups will fare well. In mid-April, we lifted the S&P managed health care group to an above benchmark allocation and posited that the selloff in this group was overdone as the odds of “Medicare For All” becoming law were slim. Moreover, a tight labor market along with melting medical cost inflation would boost the industry’s margins and profits (Chart 21). This week, we upgraded the defensive S&P hypermarkets index to overweight arguing that the souring macro landscape coupled with a firming industry demand outlook will support relative share prices (Chart 22). Chart 21 (ANASTASIOS)Buy Hypermarkets

Buy Hypermarkets

Buy Hypermarkets

Chart 22 (ANASTASIOS)Stick With Managed Health Care

Stick With Managed Health Care

Stick With Managed Health Care

Dhaval: To be fair, I am not a pessimist. Provided the global bond yield stays well below 2.5 percent, the support to risk-asset valuations will prevent a major dislocation. But in a growth down-oscillation, the big game in town will be sector rotation into pro-defensive investment plays, especially into those defensives that have underperformed (Chart 23). Chart 23 (DHAVAL)Switch Out Of Growth-Sensitives Into Healthcare

Switch Out Of Growth-Sensitives Into Healthcare

Switch Out Of Growth-Sensitives Into Healthcare

On this basis: Overweight Healthcare versus Industrials. Overweight the Eurostoxx 50 versus the Shanghai Composite and the Nikkei 225. Overweight U.S. T-bonds versus German bunds. Overweight the JPY in a portfolio of G10 currencies. Mathieu: And now, the optimists: Doug: So What? is the overriding question that guides all of BCA’s research: What is the practical investment application of this macro observation? But Why Now? is a critical corollary for anyone allocating investment capital: Why is the imbalance you’ve observed about to become a problem? As Herbert Stein said, “If something cannot go on forever, it will stop.” Imbalances matter, but Dornbusch’s Law counsels patience in repositioning portfolios on their account: “Crises take longer to arrive than you can possibly imagine, but when they do come, they happen faster than you can possibly imagine.” Look at Chart 24, which shows a vast white sky (bull markets) with intermittent clusters of gray (recessions) and light red (bear markets) clouds. Market inflections are severe, but uncommon. When the default condition of an economy is to grow, and equity prices to rise, it is not enough for an investor to identify an imbalance, s/he also has to identify why it’s on the cusp of reversing. Right now, as it relates to the U.S., there aren’t meaningful imbalances in either markets or the real economy. Chart 24 (DOUG)Recessions And Bear Markets Travel Together

Recessions And Bear Markets Travel Together

Recessions And Bear Markets Travel Together

Even if we had perfect knowledge that a recession would arrive in 18 months, now would be way too early to sell. The S&P 500 has historically peaked an average of six months before the onset of a recession, and it has delivered juicy returns in the year preceding that peak (Table 1). Bull markets tend to sprint to the finish line (Chart 25). If this one is like its predecessors, an investor risks significant relative underperformance if s/he fails to participate in its go-go latter stages. Table 1 (DOUG)The S&P 500 Doesn’t Peak Until Six Months Before A Recession …

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

Chart 25

We are bullish on the outlook for the next six to twelve months, and recommend overweighting equities and spread product in balanced U.S. portfolios while significantly underweighting Treasuries. Peter: I agree with Doug. Equity bear markets seldom occur outside of recessions and recessions rarely occur when monetary policy is accommodative. Policy is currently easy, and will get even more stimulative if the Fed and several other central banks cut rates. Global equities are not super cheap, but they are not particularly expensive either. They currently trade at about 15-times forward earnings. Given the ultra-low level of global bond yields, this generates an equity risk premium (ERP) that is well above its historical average (Chart 26). One should favor stocks over bonds when the ERP is high. Chart 26A (PETER)Equity Risk Premia Remain Elevated (I)

Equity Risk Premia Remain Elevated (I)

Equity Risk Premia Remain Elevated (I)

Chart 26B (PETER)Equity Risk Premia Remain Elevated (II)

Equity Risk Premia Remain Elevated (II)

Equity Risk Premia Remain Elevated (II)

The ERP is especially elevated outside the United States. This is partly because non-U.S. stocks trade at a meager 13-times forward earnings, but it also reflects the fact that bond yields are lower overseas. Chart 27 (PETER)EM And Euro Area Equities Outperform When Global Growth Improves

EM And Euro Area Equities Outperform When Global Growth Improves

EM And Euro Area Equities Outperform When Global Growth Improves

As global growth accelerates, the dollar will weaken. Equity sectors and regions with a more cyclical bent will benefit (Chart 27). We expect to upgrade EM and European stocks later this summer. A softer dollar will also benefit gold. Bullion will get a further boost early next decade when inflation begins to accelerate. We went long gold on April 17, 2019 and continue to believe in this trade. Rob: For fixed income investors, the most obvious way to play a combination of monetary easing and recovering global growth is to overweight corporate debt versus government bonds (Chart 28). Within the U.S., corporate bond valuations look more attractive in high-yield over investment grade. Assuming a benign outlook for default risk in a reaccelerating U.S. economy, with the Fed easing, going for the carry in high-yield looks interesting. Emerging market credit should also do well if we see a bit of U.S. dollar weakness and additional stimulus measures in China. Chart 28 (ROB)Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

Best Bond Bets: Overweight Global Corporates & Inflation-Linked Bonds

European corporates, however, may end up being the big winner if the ECB chooses to restart its Asset Purchase Program and ramps up its buying of European company debt. There are fewer restrictions for the ECB to buy corporates compared to the self-imposed limits on government bond purchases. The ECB would be entering a political minefield if it chose to buy more Italian debt and less German debt, but nobody would mind if the ECB helped finance European companies by buying their bonds. If one expects reflation to be successful, a below-benchmark stance on portfolio duration also makes sense given the current depressed level of government bond yields worldwide. Yields are more likely to grind upward than spike higher, and will be led first by increasing inflation expectations. Inflation-linked bonds should feature prominently in fixed income portfolios, especially in the U.S. where TIPS will outperform nominal yielding Treasuries. Mathieu: Thank you very much to all of you. Below is a comparative summary of the main arguments and investment recommendations of each camp. Summary Of Views And Recommendations

