Policy

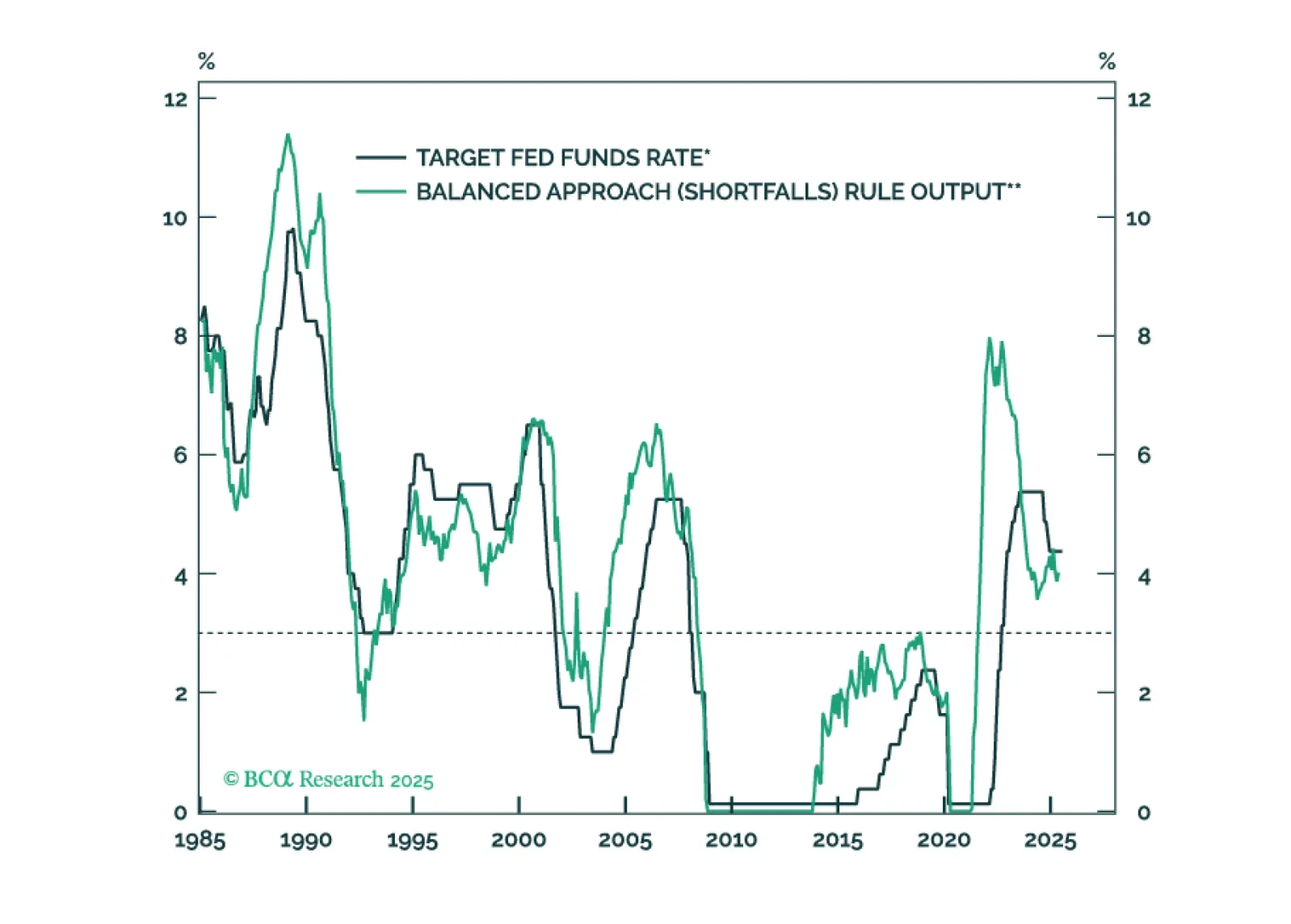

The Fed will keep rates on hold until the unemployment rate forces its hand.

