Policy

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

The market will eventually be forced to react to rising odds of a sharp US national policy reversal. Investors should overweight government bonds and defensive equity sectors.

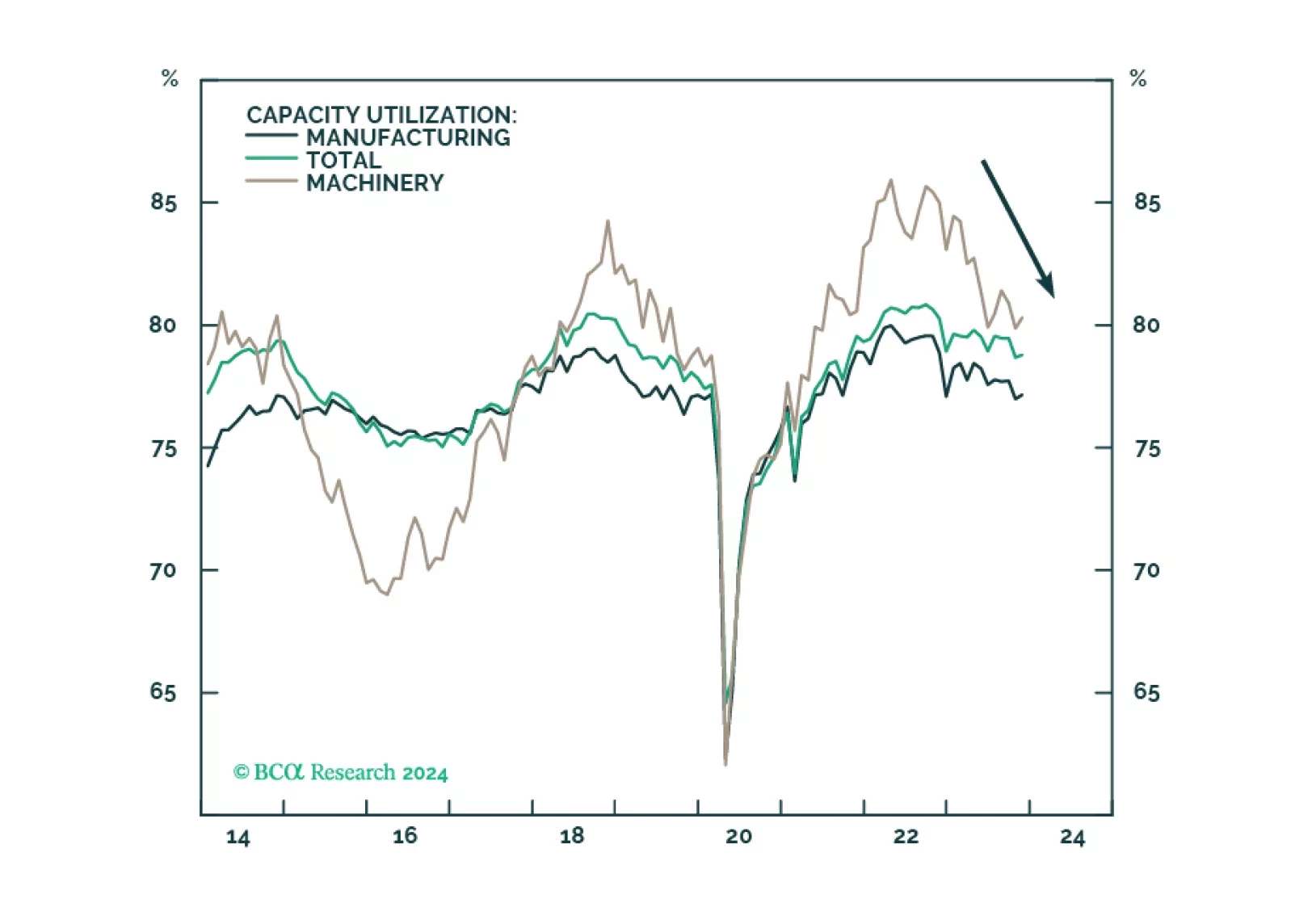

The US manufacturing renaissance, spurred on by reshoring, automation, and government spending, is running its course but progress has slowed on the back of tight monetary conditions and the manufacturing recession. The deceleration of these positive trends weighs on the outlook for the Capital Goods industry group, impeding its performance over the short term. However, we reiterate that positive long-term trends for the industry remain intact. We downgrade Capital Goods to a tactical underweight. It remains a strategic overweight.