Policy

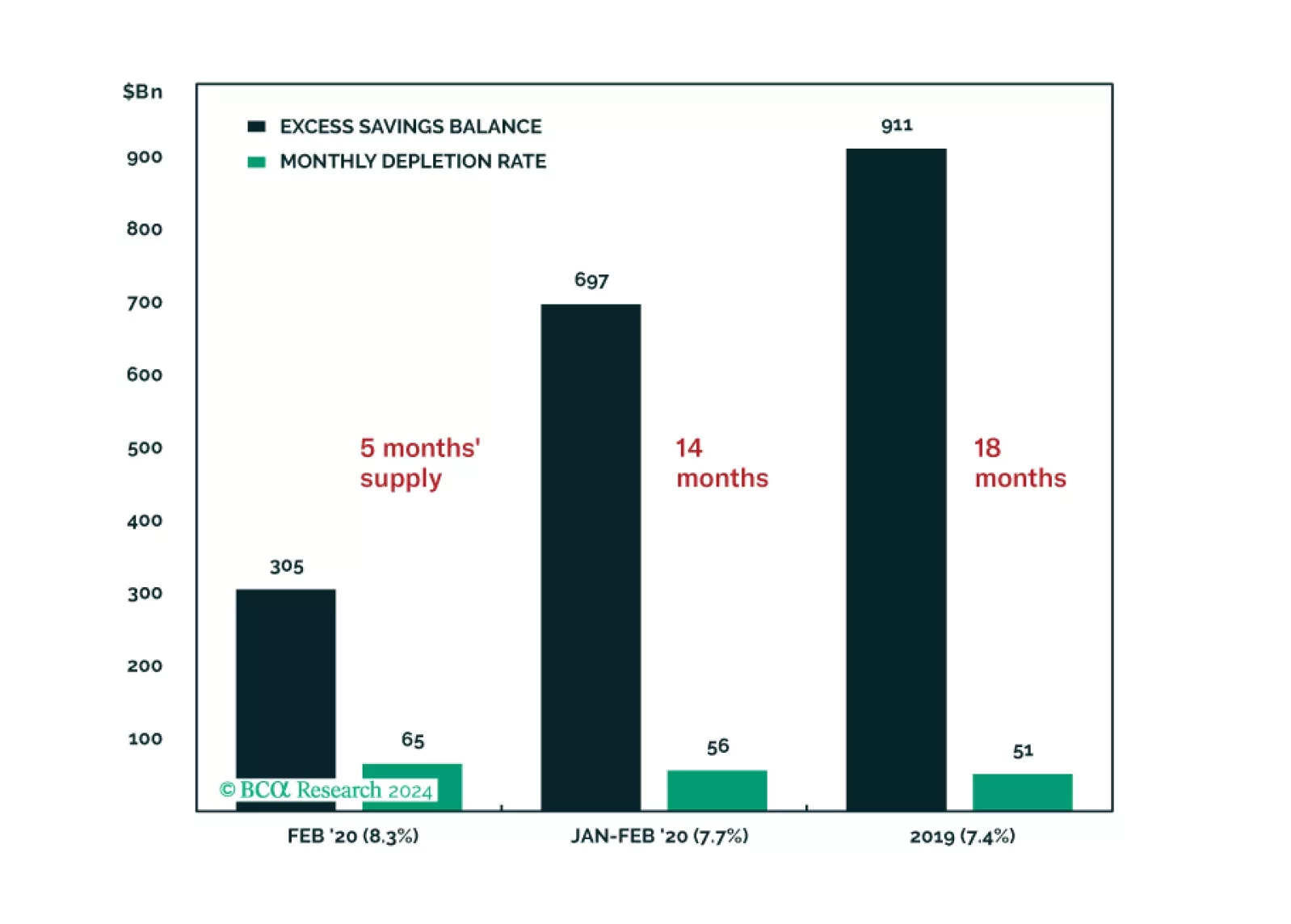

We feel as good about spurning the soft-landing narrative today as we did about spurning the recession narrative a year ago, but we are not giving into complacency. This week’s report looks at two key ways that we may be getting it wrong: by underestimating households’ asset support and the labor market’s durability. We remain tactically neutral but continue to look for opportunities to turn defensive.

