Policy

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

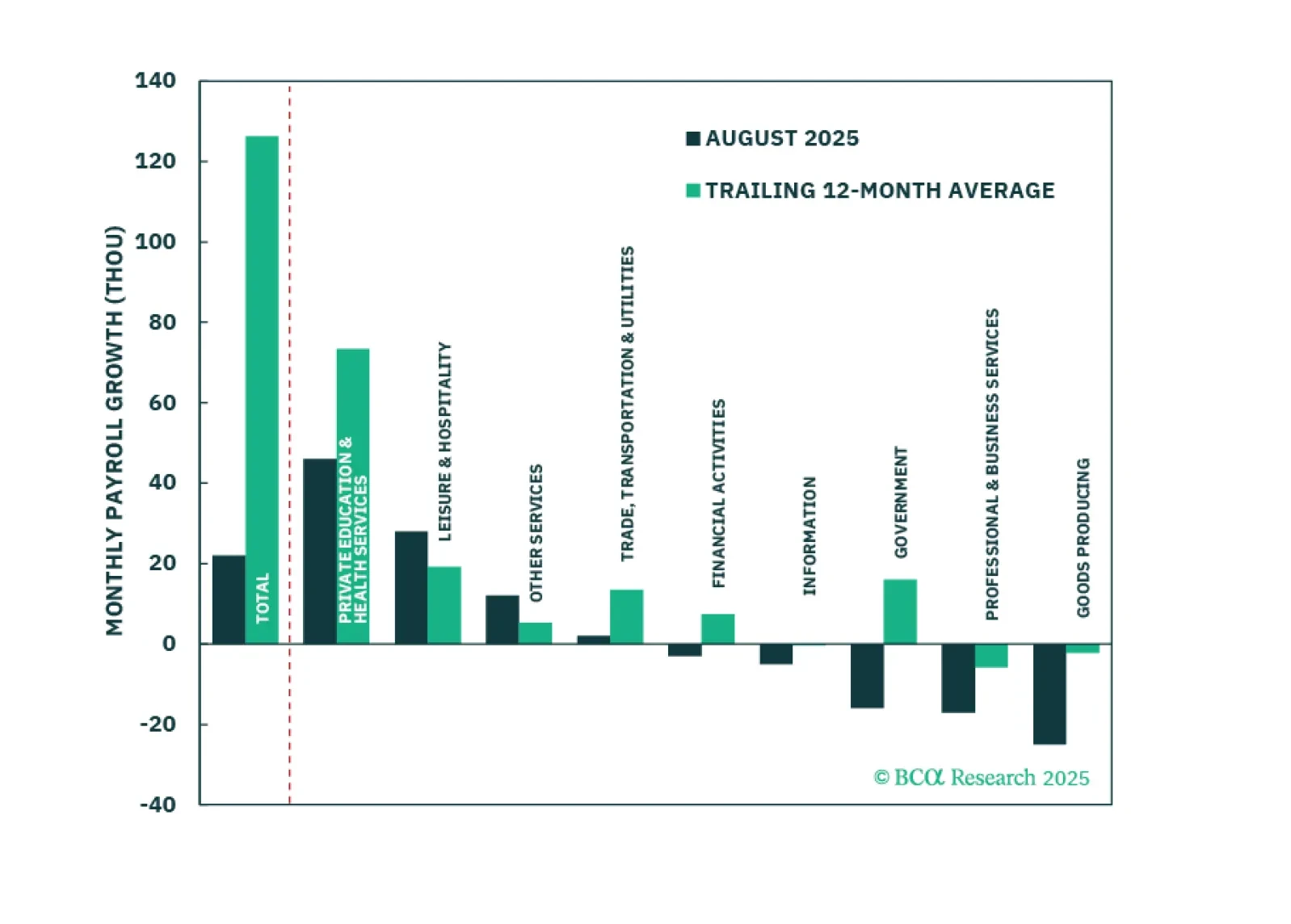

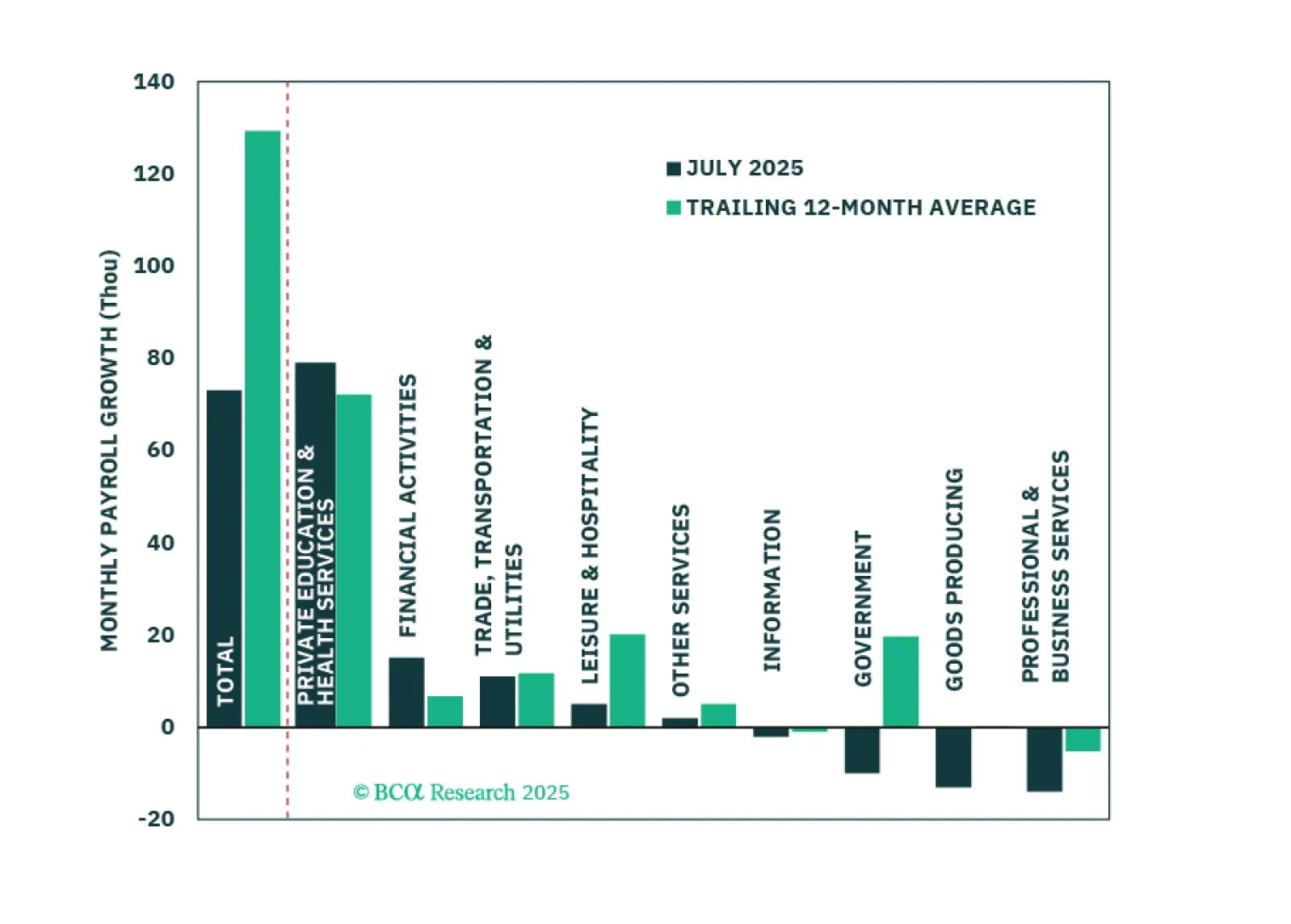

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

Our Portfolio Allocation Summary for September 2025.

