Policy

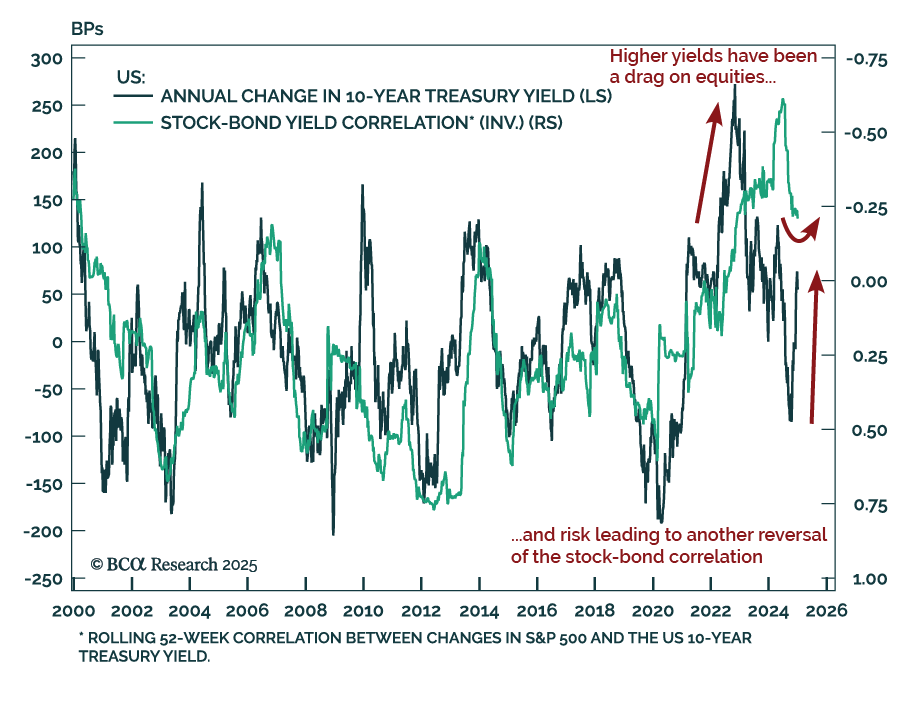

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

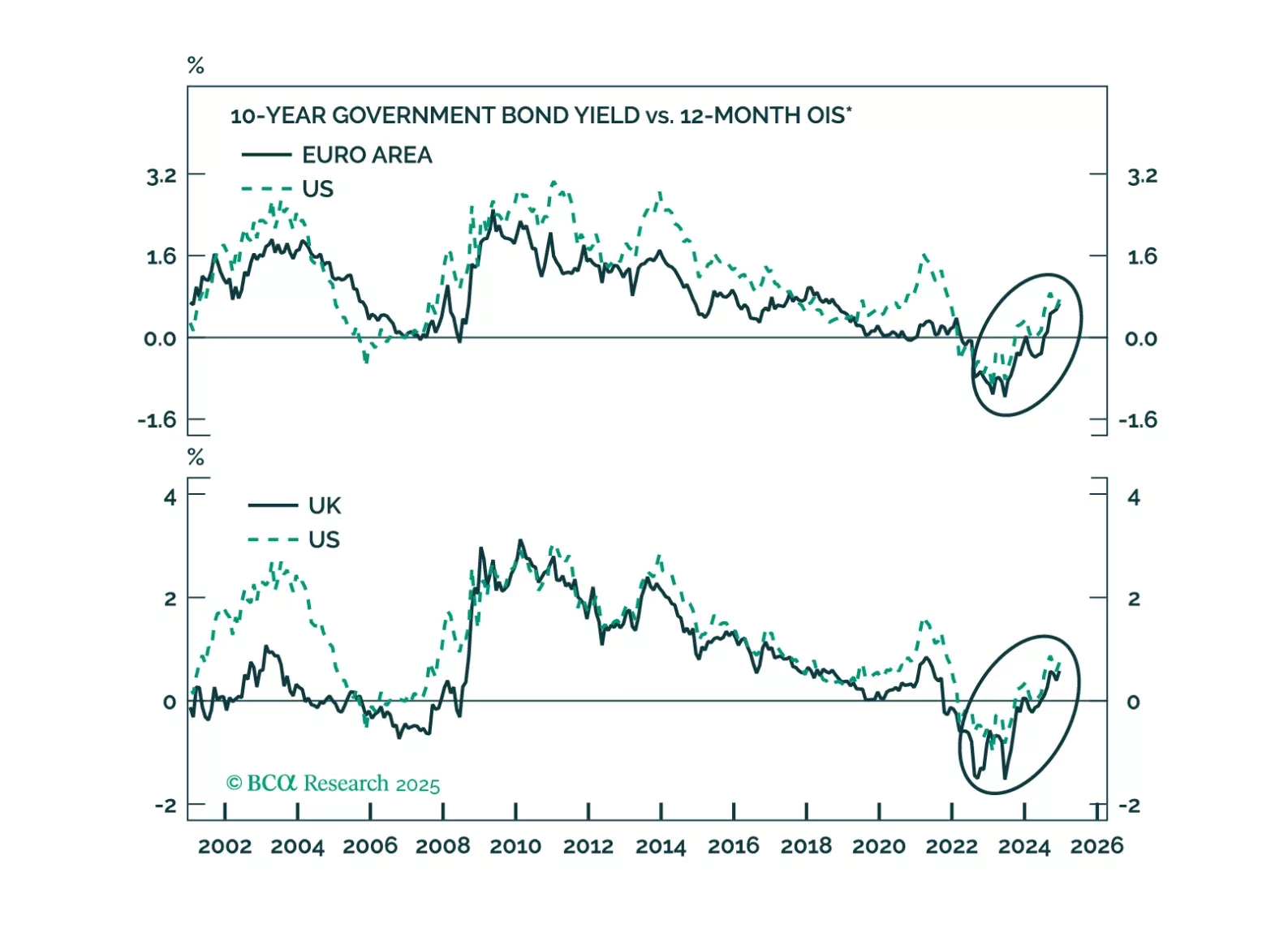

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

Thoughts on the increase in bond yields and this morning’s employment data.

