Policy

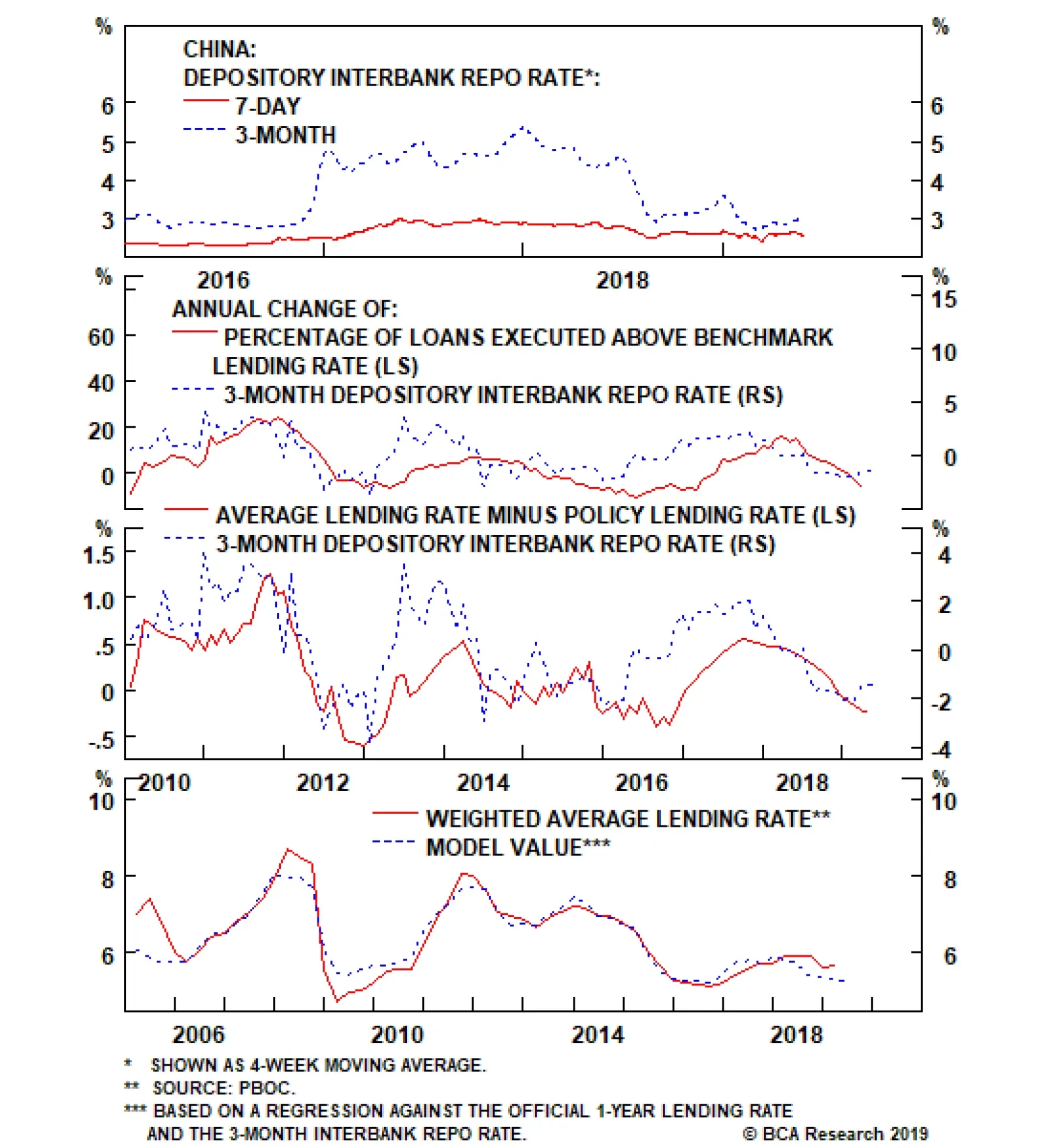

The top panel shows that while the 7-day repo rate rose in late-2016 and 2017, the rise was fairly small (on the order of 60 basis points). By contrast, the 3-month repo rate surged, which appears to have been caused by macro-prudential policy changes aimed…

Instead of aggressive and broad-based bank lending, this policy push will likely have to come in the form of quasi-fiscal spending, e.g. a significant increase in infrastructure-oriented local government bond issuance (which we include as “credit” in our…

Highlights Huge imbalance #1 is the euro area’s $150 billion trade surplus with the United States. Huge imbalance #1 has resulted from the ECB holding interest rates at the lower bound while the Fed tightened policy. The upshot is that the Fed now has the scope to cut rates while the ECB does not. Huge imbalance #2 is the euro area’s €1.5 trillion TARGET2 banking imbalance. Huge imbalance #2 means that Germany effectively has hundreds of billions of ‘Italian’ euro assets, making a euro break-up unthinkable for the euro area’s dominant economy. New structural recommendation for bond investors: overweight a 50:50 portfolio of U.S. T-bonds and Italian BTPs versus a 50:50 portfolio of German bunds and Spanish Bonos. Feature Huge Imbalance #1: The Euro Area’s $150 Billion Trade Surplus With The United States While the recent focus has been on the brewing trade war between the United States and China, trade tensions between the U.S. and Europe have also been escalating. The euro area trade surplus with the U.S. – standing near an all-time high of $150 billion – is extreme; and it is extreme because the undervaluation of the euro has made the euro area grossly over-competitive vis-à-vis the U.S., as claimed by the ECB’s own analysis (Chart I-2 and Chart I-3)! Chart of the WeekThe U.S./Euro Area Trade Imbalance Is A Near-Perfect Function Of Relative Monetary Policy

The U.S./Euro Area Trade Imbalance Is A Near-Perfect Function Of Relative Monetary Policy

The U.S./Euro Area Trade Imbalance Is A Near-Perfect Function Of Relative Monetary Policy

Chart I-2Relative Monetary Policy Has Driven The Euro's Undervaluation...

Relative Monetary Policy Has Driven The Euro's Undervaluation...

Relative Monetary Policy Has Driven The Euro's Undervaluation...

Chart I-3...And The Euro's Undervaluation Has Driven The U.S./Euro Area Trade Imbalance

...And The Euro's Undervaluation Has Driven The U.S./Euro Area Trade Imbalance

...And The Euro's Undervaluation Has Driven The U.S./Euro Area Trade Imbalance

A common counterargument is that the euro area trade surplus is simply a structural issue. If a country, such as Germany, consistently consumes less than it produces, it must show up as a structural surplus. This argument is flawed. At least half of the surplus, including for Germany, has appeared since 2014, meaning it cannot be a structural issue (Chart I-4). In any case, if an economy consumes less than it produces, a higher exchange rate should help to facilitate the adjustment, encouraging under-consuming households to buy more imports, and discouraging over-producing firms from selling into foreign markets. Chart I-4Half Of Germany's Export Surplus Appeared After 2014

Half Of Germany's Export Surplus Appeared After 2014

Half Of Germany's Export Surplus Appeared After 2014

The Chart of the Week shows the true and damning reason for the trade imbalance. The euro area’s surplus with the U.S. is a near-perfect function of relative monetary policy. To be clear, the ECB is not explicitly depressing the exchange rate to make the euro area over-competitive, the ECB is just targeting its definition of price stability. However, the ECB’s definition of price stability omits owner-occupied housing (OOH) costs, and thereby understates true euro area inflation by 0.5 percent. To the extent that the ECB thinks in terms of real interest rates based on seemingly low (excluding OOH) inflation, this means that the ECB is setting real interest rates that are far too low for the euro area economy including OOH. This has resulted in the grossly over-competitive euro and the associated $150 billion surplus with the United States. The euro area trade surplus with the U.S. is a near-perfect function of relative monetary policy. Still, for 85 percent of the euro area, even inflation excluding OOH is reliably running within a 1.5-2 percent range, very close to the ECB’s definition of price stability. And bank lending is growing at a very healthy clip. For this vast majority of the bloc, the ECB’s zero and negative interest rate policy is wholly inappropriate. However, for the 15 percent of the euro area that is called Italy, ultra-loose monetary policy does seem more appropriate. Inflation is struggling to stay above 1 percent, and bank lending is still failing to gain traction (Chart I-5 and Chart I-6). Chart I-5Italian Inflation Is Struggling To Stay Above 1 Percent

Italian Inflation Is Struggling To Stay Above 1 Percent

Italian Inflation Is Struggling To Stay Above 1 Percent

Chart I-6Italian Banks Have Not ##br##Been Lending

Italian Banks Have Not Been Lending

Italian Banks Have Not Been Lending

Therefore, an important way of thinking of the ECB’s stance is one of self-preservation – protecting the euro area’s obvious source of fissure. Effectively, the ECB is setting policy for the weakest link in the euro area, even if that policy means exacerbating strains outside the euro area – specifically, by generating a huge trade surplus with the United States. But in the interests of self-preservation, the external strain is a price worth paying. This leads us to believe that the inevitable convergence of euro area and U.S. monetary policies is now much more likely to happen via the Federal Reserve ultimately cutting rates, than by the ECB raising rates. Huge Imbalance #2: The Euro Area’s €1.5 Trillion TARGET2 Imbalance The euro area Target2 banking imbalance now stands close to €1.5 trillion (Chart I-7). What is this huge imbalance (Box 1), and why does it matter?

