Policy

Feature The U.S.-China trade talks have not yet collapsed but they appear to be reaching a “make it or break it” moment. President Donald Trump renewed his threat of heightening tariffs on Chinese imports on May 5, in the interim between two weeks of shuttle diplomacy in Beijing and next in Washington that have been billed as the final round of negotiations. Chinese officials responded to Trump’s new tariff remarks by threatening to pull out of the talks. The status of the Chinese delegation due in Washington this week is unclear as we go to press. Specifically, President Trump has claimed that he would increase the current 10% tariff rate on $200 billion worth of Chinese imports to 25%, a move that was originally due on March 1, but was delayed to extend the talks and seek a better agreement. Trump also threatened to raise tariffs on the remaining $325 billion of Chinese imports that are so far untouched. This is the most significant escalation in rhetoric since before the tariff truce agreed on December 1 between Trump and Chinese President Xi Jinping in Buenos Aires. True, the threat to increase the tariffs is a last-minute pressure tactic tied to the administration’s attempt to make this week “the final week” of the talks. American advisers have said that at the end of these two weeks they would make a recommendation to the president either to sign a deal or walk away. For this reason, it is not certain that Trump will follow through with the increase. However, we consider the threat credible. The costs of trade war are not prohibitive to the U.S. or China considering the strategic interests at stake in their great power competition (Chart 1). And since December 1, we have argued that a relapse into trade war and rising tariffs was a substantial risk at 30% odds; this threat increases those odds. Chart 1The Era Of U.S.-China Detente Is Over

The Era Of U.S.-China Detente Is Over

The Era Of U.S.-China Detente Is Over

Talks have been deteriorating for the past month at least. First, the trade grievances at the root of the trade war with China – namely corporate espionage, hacking, forced technology transfer, intellectual property theft, and the American-allied restrictions on Chinese telecoms firm Huawei – were always going to be extremely difficult to settle. These are apparently weighing on the ability of Washington and Beijing to close an agreement. Second, tensions have recently flared across the entire range of U.S.-China strategic disagreements, including most importantly North Korea and Iran. In late April, the U.S. demanded that China halt all imports of Iranian oil by the end of May in order to avoid secondary sanctions that, in theory, could affect China’s central bank and other banks. Meanwhile North Korea has conducted two minor but provocative weapon tests (including short-range missiles on May 4) since the failed summit between Trump and Kim Jong Un in Hanoi. Washington expects Beijing to keep North Korea in check and involved in diplomacy as part of the broader strategic negotiation. Taiwan and the South China Sea are also simmering due to U.S.-Taiwan diplomacy and arms sales, Chinese military drills, and the U.S. decision to treat China’s “maritime militia” like its navy. Trump’s latest threat reduces the chances of an extension of the talks beyond June to 10%, while raising the odds of a collapse in talks and escalation of trade war to 40%. As a result of these developments, and the dragging on of talks, we put the odds of a trade deal by the end of June at 50% in our April 10 report. Trump’s latest threat reduces the chances of an extension of the talks beyond June to 10%, while raising the odds of a collapse in talks and escalation of trade war to 40% (Table 1). Table 1Updated Trade War Probabilities (May 2019)

U.S. And China Get Cold Feet

U.S. And China Get Cold Feet

From the Chinese point of view, Trump’s threat makes it harder to clinch a deal. Trump’s use of sweeping, unilateral tariffs on national security grounds has forced China into an awkward position. It is politically and ideologically toxic for Beijing to appear to capitulate to coercion, i.e. nineteenth-century-style tactics of gunboat diplomacy and western imperialism. The tariff truce in Buenos Aires minimized the appearance that China is negotiating under duress, giving Xi Jinping the ability to negotiate and make concessions without losing face. While China is in the weaker position economically, and therefore would prefer a deal, it will batten down the hatches and fight a trade war if forced to do so. The risk of other executive decisions disruptive to markets is going up. The implication for investors is threefold. First, the USD and U.S. equities will continue to outperform global counterparts as trade policy uncertainty shoots back up (Chart 2). The American economy is more insulated from global trade and the dollar is counter-cyclical. But as U.S. equities have rallied and volatility will go up, U.S. equities may simply fall less rapidly than Chinese and others. Chart 2U.S. Will Outperform On Rising Trade Uncertainty

U.S. Will Outperform On Rising Trade Uncertainty

U.S. Will Outperform On Rising Trade Uncertainty

Second, our view that China’s economic stimulus will surprise to the upside is reinforced by this development, as Beijing cannot afford to withdraw or pause stimulus when it still faces such a severe external risk to its manufacturing sector and employment (Chart 3). This will counteract the negative impact to global sentiment and manufacturing expected from any additional tariffs, creating more volatility in commodity and emerging market assets. Third, as we recognized in the case of Trump’s renewed “maximum pressure” tactic on Iran, the president is apparently not concerned with minimizing risks to the economy ahead of the 2020 election. His risk appetite remains voracious. Therefore the risk of other executive decisions disruptive to markets is going up. For instance, our 35% chance that Trump will impose Section 232 tariffs on auto and auto part imports, particularly from Europe, is rising toward 50% (Chart 4). Chart 3China Cannot Afford to Withhold Stimulus

China Cannot Afford to Withhold Stimulus

China Cannot Afford to Withhold Stimulus

Chart 4

Bottom Line: The odds of a re-escalation of the trade war have risen to 40%. American equities should outperform global, while safe-haven assets, such as a portfolio hedge of Swiss bonds and gold, should catch a bid. We are closing out our long copper trade for a loss of 3.58% as well as our long Chinese equities ex-tech trade for a gain of 6.59%. Matt Gertken, Geopolitical Strategist mattg@bcaresearch.com

Highlights The business cycle has been extended, … : The expansion is nearly a year older than it was last summer, but the next recession could well be further away now than we estimated it was back then. … thanks to the Fed’s pause, … : Recessions only occur when monetary conditions are tight. The longer the Fed pauses its rate-hiking campaign, the longer the expansion will persist. … and the upshot is that the shelf life of our recommendations has been extended: Corporate earnings don’t meaningfully contract outside of recessions, so equities don’t typically enter bear markets, and bond defaults don’t typically spike, while the economy is expanding. Stay the course until monetary policy is on the way to turning restrictive: The Fed’s pause is risk-asset-friendly, and investors should continue to prioritize the return on their capital. Focusing on return of capital can wait until monetary policy turns hawkish. Feature Late last July, we began outlining our positions on the key macro drivers of financial markets: rates, credit, the business cycle, and the state of monetary policy. Laying out our big-picture views, and the rationale underpinning them, provides us with a framework for evaluating incoming data and adjusting asset-allocation strategy as necessary. Nine months on, our macro views are very nearly unchanged, and we expect they will remain so for the rest of the year. That would have come as a surprise to us last summer, when we anticipated that 2019 might finally bring the macro inflection points that would dictate de-risking portfolios to preserve capital ahead of the next bear market. The Fed’s pause has been the key to extending the shelf life of our views. We continue to expect that the transition from accommodative to restrictive monetary policy will be the catalyst for the inflection points that investors most care about: the end of the expansion, the end of the equity bull market, and the point at which spread product ceases to generate positive excess returns over Treasuries. By abandoning the gradual normalization pace it maintained throughout 2017 and 2018, the Fed has postponed its crossing of the neutral-rate Rubicon. That postponement has indefinitely extended the expansion, and the credit and equity bull markets in turn. There is no free lunch, however. Unless low rates for even longer shift the economy’s potential long-run growth rate higher, they will only pull future investment gains forward into the present. In other words, we expect the Fed’s pause will allow risk assets to reach higher cyclical peaks than they otherwise would at the cost of suffering larger declines once restrictive monetary policy settings are ultimately imposed. Barring an exogenous shock that causes a recession or some sort of financial-market scare, we expect robust investment returns, possibly crowned by an incremental melt-up in equities. The longer the Fed delays removing monetary accommodation, the longer the expansion, and the equity bull market, will continue. Our base case, then, is to stay the course with risk-friendly positioning, maintaining at least an equal weight in equities and spread product. We are expending much of our research energy on weighing the challenges to our constructive view. We are particularly focused on signs that the nine rate hikes the Fed has already executed might be slowing the economy, that the economy is at risk of overheating, or that investor euphoria constrains future returns. This week’s report considers the current backdrop on all three counts. Has The Fed Already Squeezed The Economy? At first blush, the first quarter’s real 3.2% growth would seem to do in the notion that the Fed has already reined in the economy. Alas, there was much less to the GDP release than meets the eye, as it was goosed by a 100-basis-point (“bps”) contribution from net exports and a 65-bps contribution from inventory restocking (Chart 1). Real final domestic demand grew by only 1.5%. Measured against 2018’s 3% growth in real final domestic demand, and 2.5% and 2.4% in 2017 and 2016, respectively, the first quarter represented a noticeable slowdown. Given the 40-bps decline in fiscal thrust from 2018 to 2019 (Chart 2), some growth deceleration is inevitable this year. Thanks to a projected 40 bps of fiscal stimulus, we expect that growth will still exceed the economy’s long-run approximate 2% potential growth rate. We are undeterred by the first quarter’s underlying weakness, though, because the economy is not likely to face such daunting challenges again this year. The first quarter began on the heels of a sudden 19% peak-to-trough decline in the S&P 500 that shaved nearly $4 trillion from household wealth; a similar blowout in credit spreads spooked would-be home buyers and must have made some business borrowers table their investment plans. Chart 1Much Less Than Meets The Eye

