Recession-Hard/Soft Landing

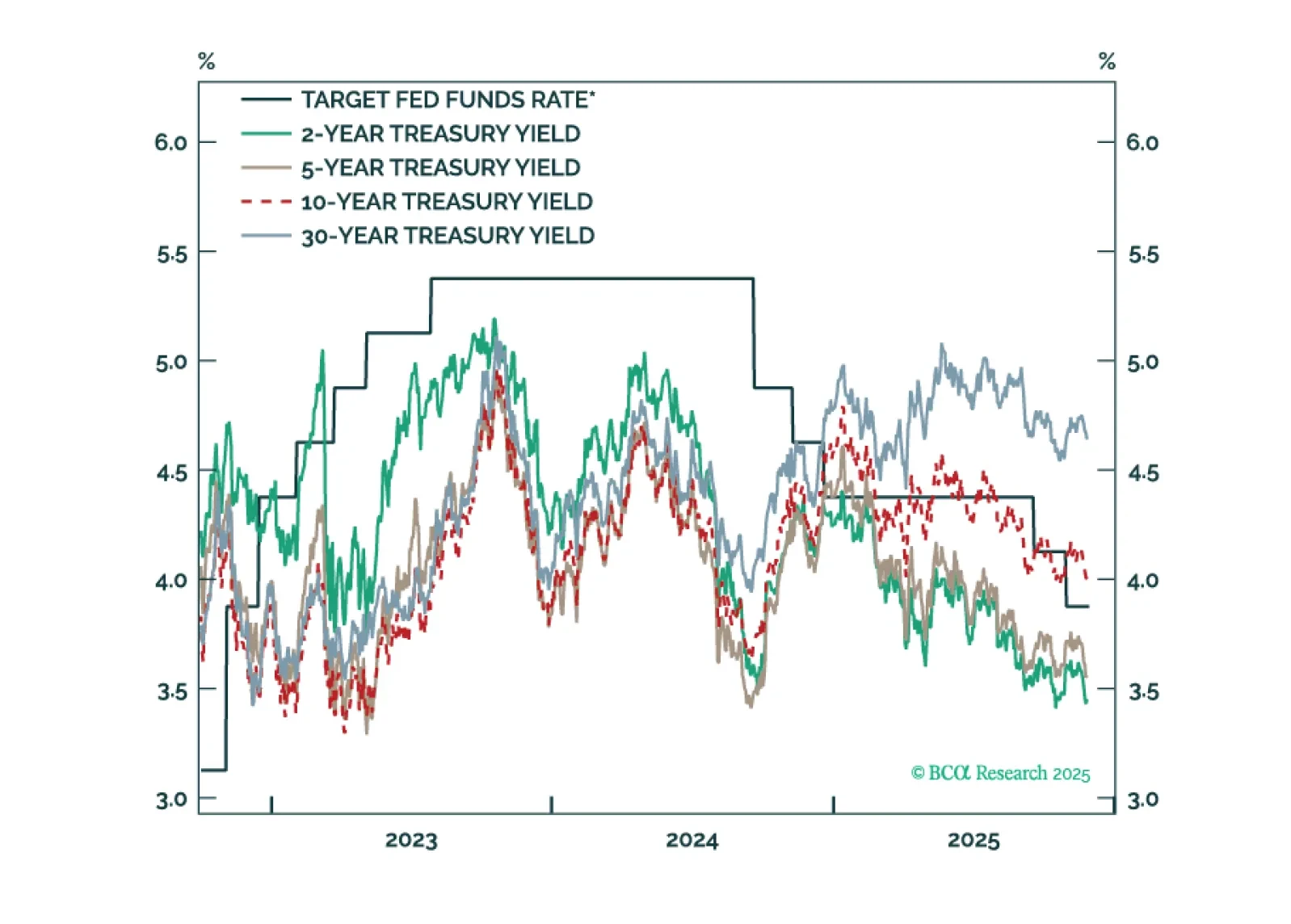

Our key US fixed income views for 2026.