Chart I-7

Box 1: What Is Target2? Target2 stands for Trans-European Automated Real-time Gross settlement Express Transfer system. It is the settlement system for euro payment flows between banks in the euro area. These payment flows result from trade or financial transactions such as deposit transfers, sales of financial assets or debt repayments. If the banking system in one member country has more payment inflows than outflows, its national central bank (NCB) accrues a Target2 asset vis-à-vis the ECB. Conversely, if the banking system has more outflows than inflows, the respective NCB accrues a Target2 liability vis-à-vis the ECB. Target2 balances therefore show the cumulative net payment flows within the euro area. The ECB delegated its QE sovereign bond purchases to the respective national central banks. In the case of Italian BTPs, Italian investors sold their bonds to the Bank of Italy and deposited the cash in banks healthier than those in Italy – for example, in Germany. Strictly speaking, this outflow of Italian cash to German banks is not the same as the deposit flight during the depths of the euro debt crisis in 2012. Rather, we might call it precautionary cash management. Nevertheless, in Eurosystem accounting terms it still means that the Bank of Italy has a new asset – the BTP – denominated in ‘Italian’ euros, while the Bundesbank has a new liability to German banks denominated in ‘German’ euros. The Target2 imbalance is the aggregate of such mismatches between Eurosystem assets denominated in ‘Italian and other periphery’ euros and liabilities denominated in ‘German and other core’ euros. If Italy owes Germany half a trillion euros then it is Germany that has the problem. Does the €1.5 trillion imbalance really matter? No, as long as an ‘Italian’ euro equals a ‘German’ euro, the imbalance is just an accounting identity within the Eurosystem. But if Italy and Germany started using different currencies, then suddenly it would matter with a vengeance. The Bank of Italy asset would be redenominated into lira, while the Bundesbank liability to German banks would be redenominated into deutschemarks. Thereby the ECB would end up with fewer assets than liabilities, and a solvency shortfall potentially equivalent to hundreds of billions of euros would end up on the shoulders of the ECB’s shareholders – largely, German taxpayers. To paraphrase John Maynard Keynes, if Italy owes Germany half a billion euros, then Italy has a problem; but if Italy owes Germany half a trillion euros, then it is Germany that has the problem (Chart I-8 and Chart I-9). In effect, the Target2 huge imbalance is a huge force for euro area self-preservation – because break-up means mutually assured destruction. Chart I-8The Target2 Imbalance Reflects The Cross-Border Flow Of Italian Investor Cash...

The Target2 Imbalance Reflects The Cross-Border Flow Of Italian Investor Cash...

The Target2 Imbalance Reflects The Cross-Border Flow Of Italian Investor Cash...

Chart I-9...To German##br## Banks

...To German Banks

...To German Banks

A New Structural Recommendation For Bond Investors To sum up, the euro area has two huge imbalances: one external, the other internal. The external imbalance is the $150 billion trade surplus with the United States. This huge imbalance has resulted from the ECB holding interest rates at the lower bound while the Fed tightened policy. The upshot is that the Fed now has the scope to cut rates while the ECB does not. And this makes the U.S. T-bond a much better haven asset than the German bund. The Target2 imbalance is a huge force for euro area self-preservation. The internal imbalance is the €1.5 trillion euro area Target2 imbalance. This huge imbalance means that Germany effectively has hundreds of billions of Italian ‘euro’ assets, making a euro break-up unthinkable for the euro area’s dominant economy. On this premise, the Italian BTP – which is offering a generous yield premium for such a break-up risk – is a good structural investment. Therefore, our new structural recommendation for bond investors is to overweight: A 50:50 portfolio of U.S. T-bonds and Italian BTPs Versus A 50:50 portfolio of German bunds and Spanish Bonos. Since 2018, the T-bond/BTP combination has underperformed by 20 percent and has considerable scope for ultimate catch-up one way or another (Chart I-10). Chart I-10A U.S. T-Bond/Italian BTP Combo Can Catch Up With A German Bund/Spanish Bono Combo

A U.S. T-Bond/Italian BTP Combo Can Catch Up With A German Bund/Spanish Bono Combo

A U.S. T-Bond/Italian BTP Combo Can Catch Up With A German Bund/Spanish Bono Combo

Fractal Trading System * There are no new trades this week. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-11

Bitcoin

Bitcoin

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights A financial market riot point remains likely over the coming few months to force policymakers, including those in China, to address the economic weakness that a full-tariff scenario will entail. The near-term outlook is bearish for China-related assets, but investors should stay cyclically bullish in anticipation of a strong reflationary response. It is not clear whether further monetary easing will occur over the coming year, given that monetary conditions have already eased substantially. But an RRR cut coupled with a benchmark lending rate cut is now a real possibility, and would signal that the monetary policy dial has been turned to “maximum stimulus”. Monthly credit growth needs to be approximately 2.8-3 trillion RMB per month in May and June in order to be consistent with a 2015/2016-magnitude policy response. May’s number may fall short of this, but that would set up June as a make-it or break-it month for credit creation. Chinese credit growth surged in 2012, but economic activity did not significantly accelerate. A repeat of this scenario is a risk to our cyclically bullish stance, but three reasons suggest it is not likely to occur. Investors should stay long USD-CNH over the cyclical horizon despite warnings from Chinese policymakers not to short the RMB. Feature Tensions between China and the U.S. have worsened materially over the past two weeks, in line with our view that an actual trade agreement this year (not just continued negotiations) is much less likely. The Huawei blacklist, stalled negotiations, a sharp escalation in preparatory nationalist rhetoric in China, and President Xi Jinping’s declaration in a Jiangxi province speech that the country is embarking on a new “Long March”1 significantly diminishes the possibility of a deal that addresses the U.S.’ structural concerns. Chart 1A Market Riot Point Is Coming

A Market Riot Point Is Coming

A Market Riot Point Is Coming

This implies that any agreement would require President Trump to capitulate and accept a temporary deal relating simply to the balance of trade between the two countries. It is possible that this occurs over the coming 6-12 months (in time for Trump to attempt a declaration of victory before the 2020 election), but it is not likely to occur before real economic (and thus financial market) pain arrives. This supports our view that a major financial market riot point is likely over the coming few months to force policymakers, including those in China, to address the economic weakness that a full-tariff scenario will entail (Chart 1). Given this, we would not recommend a long position in Chinese stocks, either in absolute terms or relative to the global benchmark, for investors with a time horizon of less than 3 months. However, over a strictly cyclical (i.e. 6-12 month) time horizon, we would recommend staying long/overweight Chinese stocks (in hedged currency terms) on the basis that policymakers will ultimately respond as needed, lest they face an unstable deceleration in economic activity that may become difficult to stop. In this week’s report we address the following three questions facing China-exposed investors over the coming year, before concluding with a brief note about the RMB: Can the PBOC provide more of a reflationary impulse if needed, and if so, how? How can investors tell whether policymakers are stimulating as required from the monthly credit data? What are the odds that China will stimulate aggressively and the economy does not meaningfully reaccelerate? How Can The PBOC Ease Further? We argued in our May 15 Weekly Report that a 2015/2016-magnitude policy response will again be required in order for policymakers to be confident that the upcoming trade shock will be overcome.2 In our view, this response, instead of aggressive and broad-based bank lending, will likely have to come in the form of quasi-fiscal spending, e.g. a significant increase in infrastructure-oriented local government bond issuance (which we include as “credit” in our adjusted total social financing calculation). However, we have received several questions from clients asking about the outlook for monetary policy in a full-tariff scenario, particularly the question of what the PBOC can do to provide even more of a reflationary response. Most investors would simply assume that the PBOC would cut interest rates even further, and this is certainly a possible outcome over the coming year. But even if the PBOC were to cut interest rates, it is not always clear to investors what rate should or will be cut. Confusion surrounding China’s monetary policy landscape has been high ever since the PBOC established an interest rate corridor system in 2015, and a review of what has occurred over the past 2½ years is warranted in order to better understand the implications of future policy decisions. A 2015/2016-magnitude policy response will again be required in order for policymakers to be confident that the upcoming trade shock will be overcome. Chart 2The Simple (But Incomplete) View Of China's New Monetary Regime