Much Less Than Meets The Eye

Much Less Than Meets The Eye

Chart 2Fiscal Policy Is Still Easy

Fiscal Policy Is Still Easy

Fiscal Policy Is Still Easy

The quarter also began in the midst of the 35-day federal government shutdown that lasted nearly all of January. Furloughed government employees would eventually receive back pay for the days they were involuntarily idle, but many had no choice but to curtail spending until they did, causing ripple effects in communities with high concentrations of federal employees. The White House Council of Economic Advisers estimated that the shutdown trimmed 10 basis points a week from GDP. We presented the high-level outlook for GDP growth a month ago, with particular emphasis on the consumption outlook.1 Our constructive consumption view is a function of the surging labor market’s impact on household incomes and the post-crisis shoring up of household balance sheets. Consumer confidence has declined from its cyclical peak, but it remains elevated relative to history, and the expectations component has historically marched in lockstep with consumption (Chart 3). The two series have diverged over the last few years, perhaps because of a desire to shore up balance sheets, but consumer confidence remains elevated, and is positioned to support spending in much the same way as bulked-up household balance sheets (Chart 4). Chart 3Ample Confidence Leaves Plenty Of Room For More Spending

Ample Confidence Leaves Plenty Of Room For More Spending

Ample Confidence Leaves Plenty Of Room For More Spending

Solid consumption should bolster nonresidential investment, and survey data suggest that it is not about to roll over in any event (Chart 5). Residential investment has exerted a modest drag on GDP for seven of the last eight quarters, but homes remain quite affordable relative to history, and we still see the single-family housing market as undersupplied. Our GDP outlook showed that the state and local component of government spending should be well supported by growing household incomes, and ventured that it’s hard to see how federal spending will slip in a presidential election year. Last week’s preliminary bipartisan discussions about a $2 trillion infrastructure-spending plan would seem to ensure that it won’t. Chart 4Consumption Fundamentals Are Solid ...

Consumption Fundamentals Are Solid ...

Consumption Fundamentals Are Solid ...

Chart 5... Which Bodes Well For Capex

... Which Bodes Well For Capex

... Which Bodes Well For Capex

Are There Signs That The Economy Could Overheat? With its pause, the Fed has indicated that it sees little near-term risk of economic overheating. The available data support that conclusion. Even after a steady multi-year recovery, cyclical spending as a share of GDP is only around its long-run average level (Chart 6, top panel). The three components of cyclical spending that are prone to harmful inventory overhangs – consumer durables (Chart 6, second panel), commercial real estate (Chart 6, fourth panel), and residential real estate (Chart 6, bottom panel) – are all at fairly low levels relative to history. Only equipment and intellectual property is elevated (Chart 6, third panel), but the bulk of its growth is attributable to investment in software and R&D, neither of which carries the same fraught inventory implications as the tangible-good components. One silver lining of the tepid expansion is that it hasn’t ever revved up the engine enough to overheat. Chart 6Cyclical Spending Is Well Below Past Peaks

Cyclical Spending Is Well Below Past Peaks

Cyclical Spending Is Well Below Past Peaks

Chart 7Inventories Are Elevated ...

Inventories Are Elevated ...

Inventories Are Elevated ...

The wholesale inventory-to-sales ratio is elevated (Chart 7), and registers as a yellow light. The labor market is running hot, and we believe it will eventually force the Fed to resume tightening policy, but probably not in any meaningful way until 2020. Injecting a substantial amount of stimulus into an economy already operating at capacity is a textbook recipe for inflation, but inflation is a lagging indicator and the steep decline in oil prices has held back headline price measures. The bottom line is that the aggregate macro data do not suggest that the U.S. economy is in any immediate danger of overheating. Are Investors Too Optimistic? Investor sentiment is properly viewed as a contrarian indicator. When investors are depressed, equity multiples are low and forward earnings expectations are restrained. When they’re euphoric, equity multiples are high and forward earnings expectations are ambitious. The multiple/expectations interaction makes for juicy prospective returns when sentiment is washed out, and stingy prospective returns when sentiment is ebullient. Chart 8... But Sentiment Is Not

... But Sentiment Is Not

... But Sentiment Is Not

Barron’s semi-annual Big Money poll of money managers, published in its April 29th edition, suggests that sentiment is nowhere near either extreme, though its respondents are less constructive on equities and the economy than we are. Fewer than half of money managers are bullish on equities over the next twelve months for the first time since 2016, and more of their clients are bearish than bullish. The bullish managers’ expectations were modest; they saw the S&P 500 gaining just over 4% by year-end, and another 3% in the first half of 2020.2 The Barron’s data aligns with other sentiment surveys: individual investor bullishness is below its historical mean (Chart 8, second panel), while advisor optimism is about a standard deviation above its average (Chart 8, third panel), and trader sentiment is slightly bullish (Chart 8, bottom panel). Recession fears continue to dog the markets. Economic slowdown or recession was the most common concern (28%), followed by earnings disappointments (21%) and Fed missteps (13%), meaning that almost two-thirds of investors are concerned about the business cycle and the possibility that the Fed might short-circuit it. One-half of respondents expect a recession to arrive by the end of next year. Their sector calls didn’t reflect a strong cyclicals/defensives bias, though they are avoiding bond proxies like REITs and Utilities, and the majority of respondents expect the 10-year Treasury to yield 3% or more a year from now. Investment Implications The U.S. economy is faring well, but continued above-trend growth is not assured. First quarter GDP was inflated by a one-off boost from net exports and inventory restocking that is not likely to be repeated. A robust labor market should support consumption, but wholesale inventories are high, and retail sales have been making large swings from month to month. We believe that Chinese policymakers have tabled their deleveraging campaign, helping the Chinese economy to rebound and pull the rest of the world along with it, but it is too early to say for certain that ex-U.S. growth has turned around. The uncertain global growth outlook provides stocks with a wall of worry, and the Fed is poised to help them climb it. The upshot is that conditions remain somewhat uncertain. That augurs well for equities and other risk assets because it will allow them to climb a wall of worry. Meanwhile, our base case scenario is that the economy will move forward at a Goldilocks pace. The neither-too-hot-nor-too-cold economy will allow the Fed to continue to be patient and refrain from hiking rates for most, if not all, of the rest of the year. While the Fed stays on hold, risk assets should find the going pretty smooth. We expect that the pause will have the effect of extending the expansion, along with the bull markets in equity and credit. We continue to believe that the Fed’s patience now will beget more aggressive tightening later. Since that tightening will bite after stocks have run up to higher levels than they would otherwise have reached, and spreads are tighter than they would otherwise have gotten, the offsetting bear-market declines will be worse. The ensuing declines are concerns for late 2020 or early 2021, however, and it is too early for investors to prepare their portfolios for them. We continue to recommend that investors remain at least equal weight equities and spread product in balanced portfolios. Doug Peta, CFA Chief U.S. Investment Strategist dougp@bcaresearch.com Footnotes 1 Please see U.S. Investment Strategy Weekly Report, “If We Were Wrong,” published April 8, 2019. Available at usis.bcaresearch.com. 2 The survey was sent to respondents in late March. The S&P 500’s average close over the last two weeks of March was 2,823, and the survey’s bulls’ year-end and mid-2020 targets were 2,946 and 3,044, respectively.