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

What Goes On Between Those Walls? BCA’s Diverging Views In The Open

Anastasios Avgeriou U.S. Equity Strategist anastasios@bcaresearch.com Peter Berezin Chief Global Strategist peterb@bcaresearch.com Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Dhaval Joshi Chief European Investment Strategist dhaval@bcaresearch.com Doug Peta Chief U.S. Investment Strategist dougp@bcaresearch.com Robert Robis Chief Fixed Income Strategist rrobis@bcaresearch.com Mathieu Savary The Bank Credit Analyst mathieu@bcaresearch.com Footnotes 1 To be fair to each individual involved, this is simplifying their views. Even within each camp, the negativity or positivity ranges on a spectrum, as you will be able to tell from the debate itself. 2 Please see BCA U.S. Equity Strategy Weekly Report, “Signal Vs. Noise,” dated December 17, 2018, available at uses.bcaresearch.com. 3 Please see BCA U.S. Equity Strategy Weekly Report, “A Recession Thought Experiment,” dated June 10, 2019, available at uses.bcaresearch.com. 4 Please see the European Investment Strategy Weekly Report “Risk: The Great Misunderstanding Of Finance,” October 25, 2018 available at eis.bcaresearch.com. 5 France is a good proxy for the euro area. 6 Please see Emerging Markets Strategy Weekly Report, “On Chinese Banks And Brazil,” available at ems.bcaresearch.com.

Highlights So What? U.S. policy uncertainty adds to a slew of geopolitical reasons to remain tactically cautious on risk assets. Why? U.S. fiscal policy should ultimately bring market-positive developments – though the budget negotiation process could induce volatility in the near-term. We expect spending to go up and do not expect a default due to the debt ceiling or another prolonged government shutdown. Former Vice President Joe Biden remains the frontrunner for the Democratic Party’s presidential nomination in 2020. But left-wing progressive candidates are gaining on him and their success will trouble financial markets. With Persian Gulf tensions still elevated, go long Q1 2020 Brent crude relative to Q1 2021. Feature Chart 1U.S. Politics Poses Risks Through Next November

U.S. Politics Poses Risks Through Next November

U.S. Politics Poses Risks Through Next November

Economic policy uncertainty is rising in the United States even as it falls around the world (Chart 1). Ongoing budget negotiations and the Democratic primary election give equity investors another reason to remain cautious in the near term. We expect more volatility. There also remain several persistent global threats to markets posed by unresolved geopolitical risks – rising Brexit risks with Boris Johnson likely to take the helm in the United Kingdom; oil supply threats amid Iran’s latest rejection of U.S. offers to negotiate its missile program; and a major confirmation of our theme of geopolitical risk rotation to East Asia, with Japan, South Korea, Hong Kong, Taiwan, and the South China Sea all heating up at once. In sum, political and geopolitical risks are showing investors a yellow light, even though the macroeconomic outlook still supports BCA’s cyclical (12-month) equity overweight. U.S. Fiscal Policy Will Remain Accommodative While U.S. monetary policy has taken a dovish turn – supported by other central banks – fiscal spending is now coming into focus for investors. We expect the budget battle to be market-relevant this year, injecting greater economic policy uncertainty, but the end-game should be market-positive. Brinkmanship will not get as bad as during the debt ceiling crises of 2011 and 2013, though market jitters will be frontloaded if Pelosi and the White House fail to conclude a deal immediately. Chart 2The 'Stimulus Cliff' Awaits President Trump

The 'Stimulus Cliff' Awaits President Trump

The 'Stimulus Cliff' Awaits President Trump

The U.S. budget process is always rocky and is usually concluded well into the fiscal year under discussion. This year the fight will be more important than over the past few years because, as the two-year bipartisan agreement of 2018 lapses, the so-called “stimulus cliff” looms over the U.S. economy and will get caught up in the epic battle over the 2020 election. The stimulus cliff is the automatic imposition of fiscal spending cuts (“sequestration”) in FY2020 that would take effect as a result of the Budget Control Act of 2011. Standard estimates of the U.S. budget deficit expect that the deficit will shrink in 2020 if the spending caps are not raised, resulting in a negative fiscal thrust (Chart 2). The result would be to decrease aggregate demand at a time when the risk of recession is relatively high (Chart 3). Chart 3Recession Odds Still High Over Next 12 Months

Recession Odds Still High Over Next 12 Months

Recession Odds Still High Over Next 12 Months

This is clearly not in President Trump’s interest, since a recession would devastate his reelection odds. Hence, Treasury Secretary Steve Mnuchin and other White House officials are pushing for a budget deal before the House of Representatives goes on recess on July 26 and the Senate on August 2. Ideally, an agreement would raise the spending caps, appropriate funds for the rest of the budget, and lift the “debt ceiling,” the statutory limit on U.S. debt. But it would be surprising if a deal came together as early as next week. A failure to agree on a budget deal before Congress goes on recess will make the market increasingly jittery. Congress can cancel the August recess, or wait until September 9 when they reconvene, but a failure to agree on something between now and then will make the market increasingly jittery. The U.S. has already surpassed the current debt limit and the latest estimates suggest that the Treasury Department’s “extraordinary measures” to meet U.S. debt payments could be exhausted by early-to-mid September.1 This would give Congress only a week in September to raise the debt limit. There are three main reasons to expect that the debt ceiling fight will not get out of hand: Chart 4Americans Stopped Worrying And Love Debt

