Policy

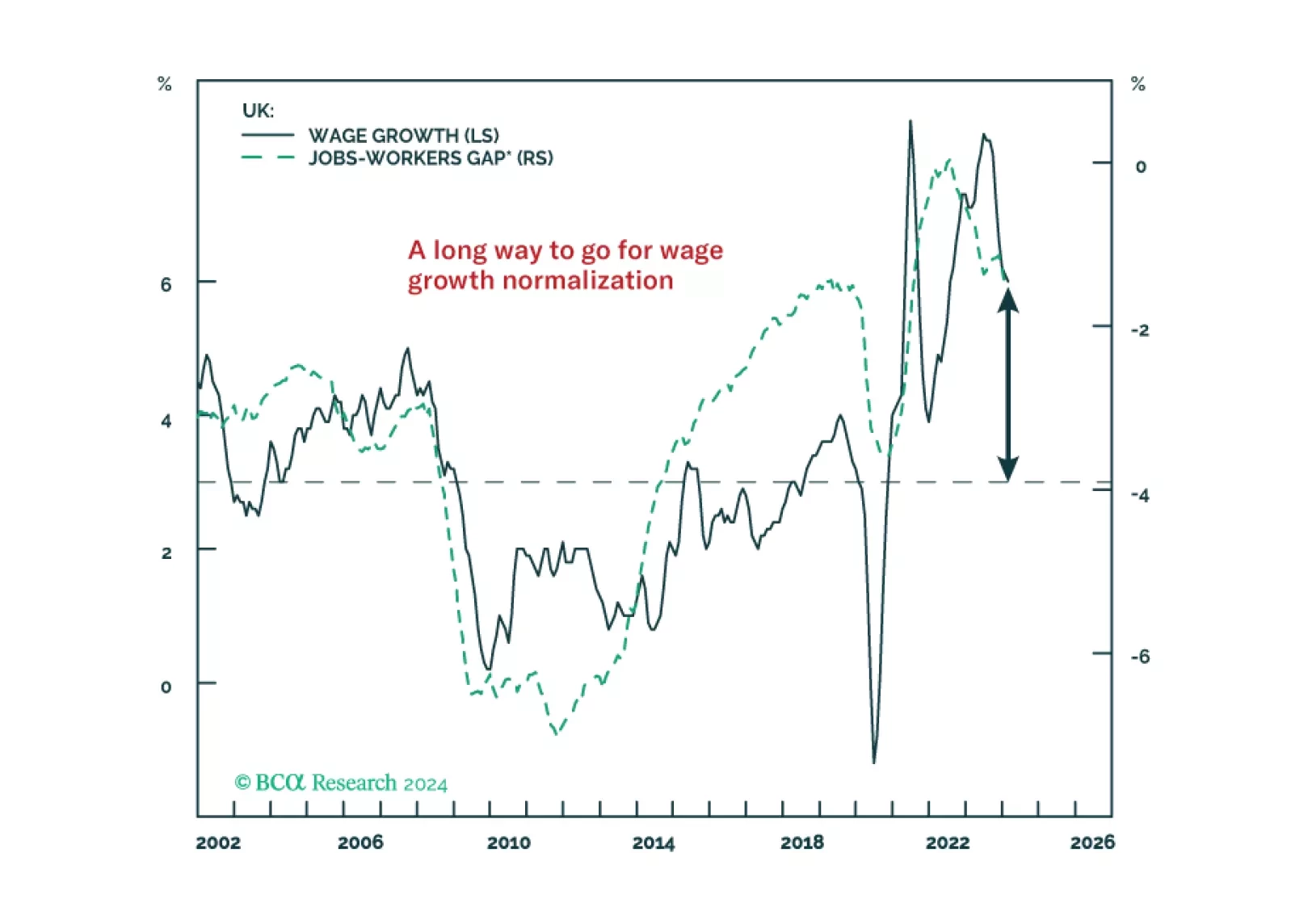

The UK labor market remains far too tight to expect wage growth to slow to levels consistent with the Bank of England inflation target. A true recession with rising unemployment is needed to finally slay the UK inflation beast. 2024 rate cuts are off the table, with the central bank having to keep monetary policy tighter for longer than markets expect and the UK economy now rebounding. We recommend downgrading UK gilts to underweight in global bond portfolios, while also looking for opportunities to buy the British pound on pullbacks versus the euro, Canadian dollar and Swedish krona.

