Policy

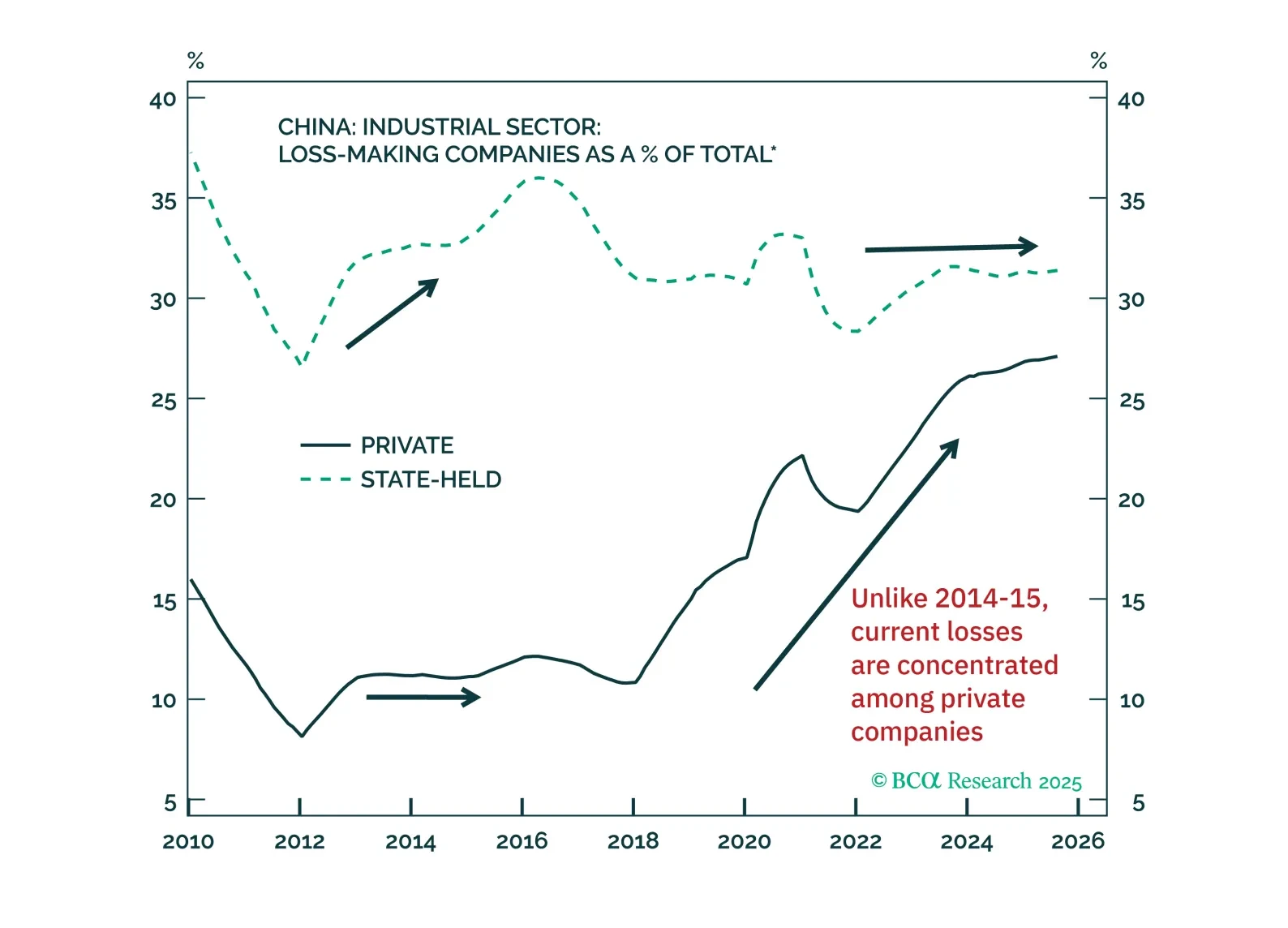

China's anti-involution policies will not end deflation or boost corporate profits on a sustainable basis. Authorities will be reluctant to cut industrial capacity as doing so would lead to layoffs. Consequently, production will continue to exceed demand, and price deflation will persist.

