Policy

The Bureau of Labor Statistics (BLS) revised down the number of workers on payrolls by 818 thousand over the twelve months period ending March 2024. This largest downward revision since 2009 thus implies that the labor market has been far less resilient than…

The DXY hit a 2024 low on Wednesday. The decline which totaled nearly 5% from its April highs, gathered pace this month (a 3% decline in August) when labor market worries spooked markets. The Fed had already telegraphed it was getting closer to cutting…

According to BCA Research’s Foreign Exchange Strategy service, the domestic economy does not really explain the recent weakness in the Norwegian krone. Some of this weakness can be attributed to structural and idiosyncratic factors, one being persistent…

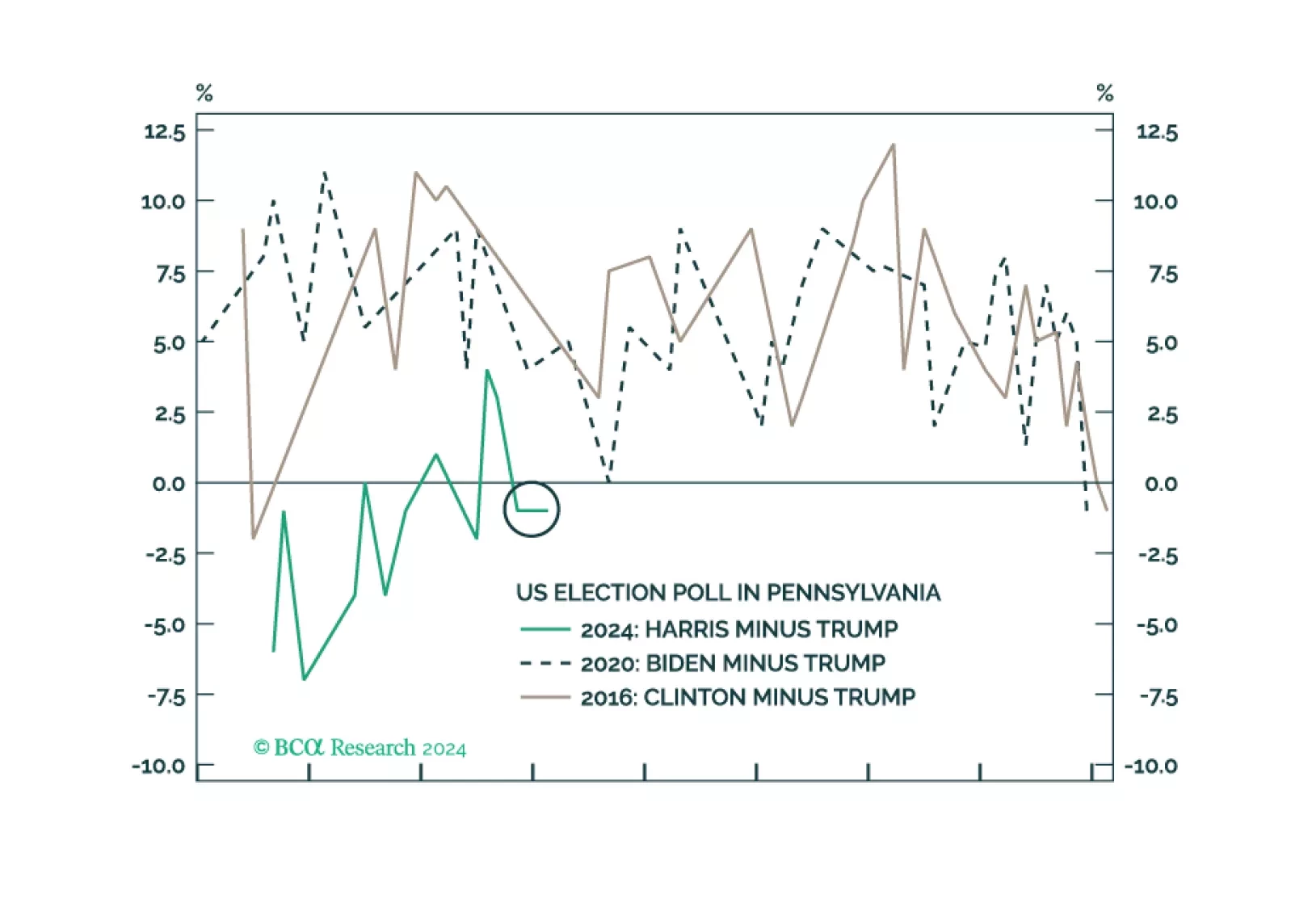

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

Canadian headline CPI decelerated from 2.7% y/y to 2.5% in July, the slowest pace in over 3 years. Notably, core median and trimmed-mean CPI eased further than expected, to 2.4% and 2.7% y/y respectively, 0.1 ppt below anticipations. Lower prices for…

