Policy

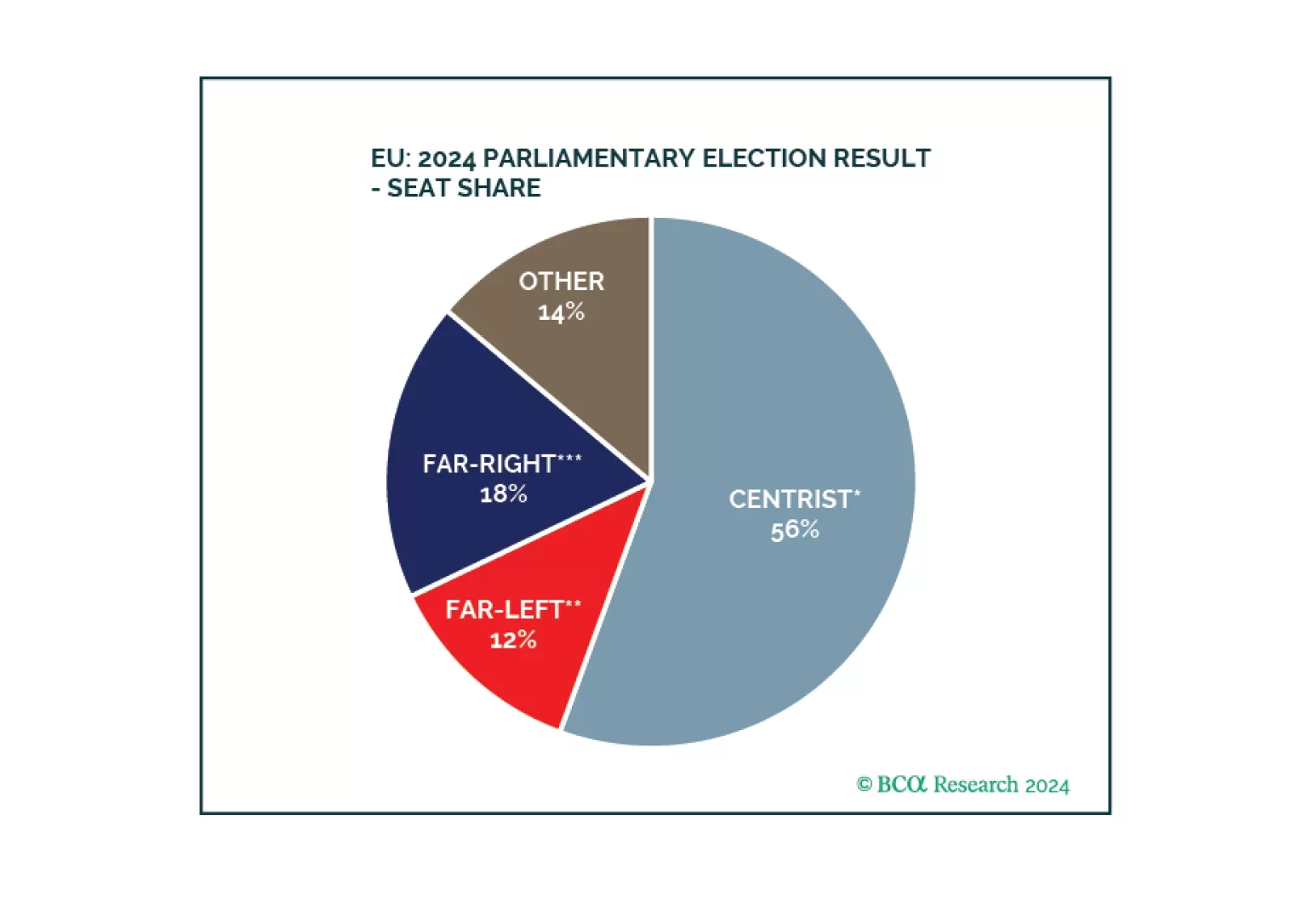

Europe did not witness a major policy reversal. Inflationary pressures are coming down, enabling the ECB to cut rates and European states to maintain soft budgets. Geopolitical challenges ensure that European parties continue to cooperate on national defense, economic security, and energy security.