Highlights Recent data suggest central bankers remain behind the curve in boosting inflation expectations. Ergo, expect a dovish bias to persist over the next few months. Our thesis remains that global growth is in a volatile bottoming process. However, market focus could temporarily flip towards short term data weakness, which warrants taking out some insurance. Meanwhile, in an environment where volatility is low and falling, it also pays to have insurance in place. Rising net short positioning in the yen and Swiss franc is making them attractive from a contrarian standpoint. Maintain a limit-buy on CHF/NZD at 1.45. The path of least resistance for the dollar remains down. This is confirmed by incoming data that suggests the euro area economies have bottomed, which should boost the EUR/USD. The rising dollar shortage remains a key risk to our sanguine view. But the forces driving dollar liquidity lower are largely behind us. Feature Investors looking for more clarity on the global growth picture from the April data print have been left in a quandary. In the U.S., the headline first-quarter real GDP growth number of 3.2% was well above consensus but was boosted by volatile components such as inventories and net exports. Real final sales to domestic purchasers, a cleaner print for final demand, came in at 1.5%, the lowest increase since 2015. Assuming trend growth in the U.S. is around 2%, a view shared by the Federal Open Market Committee (FOMC), then the increase in first-quarter final sales was a big miss. Most importantly, the U.S. ISM manufacturing index fell to 52.8 in April, a drop that was broad-based across seven of the 10 components. Chart I-1At The Cusp Of A V-Shaped Recovery?

At The Cusp Of A V-Shaped Recovery?

At The Cusp Of A V-Shaped Recovery?

Across the ocean, European growth was a tad stronger. Italy managed to nudge itself out of a technical recession, while Spanish year-on-year growth of 2.4% helped drive euro area GDP growth to the tune of 1.2%. The most volatile components of euro area growth tend to be investment and net exports. Should both pick up on the back of stronger external demand, then GDP could easily gravitate towards 1.5%-2%, pinning it well above potential. The German PMI is currently one of the weakest in the euro zone. But forward-looking indicators suggest we are at the cusp of a V-shaped bottom over the next month or so (Chart I-1). China remains the epicenter of any growth pickup and the headline PMI numbers were soft, with the official NBS manufacturing PMI falling to 50.1 from 50.5, and the private sector Caixin manufacturing PMI falling to 50.2 from 50.8. Still, the numbers remain above the critical 50 threshold level, and well beyond the 45-48 danger zone. Export growth numbers across southeast Asia remain weak, and after a brisk rise since the start of the year, many China plays including commodity prices, the yuan, emerging market stocks, and Asian currencies are all rolling over. The bearish view is that there are diminishing marginal returns to Chinese stimulus, and the authorities need to be more aggressive to turn the domestic economy around. The reality is that policy stimulus works with a lag, and we need about three to six months before we see the effects of the current policy shift. Southeast Asian exports track the Chinese credit impulse with a lag of six months, and there is little reason to believe this time should be different (Chart I-2). Chart I-2Global Trade Should Soon Bottom

Global Trade Should Soon Bottom

Global Trade Should Soon Bottom

The broad message is that global growth likely bottomed in the first quarter. However, before evidence of this fully unfolds, markets are likely to be swayed by the ebbs and flows of higher-frequency data, making for a volatile bottoming process. We recommend maintaining a pro-cyclical bias, but taking out some insurance against a potential spike in volatility. The Fed On Hold This week’s FOMC meeting focused on the lack of inflationary pressures in the U.S. but was largely a non-event for financial markets, aside from a spike in volatility. Nonetheless, there were three key takeaways. First, the dip in inflation appears to be “transitory,” driven by lower clothing prices and financial services fees. Second, Chair Powell made it clear that the Fed will only feel the need to ease policy if inflation runs “persistently” below target. Finally, the Fed’s interpretation of its “symmetric” inflation target is slowly shifting. Many FOMC members increasingly believe that the Fed should explicitly pursue an overshoot of its 2% inflation target to make up for past misses. Taken together, we expect the Fed to remain on hold for the time being, but to eventually start raising rates again as inflationary pressures pick up. Chart I-3Inflation Should Be Higher In The U.S. Versus The Euro Area

Inflation Should Be Higher In The U.S. Versus The Euro Area

Inflation Should Be Higher In The U.S. Versus The Euro Area

The bigger picture is that in a very globalized world with fully flexible exchange rates, it is becoming more and more difficult for any one central bank to independently achieve its inflation objective. This is because, should inflation be on the rise and moving higher in one country, expectations of higher interest rates should lift its currency, which eventually tempers inflationary pressures, and vice versa. This is obviously a very simplistic view of the world economy, since other factors such as demographics, productivity, labor mobility, openness of the economy, and policy divergences among others, play important roles. However, it is remarkable that almost every developed market central bank has continued to attempt to boost inflation to the 2% level since the Global Financial Crisis, but very few have been able to achieve this independently. In a very globalized world with fully flexible exchange rates, it is becoming more and more difficult for any one central bank to independently achieve its inflation objective. Take the case of Europe versus the U.S., two economies that could not be more different. Euro area imports constitute about 41% of GDP, while the number in the U.S. is only 15%, so tradeable prices matter a lot more for the former. Meanwhile, the demographic profile is worse in Europe, with the old-age dependency ratio at 32% in Europe versus 23% in the U.S. Finally, other measures of supply-side constraints such as labor market slack or capacity utilization suggest the euro area is well behind the U.S. on the path toward a closed output gap (Chart I-3). Despite this, since 2015, headline inflation in both the U.S. and euro area have moved tick-for-tick. Yes, policy divergences between the two countries have been very wide, either via the lens of quantitative easing or simply the differential in policy rates (Chart I-4). But the fact that the magnitude and direction of overall inflation has moved homogenously, begs the question of the ability of either central bank to influence overall prices. One explanation could be that variations in headline CPI are largely driven by volatile items that tend to be exogenous, while variations in core CPI tend to be mostly driven by endogenous factors. This is confirmed by most research that suggest there is a weak link between rising commodity prices and longer-term inflation.1 That said, over the shorter run, commodity price gyrations can dominate and be the main driver of inflation expectations (Chart I-5). Chart I-4U.S. And Euro Area Overall CPI Are Broadly Similar

U.S. And Euro Area Overall CPI Are Broadly Similar

U.S. And Euro Area Overall CPI Are Broadly Similar

Chart I-5In The Short Term, Commodity Prices Matter For Inflation Expectations

In The Short Term, Commodity Prices Matter For Inflation Expectations

In The Short Term, Commodity Prices Matter For Inflation Expectations

The bottom line is that muted inflationary pressures are a global phenomenon, and not centric to the U.S. This means that as a whole, global central banks are set to stay accommodative for the time being, which will be bullish for global growth (Chart I-6). This warrants maintaining a pro-cyclical stance but being extremely selective in what might be a volatile bottoming process. Chart I-6Global Monetary Policy Needs To Ease Further

bca.fes_wr_2019_05_03_s1_c6

bca.fes_wr_2019_05_03_s1_c6

Maintain A Pro-Cyclical Stance With the S&P 500 breaking to all-time highs, crude oil prices up around 40% from their lows, and U.S. 10-year Treasury yields rolling over relative to the rest of the world, this has historically been fertile ground for high-beta currency trades. That said, the lack of more pronounced strength in pro-cyclical currencies like the Australian, New Zealand, and Canadian dollars suggest that caution prevails. Our bias is that currency markets continue to fight a tug-of-war between strong dollar fundamentals and fading tailwinds. Our portfolio consists mostly of trades along the crosses, but we have been cautiously adding to U.S. dollar short positions over the past few weeks: Long AUD/USD: Our limit-buy on the Aussie was triggered at 0.70. Data out of Australia are showing tentative signs of a bottom. Last week’s important jobs report showed that the economy continues to offer more employment than the consensus expects. Meanwhile, the credit growth data out of Australia this week suggests that macro-prudential policies continue to drive a wedge between owner-occupied and investor housing (Chart I-7). House prices in Australia are already deflating to the tune of around 6%. Once the cleansing process is through, we expect house price growth to eventually converge toward levels of credit and/or natural income growth. Moreover, the Australian dollar remains a commodity currency, and will benefit from rising terms-of-trade. Iron ore prices remain firm on the back of supply-related issues. Meanwhile, a rising mix of liquefied natural gas in the export basket will provide tailwinds as China continues to steer its economy away from coal. Finally, Chinese credit growth has been a key determinant of the re-rating of Australian equities. Ergo, a rising Chinese credit impulse will ignite Australian share prices, and by extension the Australian dollar (Chart I-8). Chart I-7Australian Credit Growth Converging To Steady State

