Policy

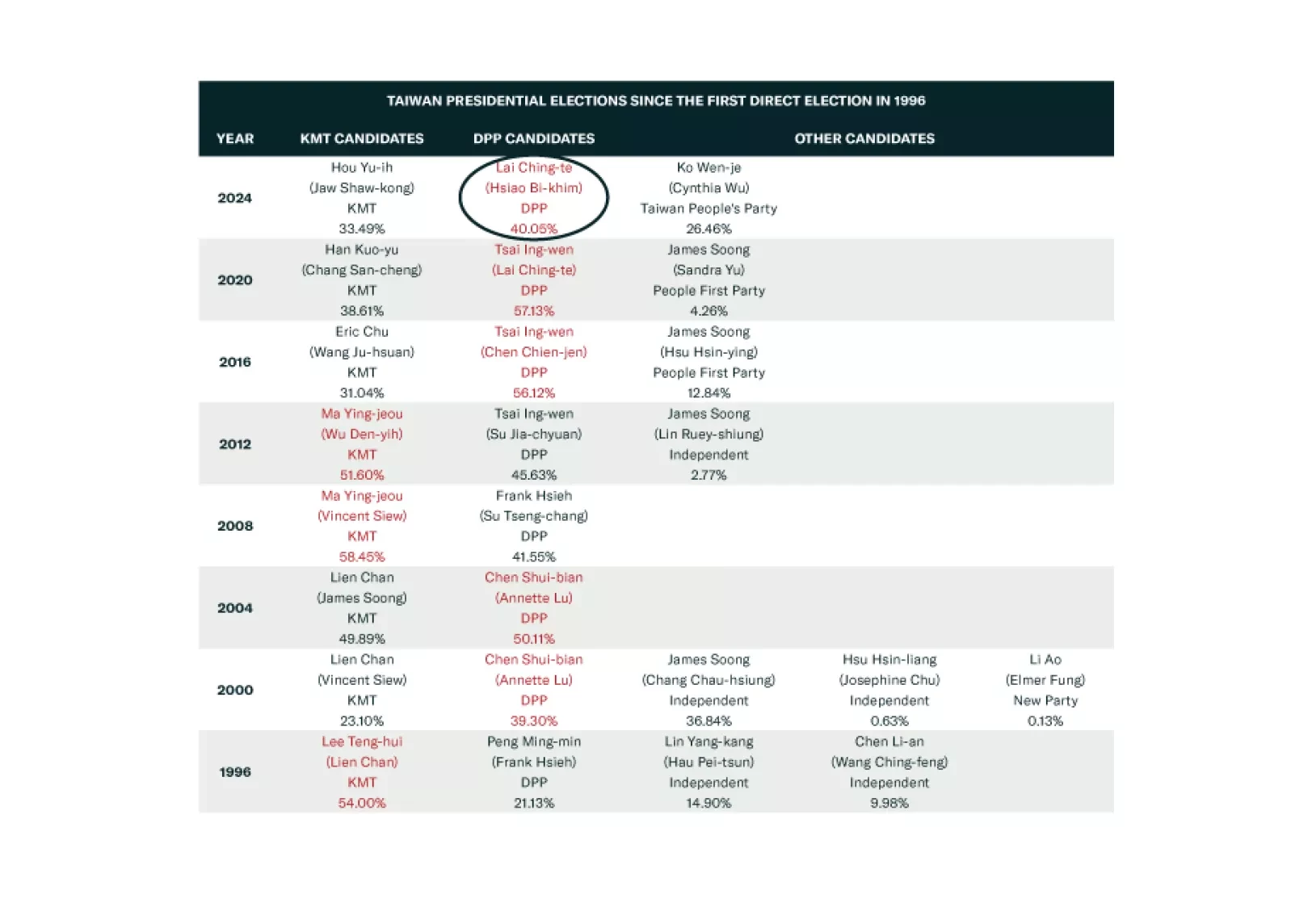

Taiwan’s election will lead to serious Chinese military and economic pressure but not full-scale war. War is a long-term concern. Investors should short TWD-USD.

We share the edited transcript of a webinar we participated in discussing global trade, trade wars and tariffs, as well as de-risking strategies.