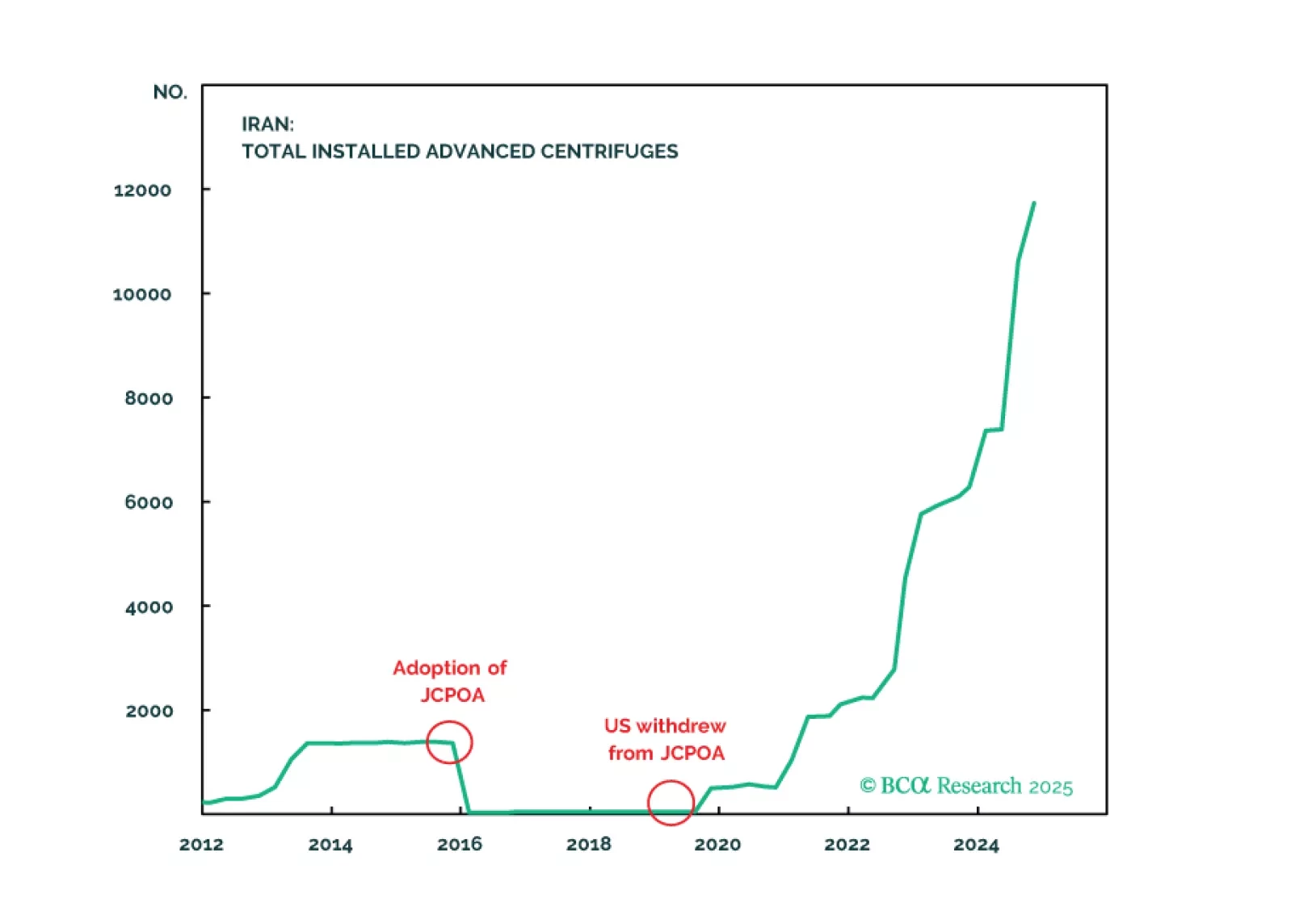

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

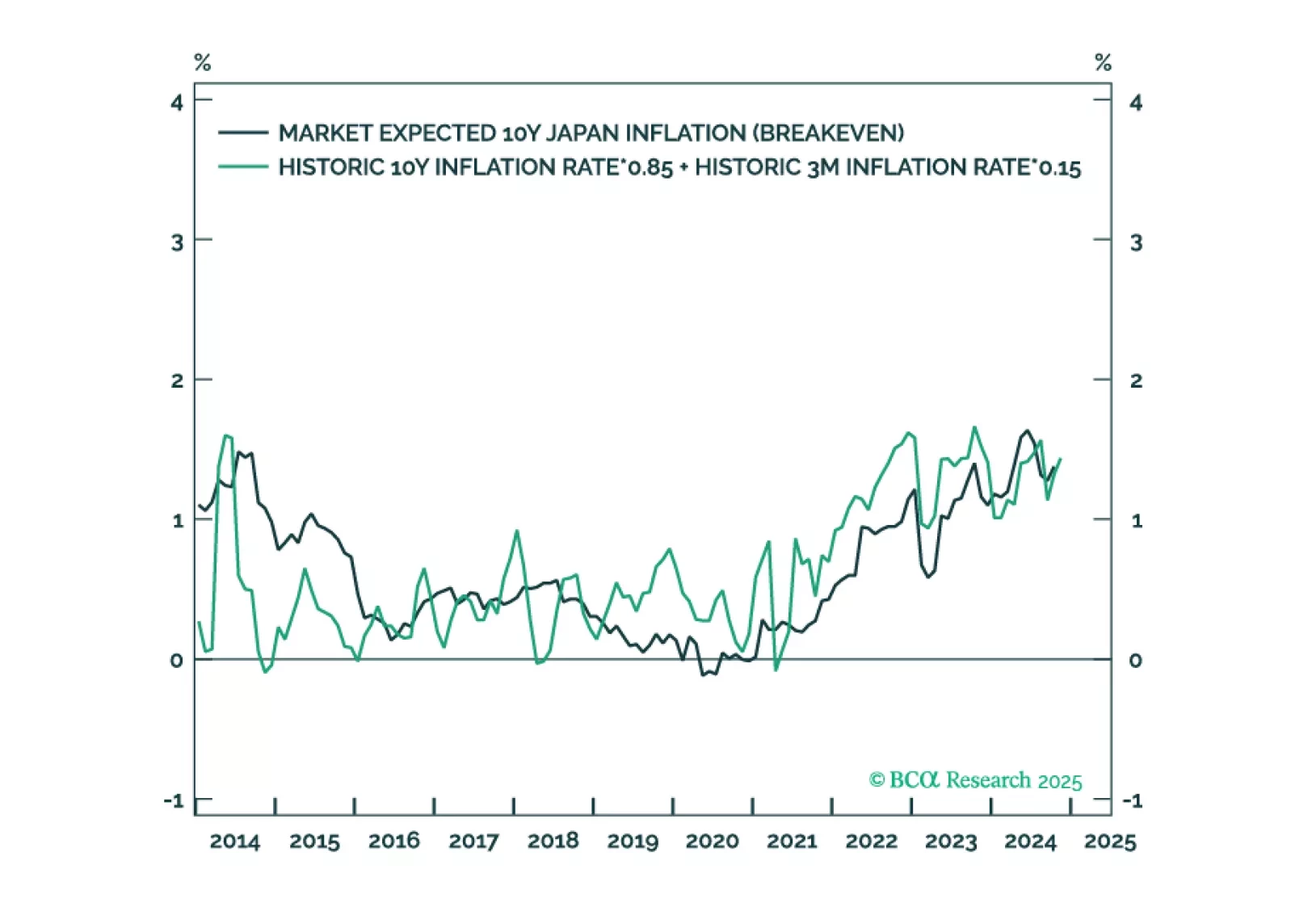

In most developed economies, rising inflation expectations will lift them further above the 2 percent target, limiting the scope for further interest rate cuts. But in Japan, rising inflation expectations will lift them up to the BoJ’s 2 percent target, removing the BoJ’s justification for its zero-interest rate policy. The normalisation of Japan’s monetary policy poses a big structural risk to stocks because Japan has been the main source of financial market liquidity, and thereby, of rising stock market valuations. From a timing perspective though, wait until the complexities of the price trends in USD/JPY and/or Nasdaq versus 30-year T-bond have collapsed. Plus: go tactically long copper.