Australian Credit Growth Converging To Steady State

Australian Credit Growth Converging To Steady State

Chart I-8More Chinese Credit Will Help Australian Equities

More Chinese Credit Will Help Australian Equities

More Chinese Credit Will Help Australian Equities

Long GBP/USD: Our buy-limit order on the British pound was triggered at 1.30 on March 29th. As we argued back then, the pound is sitting exactly where it was after the 2016 referendum results, but the odds of a hard Brexit have significantly fallen since then. On the domestic front, economic surprises in the U.K. relative to both the U.S. and euro area continue to soar. The reality is that the pound and U.K. gilt yields should be much higher – solely on the basis of hard incoming data. Employment growth has been holding up very well, wages are inflecting higher, and the average U.K. consumer appears in decent shape. Full-time employees continue to creep higher as a percentage of overall employment (Chart I-9). This view was echoed in yesterday’s Bank Of England (BoE) policy meeting, where the central bank raised its growth forecast while striking a more hawkish tone. Chart I-9U.K.: What Brexit?

U.K.: What Brexit?

U.K.: What Brexit?

Chart I-10Sweden: Volatile Bottom

Sweden: Volatile Bottom

Sweden: Volatile Bottom

Long SEK/USD: The Swedish krona should be one of the first currencies to benefit from any bottoming in European growth (Chart I-10). The Swedish economy appears to have bottomed relative to that of the U.S., making the USD/SEK an attractive way to play USD downside. From a technical perspective, the cross is trading at its lowest level since the global financial crisis (Chart I-11). Economic surprises in the U.K. relative to both the U.S. and euro area continue to soar. The main appeal of the Swedish krona is that it is extremely cheap. Meanwhile, despite negative interest rates, Swedish household loan growth has been slowing as consumers are increasingly financing purchases through rising wages. This will alleviate the need for the Riksbank to maintain ultra-accommodative policy, despite its recent dovish shift. Buy Some Insurance Given current low levels of volatility and elevated equity market valuations, the dollar would have been a great insurance policy for any stock market correction. But with U.S. interest rates having risen significantly versus almost all G10 countries in recent years, the dollar has itself become the object of carry trades. This has also come with a good number of unhedged trades, as the rising exchange rate has lifted hedging costs. Chart I-11How Much Lower Could The Swedish Krona Go?

How Much Lower Could The Swedish Krona Go?

How Much Lower Could The Swedish Krona Go?

Chart I-12Buy Some##br## Insurance

Buy Some Insurance

Buy Some Insurance

It will be difficult for the dollar to act as both a safe-haven and carry currency, because the forces that drive both move in opposite directions. As markets become volatile and some carry trades are unwound, unhedged trades will become victim to short-covering flows. Currencies such as the Japanese yen and the Swiss franc that could have been used to fund carry trades are ripe for reversals. This suggests at a minimum building some portfolio hedges. One such hedge is going long the CHF/NZD. This trade has a high negative carry, so we do not intend to hold it for longer than three months. But it should pay off handsomely on any rise in volatility (Chart I-12). Maintain a limit-buy at 1.45. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Stephen G Cecchetti and Richhild Moessner, “Commodity Prices And Inflation Dynamics,” Bank Of International Settlements, Quarterly Review, (December 2008). Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. continue to moderate: Annualized Q1 GDP came in at 3.2% quarter-on-quarter, well above estimates. Personal income increased by 0.1% month-on-month in March, below the estimated 0.4%. On the other hand, personal spending increased by 0.9% month-on-month in March. PCE deflator and core PCE deflator fell to 1.5% and 1.6% year-on-year, respectively in March. Michigan consumer sentiment index slightly increased to 97.2 in April. Markit manufacturing PMI increased from 52.4 to 52.6 in April, while ISM manufacturing PMI fell to 52.8. Q1 nonfarm productivity increased by 3.6%, surprising to the upside. DXY index fell by 0.3% this week. On Wednesday, the Fed announced their decision to keep interest rates on hold at current levels, further suggesting that there is no strong case to move rates in either direction based on recent economic developments. Moreover, Fed chair Powell reiterated their strong commitment to the 2% inflation target. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 Beware Of Diminishing Marginal Returns- April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area are improving: Money supply (M3) in the euro area increased by 4.5% year-on-year in March. The sentiment in the euro area remains soft in April: economic sentiment indicator fell to 104; business climate fell to 0.42; industrial confidence fell to -4.1; consumer confidence was unchanged at -7.9. Q1 GDP came in at 1.2% year-on-year, surprising to the upside. Unemployment rate fell to 7.7% in March. Markit PMI increased to 47.9 in April. EUR/USD appreciated by 0.3% this week. European data keep grinding higher. Italian GDP moved back into positive territory in Q1. Spanish GDP also rebounded in Q1. Positive Chinese credit data suggests the euro will soon benefit from rising Chinese imports. Report Links: Reading The Tea Leaves From China - April 12, 2019 Into A Transition Phase - March 8, 2019 A Contrarian Bet On The Euro - March 1, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been positive: The unemployment rate in March increased slightly to 2.5%; job-to-applicant ratio was unchanged at 1.63. Tokyo consumer price inflation increased to 1.4% year-on-year in March, the highest level since October 2018. Industrial production fell by 4.6% year-on-year in March. However, projections for April suggest a 2.7% month-on-month jump. Retail sales grew by 1% year-on-year in March, higher than expected. Housing starts grew by 10% year-on-year in March. This is the highest growth level since February 2017. USD/JPY fell by 0.2% this week. The Japanese government’s intention to raise sales tax this October could be a highly deflationary outcome. However, there is still an outside chance that the tax hike will be postponed. We continue to recommend yen as a safety hedge. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 A Trader’s Guide To The Yen - March 15, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been positive: U.K. mortgage loans in March increased to 40K. Nationwide housing prices increased by 0.9% on a year-on-year basis in April. Markit manufacturing PMI came in above expectations at 53.1 in April, even though it fell; Markit construction PMI however increased to 50.5. Money supply (M4) increased by 2.2% year-on-year in March. GBP/USD increased by 1% this week. The Bank of England kept rates on hold at 0.75% this week. In the May inflation report, the BoE mentioned that U.K.’s economic outlook will depend significantly on the nature and timing of EU withdrawal, and the new trading agreement with EU in particular. But governor Carney struck a slightly hawkish tone, revising up GDP estimates and guiding the next policy move as a rate hike. Report Links: Not Out Of The Woods Yet - April 5, 2019 A Trader’s Guide To The Yen - March 15, 2019 Balance Of Payments Across The G10 - February 15, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have shown tentative signs of recovery: Private sector credit growth fell to 3.9% year-on-year in March. However, this is heavily biased downwards by lending to home investors that has slowed to a crawl. The Australian Industry Group (AiG) manufacturing index increased to 54.8 in April. RBA commodity index increased by 14.4% year-on-year in April. AUD/USD fell by 0.4% this week. The data are starting to look brighter in Q2, suggesting that the economy might have bottomed in Q1. The Australian dollar is likely to grind higher, especially driven by rising terms of trade. Report Links: Beware Of Diminishing Marginal Returns- April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 Into A Transition Phase - March 8, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand are mixed: ANZ activity outlook increased by 7.1% in April. ANZ business confidence in April improved to -37.5. On the labor market front in Q1, the employment change fell to 1.5% year-on-year; unemployment rate was unchanged at 4.2%, but participation rate fell to 70.4%; labor cost index fell to 2% year-on-year. Building permits contracted by 6.9% month-on-month in March. NZD/USD depreciated by 0.4% this week. The data from New Zealand continue to underperform its antipodean neighbor. We anticipate this trend will persist. Stay long AUD/NZD, currently 0.5% in the money. Report Links: Not Out Of The Woods Yet - April 5, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada continue to underperform: GDP in February contracted by 0.1% on a month-on-month basis. Markit manufacturing PMI fell below 50 to 49.7 in April. USD/CAD fell by 0.1% this week. During Tuesday’s speech, Governor Poloz acknowledged recent negative developments in the Canadian economy, and blamed it on the U.S.-led trade war, as well as the sharp decline in oil prices late last year. While a bottoming in the global growth could be a tailwind for the Canadian economy near-term, a Ricardian equivalence framework will suggest fiscal austerity over the next few years, will be a headwind for long-term CAD investors. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Into A Transition Phase - March 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been negative: KOF leading indicator fell to 96.2 in April. Real retail sales contracted by 0.7% year-on-year in March. SVME PMI fell below 50 to 48.5 in April. USD/CHF fell by 0.1% this week. The reduced volatility worldwide could make the Swiss franc less attractive. Moreover, the relative outperformance of the euro area is a headwind for the franc. Our long EUR/CHF position is now 1% in the money. We intend to trade the franc purely as an insurance policy near-term. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway has been positive: Retail sales increased by 0.6% in March, in line with expectations. This was a marked improvement from the 1.2% drop in February. The unemployment rate held low at 3.8% USD/NOK increased by 1% this week. We expect the Norwegian krone to pick up based on the strong fundamentals and positive oil price outlook. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Balance Of Payments Across The G10 - February 15, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been mostly positive: Retail sales increased on a month-on-month basis by 0.5% in March, but fell to 1.9% on a yearly basis. Producer price index was unchanged at 6.3% year-on-year in March. Trade balance came in at a large surplus of 7 billion SEK in March. Manufacturing PMI fell to 50.9 in April, but notably, import orders and backlog orders rose. USD/SEK increased by 0.4% this week. Despite the RiksBank’s dovish shift last week, we continue to favor our long SEK position. Our conviction is rooted in the fact that the Swedish krona is undervalued, and relative PMI trends favor Sweden vis-à-vis the U.S. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