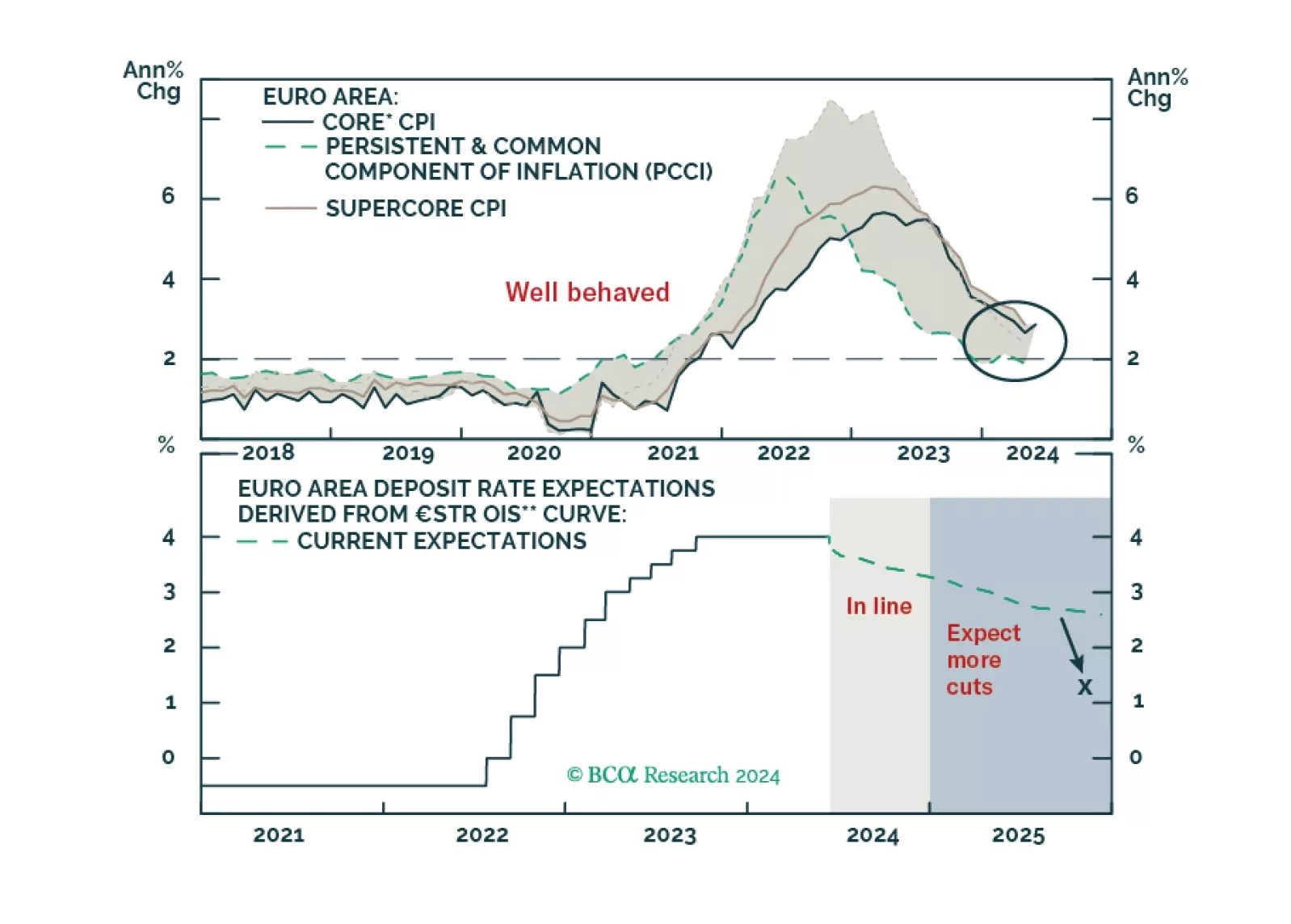

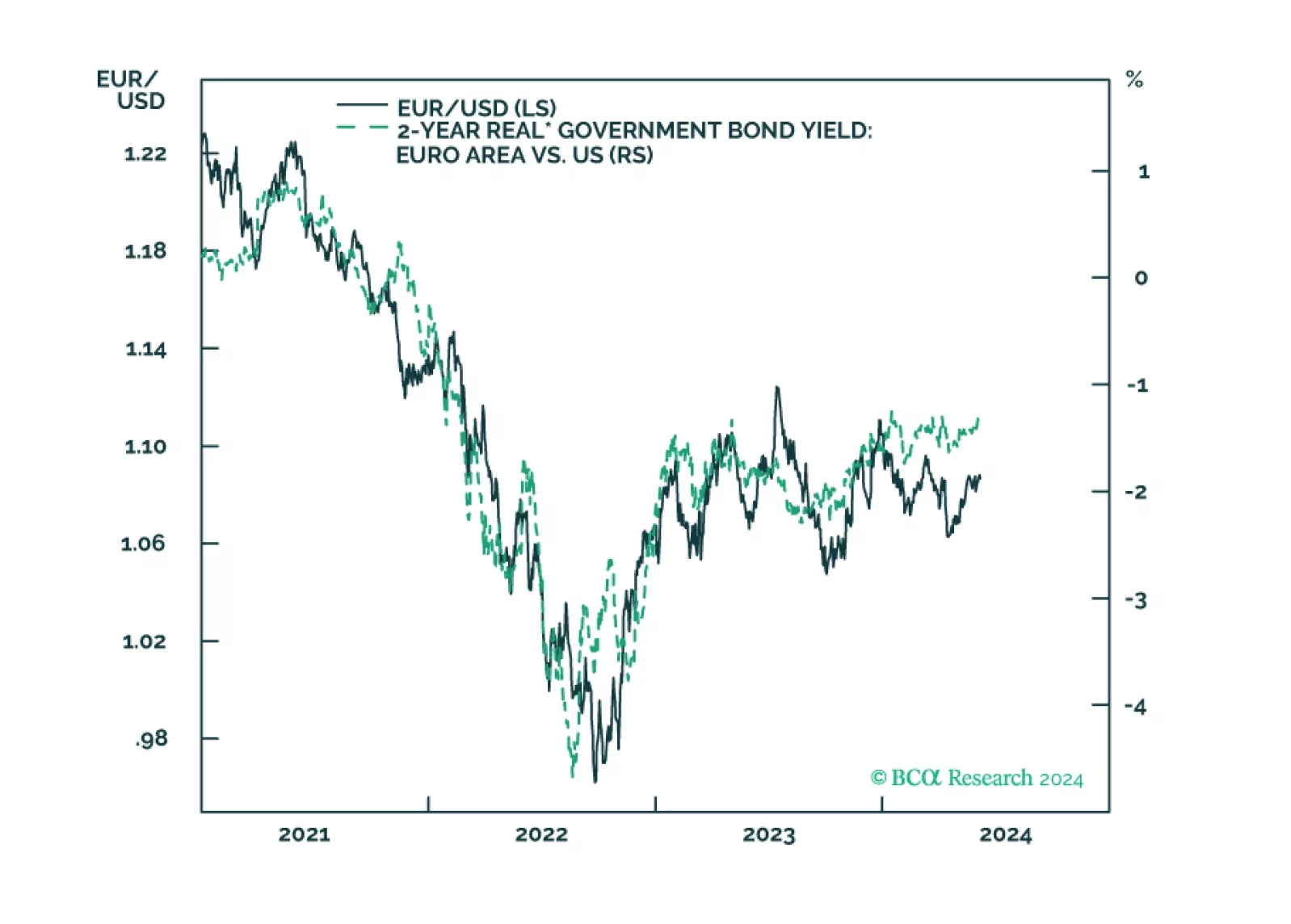

