Policy

Eurozone headline CPI inflation unexpectedly accelerated in July, from 2.5% y/y to 2.6%. Core CPI remained stable at 2.9% despite expectations it would ease. EU Harmonized CPI accelerated in the regions’ three largest economies, surprising by a large margin…

FOMC members unanimously voted in favor of keeping rates on hold in July but signaled that a September cut is on the table. Inflationary pressures have indeed continued to ease over the past several months. Notably, the Employment Cost Index (ECI) – the…

The Bank of Japan hiked its policy rate by 15 bps from 0.10% to 0.25% on Wednesday, and announced further quantitative tightening, reducing its pace of monthly bond buying from JPY 6 trillion to JPY 3 trillion. While the central bank had previously…

The Fed kept rates steady today, but teed up an initial rate cut in September while putting more emphasis on the employment side of its dual mandate.

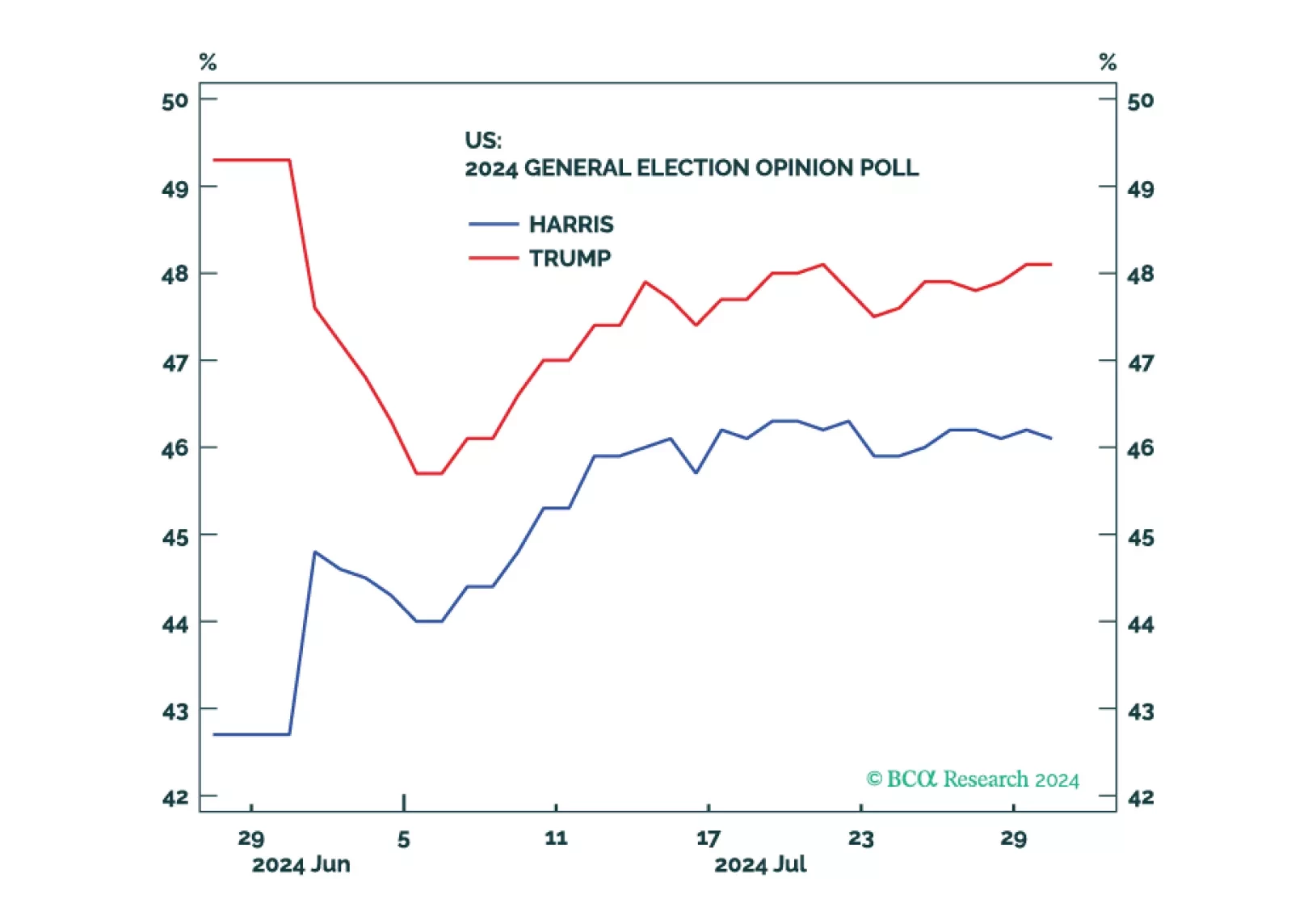

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

Eurozone GDP surprised to the upside in Q2, growing by 0.3% q/q annualized against expectations of 0.2%. Stronger-than-expected expansions in France (0.3% q/q vs 0.2%) and Spain (0.8% q/q vs 0.5%), as well as steady growth in Italy (0.2% q/q), offset a…

