Recession-Hard/Soft Landing

Executive Summary The Fed, Bank of England (BoE) and Reserve Bank of Australia all hiked rates last week. The BoE, however, signaled a note of caution on future UK growth, given soaring energy prices and plunging consumer and business confidence. Interest rate markets are pricing in a peak in UK policy rates over the next year near 2.5%, above realistic estimates of neutral that are more in the 1.5-2% range. UK productivity and potential growth remain too weak to support a higher neutral rate than that. With the BoE forecasting near recessionary conditions over the next couple of years if those market-implied rate hikes come to fruition, the time is right to increase exposure to UK government bonds in global fixed income portfolios. UK Rate Expectations Are Too High

UK Rate Expectations Are Too High

UK Rate Expectations Are Too High

Bottom Line: Markets are overestimating how much additional tightening the Bank of England can deliver. We are upgrading our recommended strategic stance on UK Gilts from underweight (2 out of 5) to overweight (4 out of 5). Not All Central Bankers Can Credibly Restore Credibility Chart 1Developed Market Bond Yields Back To 2018 Highs

Developed Market Bond Yields Back To 2018 Highs

Developed Market Bond Yields Back To 2018 Highs

Three more central bank meetings, three more rate hikes. Last week brought a 50bp hike from the Fed, a 25bp hike – the first of this tightening cycle – by the Reserve Bank of Australia (RBA) and a 25bp rate increase from the Bank of England (BoE). The Fed and RBA moves did little to stabilize the government bond bear markets in the US and Australia, but the BoE was able to provide a temporary reprieve for the Gilt selloff by playing up potential UK recession (stagflation?) risks. Bond yields worldwide remains laser focused on high global inflation and the associated monetary policy response that will be needed to stabilize inflation expectations (Chart 1). That includes both interest rate hikes and reducing the size of bloated central bank balance sheets. The threat of such “double tightening” is weighing on global growth expectations and risk asset valuations. The MSCI World equity index is down -6.4% (in USD terms) so far in the Q2/2022 and down -14.5% since the mid-November/2021 peak. Although in a more mitigated way, credit markets are also being impacted, with the Bloomberg Global High-Yield index down -2.6% so far in Q2 on an excess return basis versus government bonds. Rate hike expectations have started to catch up to elevated inflation expectations, at least according to inflation linked bonds. The yield on 10-year US TIPS now sits at +0.29%, a huge swing from the -1% level seen just one month ago (Chart 2). The 10-year real yield is even higher in Canada (+0.81%) where the Bank of Canada just delivered its own 50bp rate hike in April. On the other hand, 10-year real yields remain deeply below 0% in Europe and the UK, where central bankers have been providing less explicit guidance on future rate hikes and asset purchase reductions compared to the Fed or Bank of Canada. Interest rate markets remain reluctant to price in significantly positive real policy interest rates at the peak of the current tightening cycle. Our proxy for the real terminal rate expectation, the 5-year/5-year overnight index swap rate (OIS) minus the 5-year/5-year CPI swap rate, is only +0.18% in the US. It is still deeply negative in Europe (-1.53%) and the UK (-0.97%). Our estimates of the term premium component of 10-year government bond yields in those three markets is rising alongside interest rate expectations yet remains deeply negative in Europe and the UK (Chart 3). Chart 2Real Rate Divergences In The Face Of A Global Inflation Shock

Real Rate Divergences In The Face Of A Global Inflation Shock

Real Rate Divergences In The Face Of A Global Inflation Shock

Chart 3Markets Still Pricing In Structurally Low Rates

Markets Still Pricing In Structurally Low Rates

Markets Still Pricing In Structurally Low Rates

Of those three major bond markets, we see the UK term premium as being the least likely to see additional upward repricing, with the BoE less likely than the Fed or ECB to push for an aggressively smaller balance sheet given domestic economic risks. UK Rate Expectations Are Too Hawkish Chart 4Our BoE Monitor Justifies Recent Tightening Moves

Our BoE Monitor Justifies Recent Tightening Moves

Our BoE Monitor Justifies Recent Tightening Moves

The Bank of England raised rates by 25bps last week, pushing Bank Rate to a 13-year high of 1.0%. The decision was a 6-3 majority, with three Monetary Policy Committee (MPC) members calling for a 50bp hike – matching recent moves by other G-10 central banks like the Fed and Bank of Canada – given tight UK capacity constraints (i.e. low unemployment) and high realized inflation. The MPC noted that additional rate increases would likely be necessary to tame very high UK inflation, a message confirmed by the elevated level of our UK Central Bank Monitor (Chart 4). However, the new economic forecasts presented by the BoE painted a gloomy picture on UK growth, raising the risks of a recession even as UK inflation is expected to continue climbing to a 10% peak in late 2022 on the back of high energy prices.1 Strictly looking at current inflation, the case for the BoE to continue hiking rates is obvious. Yet the BoE may now be placing more weight on the downside risks to growth from the energy shock, at a time when fiscal tightening is no longer providing stimulus. In the press conference following last week’s MPC meeting, BoE Governor Andrew Bailey noted the difficult situation policymakers are facing given the huge surge in energy prices that is fueling inflation while also weighing on household and business real incomes. So what is “neutral” anyway? Related Report Global Fixed Income StrategyThe UK Leads The Way The BoE is one of the least transparent major central banks when it comes to providing guidance on what it thinks the neutral policy rate is. Market participants are left to arrive at their own conclusions and those can vary substantially, as is currently the case. The UK OIS curve is discounting a peak in rates of 2.72% in 2023 and discounting rate cuts after that starting in 2024. Yet the respondents to the BoE’s new Market Participants Survey are calling for a much lower trajectory with rates peaking at 1.75% before falling to 1.5% in 2024 (Chart 5). Those rate levels are in the lower half of the range of longer-run neutral rate estimates from the same Market Participants Survey, between 1.5% and 2.0% (the shaded box in the chart). Chart 5UK Rate Expectations Are Too High

UK Rate Expectations Are Too High

UK Rate Expectations Are Too High

Chart 6Recessionary BoE Forecasts, Except For GDP

Recessionary BoE Forecasts, Except For GDP

Recessionary BoE Forecasts, Except For GDP

Combining the messages from the OIS curve and the Survey, markets are pricing in a path for the BoE Bank Rate that will become restrictive by mid-2023, with another 172bps of rate hikes. The BoE uses market pricing for future interest rates in its economic forecasts. The Bank’s models suggest that a move to raise rates to 2.5% in response to high UK inflation, as markets are discounting, would result in a severe UK downturn that would both push up unemployment from the current 3.7% to 5.4% by Q2/2025 (Chart 6). Headline inflation would plunge to 1.3% over the same period as the UK output gap widens to -2.25% of GDP from the current “excess demand” level of +0.5%. Oddly enough, the BoE is only forecasting a flat profile for real GDP growth over that entire three-year forecasting period, although there will clearly be some negative GDP prints during that period to generate such a massively disinflationary outcome. A mixed picture on UK growth Currently, the UK economy is flashing some warning signs on growth momentum. The UK manufacturing PMI was 55.8 in April, still well above the 50 level indicating growth but 9.8 pts below the cyclical peak in 2021 (Chart 7). The services PMI is in better shape at 58.9, but it did dip lower in the latest reading. The GfK consumer confidence index has fallen sharply in response to contacting real household income growth, reaching the second-lowest reading in the history of the series dating back to 1974 in April. This is a warning sign for consumer spending – retail sales fell in April for the first time in fifteen months (middle panel). Business confidence is also impacted by the high costs of both energy and labor that is squeezing profit margins. UK real investment spending is nearly contracting on a year-over-year basis, despite the robust readings on investment intentions from the BoEs’ Agents Survey of UK businesses (bottom panel).UK firms are facing higher wage costs at a time of very tight labor market and robust labor demand. The BoE estimates that UK private sector wage growth, after adjusting for compositional effects related to the pandemic, will accelerate to 5.1% by the end of Q2/2022 (Chart 8). Chart 7UK Growth Facing Inflationary Headwinds

UK Growth Facing Inflationary Headwinds

UK Growth Facing Inflationary Headwinds

Chart 8UK Labor Market Remains Healthy

UK Labor Market Remains Healthy

UK Labor Market Remains Healthy

Chart 9Will House Prices Signal The Peak In UK Inflation?