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

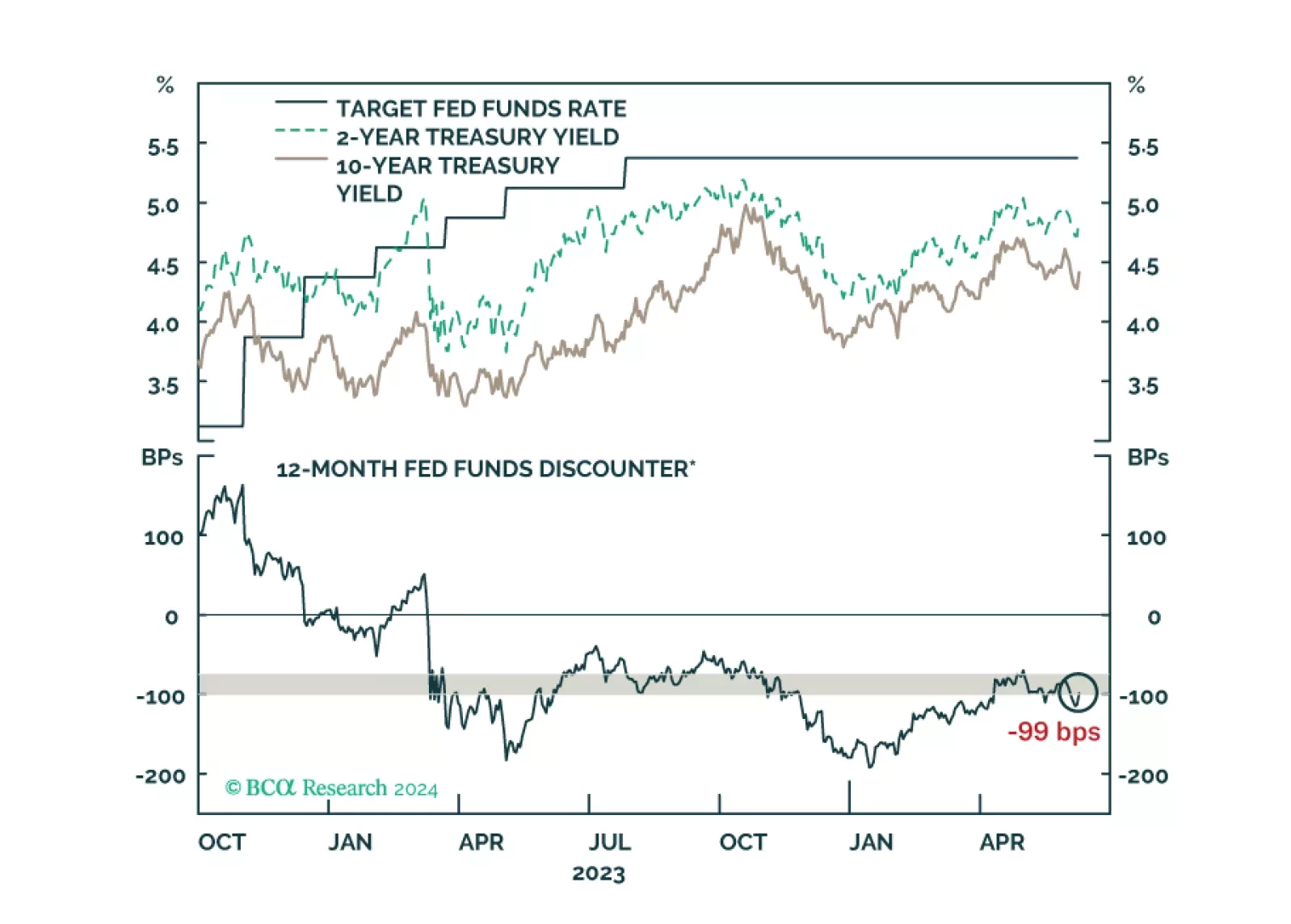

US Treasury yields bounced after this morning’s employment report. We offer our updated views about how long the recent trading range will hold.

