Policy

According to BCA Research’s GeoMacro Strategy service, while the idea that Donald Trump would allow China to build factories in the US does not mesh with the contemporary media narrative, it would fit the historical track record. The last time that the US had…

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

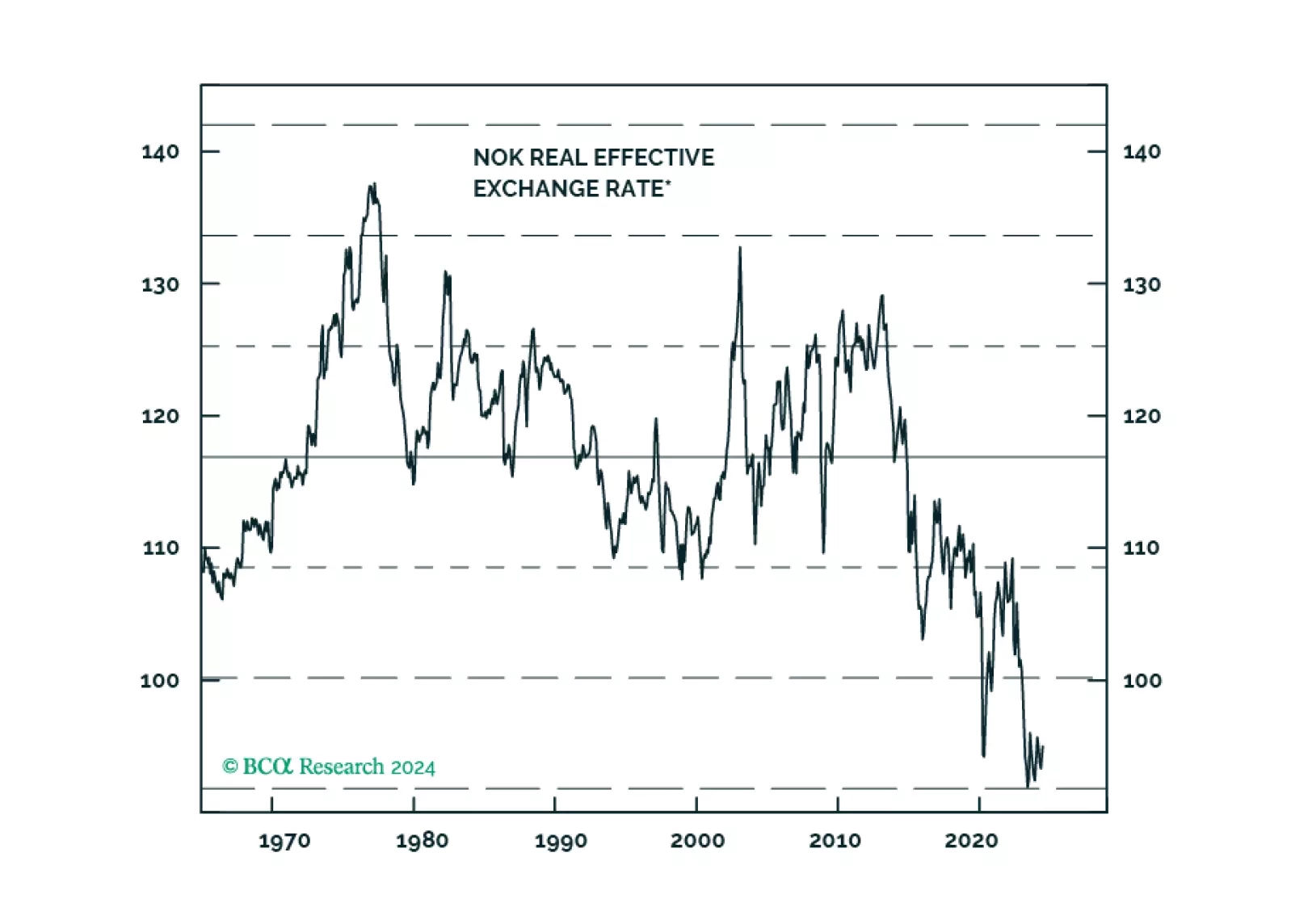

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

US industrial production fell by a larger-than-expected 0.6% m/m in July, the largest monthly decline so far this year. Capacity utilization also decreased a full percentage point to 77.8% Although Hurricane Beryl distorted these nationwide July numbers,…

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

Headline and core CPI eased for the fourth consecutive month in July, ticking down 0.1 ppt to 2.9% and 3.2% y/y, respectively. The 3-month and 6-month moving averages continued to edge lower as a result, with the former now reaching a three-and-half-year low…

The Reserve Bank of New Zealand unexpectedly embarked on an easing pivot in August, cutting the Official Cash Rate by 25 bps to 5.25%. The central bank also signaled further rate cuts by lowering its rate benchmark forecast to 4.92% by December 2024 and 3.85%…

Goods prices have normalized following the pandemic binge on goods spending and have contributed to easing price pressures overall. A large drop in vehicle prices largely drove the decrease in July’s CPI and we have questioned the sustainability of an…

According to BCA Research’s Geopolitical Strategy service, US policy will have an impact on China’s willingness to adopt a preemptively hawkish foreign policy. But the US is in the middle of a chaotic election that marks the climax of a historic populist…

Subdued demand for credit among Chinese private-sector businesses and households persisted through July. Aggregate financing missed expectations, growing CNY 0.8bn to CNY 18.9bn in July on a YTD basis. New loans grew CNY 0.2bn to CNY 13.5bn, below the CNY…