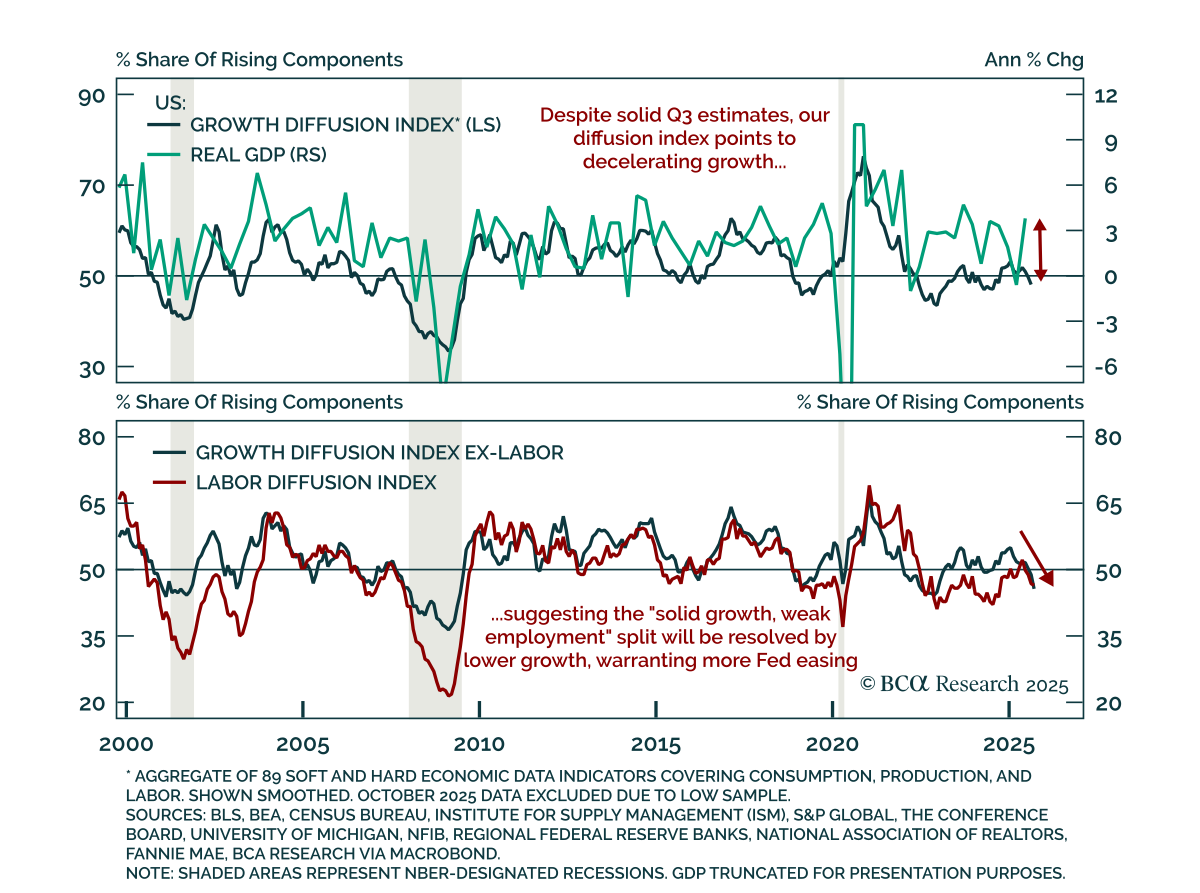

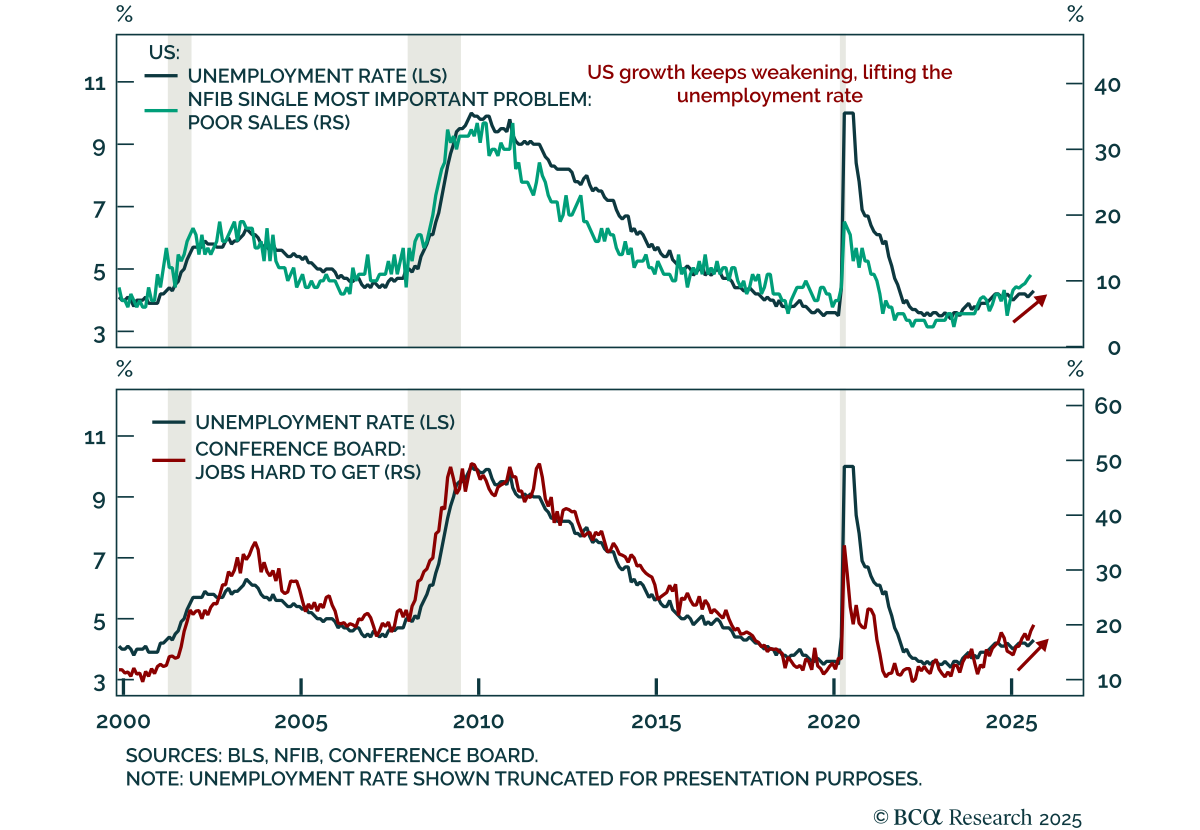

We expect the divergence between resilient growth and weakening employment to be resolved by lower growth estimates, supporting long duration and steepeners. Economic activity and employment usually move together in a circular relationship: spending drives…