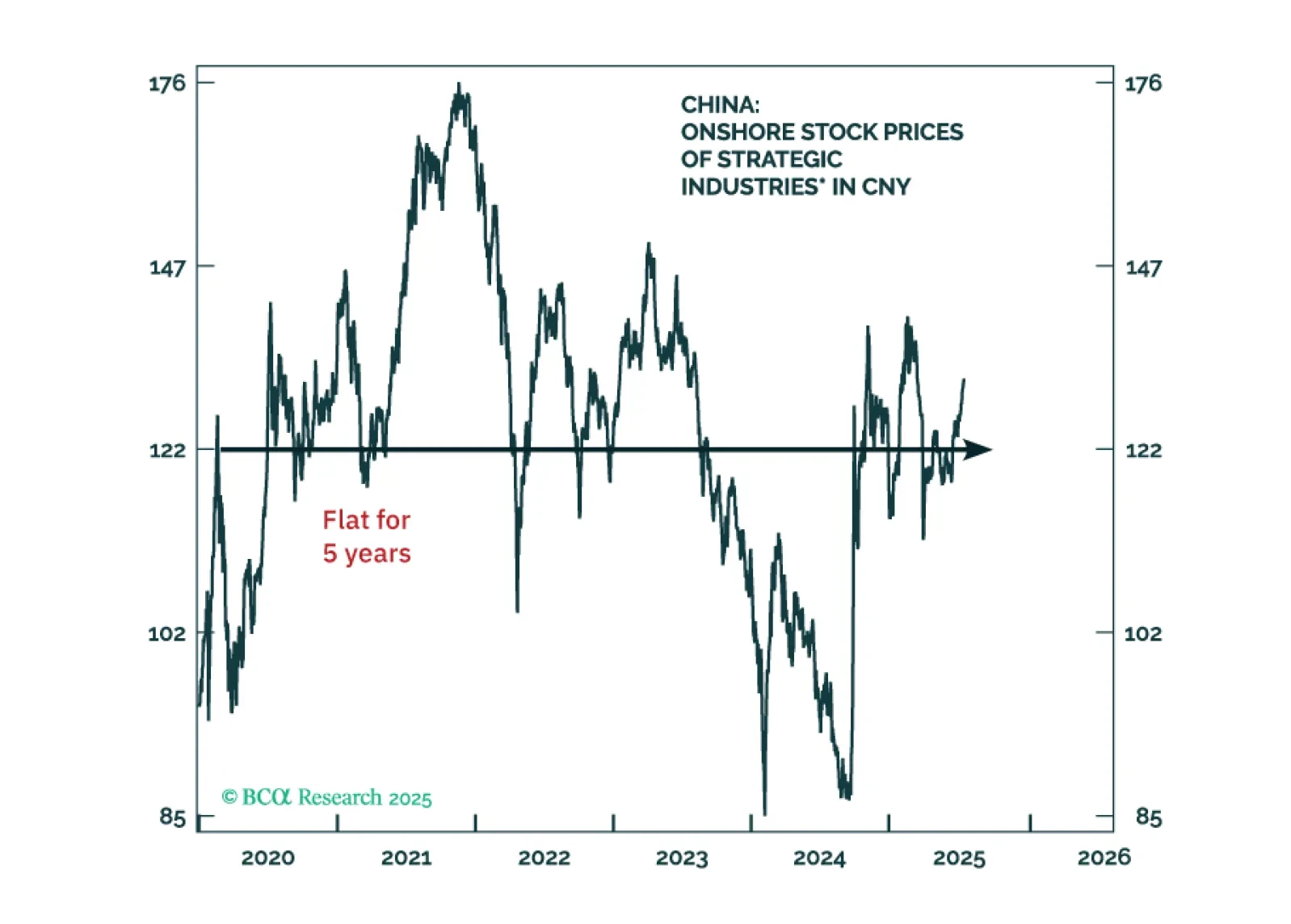

Investors often ask us which industries the Chinese government is prioritizing for expansion. The assumption is that investing in sectors hand-picked authorities will produce solid investment returns. Yet, this assumption has not held over the past decade.