In a widely expected move, the Riksbank lowered its policy rate from 3.75% to 3.5% in August. It had kept rates on hold in June, after having led many other major DM central banks in easing policy in May. The Riksbank also signaled it could cut as many as…

According to BCA Research’s US Investment Strategy and US Bond Strategy services, the drivers of the structural downtrend in real interest rates include: demographic trends (declining fertility rates, longer life expectancy and a rising dependency…

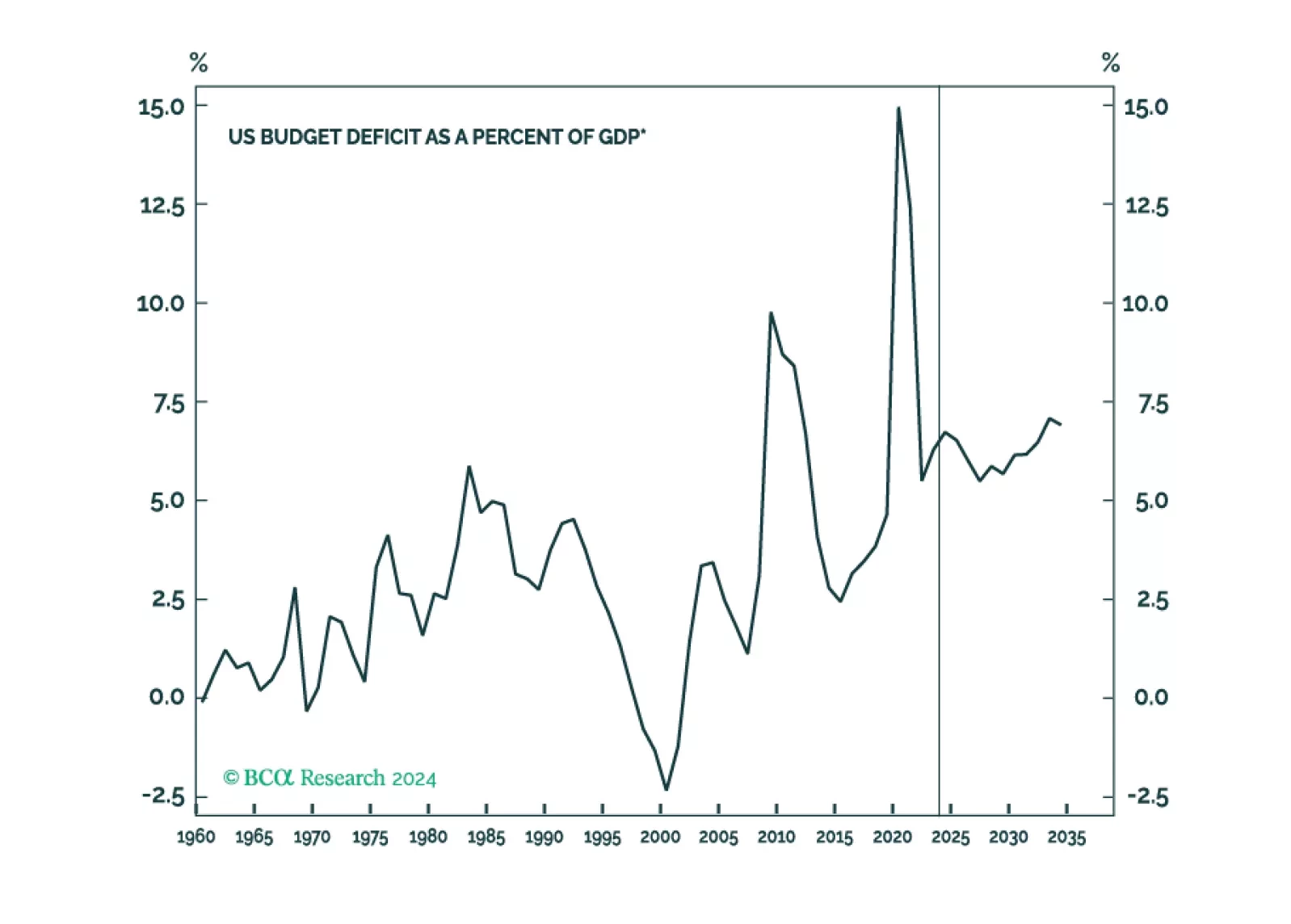

The US fiscal outlook is more unappetizing than it was before the pandemic, but we are not convinced that a difficult day of reckoning awaits. A Treasury market crisis is conceivable, but it is far from inevitable.

Housing starts and permits both disappointed in July. New construction contracted 6.8% m/m, from a 1.1% expansion in June. Permits, which typically lead housing starts, declined 4.0% m/m in July from 3.9% growth in the previous month. Concurrently, the NAHB…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. They rebounded sharply in July from a previous contraction, largely exceeding expectations. Notably,…