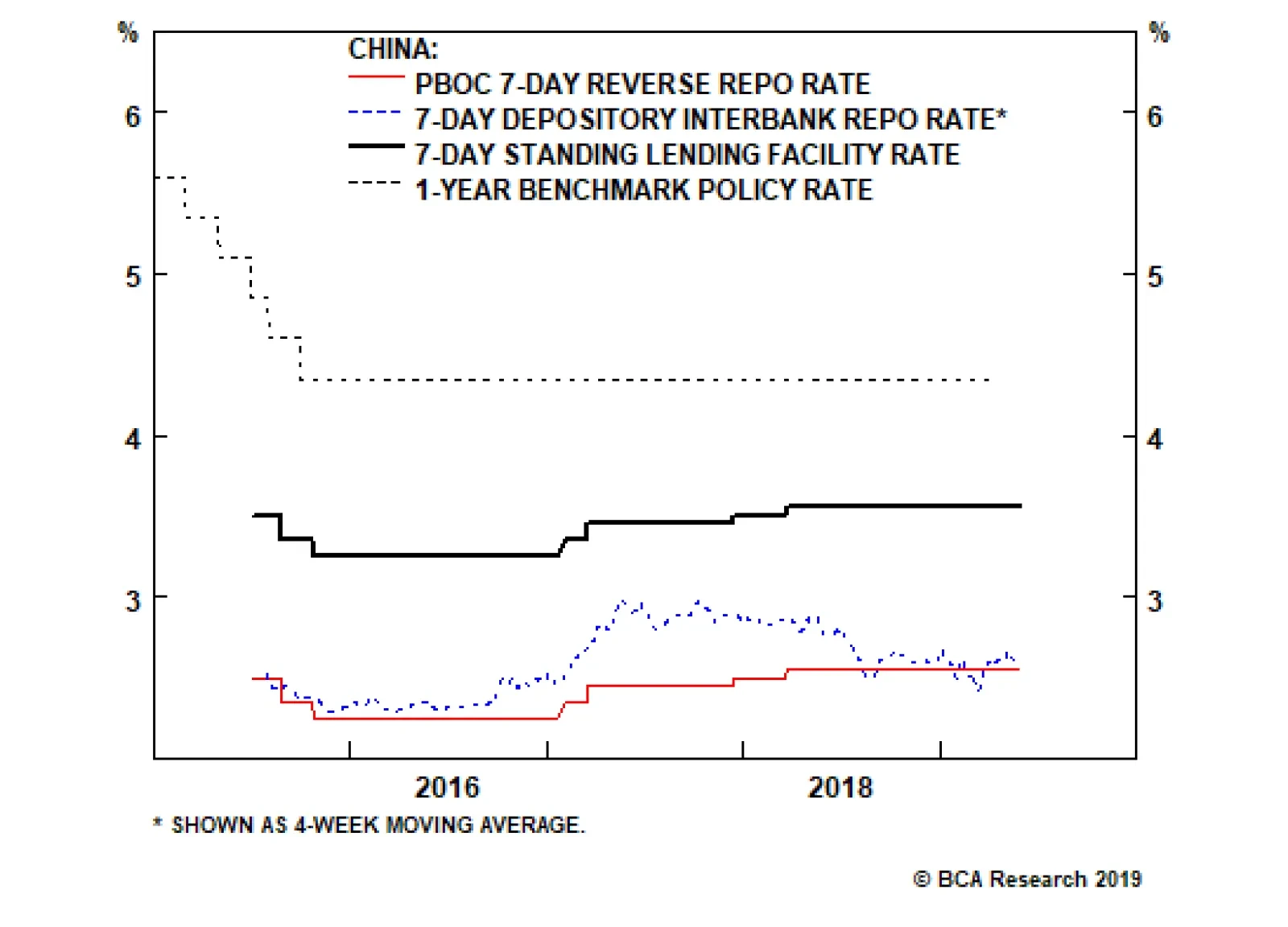

The Simple (But Incomplete) View Of China's New Monetary Regime

The Simple (But Incomplete) View Of China's New Monetary Regime

Chart 2 outlines how China’s new monetary regime is officially described by the PBOC. The benchmark lending rate, China’s “old” policy rate that established a base regulated rate for banks to price their loans, was replaced in 2015 with a corridor system. The target rate in this system is the 7-day interbank repo rate, which can be seen in Chart 2 is often at the low end of the corridor. However, we explained in a February 2018 Special Report why Chart 2 is only half of the story.3Charts 3 - 5 show the other half: Chart 3 shows that while the 7-day repo rate rose in late-2016 and 2017, the rise was fairly small (on the order of 60 basis points). By contrast, the 3-month repo rate surged, which appears to have been caused by macro-prudential policy changes aimed at severely curtailing the issuance of wealth management products by non-depository financial institutions. Chart 4 highlights that there is a strong (and leading) relationship between changes in China’s 3-month interbank repo rate and 1) changes in the percentage of loans issued above the benchmark rate and 2) changes in the gap between the weighted-average interest rate and the benchmark rate. Chart 5 shows that China’s weighted average interest rate can be successfully modelled by a regression on the benchmark lending rate and the 3-month interbank repo rate. Chart 3The 3-Month Repo Rate Has Been More Important Than The 7-Day

The 3-Month Repo Rate Has Been More Important Than The 7-Day

The 3-Month Repo Rate Has Been More Important Than The 7-Day

Chart 4A Strong Link Between 3-Month Repo Rates And Economy-Wide Rates

A Strong Link Between 3-Month Repo Rates And Economy-Wide Rates

A Strong Link Between 3-Month Repo Rates And Economy-Wide Rates

The relationships shown in Charts 3 - 5 are weaker if the 3-month repo rate is replaced with the 7-day rate, highlighting that while the latter is the new de jure policy rate in China, the former has been the de facto policy and market-driven lending rate among banks and non-financial institutions over the past 2½ years. Chart 5The Benchmark Lending And 3-Month Repo Rates Explain Effective Lending Rates

The Benchmark Lending And 3-Month Repo Rates Explain Effective Lending Rates

The Benchmark Lending And 3-Month Repo Rates Explain Effective Lending Rates

Our framework for examining China’s monetary policy environment leads us to conclude that there are three things the PBOC can do to meaningfully ease further, were they to decide to do so: The most impactful action that the PBOC could take is to cut the benchmark lending rate. While banks in China are no longer required to price loans in reference to the benchmark rate, in practice many still do. Roughly 2/3rds of loans in China have been priced at an interest rate above the benchmark over the past year, and Chart 5 noted that the weighted average interest rate is a direct function of the benchmark rate. As such, a cut to the benchmark rate is likely to feed directly into lower lending rates. Chart 3 showed that the substantial spread between the 3-month and 7-day repo rates that prevailed from late-2016 to mid-2018 has all but disappeared, implying that the PBOC cannot lower interest rates much further by dialing back on macro-prudential regulation. Instead, if it wants interbank rates to fall meaningfully, lowering the corridor around the 7-day rate by cutting the floor (the PBOC’s 7-day reverse repo rate) will likely be required. This would be carried out with further reductions to the reserve requirement ratio (RRR). Third, while Chart 5 showed that our model for the weighted average lending rate has done a very good job over the past few years, it is clear that a gap has opened up between the actual rate and that predicted by the model. The most likely explanation of this gap is that it is due to a risk premium applied by banks, possibly in response to the re-orientation of riskier funding demands that had previously been fulfilled by the shadow banking sector to on-balance sheet loans from depository institutions. It is not clear what policy tools are at the PBOC’s disposable to reduce the gap, but doing so has the potential to lower average interest rates by a non-trivial amount. The relative easiness of monetary conditions is the key difference between today and 2012. It is not clear yet which option the PBOC will pursue over the coming year or whether further monetary easing will occur, but an RRR cut coupled with a benchmark lending rate cut is now a real possibility. If it happens, it would be a clear signal for investors that the monetary policy dial has been turned to “maximum stimulus”. Inferring Reluctance Or Capitulation From Monthly Credit Growth The second issue that investors will be wrestling with over the coming few months relates to the question of whether the month-to-month pace of credit growth is consistent with the magnitude of the reflationary response that we believe will be required. To the extent that significantly more monetary easing occurs over the coming year, it is likely to have happened because policymakers were overly reluctant to green-light a renewed and substantial re-acceleration in credit growth and were then forced to fight a destabilizing slowdown in the economy. Chart 6A Strong Credit Response Will Be Required In Response To A Full Tariff Scenario

A Strong Credit Response Will Be Required In Response To A Full Tariff Scenario

A Strong Credit Response Will Be Required In Response To A Full Tariff Scenario

We have used the metric of new credit to GDP as the primary method to judge the relative size of previous credit booms, and have argued that a return to 30% on this measure will likely be required in response to a full 25% tariff scenario (Chart 6). Unfortunately, China’s unique seasonality patterns and the lack of official seasonally adjusted data make it difficult for investors to judge whether incoming credit data is consistent with the required policy response. Previously, we have shown seasonally adjusted measures of credit using a simple application of X12 ARIMA, the statistical seasonal adjustment program used by the U.S. Census Bureau. But Charts 7 and 8 present a different approach. The charts show the average cumulative amount of adjusted total social financing as the calendar year progresses, along with a ±0.5 standard deviation band, based on the 2010 to 2018 period. The thick black line in both charts shows the progress in new credit creation this year, assuming an 8% annual nominal GDP growth rate for the remainder of the year. Chart 7 shows the cumulative progress in credit assuming a 27% new credit to GDP ratio for the year (corresponding to a half-strength credit cycle relative to past episodes), whereas Chart 8 assumes 30%.

