Policy

Mainland residents’ investments in gold, other metals, and Hong Kong-traded stocks are a form of capital outflow. Chinese authorities will counter any excessive capital flight with stricter administrative controls. Thus, markets benefiting from these flows will likely be hurt.

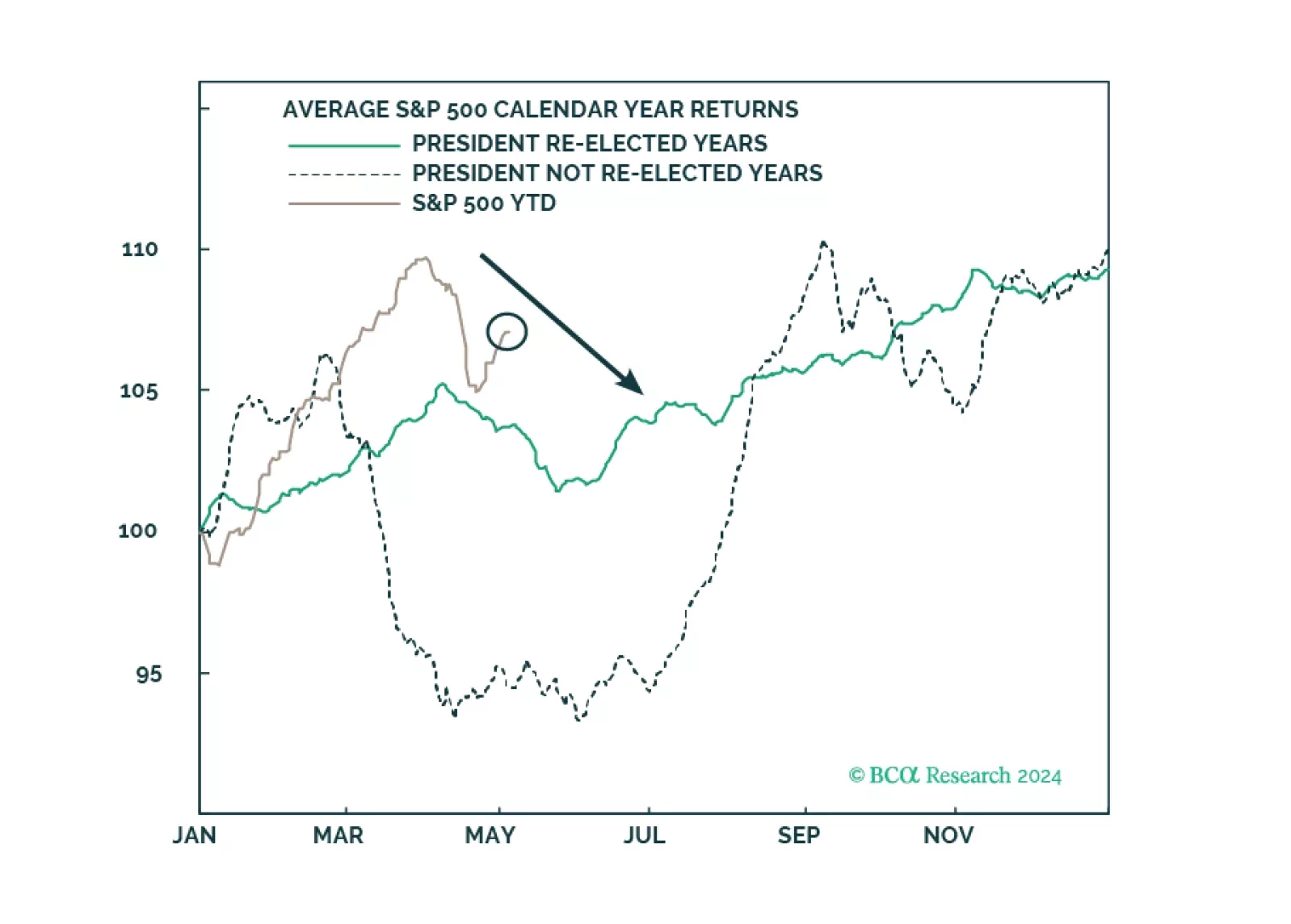

Investors should prepare for economic data to weaken even as policy uncertainty and geopolitical risk skyrocket ahead of the US election.