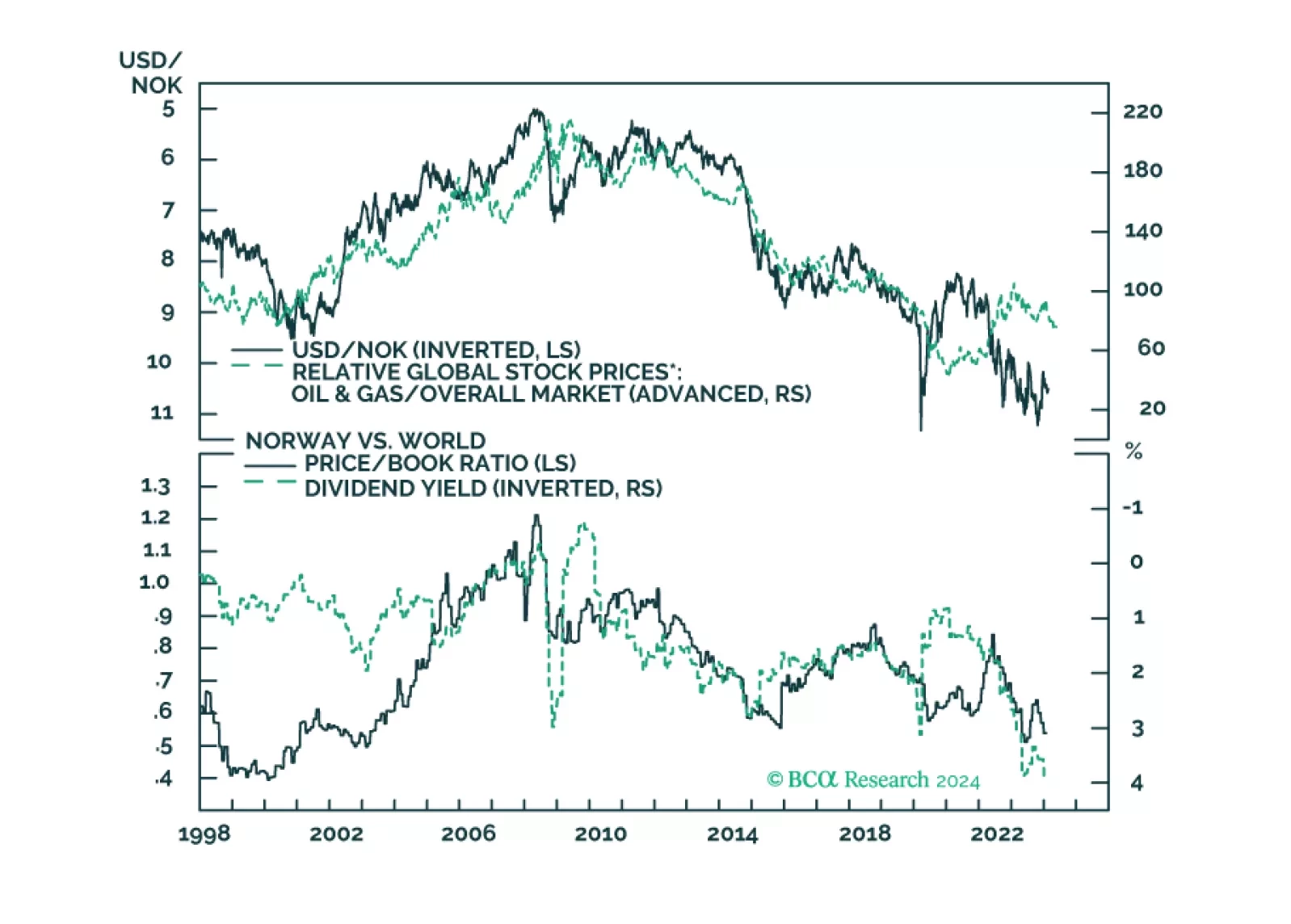

In this insight, we provide an update on the Norwegian krone, with attractive trade ideas over a long-term horizon. Shorter-term, our neutral-to-positive view on the dollar keeps us on the sidelines for USD/NOK.