Chart 7

Chart 8

In our view, these charts are revelatory. First, Chart 7 provides evidence that policymakers have been reluctant to allow credit growth to surge. The chart shows that credit growth ran well above a half-strength credit cycle pace in the first quarter of the year; following this, through either administrative controls or jawboning, policymakers lowered the pace of credit growth in April such that it moved back within the range. By contrast, Chart 8 highlights that the pace of Q1 credit growth was exactly right in a 30% new credit to GDP scenario, and that April fell short. In order to be back within the range by June, Chart 8 suggests that monthly credit growth needs to be on the order of 2.8-3 trillion RMB per month in May and June, just a slightly slower pace than what investors observed in March. It is quite possible that May’s credit number will fall short of 2.8-3 trillion RMB, given that the increase in the second round tariffs only occurred on May 10 and that Chinese policymakers have so far seemed reluctant to pull the trigger. But this also heightens the risk of a serious near-term selloff in the domestic equity market, and would set up June as a make-it or break-it month for credit creation. Stimulus Without A Recovery? Revisiting The 2012 Scenario Chart 9The 2012 Scenario: Strong Credit, But A Modest Improvement In Activity

The 2012 Scenario: Strong Credit, But A Modest Improvement In Activity

The 2012 Scenario: Strong Credit, But A Modest Improvement In Activity

A final question facing investors this year is whether it is possible that the Chinese economy fails to respond to strong efforts by policymakers to stimulate the economy. Chart 9 shows that a similar situation occurred in 2012; while the surge in new credit to GDP did stabilize economic activity and caused a modest uptrend, the economic improvement was much smaller than what the relationship shown in the chart would imply. In our view, there are three reasons to believe that a 2012 scenario will not repeat itself: First, Chart 10 shows that the Q1 rebound in new credit to GDP appears to have halted the decline in investment-relevant Chinese economic activity. There is no basis to suggest that an uptrend in activity has begun, but the fact that the economy has even started to respond to the pickup in credit growth is a positive sign. Second, Chart 11 highlights one important difference between 2012 and today. The chart shows that our leading indicator for China’s economy did not rise as much as new credit to GDP, and that this occurred because monetary conditions remained relatively tight from the beginning of 2012 all the way through to early-2015. This relative tightness in monetary conditions occurred because of fairly elevated interest rates, and due to a persistent rise in the real effective exchange rate. However, the collapse in the weighted average lending rate following the 2015/2016 economic slowdown has eased monetary conditions in a lasting way, suggesting that a similar rise in new credit to GDP should have a strongly positive effect on Chinese economic growth. This also underscores our earlier point: monetary policy has already largely returned to 2015/2016 levels, meaning that it is fiscal/administrative action to boost credit growth that is missing. Third, Chart 12 highlights that the pace of inventory accumulation represents another key difference between the current economic environment and that of 2012. The chart shows that the change in China’s level of industrial inventories relative to exports (both measured in value terms) rose sharply in 2011 and 1H 2012, only to slow significantly over the following year (which may have weighed on the rebound in activity in 2012 and 2013). In contrast, the chart shows that inventories have recently been contracting at their fastest pace relative to exports since 2011, implying that the drag on production from potential destocking may be minimal. Chart 10A (Very) Tentative Sign Of Stabilization

A (Very) Tentative Sign Of Stabilization

A (Very) Tentative Sign Of Stabilization

Chart 11Monetary Conditions Are Considerably Easier Today

Monetary Conditions Are Considerably Easier Today

Monetary Conditions Are Considerably Easier Today

There are, however, two caveats to the above analysis. First, on the inventory front, Chart 12 shows that the level of industrial inventories to exports is fractionally higher than it was in 2012, even though it has declined significantly from its 2017 high. The level of inventories has been rising relative to exports for some time, and thus the “equilibrium” level is not clear. But to the extent that a prolonged trade war with the U.S. requires meaningfully lower inventory levels in China, then destocking may become more of a drag than we expect. Second, Chart 11 shows that while monetary conditions are much easier today than they were in 2012, money growth is much weaker. A weaker-than-expected recovery in Chinese economic activity is much more likely if money growth remains weak, although we cannot reasonably envision an outcome where credit growth surges and growth in the money supply does not. A Brief Note On The RMB We noted in our May 15 Weekly Report4 that a significant rise in new credit to GDP and a meaningful decline in the currency would be required to stabilize China’s economy if the U.S. proceeds with 25% tariffs on all imports from China. Consequently, we recommended that investors hedge the inherent RMB exposure from a long US$ cyclical position in Chinese stocks by opening a long USD-CNH trade, with the expectation that a break above 7 in the coming weeks was likely (Chart 13). Chart 12Inventories Have Been Meaningfully Reduced

Inventories Have Been Meaningfully Reduced

Inventories Have Been Meaningfully Reduced

Chart 13In A Full Tariff Scenario, A Defense Of 7 Is Only A Near-Term Event

In A Full Tariff Scenario, A Defense Of 7 Is Only A Near-Term Event

In A Full Tariff Scenario, A Defense Of 7 Is Only A Near-Term Event

Recently, Xiao Yuanqi, the spokesman for the China Banking and Insurance Regulatory Commission, was quoted as saying that “those who speculate and short the yuan will [surely] suffer heavy loss[es]”,5 which many investors took to mean that China will defend USD-CNY = 7 at all costs. In our view this may be true in the short-term, but is unlikely to occur over a 6-12 month time horizon in a full 25% tariff scenario. Policymakers have become much more attuned to sharp declines in the currency after the major episode of capital flight that occurred in 2015 and 2016, and are keen to ensure that any movements in the exchange rate are orderly. However, complete currency stability in the face of a major shock to the export sector means that the required rise in the “macro leverage ratio” to stabilize the economy will be even higher, highlighting that an orderly depreciation in the currency is the lesser of two evils. As such, we interpret these recent comments from policymakers as an attempt to prevent a breach in USD-CNY = 7 over the short-term, and an attempt to control the pace of decline over the longer term in a full-tariff scenario. The conclusion for investment strategy is that China-exposed investors should stay long USD-CNH over the cyclical horizon, but should limit the leverage of the position and should expect frequent short-term reversals. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Weekly Report, “Is Trump Ready For The New Long March?” dated May 24, 2019, available at gps.bcaresearch.com. 2 Please see China Investment Strategy Weekly Report, “Simple Arithmetic,” dated May 15, 2019, available at cis.bcaresearch.com. 3 Please see China Investment Strategy Special Report, “Seven Questions About Chinese Monetary Policy,” dated February 22, 2018, available at cis.bcaresearch.com. 4 Please see China Investment Strategy Weekly Report, “Simple Arithmetic,” dated May 15, 2019, available at cis.bcaresearch.com. 5 Reuters News, “China’s top banking regulator says yuan bears will suffer ‘heavy losses’,” dated May 25, 2019. Cyclical Investment Stance Equity Sector Recommendations

Highlights Corporate Bonds: Corporate bond spreads have been slow to price-in the escalation of the U.S./China trade dispute. Nimble investors should take steps to mitigate their near-term (0-3 month) exposure to credit spreads, but remain overweight corporate bonds (both investment grade and high-yield) on a 6-12 month investment horizon. Duration: With 50 bps of rate cuts already priced into the market for the next 12 months, there is very little money to be made from extending duration and potentially a lot of money to be made by keeping duration low. This is especially true given that the Fed has so far done nothing to suggest that rate cuts are on the table. TIPS: Long-maturity TIPS breakeven inflation rates look cheap on our model, and the core PCE deflator’s sharp drop probably overstates the deflationary pressures in the economy. Maintain an overweight allocation to TIPS versus nominal Treasuries in U.S. bond portfolios. Feature Concerns that the ongoing U.S./China trade war will exacerbate the decline in global growth flared again last week, and our geopolitical strategists see high odds of further near-term escalation.1 For starters, China has not yet retaliated to the U.S. Commerce Department’s blacklisting of Huawei and a handful of other Chinese tech firms. Meanwhile, the U.S. stands ready to extend tariffs across the full slate of imported Chinese goods. To cap it all off, there are currently no firm plans for the resumption of talks between the countries’ respective negotiating teams, and no assurance that Presidents Donald Trump and Xi Jinping will speak to each other at the G20 Summit in Japan on June 28-29. Credit Spreads Are Too Complacent Chart 1Corporate Bonds At Risk