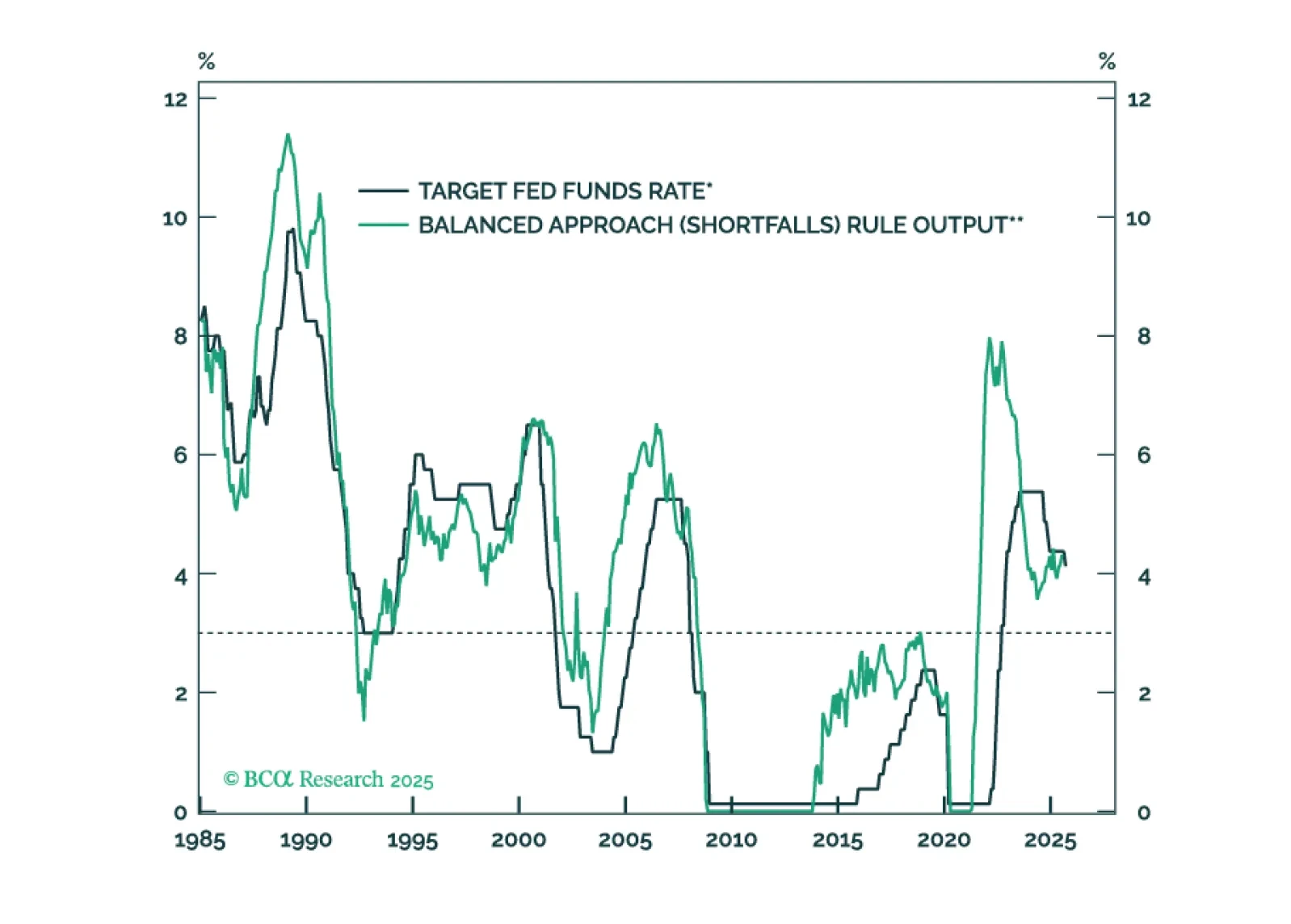

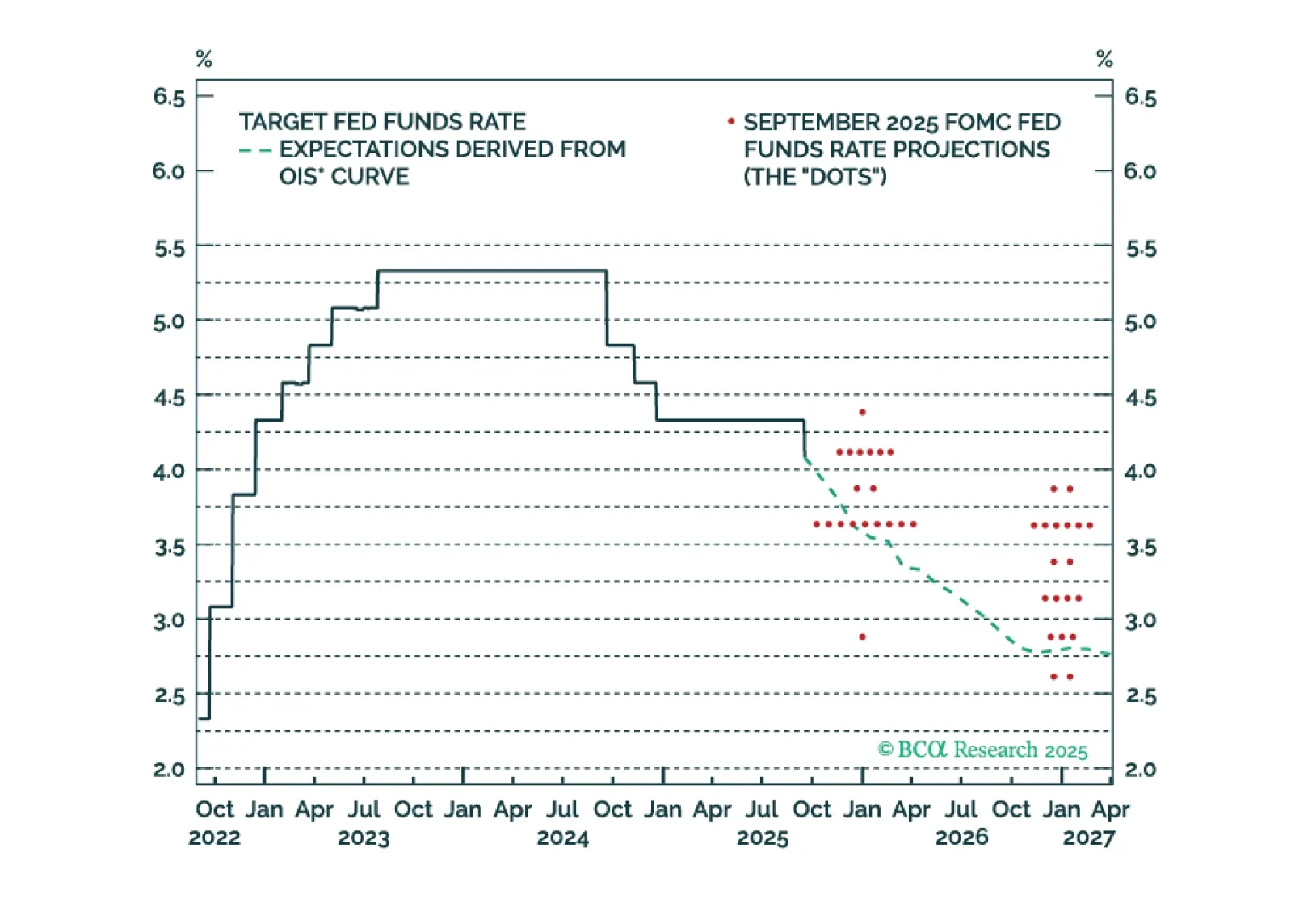

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

