Policy

We look at the implications a various European central bank meetings this week, for currency strategy.

In a widely expected move, the Bank of England (BoE) kept its policy rate unchanged at 5.25% in June. Although MPC members voted seven-to-two in favor of not cutting rates, a tweak in communication noting that the decision was “finely balanced”, hinted at the…

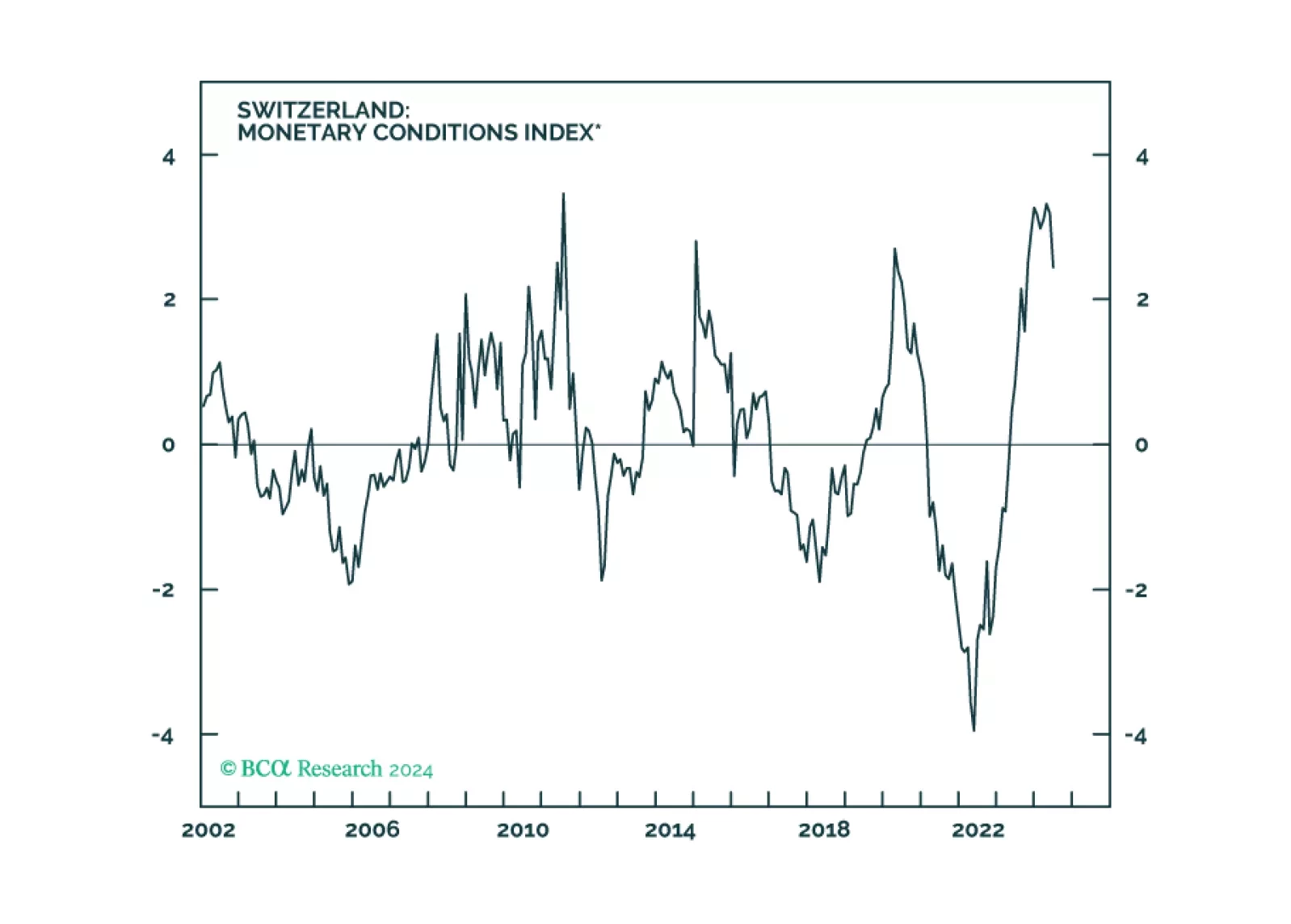

The Swiss National Bank (SNB) was the first major central bank to embark on a dovish pivot back in March. It lowered borrowing costs Thursday for a second consecutive meeting, from 1.5% to 1.25%, despite expectations that it would hold the policy rate…