Americans Stopped Worrying And Love Debt

Americans Stopped Worrying And Love Debt

First, a technical default on U.S. debt could result in a failure to meet politically explosive obligations, such as sending social security checks to seniors. No one in Washington would benefit from such a failure and President Trump would suffer the most. Second, the public is not as worried about national deficits and debt today as it was in the aftermath of the financial crisis (Chart 4). Democrats, as the pro-government party, do not have an incentive to stage a showdown over the debt like Tea Party Republicans did under the previous administration. To be fair, they did do so in January 2018, but backed off after merely two days due to high political costs. Third, the one budget conflict that could create a catastrophic impasse – funding for Trump’s border wall – can be assuaged by Trump’s use of executive action, as he demonstrated by declaring a national emergency and appropriating military funds for fencing. Trump is fighting a general election in 2020 and is unlikely to use the debt ceiling as leverage to the point that the U.S. defaults on its obligations. The risk to investors, however, is that he goes back to threatening a 25% tariff on Mexico if it fails to staunch the flow of immigrants from Central America. What if the Republicans and Democrats cannot agree on the budget and spending caps? Democrats say they will not raise the debt limit unless they get non-defense spending increases. House Democrats need to reward their constituents for voting for them in 2018 and want to increase non-defense spending at “parity” with increases to defense spending. They also want to reduce the defense increases that Republicans seek in order to pay for non-defense increases. President Trump and the Republicans have a higher defense target and a lower non-defense target. The truth is that the Republicans and Democrats have agreed three times to increase spending caps beyond the levels required under the 2011 law – and they have done so most emphatically under President Trump with the FY2018-19 agreement (Chart 5). This year the two parties stand about $17 billion apart on defense and $30 billion apart on non-defense spending.2 We would expect both sides to splurge on spending and get what they want, but they could also split the difference: the amounts are small but the acrimony between the two parties could extend the talks. Congress may have to pass one or more “continuing resolutions” (stopgap measures keeping spending levels constant) to negotiate further. A continuing resolution could at least raise the debt ceiling and leave the rest of the budget negotiation until later, removing the majority of the political risk under discussion.

Chart 5

Chart 6

Is another government shutdown possible? Yes, but not to the extent of early 2019. Trump saw a sharp drop in his approval ratings during the longest-ever government shutdown last year (Chart 6). Brinkmanship could lead to another shutdown, but he is likely to capitulate before it becomes prolonged. In early 2020, he wants to be lobbing grenades into the Democratic primary election rather than giving all of the Democrats an easy chance to criticize him for dysfunction in Washington. Ultimately, Trump can simply refrain from vetoing whatever the House and Senate agree – it is not in his interest to shrink the budget deficit in an election year. The Democrats’ spending increases would boost aggregate demand and are thus in President Trump’s personal interest. Trump is the self-professed “king of debt” – he is not afraid to agree to a deal that will be criticized by fiscal hawks. The latter have far less influence in Congress anyway since the 2018 midterm election. Why should House Democrats extend the economic expansion knowing that it would likely improve President Trump’s reelection chances? Because Trump will capitulate to most of their spending demands; voters would punish them if they are seen deliberately engineering “austerity”; and they need to show voters that they can govern. As for the 2020 race, they will focus on other issues: they will attack Trump on trade and immigration and focus on social policy: health care, the minimum wage, taxes and inequality, climate change, and student debt. What will be the fiscal and economic impact of a budget deal? The budget deal under negotiation ($750 billion in defense discretionary spending, $639 billion in non-defense discretionary spending) would raise the spending cap by about $145 billion – this is slightly above the $112 billion negative fiscal thrust expected in 2020.3 The result is that the U.S. fiscal drag expected in 2020 will at least be eliminated (if not turned into a fiscal boost), helping to prolong the cycle. The removal of fiscal drag will coincide with monetary easing, which is positive for markets since inflation is subdued. The Federal Reserve abandoned rate hikes this year (after four last year) because of the asymmetric risk of deflation relative to inflation (Chart 7). The FOMC believes that they can always jack up interest rates to combat an inflation overshoot, as their predecessors did in the 1980s, but that they are constrained by the zero lower-bound in interest rates. They may never recover from a loss of credibility and collapse of inflation expectations, so an insurance policy is necessary. The result is likely to be one or two rate cuts this year, which has already improved financial conditions. Chart 7The Fed Fears The Asymmetric Threat Of Deflation

The Fed Fears The Asymmetric Threat Of Deflation

The Fed Fears The Asymmetric Threat Of Deflation

Bottom Line: Budget brinkmanship could become a near-term source of volatility but it is ultimately likely to be resolved with the pro-market outcome of less fiscal drag in 2020. The debt ceiling debate is unlikely to result in a U.S. default and any government shutdown is likely to resemble the short one of 2018 more than the long one of 2019. We expect U.S. equities to grind higher over the 12-month cyclical horizon, but we remain exceedingly cautious on a three-month tactical horizon. The price of Trump’s capitulation on border funding could be a renewed threat of tariffs against Mexico. The Budget Deal, Geopolitics, And The Dollar Chart 8China Shifts From Reform To Stimulus