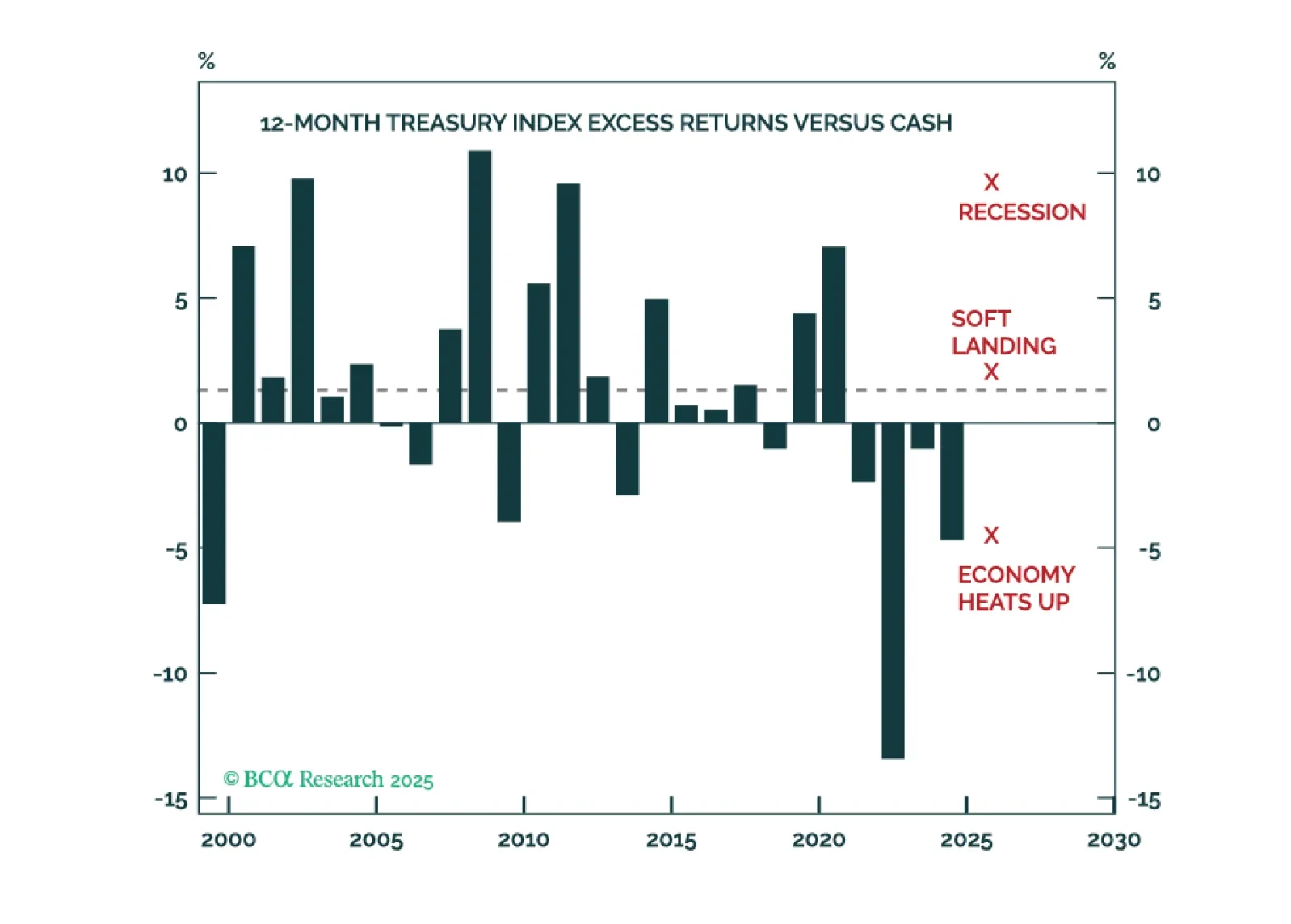

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