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

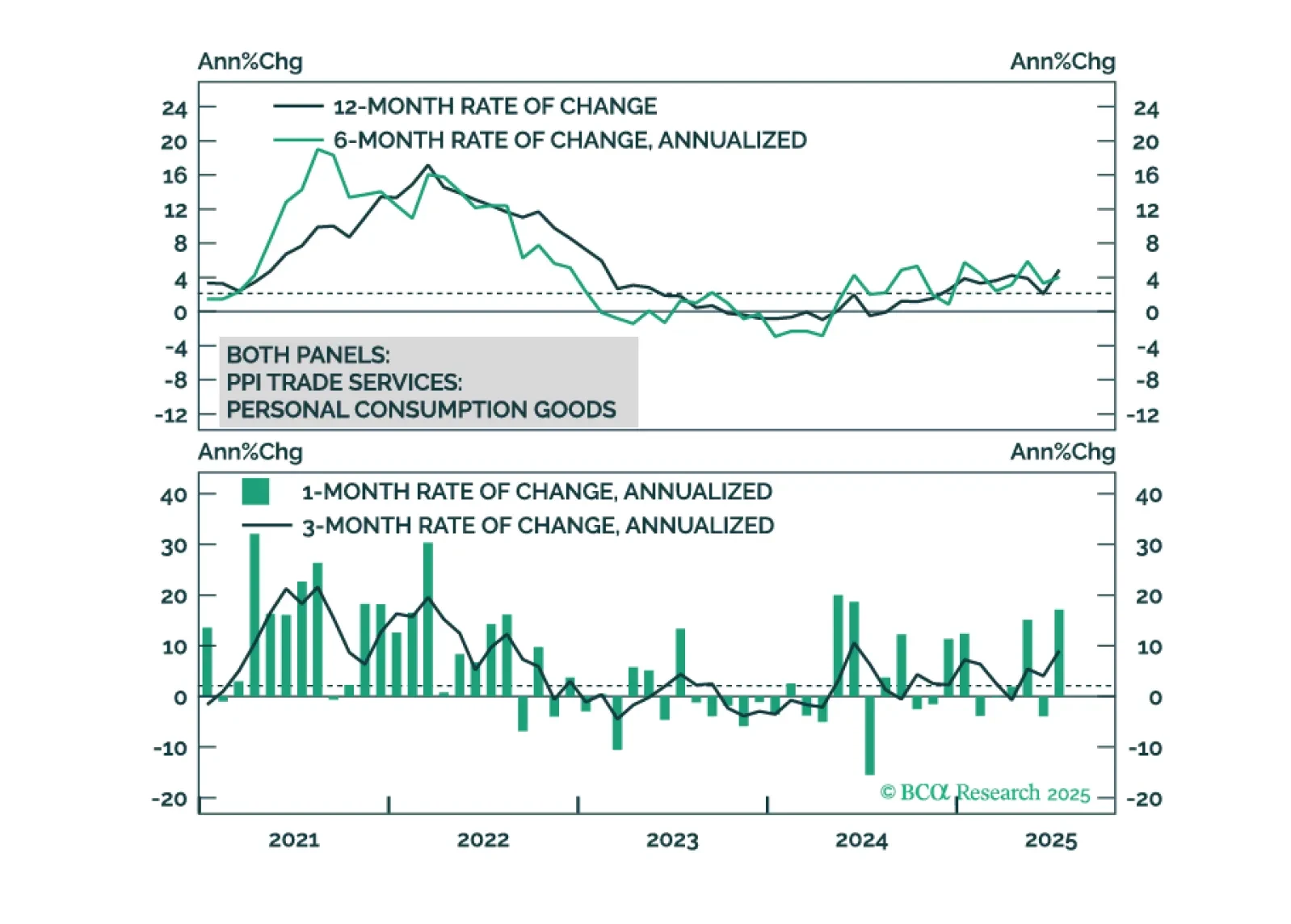

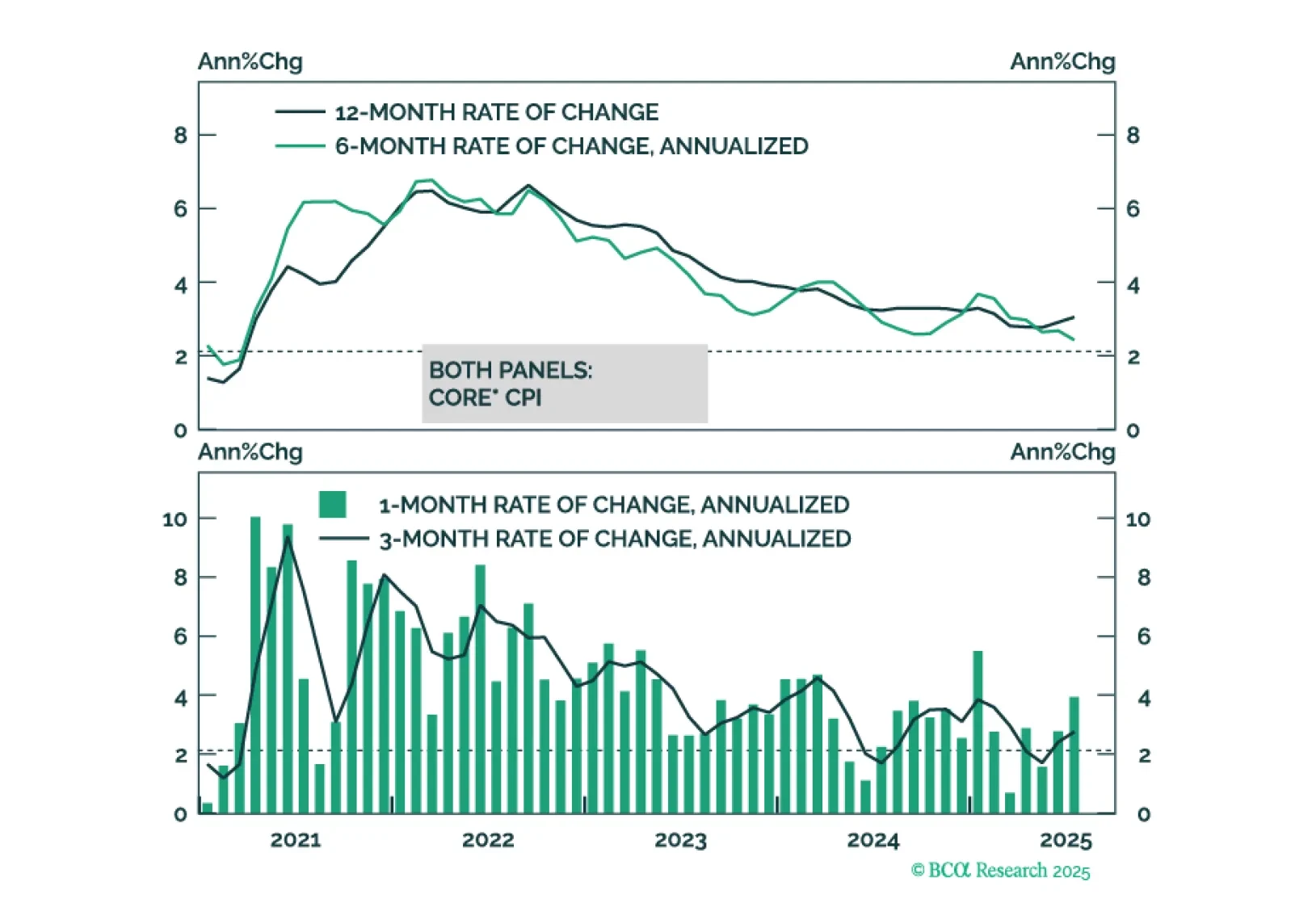

