Policy

In a widely expected move, the Bank of Canada (BoC) cut interest rates by a quarter of a percentage point for a third consecutive month in September, lowering the benchmark overnight rate to 4.25%. Policymakers also signaled further easing ahead. Both the…

According to BCA Research’s GeoMacro Strategy service, there are two main pressure points that the US can utilize against China. First, the US consumer market is the largest in the world. Despite having diversified away from the US, it remains a very…

The 2Y/10Y segment of the yield curve is flirting with un-inversion. Aggressive rate cut expectations have largely driven its steepening, with the 2-year Treasury yields falling nearly 100 bps over the past couple of months. Our colleagues at the Bank…

Significantly stronger-than-expected consumer spending growth led to an upward revision to US GDP growth in Q2. That said, gross domestic income (GDI) has been lagging behind GDP. It increased 1.3% q/q in Q2, at the same rate as in Q1, and well below Q2’s…

According to BCA Research’s European Investment Strategy service, an increase in borrowing costs will further weaken vulnerable corporate balance sheets. As suggested by their Corporate Health Monitors (CHMs), the health of High-Yield corporate balance sheets…

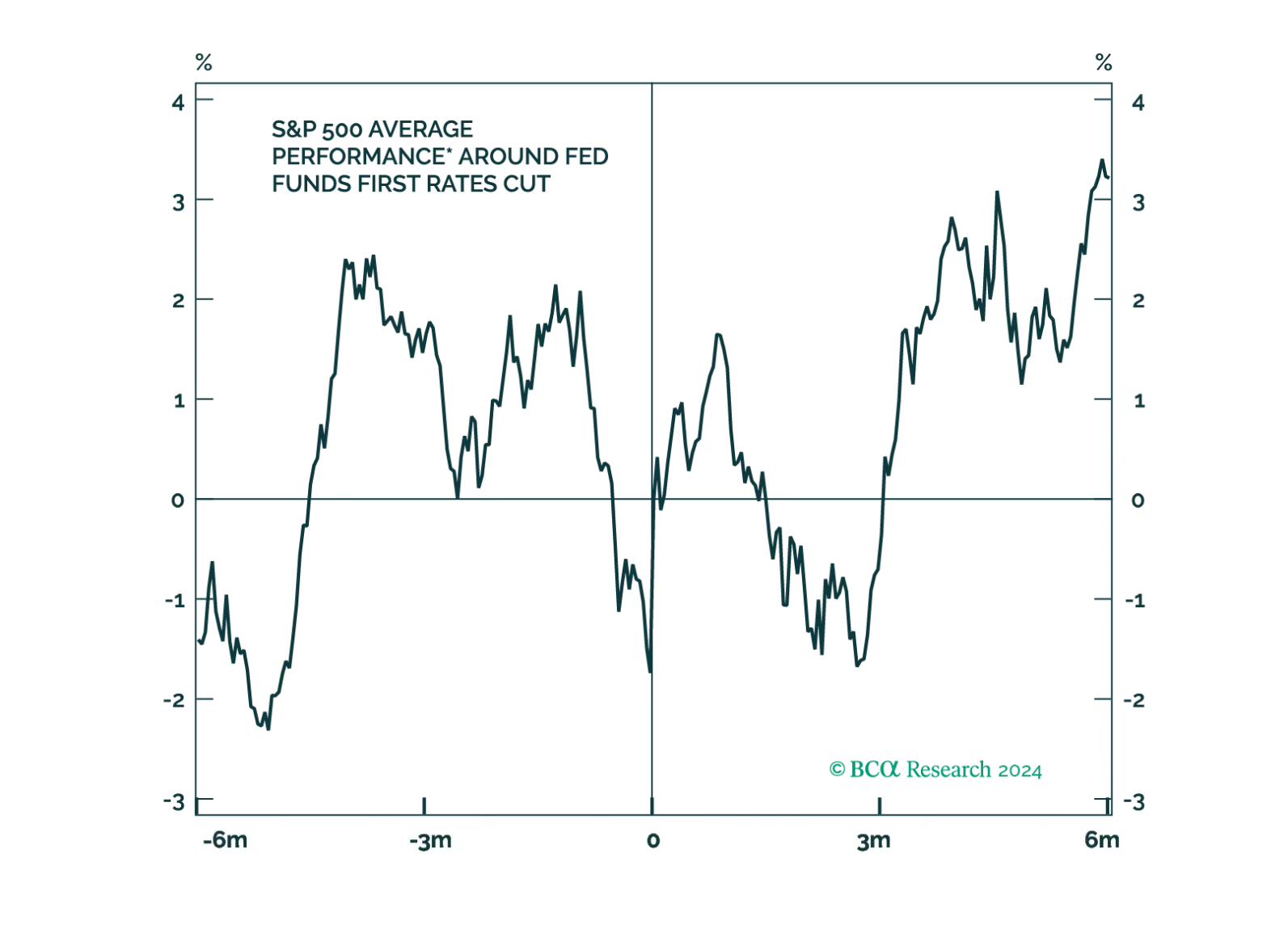

Even after the Fed cuts rates, policy will remain restrictive for some time. Moreover, in history, stocks have tended to fall around the first rate cut. We remain cautious on the outlook for the economy and risk assets.