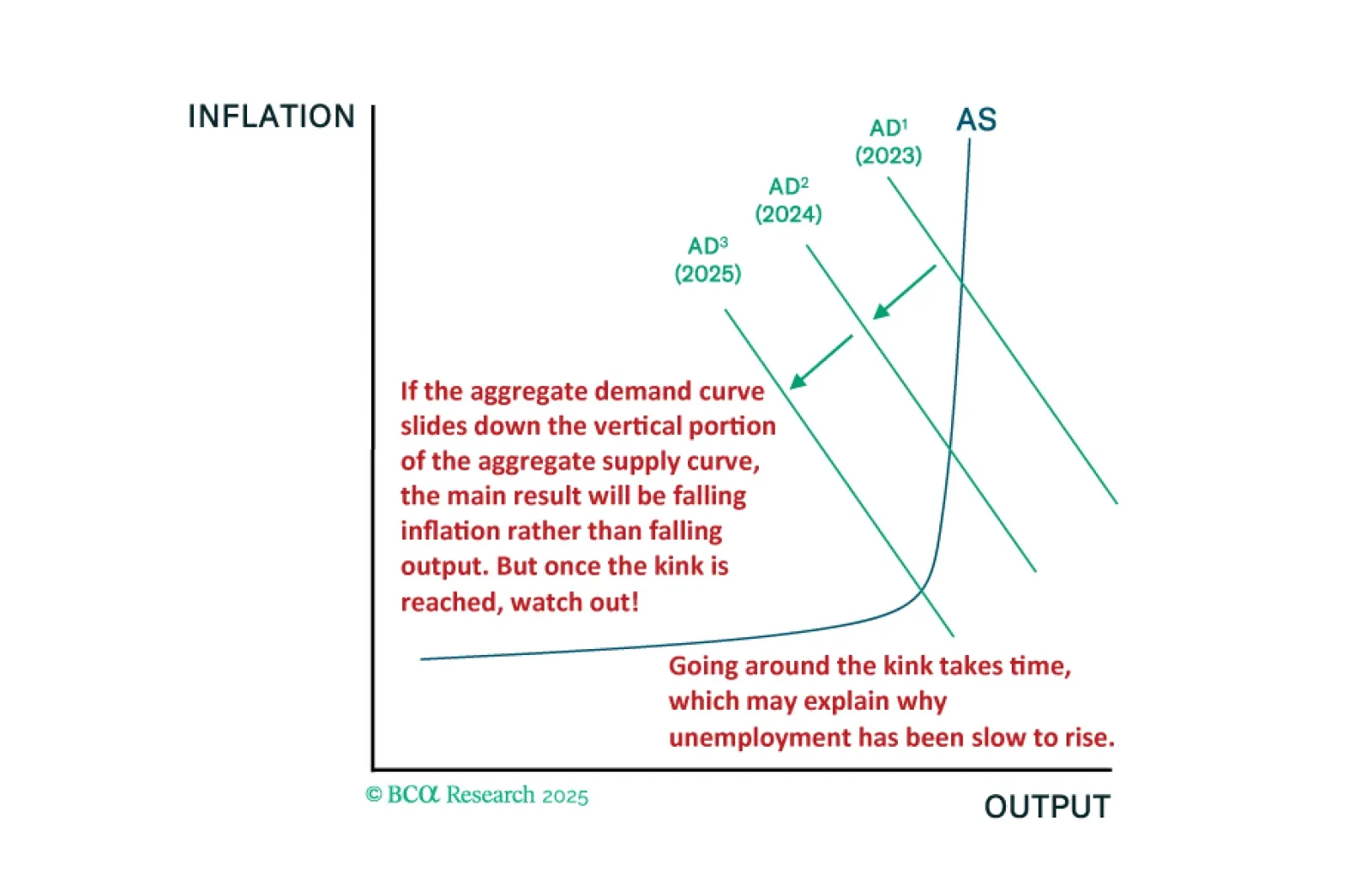

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