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

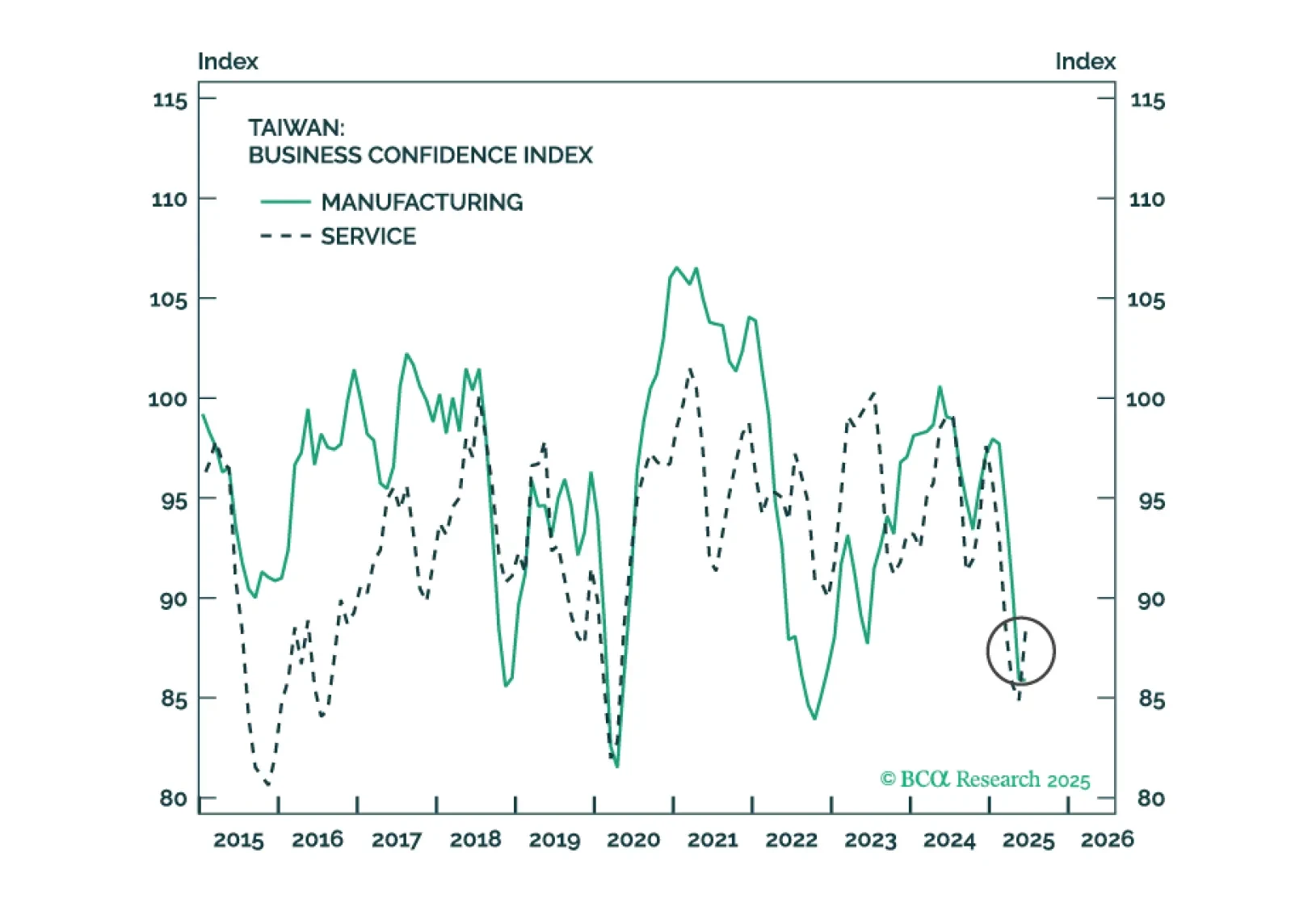

Taiwan’s failed recall election reduces 12-month geopolitical risk for Taiwanese and Chinese equities on the margin. We are reviewing our long European industrials / short Chinese industrials trade.

Our Portfolio Allocation Summary for August 2025.

