Recession-Hard/Soft Landing

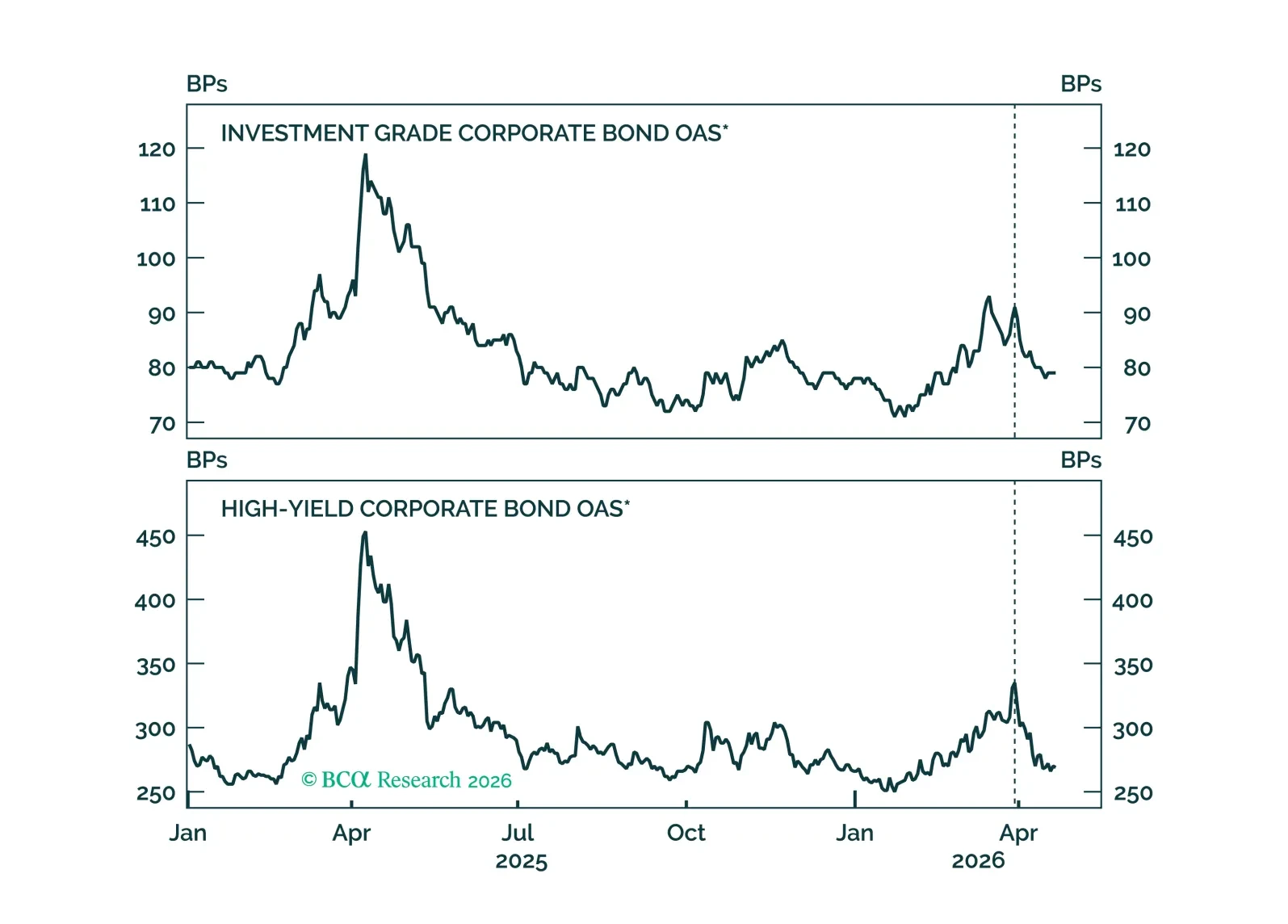

We recommend increasing exposure to spread product as the US economy transitions back into a low rate vol regime.