China Shifts From Reform To Stimulus

China Shifts From Reform To Stimulus

What does this fiscal outlook imply for the U.S. dollar? Near-term moves will probably be negative, since the fiscal boost outlined above will not be comparable to 2018-19, and meanwhile our view on China’s stimulus is bearing out reasonably well (Chart 8). Improvements in global growth, Fed cuts, and rising oil prices will weigh on the greenback even though later we expect the dollar to recover on the back of renewed U.S.-China conflict and global recession in 2021 or thereafter. Beyond the recession, two of our major political and geopolitical themes continue to point to large downside risk to the dollar: populist politics and multipolarity, or geopolitical competition among the world’s great powers. Beyond the recession, two of our major political and geopolitical themes continue to point to large downside risk to the dollar: populist politics and multipolarity. Populism and the Fed: Domestically, the United States is seeing a rise in populism that is continuing across administrations and political parties. This is conducive to easier monetary policy. Left-wing firebrand Alexandria Ocasio-Cortez’s (AOC) recent exchange with Fed Chairman Jay Powell highlights the trend. AOC asked one of the most frequent questions that BCA’s clients ask: Does the Phillips Curve still work? Powell answered that in recent years it has not. President Trump’s Economic Director Larry Kudlow applauded AOC, saying “she kind of nailed that” (obviously the administration is pushing for lower rates). If inflation is not a risk, monetary policy need not guard against it. This interchange should be taken in the context of President Trump’s attempts to jawbone Powell into rate cuts and the notable monetary promiscuousness of his ostensibly “hard money” Federal Reserve nominees. The extremely different ideological and institutional profiles of these various policymakers suggests that a new consensus is forming that is conducive to more dovish monetary policy than otherwise expected over the long run. Populists of any stripe, from Trump to AOC, would like to see lower interest rates, higher nominal GDP growth, and a lower real debt burden on households. We are reminded of an oft-overlooked point about the stagflation of the 1970s. Fed Chair Arthur Burns is usually depicted as a lackey of President Richard Nixon who succumbed to political influence and failed to raise interest rates adequately to fight inflation. But this is only part of the story. Leaving aside that the Fed only had a single mandate of minimizing unemployment at that time, Burns was conflicted. He saw the need to fight inflation, but he had more than Nixon’s wrath to fear. He also dreaded the impact on the Fed’s credibility and popular support as an institution if he hiked rates too aggressively and stoked unemployment (Chart 9).4 Chart 9Rate Hikes Are Hard To Defend Amid High Unemployment

Rate Hikes Are Hard To Defend Amid High Unemployment

Rate Hikes Are Hard To Defend Amid High Unemployment

In other words, populism can constrain the Fed from the bottom up as well as from the top down in a context of rising unemployment.5 Multipolarity and Currency War: Since President Trump’s election we have highlighted that dollar depreciation is likely to be the administration’s ultimate aim if President Trump’s overall economic strategy is truly to stimulate growth, reduce the trade deficit, and repatriate manufacturing. Jacking up growth rates relative to the rest of the world while disrupting global trade via tariffs is a recipe for a strong dollar that undermines the attempt to bring jobs back from overseas. We have always argued that China would not grant the U.S. “shock therapy” liberalization and market opening – and that neither China, nor Europe, nor Japan would or could engage in currency appreciation along the lines of a new Smithsonian or Plaza Accord. The U.S. does not have as much geopolitical clout as it had in the 1970s-80s when it forced major currency deals on its allies and partners. The remaining option is for the U.S. to attempt unilateral depreciation. The combination of profligate spending, easy monetary policy, and populism may do the trick. But it is also possible that President Trump will attempt to engineer depreciation through Treasury Department intervention. If a slide toward recession threatens his reelection – or he is reelected and hence gets rid of the first-term reelection constraint – his unorthodox policies pose a significant risk to the dollar. Bottom Line: The U.S. dollar faces near-term risks as growth rebalances towards rest of the world, but will probably resume its rise in the impending recessionary environment and expected re-escalation of tensions with China. Over the long run, it faces severe risks due to fiscal mismanagement, domestic populism, and geopolitical struggle. A Progressive Overshoot Will Hurt Democrats … And Equities Chart 10A Democratic Win Will Weigh On Animal Spirits

A Democratic Win Will Weigh On Animal Spirits

A Democratic Win Will Weigh On Animal Spirits

The Democratic Party’s primary election is also a risk to the equity rally. We see a 45% risk that President Trump will be unseated in November 2020 and hence that the U.S. will once again experience a dramatic policy reversal (as in 2000, 2008, and 2016). The risks are to the downside because the market is at all-time highs and Democratic proposals include raising taxes on corporations and re-regulating the economy (Chart 10). Whether you accept our 55% odds of Trump reelection, the race will be a continual source of uncertainty for investors going forward. How extreme is the uncertainty? Former Vice President Joe Biden remains the frontrunner in the race, though he has lost his initial bump in opinion polls (Chart 11). Biden’s success is market-positive relative to the other Democratic candidates since he is an establishment politician and a known quantity. Given his age, a Biden presidency would likely last for one term and focus on repudiating Trumpism and consolidating the Obama administration’s signature achievements (the Affordable Care Act, Dodd-Frank, the Joint Comprehensive Plan of Action, environmental regulation, etc). Greater predictability in the health care sector and a return to lower-level tensions with Iran would be market-positive. The financial sector would be consoled by the fact that nothing worse than Dodd-Frank would be in the offing.

Chart 11

A Biden victory would be more likely to yield Democratic control of the senate than a progressive candidate’s victory.6 This means that the risk of Democrats taking full control of government and passing more than one major piece of legislation after 2020 increases with Biden. Yet any candidate capable of defeating Trump is likely to take the senate in our view; and Biden’s legislative initiatives are likely to be more centrist.7 So as long as Biden remains in the lead in primary polling, he increases his chances of winning the nomination, maximizes the 45% chance of Democrats winning the White House, and decreases the intensity of the relative policy uncertainty facing markets. The risk to the Democrats is … a left-wing or progressive overshoot that knocks out Biden in the primary, replacing him with a progressive candidate who may not be as electable in the general election.