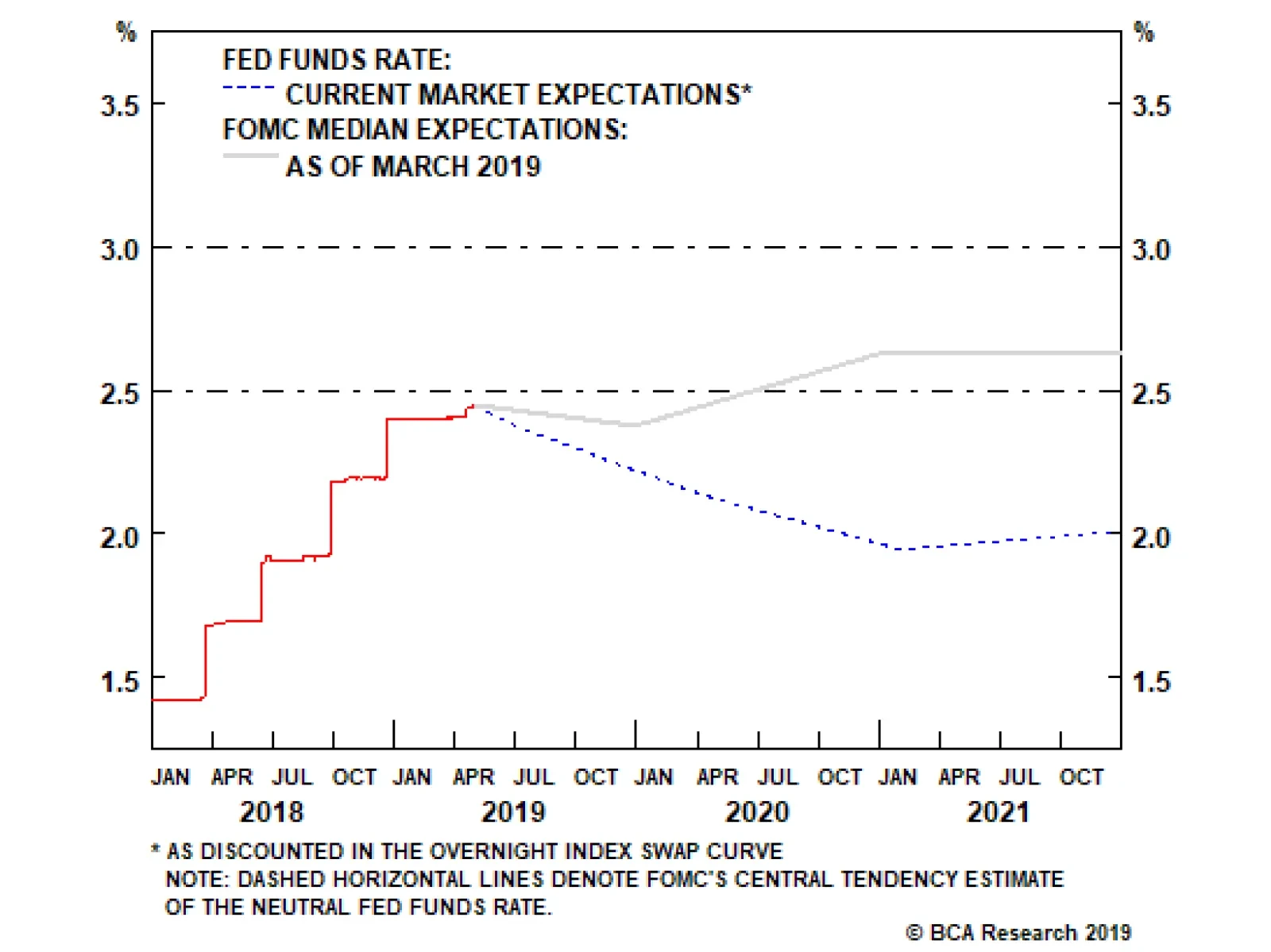

Highlights This week’s FOMC meeting confirmed that the Fed is on hold. We would downplay Powell’s reference to the decline in inflation as being “transitory”. Strictly speaking, he is correct. All of the decline in core inflation since last September has occurred in just two categories: financial services and clothing/footwear. The bigger point is that the Fed no longer sees fit to raise rates even though the unemployment rate is at a 50-year low and real rates are barely positive. Both the Fed and the markets have completely bought into two of Larry Summers’ core views, which are that the neutral rate of interest is much lower today than in the past, and that the Fed should wait to see the “whites of inflation’s eyes” before raising rates any further. We think the neutral rate will prove to be higher than widely believed and that the Fed will eventually find itself far behind the curve. Risk assets may see heightened volatility over the next few days as markets adjust to the fact that rate cuts are not forthcoming. Nevertheless, with rates still far below our estimate of neutral, the path of least resistance for global equities remains to the upside. The bull market in stocks will only end when inflation moves significantly higher, requiring the Fed to hike rates aggressively. That is unlikely to happen during the next 12 months. Feature Gentle Jay Ruffles The Markets … Transitorily This week’s FOMC statement confirmed that the Fed is on hold. In sharp contrast to his claim last October that rates were “a long way from neutral,” Chair Powell stressed during his press conference that there was no strong case for moving rates in “either direction.” Equities initially rose, while the dollar weakened, only to reverse direction following Powell’s subsequent comment that the recent decline in inflation was “transitory.” We would not make a big deal of Powell’s “transitory” remark. As a factual matter, he is correct. Table 1 shows that almost all of the decline in core PCE inflation from 2% in September 2018 to 1.6% in March 2019 can be explained by a drop in inflation in two categories: financial services and clothing/footwear. The former was weighed down by the steep decline in equity prices late last year (Chart 1). The latter was affected by a methodological change in how the Bureau of Labor Statistics calculates apparel prices.1 Table 1Weaker Core PCE Inflation Driven Mainly By Financial Services