Will House Prices Signal The Peak In UK Inflation?

Will House Prices Signal The Peak In UK Inflation?

A robust labor market and quickening wage growth is forcing the BoE to maintain a relatively hawkish bias at a time of high energy inflation, even with the growth outlook darkening in the central bank’s own forecasts. Booming house prices are also making the central bank’s job more challenging. The annual growth rate of the Nationwide UK house price index reached 12.4%, a 17-year high, in March. However, rising mortgage rates and declining household real incomes will likely begin to eat into housing demand and, eventually, help slow the rapid pace of house price growth (Chart 9, bottom panel). Summing it all up, the overall UK inflation picture, including wages and housing costs in addition to energy prices and durable goods prices, will force the BoE to deliver a few more rate hikes before year-end before reaching a peak level that is lower than current market pricing. The neutral UK interest rate is likely very low Chart 10Structurally Weak UK Growth = A Low Neutral Rate

Structurally Weak UK Growth = A Low Neutral Rate

Structurally Weak UK Growth = A Low Neutral Rate

The UK economy has suffered from structurally low potential economic growth dating back to the Brexit referendum in 2016. UK businesses stopped investing in the face of the uncertainty over the UK’s relationship with Europe. There has basically been no growth in UK fixed investment over the past five years. In response, UK productivity has only grown an annualized 0.9% over that same period (Chart 10) and the OECD’s estimate of UK potential GDP growth has been cut from 2% to 1.1%. With such low potential growth, the neutral BoE policy interest rate is likely even lower than the 1.5-2% range of estimates from the BoE’s Market Participant Survey. Tighter fiscal policy also lowers the neutral UK interest rate, with the UK Office of Budget Responsibility forecasting a narrowing of the UK budget deficit of -13.6 percentage points between the 2021 peak and 2027 (bottom panel). A flat UK Gilt curve is also a sign that the neutral interest rate is quite low. The 2-year/10-year Gilt curve now sits at a mere -49bps with Bank Rate only at 1% (Chart 11). While this is modestly steeper from the near-inversion of the curve seen at the start of 2022, a very flat curve at a nominal policy rate of only 1% suggests that the neutral rate is not far from the current level. Sluggish UK equity market performance and widening UK corporate credit spreads also argue that Bank Rate may already be turning restrictive, although a lower trade-weighted pound is helping to mitigate the overall tightening of UK financial conditions. Chart 11UK Financial Conditions Are Not Restrictive (Yet)

UK Financial Conditions Are Not Restrictive (Yet)

UK Financial Conditions Are Not Restrictive (Yet)

Chart 12Pressure On The BoE Will Not Peak Until Inflation Does

Pressure On The BoE Will Not Peak Until Inflation Does

Pressure On The BoE Will Not Peak Until Inflation Does

In the end, the pressure on the BoE to tighten will not ease until UK inflation peaks. The BoE is suffering a severe credibility crisis, with its own public opinion survey showing the deepest level of public dissatisfaction with the bank since the Global Financial Crisis (Chart 12). Inflation expectations are at similar levels that prevailed during that period, although the unique nature of the current inflation upturn, fueled by global supply-chain squeezes and war-related boosts to commodity prices, will likely prevent a repeat of the relatively fast reversal of inflation expectations seen after the Global Financial Crisis. Investment Implications – Get Ready For Gilt Outperformance Chart 13Upgrade UK Gilts To Overweight

Upgrade UK Gilts To Overweight

Upgrade UK Gilts To Overweight

With the BoE already pushing Bank Rate towards a plausible neutral range, we do not expect many more rate hikes in the UK. Our base case is that the BoE hikes 2-3 more times by year-end, pushing Bank Rate to 1.5-1.75%, before pausing. This would represent a lower peak in policy rates than currently priced in the UK OIS curve. That is a relatively dovish outcome that typically leads to positive performance for a government bond market according to our “Global Golden Rule” framework, which we will revisit in next week’s Strategy Report. For now, however, we see a strong case to turn more positive on UK Gilts, with the BoE likely to deliver fewer rate hikes than discounted (Chart 13). The BoE is also far less likely to begin reducing its balance sheet by selling its Gilt holdings back to the market. BoE Governor Bailey strongly hinted last week that such aggressive quantitative tightening (QT) was not a given, even after the Bank research staff presents its proposals to the MPC in August. A delay in QT would also be a factor boosting UK Gilt performance versus other developed economy bond markets where more aggressive reductions in central bank balance sheets are more likely, like the US and potentially even the euro area. This week, we are upgrading our recommended strategic UK weighting from underweight to overweight. In next week’s report, we will consider the proper allocation for the UK within our model bond portfolio, after reviewing potential bond return forecasts stemming from our Global Golden Rule. Bottom Line: Markets are overestimating how much additional tightening the Bank of England can deliver. We are upgrading our recommended strategic stance on UK Gilts from underweight (2 out of 5) to overweight (4 out of 5). Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 The mechanical way that the UK government’s energy price regulator, Ofgem, sets price caps on retail gas and electricity costs - based on changes in wholesale energy costs implied by futures curves – means that UK household energy prices will rise by 40% in October, according to BoE estimates. GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

It’s Time To Flip The Script - Upgrade UK Gilts

It’s Time To Flip The Script - Upgrade UK Gilts

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

It’s Time To Flip The Script - Upgrade UK Gilts

It’s Time To Flip The Script - Upgrade UK Gilts

Tactical Overlay Trades

In lieu of next week’s report, I will be presenting a webcast titled ‘The 5 Big Mispricings In The Markets Right Now, And How To Profit From Them’. I do hope you can join. Executive Summary Just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes are setting in train a global recession. Demand is already cool, so aggressive rate hikes will take it to outright cold. The risk is elevated because central banks are desperate to repair their damaged credibility on fighting inflation, and it may be their last chance. Inflationary fears and hawkishness from central banks are weighing on bonds and stocks, and it may take some weeks, or months, for inflation fears to recede. But we could be approaching a turning point. By the summer, core inflation should be receding. Furthermore, the fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility that have signalled inflection points. Fractal trading watchlist: 30-year T-bond, NASDAQ, FTSE 100 versus Euro Stoxx 50, Netherlands versus Switzerland, and Petcare (PAWZ). US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