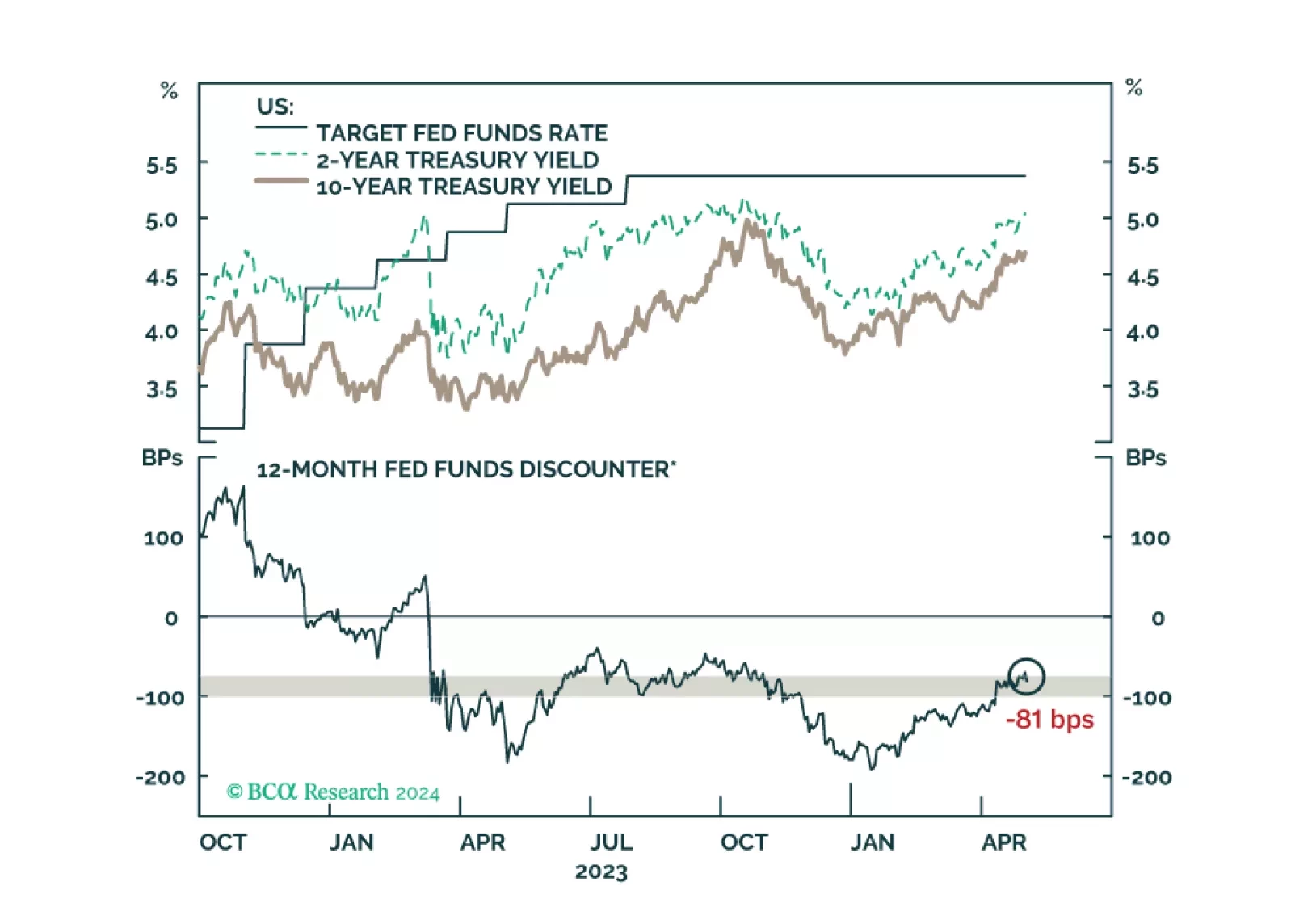

Updated views on US Treasury yields and the dollar following today’s FOMC meeting.