Chart 12

The risk to the Democrats is that the leftward policy shift within the party (Chart 12) may lead to a left-wing or progressive overshoot that knocks out Biden in the primary, replacing him with a progressive candidate who may not be as electable in the general election. This would give President Trump the ability to capitalize on his advantage as the incumbent by inveighing against socialism. Most of the major progressive candidates are electable – they have a popular and electoral path to the White House – as revealed by their successful head-to-head polling against Trump in battleground state opinion polling (Chart 13). But these pathways are narrower than Biden’s. Biden is the only candidate whose name has been on the ballot in two presidential elections carrying the critical Rust Belt swing states Michigan, Pennsylvania, and Wisconsin (not to mention Ohio and Florida). He is from Pennsylvania. And he is more competitive than most of his rivals in the American south and southwest, giving him the potential to pick up Florida or Arizona in the general election. But none of this matters if Biden cannot win the Democratic nomination first.

Chart 13

The risk of a progressive overshoot is growing at present. Biden is losing his lead in the primary polling, as mentioned. Progressive candidates taken together are polling better than centrists, contrary to previous Democratic primaries (Chart 14). This is true even if we define centrists broadly, for instance to include Buttigieg (Chart 15). Biden is in a weaker position than Hillary Clinton in 2007 – and the more progressive candidate Obama ultimately defeated her (Chart 16). Biden has now slipped to second place in one national poll and some state polls.

Chart 14

The second round of Democratic debates on July 30-31 will be a critical testing period for whether Biden can maintain frontrunner status. The first round fulfilled our expectation of boosting the progressives at his expense, especially Elizabeth Warren. It surprised us in dealing a blow to the campaign of Bernie Sanders, the independent Senator from Vermont who initiated the progressive left’s surge with his hard-fought race against Hillary Clinton in 2016.

Chart 15

Chart 16

Sanders is more competitive than the other progressives in the Rust Belt, and in the general election, based on his head-to-head polling against Trump. Yet he has fallen behind in recent Democratic primary polling, ceding ground to Warren, Harris, and Buttigieg, who are all his followers in some sense. The second debate is a critical opportunity for him to arrest the loss of momentum. Otherwise he is likely to be fatally wounded: a collapse in polling beneath his floor of about 15%, and relative to other progressives, despite extensive name recognition, will make it very difficult for him to recover in the third round of debates in September. His votes will go toward other progressives, particularly Buttigieg – the other white male progressive-leaning candidate who is competitive in the Midwest.8 Our 55% base case that Trump is reelected rests on the high historical reelection rate for incumbents, particularly in the event of no recession during the first term – yet discounted due to Trump’s relatively low nationwide popularity, as it is reminiscent of a president in a recessionary environment (Chart 17). Trump has his ideological base more fired up than Obama did (Chart 18), which helps drive voter turnout, although as a result he risks losing support from the rest of the population. Still, Trump’s approval rating is in line with Obama’s at this stage in his first term. As long as the economy holds up and Trump does not suffer a foreign policy humiliation, he should be seen as a slight favorite.

Chart 17

Chart 18

A Trump victory is not positive for risk assets, aside from a relief rally on policy continuity. This is because in a second term he cannot reproduce the same magnitude of pro-market effects (huge tax cuts and deregulation) yet, freed from the need for reelection, he has fewer political constraints in producing higher magnitude anti-market effects (tariffs and/or sanctions on China, Iran, Russia, and possibly the EU and Mexico). This view dovetails with the BCA House View which remains overweight equities relative to bonds and cash over a cyclical (12 month) horizon but underweight over the longer run with the expectation that a recession will loom. Bottom Line: The Democratic Primary election should start having an impact on markets – the general election is likely to be too close for market participants to have a high conviction, driving up uncertainty. Uncertainty will be especially pronounced if, and as, leftwing or progressive candidates outperform in the primary races and poll well against Trump in the general election. This dynamic is negative for business sentiment and the profit outlook, especially if Biden’s polling falls further in the wake of the second debate. Investment Conclusions We recommend staying long JPY-USD, long gold, and short CNY-USD. We remain overweight Thai equities within emerging markets, a defensive play. And we would not close our tactical overweight in health care sector and health care equipment sub-sector relative to the S&P 500. The rally in Chinese equities – despite China’s Q2 GDP growth rate of 6.2%, the worst in 27 years – brings full circle the view we initiated in April 2017 that Chinese President Xi Jinping’s consolidation of power would result in a major deleveraging drive that would drag on the global economy. Since February we have argued that the U.S. trade war has pushed Chinese policymakers to favor stimulus over reform – but we have also maintained that the effectiveness of stimulus is declining, especially as a result of the trade war hit to sentiment. Nevertheless, as a result of this turn in Chinese policy – along with the turn in U.S. monetary and fiscal policy – we see the global macroeconomic outlook improving. Combining this view with ongoing tensions in the Persian Gulf and the expectation that oil markets will tighten, we recommend our Commodity & Energy Strategy’s trade of going long Brent crude Q1 2020 versus Q1 2021. Matt Gertken, Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 See U.S. Department of Treasury, “Secretary Mnuchin Sends Debt Limit Letter to Congress,” July 12, 2019, home.treasury.gov. Jordan LaPier, “New Projection: Debt Limit “X Date” Could Arrive in September,” July 8, 2019, bipartisanpolicy.org. 2 See Jordain Carney and Niv Elis, White House, Congress inch toward debt, budget deal,” July 17, 2019, thehill.com. 3 See the Congressional Budget Office, “The Budget and Economic Outlook: 2019 to 2029,” January 2019; “Final Sequestration Report for Fiscal Year 2019,” February 2019; and Theresa Gullo, “Discretionary Appropriations Under the Budget Control Act,” Testimony before the Committee on the Budget, United States Senate, February 27, 2019, www.cbo.gov. 4 See James L. Pierce, “The Political Economy of Arthur Burns,” The Journal of Finance 34: 2 (1979), pp. 485-96, esp p. 489 regarding a congressional testimony: “Interestingly, no questions were raised or innuendo offered that monetary expansion would be excessive to support Richard Nixon’s reelection efforts. Instead, Burns was urged by the Democrats to follow an expansionary monetary policy in order to reduce the level of unemployment.” See also Athanasios Orphanides and John C. Williams, “Monetary Policy Mistakes and the Evolution of Inflation Expectations,” Federal Reserve Bank of San Francisco, Working Paper 2010-12 (2011), www.frbsf.org. 5 An analogy might be drawn with the Supreme Court, whose independence as one of three constitutional branches is much more firmly grounded in U.S. law than the Fed’s, but nevertheless cannot make decisions in an ivory tower. It must consider the effects of its judgments on popular opinion, since universally deplored decisions would reduce the court’s credibility and legitimacy in the eyes of the public over time and ultimately the other government branches’ adherence to those decisions. 6 This is both because Biden is more electable (thus more likely to bring a vice president who can break a tie vote in the senate) and because his candidacy can help Democrats in all of the senate swing races – for example, Arizona as well as Colorado and Maine. Harris is not as helpful in Maine while Warren and Sanders are not as helpful in Arizona. 7 Biden would return to the 39.6% top marginal individual tax rate and double the capital gains tax on those earning incomes of more than $1 million. See Biden For President, “Health Care,” joebiden.com. 8 Conversely, if Biden somehow collapses, Buttigieg unlike Sanders has the option of moving toward the political center to absorb Biden’s large reservoir of support.