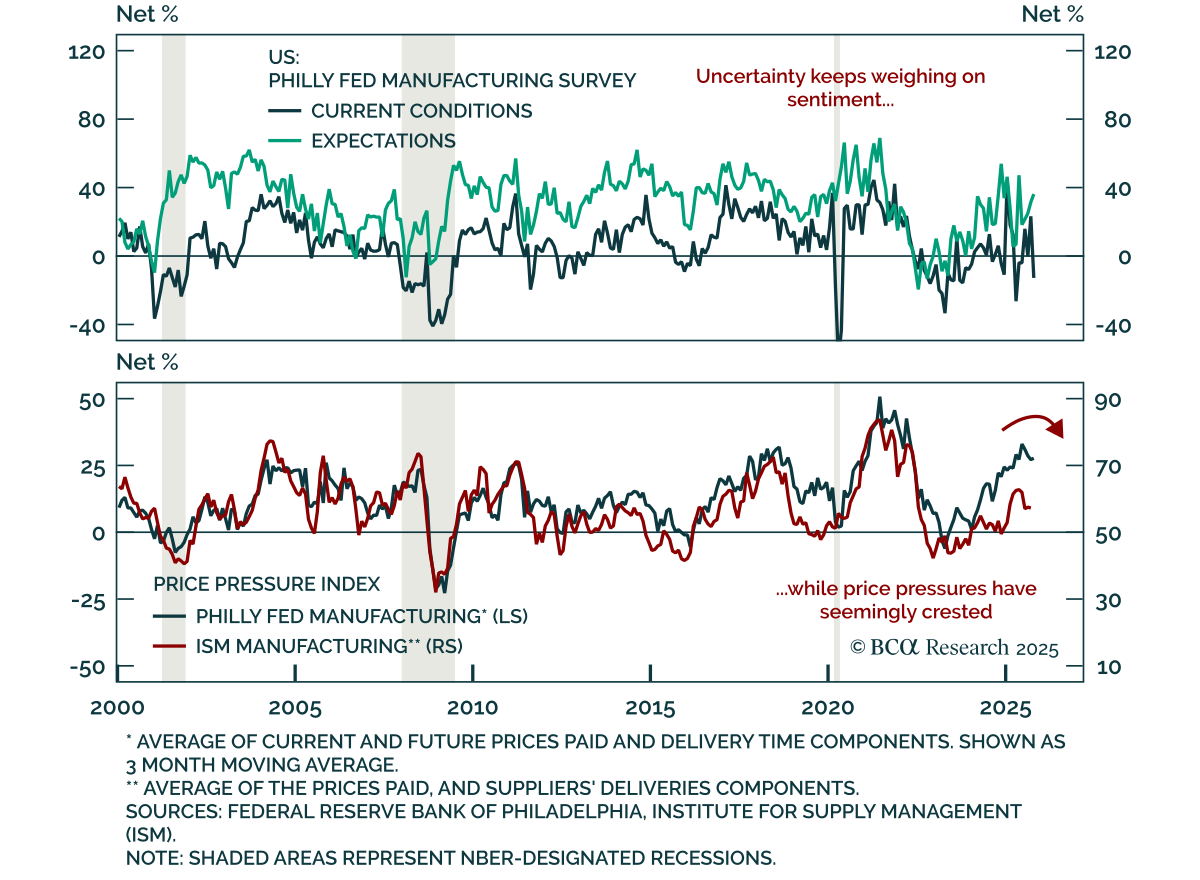

The October Philadelphia Fed manufacturing survey was mixed, showing weak headline data but steadier underlying components. The headline index fell to -12.8 from 23.2, the lowest level since April 2025. Underlying details were not as dire: shipments moderated…

