Policy

Our Portfolio Allocation Summary for January 2025.

Job openings once again beat expectations in November, increasing to 8.1m from 7.8m in October. However, hires and quits decreased and layoffs increased. The gap between quits and layoffs, a leading indicator of labor market demand, ticked down. The jobs gap,…

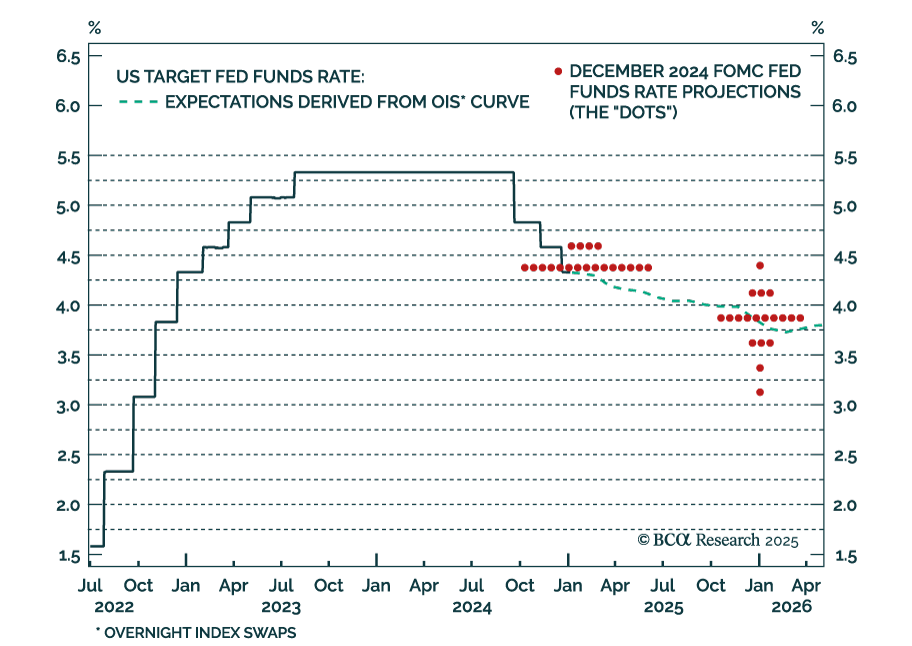

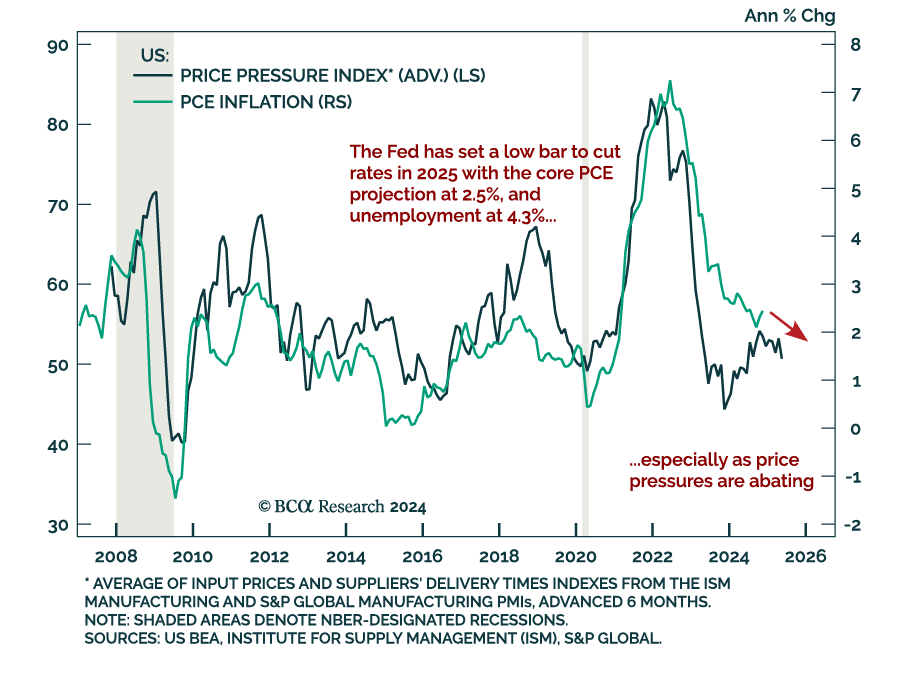

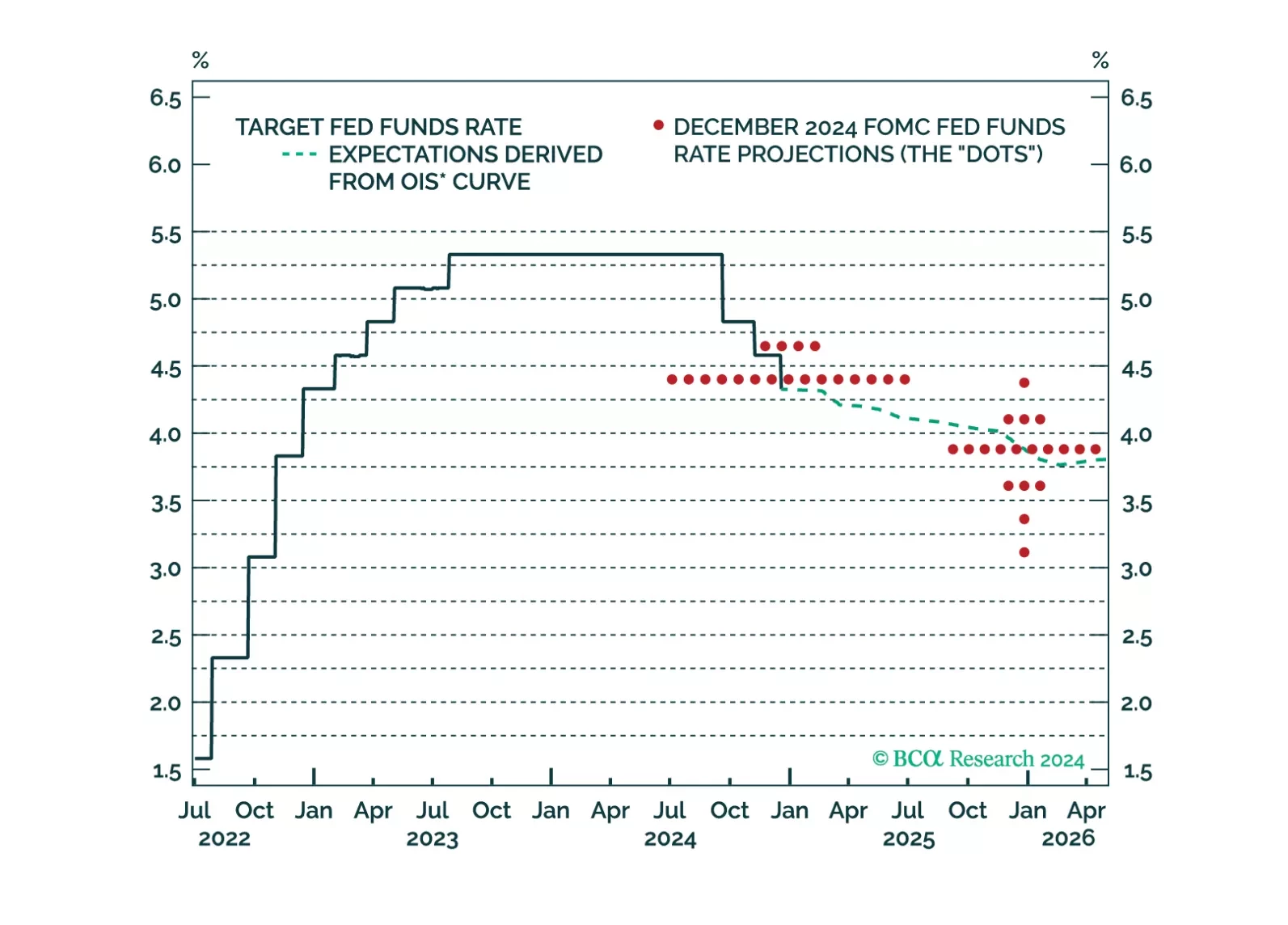

Our US Bond Strategy team published their outlook for the Fed in 2025. They expect more cuts than the 50 bps signaled by the Fed at its December meeting. Core PCE inflation is tracking well below the Fed’s 2.5% forecast, while unemployment could exceed…