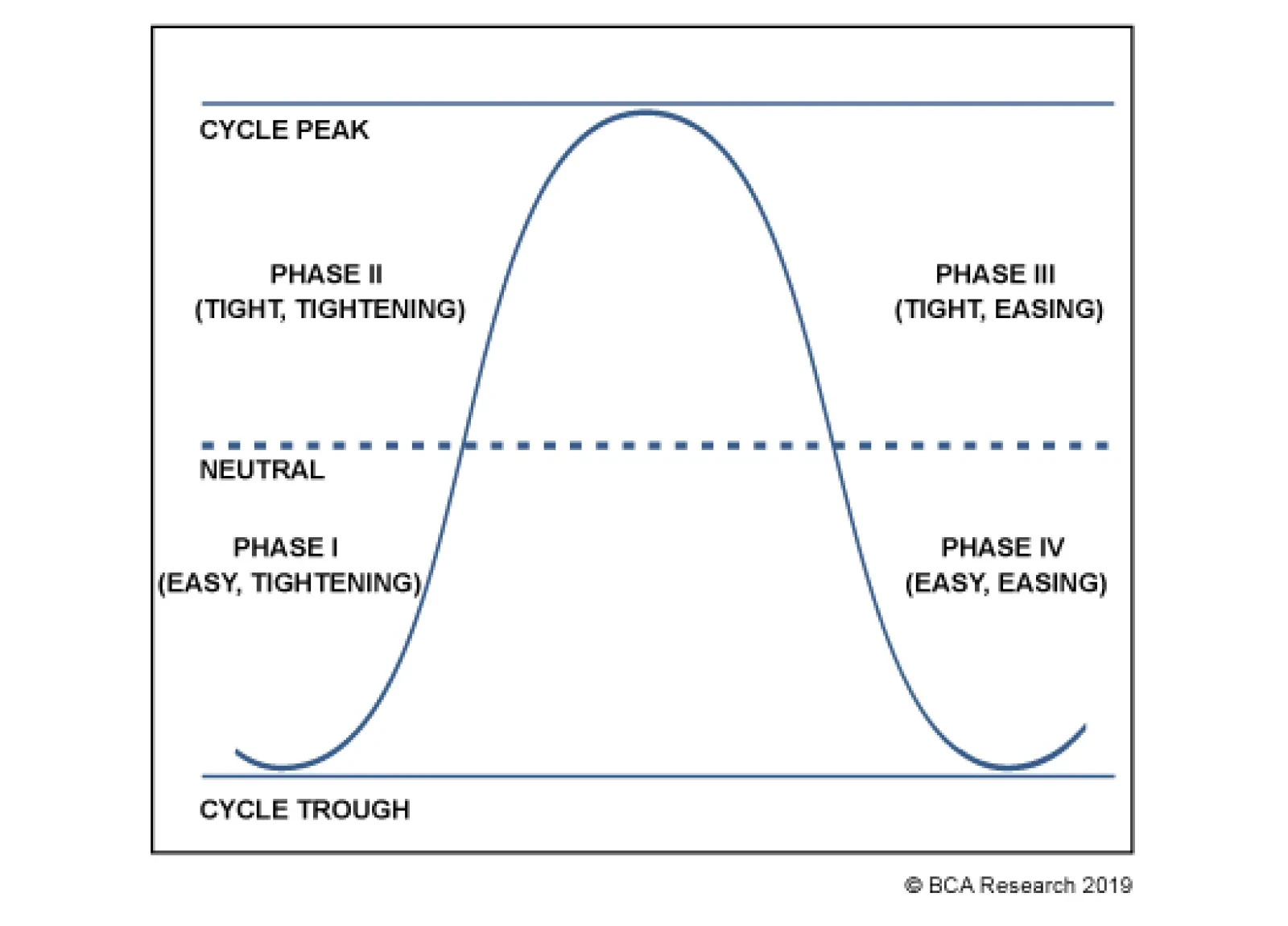

We decompose the fed funds rate cycle into four phases based on the interaction between the level of rates and their direction, as follows: Phase I represents the early stage of the withdrawal of monetary stimulus. This phase begins with the first rate…