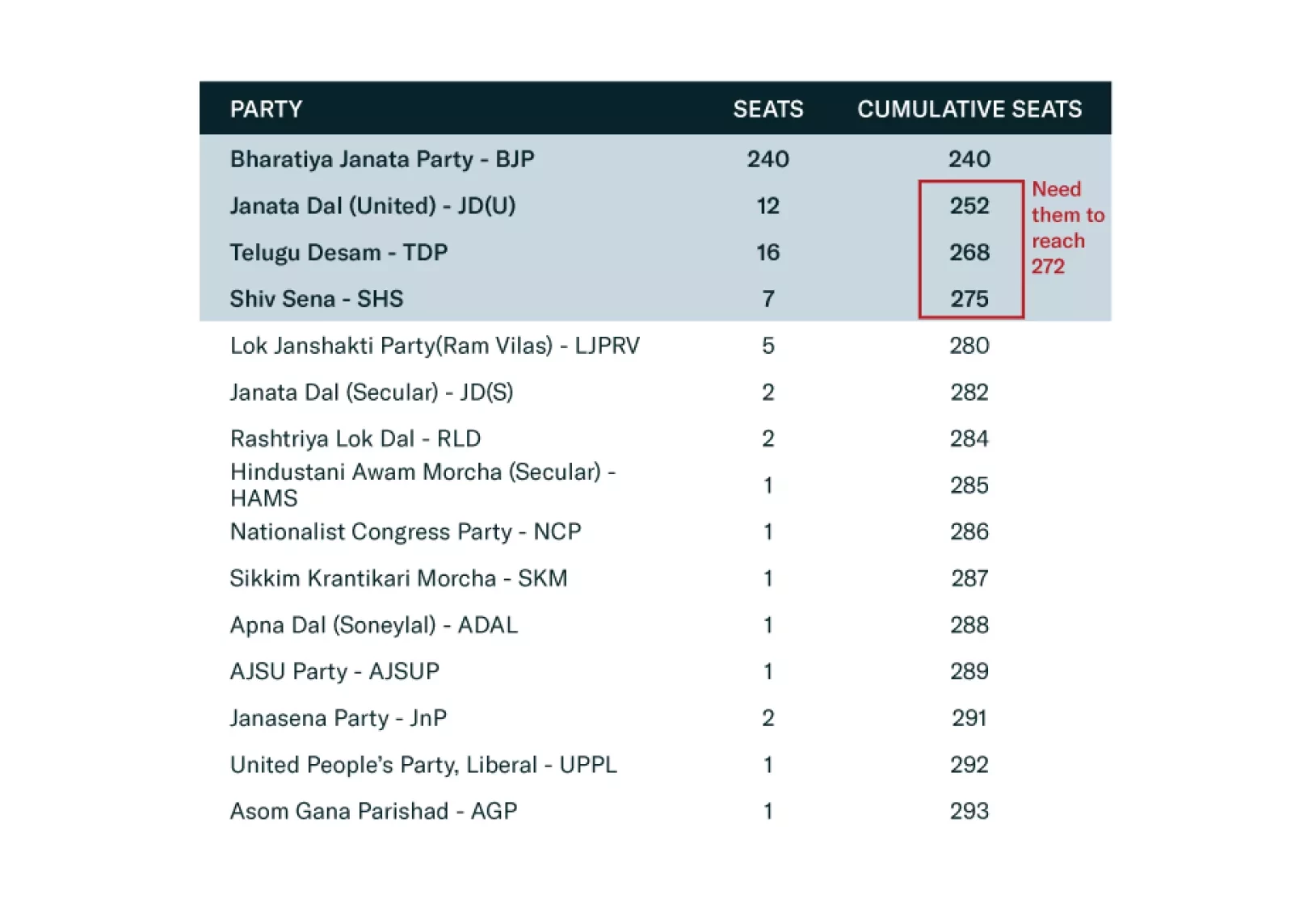

Prime Minister Narendra Modi won a third term and will become the third longest-serving prime minister of India. While investors responded negatively to the BJP’s loss of an outright majority, Modi and the NDA will continue to perpetuate the reforms they have already put into motion. The result also affirms that Indian democracy continues to thrive, contrary to the narrative that Modi had formed an authoritarian grip on the country, a view we always rejected.

A short insight on the ECB and near-term implications for European asset markets.