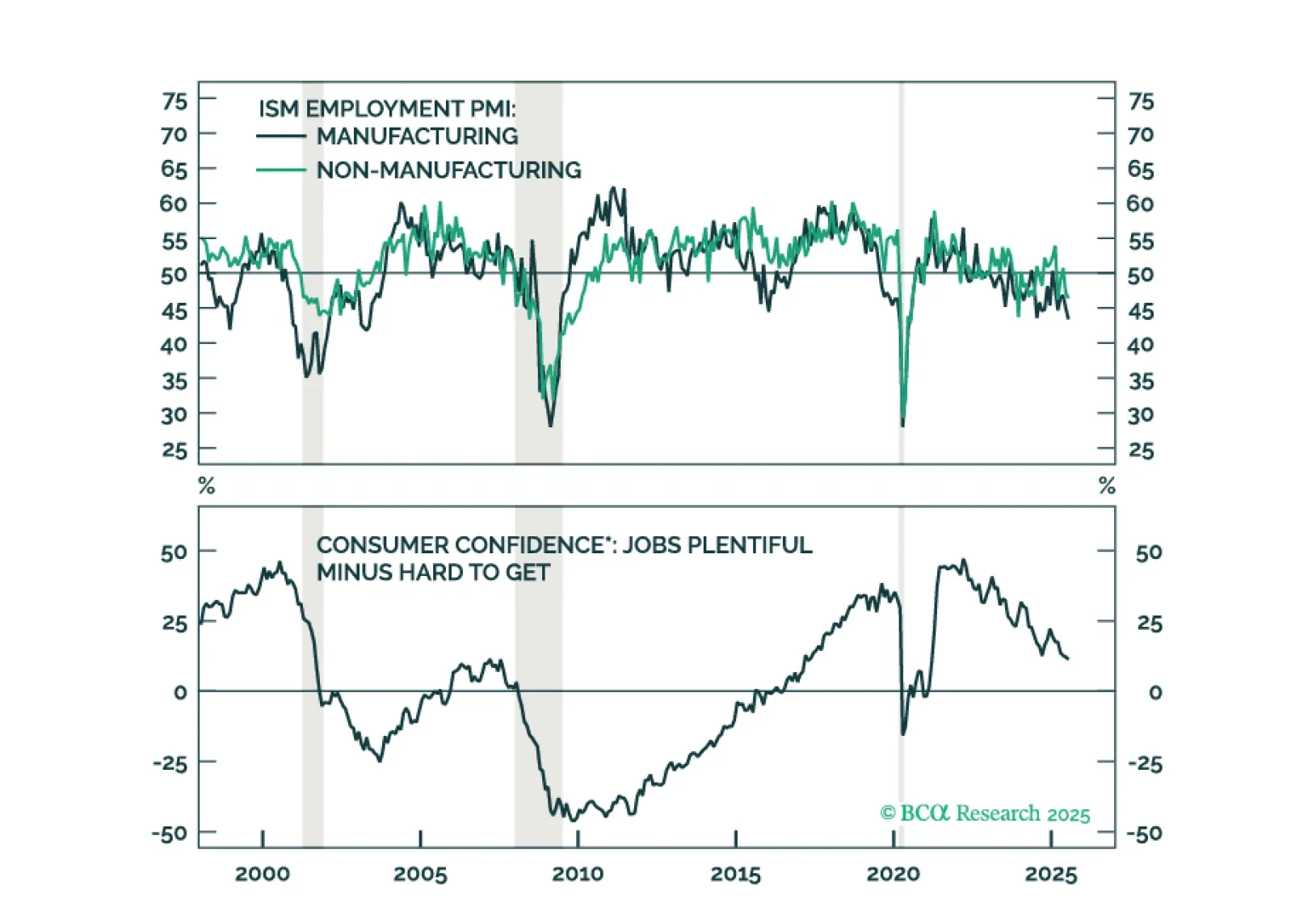

Economic activity and hiring cooled significantly in the first half of the year. The most important question for investors is whether this signals an imminent increase in labor market slack.