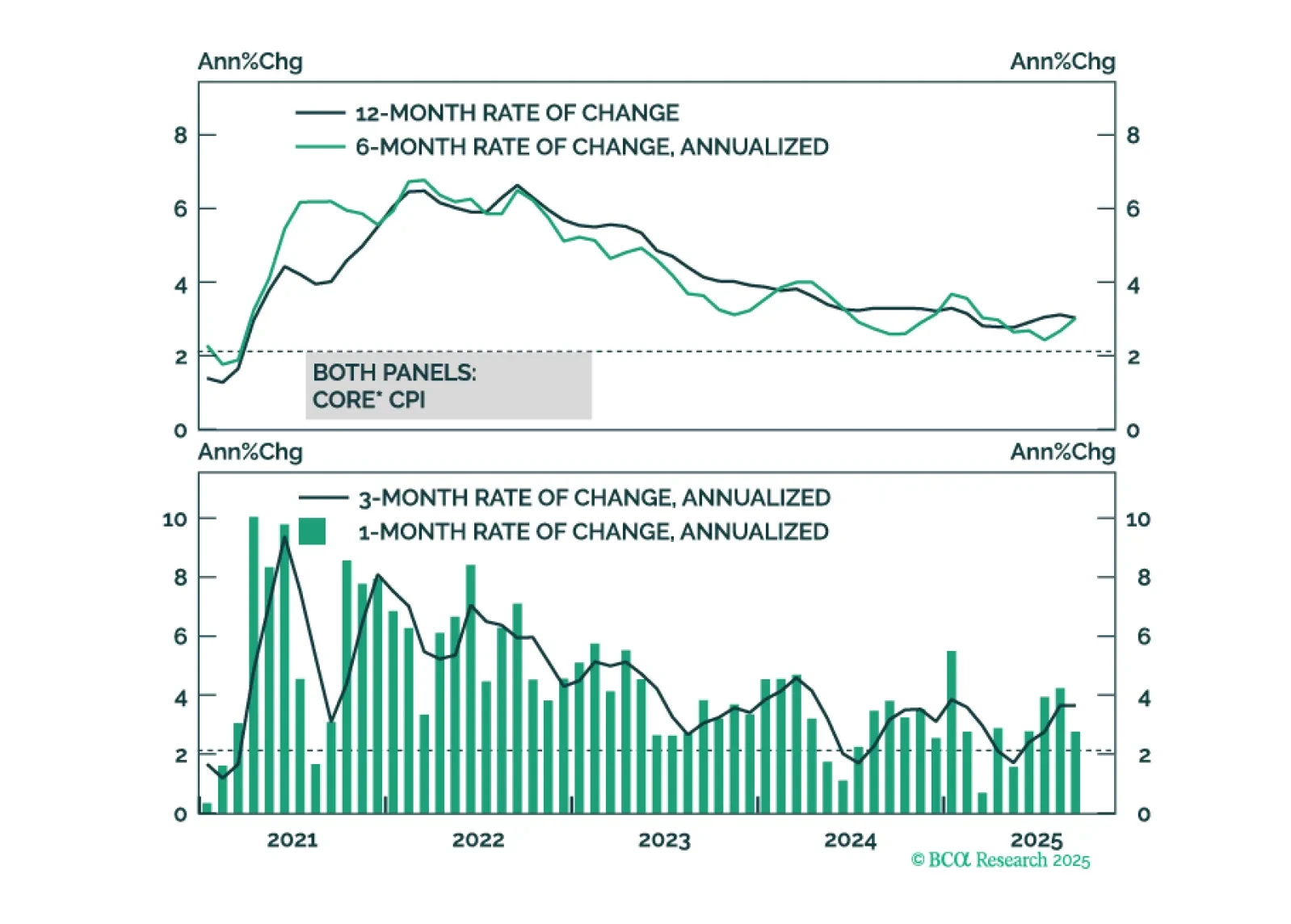

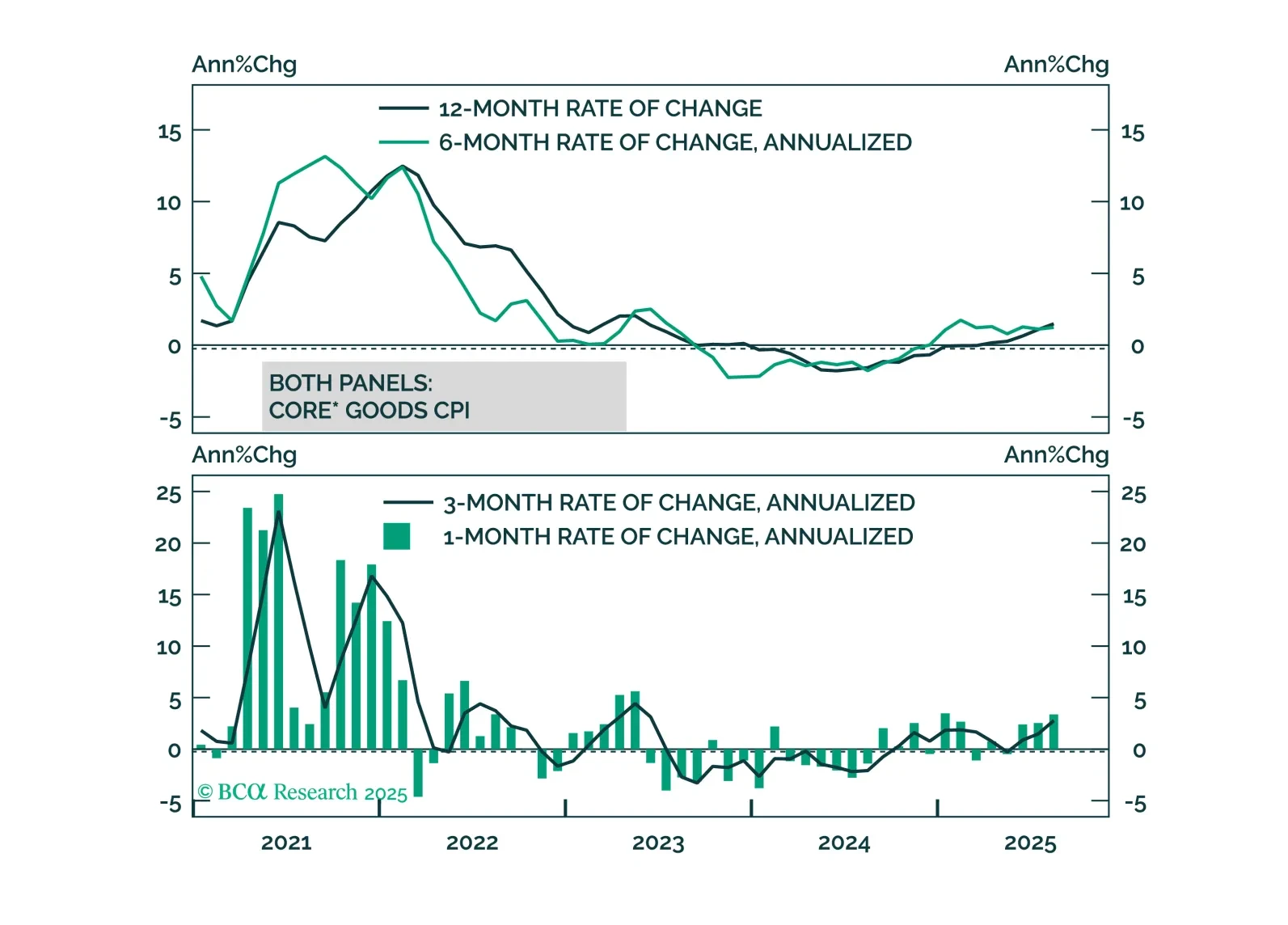

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