Larry Summers: Shadow Fed Chair

Larry Summers: Shadow Fed Chair

Chart 1Stock Market Swings Feed Into Price Indices

Stock Market Swings Feed Into Price Indices

Stock Market Swings Feed Into Price Indices

The more important takeaway is that the Fed is now in a “wait and see” mode. Considering that the unemployment rate is at a 50-year low and real rates are barely positive, this is an extraordinary development. How to explain it? Two words: Larry Summers. Everyone Loves Larry Six years after President Obama dashed Larry Summers’ hopes of becoming the next Fed chair by anointing Janet Yellen instead, the former Treasury Secretary’s shadow hangs over the central bank like never before. Two of Summers’ key views – that the neutral rate of interest is much lower today than in the past, and that the Fed should wait to see the “whites of inflation’s eyes” before raising rates any further – have become accepted wisdom not just at the Fed, but on Wall Street as well. At the same time, another of Larry Summers’ core beliefs, that the Fed should aim for an inflation rate above the current target of 2%, is gaining traction. This raises an important question: What would it mean for investors if all these hypotheses turned out to be wrong? Let’s examine the arguments. How Low Is The Neutral Rate Of Interest? Conceptually, the interest rate on safe government securities should adjust to ensure that global savings equal investment. Interest rates will fall if either desired savings rise or desired investment declines (Chart 2). To the extent that some countries have more savings and/or fewer worthwhile domestic investment opportunities than others, they will run current account surpluses. Countries with less savings and better investment prospects will run current account deficits (Chart 3).

Chart 2

Chart 3

There is a strong case to be made that the neutral rate of interest has fallen over the past few decades. Potential GDP growth in developed economies has slowed. This has reduced the need for new capital investment. The advent of the digital age, or the “demassification” of the economy as Summers calls it, has also brought down the amount of physical capital firms need to function. Meanwhile, China’s entry into the global economy greatly expanded productive capacity without a concomitant increase in spending, thus creating the “savings glut” that Ben Bernanke first described in 2005. The question is how will these forces evolve over the coming years? According to the standard “accelerator” model, the optimal level of investment spending is determined by the growth rate of aggregate demand.2 As Chart 4 illustrates, most of the decline in trend real GDP growth in developed economies occurred between 1960 and 2000. Growth may decelerate further over the next decade, but not by much.

Chart 4

Chart 5Dependency Rates Are Rising Again In Developed Economies

Dependency Rates Are Rising Again In Developed Economies

Dependency Rates Are Rising Again In Developed Economies

Investment growth in China is likely to slow, but savings could also decline as a more robust consumer culture emerges and the government continues to take steps to strengthen the social safety net. Population aging in China and elsewhere could also erode savings. Falling fertility rates in most of the world starting in the early 1960s led to a decline in dependency rates in the 1980s and 1990s (Chart 5). However, now that baby boomers are starting to retire, dependency rates are rising. Once health care spending is included, consumption increases in old age, especially in the last few years of life (Chart 6). Globally, the ratio of workers-to-consumers peaked earlier this decade. The pace of the decline in this ratio is set to accelerate over the next few decades (Chart 7). More desired consumption relative to any given level of production implies less savings and a higher neutral rate of interest. Chart 6Savings Over The Life Cycle

Savings Over The Life Cycle

Savings Over The Life Cycle

Chart 7The Worker-To-Consumer Ratio Has Peaked Globally

The Worker-To-Consumer Ratio Has Peaked Globally

The Worker-To-Consumer Ratio Has Peaked Globally

Even in Japan, the neutral rate may be stealthily moving higher (Chart 8). Despite an influx of women into the labor market, the household savings rate has fallen from nearly 20% in the early 1980s to around 4% of late. The ratio of job openings-to-applicants has risen to a 45-year high. The trade balance has moved into deficit. Yet, 20-year inflation swaps are trading at 0.3%, implying that investors do not expect the Bank of Japan to achieve its 2% inflation target anytime soon. They may be in for a big surprise. Gauging The Cyclical Drivers Of The Neutral Rate At its core, the secular stagnation thesis is a theory about the long-term determinants of interest rates. It says little about the appropriate level of interest rates over cyclical horizons of a few years, even though that is the period over which monetary policy decisions tend to affect the economy. Today, aggregate demand in the United States is being buoyed by a number of cyclical forces. These include very loose fiscal policy, fairly strong credit growth (especially among corporates), high levels of asset prices, and faster wage growth at the bottom of the income distribution (Chart 9). All of these forces are helping to lift the neutral rate of interest. Chart 8Japan May Be Slowly Moving Towards Higher Inflation

Japan May Be Slowly Moving Towards Higher Inflation

Japan May Be Slowly Moving Towards Higher Inflation

Chart 9U.S.: Cyclical Forces Are Propping Up Demand

U.S.: Cyclical Forces Are Propping Up Demand

U.S.: Cyclical Forces Are Propping Up Demand

Consider the impact of looser fiscal policy. The IMF estimates that the U.S. structural budget deficit averaged 3.2% of GDP in 2015. In 2019, the IMF reckons it will average 5.2% of GDP. The budget deficit could rise further if Trump and Congress succeed in negotiating a new infrastructure package or if, as is likely, the Democrats insist on new spending measures as a condition for increasing the debt ceiling later this year. For the sake of argument, let us suppose that every $1 of additional fiscal stimulus adds $1 to aggregate demand. In this case, fiscal policy has added about 2% of GDP to annual aggregate demand over the past five years. Suppose that a one percentage-point increase in aggregate demand raises the appropriate level of interest rates by one percentage point, which is in line with the specification of the Taylor Rule that former Fed Chair Janet Yellen favored. This implies that fiscal policy alone has raised the neutral rate by over two percentage points over this time period. Laubach-Williams And The Fed Pause The discussion above suggests that the neutral rate of interest may be much higher than what the widely-used Laubach-Williams (LW) model implies. The LW model essentially calculates the trend growth rate of the economy in order to come up with its estimate for the neutral rate (Chart 10). It is an overly simplistic approach, as it ignores all the other factors influencing savings and investment decisions. Nevertheless, it seems to be driving the Fed’s thinking to a significant degree.

Chart 10

Chart 11Things That Make The Fed Go "Hmm"...

Things That Make The Fed Go "Hmm"...

Things That Make The Fed Go "Hmm"...

The real fed funds rate reached the LW estimate for the first time in 11 years last December (Chart 11). While we would not go as far as crediting the model for the Fed’s decision to go on hold – the sell-off in stocks and the flattening of the yield curve played a much larger role – the Fed’s reliance on the model does explain why it has maintained a dovish stance this year even as financial conditions have eased. Waiting For The Whites Of Inflation’s Eyes To his credit, John Williams, who helped develop the model more than 15 years ago, and now serves as the President of the New York Fed and the Vice Chair of the FOMC, has stressed that there is a wide band of uncertainty around any estimate of the neutral rate. Given this inherent uncertainty, a growing number of policymakers have shifted towards the Summers view that it is better to err on the side of caution and take a go-slow approach to raising rates. The rationale is straightforward: If the neutral rate turns out to be higher than expected and inflation starts to accelerate, central banks can always tighten monetary policy. In contrast, if the neutral rate is very low, the decision to raise rates could plunge the economy into a downward spiral. Historically, the Fed has cut rates by about six percentage points during recessions (Chart 12). At present rates of inflation, that would surely mean that the zero lower bound on interest rates would be reached, at which point monetary policy becomes increasingly impotent. Chart 12The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

A major drawback to waiting too long to raise rates is that it can take up to 18 months for changes in monetary policy to affect the economy. Inflation is also a highly lagging indicator: It normally does not peak until after a recession has begun, and does not bottom until the recovery is well underway (Chart 13). By the time you realize that the economy is overheating, it may be too late to prevent inflation from rising.