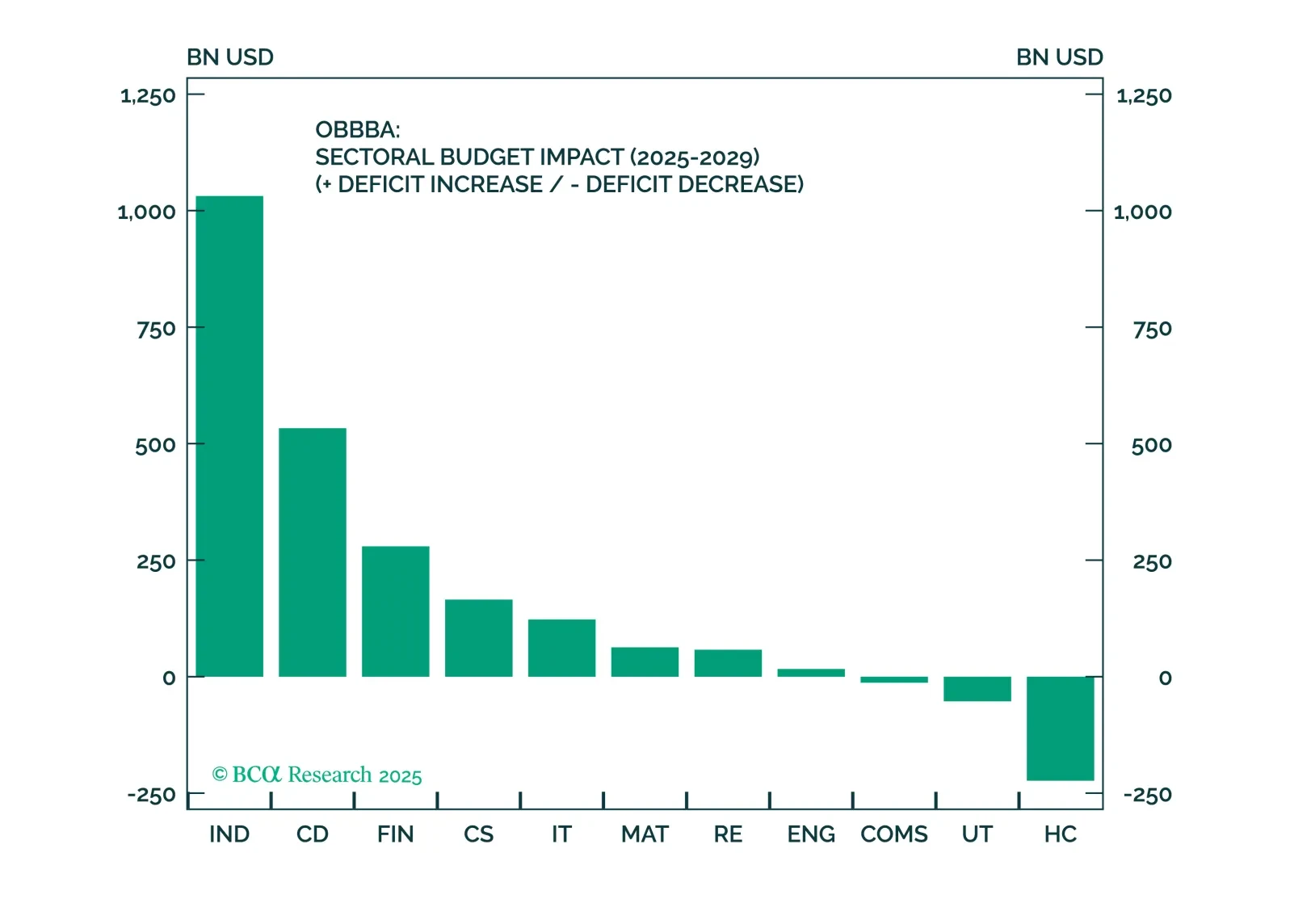

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