Bottom Line: Tactically cautious, but long-term investors who do not need to time the market bottom should overweight bonds and overweight long-duration defensive equities versus short-duration cyclical equities – for example, overweight US versus non-US equities. Feature The First World War, the historian AJP Taylor famously argued, was “imposed on the statesmen of Europe by railway timetables.” Taylor proposed that the railways and their timetables were so central to troop mobilisation – and specifically, the German Schlieffen Plan – that a plan once set in motion could not be stopped. “Once started the wagons and carriages must roll remorselessly and inevitably to their predestined goal.” Otherwise, the whole process would unravel, and an opportunity to demonstrate military credibility would be lost that might never come again. Today, could a global recession be imposed upon us by central bank timetables for aggressive rate hikes? Just as it was difficult to unwind the troop mobilisation that led to the Great War, it will be difficult to back down from the aggressive rate hikes that the central banks have timetabled, at least in the near term. Otherwise, an opportunity to demonstrate inflation fighting credibility would be lost that might never come again. Just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes may set in train another global recession. Unfortunately, central banks do not have precision weapons. Quite the contrary, monetary tightening is a blunt instrument which works by cooling overall demand. But demand is already cool, as evidenced by the contraction of the US economy in the first quarter. In their zeal to repair their damaged credibility on fighting inflation, the danger is that central banks take the economy from cool to outright cold. Granted, the US economy was dragged down by a drop in inventories and net exports. But even US domestic demand – which strips out inventories and net exports – is barely on its pre-pandemic trend (Chart I-1). Meanwhile, the euro area economy is still 5 percent below its pre-pandemic trend (Chart I-2). To reiterate, by hiking rates aggressively into economies that are at best lukewarm, central banks are risking an outright recession. Chart I-1US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

US Inflation Is Hot, But Demand Is Not

Chart I-2Euro Area Inflation Is Hot, But Demand Is Not

Euro Area Inflation Is Hot, But Demand Is Not

Euro Area Inflation Is Hot, But Demand Is Not

Our Three-Point Checklist For A Recession Has Three Ticks My colleague Peter Berezin has created a three-point checklist for a recession: The build-up of an imbalance makes the economy vulnerable to downturn. A catalyst exposes this imbalance. Amplifiers exacerbate the downturn. Is there a major imbalance? You bet there is. The post-pandemic 26 percent overspend on durable goods in the US constitutes one of the greatest imbalances in economic history. Other advanced economies also experienced unprecedented binges on durable goods. The catalyst that is exposing this major imbalance is the realisation that durable goods are, well, durable. So, if you overspent on durables in 2020/21, then the risk is that you symmetrically underspend in 2022/23 (Chart I-3). The post-pandemic 26 percent overspend on durable goods in the US constitutes one of the greatest imbalances in economic history. Meanwhile, a future underspend on goods cannot be countered by an overspend on services because the consumption of services is constrained by time, opportunity, and biology. There is a limit to how often you can eat out, go to the movies, or go to the doctor (Chart I-4). Indeed, for certain services, an underspend will persist, because we have made some permanent post-pandemic changes to our lifestyles: for example, hybrid office/home working and more online shopping and online medical care. Chart I-3An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

An Overspend On Goods Can Be Corrected By A Subsequent Underspend...

Chart I-4...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

...But An Underspend On Services Cannot Be Corrected By A Subsequent Overspend

Finally, the amplifier that will exacerbate the downturn is monetary tightening. If central banks follow their railway timetables for aggressive rate hikes, a goods downturn will magnify into an outright recession. So, in Peter’s three-point checklist, we now have tick, tick, and tick. Inflation Is Hot, But Demand Is Not If economic demand is at best lukewarm, then what caused the post-pandemic inflation that central banks are now fighting? The simple answer is massive fiscal stimulus combined with the equally massive shift in spending to durable goods. Locked at home and flush with government supplied cash, we couldn’t spend it on services, so we spent it on goods. This created a massive shock in the distribution of demand, out of services whose supply could easily adjust downwards, and into goods whose supply could not easily adjust upwards. For example, airlines could cut back their flights, but auto manufacturers couldn’t make more cars. So, airfares didn’t collapse but used car prices went vertical! The causality from stimulus payments to durable goods spending to core inflation is irrefutable. The causality from stimulus payments to durable goods spending to core inflation is irrefutable. The biggest surges in US durable goods spending all coincided with the government’s stimulus checks (Chart I-5). And the three separate surges in month-on-month core inflation all occurred after surges in durable goods demand (Chart I-6). As further proof, core inflation is highest in those economies where the stimulus checks and furlough schemes were the most generous – like the US and the UK. Chart I-5Stimulus Checks Caused The Surges in Durable Goods Spending

Stimulus Checks Caused The Surges in Durable Goods Spending

Stimulus Checks Caused The Surges in Durable Goods Spending

Chart I-6The Surges In Durable Goods Spending Caused The Surges In Core Inflation

The Surges In Durable Goods Spending Caused The Surges In Core Inflation

The Surges In Durable Goods Spending Caused The Surges In Core Inflation

What Does All This Mean For Investment Strategy? Our high conviction view is that the pandemic’s inflationary impulse combined with the Ukraine war will turn out to be demand-destructive, and thereby ultimately morph into a deflationary impulse. Yet central banks are all pumped up to demonstrate their inflation fighting credibility. Given that this credibility is badly damaged, it may be their last opportunity to repair it before it is shattered forever. To repeat, just as the railway timetables set in train the First World War, central bank timetables for aggressive rate hikes may set in train another global recession. That said, a recession is not inevitable. The interest rate that matters most for the economy and the markets is not the policy rate that central banks want to hike aggressively, it is the long-duration bond yield. A lower bond yield can underpin both the economy and the financial markets, just as it did during the pandemic in 2020. But to the extent that the bond market is following the real economic data, we are in a dangerous phase. Because, as is typical at an inflection point, the real data will be noisy and ambiguous. Meaning it may take some weeks, or months, for inflation fears to be trumped by growth fears. On March 10th, in Are We In A Slow-Motion Crash? we predicted: “On a tactical (3-month) horizon, the inflationary impulse from soaring energy and food prices combined with the choke on growth from sanctions will weigh on both the global economy and the global stock market. As such, bond yields could nudge higher, the global stock market has yet to reach its crisis bottom, and the US dollar will rally” That prediction proved to be spot on! Recession, or no recession, we are still in a difficult period for markets because inflationary fears and hawkishness from central banks are weighing on bonds and stocks, while buoying the US dollar. As such, tactical caution is still warranted. Fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility. But we could be approaching a turning point. By the summer, core inflation should be receding. Furthermore, the fractal structures of the sell-offs in both the 30-year T-bond and the tech-heavy NASDAQ index are approaching points of extreme fragility that have reliably signalled previous inflection points (Chart I-7 and Chart I-8). Chart I-7The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

The Sell-Off In The 30-Year T-Bond Is Approaching Fractal Fragility

Chart I-8The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The Sell-Off In The NASDAQ Is Approaching Fractal Fragility

The advice for long-term investors who do not need to time the market bottom is: Bonds will ultimately rally. Overweight the 30-year T-bond and the 30-year Chinese bond. Equities will be conflicted between slowing growth which will weigh on cyclical profits, and falling bond yields which will buoy long-duration valuations. Therefore, overweight long-duration defensive sectors and markets versus short-duration cyclical sectors and markets. For example, overweight US versus non-US equities. Fractal Trading Watchlist As just discussed, the sell-offs in the 30-year T-bond and the NASDAQ are approaching points of fractal fragility that have signalled previous turning points. Hence, we are adding both investments to our watchlist. Also added to our watchlist is the outperformance of the FTSE100 versus Euro Stoxx 50, and the underperformance of Netherlands versus Switzerland, both of which are approaching potential reversals. Our final addition is Petcare (PAWZ). After a stellar 2020, Petcare gave back most of its gains in 2021. But this underperformance is now approaching a point of fragility which might provide a new entry point. There are no new trades this week, but the full watchlist of investments at, or approaching, turning points is available on our website: cpt.bcaresearch.com Fractal Trading Watchlist: New Additions A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Chart 1The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

