Policy

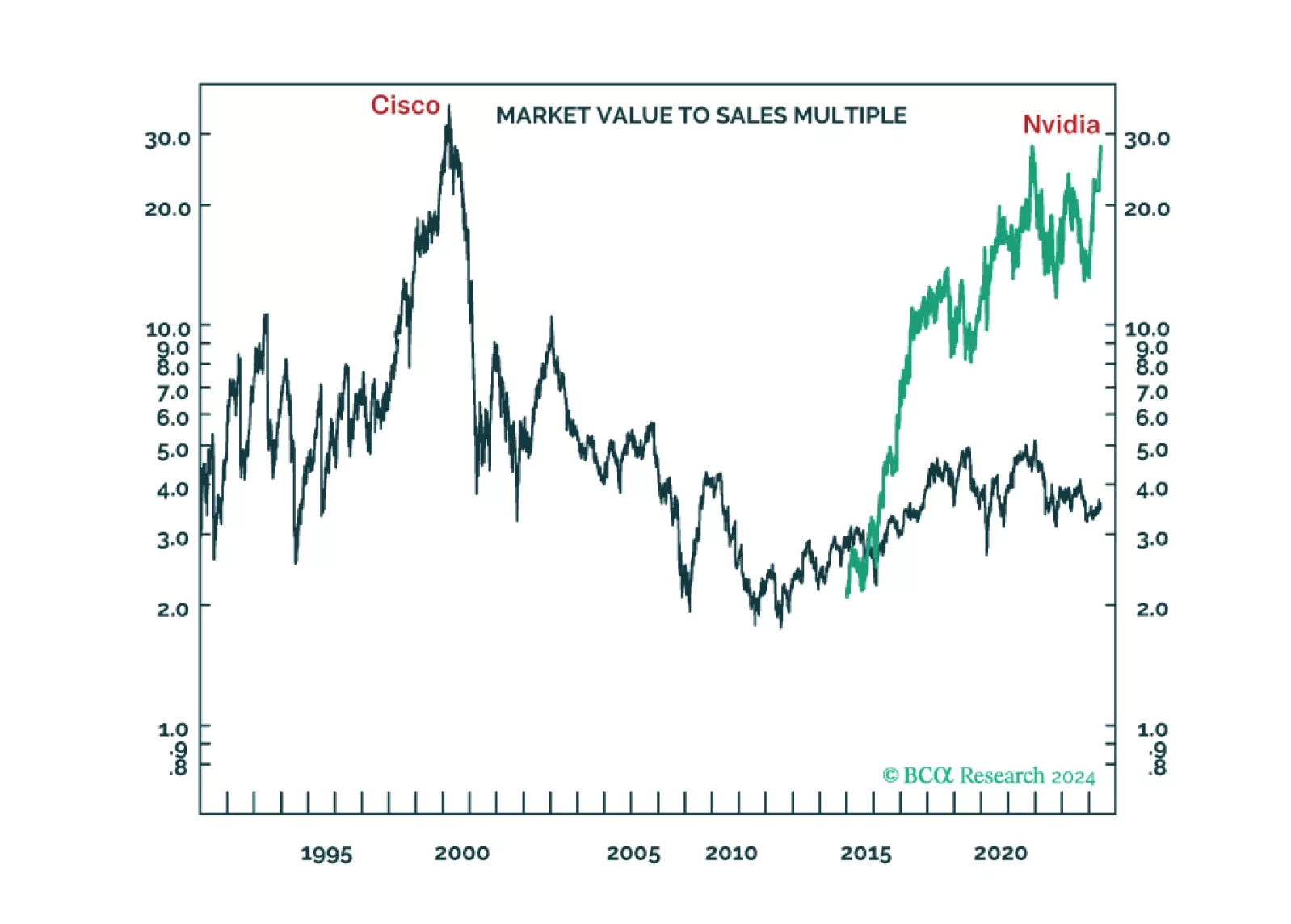

The long-term winners from the generative-AI gold rush are unlikely to be the ‘picks and shovels’ stock Nvidia or the overvalued US superstars of Web 2.0. We discuss the structural investment implications. Plus: time to go tactically overweight global consumer discretionary (RXI).