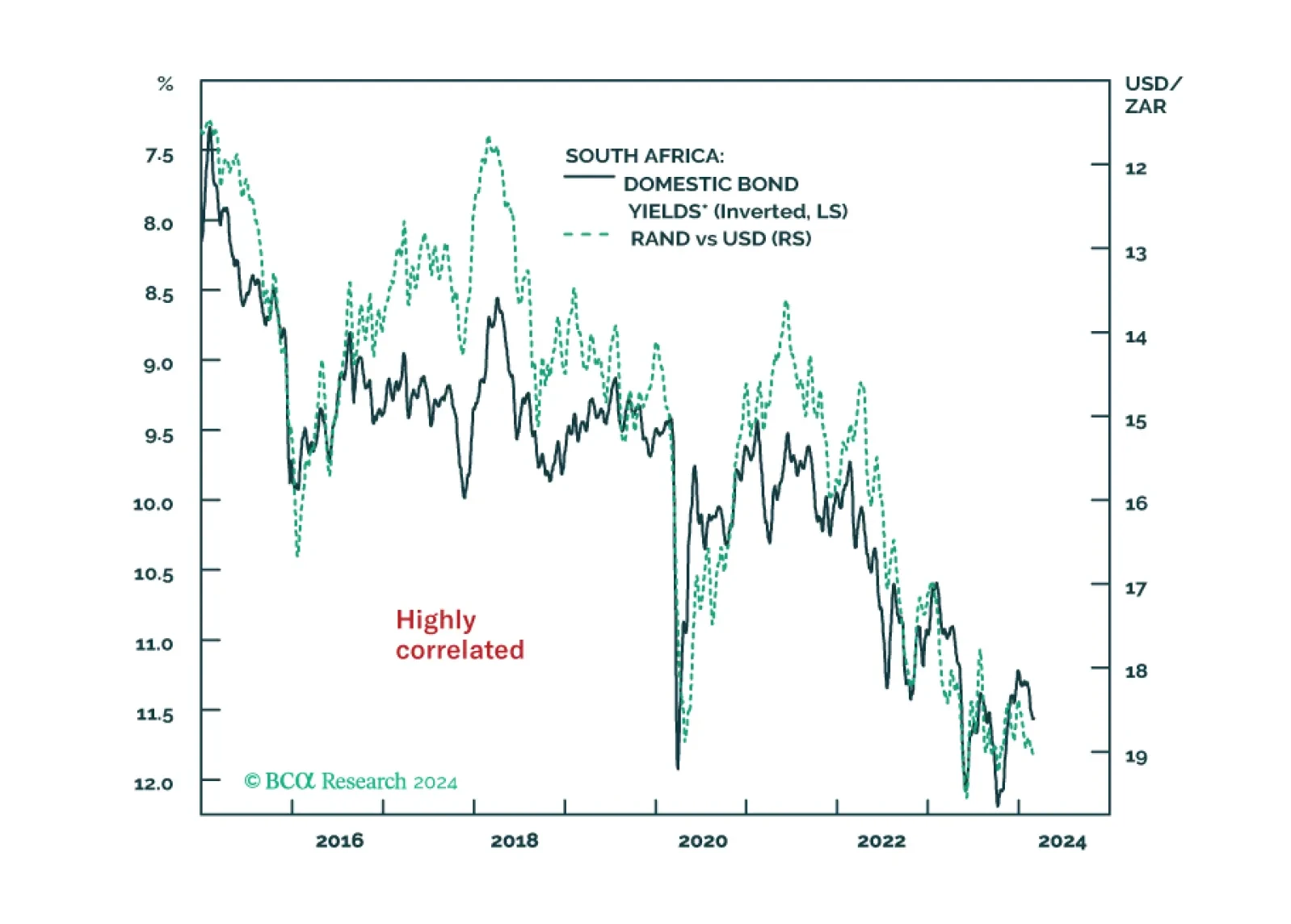

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

In this BCA Special Report, we ask what policies investors should expect if Donald Trump wins the 2024 Presidential election. The answer is that a second Trump term would be much less positive for risky assets than the first. While the US will remain democratic and geopolitically preeminent no matter the outcome of the 2024 election, a second term Trump administration would likely oversee large budget deficits, continued wealth inequality, labor shortages, high import prices, and an erosion of checks and balances, possibly including at the Federal Reserve. Trade policy under a second Trump presidency represents the greatest cyclical risk to investors, and the sequencing of policies in general will be important to monitor. An early legislative priority of immigration over tax cuts, alongside the rapid imposition of new tariffs, would be the worst alignment for risky assets.