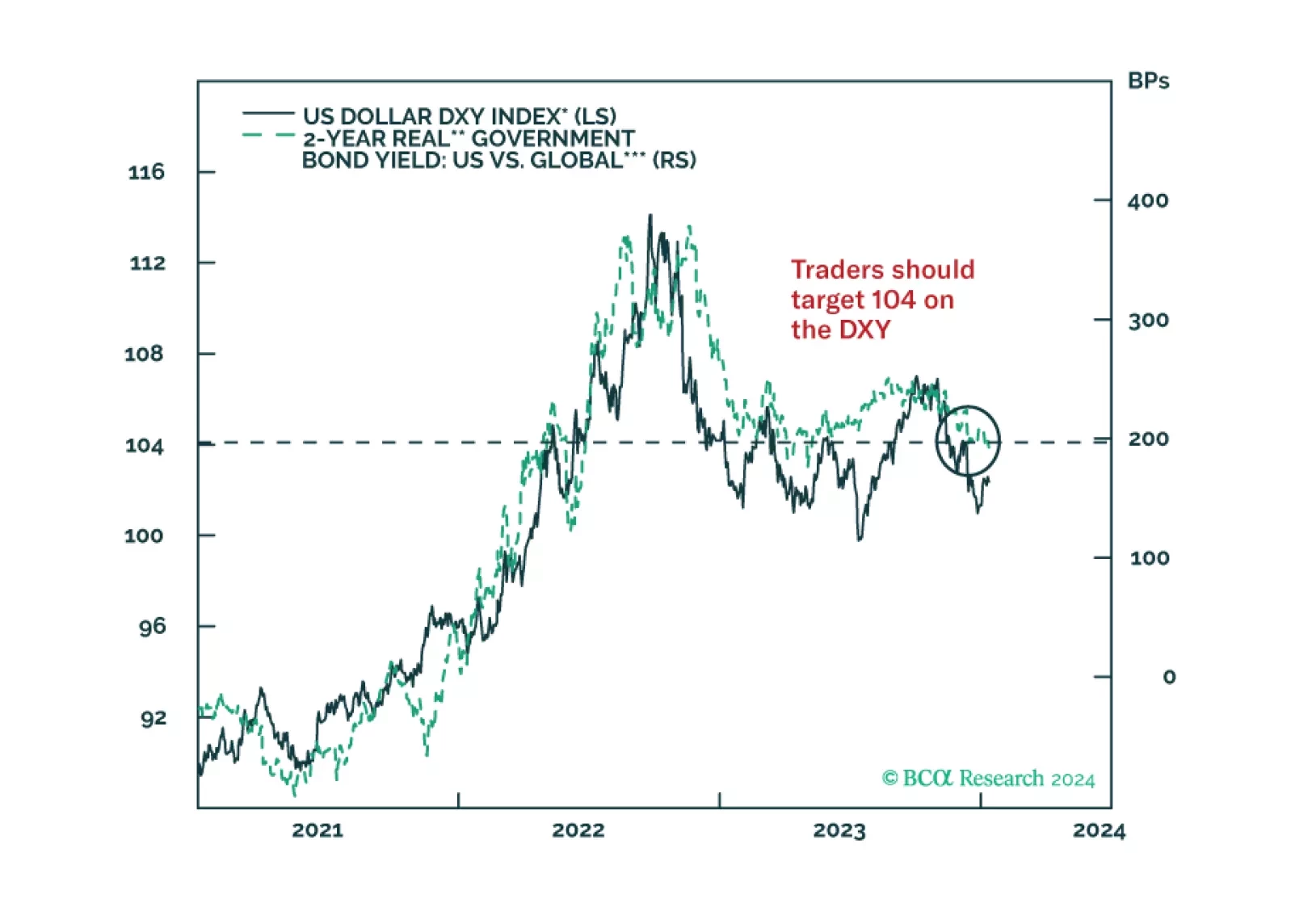

In light of the hotter-than-expected US CPI report, we look at what interest rate currency investors should focus on. Our conclusion largely keeps our existing trades in place, as published in our outlook, a few weeks ago.