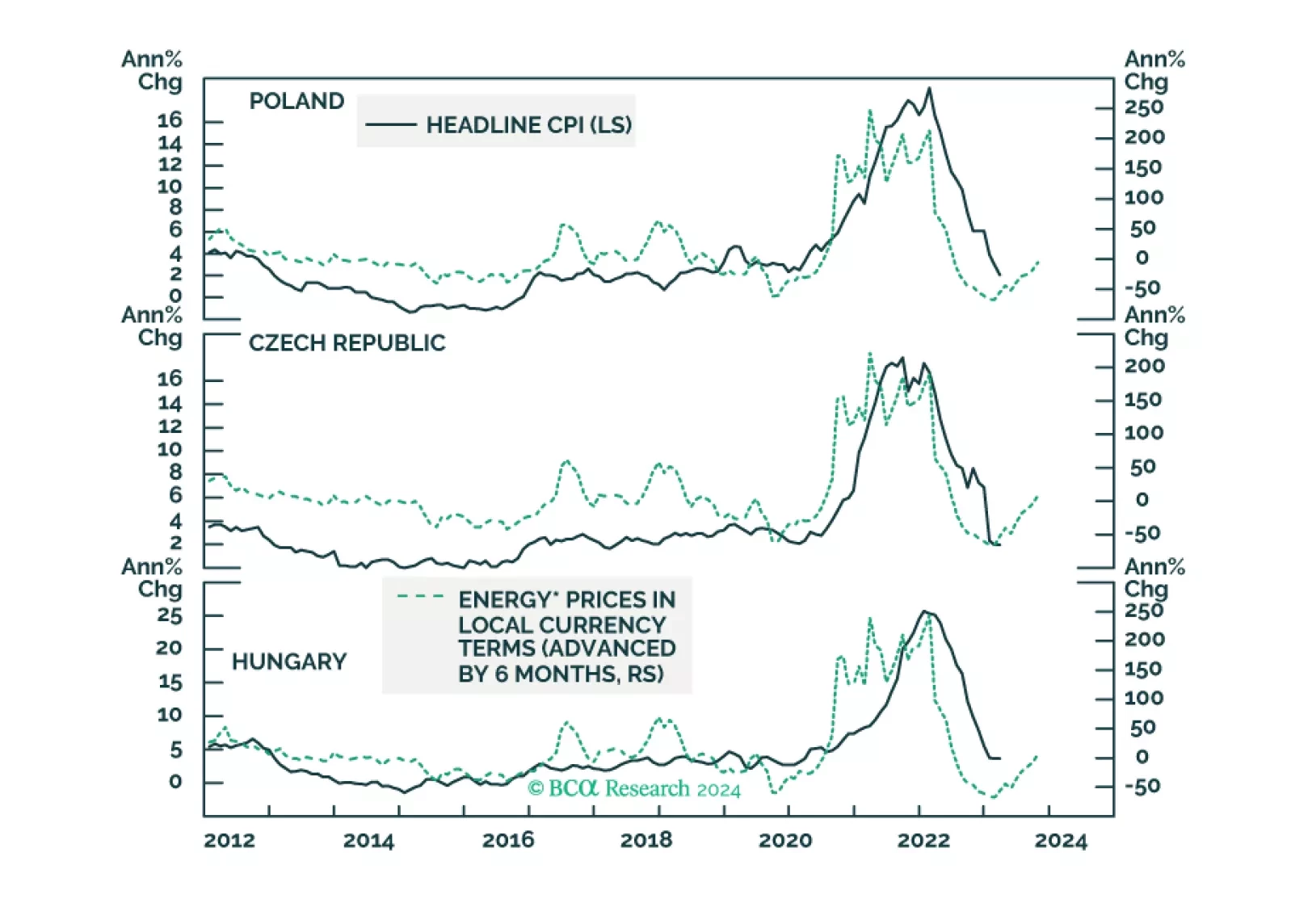

The disinflation process is over in Poland and Hungary. Only the Czech Republic will see its core inflation meet its central bank target this year. The reason is much tighter labor market dynamics in the first two. Investors should continue to short a basket of CE3 currencies vis-à-vis the US dollar.