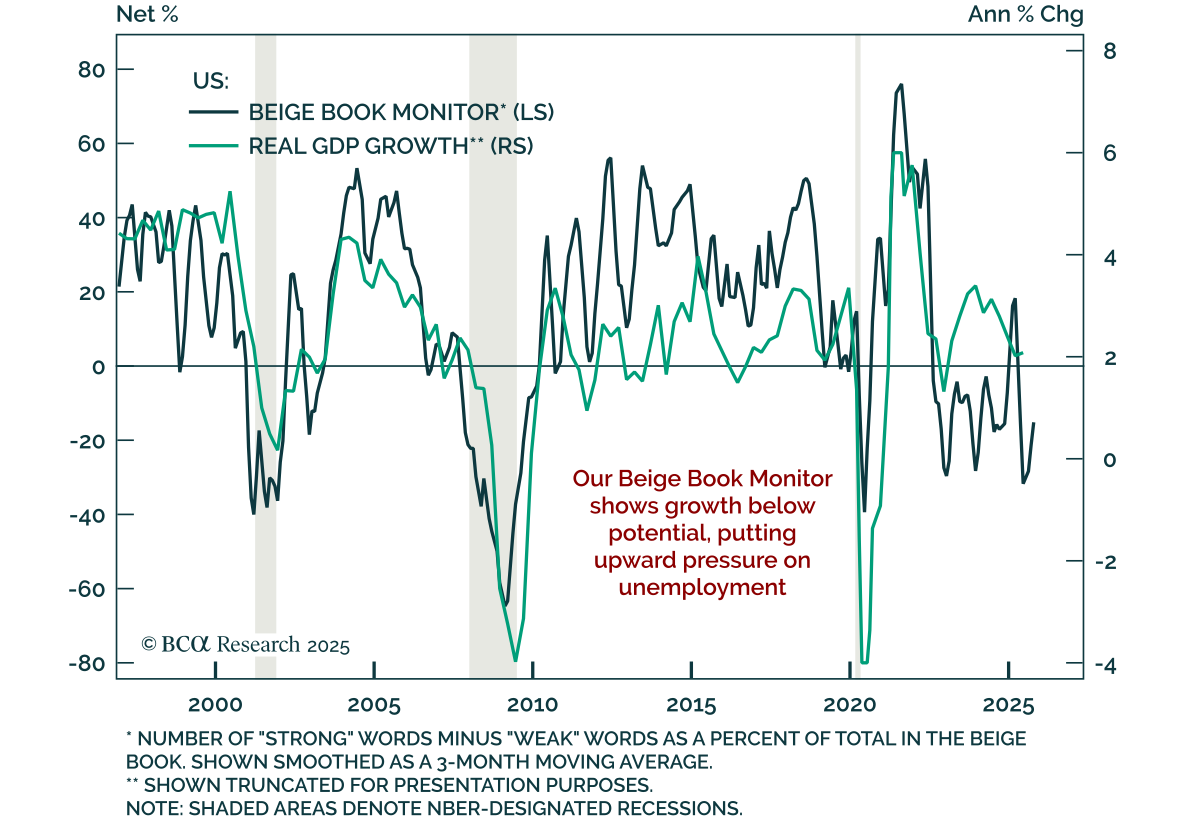

The October Fed Beige Book points to slowing growth as uncertainty continues to weigh on activity. Fed contacts reported consumer spending recently decreased, though auto sales were supported by EV purchases ahead of the expiration of tax credits. Lower- and…