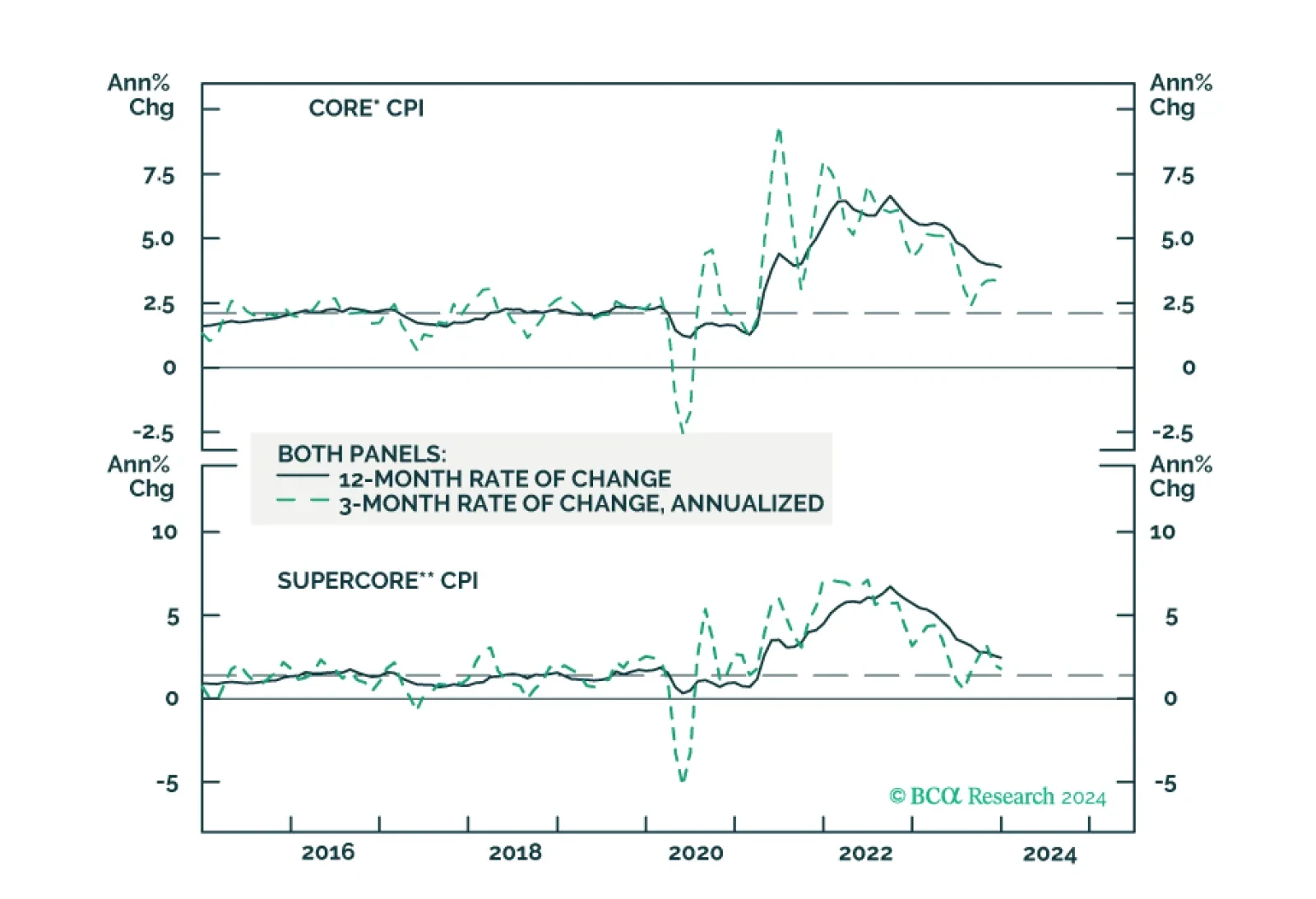

We update our inflation forecast following this morning’s CPI report.