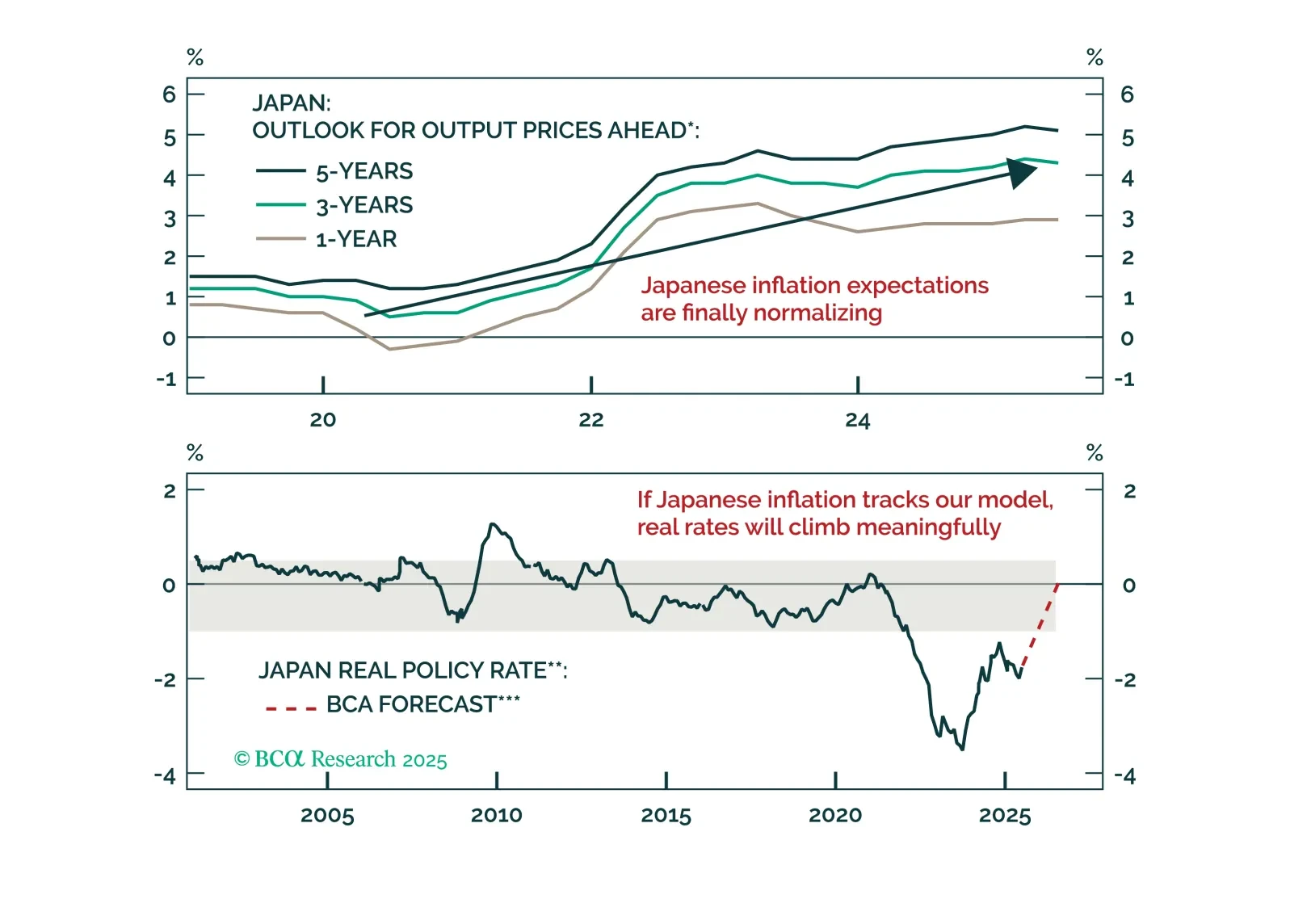

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.