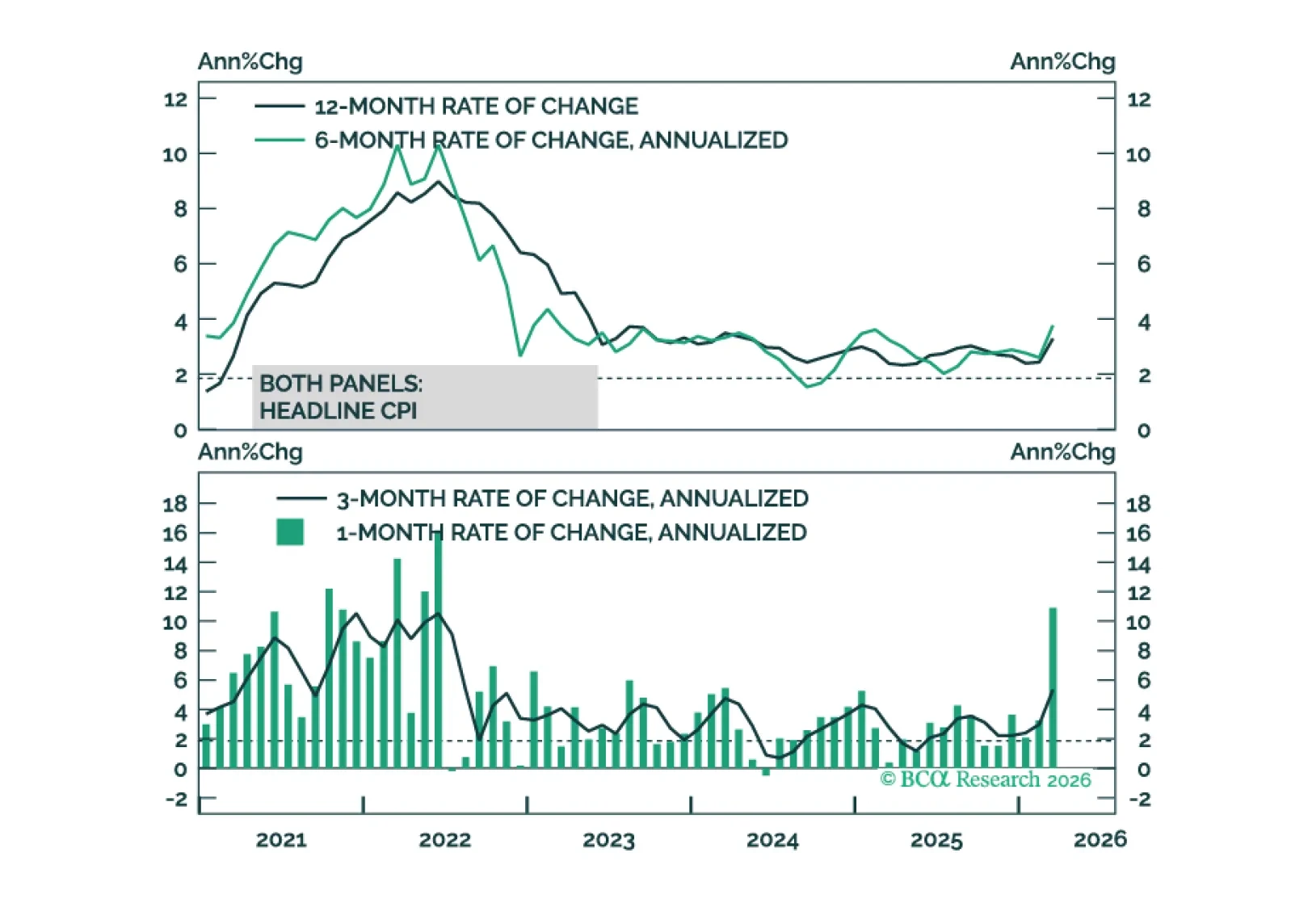

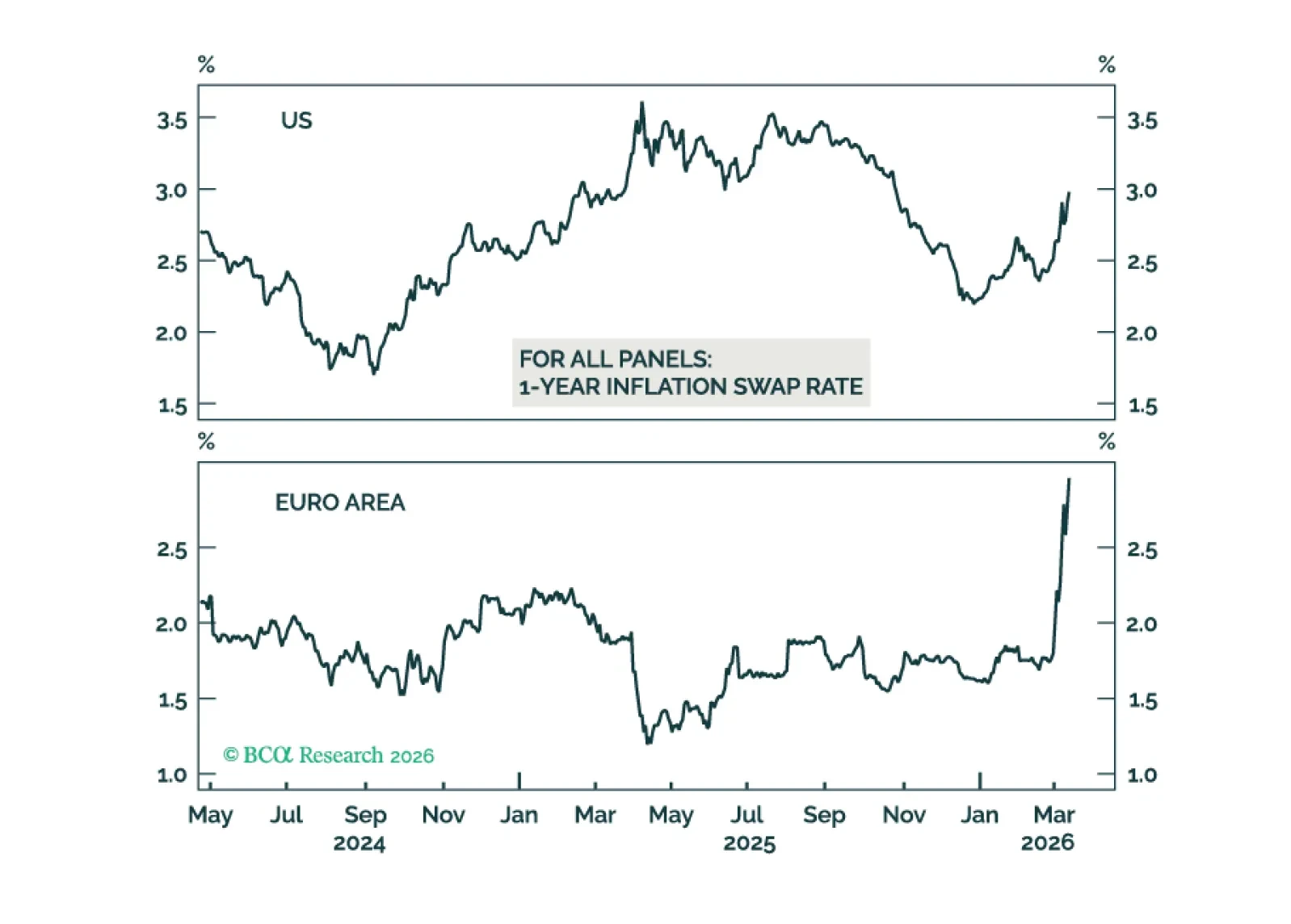

Inflation’s underlying trend was headed lower prior to the Iran war. This makes the recent back-up in bond yields look like an attractive buying opportunity.