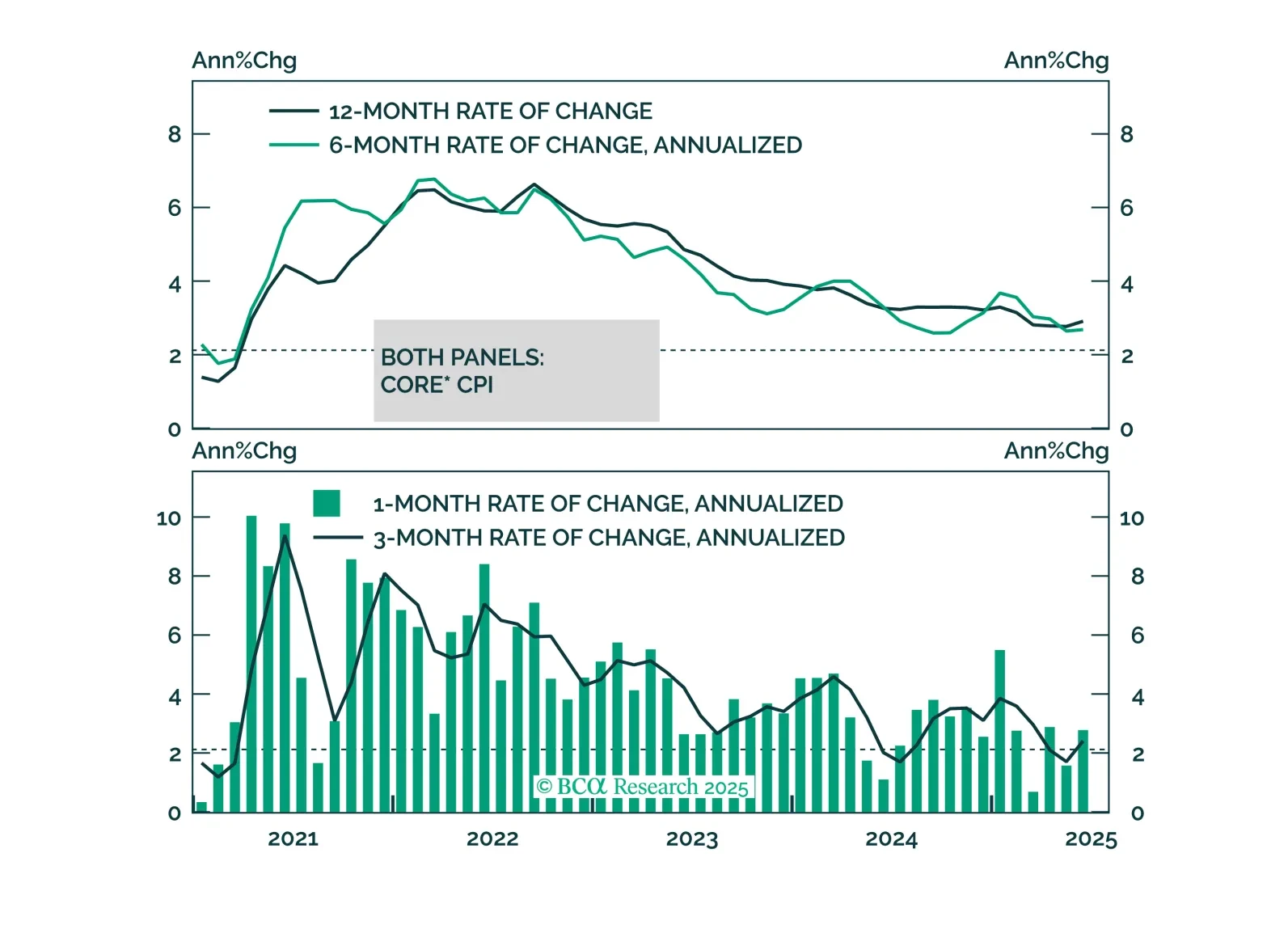

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.