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

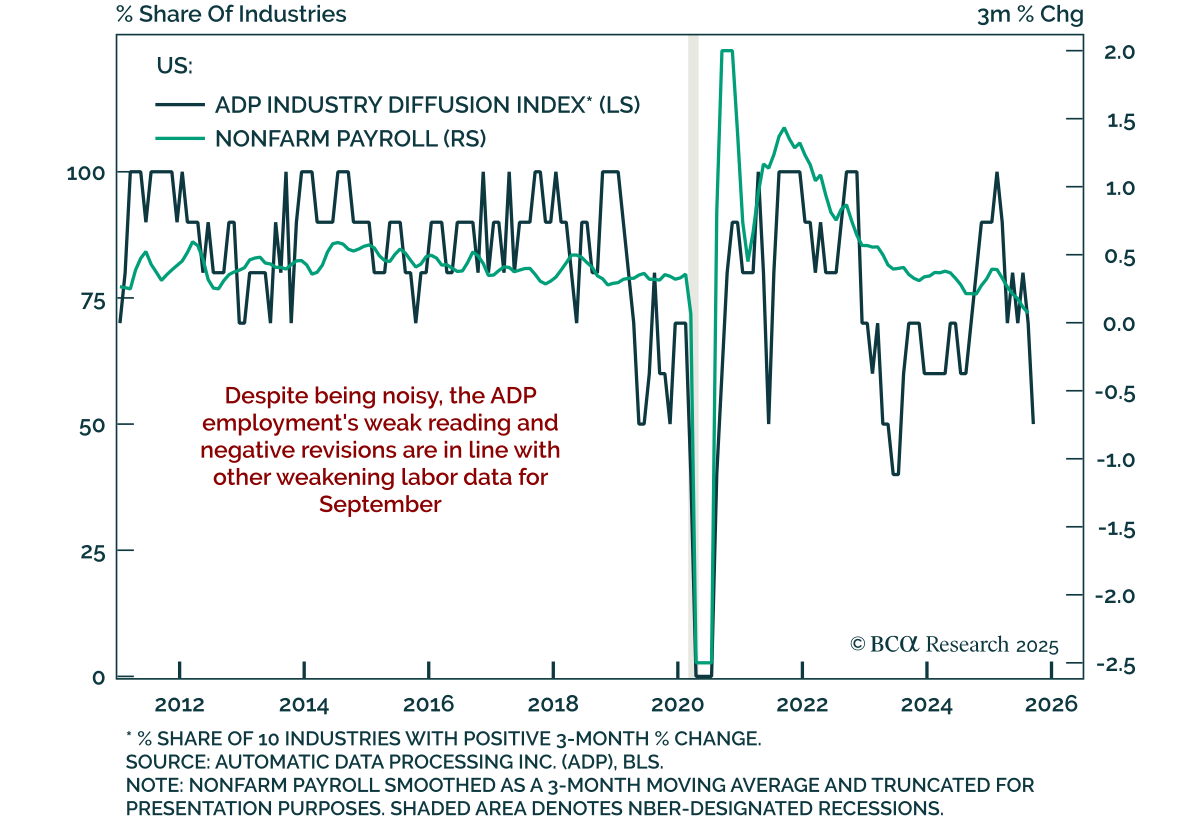

The September ADP report contracted by 32k jobs, missing expectations and extending the trend of weakening employment. August was revised lower to a 3k contraction, marking two consecutive months of decline after also contracting in June. The report was noisy…