Chart 13

Of course, in the minds of many influential economists, higher inflation would be a virtue rather than a vice. Summers has argued that the Fed should aim to bring inflation into a range of 3%-to-4% in order to ensure that real rates can fall far enough into negative territory during the next recession. Higher inflation could also alleviate the nominal wage rigidity problem, thus allowing real wages to adjust more readily in response to economic shocks. The risk of aiming for higher inflation is that you will get more of it than you bargained for. True, inflation was broadly stable in the mid-to-late 1980s at around 4%, but this followed a period of much higher inflation in the late 1970s/early 1980s (Chart 14). It may be more difficult to stabilize inflation after it has risen than after it has fallen. This is especially likely to be the case if the central bank has purposely taken steps to raise inflation. Chart 14Inflation Was Broadly Stable At Around 4% In The Mid-To-Late 1980s

Inflation Was Broadly Stable At Around 4% In The Mid-To-Late 1980s

Inflation Was Broadly Stable At Around 4% In The Mid-To-Late 1980s

Supersymmetry: Inflation Edition The Fed is not about to raise its inflation target anytime soon. It is, however, rethinking the manner in which it conducts monetary policy in a way that will probably lead to somewhat higher inflation. Under the Fed’s existing framework, its “symmetric” inflation target is not supposed to be backward-looking. Symmetry simply means that the Fed targets 2% inflation every year, allowing for an equal probability of inflation ending up overshooting its mark as undershooting it. If inflation has missed its target in the past, this does not give the Fed license to try to exceed it in the future. Bygones are bygones.

Chart 15

Chart 16Inflation Has Been Below The Fed's 2% Target For The Past 10 Years

Inflation Has Been Below The Fed's 2% Target For The Past 10 Years

Inflation Has Been Below The Fed's 2% Target For The Past 10 Years

This definition of symmetry is starting to shift to one that is both forward-looking and backward-looking. This effectively brings the Fed one step closer to adopting price-level targeting – an idea John Williams has spoken glowingly about. Under a price-level targeting regime, the Fed would try to keep the price level on a predetermined trend (Chart 15). Inflation undershoots would have to be rectified with overshoots, and vice versa. This is obviously relevant for the current environment. Chart 16 shows that the core PCE deflator is now 4.6% below where it would have been if it increased by 2% per year since the financial crisis. Even if the Fed did not change its inflation target, bringing the deflator back towards its pre-crisis trend would still require that inflation run above the Fed’s target over the next few years. As Neel Kashkari said earlier this year: “We officially have a symmetric target and actual inflation has averaged around 1.7%, below our 2% target, for the past several years. So if we were at 2.3% for several years that shouldn't be concerning.”3 Investment Conclusions Risk assets may see heightened volatility over the next few days as markets adjust to the fact that rate cuts are not forthcoming. Nevertheless, with rates still far below our estimate of neutral, the path of least resistance for global equities remains to the upside. Recessions typically do not occur when monetary policy is accommodative. The stock market, in turn, rarely falls in a sustained manner when the economy is expanding (Chart 17). This view prompted us to upgrade global equities in December. We remain cyclically bullish today. Chart 17Recessions And Bear Markets Usually Overlap

Recessions And Bear Markets Usually Overlap

Recessions And Bear Markets Usually Overlap

Regionally, we do not have any strong preferences at the moment, but expect to upgrade EM and Europe by this summer. Despite the occasional disappointment such as this month’s manufacturing ISM, a broad swath of the evidence suggests global growth is reaccelerating (Chart 18). EM and European stocks tend to outperform in that environment. The dollar tends to weaken when the global economy strengthens (Chart 19). Hence, the greenback should enter a soft patch over the coming months which could last until the second half of next year. Chart 18Global Growth Is Reaccelerating

Global Growth Is Reaccelerating

Global Growth Is Reaccelerating

Chart 19The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

Global bond yields will drift higher over the coming months as global growth surprises on the upside. Investors should position for somewhat steeper yield curves globally. The U.S. yield curve will flatten again late next year as inflation starts to reach levels that even a dovish Fed is not comfortable with. This will likely set the stage for an inversion of the yield curve in early 2021 and a global recession later that same year. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1 “Government Economists Turn to Big Data to Track the Economy,” The Wall Street Journal, April 30, 2019. 2 In most economic models, the capital-to-output ratio is assumed to converge towards a stable level over time. By definition, the capital stock in Year t is determined by the capital stock in Year t-1 plus whatever net investment (gross investment minus depreciation) takes place in Year t. In general, the optimal net investment-to-GDP ratio will equal the product of the capital-to-output ratio and the growth rate of GDP. For example, suppose that the capital-to-output ratio is three (meaning that the capital stock is three times as large as GDP). If output does not change from one year to the next, no additional net investment would be necessary to maintain a stable capital-to-output ratio. However, if output is growing at 2%, net investment of 3X2%=6% of GDP would be required. 3 “Fed's Kashkari says some overshoot on inflation would not be alarming,” Reuters, April 11, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 20

Tactical Trades Strategic Recommendations Closed Trades

Yesterday, the Fed dashed the hopes of traders betting on an interest rate cut this year. The FOMC is on pause for now, and it will not respond to what it perceives as a transitory inflation slowdown. The Fed reaction function has also evolved. The Fed…

Highlights Open an equity market relative overweight to Europe versus China. Upgrade Denmark to neutral. Downgrade the Netherlands to underweight. Maintain Switzerland at overweight. With the Euro Stoxx 50 now up almost 20 percent from its January 3 low, the majority of this year’s absolute gains have already been made. Core euro area bond yields will edge modestly higher… …and EUR/USD will appreciate, as the backward-looking data on which the ECB depends catches up with the more perky real-time economic data. Feature Vertical charts scare us, as we contemplate falling over the edge. But they also excite us, as we contemplate a lucrative investment opportunity. Right now, the vertical chart that is causing us palpitations is technology versus healthcare (Chart of the Week). Chart of the WeekTechnology Versus Healthcare Has Gone Vertical!

Technology Versus Healthcare Has Gone Vertical!

Technology Versus Healthcare Has Gone Vertical!

The technology versus healthcare sector pair is critical, because it looms large in several stock markets’ ‘fingerprint’ sector skews. Meaning that the technology versus healthcare relative performance has unavoidable consequences for regional and country stock market allocation (Chart I-2 and Chart I-3). The technology versus healthcare sector pair is critical, because it looms large in several stock markets’ ‘fingerprint’ sector skews. Chart I-2When Technology Underperforms Healthcare, Netherlands Underperforms Switzerland

When Technology Underperforms Healthcare, Netherlands Underperforms Switzerland

When Technology Underperforms Healthcare, Netherlands Underperforms Switzerland

Chart I-3When Technology Underperforms Healthcare, China Underperforms Switzerland

When Technology Underperforms Healthcare, China Underperforms Switzerland

When Technology Underperforms Healthcare, China Underperforms Switzerland

Specifically, from a European stock market perspective, the Netherlands is overweight technology while Switzerland and Denmark are both overweight healthcare. Further afield, the U.S. is overweight technology while China is both overweight technology and underweight healthcare. Explaining Verticality And The Subsequent Fall What creates vertical charts? To answer the question, let’s turn it on its head: what prevents vertical charts? The answer is: the presence of value investors. In a healthy market, a cohort of value investors will sit on the side lines and only transact with the marginal seller when the price falls to a semblance of value. In other words, the value sensitive investors help to set the price, preventing verticality. But if the value sensitive cohort switches out of character to join a strong uptrend, the cohort will suddenly become value insensitive. In this case, the marginal seller will set the price higher and the formerly uninterested value sensitive buyer will now buy at the higher price. The market has morphed into a trend-following market. As more of the value cohort switch sides, the process adds rocket fuel to the rally. Driven by the ‘fear of missing out’ the marginal buyer will buy at larger and larger price increments, and the chart becomes vertical. What triggers the subsequent fall? When all of the value cohort have joined the uptrend, the fuel has run out: the marginal seller will no longer find a willing marginal buyer at the elevated price. At this critical point, one of two things will happen. Either: a completely new cohort of even deeper value investors will switch out of character and provide new fuel to the trend, allowing it to continue. Or: the deep value investors will stay true to character and will only deal with the marginal seller when the price falls, perhaps sharply, to a semblance of deep value. Technology versus healthcare is now at this critical technical point at which the probability of trend-reversal has significantly increased. Both the theoretical and empirical evidence suggests that at this critical point, the probability of trend-continuation decreases to about a third and the probability of a trend-reversal increases to about two-thirds. Technology versus healthcare is now at this critical technical point at which the probability of trend-reversal has significantly increased (Chart I-4). Chart I-4Technology Versus Healthcare: The Probability Of A Trend-Reversal Is High