The Strong Trend In The 18-Month-Out US Interest Rate Future Is Fragile

Chart 2The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

The Strong Trend In The 3 Year T-Bond Is Fragile

Chart 3AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

AUD/KRW Is Vulnerable To Reversal

Chart 4Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Canada Versus Japan Is Reversing

Chart 5Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Canada's TSX-60's Outperformance Might Be Over

Chart 6US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

US Healthcare Providers Vs. Software At Risk of Reversal

Chart 7A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

A Potential Switching Point From Tobacco Into Cannabis

Chart 8Biotech Is A Major Buy

Biotech Is A Major Buy

Biotech Is A Major Buy

Chart 9CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

CAD/SEK Reversal Has Started

Chart 10Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Financials Versus Industrials To Reverse

Chart 11Norway's Outperformance Could End

Norway's Outperformance Could End

Norway's Outperformance Could End

Chart 12Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Greece's Brief Outperformance To End

Chart 13BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

BRL/NZD At A Resistance Point

Chart 14The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

The Outperformance Of Resources Versus Healthcare Is Vulnerable To Reversal

Chart 15The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

The Outperformance Of Resources Versus Biotech Has Started To Reverse

Chart 16Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Cotton's Outperformance Is Vulnerable To Reversal

Chart 17US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

US Homebuilders' Underperformance Has Reached A Potential Turning Point

Chart 18Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Switzerland's Outperformance Vs. Germany Has Started To End

Chart 19The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

The Rally In USD/EUR Could End

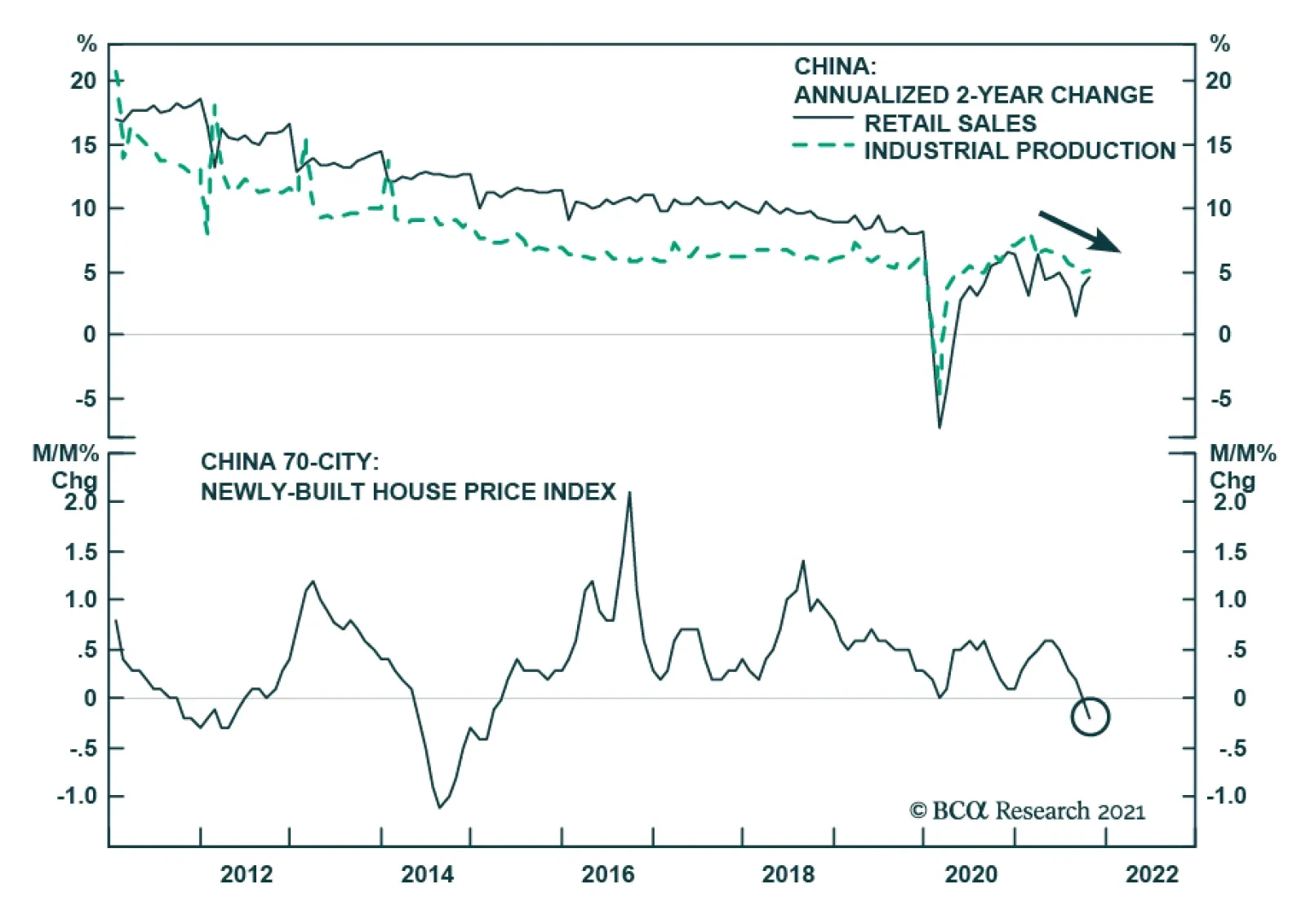

Chart 20The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

The Outperformance Of MSCI Hong Kong Versus China Is Vulnerable To Reversal

Chart 21A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

A Potential New Entry Point Into Petcare

Chart 22FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

FTSE100 Outperformance Vs. Euro Stoxx 50 Vulnerable To Reversal

Chart 23Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Netherlands Underperformance Vs. Switzerland Close To Exhaustion

Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Fractal Trading System Fractal Trades

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

Central Bank ‘Railway Timetables’ Are Dragging Us Into Recession

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Several factors point to both an improvement and a deterioration in economic and financial market conditions, underscoring that the 6- to 12-month investment outlook is unavoidably uncertain. On the one hand, the US will likely avoid a recession over the coming year, slowing headline inflation will boost real wages and lower the equity risk premium, bond yields will not move much higher this year, and US services spending will support consumption as the pandemic continues to recede in importance. These are positive factors that will work to support economic activity and risky asset prices. On the other hand, the US will likely experience a recession scare focused on the housing market, the European economy may contract, Omicron’s spread in China threatens a further rise in shipping costs and a trade shock for Europe, and US inflation expectations may unanchor despite a falling inflation rate. For now, investors should remain minimally-overweight stocks over a 6- to 12-month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. Within a global equity allocation, we recommend that investors maintain a neutral regional stance. The larger risk of a recession in Europe than in the US would normally imply that investors should be overweight US stocks, but euro area stocks have already underperformed global stocks significantly since Russia’s invasion of Ukraine. Within a fixed-income portfolio, we recommend that investors maintain a modestly short duration stance despite our forecast that long-maturity bond yields will not increase much this year. More nimble investors should be neutral duration, and should test a long stance if US data releases begin to exhibit meaningfully negative surprises. The US dollar is likely to strengthen over the near term, but we expect it to be lower a year from today. The Scourge Of Harry Truman US President Truman famously lamented the need for “one-handed” economists. His complaint reflected how essential it is for economic policymakers to receive clear advice about the best path forward. Investors understandably have even less tolerance for ambiguity than Truman did about the macro landscape and the attendant investment implications. However, there are times when the economic and financial market outlook is unavoidably uncertain. The current economic and geopolitical environment easily qualifies as one of those instances. Several factors point to both an improvement and a deterioration in economic and financial market conditions, which we review in detail below. The likely avoidance of a recession in the US over the coming year suggests that investors should remain minimally-overweight stocks over a 6- to 12-month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. What Could Go Right The US Will Likely Avoid A Recession Over The Coming Year Chart I-1The Odds Of A US Recession Are Currently Low

