Real Estate

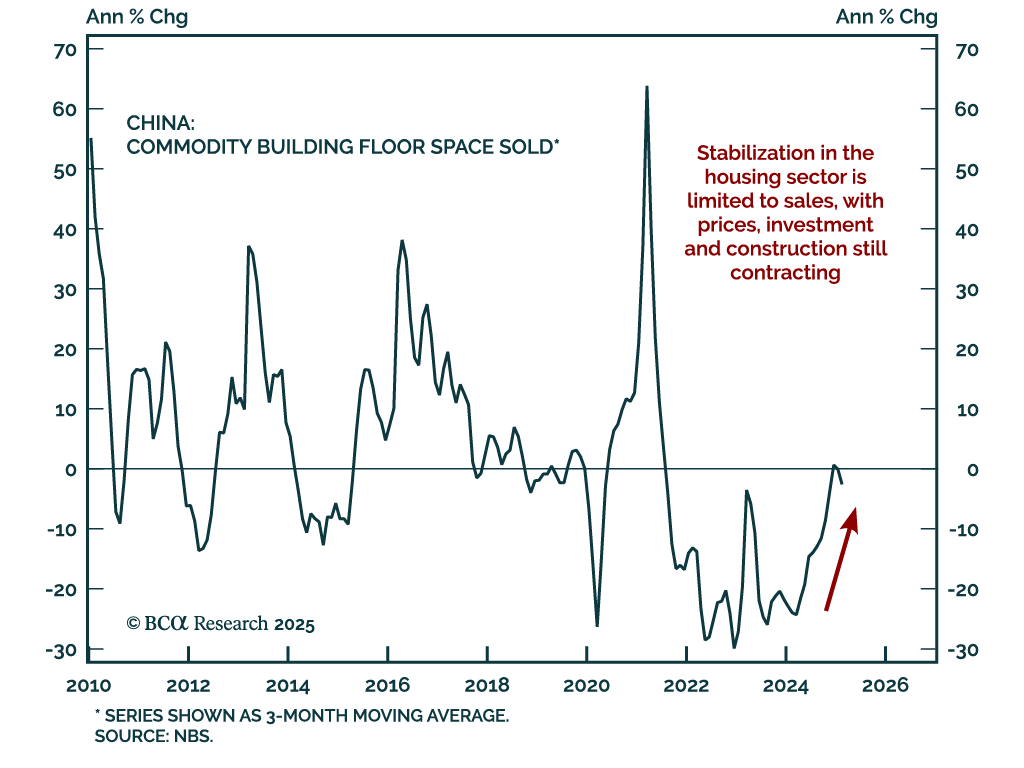

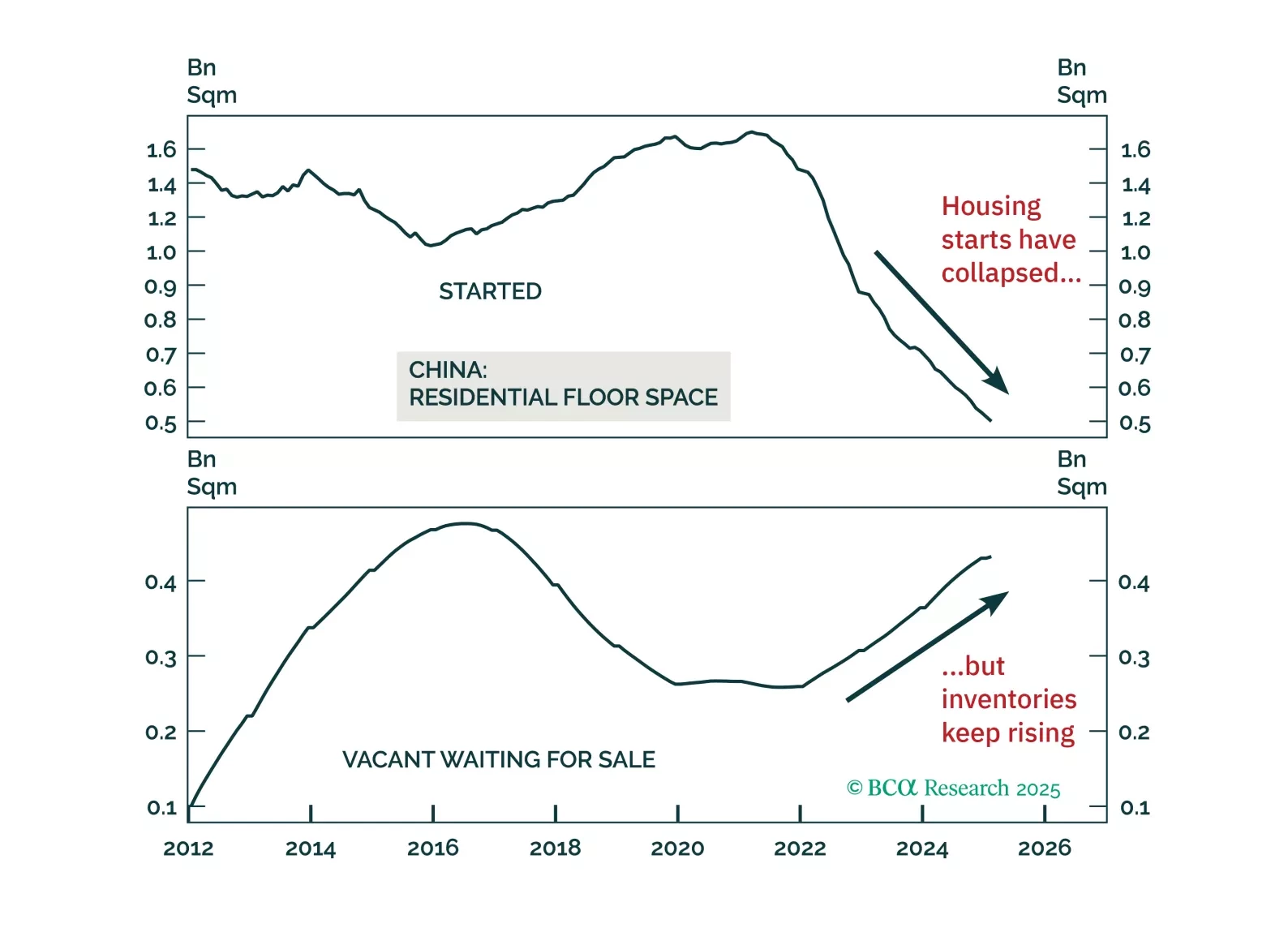

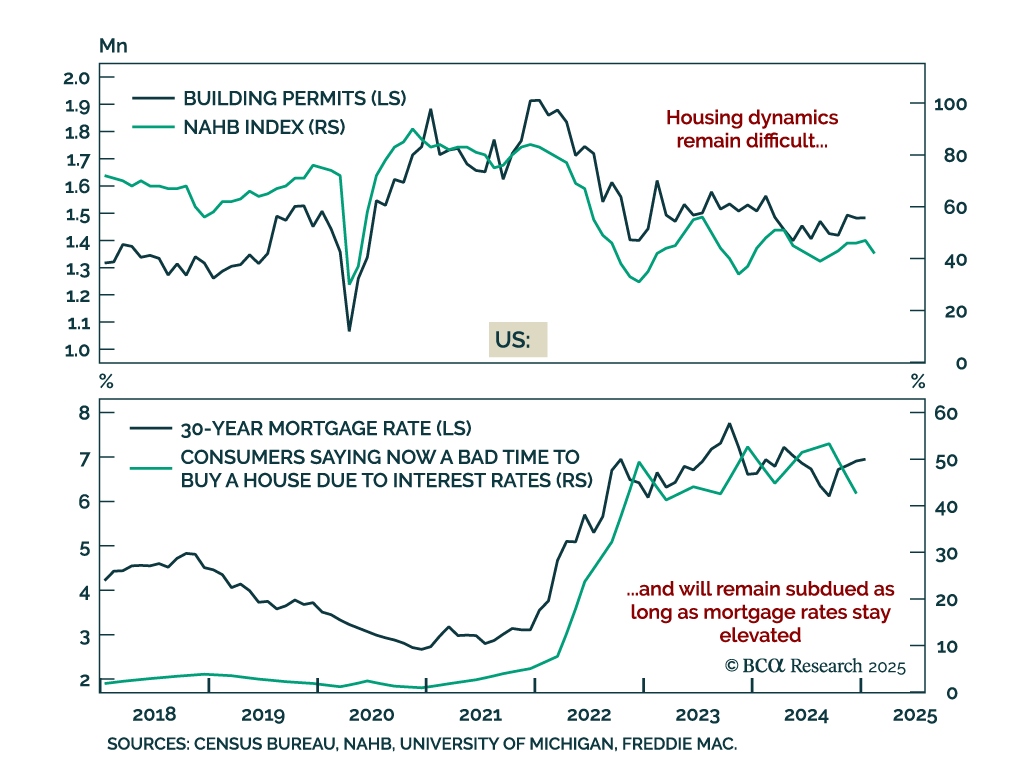

Data released this Monday suggests that while China’s housing market is no longer worsening, the secular adjustment remains ongoing. Although aggregate housing demand may be stabilizing at a low level, supply will continue to significantly outpace demand, indicating that home price deflation will persist. Additionally, property developers’ poor financing will hinder new project initiations, leading to a further decline in housing starts over the next six to 12 months.