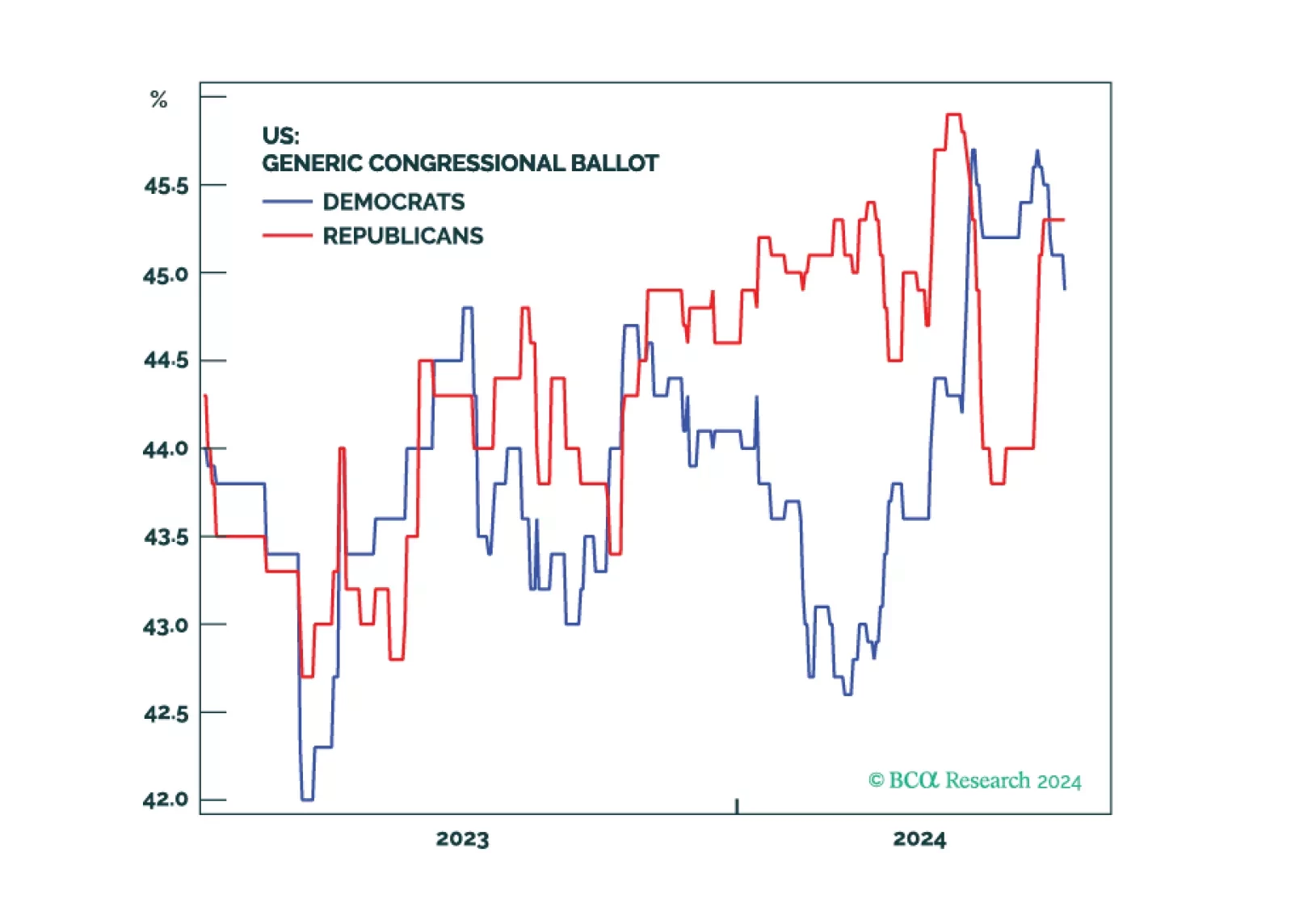

Republicans are favored in the House and Senate even if they do not win the White House. A Democratic sweep is a 20% risk. The policy implication would be inflationary, but not so much as under a Republican sweep. Election uncertainty should increasingly weigh on cyclical and high-beta assets in the second half of 2024.