The Odds Of A US Recession Are Currently Low

The Odds Of A US Recession Are Currently Low

We downgraded our odds of an above-trend 2022 growth scenario in last month’s report,1 but noted that a stagflation-lite environment of below-trend growth and above-target inflation was a more likely outcome than recession. We based this assessment on our view that the US neutral rate of interest is likely higher than the Fed and investors expect, which we discussed at length in past reports.2 Chart I-1 highlights that our recession probability indicator also supports this view, as it does not yet signal that a recession is on the horizon.3 Table I-1 highlights the components of the model (which is significantly influenced by the Conference Board’s LEI), and shows that the model is not providing a meaningful warning signal. The Fed funds rate component of the model will likely flash red next month following the FOMC meeting, and we have listed it as providing a warning signal in Table I-1. But rising rates themselves have not proven to be a particularly timely indicator of a recession; this is similarly true with rising inflation expectations and oil prices. We noted in last month’s report that a surge in oil prices has not been an especially consistent indicator of a recession since 2000. Table I-1The Components Of Our Recession Model Are Not Yet Flashing A Warning Sign

May 2022

May 2022

The yield curve component of the model is based on the spread between the 10-year Treasury yield and the 3-month T-bill yield in order to minimize false recession signals, and we agree that the 10-year / 2-year spread has better leading properties. But even the latter curve measure has recently moved back into positive territory (Chart I-2), which will certainly qualify as a false yield curve signal if a recession is avoided over the coming 18 months. Within the components of the Conference Board’s LEI, Table I-1 highlights that there have been signs of weakness from the manufacturing sector, consumer expectations, and the credit market. Chart I-3 aggregates the deviation of six of these components from their trend, and shows that they have indeed been consistent with a significant slowdown in economic activity. Chart I-2The 2/10 Yield Curve Is No Longer Inverted

The 2/10 Yield Curve Is No Longer Inverted

The 2/10 Yield Curve Is No Longer Inverted

Chart I-3The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

The Weakest Components Of The Conference Board's LEI Are Not Yet Signaling A Recession

However, two caveats are warranted. First, part of this weakness reflects the ongoing shift from goods to services spending, unraveling the massive surge in goods spending that occurred during the pandemic (Chart I-4). Second, Chart I-3 highlights that similar weaknesses occurred in the past outside of the context of a recession, most notably in 1995/1996, in the aftermath of the 1994 bond market crisis; in 1998/1999, following the Long-Term Capital Management (LTCM) crisis; in 2015, following the collapse in oil prices; and, finally, in 2018/2019, in response to the Trump administration’s trade war. None of these instances resulted in a contraction in output. Headline Inflation Is Likely To Come Down Headline consumer price inflation is currently extremely high in the US. Rising prices do not just reflect energy, food, or pandemic-related effects. Chart I-5 highlights that trimmed mean CPI and PCE inflation rates have accelerated significantly since last summer, and are currently running at 6% and 3.6% year-over-year rates, respectively. Chart I-4Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Part Of The Weakness In Manufacturing Activity Indicators Reflects A Shift In Spending From Goods To Services

Chart I-5There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

There Is More To High Inflation Than Food, Energy, And Pandemic-Related Effects...

However, it seems likely that inflation has peaked in the US (or is about to do so), even abstracting from base effects.Chart I-6 highlights that the one-month rate of change in trimmed mean measures seemingly peaked in October and January, and shows that the level of used car prices also appears to be trending lower (panel 2). The ongoing shift away from goods to services spending noted above will also push core ex-COVID-related consumer prices lower. Finally, BCA’s Commodity & Energy strategy service is forecasting that Brent crude oil prices will average roughly $90/bbl for the remainder of the year, which would likely bring US gasoline prices back toward $3.50/gallon and will lower both headline inflation and energy passthrough effects to core prices (Chart I-7). Chart I-6... But The Rate Of Headline Inflation Has Likely Peaked

... But The Rate Of Headline Inflation Has Likely Peaked

... But The Rate Of Headline Inflation Has Likely Peaked

Chart I-7Our Forecast For Oil Implies US Gasoline Prices Will Fall

Our Forecast For Oil Implies US Gasoline Prices Will Fall

Our Forecast For Oil Implies US Gasoline Prices Will Fall

A meaningful deceleration in inflation will help reverse some of the recent decline in real wage growth that has occurred, and will likely lower the equity risk premium (see Section 2 of this month’s report). Long-Maturity Bond Yields Will Not Move Much Higher This Year Chart I-8Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Our Inflation Probability Model Is Signaling Core Inflation That Is Roughly In Line With The Fed's Latest Forecast

Chart I-8 highlights that our inflation probability model is currently signaling core PCE inflation of roughly 4.3% over the coming year. This is only moderately above the Fed’s forecast for this year, suggesting that a moderation in the rate of inflation makes it more likely that the Fed will raise rates in line with, or only moderately above, what was projected in the March Summary of Economic Projections (1.9% by the end of this year, and 2.8% by the end of 2023). By contrast, Chart I-9 highlights that the OIS curve is pricing the Fed funds rate at 80 basis points higher by the end of this year than what the Fed projected in March, suggesting that the bar for further hawkish surprises is quite high. We agree that the Fed will likely front-load a good portion of its planned tightening this year, and we agree that a 50 basis point hike is likely next month and also possibly in June. However, it is quite possible that the Fed will ultimately raise rates over the coming year at a slower pace than investors currently anticipate, which would lower yields at the front end of the curve. Chart I-9The Bar For Further Hawkish Surprises From The Fed Is Quite High

May 2022

May 2022

If short-maturity yields are flat or trend modestly lower over the coming year, then a significant further rise in long-maturity yields would likely necessitate a major shift in neutral rate expectations on the part of investors or the Fed. We believe that such a shift will eventually occur, as the economic justification for long-maturity bond yields well below trend rates of economic growth disappeared in the latter half of the last economic expansion. However, we noted in last month’s Special Report that a low neutral rate outlook has become entrenched in the minds of investors and the Fed, and is only likely to change once the Fed funds rate rises meaningfully and a recession does not materialize.4 BCA’s fixed-income team currently recommends that investors maintain a neutral duration stance; the Bank Credit Analyst service is more inclined to recommend a modestly short stance. However, the key point for investors is that another significant rise in long-maturity bond yields is unlikely over the coming year, which is positive for economic activity and investor sentiment. The Pandemic Will Recede In Importance, Supporting Services Spending Chart I-10COVID Hospitalizations And Deaths Remain Low In The DM World

COVID Hospitalizations And Deaths Remain Low In The DM World

COVID Hospitalizations And Deaths Remain Low In The DM World

While the pandemic is clearly not over in China (discussed below), it is likely to continue to recede in importance in the US and other highly vaccinated, and relatively highly exposed DM economies. Despite the fact that confirmed cases of COVID-19 have risen in the DM world in March and April, Chart I-10 highlights that there has been very little increase in ICU patients or deaths. A recent study from the US CDC suggests that 58% of the US population overall and more than 75% of younger children have been infected with the SARS-COV-2 virus since the start of the pandemic.5 When combined with a vaccination rate close to 70%, that signals an extraordinarily high national immunity to severe illness from the disease. Chart I-11 also highlights that deliveries of Pfizer’s Paxlovid continue to climb in the US, a drug that seemingly works against all known variants and has been found to reduce hospitalizations from COVID significantly if taken within the first five days of symptoms. Given that the decline in services spending that we showed in Chart I-4 has been clearly linked to the pandemic, we expect that a slowing pandemic will continue to support services spending. Goods spending is normally a more forceful driver of economic activity than is the case for services spending, but the magnitude of the recent contribution to growth from services spending has been absolutely unprecedented in the post-World War II economic environment (Chart I-12). This underscores that a continued recovery in services spending relative to its pre-pandemic trend will provide a ballast to overall consumer spending as goods spending continues to normalize. Chart I-11Paxlovid To The Rescue!