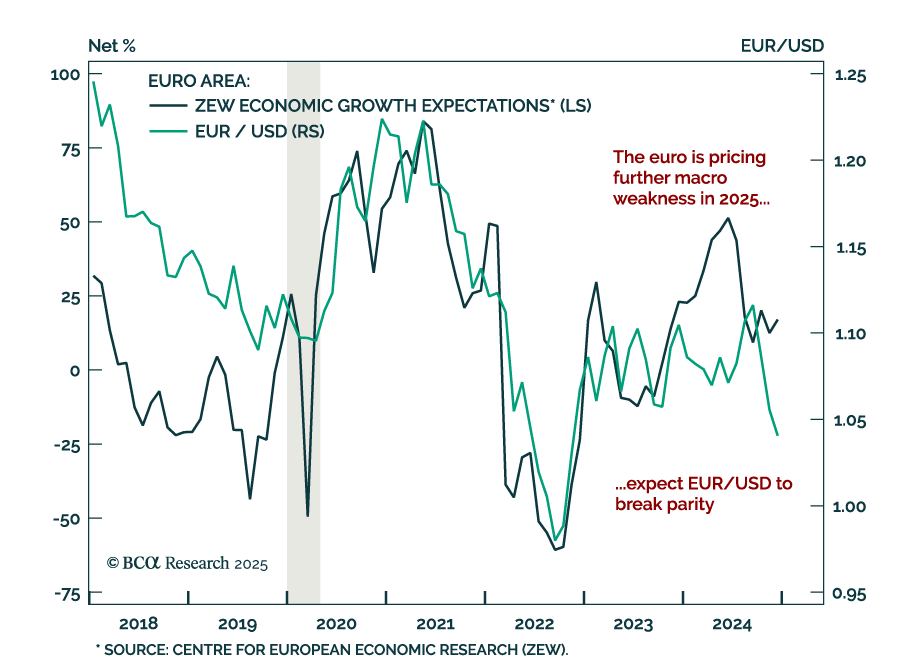

The euro broke the support level of its 2-year trading range against the USD, extending the strong dollar trend witnessed since September of last year. This trend will continue in Q1 2025. Despite global yields rallying in late 2024, the Bund-Treasury…

The Fed’s preferred measure of inflation, core PCE, came in below expectations at 0.1% m/m in November, remaining steady at 2.8% y/y. The monthly advance was the lowest since May. The inflation deceleration was broad-based. Core services inflation increased…

The November UK CPI, in line with estimates, hit an eight-month high, accelerating from 2.3% y/y to 2.6%. Core and services inflation were also strong at 3.5% (vs. 3.3% in October) and 5.0% (flat from October), respectively. Services inflation…

The Federal Reserve cut the fed funds rate by 25 bps to a 4.25%-4.5% range, as expected. However, it was a “hawkish cut”; the FOMC signaled a slower pace of easing ahead. The statement signalled less urgency, saying the “extent and timing” for further cuts…

Our Global Fixed Income and FX strategists published their 2025 outlook, and provide five key views for the year ahead. Duration revival: After three years of underperformance versus cash, government bonds will outperform in either a soft-landing…