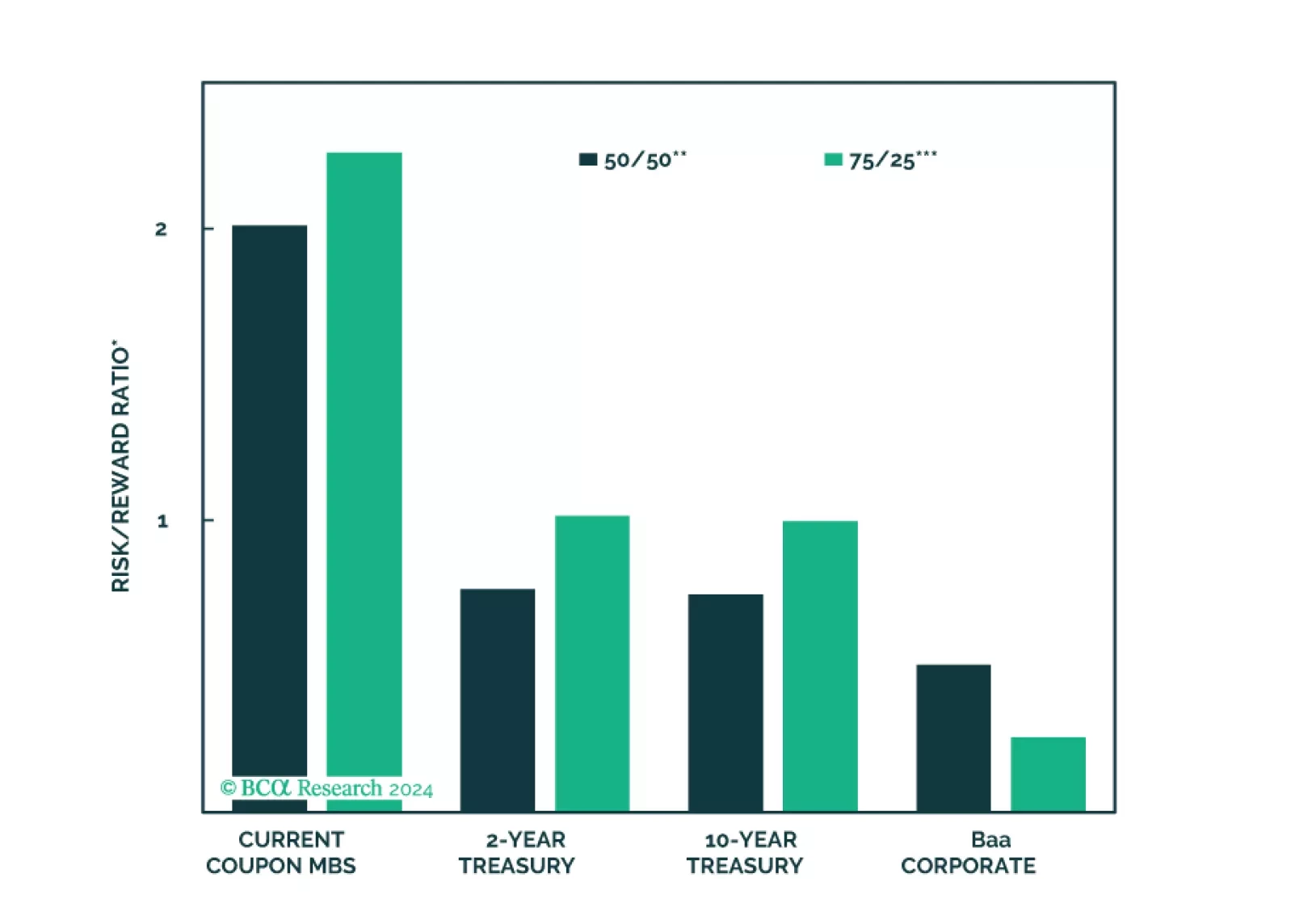

In its latest Special Report, BCA Research’s US Bond Strategy service considers the relative merits of four different fixed income investments in the current economic environment: 2-year Treasuries, 10-year Treasuries, Baa-rated corporate bonds and current…

We consider the relative merits of four different fixed income investments in the current economic environment: 2-year Treasuries, 10-year Treasuries, Baa-rated corporate bonds and current coupon Agency MBS.

On the surface, UK inflation appears to be on the right track. The May CPI release came in broadly within expectations. Headline inflation eased from 2.3%y/y to 2.0%y/y – directly on the BoE’s target for the first time since July 2021. Core CPI (excluding…

The ECB delivered its first rate cut in June, moderating the degree of restriction rather than pivoting outright to easy monetary policy settings. Indeed, the rate cut was accompanied by an upward revision of inflation and growth forecasts. Since then,…

According to BCA Research’s China Investment Strategy service, Beijing will engage in ongoing negotiations with the EU regarding its import tax decision rather than impose meaningful retaliatory measures. The EU and China appear to be negotiating ahead of…

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

The Reserve Bank of Australia kept its cash rate at 4.35% at its policy meeting on Tuesday, in line with market expectations. Australia’s monthly measure of headline inflation came in at 3.6% in April, still considerably above the midpoint of the RBA’s 2-3%…