Paxlovid To The Rescue!

Paxlovid To The Rescue!

Chart I-12Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

Real Services Spending Will Continue To Be A Forceful Driver Of US Economic Activity

What Could Go Wrong The US Will Likely Experience A Recession Scare Chart I-13US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

US Housing Affordability Has Cratered, In Large Part Due To Surging House Prices

Despite our view that the US economy will avoid a recession over the coming year, it seems likely that investors will experience a recession scare at some point over the coming 6 to 12 months. Even though it has recently moved back into positive territory, the inversion of the 2-10 yield curve has set the scene for a recessionary overtone to any visible weakness in the US macro data over the coming months. We noted above that the manufacturing and goods-producing sectors of the US economy are likely to slow as spending returns to services. More importantly, the extremely sharp increase in mortgage rates will likely cause at least a temporary slowdown in US housing activity, even if that slowdown does not ultimately prove to be contractionary.Chart I-13 highlights that the recent increase in mortgage rates will cause US housing affordability to deteriorate back to 2007 levels. While rising mortgage rates will be the proximate cause of this deterioration in affordability, panel 2 highlights that the real culprit has been a significant increase in house prices relative to income. There is strong evidence pointing to the fact that US real residential investment has been too weak since the global financial crisis (GFC).6 We agree that high prices will likely spur additional housing construction (which will support growth). But over the nearer-term, the sharp deterioration in affordability may imply that house price appreciation will have to fall below the rate of income growth, which would represent a very sharp correction in house price gains that would almost assuredly appear recessionary for a time. The European Economy May Contract We have discussed the risk of a European recession in past reports, and noted that it would be almost certain to occur in a scenario in which Russia’s energy exports to Europe were to be completely cut off. We continue to see this as an unlikely scenario, although the odds have increased significantly of late in light of Russia’s halt of gas supplies to Bulgaria and Poland and Germany’s apparent acceptance of an oil embargo against Russia. However, Chart I-14 highlights that a recession, at least a technical one, may occur in Germany even if its imports of Russian natural gas are not interrupted. The chart shows that the German IFO business climate indicator for manufacturing has deteriorated more than the Markit PMI has, and panel 2 highlights that IFO-reported service sector sentiment is considerably worse than what was suggested by the Markit services PMI. Chart I-15 highlights that European stocks are not fully priced for a European recession, either in relative or absolute terms. This underscores the risk to global equities if real euro area growth falls meaningfully below current consensus expectations of 1.9% this year. Chart I-14German Business Sentiment Suggests A Possible Recession

German Business Sentiment Suggests A Possible Recession

German Business Sentiment Suggests A Possible Recession

Chart I-15Euro Area Stocks Are Not Fully Priced For A European Recession

Euro Area Stocks Are Not Fully Priced For A European Recession

Euro Area Stocks Are Not Fully Priced For A European Recession

Omicron Will Continue To Spread In China Table I-2The Ports Of Shanghai and Ningbo Are Quite Important To Chinese Trade Flows

May 2022

May 2022

Confirmed cases of COVID-19 have surged in China over the past two months, and it is now clear that the country’s zero-tolerance policy will fail to contain the spread of the disease. We initially downgraded the odds of our above-trend growth scenario in our January report specifically in response to the risk that the Omicron variant of the virus posed to China.7 That risk that is now manifesting itself most acutely in Shanghai, but also increasingly in other coastal and northeastern provinces. Chart I-16COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

COVID Restrictions In China Are Causing Significant Delays In Suppliers' Delivery Times

China’s COVID surge has two implications for the global economic and financial market outlook. The first is that the surge has led to increased port congestion and shipping delays, which clearly threaten to cause a further rise in global shipping costs. We have noted in past reports that shipping costs from China to the West Coast of the US surged following the one month shutdown of the port of Yantian last year. Table I-2 highlights that the ports of Shanghai and nearby Ningbo handle nearly 30% of China’s total ocean shipping volume. Chart I-16 highlights that road traffic restrictions in the Yangtze River Delta have caused significant delays in suppliers’ delivery times, further raising the risk of bottlenecks that may take months to clear. Chart I-17China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

China's Battle With Omicron Further Raises The Risk Of A Euro Area Recession

The second implication of China’s COVID surge is that China’s contribution to global growth is at risk of declining significantly further, at least for a time. If Chinese economic activity slows sharply in response to the lockdowns and a further spread of the disease, we fully expect Chinese policymakers to provide further stimulus to support household income in line with what occurred in DM countries two years ago. In addition, some investors have argued that reduced commodity demand from China is actually desirable in the current environment, as it would further reduce inflationary pressure in the US and other developed economies. However, Chart I-17 highlights that Chinese import growth has already slowed very significantly, which has clearly impacted euro area exports. European exports to China are not predominantly commodity-based, and it is yet unclear whether the form of stimulus that Chinese policymakers will introduce will be particularly import-intensive. As such, China’s failure to contain Omicron further adds to the risk of the European recession we noted above, and threatens our view that US headline inflation will trend lower this year. Inflation Expectations May Unanchor Despite Slowing Inflation We discussed above that US inflation will decelerate this year and that this may allow the Fed to raise interest rates at a slower pace than currently expected by market participants. One risk to this view is the possibility that inflation expectations may unanchor to the upside, despite an easing in inflation. Even though inflation expectations have not trended in a different direction than actual inflation since the GFC, Chart I-18 highlights that this has occurred in the past (from 2001-2006). In our view, the level of inflation that is likely to prevail over the coming two years will be an extremely important determinant of whether inflation expectations break above their post-2000 range. For now, Chart I-18 highlights that the Fed’s expectation for core inflation this year is reasonable, but it remains an open question whether core inflation will decelerate below 3% next year as the Fed is forecasting. This is notable, because US core PCE inflation peaked at a rate of 2.6% during the 2002-2007 economic expansion, which is the period when stable long-dated inflation expectations were prevalent. Chart I-19 highlights that market-based inflation expectations are currently challenging or have risen above their 2004-2014 average. We noted in last month’s report that long-dated household inflation expectations will be historically low, even if inflation decelerates in line with what near-dated CPI swaps are forecasting. Chart I-18Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Inflation Expectations May Still Unanchor Even If The Inflation Rate Comes Down

Chart I-19Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

Market-Based Inflation Expectations May Soon Rise Above Pre-GFC Range

The bottom line for investors is that a slowing of inflation over the coming several months may not be enough to prevent long-term inflation expectations from rising. That raises the risk of an even more aggressive pace of interest rates than currently expected by investors, because the Fed is determined to avoid repeating the mistakes of the 1970s when rising inflation expectations led to a wage-price spiral that required years of comparatively tight monetary policy to correct. By contrast, the Fed will view a temporary income-statement recession stemming from a sharp rise in interest rates as the lesser of two evils. A recession to prevent a long-lasting wage-price spiral would also probably be better for investors over the longer run, but a recession would clearly imply a significant decline in risky asset prices at some point over the coming two years were it to occur. Investment Conclusions Chart I-20Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

Despite The Risks Facing Europe, Euro Area Stocks Are Not A Clear Underweight Candidate