Highlights A lower fed funds rate will not necessarily boost equities, … : A chorus of Wall Street strategists has recently advised investors to curb their enthusiasm about looming rate cuts. … because stocks are more sensitive to the relative level of the fed funds rate than they are to its direction: The Street strategists’ advice is sound, even if they haven’t homed in on its true rationale. Monetary policy’s influence on equity returns is primarily a function of the fed funds rate’s relationship to the equilibrium rate, not the direction in which it’s moving. Monetary policy settings remain accommodative, in our view, … : We estimate that the equilibrium fed funds rate remains well above the target fed funds rate. One or two rate cuts will push monetary policy even further into accommodative territory. ... and investors should therefore remain at least equal weight equities: Over the last 60 years, investors would have done exceptionally well if they had simply owned stocks when monetary policy settings were easy, and avoided them when they were tight. Feature Dear Client, We are in the midst of collaborating with several of our colleagues on a roundtable Special Report outlining the view differences between BCA’s most bullish and bearish strategists, scheduled to be published on Friday, July 19th. In the absence of a major event between now and then, the July 19th roundtable report will replace the July 22nd U.S. Investment Strategy. We will return to our usual format on Monday, July 29th. Best regards, Doug Peta U.S. equities have rallied smartly since Fed officials began hinting at rate cuts in early June. The S&P 500 advanced nearly 7% last month on rate cut hopes, and tacked on close to another 2% by making new highs in each of July’s first three sessions. As the gains grew, however, so too did the admonitions from equity strategists at leading broker-dealers that they were getting out of hand. Over the last month, no less than four shops wrote reports warning that rate cuts will not necessarily boost equities. From the financial media’s summaries of the reports, the curb-your-enthusiasm conclusion stems from a straightforward analysis of rate-cut impacts over the last 35 years. According to Goldman Sachs by way of Barron’s, the S&P 500 posted double-digit returns in the year following the start of all five of the rate-cutting cycles that occurred from the mid-eighties to the end of the nineties, before performing terribly following the cuts that began in 2001 and 2007.1 The Street-wide takeaway was that rate cuts worked wonders for stocks when the Greenspan put was still a fresh concept, but the inverse relationship between interest rates and equity multiples that initially prevailed has since been supplanted by a direct relationship. It is surely true that rate cuts are not a magic bullet for equities, but we find the flipped-correlation hypothesis wanting. There is more to the question of how monetary policy impacts equities than just the direction of rates. The state of monetary policy – accommodative or restrictive – matters, too. Even though assessments of the state of policy are necessarily uncertain, they allow for a much more sophisticated analysis of policy impacts. Without estimating the equilibrium fed funds rate, an investor cannot go beyond simple observations of the correlation between policy rates and equity returns to the causal interactions that drive the observed correlations. Numerators And Denominators When an investor buys a stock, s/he is buying a pro rata claim on the future earnings of the company that issued it. The value of that claim is a function of the company’s estimated future earnings and the interest rate used to discount them. Expressed as an equation, the fundamental value of a share of stock is as follows, where r is the reference interest rate: Year 1 Earnings + Year 2 Earnings + Year 3 Earnings + … + Year n Earnings (1+r) (1+r)2 (1+r)3 (1+r)n That equation can be simplified and rewritten as: Fundamental Value = ∑nt=1(Year t Earnings) (1+r)t It’s a stretch to think that equities’ reaction to rate cuts reversed after the year 2000. The final form of the equation shows that the underlying value of a share of stock is directly related to its future earnings and inversely related to interest rates. When the broker-dealer analyses conclude that the ‘80s-‘90s inverse relationship between stock prices and rate cuts has flipped since the turn of the millennium, they’re asserting that the relative sensitivities of stock prices to changes in the numerator (earnings) and the denominator (interest rates) have changed. That’s a mouthful, but the effect can be seen clearly by holding the numerator constant: if earnings don’t change, stock prices are inversely related to changes in interest rates. Relaxing the constant earnings assumption, the inverse relationship between rate cuts and stock prices in the ‘80s and ‘90s could only have occurred if earnings rose when the Fed cut, or if earnings fell when the Fed cut rates, but not so much that they offset the beneficial impact of the reduction in the discount rate. An Empirical Curveball When investors think about the impact of changes in interest rates on stock prices, they tend to assume that earnings remain constant. They therefore conclude that lower rates are good for stocks and higher rates are bad for them. The underlying assumption is flawed, however, because it ignores the fact that earnings are themselves a function of the macro backdrop that influences interest rates. Rising real interest rates are most often a sign of gathering economic momentum; since the end of World War II, U.S. equities have performed markedly better when real long-term Treasury yields were rising than they have when they were falling (Chart 1). Chart 1Stocks Do Better When Real Rates Rise

Stocks Do Better When Real Rates Rise

Stocks Do Better When Real Rates Rise

Investors’ appetite for equities reinforces the direct relationship between earnings and rates, as long as rates are not at extremes. Trailing P/E multiples have risen with real interest rates except when rates are negative or above 4% (Chart 2). When real rates are negative, deflation is a real possibility and fearful investors value future earnings streams conservatively. When they’re above zero, investors have been willing to let multiples rise with real rates, until rates get high enough to squeeze profitability.

Chart 2

The key, then, is what is going to happen with real yields if the Fed does indeed cut rates. Will 50 basis points (“bps”) of incremental accommodation (we expect 25-bps cuts in July and September) help to extend the expansion, or will it be too little, too late to impede the course of a recession that’s already begun? In the former case, economic growth will get a boost, and real yields and corporate earnings will go along for the ride. In the latter, the economy will contract, drawing real yields and corporate earnings into its vortex. We believe monetary policy is still squarely accommodative, and therefore have both feet planted firmly in the bullish camp. The Fed Funds Rate Cycle Our fed funds rate cycle framework helps us to assess the line of demarcation between accommodative and restrictive policy settings and thereby project the direction of corporate earnings following rate cuts. To refresh, we decompose the fed funds rate cycle into four phases based on the interaction between the level of rates and their direction (Diagram 1), as follows: Diagram 1The Fed Funds Rate Cycle

How Will Equities Respond To Rate Cuts?