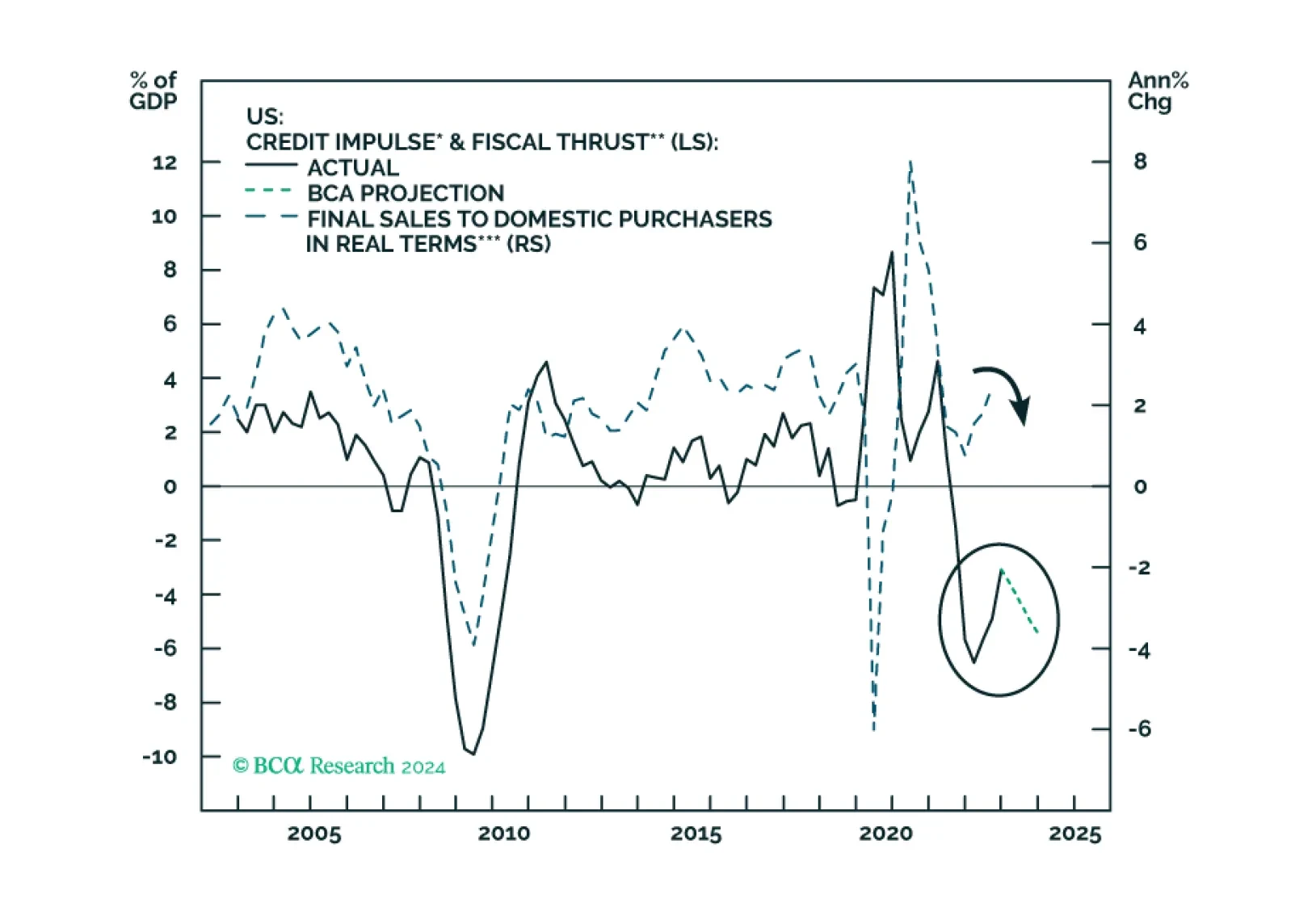

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.

Increasing gray-zone confrontations and another round of tariff and non-tariff barriers to trade are not being reflected in commodity prices. This is keeping inflationary pressures emanating from the real economy subdued. That said, inflation risks are increasing as threats to commodity supplies and supply chains grow. Standard monetary policy focused on aggregate-demand management is ill-suited for addressing these risks, and could exacerbate supply-side tightness. We remain long oil- and metals-producer equities exposure via the XOP and XME ETFs, and to commodities outright via the COMT ETF.