Historically, interest-rate sensitive sectors such as financials and real estate have tended to post the highest returns in the 3 months preceding the first Fed rate cut. Interestingly, industrials, typically a deep cyclical sector, have also tended to post…

Preliminary estimates suggests that the Swedish economy unexpectedly contracted in Q2. The seasonally adjusted GDP Indicator declined by 0.8% q/q, following a 0.7% Q1 rise in actual GDP growth. Flash estimates lack details and are prone to revisions.…

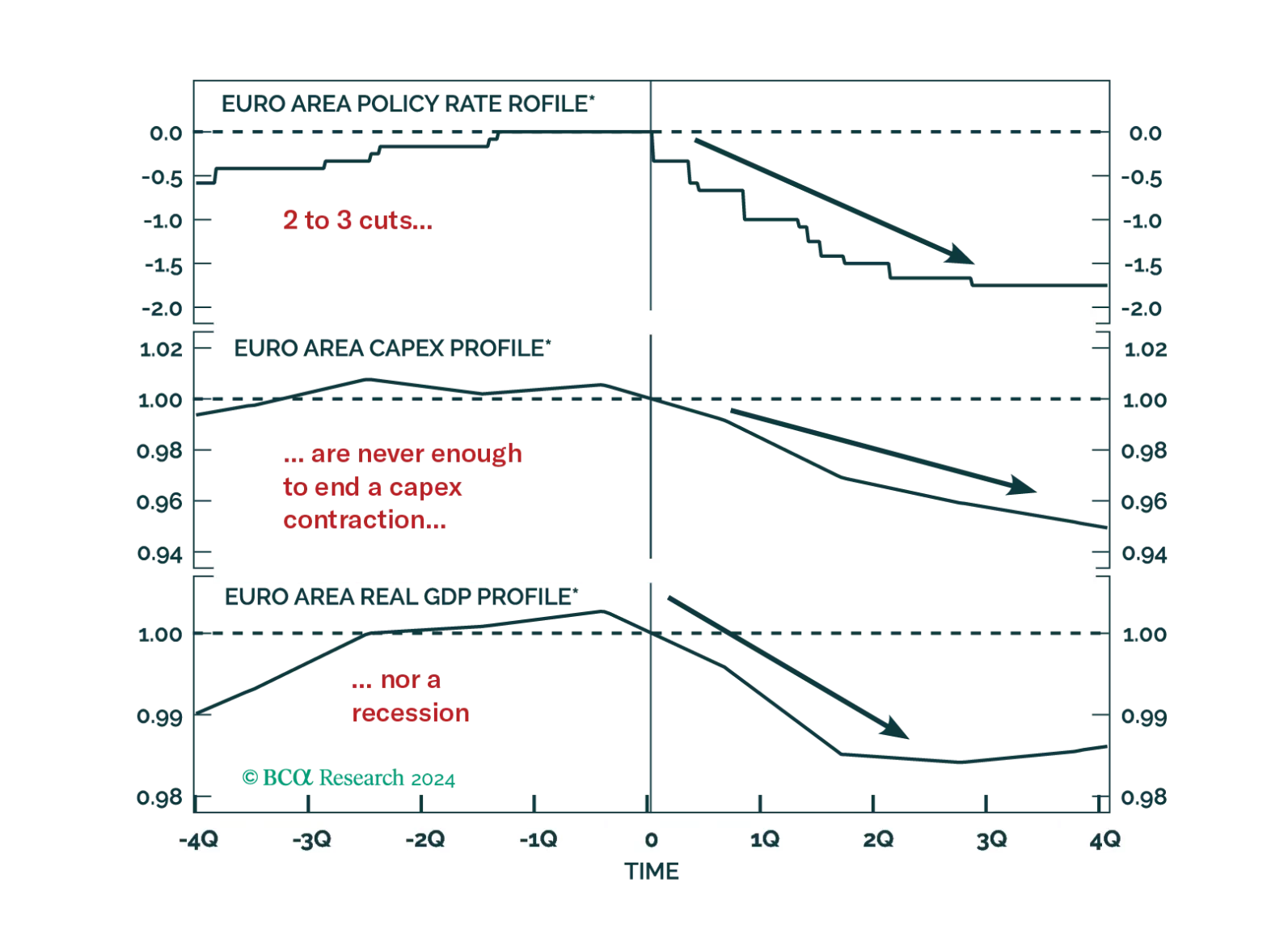

According to BCA Research’s European Investment Strategy service, a foreign shock is likely to tip the Eurozone economy into a recession because important vulnerabilities have emerged domestically. Policy is restrictive. Real interest rates stand 370bps…

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?