From the perspective of allocating to risky assets, the most important question for investors to answer is whether the US is likely to experience a recession over the coming year. As we noted above, in our view the answer is “no”, which implies that US earnings growth will remain positive and that investors should not be underweight stocks within a global multi-asset portfolio. It is true that earnings can decline outside of the context of a recession, but we discuss in Section 2 of our report that this has almost always been associated with a significant contraction in profit margins. The factors that have historically been associated with a nonrecessionary decline in profit margins may occur later this year, but our indicators so far point more to flat margins rather than a significant decline. For now, investors should remain minimally-overweight stocks over a 6 to 12 month time horizon, although that assessment may change in either a bullish or bearish direction over the coming several months. Within a global equity allocation, we recommend that investors maintain a neutral regional allocation. The larger risk of a recession in Europe than in the US would normally imply that investors should be overweight US stocks, but euro area stocks have already underperformed global stocks significantly since Russia’s invasion of Ukraine. Chart I-15 highlighted that they will underperform further if euro area growth turns negative. It is not clear, however, if that risk warrants an underweight stance today, especially considering the enormous valuation advantage offered by euro area stocks versus their US counterparts and the fact that the euro has already fallen to a five-year low (Chart I-20). Chart I-21Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

Favor A Neutral Stance Towards Cyclical Stocks Versus Defensives

Within the dimensions of the equity market, Chart I-21 highlights that the outperformance of cyclicals versus defensives was already late at the onset of Russia’s invasion of Ukraine, and that the uptrend in relative performance has seemingly ended. Still, a moderately overweight stance toward stocks overall does not especially support an underweight stance toward cyclicals; therefore, we recommend a neutral stance over the coming year. We continue to recommend that investors (modestly) favor value stocks over growth stocks on the basis of better value and as a hedge against potentially higher long-maturity yields, although we acknowledge that most of the outsized outperformance of growth stocks during the pandemic has already reversed. Despite their recent underperformance, we continue to favor global small-cap stocks over their large-cap peers, as they are now unequivocally inexpensive and have seemingly already priced in a likely recession scare in the US later this year (Chart I-22). Within a fixed-income portfolio, we recommend that investors maintain a modestly short duration stance despite our forecast that long-maturity bond yields will not increase much this year. We are wary of recommending a neutral duration stance given the possibility that investors or the Fed may upwardly revise their neutral rate expectations earlier than we anticipate; however, investors are also likely to see long-maturity yields come down for a time in response to a housing market slowdown over the coming several months. More nimble investors should be neutral duration, and should test a long stance if US data releases begin to exhibit meaningfully negative surprises. Finally, while we are bearish toward the dollar on a 6- to 12-month time horizon, it is likely to strengthen over the near term. Chart I-23 highlights that our composite technical indicator for the US dollar is now clearly in overbought territory. We expect that a downtrend will begin once the war in Ukraine reaches a durable conclusion and clarity about the economic impact of the spread of Omicron in China – and the likely policy response – emerges. Chart I-22The Selloff In Small Caps Seems Overdone

The Selloff In Small Caps Seems Overdone

The Selloff In Small Caps Seems Overdone

Chart I-23US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

US Dollar And Indicator The Dollar Is Ripe For A Major Pullback Beyond Likely Near-Term Strength

Jonathan LaBerge, CFA Vice President The Bank Credit Analyst April 28, 2022 Next Report: May 26, 2022 II. The US Equity Market: A Fundamental, Technical, And Value-Based Review All four of our US Equity indicators are currently pointing in a bearish direction. Our Monetary Indicator has fallen to a three decade low, our Technical Indicator has broken into negative territory, our Valuation Indicator still signals extreme equity pricing, and our Speculation Indicator does not yet support a contrarian buy signal. Still, we do not expect a US recession over the coming year, which implies that S&P 500 revenue growth will stay positive. Nonrecessionary earnings contractions are rare, and are almost always associated with a significant contraction in profit margins. Our new profit margin warning indicator currently suggests the odds of falling margins are low, although the risks may rise later this year. Stocks are extremely expensive, but rich valuations are being driven by extremely low real bond yields, rather than investor exuberance. Valuation is unlikely to impact US stock market performance significantly over the coming year unless long-maturity bond yields rise substantially further. Technical analysis of stock prices has a long and successful history at boosting investment performance, which ostensibly suggests that investors should be paying more attention to technical conditions in the current environment. However, technical trading rules have been less helpful in expansionary environments when inflation is above average and when stock prices and bond yields are less likely to be positively correlated (as is currently the case). As such, the recent technical breakdown of the US equity market may simply reflect a reduced signal-to-noise ratio associated with these economic and financial market regimes. For now, we see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio over the coming 6 to 12 months. Rising odds of a recession, declining profit margins, and a large increase in investor or Fed expectations for the neutral rate of interest are the most significant threats to the equity market, the risks of which should be monitored closely by investors. In Section 1 of our report, we reviewed why a recession in the US is unlikely over the coming 6 to 12 months. However, we also highlighted that the risks to the economic outlook are meaningful and that an aggressively overweight stance toward risky assets is currently unwarranted. During times of significant uncertainty, investors should pay relatively more attention to long-term economic and financial market indicators with a reliable track record. In this report we begin by briefly reviewing the message from our US Equity Indicators, and then turn to a deeper examination of the top-down outlook for earnings, the determinants of rich valuation in the US stock market, and whether investors should rely on technical indicators in the current environment. We conclude that, while an indicator-based approach is providing mixed signals about the US equity market, we generally see our indicators as supportive of a cautious, minimally-overweight stance toward stocks within a multi-asset portfolio. Aside from tracking the risk of a recession, investors should be closely attuned to signs of a contraction in profit margins or shifting neutral rate expectations as a basis to reduce equity exposure to below-benchmark levels. A Brief Review Of Our US Equity Indicators Chart II-1Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Our Equity Indicators Are Pointing In A Bearish Direction

Chart II-1 presents our US Equity Indicators, which we update each month in Section 3 of our report. We highlight our observations below: Chart II-1 shows that our Monetary Indicator has fallen to its lowest level since 1995, when the Fed surprised investors and shifted rapidly in a hawkish direction. The indicator is most acutely impacted by the speed of the rise in 10-year Treasury yields and a massive surge in the BCA Short Rate Indicator to levels that have not prevailed since the late 1970s (Chart II-2). Our Technical Indicator has recently broken into negative territory, which we have traditionally interpreted as a sign to sell stocks. The indicator has been dragged lower by a deterioration in stock market breadth across several tracked measures and by weak sentiment (Chart II-3). The momentum component of the indicator is fractionally positive but is exhibiting clear weakness. Our Valuation Indicator continues to highlight that US equities are extremely overvalued relative to their history, despite the recent sell-off in stock prices. Our Speculation Indicator arguably provides the least negative signal of our four indicators, at least from a contrarian perspective. In Q1 2021, the indicator nearly reached the all-time high set in March 2000, but it has since retreated significantly and has exited extremely speculative territory. While this may eventually provide a positive signal for stocks, equity returns have historically been below average during months when the indicator declines. Thus, the downtrend in the Speculation Indicator still points to weakness in stock prices, at least over the nearer term. Chart II-2Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Our Monetary Indicator Is Falling In Part Because Of Surging Interest Rate Expectations