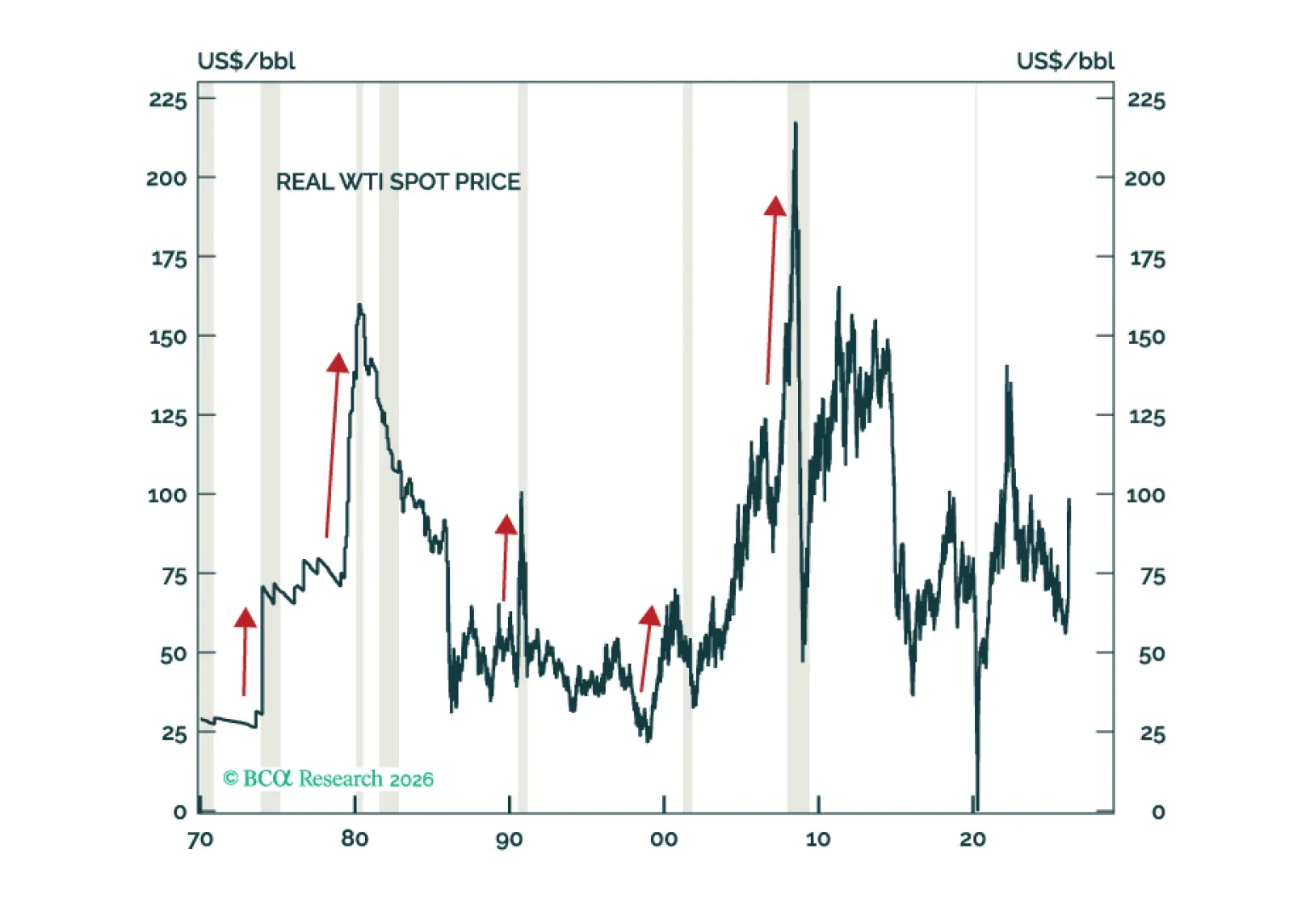

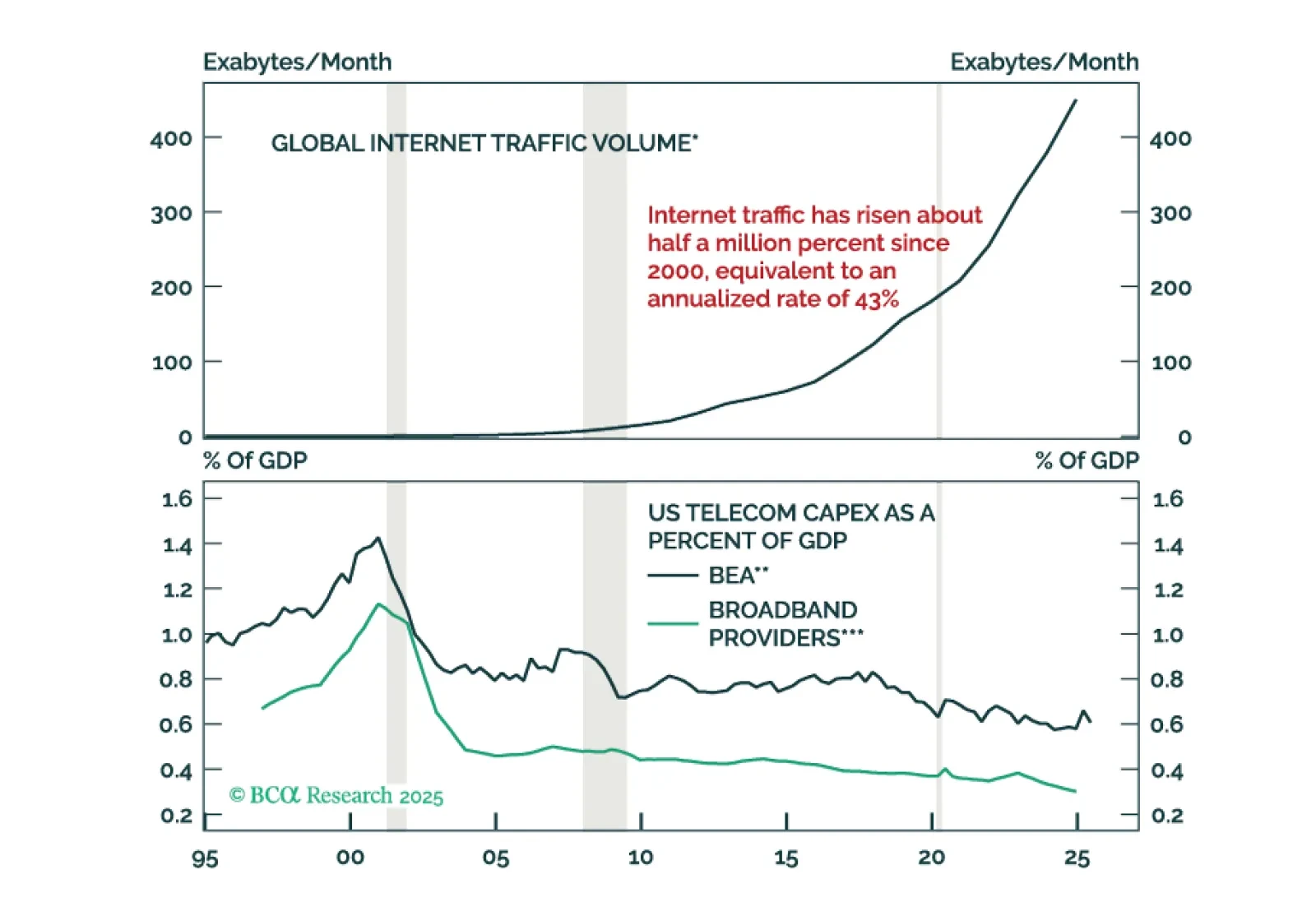

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

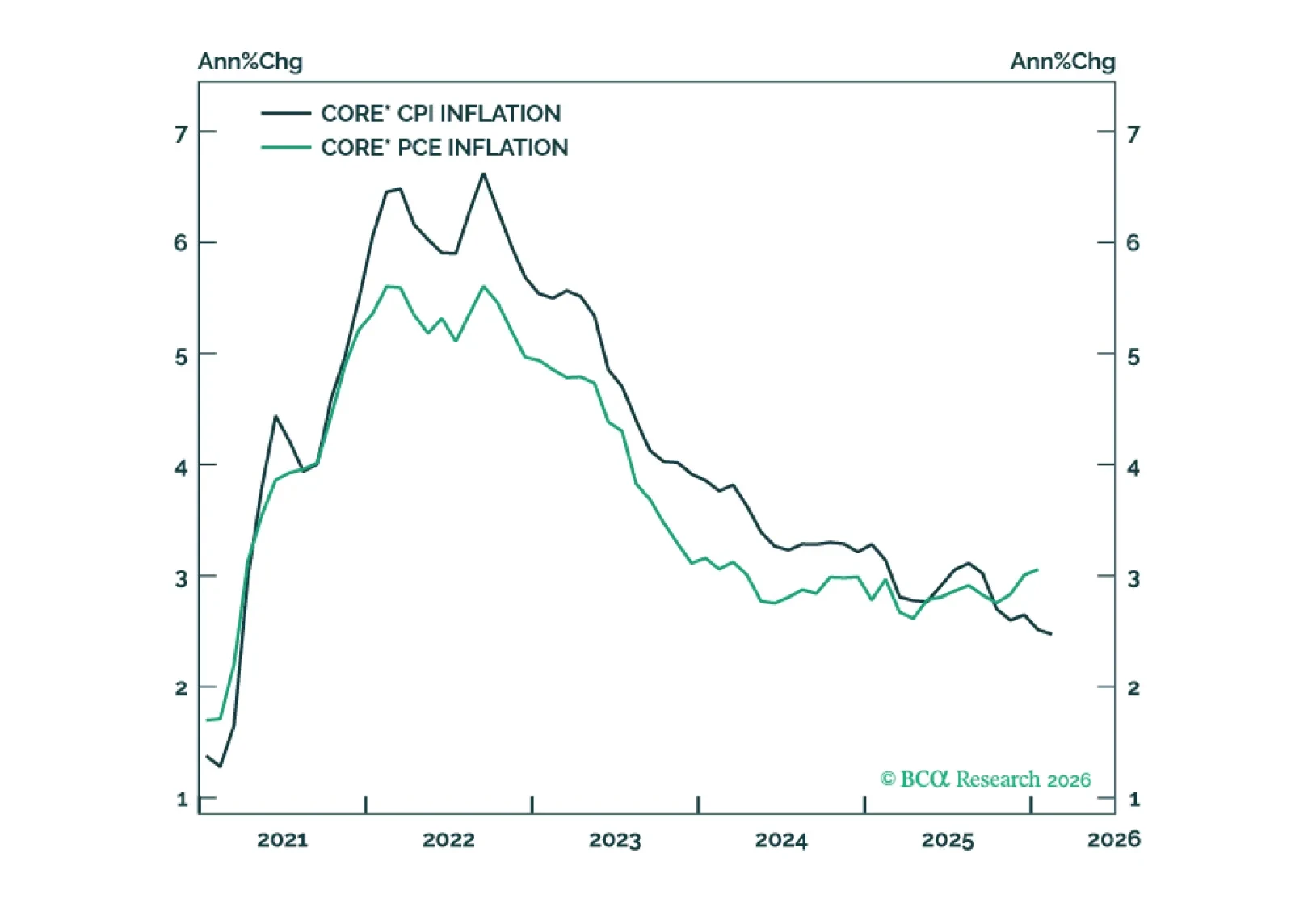

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