Corporate Bonds At Risk

Corporate Bonds At Risk

While Treasury yields responded to the turmoil by dropping for the second consecutive week, the spillover to corporate bond markets has been less severe. Chart 1 on page 1 shows that corporate bond excess returns have de-coupled from the CRB Raw Industrials index during the past 12 months. The CRB Raw Industrials index tracks a broad basket of commodity prices, making it an excellent real-time indicator of the market’s assessment of global growth. Like Treasury yields, the CRB index has fallen sharply during the past two weeks. The wide gulf between corporate bond and commodity returns suggests that we will soon see either a sell-off in the corporate bond market or a positive re-rating of global growth that sends the CRB index higher. Recent history provides examples of both cases (Chart 2). The CRB index rose to meet corporate bond returns in 2012, but dragged corporate bond returns lower in 2014. Given the long list of potential negative trade catalysts, some near-term downside for corporate bond excess returns appears more likely. But it’s not just political headlines that make us cautious about the near-term outlook for credit spreads. The uncertainty created by the U.S./China trade dispute is now finding its way into the economic survey data. Flash Manufacturing PMIs for the U.S., Eurozone and Japan all fell in May, with respondents quick to blame the decline on global trade tensions. Much like the CRB index, PMI readings are sending a starkly different message than credit spreads. Either trade tensions will ease during the next couple of months, sending PMIs higher, or corporate bond spreads will widen. A model of U.S. capacity utilization based on lagged junk spreads predicts that capacity utilization will rise from its current 78% to 80% during the next six months (Chart 3). However, both the Markit and ISM Manufacturing PMIs suggest a further decline is more likely. Once again, either trade tensions will ease during the next couple of months, sending the PMIs higher, or corporate bond spreads will widen. Chart 2Position For Reconvergence

Position For Reconvergence

Position For Reconvergence

Chart 3Capacity Utilization & Junk Spreads

Capacity Utilization & Junk Spreads

Capacity Utilization & Junk Spreads

We recommend that investors take measures to limit their near-term (~3-month) exposure to corporate spread risk. Stay Positive On A Cyclical (6-12 Month) Horizon Chart 4Expect More Stimulus From China

Expect More Stimulus From China

Expect More Stimulus From China

While near-term caution is warranted, we would still position for positive corporate bond excess returns (both investment grade & high-yield) on a 6-12 month investment horizon. Ultimately, the U.S. and China will navigate toward some sort of truce, and the negative impact from tariffs is unlikely to derail the U.S. economic recovery.2 What’s more, Chinese policymakers will accelerate their stimulus efforts to mitigate the negative impact of higher tariffs. Our China Investment Strategy service tracks a composite of six money and credit growth indicators that lead Chinese economic activity. This leading indicator has already bottomed, and our strategists anticipate a return to stimulus levels reminiscent of mid-2016 (Chart 4).3 As long as a U.S. recession is avoided, corporate bond spreads will eventually settle near levels seen in the late stages of previous economic cycles (Chart 5A & Chart 5B).4 Chart 5AInvestment Grade Spread Targets

Investment Grade Spread Targets

Investment Grade Spread Targets

Chart 5BHigh-Yield Spread Targets

High-Yield Spread Targets

High-Yield Spread Targets

Bottom Line: Corporate bond spreads have been slow to price-in the escalation of the U.S./China trade dispute. Nimble investors should take steps to mitigate their near-term (0-3 month) exposure to credit spreads, but remain overweight corporate bonds (both investment grade and high-yield) on a 6-12 month investment horizon. Risk & Reward In The Treasury Market Unlike credit spreads, Treasury yields have responded aggressively to the negative news flow. The 10-year Treasury yield currently sits at 2.32%, 7 bps lower than at this time last week. Meanwhile, the overnight index swap curve is priced for two full 25 basis point rate cuts over the next 12 months. Interestingly, while market prices imply 50 bps of rate cuts during the next year, the New York Fed’s Survey of Market Participants shows that, as of the May FOMC meeting, investors didn’t actually expect rate cuts any time soon. The shaded region in Chart 6 shows the interquartile range of the surveyed investors’ fed funds rate forecasts, while the dashed black line shows the median forecast. The survey responses convey widespread consensus that the fed funds rate will remain flat until the end of the year – the 25th percentile, median and 75th percentile are all equal until the end of 2019. Then, heading into 2020, the 75th percentile of the distribution starts to forecast rate hikes. The 25th percentile doesn’t move in the direction of rate cuts until Q4 2020, and the median forecaster sees the fed funds rate staying put at least through the second half of 2021. Chart 6Market And Survey Expectations Differ

Market And Survey Expectations Differ

Market And Survey Expectations Differ

Why would market prices imply a much lower path for the fed funds rate than actual investor survey responses? The most likely reason relates to assessments about the balance of risks. When responding to surveys, investors will usually provide their modal (or most likely) outcome. However, investor bets in financial markets will reflect a dollar-weighted average of different possible scenarios. It’s possible that while investors think a flat fed funds rate is the most likely outcome, they also view rate cuts as a higher probability tail risk than rate hikes. They therefore invest some of their money to hedge that risk, even if it does not reflect their base case view.

Chart 7

The intuition that rate cuts remain a “tail risk” is confirmed by another question from the survey. This question asks investors to consider a time period between now and the end of the year, and then attach a probability to the Fed’s next move i.e. whether it will be hike, a cut, or whether there will be no change in the funds rate until the end of 2019 (Chart 7). As of the April/May survey, market participants thought the odds of a hike were 23%, odds of a cut were 17% and the odds of flat rates until the end of the year were 59%. Before the Fed meeting in March, investors saw 50% chance of a hike, 13% chance of a cut, and 37% chance of no change. The overall message is that investors continue to view a 2019 rate cut as a tail risk, but one that’s perceived probability is rising. In any event, for our purposes it doesn’t really matter how investors respond to surveys. According to our Golden Rule of Bond Investing, if the actual change in the fed funds rate over the next 12 months exceeds what is currently priced into the OIS curve for that period, then below-benchmark portfolio duration positions will pay off.5 In fact, the Golden Rule even gives us a framework for translating different rate hike/cut scenarios into expected 12-month Treasury returns (Table 1). Table 1The Golden Rule Of Bond Investing

Hedge Near-Term Credit Exposure

Hedge Near-Term Credit Exposure

Based on current prices, if the fed funds rate holds steady for the next 12 months – as the median market participant expects – we calculate that the Bloomberg Barclays Treasury Master Index will lose between 1.98% and 2.41% relative to cash. Even in the scenario where the Fed delivers two rate cuts during the next 12 months, we would still expect Treasury index returns to lag cash by 12-13 bps. Negative excess returns in the “two rate cut” scenario are due to the negative carry in the Treasury index. Capital gains/losses would be close to zero in that scenario, since the change in the fed funds rate is exactly equal to the market’s expectations. Investors continue to view a 2019 rate cut as a tail risk, but one that’s perceived probability is rising. What’s evident from those figures is that there is currently very little money to be made betting on rate cuts, and quite a bit to be made betting on rate hikes. The risk/reward balance in the Treasury market clearly favors keeping portfolio duration low. But What Will The Fed Actually Do? The minutes from the last FOMC meeting show broad consensus around the Fed’s current “on hold” policy stance, though it’s notable that “a few” participants thought rate hikes would be appropriate if the economy evolved in line with their expectations. The minutes contain no mention of a possible rate cut. Our sense is that it would require a further sharp tightening of financial conditions or significantly worse economic data before the Fed seriously considers cutting rates. Our Fed Monitor – an aggregate indicator that measures economic growth, inflation and financial conditions – is currently very close to the zero line, a level consistent with the Fed’s “on hold” stance (Chart 8). The ISM Manufacturing PMI is also firmly above the 50 boom/bust line. Historically, Fed rate cuts are usually preceded by a negative reading from our Fed Monitor and a sub-50 PMI. We would be looking for those two signals before expecting the Fed to cut rates. Chart 8Sub-50 ISM Required Before The Fed Cuts Rates

Sub-50 ISM Required Before The Fed Cuts Rates

Sub-50 ISM Required Before The Fed Cuts Rates

Bottom Line: With 50 bps of rate cuts already priced into the market for the next 12 months, there is very little money to be made from extending duration and potentially a lot of money to be made by keeping duration low. This is especially true given that the Fed has so far done nothing to suggest that rate cuts are on the table. Inflation & TIPS Chart 9Adaptive Expectations Model

