Policy

Savings must either flow into domestic investment, or abroad. Saving too much, with nowhere to funnel it, is breaking China’s economic model according to our Global Investment Strategy colleagues. As China's share of global manufacturing climbed to 30%,…

Trump may be slightly favored for the White House but the US election is still extremely close. Odds of a contested or contingent election are rising, which should cause stock market volatility. A Republican sweep should cause more volatility. Democratic gridlock is next most likely but benign for stocks in the short run.

Developed markets Flash PMIs estimates for October were mixed, with resilient US numbers and weakness elsewhere. The eurozone composite met expectations but remains below the 50-level expansion threshold. Germany outperformed expectations as foreshadowed…

Our Counterpoint Strategy team believes the equity bull market’s biggest risk is the reversal of the divergence between Japanese and US real yields. Japan’s real policy interest rate differential versus the US stands at an unprecedented and unsustainable…

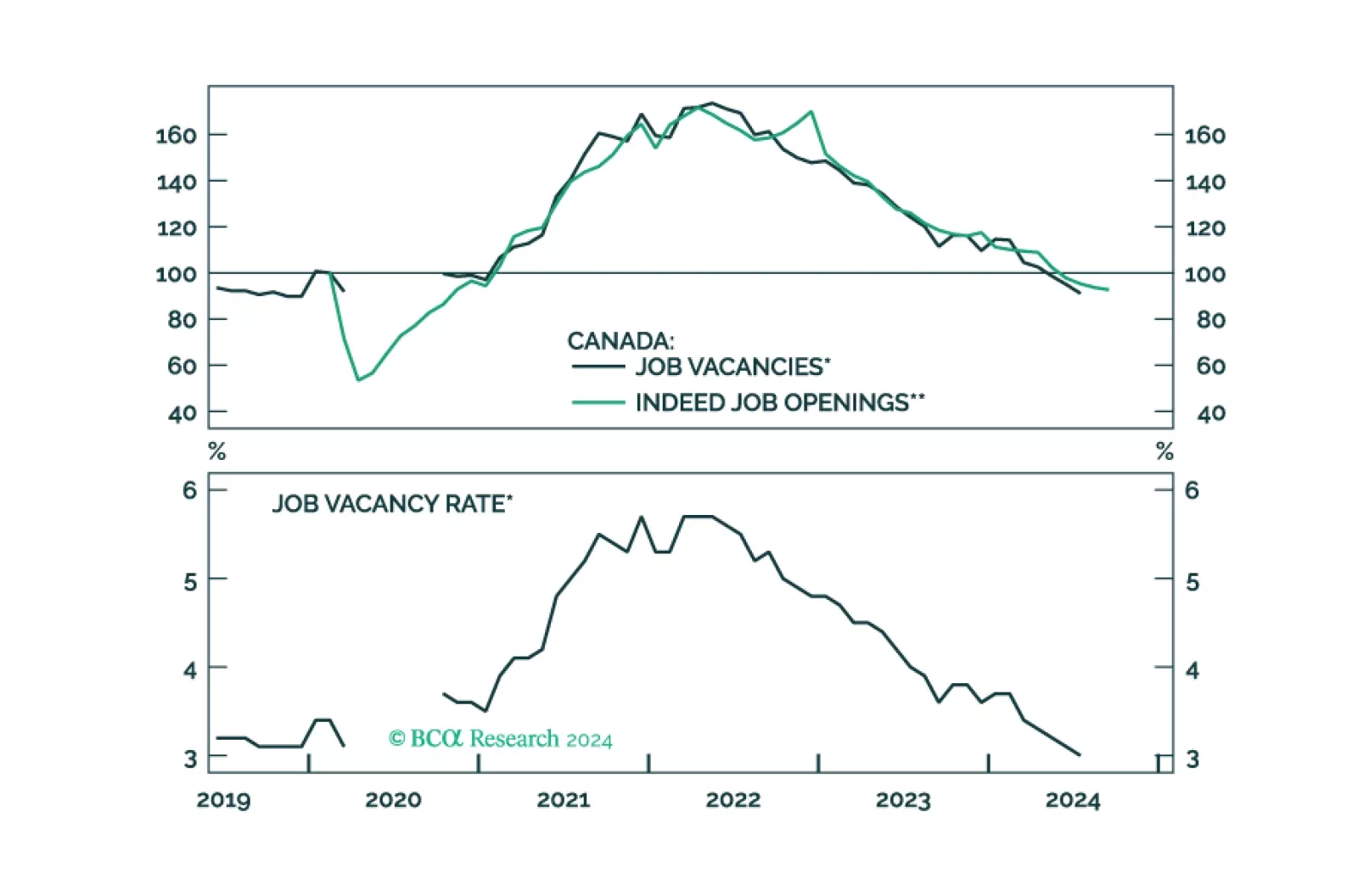

In this Insight, we evaluate if there is more juice in our macro bet of being long June 2025 CORRA versus SOFR futures, and correspondingly, being short the CAD, for investors with a 1-3 month horizon.

Flash estimates for European consumer confidence met expectations at -12.5 in October, rising from -12.9 in September. Despite this positive development, Euro Area sentiment remains poor. Consumer confidence remains below its long-term average and near the…

After cutting three times already since June, the Bank of Canada fulfilled market expectations and cut the overnight rate by 50 bps to 3.75%. The BoC sees risks around inflation as roughly balanced over its projection horizon, and is focused on “sticking the…

The Federal Reserve’s Beige Book, its survey of business contacts, shows an economy that has seen little growth since early September. The Fed’s contacts confirmed the manufacturing recession reflected in other data sources. Loan demand was mixed, as…

The US dollar had a strong October thus far, breaching its 20-,50- and 200-day moving averages with a 4% increase and only three trading days in the red. The DXY now sits above where it was before the August selloff in risk assets. What’s behind this…