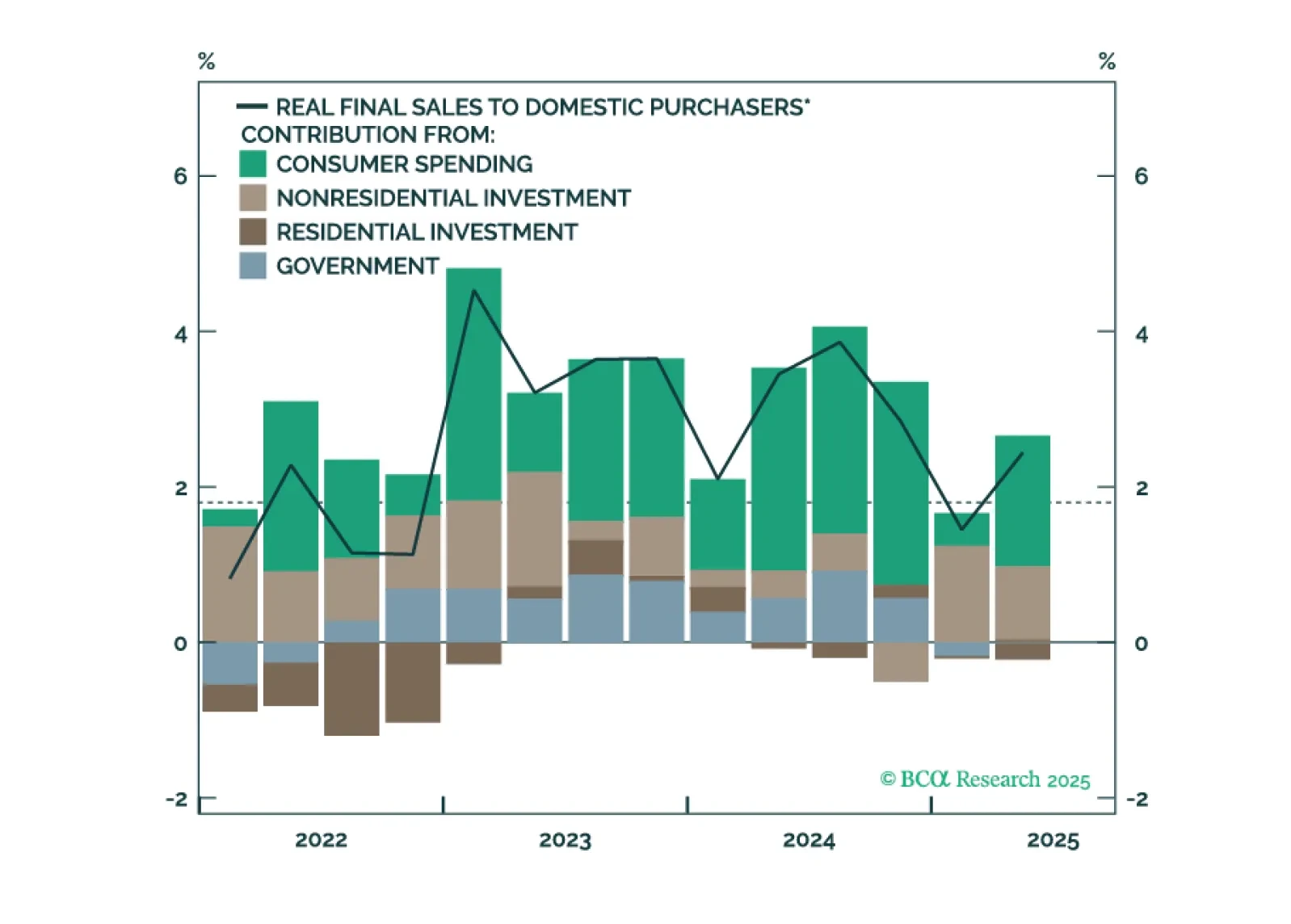

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

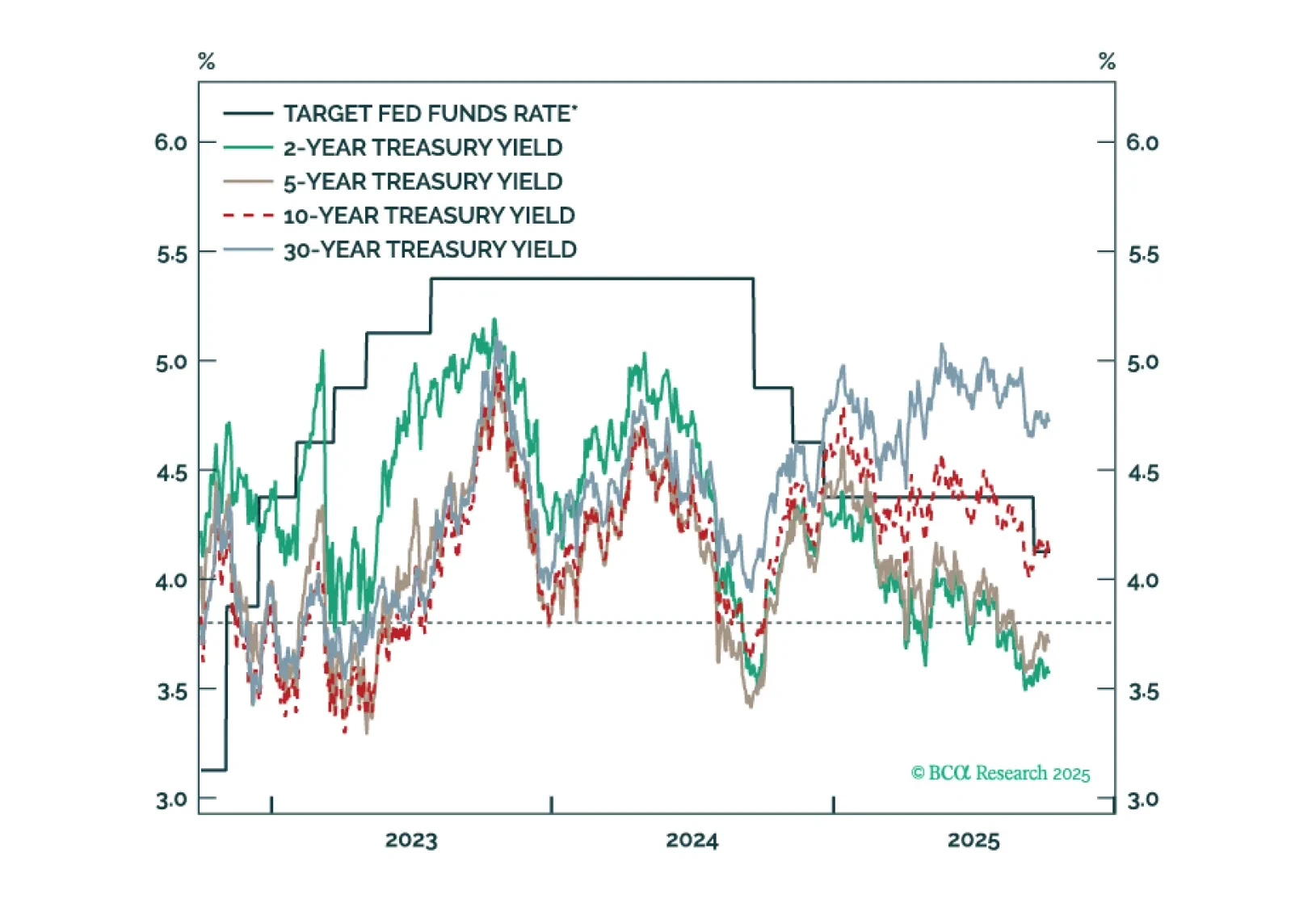

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