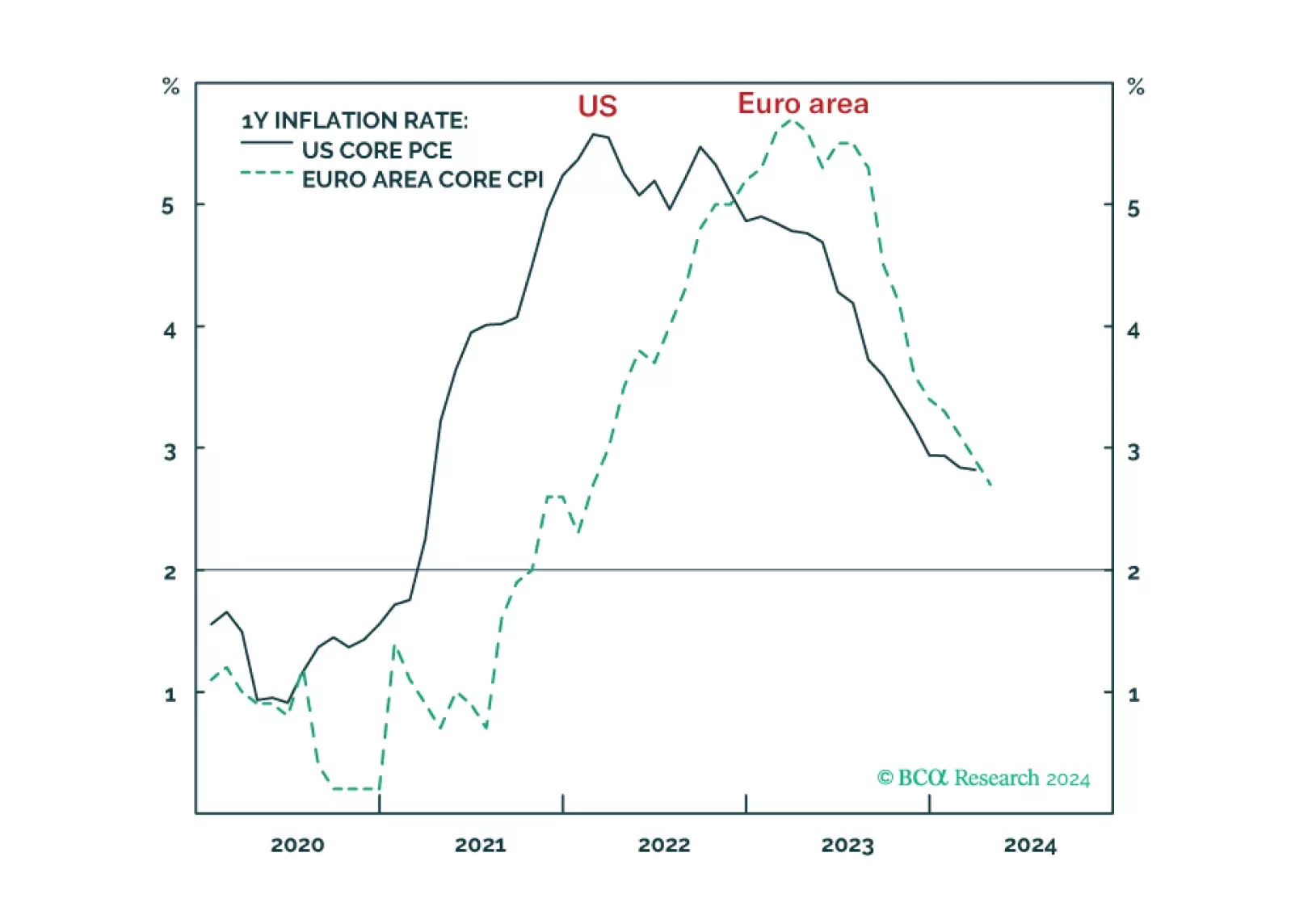

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.