Adaptive Expectations Model

Adaptive Expectations Model

It’s not just nominal Treasury yields that dropped during the past two weeks. Long-maturity TIPS breakeven inflation rates – the spread between nominal Treasury yields and TIPS yields – also fell precipitously. The 10-year TIPS breakeven inflation rate is currently 1.76% and the 5-year/5-year forward breakeven is only 1.9%. These figures suggest that the market does not trust the Fed to meet its inflation target in the long-run. Our main valuation tool for the 10-year TIPS breakeven rate is our Adaptive Expectations Model.6 It derives a fair value for the 10-year breakeven based on: The 10-year rate of change in the core consumer price index The 12-month rate of change in the headline consumer price index The New York Fed’s Underlying Inflation Gauge At present, the 10-year TIPS breakeven rate is 20 bps below the model’s fair value (Chart 9). It shouldn’t be too surprising that TIPS look cheap relative to nominals. Recent inflation data have been weak and the Fed has written off the weakness as “transitory”, leading to doubts about whether it will keep rates low enough to meet its target. For our part, we think investors should take advantage of low breakevens and overweight TIPS versus nominal Treasuries in U.S. bond portfolios. In fact, the Fed’s characterization of low inflation as “transitory” seems correct. Chart 10 shows both the core and trimmed mean PCE deflators. The dramatic fall in the core measure, which strips out food and energy prices from the headline number, is what has caught the market’s attention. But it’s important to note that trimmed mean PCE inflation has not confirmed the decline. In fact, it remains in a multi-year uptrend. Recent inflation data have been weak, but the Fed has written off the weakness as “transitory”. Chart 10Low Inflation Looks "Transitory"

Low Inflation Looks "Transitory"

Low Inflation Looks "Transitory"

This is the third time during this cycle that core PCE inflation has diverged negatively from the trimmed mean. Core eventually rebounded and re-converged with the trimmed mean in both of the prior two episodes. The Fed is banking on the third time playing out the same way, and we think it would be unwise to bet against them. Recently released research from the Federal Reserve Bank of Dallas shows that trimmed mean PCE inflation provides a less-biased real-time estimate of the headline figure than the traditional core measure. The latter tends to run too low. The trimmed mean is also more closely related to labor market slack.7 Bottom Line: Long-maturity TIPS breakeven inflation rates look cheap on our model, and the core PCE deflator’s sharp drop probably overstates the deflationary pressures in the economy. Maintain an overweight allocation to TIPS versus nominal Treasuries in U.S. bond portfolios. Ryan Swift U.S. Bond Strategist rswift@bcaresearch.com 1 Please see Geopolitical Strategy Weekly Report, “Is Trump Ready For The New Long March?” dated May 24, 2019, available at gps.bcaresearch.com 2 The potential economic impact from tariffs is discussed in Global Investment Strategy Weekly Report, “Tarrified,” dated May 16, 2019, available at gis.bcaresearch.com 3 Please see China Investment Strategy Weekly Report, “Simple Arithmetic,” dated May 15, 2019, available at cis.bcaresearch.com 4 For details on how we determine the spread targets shown in Charts 5A & 5B, please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 5 Please see U.S. Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com 6 For details on the model’s construction please see U.S. Bond Strategy Weekly Report, “Adaptive Expectations In The TIPS Market,” dated November 20, 2018, available at usbs.bcaresearch.com 7 https://www.dallasfed.org/-/media/Documents/research/papers/2019/wp1903… Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Falling Yields: There have been three main drivers of the latest decline in global bond yields: slower global growth, softer inflation expectations and increased safe-haven demand for bonds given the intensifying U.S.-China trade conflict. The first two are more than fully discounted in current yield levels, but the latter is likely to persist in the near-term with no resolution of the trade conflict in sight. Model Portfolio Adjustments: We are tactically reducing the sizes of the overall strategic tilts in our model bond portfolio – below-benchmark duration exposure and overweight global corporates vs. governments. There is a growing risk of deeper selloffs in global equity and credit markets if the June G-20 meeting produces no positive signals on ending the trade dispute. We do not yet see a case to position more defensively on a medium-term horizon, however, given the pickup in “early” global leading economic indicators. Feature Chart of the WeekYields Discount A Lot Of Bad News

Yields Discount A Lot Of Bad News

Yields Discount A Lot Of Bad News

The investment backdrop at the moment – slowing global growth momentum, softening inflation expectations, an increasingly prolonged U.S.-China trade dispute with no immediate sign of resolution, and a strengthening U.S. dollar– is fairly bond bullish. Unsurprisingly, government bond yields in the developed markets have fallen to levels more consistent with a less certain macro environment. At one point last week, the 10-year U.S. Treasury yield dipped as low as 2.30%, while the 10-year German Bund fell deeper into negative territory at -0.13%. There are now expectations of easier monetary policy discounted in yield curves of several countries, most notably the U.S. where markets are priced for 50bps of Fed rate cuts over the next year – despite no indication from the Fed that cuts are coming anytime soon. From a valuation perspective, bond yields are starting to look a bit stretched to the downside (Chart of the Week). The term premium component of yields has fallen to near post-crisis lows in the majority of countries, while the U.S. dollar has surged despite lower U.S. interest rate expectations – both indications of investors driving up the value of traditional safe-havens at a time of uncertainty. Looking purely at the growth side of the equation, the downward momentum in bond yields should start to fade with the global leading economic indicator now in the process of bottoming out. That does not mean, however, that yields could not fall further in the near-term if the trade headlines get worse and risk assets sell off more meaningfully – an outcome that grows increasingly likely as the two sides in the trade war seem to be digging in for a longer battle. The State Of The World Since The “TTT” Our colleagues at BCA Geopolitical Strategy now believe that there is only a 40% chance of a U.S.-China trade deal by the end of June. This could trigger a deeper selloff in global equity and credit markets if investors begin to price in a larger and more prolonged hit to economic growth and corporate profits from the U.S. tariffs. This would trigger even greater safe-haven flows into government bonds, pushing yields lower through a more negative term premium. The much lower level of U.S. Treasury yields has helped limit the hit to risk asset prices from the elevated uncertainty over global trade. Since the “Trump Tariff Tweet” (TTT) of May 5, when the new round of tariffs on U.S. imports from China was announced which sparked the new leg of the trade war, the fall in benchmark 10-year government bond yields across the developed world can be fully explained by the fall in the term premium (Table 1). For example, the 10-year U.S. Treasury yield has fallen -14bps since the TTT, while our estimate of the term premium on the 10-year Treasury as decreased by -20bps. Over the same time period, 10-year U.S. inflation expectations have also fallen -11bps, but the market has only priced in an additional -5bps of Fed rate cuts over the next year according to our Fed Discounter. Table 1Decomposing 10-Year Government Bond Yield Changes Since The "Trump Tariff Tweet"

The Message From Low Bond Yields

The Message From Low Bond Yields

The big difference between last December and today is the much lower level of U.S. Treasury yields. Lower yields have helped mute the hit to risk asset prices from the elevated uncertainty over global trade since the TTT (Chart 2). The Fed’s more dovish pivot in the early months of 2019 has helped push Treasury yields lower as investors have moved from pricing in rate hikes to discounting rate cuts. Even traditional “risk-off” measures like the VIX, U.S. TED spreads, the price of gold and the Japanese yen have only risen modestly since the TTT compared to the big moves seen back in December when investors feared that the Fed would tighten right into a U.S. recession (Chart 3). Chart 2Risk Assets Remain Relatively Calm

Risk Assets Remain Relatively Calm

Risk Assets Remain Relatively Calm

Chart 3Falling Bond Yields Helping Keep Vol Subdued

Falling Bond Yields Helping Keep Vol Subdued

Falling Bond Yields Helping Keep Vol Subdued

Easier monetary policy, if delivered, can help underwrite a rebound in equity and credit markets. When looking across the array of financial market returns since the TTT (Table 2), the only developed economies that have seen equities appreciate are Australia and New Zealand – countries where rate cuts are being signaled by policymakers (or already delivered, in the case of New Zealand). Table 2Asset Returns By Country Since The "Trump Tariff Tweet"

The Message From Low Bond Yields

The Message From Low Bond Yields

In the case of the U.S., however, numerous Fed officials have stated recently that no changes to U.S. monetary policy are likely without decisive evidence that the new round of China tariffs and trade uncertainty was having a major negative impact on U.S. growth. On that front, forward-looking measures of U.S. economic activity, like the Conference Board leading economic indicator or our models for U.S. employment and capital spending, are not pointing to an imminent sharp slowing of U.S. growth (Chart 4). At the same time, leading indicators like our global LEI diffusion index and the China credit impulse are both signaling that global growth momentum may soon start surprising to the upside (Chart 5). Chart 4No U.S. Recession Signal Yet From These Indicators

No U.S. Recession Signal Yet From These Indicators

No U.S. Recession Signal Yet From These Indicators

Chart 5Some Reasons For Optimism On Global Growth

Some Reasons For Optimism On Global Growth

Some Reasons For Optimism On Global Growth

If the Fed does not see a case to deliver the rate cuts that are now discounted, or even to just signal to the markets that easier policy is coming soon, then there is a greater chance of a deeper pullback in U.S. equity and credit markets from any new negative news on trade. This suggests that the risk-aversion bid for U.S. Treasuries will result in an even more deeply negative U.S. term premium and lower bond yields. Easier monetary policy, if delivered, can help underwrite a rebound in equity and credit markets. Already, we are seeing such increasingly negative correlations between returns on equities and government bonds across the major developed markets. In Charts 6 & 7, we show the rolling 52-week correlation between local government bond and equity returns for the U.S., euro area, Japan, U.K., Canada and Australia. For each country, we also plot that correlation versus our estimate of the term premium on 10-year government bond yields. Chart 6Safe Haven Demand For Bonds ...