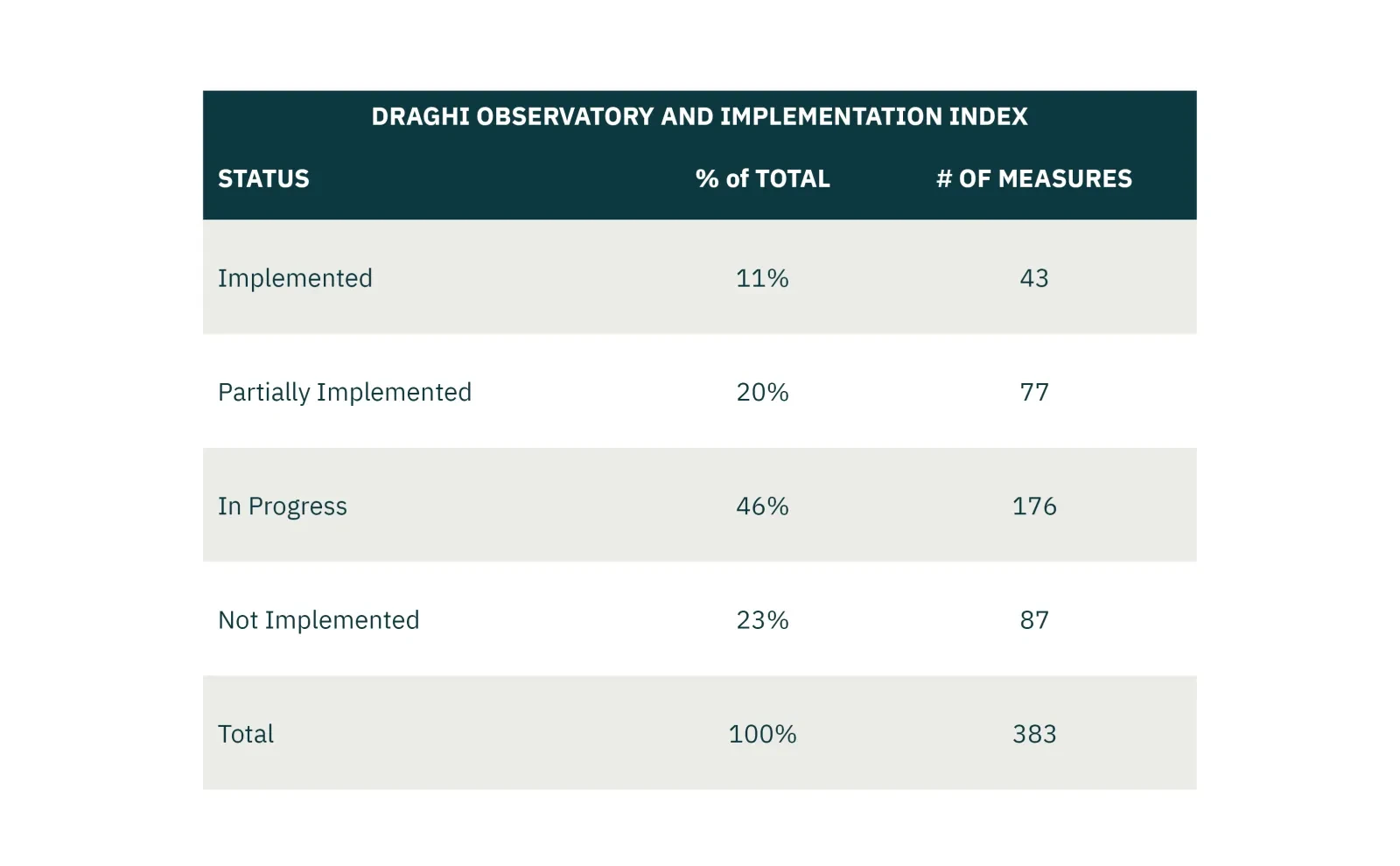

One year in, the EU is progressing slowly in implementing Mario Draghi's recommendations to restore Europe’s competitiveness. The lack of progress is due more to the various pushbacks from European capitals and the lack of proper funding than a lack of ambition. Our overall assessment remains positive, given the EU is adopting many of the priorities from Draghi’s report.