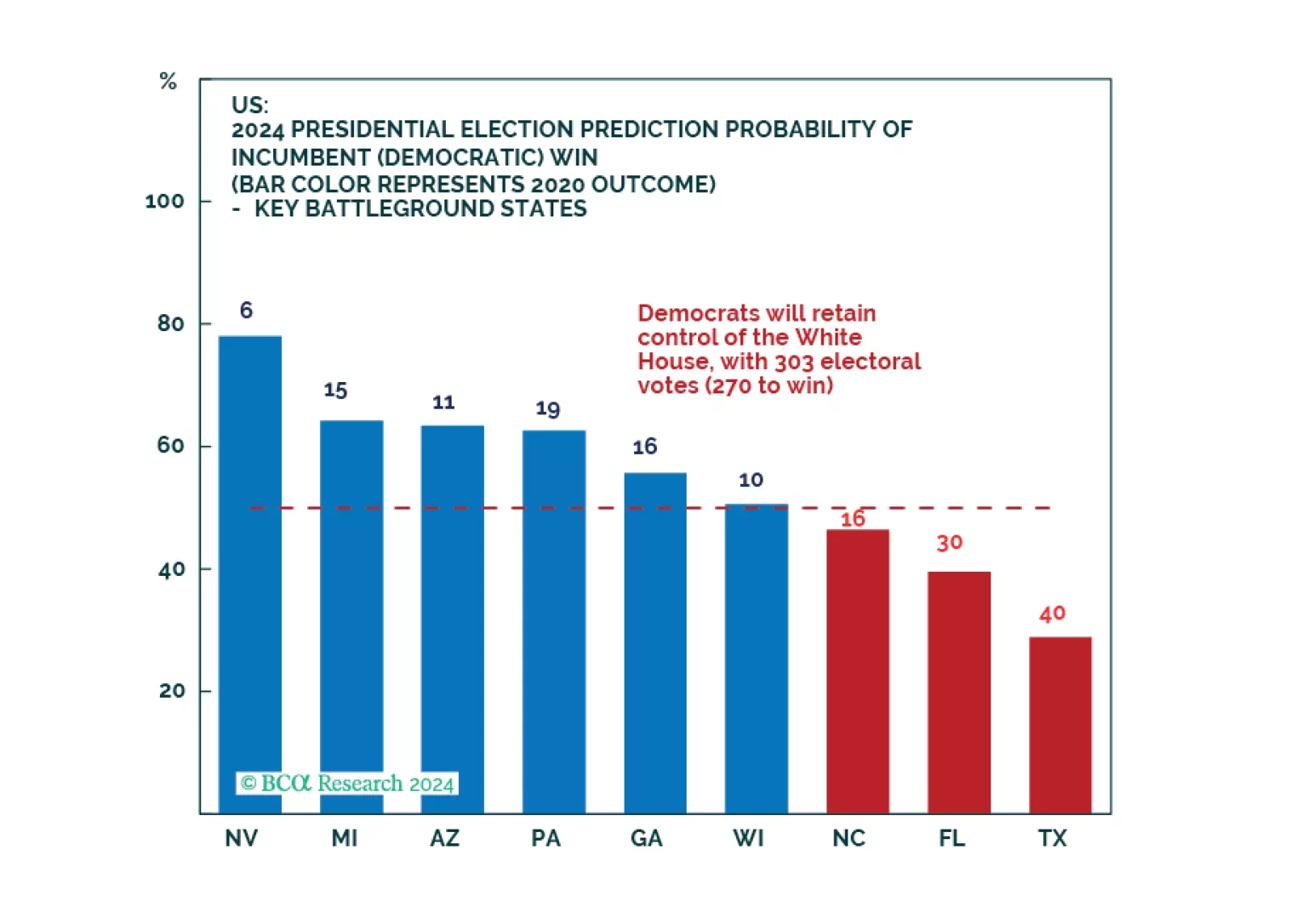

Democrats will not win a full sweep and implement drastic new tax hikes. However, our quant model still favors them to win the White House and just upgraded their odds. While we expect equity volatility around the election, investors do not need to worry about corporate tax hikes.

US nominal personal income growth accelerated from 0.2% m/m to 0.3% in July, faster-than-anticipated, whereas personal spending accelerated from 0.3% to 0.5%, in line with expectations. The savings rate edged lower from 3.1% to a 16-year-low of 2.9%. …

After surprising to the upside in July on higher energy costs, Eurozone CPI resumed its deceleration in August. Headline and core CPI declined from 2.6% y/y to 2.2% and from 2.9% to 2.8%, respectively. Energy prices contracted 0.3% y/y from July’s 1.2%…

Tokyo’s CPI is a timely leading indicator of nationwide price pressures. In August, the headline, core (ex-food) and the “core core” (ex-food and energy) measures all accelerated by larger-than-expected margins, reaching 2.6%, 2.4% and 1.6% y/y, respectively.…