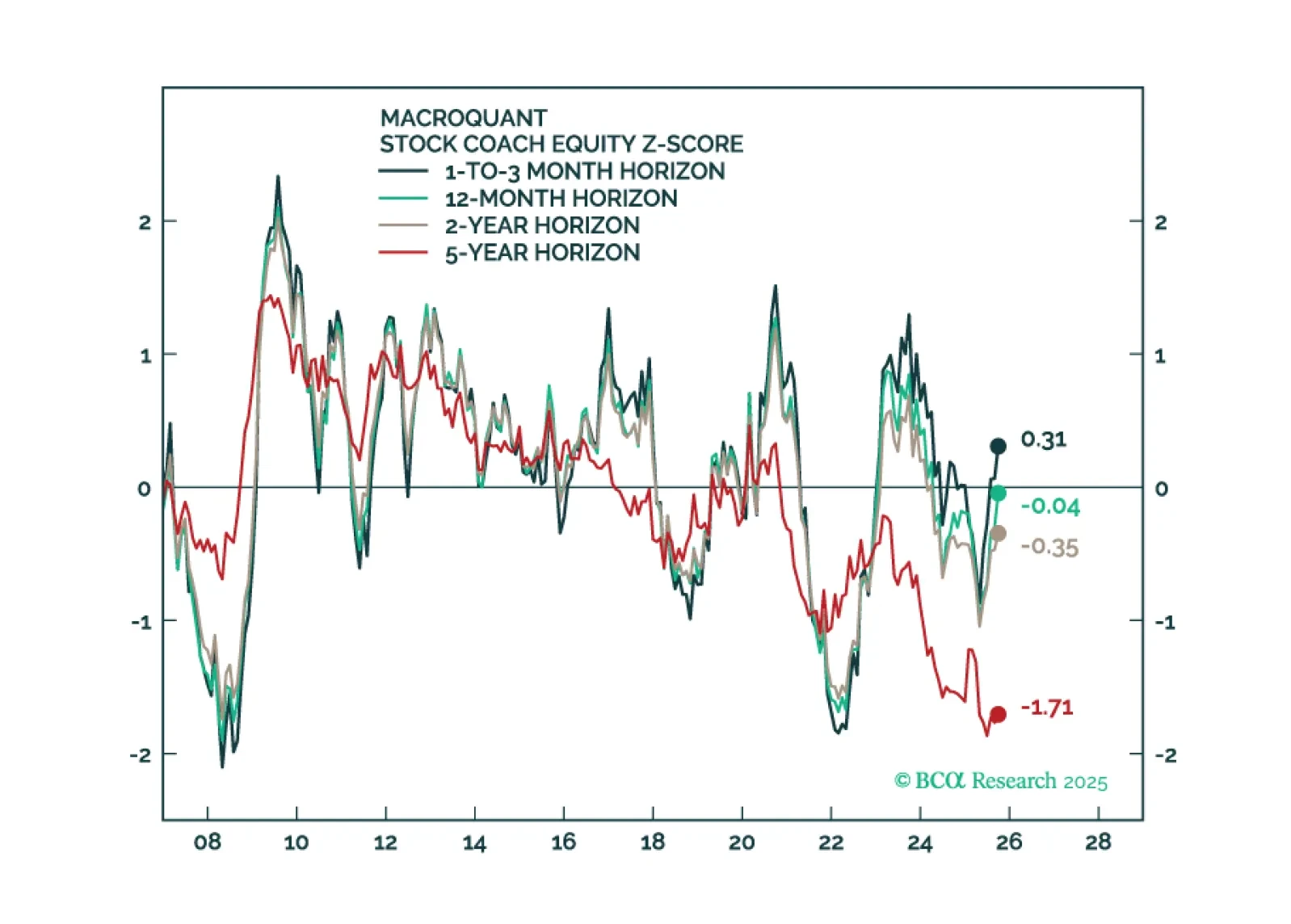

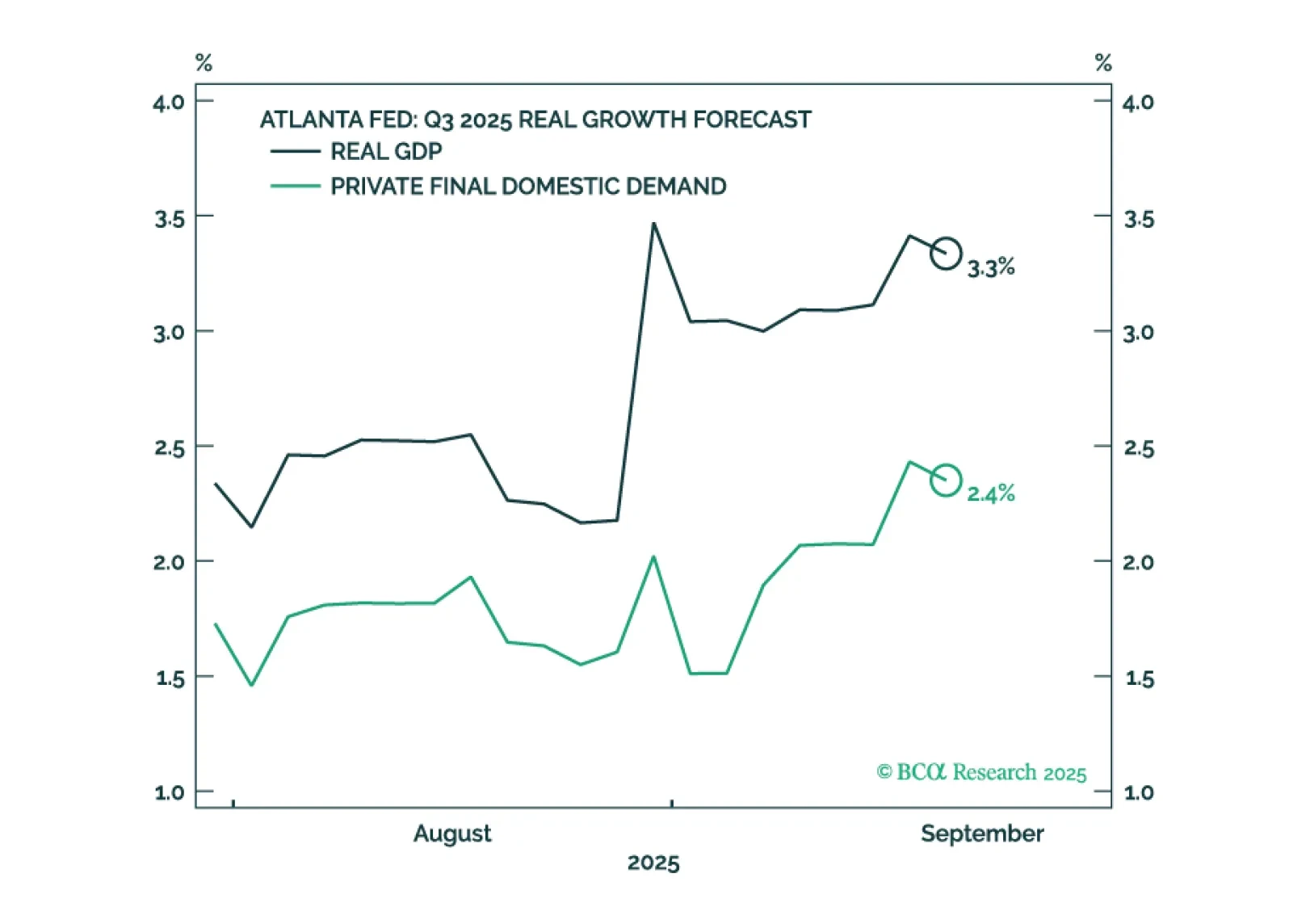

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

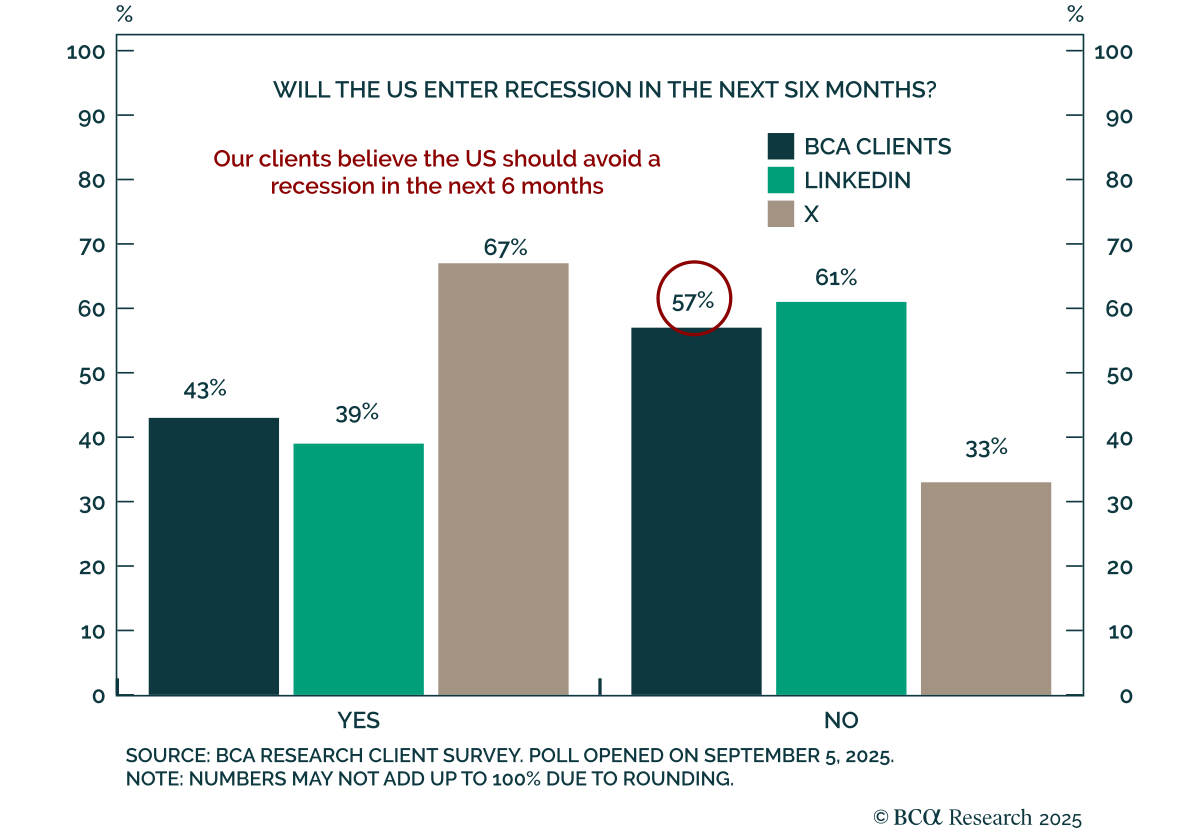

BCA clients are divided on whether the US economy is heading into a recession, but lean towards the view that it will be avoided. In the latest weekly