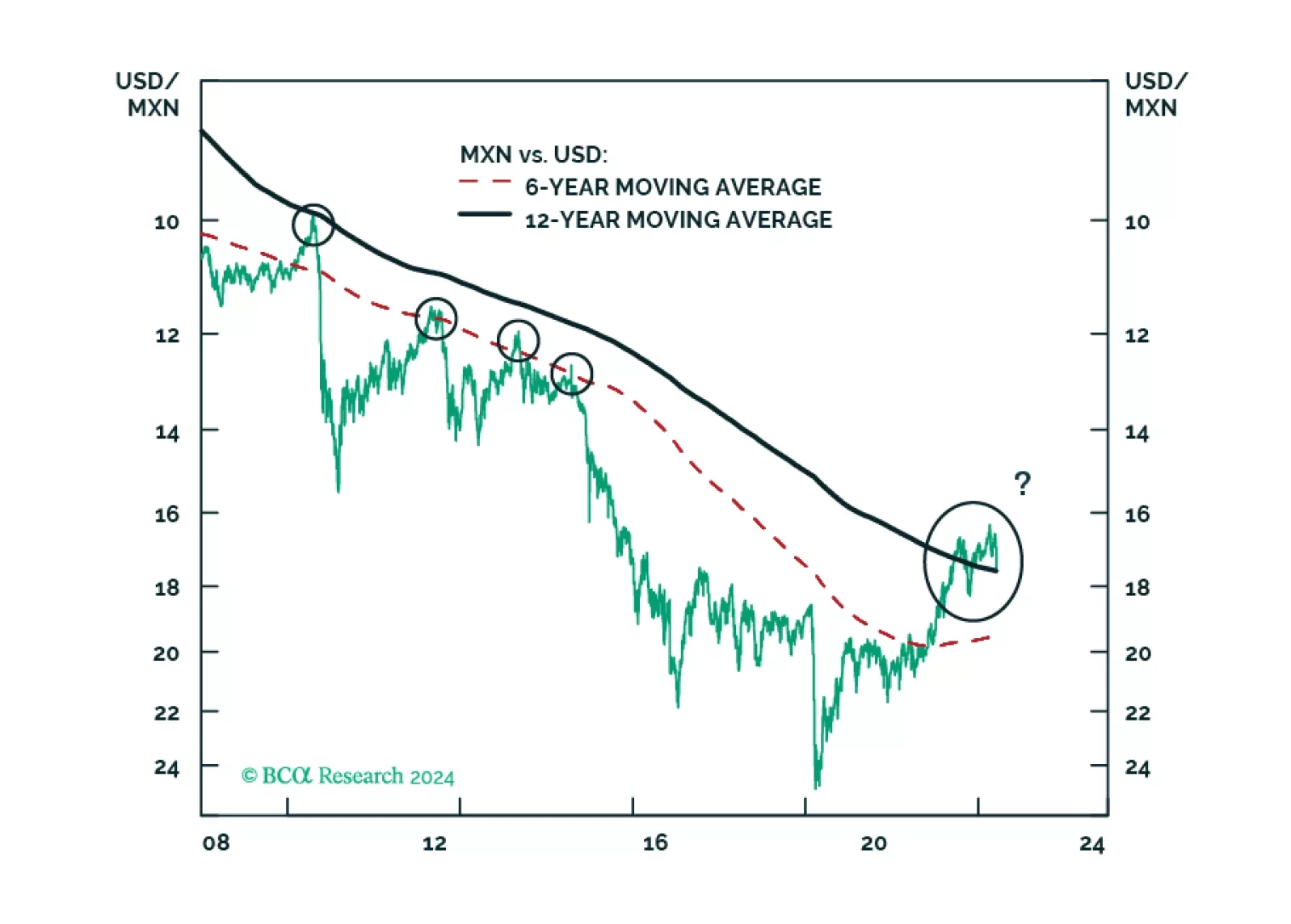

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

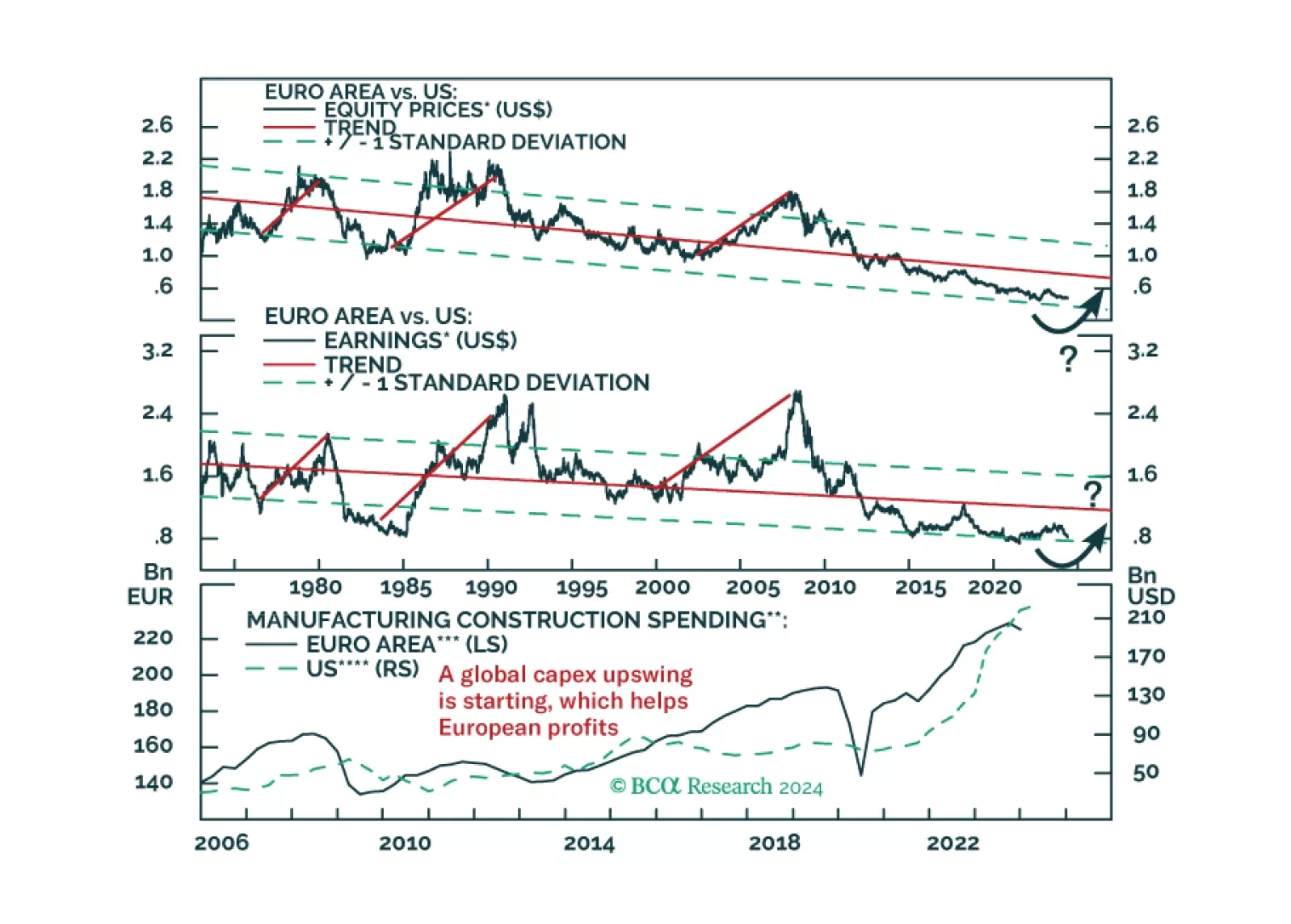

European stocks have massively underperformed US ones since the GFC. Demographics and productivity say this trend will continue, but is that really so?