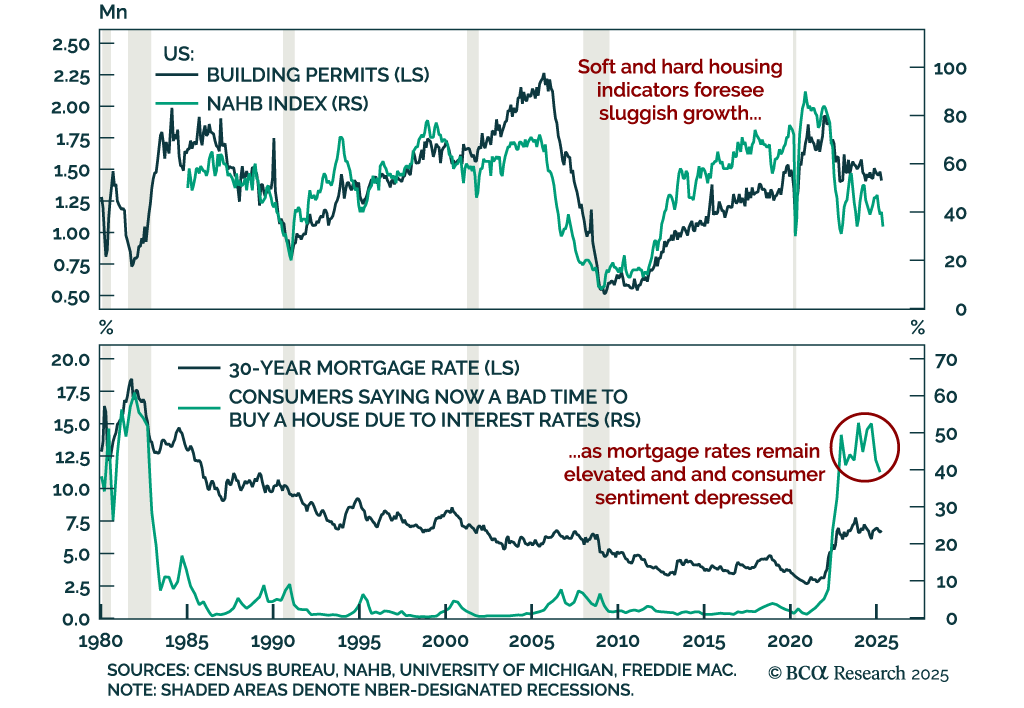

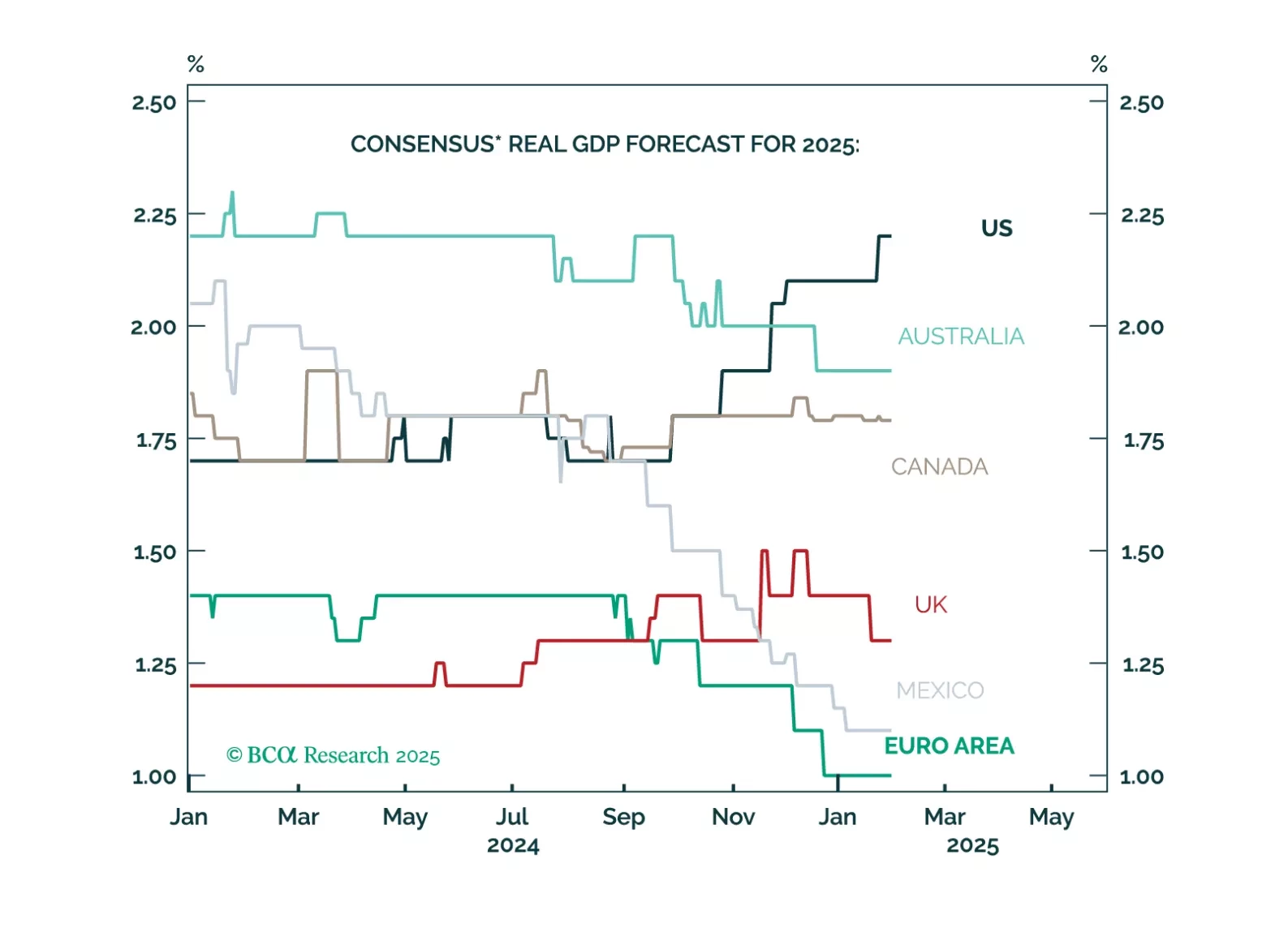

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