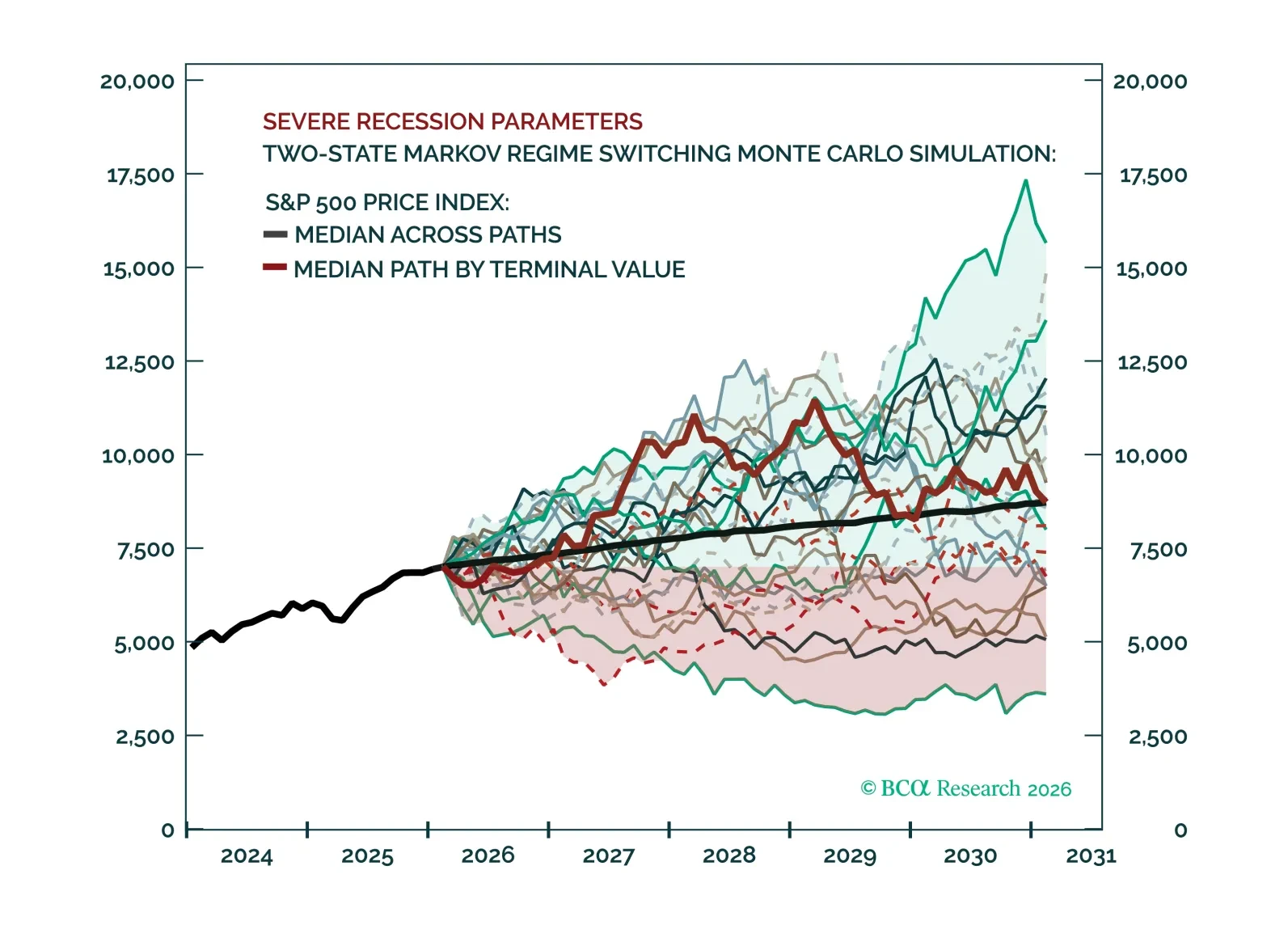

Recessions are inevitable but unpredictable. While earnings drive long‑term equity performance through the cycle, around turning points fundamentals follow a predictable sequence: multiples contract first, then prices, then earnings. Recessions can shift sector leadership, but simulations show that medium‑term index‑level upside remains intact unless future downturns are materially more severe than in history.