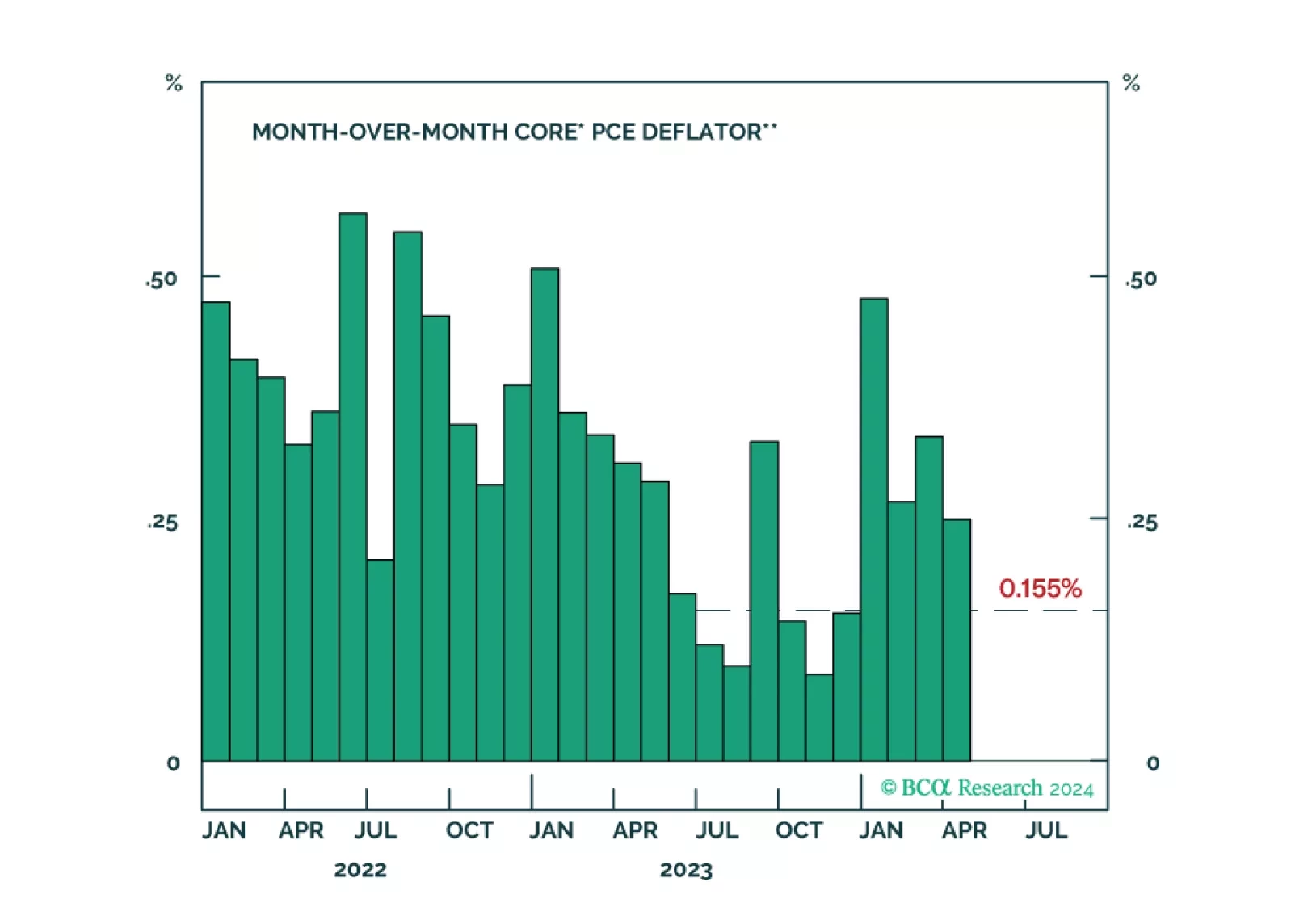

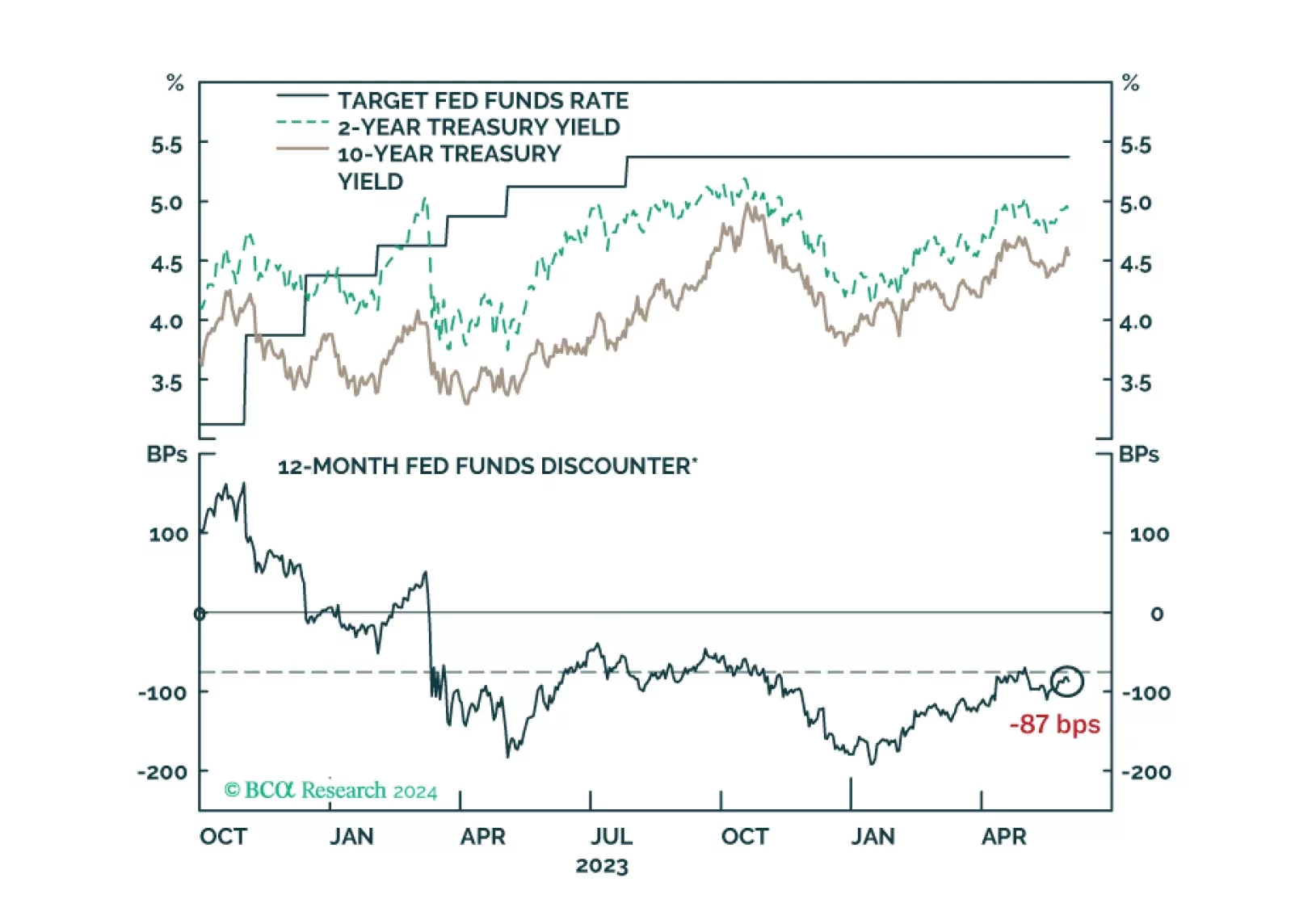

We comment on whether Treasury market valuation is sufficiently attractive to get long bonds and consider some of the common arguments for why yields may yet make new highs.