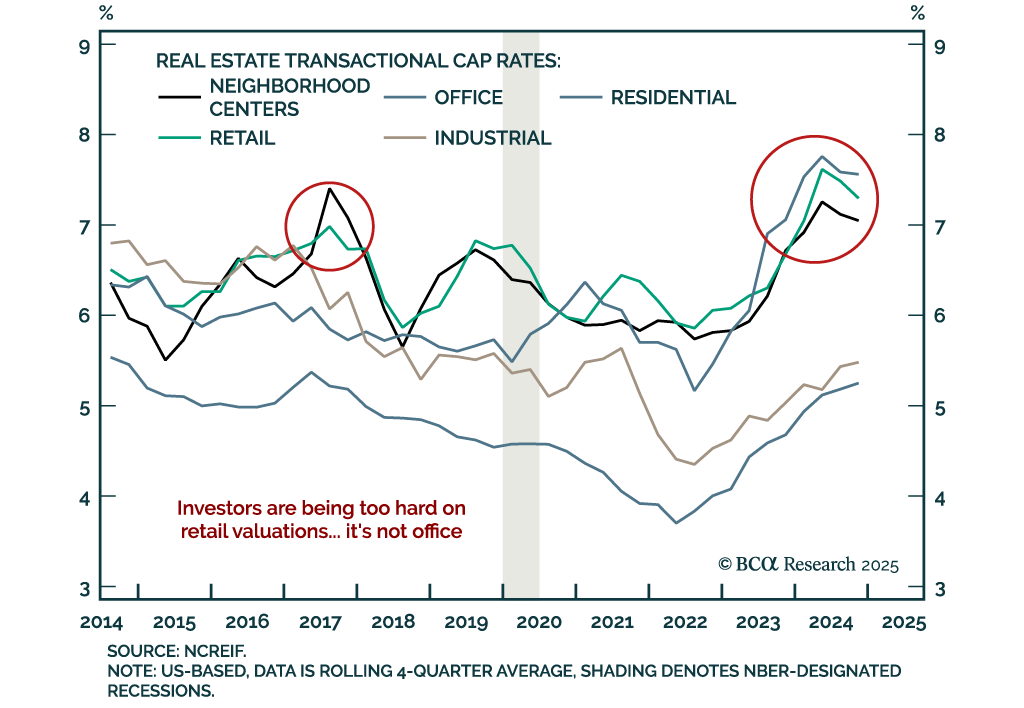

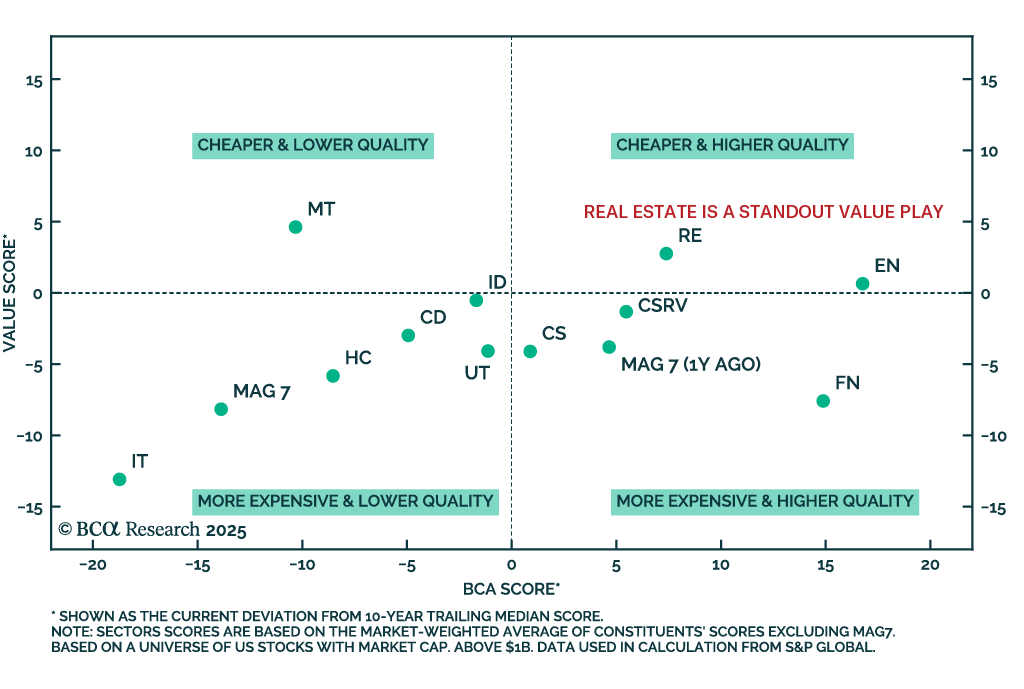

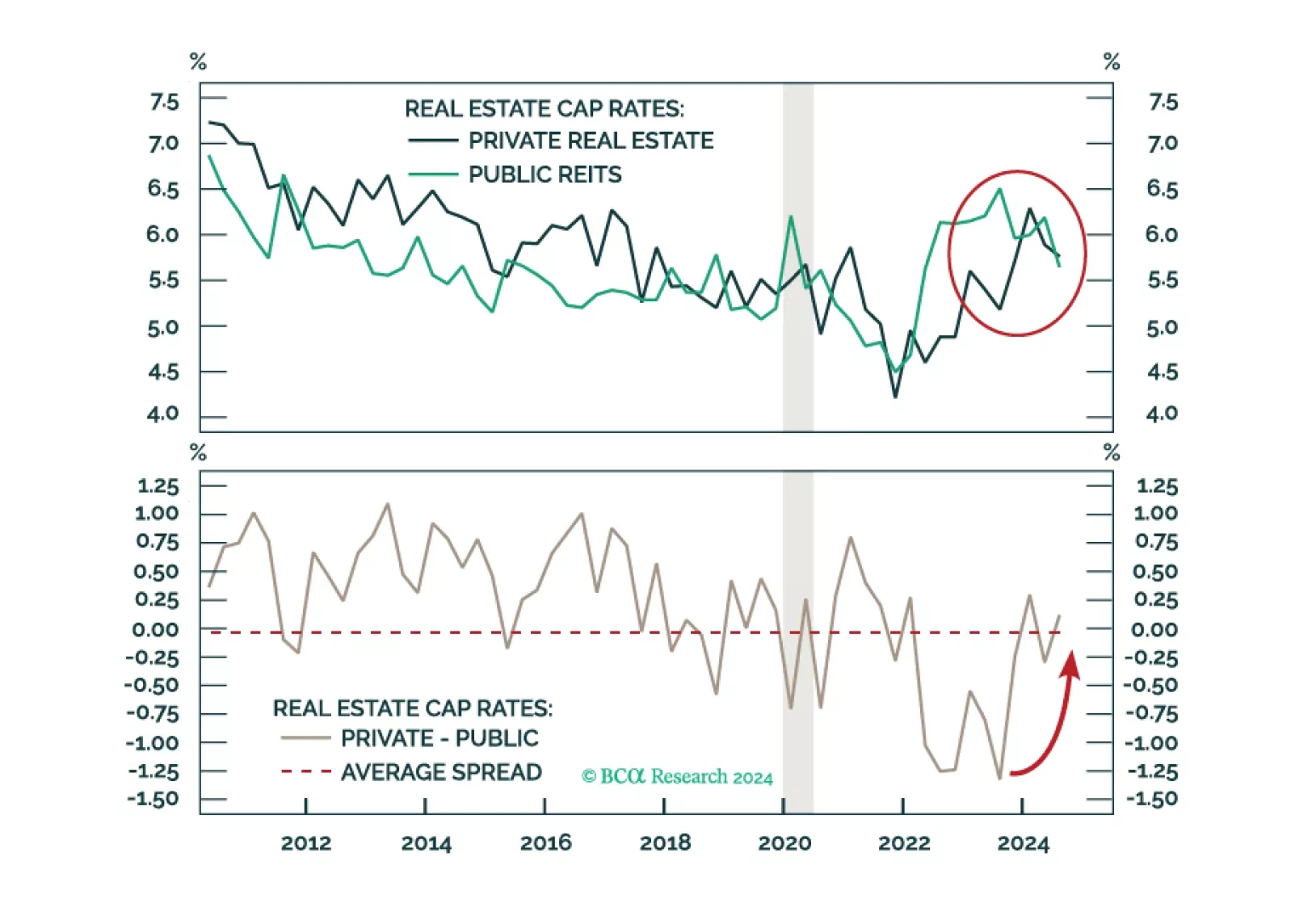

Private Real Estate and Public REITs differ beyond just being liquid or illiquid. Looking through surface-level metrics uncovers valuable choices for investors. When analyzing the opportunity for today’s next dollar, Private Real Estate is more attractive.