Safe Haven Demand For Bonds...

Safe Haven Demand For Bonds...

Chart 7... Helping Drive Down Term Premia

...Helping Drive Down Term Premia

...Helping Drive Down Term Premia

It is clear that there is a significant “risk-aversion bid” for government bonds right now, given the increasingly negative stock/bond correlations and falling term premia. One possible interpretation is that falling bond yields are being driven more by fears of a risk-off selloff in global equity and credit markets rather than rational pricing of future monetary policy or inflation expectations because of slowing growth. Interestingly, Australia – where the central bank has been signaling that rate cuts are imminent – is the only exception in this list of countries where the stock/bond correlation is not negative. There, the deeply negative term premium is more about weakening growth and low inflation expectations, which is forcing a dovish response from the Reserve Bank of Australia, rather than a risk aversion bid for safe assets from investors. It is clear that there is a significant “risk-aversion bid” for government bonds right now, given the increasingly negative stock/bond correlations and falling term premia. Net-net, while bond yields discount a lot of bad news and now look too low compared to tentative signs of improving global growth, it is hard to build a case for an imminent rebound in global bond yields without signs that U.S. and China are getting closer to a trade deal. Bottom Line: There have been three main drivers of the latest decline in global bond yields: slower global growth, softer inflation expectations and increased safe-haven demand for bonds given the intensifying U.S.-China trade conflict. The first two are more than fully discounted in current yield levels, but the latter is likely to persist in the near-term with no resolution of the trade conflict in sight. Tactical Risk-Reduction Adjustments To Our Model Bond Portfolio Chart 8Easier Monetary Policy Required In Europe & Australia

Easier Monetary Policy Required In Europe & Australia

Easier Monetary Policy Required In Europe & Australia

Given the growing potential for a larger selloff in global risk assets if no U.S.-China trade deal comes out of next month’s G-20 meeting (where Presidents Trump and Xi will both be in attendance), we think it is prudent to make some tactical adjustments to the recommended weightings within our model bond portfolio. These moves will provide a partial hedge against any near-term widening of global credit spreads or further reduction in government bond yields in the event of a complete breakdown of the trade talks. Specifically, we are making the following changes: Duration Exposure: We are increasing the overall duration of the model bond portfolio by 0.5 years, which still leaves a duration position that is 0.5 years below the custom benchmark index of the portfolio. We are doing this by increasing allocations to the longer maturity buckets in the U.S., Japan and France. Credit Exposure: We are cutting the sizes of our recommended overweight tilts for U.S. corporates in half for both investment grade and high-yield. This is a combined reduction of nearly 4% of the portfolio that will be used to fund the increase in duration on the government bond side. We are making no other changes to our government bond country allocations, staying overweight in core Europe (Germany plus France), Japan and Australia where our Central Bank Monitors are calling for a need for easier monetary policy (Chart 8). We are also staying overweight U.K. Gilts, where yields continue to trade more off Brexit uncertainty than domestic economic growth or inflation pressures. We are not making any changes to the model bond portfolio exposure to euro area corporate debt or Italian governments, riskier spread products where we are already underweight. We are, however, maintaining our weightings for U.S. dollar denominated EM sovereign and corporate debt at neutral. EM debt has performed relatively well versus developed market equivalents since the May 5 “Trump Tariff Tweet” (TTT). We understand that not downgrading EM seems counterintuitive when we are trying to position more defensively in the model portfolio. We prefer to reduce exposure to U.S. credit, however, given that EM debt has performed relatively well versus developed market equivalents since the May 5 TTT (Table 3), and with EM spreads now at more attractive levels relative to U.S. investment grade (Chart 9). In addition, EM credit tends to perform better during periods when Chinese credit growth is accelerating, as is currently the case (bottom panel) – and which may continue if China’s policymakers eventually turn to more domestic stimulus measures to combat the effects of U.S. tariffs, as seems likely. Table 3Credit Market Performance Since The "Trump Tariff Tweet"

The Message From Low Bond Yields

The Message From Low Bond Yields

Chart 9EM Credit Offers Value Versus U.S. Corporates

EM Credit Offers Value Versus U.S. Corporates

EM Credit Offers Value Versus U.S. Corporates

Importantly, these are all only tactical changes to our model portfolio to partially protect against the risk of U.S. credit spread widening in the event of more negative news on the U.S.-China trade front. We still have not changed our strategic (6-12 month) views on global bond yields (higher) and global corporates (outperforming government bonds) given the tentative signs of improving global growth from the leading indicators. Bottom Line: We are tactically reducing the sizes of the overall strategic tilts in our model bond portfolio – below-benchmark duration exposure and overweight global corporates vs. governments. There is a growing risk of deeper selloffs in global equity and credit markets if the June G20 meeting produces no positive signals on ending the trade dispute. We do not yet see a case to position more defensively on a medium-term horizon, however, given the pickup in “early” global leading economic indicators. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

The Message From Low Bond Yields

The Message From Low Bond Yields

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Treasury yields have tumbled despite a solid U.S. economy: The 10-year Treasury bond yielded just under 3% when we started beating the below-benchmark-duration drum last summer; now it’s hovering around 2.3%. The golden rule of bond investing argues against positioning for further declines, … : The returns to duration strategies hinge on the difference between actual and expected moves in the fed funds rate. With the money market looking for two cuts over the next twelve months, the fed funds rate is more likely to surprise to the upside than the downside. … but could a lack of borrowing keep yields low?: If debt-fueled spending has gone out of fashion in the U.S., global savings could overwhelm investment, and rates might have to fall further to bring them back into balance. Feature The ride has gotten bumpier as the trade tensions between the U.S. and China have heated up, but our recommendations have held up well since last summer. Equal-weighting equities, underweighting bonds and overweighting cash helped preserve capital during the fourth-quarter selloff, while our early and late January upgrades of equities (while downgrading cash) and spread product (while further downgrading Treasuries), respectively, have proven to be beneficial.1 On a total return basis, the S&P 500 is up over 12% since our upgrade, and the Barclays Bloomberg Corporate and High Yield Indexes have generated excess returns over Treasuries of around 175 and 75 basis points (“bps”), respectively, despite ceding much of their previous leads.2 Even the TIPS ETF (TIP) has held its own with the equivalent-duration nominal-Treasury ETF (IEF). The below-benchmark duration call has eroded some of the overall outperformance, however, and there has been some debate within BCA about whether or not we should change the view. We still do not believe the monetary policy outlook merits a duration-view change. We remain constructive on the outlook for global growth, despite the escalation in tensions between U.S. and Chinese trade negotiators, and therefore do not see a fundamental reason to expect lower real rates. The idea that soft credit growth could hold rates down is interesting, but one would have to believe the spendthrift U.S. leopard really has changed its spots to position a portfolio in line with it. Fed Policy Chart 1Caution: Falling Rate Expectations

Caution: Falling Rate Expectations

Caution: Falling Rate Expectations

As of Thursday’s close, the money market was pricing in a 100% chance of a 25-bps rate cut by Thanksgiving, a 100% chance of a 50-bps rate cut by this time next year, and a 45% chance of a third cut by Thanksgiving 2020 (Chart 1, bottom panel). The FOMC has paused its rate-hiking campaign, to be sure, but the idea that it will soon embark on a rate-cutting campaign seems like a stretch. The minutes from the FOMC’s April 30th-May 1st meeting, released last week, painted a picture of a fundamentally solid economy. The balance between hawks and doves remained roughly equal, with “a few participants” calling for a coming need to firm policy, given the swiftness with which inflation pressures can build in a tight labor market, while “a few other participants” noted that the unemployment rate is not the be-all and end-all measure of resource utilization. From an investment strategy perspective, we think our U.S. Bond Strategy service’s golden rule provides the best insight. Below-benchmark-duration positioning will outperform if the Fed cuts less (or hikes more) over the next twelve months than markets expect; above-benchmark-duration will win if the Fed cuts more (or hikes less) than markets expect. Some strategists within BCA have raised the possibility that market expectations could force the Fed’s hand. The reason that the Fed is especially loath to disappoint markets in what might be called the forward-guidance era of central banking, but we think there’s an important distinction between taking care not to surprise markets and surrendering one’s free will to them, as parents of young children can attest. Bottom Line: We think the money markets are significantly overestimating the possibility that the Fed will soon cut the fed funds rate, increasing the potential returns from below-benchmark-duration positioning. The Rates Checklist Table 1Rates View Checklist

Is America Not Borrowing Enough?