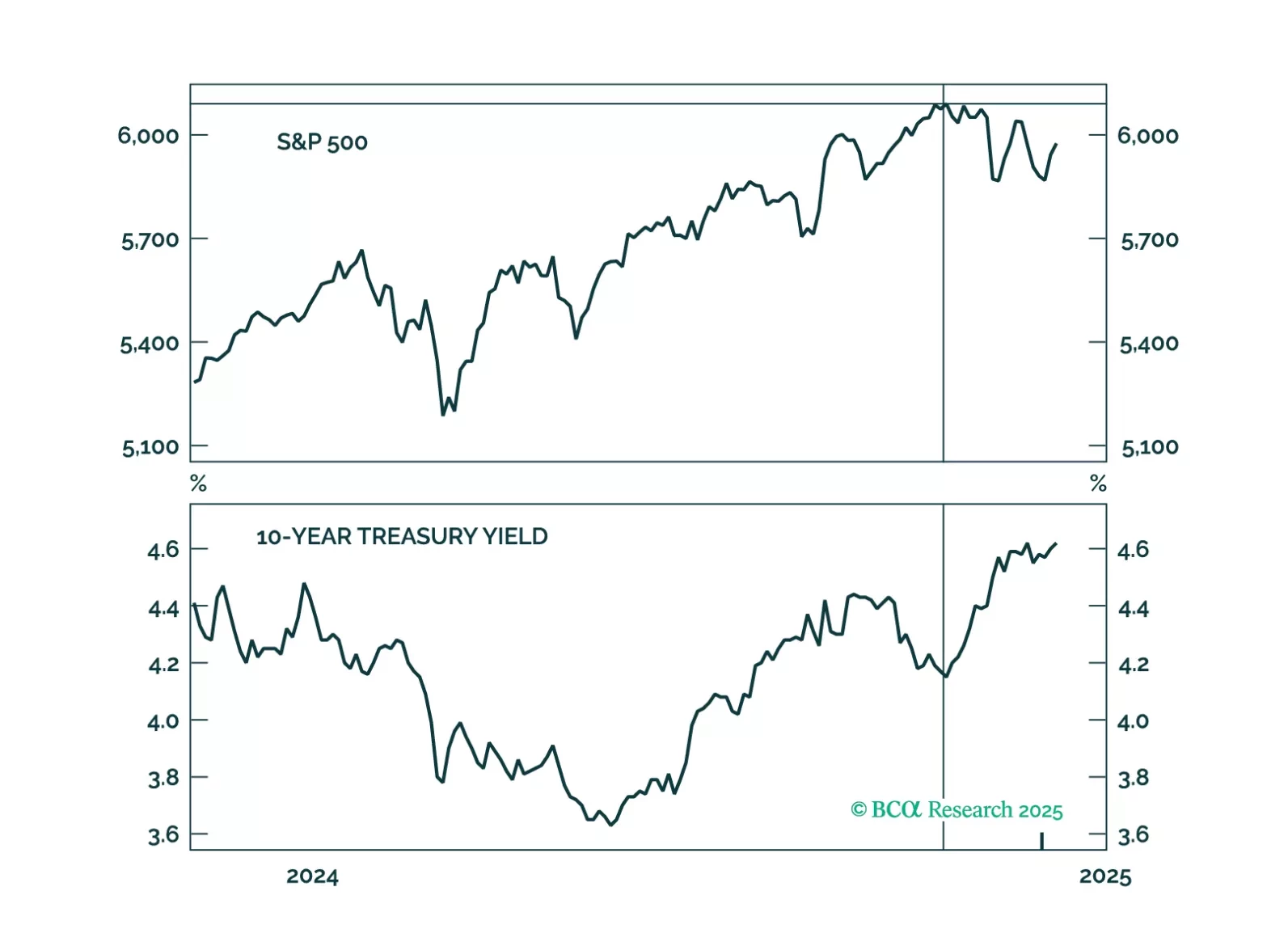

Our thoughts on this afternoon’s Fed decision and the bond market reaction.