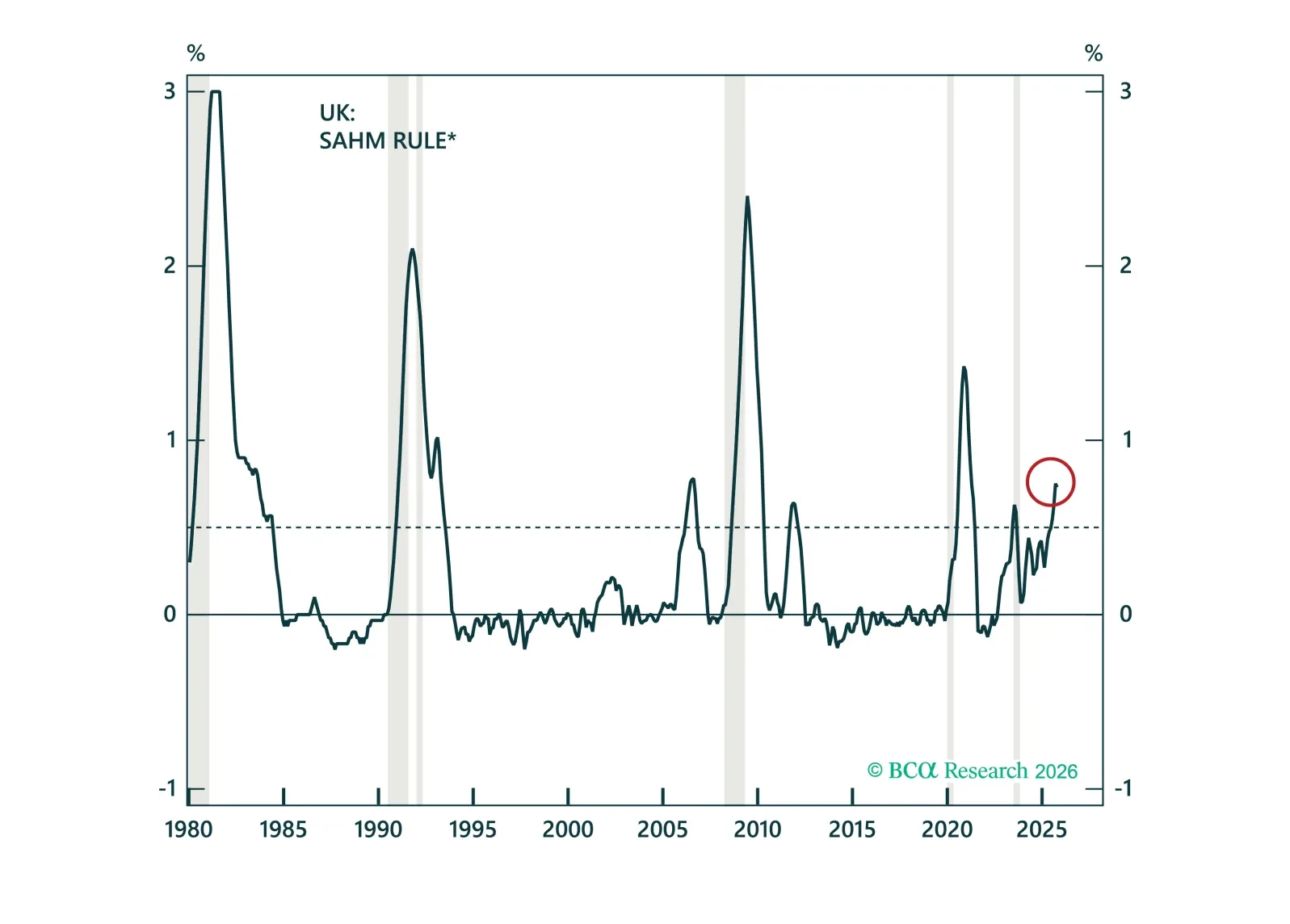

Recession risks in the UK are clearly rising. In this Special Report, we unpack why labor market deterioration, falling wage growth, and normalizing inflation support deeper BoE cuts ahead. We then discuss how to position across gilts, the pound, and UK equities.