Technology Versus Healthcare: The Probability Of A Trend-Reversal Is High

Technology Versus Healthcare: The Probability Of A Trend-Reversal Is High

Therefore, on a tactical horizon, it is now appropriate to underweight technology versus healthcare – which, to reiterate, carries unavoidable consequences for country and regional stock market allocation: Open an overweight to Europe versus China. Upgrade Denmark to neutral. Downgrade the Netherlands to underweight. Maintain Switzerland at overweight. Distinguishing Between Valuation And Growth Is Extremely Difficult There is another problem for value investors. Over short periods – meaning less than a year – it is very difficult, if not impossible, to decompose a price return into its two components: the component coming from the change in valuation and the component coming from the change in earnings growth expectations. A stock market’s actual earnings are highly sensitive to small changes in economic growth. This is universally the case but is especially true in Europe, because the European stock market’s skew towards growth-sensitive cyclicals gives it a very high operational leverage to GDP growth: a seemingly minor 0.5 percent change in economic growth translates into a major 25 percent change in stock market earnings growth (Chart I-5). The slightest improvement in economic growth expectations causes the market to upgrade its forecasts for earnings very sharply. Chart I-5A Minor Upgrade To Economic Growth = A Major Upgrade To Profits Growth

A Minor Upgrade To Economic Growth = A Major Upgrade To Profits Growth

A Minor Upgrade To Economic Growth = A Major Upgrade To Profits Growth

Given this very high operational leverage, the slightest improvement in economic growth expectations causes the market to upgrade its forecasts for earnings very sharply. Which of course lifts the market’s price, P, very sharply. In contrast, equity analysts’ forecasts for earnings, which drive the market’s ‘official’ forward earnings, E, adjust much more slowly. As my colleague, Chris Bowes explains: “analysts get married to a view and usually require overwhelming evidence to materially change it.” The upshot is that the P rises very sharply but the official forward E does not, meaning that the official forward P/E also rises very sharply. This gives the impression that the move is mostly valuation driven, but the truth is that the move is mostly earnings growth driven. In a similar vein, when central banks guide interest rates lower, how much of the equity market’s move is due to a higher valuation, and how much is due to improved prospects for economic growth resulting from the central bank policy change? Over relatively short periods of time, it is extremely difficult to tell. All of which provides an important lesson: over short periods, do not focus on separately forecasting the valuation change and earnings growth change of a stock market. Much better to forecast the stock market price directly, by focussing on the two main things which will drive it: changes to central bank policy, and changes to short-term real-time economic growth. Focus On Central Banks And Short-Term Economic Growth Central bank policy now ‘depends’ on relatively longer-term changes (say, year-on-year) in backward-looking data, most notably the consumer price index. Whereas the stock market’s earnings growth expectations take their cue from shorter-term changes in real-time economic indicators (Chart I-6). Chart I-6Quarter-On-Quarter Growth Is Rebounding

Quarter-On-Quarter Growth Is Rebounding

Quarter-On-Quarter Growth Is Rebounding

Hence, the ‘sweet spot’ for equity markets is when, in simple terms, year-on-year CPI inflation is decelerating, implying central banks will become more dovish, while quarter-on-quarter economic growth is accelerating, implying the market will upgrade earnings growth (Chart I-7). The stock market’s earnings growth expectations take their cue from shorter-term changes in real-time economic indicators. The ‘weak spot’ for equity markets is the exact opposite, when year-on-year CPI inflation is accelerating, implying central banks will become less dovish, while quarter-on-quarter economic growth is decelerating, implying the market will downgrade earnings growth. As 2019 progresses, our high-conviction prediction is that equity markets will move from a sweet spot to a weak spot. With the Euro Stoxx 50 now up almost 20 percent from its January 3 low, it implies that the majority of 2019’s gains have already been made in the first four months of the year – and the market is unlikely to be significantly higher at the end of the year. Compared to the equity market, the bond, interest rate, and currency markets are – almost by definition – much more dependent on central banks’ lagging reaction functions than on real-time growth. Which solves the mystery as to why bond yields are close to new lows while equity markets are close to new highs. It also solves the mystery as to why EUR/USD has lagged the very clear recovery in euro area real-time growth and in euro area stock markets (Chart I-8). Central banks are following lagging indicators. Chart I-7Stock Markets Take Their Cue from Real-Time Indicators

Stock Markets Take Their Cue from Real-Time Indicators

Stock Markets Take Their Cue from Real-Time Indicators

Chart I-8Central Banks Are Following Lagging Indicators, Stock Markets Are Following Real-Time Indicators

Central Banks Are Following Lagging Indicators, Stock Markets Are Following Real-Time Indicators

Central Banks Are Following Lagging Indicators, Stock Markets Are Following Real-Time Indicators

But as the backward-looking data, on which the ECB depends, catches up with the more perky real-time data, core euro area bond yields will edge modestly higher, and EUR/USD will gently appreciate. Next week, in lieu of the usual weekly report, I will be giving this quarter’s webcast titled ‘From Sweet Spot to Weak Spot?’ live on Wednesday May 8 at 10.00 AM EDT (3.00 PM BST, 4.00 PM CEST, 10.00 PM HKT). Through a series of key charts, the webcast will reveal the prospects and opportunities for all asset-classes through the remainder of 2019. At the end of the webcast, I will also unveil a brand new investment recommendation. So don’t miss it! Fractal Trading System* Supporting the arguments in the main body of this report, fractal analysis suggests that the recent rally in China’s stock market is at a technical point that has reliably signaled previous major reversals. Accordingly, this week’s recommended trade is a stock market pair trade, short China versus Japan. Set the profit target at 2.5 percent with a symmetrical stop-loss. We now have six open positions. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-9Short China Vs. Japan

Short China VS. Japan

Short China VS. Japan

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights The March data brought the first signs of a stabilization in China’s “hard” economic data, albeit from a weak level. The April PMIs disappointed, but they remained in expansionary territory; this is in addition to a continued significant improvement in the trade-related subcomponents of the official survey. Chinese credit growth is unlikely to relapse over the coming year, despite recent investor concerns that Chinese policymakers may dial back their stimulus efforts. The pace of growth may moderate, but halting the uptrend in growth this year would constitute a major policy mistake that we do not expect. Chinese stocks may trend flat-to-down in the very near term as investors await a signed trade deal with the U.S. and further signs of a recovery in activity. Over the next 6-12 months, however, an overweight stance is warranted, barring a major relapse in our leading indicator. Feature Tables 1 and 2 on pages 2 and 3 highlight key developments in China’s economy and its financial markets over the past month. On the growth front, March’s data brought the very first (albeit modest) signs of stabilization in actual Chinese economic activity. While the April manufacturing PMIs released earlier this week disappointed, the trade related components of the official survey continued to improve meaningfully, which implies that an improvement in domestic demand is still early. This conclusion is not particularly surprising given that the first green shoots in the actual data are emerging from a depressed level of activity. Credit growth has only recently picked up, implying that actual activity will strengthen over the coming 6-12 months followed a signed trade deal and a continued (modest) uptrend in credit. Table 1China Macro Data Summary

China Macro And Market Review

China Macro And Market Review

Table 2China Financial Market Performance Summary

China Macro And Market Review

China Macro And Market Review