Chart II-3All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

All Three Components Of Our Technical Indicator Are Falling

In summary, all four of our US Equity indicators are currently pointing in a bearish direction, which clearly argues against an aggressively overweight stance favoring equities within a multi-asset portfolio. At the same time, we reviewed the odds of a US recession over the coming year in Section 1 of our report and argued that a recession is not likely over the coming 12 months. Thus, one key question for investors is whether a nonrecessionary contraction in earnings is likely over the coming year. We address this question in the next section of our report, before turning to a deeper examination of the relative importance of equity valuation and technical indicators. Gauging The Risk Of A Nonrecessionary Earnings Contraction Chart II-4Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Nonrecessionary Earnings Declines Usually Occur Due To Falling Margins

Based on S&P data, there have been five cases since 1960 when 12-month trailing earnings per share fell year-over-year, while the economy continued to expand (Chart II-4). Sales per share growth remained positive in four of these cases (panel 2), underscoring that falling profit margins have been mostly responsible for these nonrecessionary earnings declines. We have noted our concern about how elevated US profit margins have become and have argued that a significant further expansion is not likely to occur over the coming 12-24 months.8 To gauge the risk of a sizeable decline in margins over the coming year, we construct a new indicator based on the seven instances when S&P 500 margins fell outside the context of a recession. This includes two cases when margins fell but earnings did not (because of buoyant revenue growth). We based the indicator on these five factors: Changes in unit labor cost growth to measure the impact of wage costs on firm profitability; Lagging changes in commodity prices as a proxy for material costs; The level of real short-term interest rates as a proxy for borrowing costs; Changes in a sales growth proxy to measure the impact of operating leverage on margins; And changes in the ISM manufacturing index to capture any residual impact on margins from the business cycle. Chart II-5The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

The Odds Of A Nonrecessionary Profit Margin Contraction Are Currently Low

Chart II-5 presents the indicator, which is shaded both for recessionary periods and the seven nonrecessionary margin contraction episodes we identified. While the indicator does not perfectly predict margin contractions outside of recessions, it did signal 50% or greater odds of a margin contraction in four of the seven episodes we examined, and signals high odds of a contraction in margins during recessions. Among the three cases in which the indicator failed to indicate falling margins during an expansion, two of those failures were episodes when earnings growth did not ultimately contract. The inability to explain the 1997-1998 margin contraction is the most relevant failure of the indicator, in addition to two false signals in 1963 and 1988. Still, the approach provides a useful framework to gauge the risk of falling profit margins, and the results provide an interesting and somewhat surprising message about the relative importance of the factors we included. We would have expected that accelerating wages would have been the most significant factor explaining nonrecessionary profit margin declines. Wages were highly significant, but they were the second most important factor behind our sales growth proxy. Lagged commodity prices were the third most significant factor, followed by real short-term interest rates. Changes in the ISM manufacturing index were least significant, underscoring that our sales growth proxy already captures most of the effect of the business cycle on profit margins. This suggests that operating leverage is an important determinant of margins during economic expansions, and that investors should be most concerned about declining profit margins when both revenue growth is slowing significantly and wage growth is accelerating. The indicator currently points to low odds of a nonrecessionary margin contraction, but this is likely to change over the coming year. We expect that all five of the factors will evolve in a fashion that is negative for margins over the coming twelve months: While the pace of its increase is slowing, median wage growth continues to accelerate, even when adjusting for the fact that 1st quartile wage growth is growing at an above-average rate (Chart II-6). Combining the latter with higher odds of at or below-trend growth this year implies that unit labor costs may rise further over the coming twelve months. Analysts expect S&P 500 revenue growth to slow nontrivially over the coming year (Chart II-7). Current expectations point to growth slowing to a level that would still be quite strong relative to what has prevailed over the past decade; however, accelerating wage costs in lockstep with decelerating revenue growth is exactly the type of combination that has historically been associated with falling margins during economic expansions. Chart II-6Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Wage Growth Is Accelerating...

Chart II-7...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

...And Revenue Growth Is Set To Slow

Although these are less impactful factors, the lagged effect of the recent surge in commodity prices will also weigh on margins over the coming year, as will rising real interest rates and a likely slowdown in manufacturing activity in response to slower goods spending. In addition to our new indicator, we have two other tools at our disposal to track the odds of a decline in profit margins over the coming year. First, Chart II-8 illustrates that an industry operating margin diffusion index does a decent job at leading turning points in S&P 500 profit margins, despite its volatility. And second, Chart II-9 highlights that changes in the sales and profit margin diffusion indexes sourced from the Atlanta Fed’s Business Inflation Expectations Survey have predicted turning points in operating sales per share and margins over the past decade. Chart II-9 does suggest that profit margins may not rise further, but flat margins are not likely to be a threat to earnings growth over the coming year if a recession is avoided (as we expect). Chart II-8Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Sector Diffusion Indexes Are Not Signaling A Major Warning Sign For Margins...

Chart II-9...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

...Neither Are The Atlanta Fed Business Sales And Margin Diffusion Indexes

The conclusion for investors is that the odds of a decline in profit margins over the coming year are elevated and should be monitored, but are seemingly not yet imminent. In combination with expectations for slowing revenue growth, this implies, for now, that earnings growth over the coming year will be low but positive. Valuation, Interest Rates, And The Equity Risk Premium As noted above, our Valuation Indicator continues to highlight that US Equities are extremely overvalued relative to their history. Our Valuation Indicator is a composite of different valuation measures, and we sometimes receive questions from investors asking about the seemingly different messages provided by these different metrics. For example, Chart II-10 highlights that equity valuation has almost, but not fully, returned to late-1990 conditions based on the Price/Earnings (P/E) ratio, but is seemingly more expensive based on the Price/Book (P/B) and especially Price/Sales (P/S) ratios. In our view, this apparent discrepancy is easily resolved. Relative to the P/E ratio, both the P/B and especially P/S ratios are impacted by changes in aggregate profit margins, which have risen structurally over the past two decades because of the rising share of broadly-defined technology companies in the US equity index (Chart II-11). Barring a major shift in the profitability of US tech companies over the coming year, we do not see discrepancies between the P/E, P/B, or P/S ratios as being particularly informative for investors. As an additional point, we also do not see the Shiller P/E or other cyclically-adjusted P/E measures as providing any extra information about the richness or cheapness of US equities today, as these measures tend to move in line with the 12-month forward P/E ratio (Chart II-12). Chart II-10US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

US Equities Are Extremely Overvalued, Based On Several Valuation Metrics

Chart II-11Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

Tech Margins Have Caused Stocks To Look Especially Expensive On A Price/Sales Basis

In our view, rather than focusing on different measures of valuation, it is important for investors to understand the root cause of extreme US equity prices, as well as what factors are likely to drive equity multiples over the coming year. As we have noted in previous reports, the reason that US stocks are extremely overvalued today is very different from the reason for similar overvaluation in the late 1990s. Charts II-13 and II-14 present two different versions of the equity risk premium (ERP), one based on trailing as reported earnings (dating back to 1872), and one based on twelve-month forward earnings (dating back to 1979). Chart II-12The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

The Shiller P/E Ratio Does Not Convey Any 'New' Information About Valuation

Chart II-13The Equity Risk Premium Is In Line With Its Historical Average…

The Equity Risk Premium Is In Line With Its Historical Average

The Equity Risk Premium Is In Line With Its Historical Average

The ERP accounts for the portion of equity market valuation that is unexplained by real interest rates, and the charts highlight that the US ERP is essentially in line with its historical average based on both measures, in sharp contrast to the stock market bubble of the late 1990s. This underscores that historically low interest rates well below the prevailing rate of economic growth are the root cause of extreme equity overvaluation in the US (Chart II-15), meaning that very rich pricing can be thought of as “rational exuberance.” Chart II-14…In Sharp Contrast To The Late 1990s

...In Sharp Contrast To The Late 1990s