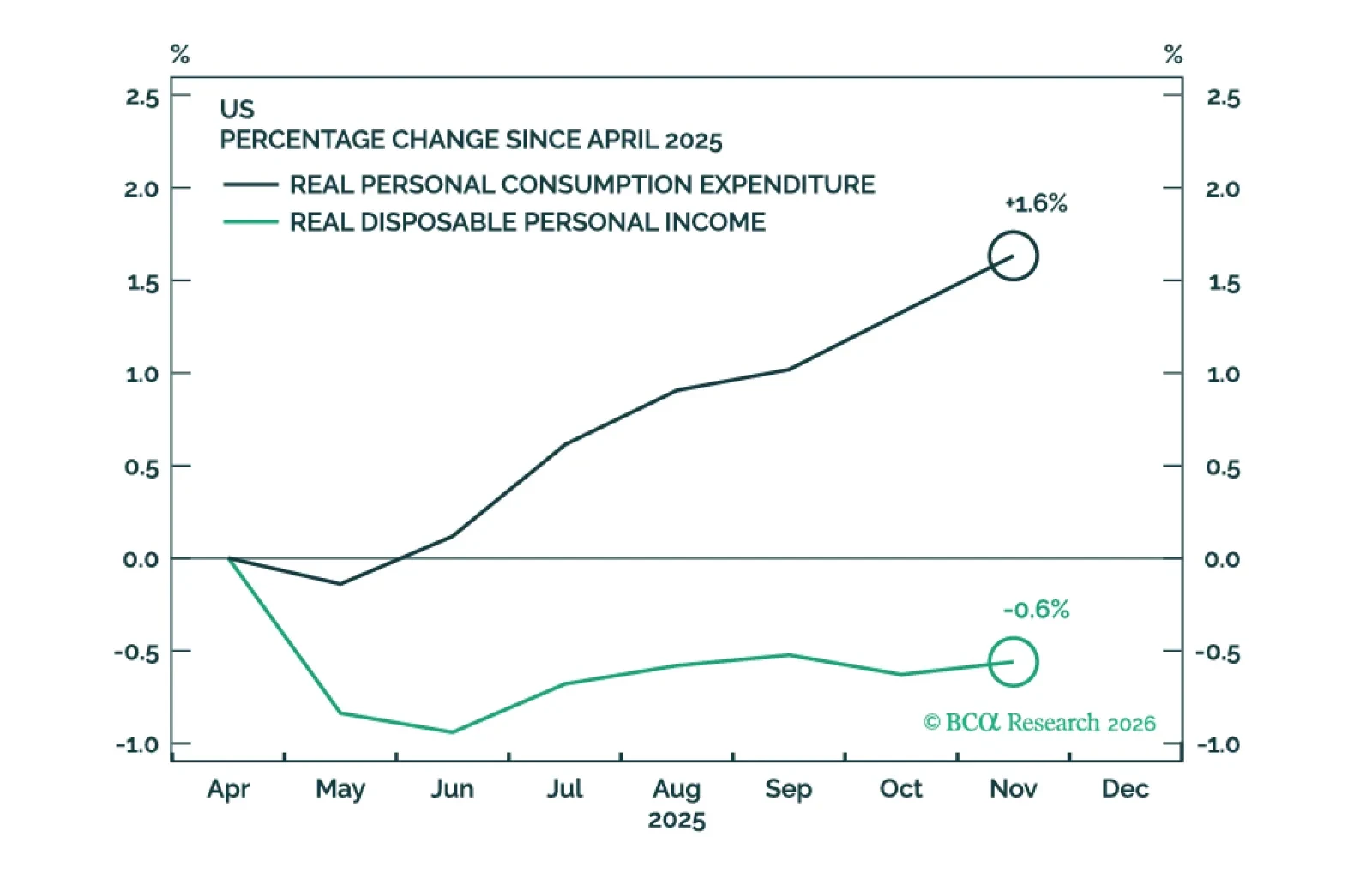

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

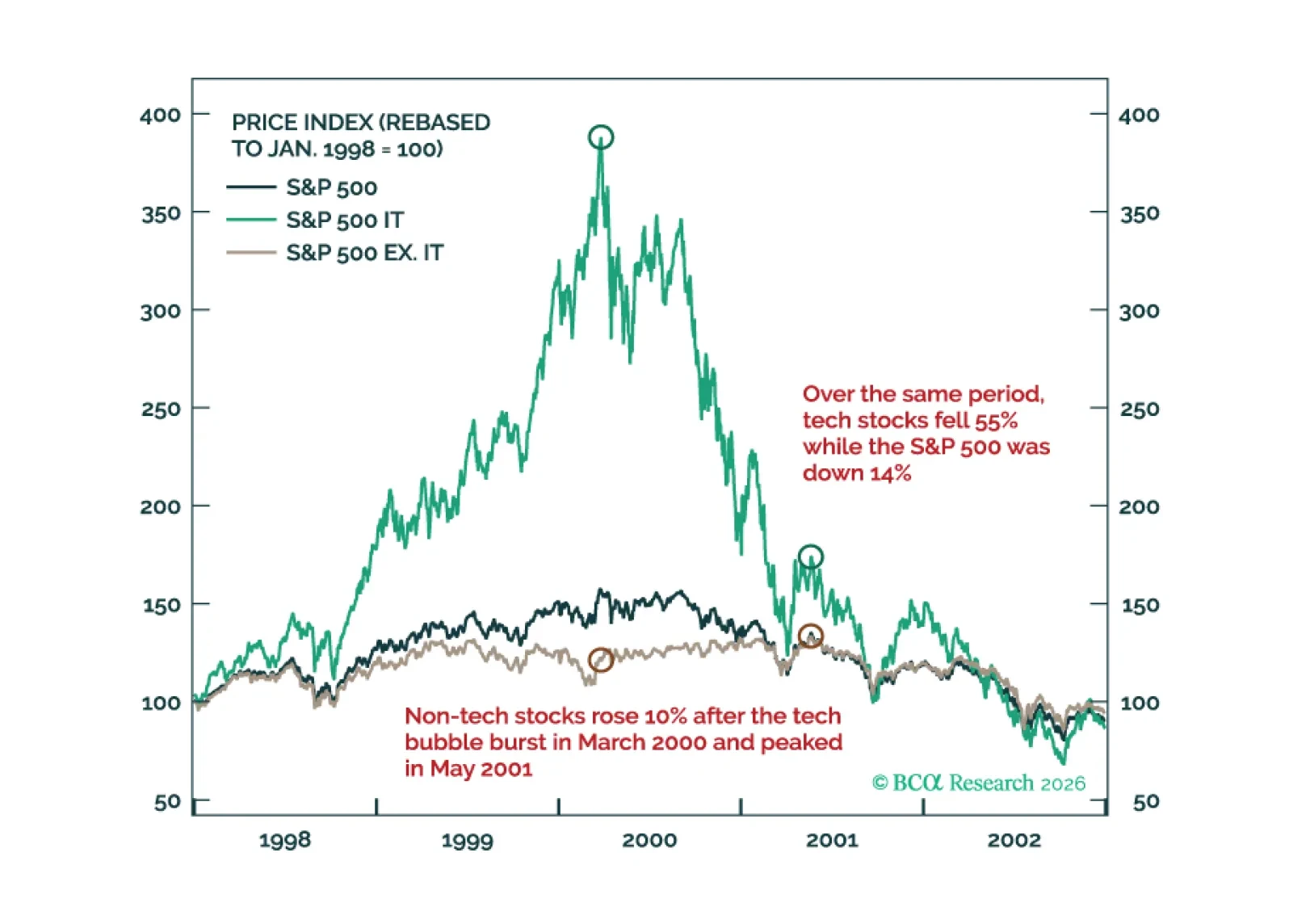

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.