Is America Not Borrowing Enough?

We developed our rates checklist3 to provide a list of real-time measures that bear on our rates view. Of the eleven items on the list, only three have met our threshold for reassessing our bearish rates call at any point over the last eight months, so we have stayed the course (Table 1). The checked boxes indicate that the evidence has been moving against us, though we would argue that the stingy 10-year Treasury yield has gotten overly carried away with discounting that evidence (Chart 1, top panel). Policy Perceptions The spread between our monetary policy expectations and the markets’ remains wide, so the prospective returns from our Fed call remain ample, and the first box remains unchecked. Thanks to last week’s two-day, 11-bps decline in the 10-year Treasury yield, we have again checked the inverted yield curve box, which first inverted for five days near the end of March, and has inverted for four days so far in May. Our empirical study of the inverted curve’s recession-signaling properties used month-end closes for the 10-year Treasury yield and the 3-month Treasury Bill rate, and found that an inverted curve had called the seven recessions that have occurred over the last 50 years with just one false positive (Chart 2). Now that the curve has inverted over a couple of daily stretches, clients have asked us just what constitutes bona fide inversion. Chart 2Accurate Yield Curve Signals Tend To Last

Accurate Yield Curve Signals Tend To Last

Accurate Yield Curve Signals Tend To Last

Per the curve’s moves over the last 50 years, we would say inversion doesn’t issue an actionable signal until it persists for at least a few months (Table 2). 1998’s false alarm encompassed just seven days between late September and early October, and covered just one month end. The intuition behind the inverted yield curve’s predictive power is that the bond market sniffs out economic weakness before the Fed officially changes course. Recognizing that the Fed will have to begin cutting rates soon, bond investors buy longer-maturity instruments to reap the biggest rewards. Investors shouldn’t overreact to tentative inversions of the yield curve. Table 2Yield Curve Inversions

Is America Not Borrowing Enough?

Is America Not Borrowing Enough?

We have argued that the next recession will not occur until the Fed has hiked the fed funds rate to a level above the equilibrium fed funds rate. Since we cannot observe the equilibrium rate in real time, we have looked to interest-rate-sensitive segments of the economy to gauge if higher rates are beginning to bite. Housing is on the front line of interest-rate sensitivity, and it remains quite affordable relative to history, suggesting that monetary policy has not yet become restrictive. Every time the inverted curve preceded a recession, the affordability index was below its long-run mean or rapidly making its way there (mid-1973); when the yield curve briefly inverted in September 1998, homes remained more affordable than average (Chart 3). Chart 3If Higher Rates Aren't Squeezing The Economy, The Yield Curve May Be Crying Wolf

If Higher Rates Aren't Squeezing The Economy, The Yield Curve May Be Crying Wolf

If Higher Rates Aren't Squeezing The Economy, The Yield Curve May Be Crying Wolf

Inflation We concede that realized inflation measures (Chart 4), and inflation expectations as proxied by the difference in TIPS and nominal Treasury yields (Chart 5), have lost momentum since last summer. Washington’s unexpected grant of six-month waivers for importing Iranian oil caused crude prices to plunge, taking headline inflation measures and inflation expectations down with them (Chart 6). Given our Commodity And Energy Strategy team’s view that oil prices will extend their rebound across the rest of this year and into next, we expect that they will again move higher. Chart 4Consumer Price Indexes, ...

Consumer Price Indexes, ...

Consumer Price Indexes, ...

chart 5... And Inflation Breakevens, ...

... And Inflation Breakevens, ...

... And Inflation Breakevens, ...

Chart 6... Are Joined At The Hip With Oil Prices

... Are Joined At The Hip With Oil Prices

... Are Joined At The Hip With Oil Prices

The Labor Market And Imbalances At Home And Abroad The labor market remains tight, so none of the labor market indicators argue for easier monetary policy and lower rates across the term structure. As far as the instability indicators go, there is as yet no sign of unsustainable activity in the economy’s key cyclical sectors. The Fed has stopped emphasizing the idea that financial sector imbalances alone might justify tighter policy, but anecdotal reports about lending standards suggest that potential vulnerabilities remain. There has not yet been an outbreak of major international distress that could deter the Fed from tightening policy, but worsening trade tensions and continued dollar strength would seem to make it slightly more likely. Bottom Line: We have checked a few boxes on our rates checklist, but the available evidence does not support adopting a more constructive view on rates. Hey, Big Spender The American consumer has long been a punching bag for Austrian School adherents and other moralists. As much as they scorn American households for living beyond their means, U.S. consumption has long played a symbiotic role in the global economy. As the engine powering the world’s largest economy, it makes an essential contribution to global aggregate demand, and provides an outlet for export powerhouses like China and Germany. An economy can only run a current account surplus provided that there are other economies running current account deficits capable of offsetting it. Measured inflation and inflation expectations were beginning to get some traction before oil collapsed upon the issuance of Iranian import waivers. In a recent blog post, former BCA Editor-in-Chief Francis Scotland posited that interest rates may not go anywhere as long as American households embrace their nascent post-crisis frugality. Using U.S. household demand as a proxy for global aggregate demand, Francis argues that if households don’t borrow and spend the way they did throughout the pre-crisis postwar era, global aggregate demand will suffer unless another profligate spender emerges to pick up the slack. Add China to the mix, and global savings could swamp global investment. Against that backdrop, savings and investment would only realign if rates fell. Newly frugal U.S. households may be helping to cap interest rates, but it’s too early to declare the end of the Debt Supercycle. Broadening the scope to include all public- and private-sector U.S. borrowing, the nominal 10-year Treasury yield has taken some cues from growth in aggregate borrowing (Chart 7). The relationship with real yields is not as strong (Chart 8), but if borrowing has some relationship to inflation, as under the guns-and-butter fiscal policy of the late sixties, nominal yields might well be a better measure. We can easily go along with the supply-and-demand intuition behind the observed relationship: when there’s stronger demand for credit, rates have to rise to entice savings and discourage investment to bring them back into balance, and vice versa. Chart 7Nominal Treasury Yields Have Been Tightly Linked With The Pace Of Loan Growth, ...

Nominal Treasury Yields Have Been Tightly Linked With The Pace Of Loan Growth, ...

Nominal Treasury Yields Have Been Tightly Linked With The Pace Of Loan Growth, ...

Chart 8... And Real Yields Have Broadly Followed The Pattern As Well

... And Real Yields Have Broadly Followed The Pattern As Well

... And Real Yields Have Broadly Followed The Pattern As Well

Government borrowing filled the void left by retrenching households and corporations in the immediate aftermath of the crisis. Household and corporate loan demand has been choppy since, however, and growth in aggregate borrowing has bumped around its mid-1950s lows throughout the expansion. We are not ready to declare that Americans have turned over a new, parsimonious leaf. The federal budget deficit soared following the passage of the stimulus package, and the CBO projects that it will continue to widen. Household debt growth is at its pre-crisis lows, but it has been accelerating ever since 2010 (Chart 9), and with debt service as a share of disposable income at its lowest level in at least 40 years, households have plenty of capacity to borrow. Chart 9Don't Count Consumers Out Just Yet

Don't Count Consumers Out Just Yet

Don't Count Consumers Out Just Yet

Bottom Line: Interest rates have moved directionally with aggregate loan growth across the postwar era. Tepid loan demand growth may well keep a lid on rates, but we are not convinced that the Debt Supercycle has really breathed its last. Investment Implications Now that the 10-year Treasury yield has drifted back down to 2.3%, we believe the distribution of potential rate outcomes a year from now is skewed to the upside. We are thereby sticking with our recommendation that investors underweight Treasuries and maintain below-benchmark-duration positioning in all fixed-income portfolios. Even if there is not a clear catalyst on the immediate horizon for higher rates, we do not think that either the U.S. or the global economy is so fragile that investors should position for further rate declines. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see the January 7 and January 28, 2019 U.S. Investment Strategy Weekly Reports, “What Now?” and “Double Breaker,” available at usis.bcaresearch.com. 2 All return data calculated as of the Thursday, May 23rd close. 3 Please see the September 17, 2018 U.S. Investment Strategy Weekly Report, “What Would It Take To Change Our Bearish Rates View?” available at usis.bcaresearch.com.