poll on the Have Your Say section of BCA's website, 43% of respondents answered that the US will enter…

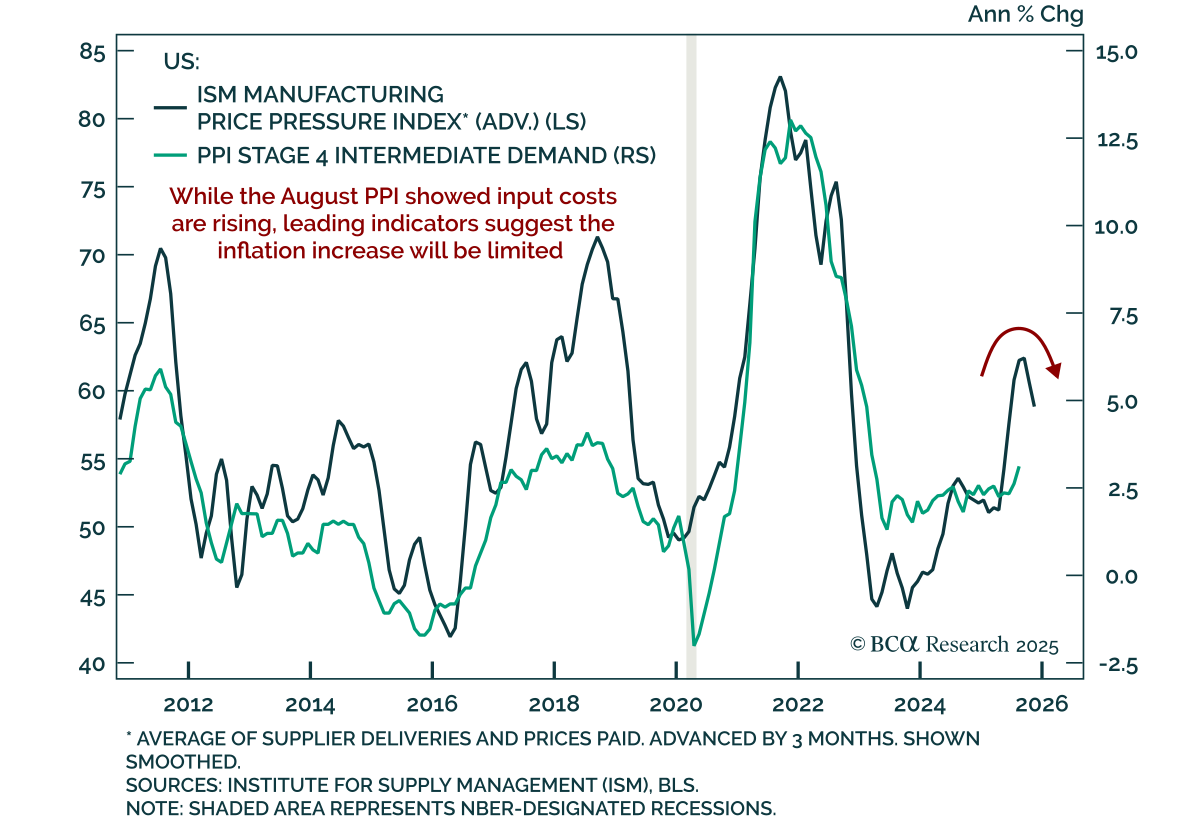

August PPI inflation cooled, reinforcing the case for Fed easing and long duration with steepeners. Headline PPI fell 0.1% m/m, bringing the annual rate down to 2.6% after July’s 0.7% gain. Core PPI (ex-food, energy, and trade) rose 0.3% m/m (2.8% y/y).…

The August US employment report confirmed a significant labor market deceleration, keeping us modestly defensive. Nonfarm payrolls rose just 22k after 79k in July, while net revisions subtracted 21k from prior months. The 3-month average slowed to 29k,…