How Will Equities Respond To Rate Cuts?

Phase I represents the early stage of the withdrawal of monetary stimulus. This phase begins with the first rate hike of a new tightening cycle and ends when the fed funds rate crosses above our estimate of the equilibrium rate. Phase II represents the latter stages of the tightening cycle, when the Fed hikes its target rate above equilibrium in a deliberate effort to cool an overheating economy. Phase III represents the early stage of the easing cycle. It begins with the first rate cut from the peak and lasts until the Fed cuts its target rate below equilibrium. Phase IV represents the late stage of the easing cycle. It encompasses both the period when the fed funds rate falls from below its equilibrium level to its cycle trough and the subsequent adjustment period when the Fed remains on hold in an effort to kick start an economic recovery. Plotting the course of the fed funds rate is a simple matter; the challenge in Diagram 1 comes in deciding where to draw the dashed line. That decision requires estimating the policy rate that neither encourages nor discourages economic activity. Our equilibrium estimate, which uses potential GDP growth to adjust a smoothed and filtered long-run series of the actual fed funds rate, can be viewed as a line in the sand separating the point where monetary policy goes from encouraging activity to discouraging it. When the funds rate is above our estimate of equilibrium, we consider policy to be tight; when it’s below our estimate of equilibrium, we consider policy to be easy. Since equilibrium is a concept, rather than an observable objective data point, we have to look at the broad sweep of economic activity to infer whether or not our equilibrium estimate is accurate. As we’ve repeatedly written, we interpret the economic data received so far this year as indicating that the U.S. economy is decelerating from its stimulus-fueled 2018 surge, but is on track to meet or exceed its long-term potential growth pace of 2 - 2.25%. We therefore do not believe that policy is tight, and that a recession has already begun, or is in the offing. Recession? What About Stock Prices? We didn’t forget about stock prices. Markets are always our primary focus, and we study the economy for insight into how it might impact their direction. The business cycle is a robust link connecting the state of monetary policy with equity performance. In the 60 years covered by our equilibrium fed funds rate estimate, recessions have only occurred when the funds rate has exceeded our estimate of equilibrium (Chart 3). Equity bear markets typically coincide with recessions – Black Monday in October 1987 is the only instance of a bear market occurring independently of a recession in the last half-century. Chart 3Recessions Only Occur When Policy Is Tight

Recessions Only Occur When Policy Is Tight

Recessions Only Occur When Policy Is Tight

For 60 years, stocks have thrived when monetary policy is easy and staggered when it is tight. S&P 500 performance across the four phases of the fed funds rate cycle reveals that it has been the level of rates vis-à-vis the equilibrium rate that has mattered for equity returns, not the direction. Annualized nominal S&P 500 price returns have been nine percentage points higher when policy is easy than when it is tight (Table 1), and the disparity widens to ten-and-a-half percentage points after adjusting for inflation (Table 2). The disparity is even more pronounced when the Fed is cutting rates – annualized Phase IV price returns beat Phase III by eleven percentage points on a nominal basis, and by thirteen-and-a-half percentage points on a real basis. Table 1Stocks Love Easy Policy, ...

How Will Equities Respond To Rate Cuts?

How Will Equities Respond To Rate Cuts?

Table 2… Especially After Adjusting For Inflation

How Will Equities Respond To Rate Cuts?

How Will Equities Respond To Rate Cuts?

Our base case is that the FOMC will cut the fed funds rate by 25 bps at its July and September meetings. The investment strategy question arising from our base-case scenario is what will that mean for equities? With reference to the dot-com bust and the financial crisis, the broker-dealers say, “nothing much.” We posit that a more sophisticated answer would consider the monetary-policy climate in which the cuts occur. Reduce equity exposure if you believe the Fed went too far hiking rates last year, but maintain/increase it if you think monetary policy has always remained accommodative. 60 years of history say that incremental accommodation will boost equities if it occurs against a backdrop of already easy policy. The S&P 500 will decline, on the other hand, if the monetary policy starting point is restrictive.2 In terms of our fed funds rate cycle framework, the equity market outcome turns on whether the cuts occur in Phase III or Phase IV. We estimate that the equilibrium rate is currently in the neighborhood of 3¼%, so we have a high level of conviction that equities will spend the rest of the year in Phase IV, the rate cycle phase that has been most conducive to equity outperformance. Investment Implications From the perspective of our monetary policy cycle framework, positioning a balanced portfolio for impending rate cuts boils down to one’s take on current monetary policy settings. If one thinks the Fed’s already tightened policy enough to squeeze the economy, s/he should sell stocks. (Some of our BCA colleagues advocate that course, and we will share the stage with them in next week’s roundtable Special Report). If one thinks, like we and the overall BCA consensus do, that the Fed hasn’t yet crossed the easy/tight Rubicon and is on a course to push the date when it will out to 2021 or beyond, one should maintain his/her equity positions and consider adding to them. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Hough, Jack, “The ‘Fed Put’ Is Kaput and Interest Rate Cuts Might Hurt Stocks,” Barron’s, July 1, 2019. 2 Remember that monetary policy impacts the economy with a lag. Cuts ameliorating too-tight policy don’t have an effect until after the initial overtightening makes its way through the system.

Incredibly, the tone shifted again in February, when Premier Li Keqiang and the PBoC publicly disputed whether the January credit spike represented “flood irrigation-style” stimulus, something Premier Li made clear was to be avoided. These shifts impacted…

The events of the past year have also demonstrated that the effectiveness of Chinese monetary policy has declined relative to past economic cycles. This, in conjunction with the reluctant/reactive nature of the monetary authorities, has clear implications for…

Canadian data has been firing on all cylinders of late, so it was no surprise that Governor Stephen Poloz decided to keep interest rates on hold today. That said, details in its monetary policy report were notably cautious: Risks from the slowdown in…