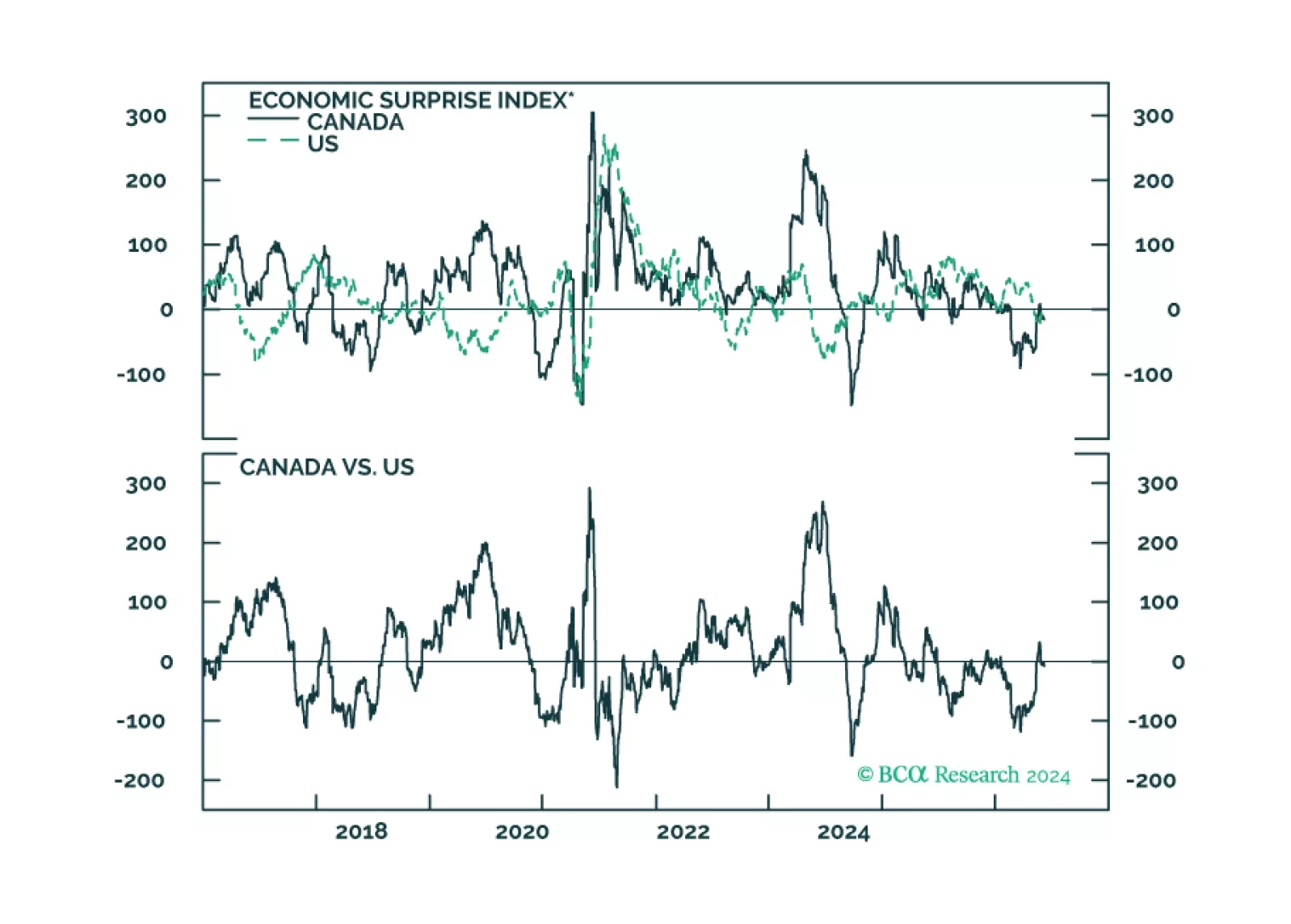

In this insight, we provide an update on the Canadian economy, given yesterday’s rate cut, and implications for Canadian assets.