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

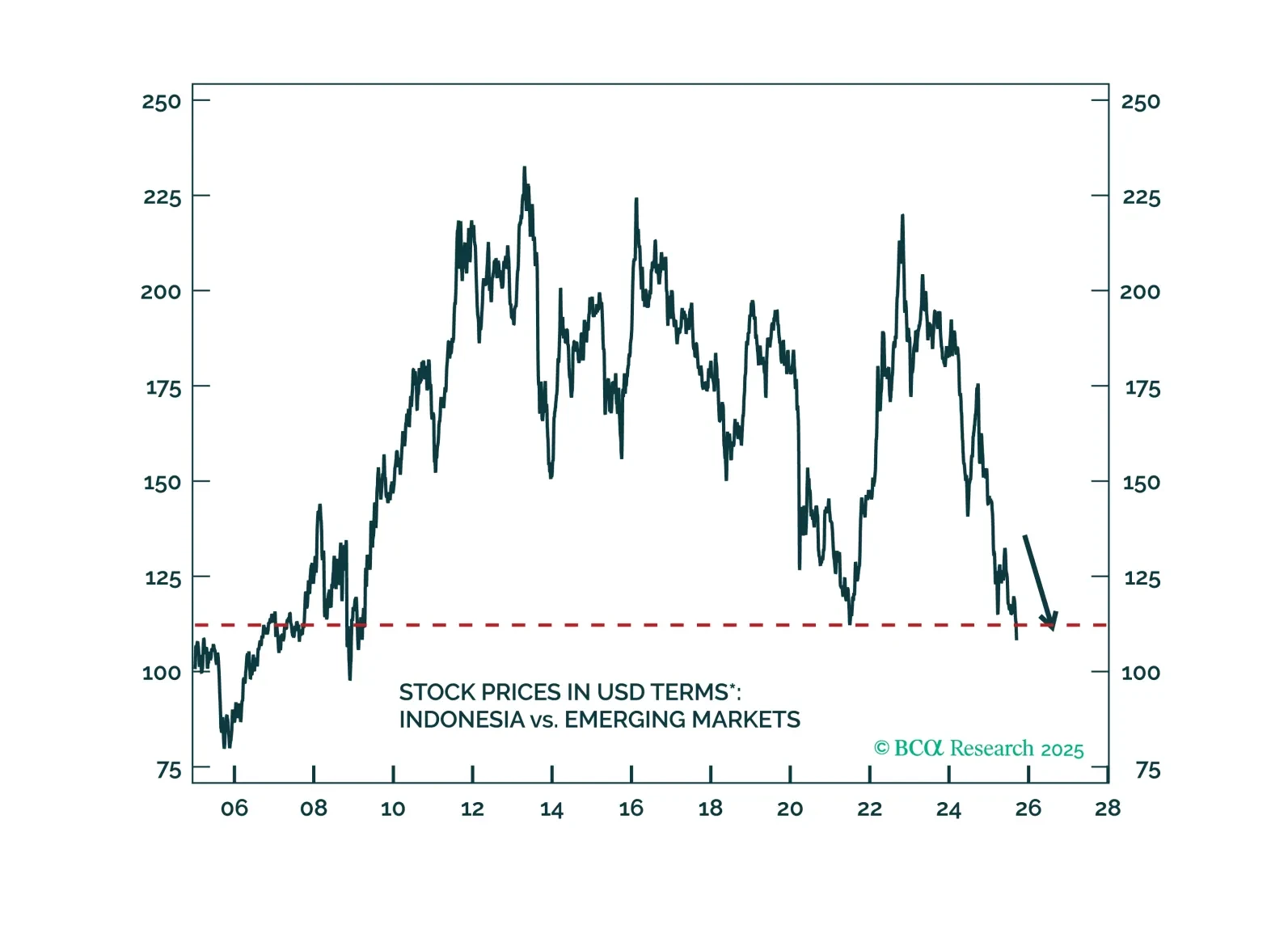

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.